1. Introduction

In recent years, massive emissions of greenhouse gases have had a serious effect on the ecosystem. The Global State of the Climate report by the World Meteorological Organization (WMO) confirms that 2015–2019 were the hottest five years in history. As the world’s industries continue to grow, industrial enterprises develop and operate, consuming fossil energy, which causes a continued rise in atmospheric CO

2 [

1]. In the face of rising global temperatures and environmental degradation, energy saving and emission reduction have also become a responsibility that all countries and regions in the world must undertake [

2,

3].

With the start of the third technological revolution and the growing prominence of environmental issues, the relationship between environmental policy and innovation has also attracted the attention of scholars around the world [

4]. Some scholars have divided environmental regulation into order-controlled and market-incentive types [

5,

6]. Carbon trading policies (CTPs) are regarded as an effective market-incentive environmental regulation (MER) to combat climate change and control greenhouse gas emissions [

7,

8]. At the same time, there is an increasing trend toward differentiated innovation quality in recent years [

9]. High-quality innovation can contribute to technological progress and environmental protection. However, low-quality innovation is often considered ineffective and a waste of resources [

10]. In response to this phenomenon, it is important to analyze the drivers of different quality innovations. To this end, we attempt to respond to the following question: can MERs improve the quality of corporate innovation?

As a major carbon emitter and the world’s largest developing country, China has taken the initiative to take responsibility and actively participate in energy-saving and emission-reduction initiatives [

11,

12]. At the Paris Conference in 2015, China pledged to reduce its carbon emission intensity by 60–65% by 2030 [

12,

13]. In the 11th Five-Year Plan, the Chinese government established the goal of energy saving and emission reduction by increasing efforts to reduce emissions and promoting energy-saving policies. Since 2013, China has launched eight pilot carbon-trading markets including Beijing, Shanghai, Shenzhen, Guangdong, Tianjin, Chongqing, Hubei, and Fujian [

14,

15]. With the EU’s restrictions on certified emission reductions (CERs) in the international market for emerging countries such as China and the improvement of the domestic carbon trading market, Chinese companies are slowly turning to the domestic carbon trading market. By 22 December 2022, the cumulative turnover of the national carbon market exceeded RMB10 billion.

Porter (1991) pointed out that appropriate environmental regulations stimulate firms to innovate technologically, and that technological innovation leads to productivity gains that offset environmental protection costs, ultimately increasing the enterprises’ competitiveness; this is the so-called “Porter Effect” [

16]. However, the subsequent literature on the “Porter Effect” has not reached a uniform conclusion. Some research has respectively examined that the “Porter Effect” does exist under environmental regulation [

17,

18]. Lanoie et al. revealed that the Lagging effect of environmental regulation on productivity is positive [

17]. Berman et al. found that US air pollution regulations can improve the productivity of refineries [

18]. However, according to Dean and Brown, environmental regulations have a negative effect on technological innovation because it increases the cost of environmental management and crowds out corporate investment in R&D [

19].

In response to the two contradictory views, some scholars have classified environmental regulation based on their functioning mechanisms into order-controlled and market-incentive types [

5,

6]. Order-controlled environmental regulation (OER) uses administrative orders to intervene directly with highly polluting enterprises to force them to meet energy efficiency and emission reduction standards [

20]. It has strong administrative aspects and is classified as direct control. For example, OERs could consist of setting strict emission and technical standards and forcibly closing down highly polluting and outdated production enterprises. MERs are based on Coase’s theorem, which establishes a market for emission rights by defining property rights over environmental resources [

21]. Significant spatial differences exist in the policy effects of different environmental policy instruments [

22]. An increasing number of studies suggest MERs have more long-term incentives than order-controlled regulations [

5,

23]. According to Dong and Feng [

23], a flexible MER may trigger positive productivity effects in the new energy sector. Milliman and Prince point out that the impact on technological innovation is stronger under an MER than under an OER [

24].

At the same time, some scholars distinguish among corporate innovation types. Some researchers have addressed the relationship between environmental regulation and low-carbon innovation. Laing et al. found that the EU Emissions Trading Scheme (EUETS) has a limited effect on low-carbon innovation [

25]. Eikeland and Skjærseth pointed out that the power sector has been more proactive than the oil sector with regard to low carbon innovation in EUETS [

26]. Additionally, Qi et al. found that China’s carbon trading policy (CCTP) can promote corporate low-carbon innovation [

27]. Some scholars have revealed the effect of environmental regulation on green innovation. For example, Zhang et al. revealed the positive impact of CCTP on the green innovation of listed companies [

28]. Additionally, some of the literature wanted to find the innovation performance of environmental regulation. Jiang et al. discovered that regional environmental regulation in China promoted innovation performance [

29]. Furthermore, according to Mo, the Korean Emission Trading Scheme (KETS) has a positive effect on innovation and thus reduce carbon emissions [

30]. These studies have analyzed the impact of market-incentive environmental regulation policies on innovation from different perspectives. However, few studies have analyzed the heterogeneous effects of CCTP on the quality of corporate innovation.

Certainly, the above research has inspired us to analyze the heterogeneous impact of CCTP on corporate innovation with different qualities. At the same time, this analysis is necessary. The variations in the quality of innovation affect the technological variations of companies and reflect the variations in the level of environmental protection. According to Thoma, low-quality innovations are usually invalid patents filed for strategic competition and contribute little to overall corporate innovation capability [

31]. These low-quality innovation patents are a waste of resources and can even lead companies to lose their market competitiveness [

10]. According to Dang and Motohashi, China’s innovation subsidy policies promote more low-quality innovation and have less impact on high-quality innovation [

32].

Previous studies focused more on the impact of environmental regulation on low-carbon innovation, green innovation, or on a single indicator of technological innovation [

27,

28,

29]. At the same time, CCTP may affect innovation that is not green innovation, but this impact may be different from green innovation [

33]. On the one hand, the implementation of the CCTP may increase the demand for low-carbon technologies, which in turn will boost the development of relevant technologies. On the other hand, the implementation of the CCTP may put companies under greater economic pressure to seek new production methods, products, or services to reduce carbon emissions and improve efficiency. How then can companies improve the quality of their patents while ensuring quantity? Can CCTP, which involves market-based incentives for environmental regulation, reduce low-quality innovation and increase high-quality innovation, thereby reducing resource waste? The existing literature does not provide a precise answer to this question.

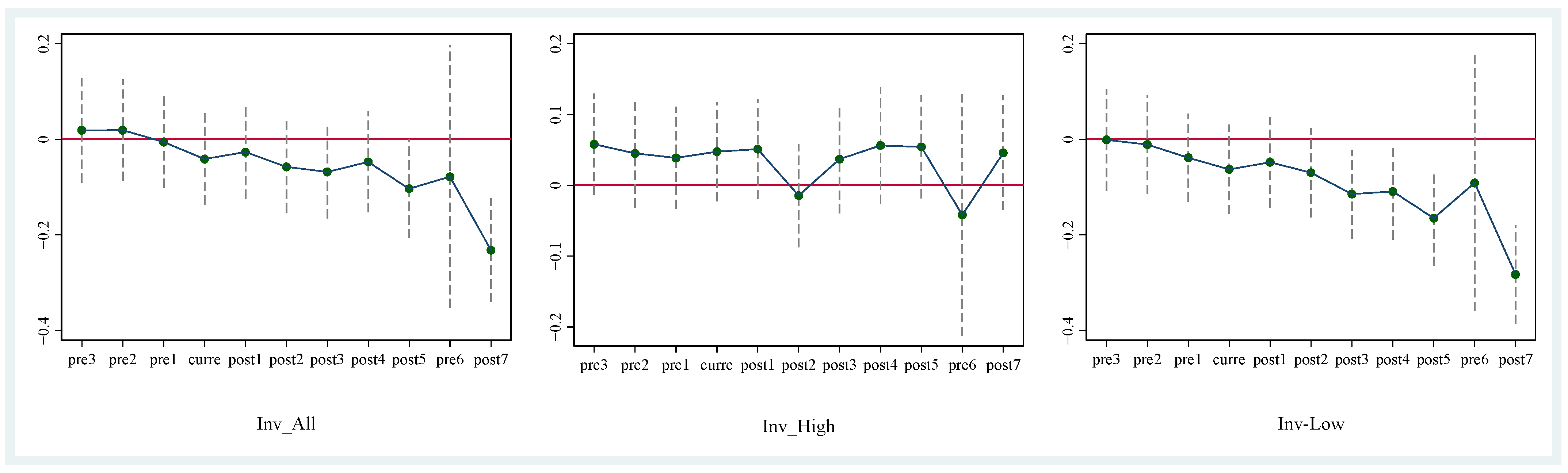

To fill this gap, we used China’s A-share listed enterprises in 2010–2020 and CCTP to conduct a quasi-natural experiment. Market-incentive environmental regulations can significantly increase high-quality corporate innovations and reduce corporate low-quality innovations. This result is robust after a serious robust test, such as a test on parallel trend assumption that excludes the impact of the national carbon trading market and considers Fujian’s carbon emissions trading policy and substitution of dependent variables. Our heterogeneity analysis results suggest the financialization level of firms and whether they are SOEs affect the effectiveness of CCTP.

The main contributions are as follows: First, we expand the literature on the impact of CTP on enterprises. Previous studies focused on the impact of CTP on carbon emission reduction effects, low-carbon innovation, green innovation, and innovation performance. Nevertheless, we focused more on the heterogeneous impact of CTP on different qualities of corporate innovation. Second, we examined the incentives for innovation of listed corporations under environmental regulation policies. High-quality innovation is an indication of the pursuit of technological breakthroughs, while low-quality innovation may favor ineffective innovation that appeals to policy. We focus on whether CTP can increase high-quality innovation and at the same time reduce low-quality innovation. Third, we use CCTP to conduct a quasi-natural experiment to test the impact of CCTP on corporate innovation, which provides a reference to investigate the question of sustainability from emerging markets.

The rest of the paper is structured as follows:

Section 2 shows the development of our hypothesis.

Section 3 presents the research design of this paper, including background, key variables, data and model.

Section 4 shows the main result and robust test.

Section 5 details the heterogeneity analysis based on the financialization level and the nature of the enterprise.

Section 7 provides the conclusions.

2. Hypothesis Development

According to Porter and Linde (1995), appropriate environmental regulations will provide an impetus for firms’ innovative activities [

34]. Thus, as a type of environmental regulation, the CCTP may produce a “Porter effect” and promote innovation in corporates. In the face of environmental pressure from CCTP, companies may purchase carbon emission quotas directly on the market to meet their emission reduction constraints or engage in innovative activities to save energy and reduce emissions. Different quality innovations may be produced in the process of corporate innovation because of the different motivations for innovation. Recent studies have often classified the quality of innovation according to the type of patent [

35,

36,

37].

We first hypothesize that CCTP will incentivize firms to engage in high-quality innovation. As a market-incentivized environmental regulation tool in China, the CCTP aims to internalize the negative externality costs of environmental pollution through the market price mechanism. Theoretically, the carbon emission trading policy makes carbon emission rights a commodity property, i.e., the allocation of resources is achieved through the market trading behavior of carbon emission rights. In this context, high-quality innovation by companies can not only improve their technology and reduce carbon emissions but also trade their excess carbon emission rights on the market for a profit. Hence, companies have an intrinsic incentive and motivation to engage in high-quality, substantial technological innovation [

38]. From the above analysis, we develop the following hypothesis.

H1. CCTP has a positive impact on high-quality innovation in enterprises.

Second, we further consider the impact of CCTP on low-quality innovation by corporates. According to Tong et al., strategic innovation for “other benefits” is common among Chinese enterprises [

39]. The “quantity over quality” strategic innovation is a significant burden on firms’ profitability, and low-quality innovation is merely a response by corporates to seek support in the face of regulatory policies, without any increase in their real innovation capacity [

38]. The CCTP is an environmental regulatory policy based on market regulation to achieve its objectives, which makes it difficult for companies to benefit from low-quality innovation. At the same time, CCTP will signal to enterprises that high-quality innovation is the only way to achieve sustainable development. In turn, it reduces low-quality innovation activities of enterprises. Thus, we propose the following hypothesis:

H2. CCTP has a negative impact on low-quality innovation in enterprises.

6. Discussion

According to the results in

Table 3, the CCTP has a positive impact on corporate high-quality innovation and this result is consistent with H1. This may be because the CCTP imposes higher technological requirements on enterprises, making them seek more innovative and advanced technologies to reduce carbon emissions. This finding validates Porter’s hypothesis [

16,

34]. It is also consistent with the conclusions of the literature on CTP and corporate innovation [

33,

38]. We further find that CCTP has a negative impact on corporate low-quality innovation. In the process of improving energy efficiency and reducing carbon emissions, corporate may facilitate the transformation from low-quality innovation to high-quality innovation.

Columns (1) and (2) of

Table 6 indicate that the CCTP significantly increases the total number of patents of low-financialized firms and has no effect on high-financialized firms. Column (5) of

Table 6 reveals that increased financialization of firms can decrease the incentive effect of CCTP on invention patents. The main reason is that a high level of corporate financialization may lead companies to focus more on return on investment rather than environmental benefits. CCTP aims to reduce carbon emissions through price incentives, but if companies are more concerned with return on investment, they may see carbon trading as an investment and thus focus more on its return rather than its environmental result when buying carbon emission quotas. Thus, higher financialization of corporations may diminish the incentives of CCTP for high-quality innovation.

As is revealed in Columns (3) and (4) of

Table 7, the impact of CCTP on high-quality corporate innovation occurs mainly in non-SOEs. This may be because SOEs hold a critical position in the Chinese economy and often receive policy assistance and other favorable policies [

63]. These policies may mitigate the impact of CCTP on their business behavior. In contrast, non-SOEs tend to face more competition and market risks and, as a result, need to pay more attention to carbon emissions [

66]; therefore, they need to be more sensitive to carbon emission issues. Furthermore, according to the results of Columns (5) and (6) of

Table 7, CCTP significantly reduces low-quality innovation in SOEs and increases low-quality innovation in non-SOEs. This may result from the fact that for SOEs, their propensity for low-quality innovation may be relatively low due to the preferential treatment and greater resource support they enjoy in terms of policy. For non-SOEs, on the other hand, their propensity to engage in low-quality innovation may be greater due to their lack of resources and policy support.

7. Conclusions

7.1. Findings

China’s national carbon trading market was launched in 2021. While innovation-driven development is a matter of sustainable economic development, the impact of carbon emissions trading policies on innovation is worth exploring. The quality of a firm’s innovation not only affects its technology but is also related to the performance of its environment. However, the literature analyzing the impact of CCTP on the quality of corporate innovation is scarce. Hence, this paper used China’s A-share listed enterprises in 2010–2020 and CCTP to conduct a quasi-natural experiment. The relevant conclusions are as follows:

First, CCTP significantly improved the quality of innovation, increasing the granting of patents for high-quality innovations while reducing the granting of patents for low-quality innovations.

Second, the level of corporate financialization affects the effectiveness of CCTP. When firms are highly financialized, it can suppress the positive impact of corporate CCTP on high-quality innovation. At the same time, highly financialized firms can enhance the negative impact of CCTP on low-quality innovation.

Finally, the CCTP has different impacts based on the various natures of enterprises. The positive impact of CCTP on high-quality innovation occurs mainly among N-SOEs. In contrast, the negative impact of CCTP on low-quality innovation occurs mainly among N-SOEs.

7.2. Policy Recommendations

Based on the findings of this paper, we offer the following policy recommendations:

First, China should continue to promote the development of a national carbon emissions trading market. Currently, China’s national carbon trading only covers the power sector, which has been an important part of the regional carbon trading market. As an energy conversion sector, improvements in the power sector can effectively reduce the proportion of primary energy consumed by coal and promote technological innovation in other energy-intensive enterprises.

Second, focus should also be given to the development of the real economy. According to the empirical results in

Section 5, corporate innovation behavior is limited by corporate financialization. Hence, it is necessary to perfect the financial market system to provide financial support to real enterprises in technology innovation.

Finally, the supervision of innovation investment in SOEs should be strengthened and these enterprises should be guided toward improving innovation quality. In China, SOEs play a leading position in the economy. Hence, the improved innovation quality of SOEs would be of real significance for the sustainable development of China’s economy.

7.3. Research Limitations

First, we have considered all the pilot region enterprises to be affected by the CCTP. This may not be consistent with the facts. In the next study, we will further match the specific list of firms in the CCTP to more accurately measure the policy effects of the CCTP.

Second, we have only examined the heterogeneous impact of CCTP on corporate innovation and have not investigated its specific transmission mechanisms in depth. In our future work, we will continue to deeply explore the internal motivations of corporate innovation and the internal mechanisms of CCTP that influence innovation.

Finally, while we have excluded the effect of a national carbon trading market from our robustness tests, we did not develop an analysis of the effect of a national carbon trading market in the electricity sector. This issue will be an important topic as the national carbon trading market develops.

{kind=link}