1. Introduction

The historical industrial revolution fast-tracked the pace of human development and improved welfare. However, the development progress has been observed to cause climate change and to degrade the environment [

1]. The changing global climate, largely wrought by activities of man, has led to rising sea levels, increasing temperature extremes, food insecurity and other economic and health consequences around the world, often at a heavy price tag [

2,

3]. The UN Sustainable Development Goal requires economies to take policy actions, including investing in renewable energy technologies, ensuring energy efficiency improvements, and controlling the financial risk of climate change and environmental pollution [

4].

Over the years, reducing environmental pollution from economic growth is largely hinged on ecologically sensitive behaviors, green technology deployment, and stringent environmental regulations [

1]. However, in recent years, one critically cited factor capable of influencing the rate of environmental pollution along the path to economic growth is financial risk [

5]. Financial risk is defined as referring to the probability of losing financially on an investment [

6,

7]. Financial risk also refers to the corporations’ inability to manage and fulfill their financial obligations due to economic instabilities and market losses, which could culminate in business collapse. Both the government and corporate establishments face financial risk, the occurrence of which is found to have profound environmental consequences [

5]. The 2019 climate report by the IMF [

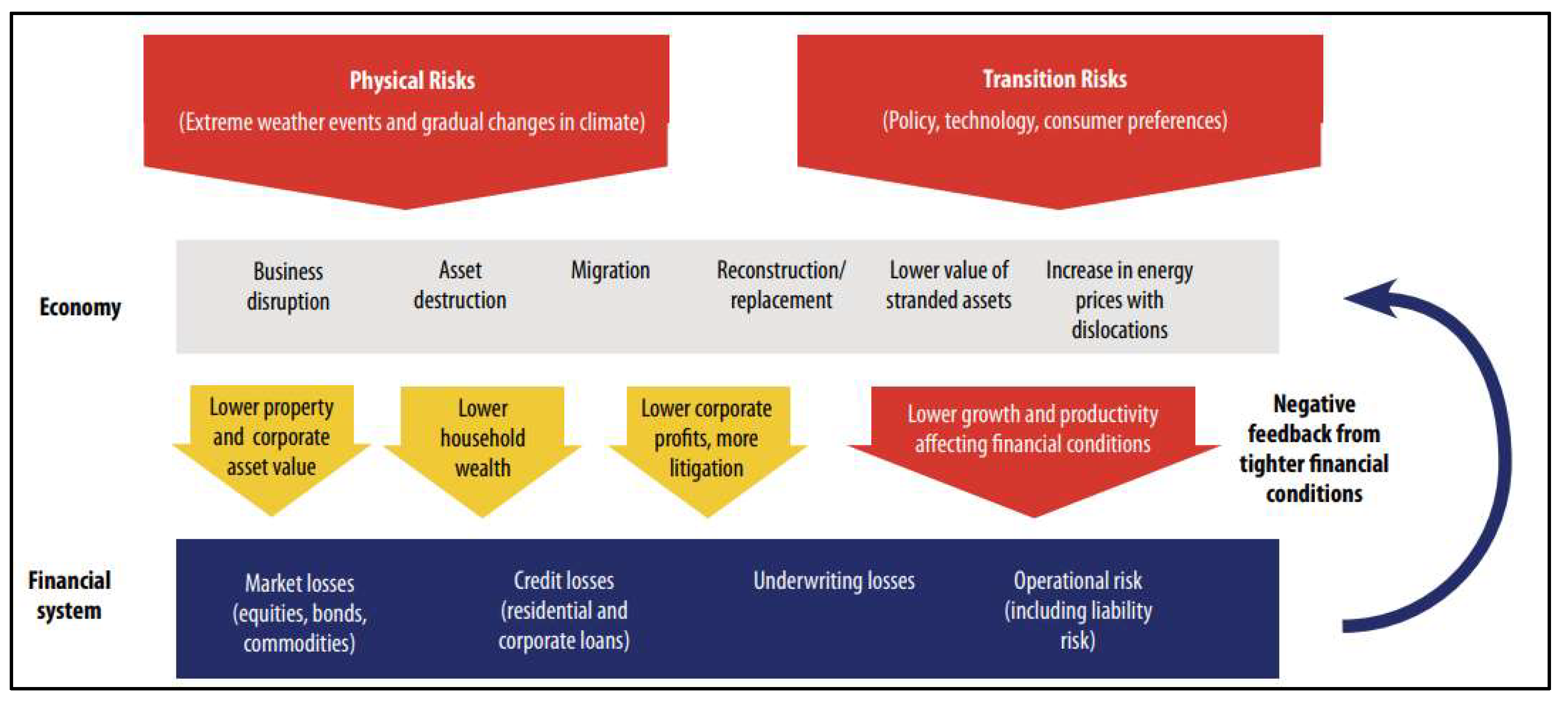

8] finds climate change to impact negatively on the financial system via two main channels (see

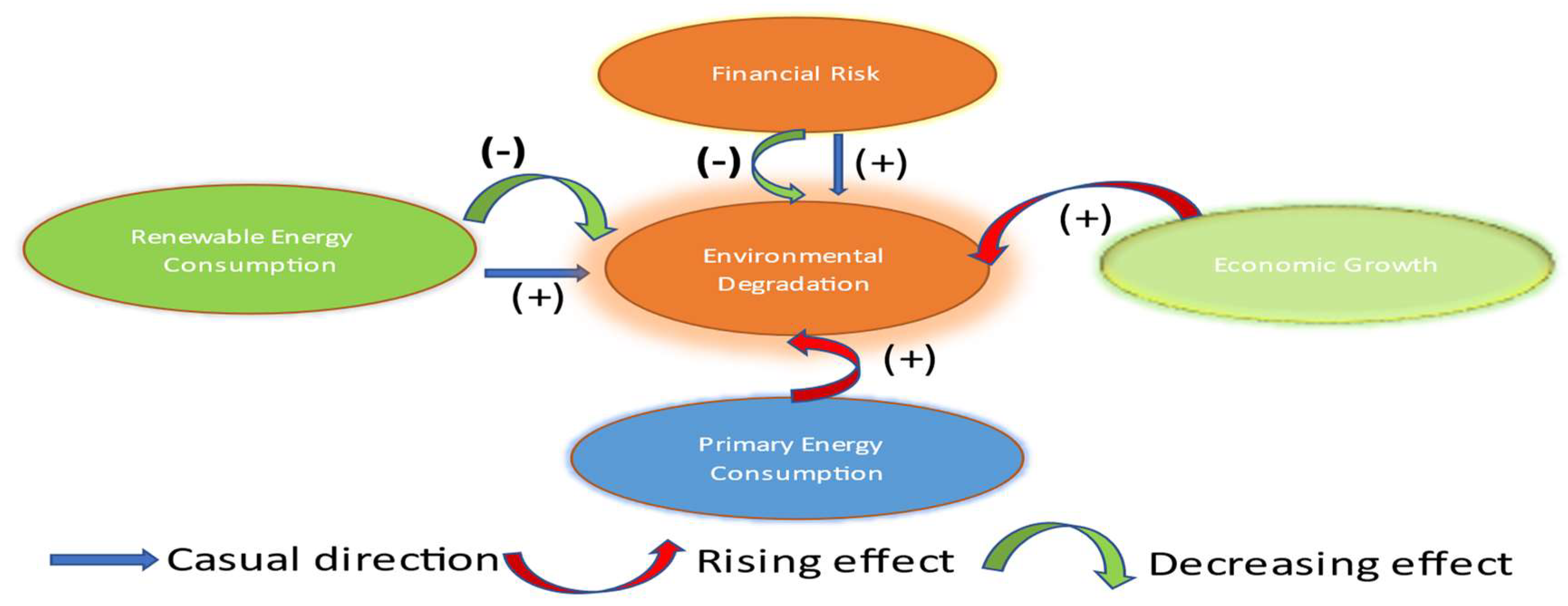

Figure 1). The first route is physical risks, which occur from harm to infrastructure and land properties. The second occurs through transition risk due to variations in climate policy, technology, and consumer sentiments in the energy transition process. Exposures to financial risk can manifest directly in corporations facing climatic shocks. Financial risk can equally happen indirectly via climate change shock on the financial system [

9,

10]. Exposures appear as a higher default risk for loan portfolios or declining asset values. Studies have found cases of natural disaster losses across the globe, causing insurance costs to increase. Corporations whose operational models neglect the economics of low-carbon emissions risk heavy losses and eventual collapse [

10,

11].

Financial risk can create financial sector instability which will have negative consequences on green technology investment funding. In periods of intense pollution, the financial sectors’ support of abatement processes promotes environmental sustainability [

3]. A recent study by [

12] established that reducing financial risk helps in controlling CO

2 emissions in the OECD member economies. This finding suggests global economies must take prudent financial risk management policy measures towards economic stabilization that ensure improvements in environmental quality and control of climate change. The lingering academic question relates to the global validity of these empirical findings since limited studies have been observed in the literature. To establish validity in this empirical claim, the case of Poland presents a fertile ground for investigation due to their historically checkered financial risk records, nature of pollution policies, and environmental quality records among peers in the European Union.

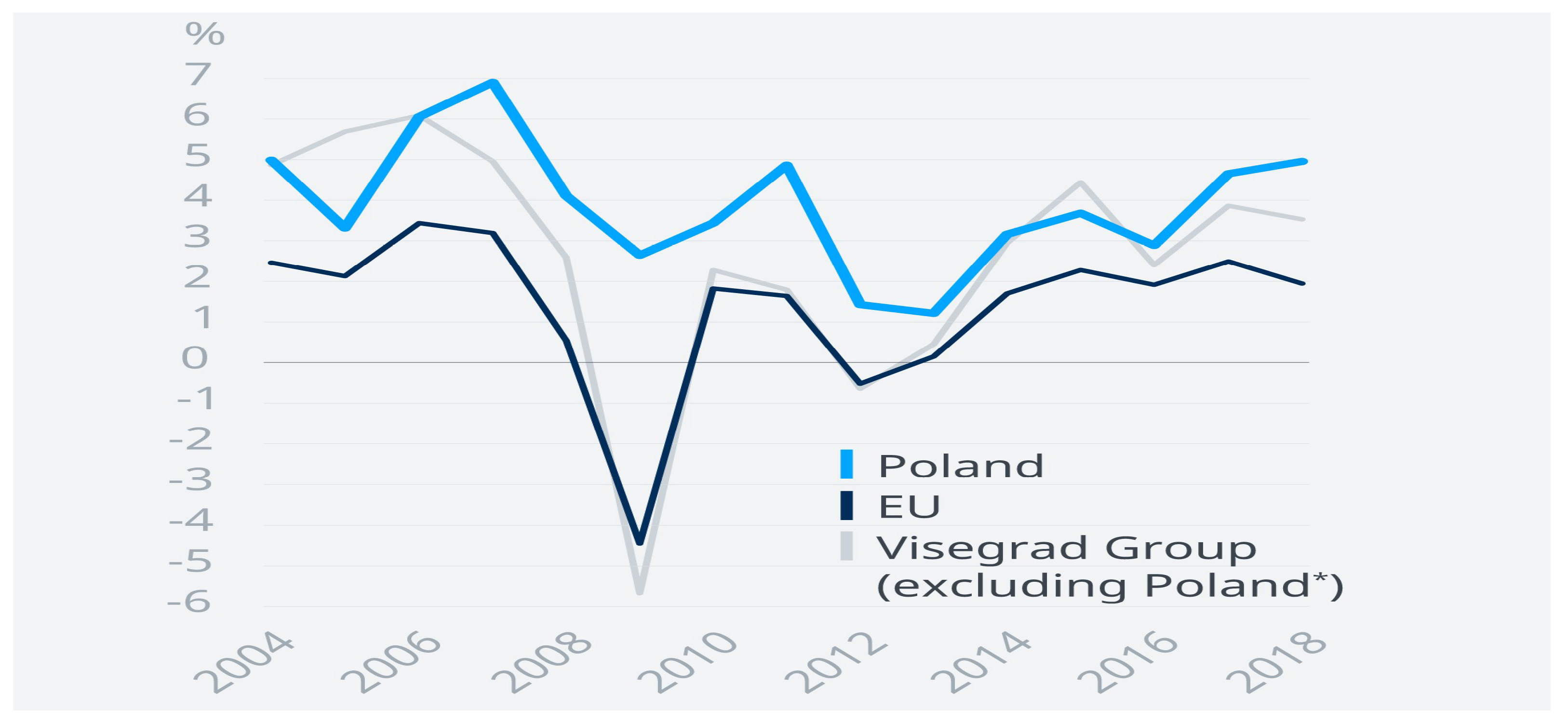

With its 2022 population at 37.8 million, and a per capita of USD 17,946, the Polish economy has had impressive economic growth over the last two decades. Annual GDP growth in Poland averaged 3.99 percent between 1996 and 2018, reaching as high as 7.10 percent in 2007, according to an OECD report. Quality of life in Poland has improved considerably, as reflected in their global well-being scores such as the recent ratings by the Better Life index of the OECD, 2022. The Polish economy has an enviable and improved business climate, facilitating its leading position in World Bank’s Doing Business ranking report among the EU and OECD peers in reforms, and it possesses a healthy utility-like banking sector.

Figure 2 illustrates historical records of Polish real GDP growth (%) since joining the EU.

The country’s sovereign credit rating is low. Sovereign credit ratings are an assessment of the ability and willingness of sovereign states to honor debt obligations [

13]. They are an important piece of information for international investors and affect the borrowing costs of debt-defaulting countries. A fast-changing corporate environment demands financial stability and liquidity, which pivots into the ability of corporations to control financial risk. The financial sector reforms by Poland insulated the country’s corporations from the ills of the 2007–2008 global financial crisis [

14]. However, recent events in the Euro-area due to the Ukraine-Russia geopolitical war and the energy sector crisis have affected the financial stability of Poland, resulting in increasing inflation, rising interest rates and financial market repricing. In addition, the monetary policy actions by the Polish Central Bank have contributed to tighter financial conditions and increased financial market volatility. Further, recent asset price shifts reflect increasing monetary policy uncertainty to moderate inflation; and the mix of high inflation outturns and rising interest rates have continued to weigh on Poland’s recent economic growth rate.

In environmental performance, Poland is a net energy importer. Beginning in 2004, when it joined the EU, Poland constructed more water treatment plants, tried to reduce CO

2 emissions by over 30% compared to 1990 levels, and implemented several policies on endangered plant and animal species. Additionally, Poland underperforms the average in terms of health and environmental quality, although performs well in several well-being metrics when compared to other countries (such as education and social ties). The quantity of PM2.5 (small air pollution particles) in the atmosphere is 22.8 micrograms per cubic meter, more than the OECD average; approximately 18% of Polish people are unhappy with the quality of their water (Better Life Index, 2023). Poland’s coal industry continues to remain a significant component of the local economy after Germany, and this is the major source of air pollution.

Table 1 illustrates the environmental performance of Poland between 1995 and 2022.

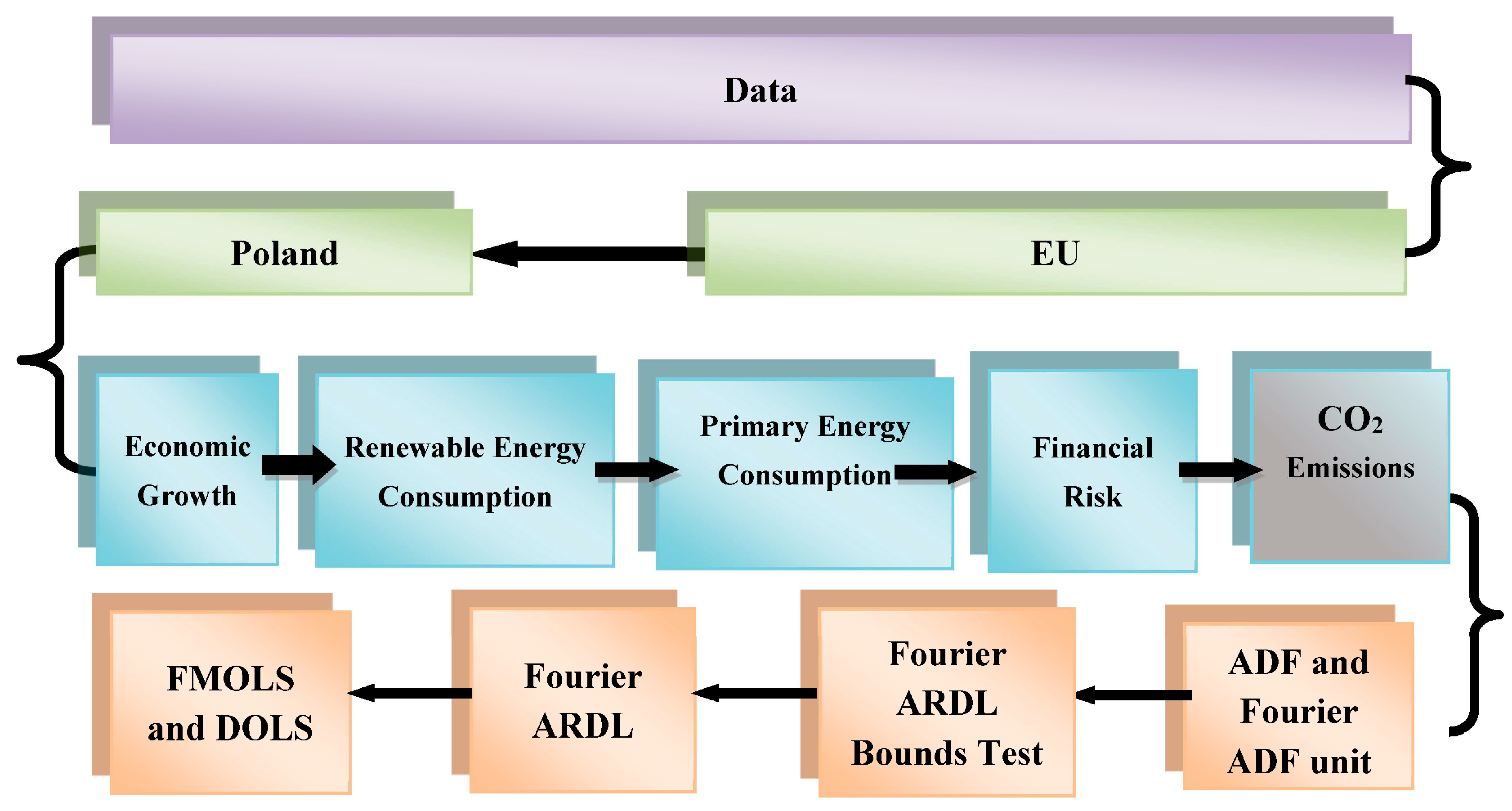

Based on this background, and since the industrial revolution, the global economy has faced the problem of global warming and environmental pollution. However, knowing that renewable technology is the savior pathway, increasing financial risk can affect research and development budgets, creating a block on our way to environmental sustainability. Limited by the literature on these relationships, this paper aims to accurately capture the effect of financial risk on environmental degradation in Poland from 1990Q1 to 2019Q4 while keeping economic growth, primary energy use, and renewable energy consumption under control. For reliable outcomes, the study employs Fourier-ARDL and Toda Yamamoto causality approaches. In contrast to previous research, this work employs a newly modified Autoregressive Distributive Lag (ARDL) cointegration test based on a Fourier function presented by [

15]. In contrast to ARDL and DARDL methods, Fourier ARDL (FARDL) has several vital features [

16,

17,

18]. First, variable integration levels are not required. Second, several seamless structural variations are easily detectable. Third, the estimator uses dummy variables to capture structural variations. The remaining sections of this paper are structured as follows:

Section 2 conducts the literature review;

Section 3 is a summary of the data, sources, and analytical methods employed;

Section 4 illustrates and discusses empirical findings; and

Section 5 closes the paper with policy suggestions.

2. Review of the Related Literature

This section is a comprehensive review of studies on the variables of interest and their relationship with environmental degradation. The review highlights relevant debates and gaps in studies linked with the purpose of the study. In the review process, four hypotheses are made:

Hypothesis 1 (H1). Increasing financial risk reduces financing of economic growth, leading to a reduction in environmental degradation in Poland.

Historically, global economies have committed to taking steps towards carbon neutrality since the 2015 UN climate conference (COP21) in Paris, with huge budgetary allocations towards renewable energy technological development. However, economies with internal and external challenges and financial risks have different stories on realizing global climate goals. Expanding the financial system requires activity commodification based on financial judgments and traded assets. The effect of financial risk on environmental degradation has gained focus in scholarly research, albeit with contradictory outcomes. In their studies, they found that participative decision-making reduces corporate risk and helps corporations to advance superior environmental performance and corporate sustainability [

19,

20,

21]. Ref. [

22] studied 111 economies between 1985 and 2014 on the nonlinear effect of country risk on CO

2 emissions and found that financial risk positively affects environmental degradation across the panel. However, this result contradicted the study of [

23] on CO

2 emissions in China, a result which validated the study by Ozturk and Acaravci (2013). However, in their recent study, [

12] found financial risk causes CO

2 emissions to increase. Financial risks can create financial instability and impact environment-related investments. This will eventually affect environmental quality. In their study, [

12] evidenced that this factor has historically been overlooked by researchers and claimed that reducing financial risk affects CO

2 in OECD. Based on this review, the paper considers that rising financial risk reduces the financing of economic growth, leading to a reduction in environmental degradation in Poland.

Hypothesis 2 (H2). Renewable energy consumption exerts a negative effect on environmental degradation in Poland.

The global economy has accelerated investments in renewable energy because scientific evidence indicates its negative effect on both economic growth and environmental quality [

24,

25,

26]. In relation to climate change, renewable energy use is validated for environmental sustainability through greenhouse gas emissions [

27]. Other scholars have found the use of renewable energy to offer both environmental and economic advantages [

28,

29], including investment portfolio diversification, expanded energy mix, and employment opportunities. The literature on renewable energy and carbon emissions has mixed outcomes based on the methodology employed in country-specific contexts, and variable considerations [

30]. While some studies find feedback causality between CO

2 emissions and renewable energy use [

31,

32], other studies find otherwise. For example, in the case of Thailand, the study by [

33] found no evidential nexus between renewable energy use and CO

2 emissions. However, a study by [

34] found that renewable energy exerted a negative effect on CO

2 emissions in 25 selected African economies between 1980 and 2012. In the case of the G-7 nations, [

35] found that renewable energy use and energy price facilitated improvements in environmental quality. With this review information, the paper hypothesizes that renewable energy consumption exerts a negative effect on environmental degradation in Poland.

Hypothesis 3 (H3). Increasing primary energy consumption facilitates rising environmental degradation in Poland.

It is generally found in the literature that economic growth is closely related to energy consumption [

36,

37,

38]. This is based on the rising threats of global warming and climate change. Scholars hypothesize that increasing economic development requires more energy consumption or productivity of energy use [

39,

40]. A study by [

41] in five ASEAN economies indicated that a statistically positive relationship existed between electricity consumption and carbon emissions non-linearly, consistent with the historical EKC hypothesis. It should be emphasized that economic theories are not explicit on the nexus between energy use, economic growth, and CO

2 emissions; recent studies have focused heavily on the Environmental Kuznets Curve (EKC) or the Carbon Kuznets Curve (CKC) hypothesis with some validation [

42,

42], invalidation [

43,

44], and inconclusive outcomes [

45]. Another comparative study on wood, concrete, and steel utility poles indicated that wood poles had little environmental effect. In their life cycle assessment of primary energy use, [

46] found that heating systems determine primary energy consumption and CO

2 emission; and that biomass-based heating systems and electricity cogeneration reduce primary energy use and CO

2 emissions. However, balancing information based on this review, the paper assumes that increasing primary energy consumption facilitates rising environmental degradation in Poland.

Hypothesis 4 (H4). Increasing economic growth augments rising environmental degradation in Poland.

Historically, several studies have claimed an association between economic growth and CO

2 emissions [

26,

47,

48]. Theoretically, EKC claims the existence of an inverted U-shaped relationship between environment and income. It states that environmental degradation increases up to some point—the turning point—as income increases. Yet after the turning point, this degradation decreases with an increase in income level [

47]. The plotted graph between income and environmental degradation has an inverted U-shape. The study by [

49] estimated the EKC for four environmental indicators along with nominal GDP in the late 1980s, and found that pollution reduction was possible with higher income levels since economic growth eventually improves environmental quality. The authors of [

50] studied the relationship between economic growth and carbon emissions, and found that rising economic output causes destruction to the environment. The study by [

51] in Mexico also found a positive association between CO

2 emissions and economic growth. In Turkey, [

52] found that economic growth positively affected CO

2 emissions using wavelet coherence approaches. For the case of ASEAN economies, [

53] assessed how economic growth related to CO

2 emissions with data between 1971 and 2017. The outcomes indicated that rising economic growth destroyed selected economies in terms of carbon emissions. Based on this, this study assumes that increasing economic growth augments rising environmental degradation in Poland.

Given this in-depth literature review, the effect of financial risk on environmental degradation has not been exhaustive. Similarly, the review has indicated that both primary energy consumption and economic growth are projected to exert a positive effect on environmental degradation in Poland, while financial risk and renewable energy are tipped to have a negative effect on environmental degradation in Poland. Given the limitations of recent empirical investigations determining factors affecting environmental degradation in Poland, this study employs novel Fourier-based ARDL and Fourier Toda Yamamoto causality estimators for its analysis. These methods have been validated to provide accurate and reliable policy-sensitive outcomes [

54].

4. Empirical Outcomes, Analysis and Discussions

This study attempts to establish the consequences of financial risk on environmental deterioration in Poland from 1990Q1 to 2019Q4 by keeping economic progress, primary energy consumption, and renewable energy usage in a controlled position. The variables examined in this inquiry are listed and explained in

Table 3.

The outcomes of the descriptive assessment (

Table 3) show no outliers in the dataset. The outcomes also indicate variables are normally distributed, paving the way for further estimation activity. The next step in the pre-estimation process is assessing the unit root properties of the variables considered for the study.

The initial assessment of this paper checks the integration properties of interest variables by employing ADF unit root with breakpoint methods. It must be stressed that structural breaks have historically been ignored in econometric analysis, and this has caused biased unit root outcomes. Before assessing the integration order of the variables, this study uses the [

64] BDS test to detect nonlinear patterns (i.e., dependence or independence). It is applied to assess varied embedding dimensions, ranging from 2 to 6, and it possesses several advantages over other alternatives. First, it is used to guide against model misspecification. Second, it helps to guide against making judgmental errors. The econometric application is defined as:

Here, T is the sample size; ɛ is a randomly selected proximity parameter; and (ɛ) is the standard deviation of the statistic’s numerator, which changes with dimension “m”.

The BDS estimates (

Table 4) show there are hidden nonlinear patterns in the time series data, and all variable values have “dimensional critical values” that are higher than the BDS estimates. This implies the existence of a nonlinear correlation between all variables.

The research then uses the Fourier ADF and ADF with breaks unit root tests to evaluate the unit root qualities of variables. However, before applying the Fourier ADF (FADF) unit root estimator, it is essential to investigate the Fourier function’s impact and determine its statistical significance. Results from the ADF with Break Point and FADF tests are illustrated in

Table 5.

The results (

Table 4) indicate that both LCO

2 and LFRI time-series variables were integrated at level (I(0)); while RE, LPEC and LGDP were integrated at the order one, showing several breakpoints in 1991Q4, 1992Q1, 1993Q1, 1997Q1, 2007Q1, 2009Q1 and 2012Q1, respectively, at 1%, 5% and 10% statistical significance levels. The mixed order of integration of the variables is recognized per the results. This makes it possible to employ Fourier ARDL-based models for the next action. However, based on the estimates, decisions are made on the ADF unit root with breaks. The article next investigates the cointegration between the chosen variables to ascertain how LFRI and the controlled variables individually and collectively affect LCO

2 in Sweden. These results validate recent research by [

65].

This study subsequently employs the Fourier-based ADL cointegration test to assess the cointegration attributes of the time-series variables, since the results show that the model is stable and does not exhibit serial autocorrelation or heteroscedasticity. Regardless of the variable integration order (I(0) or I(1)), the F-ADL test remains valid [

66]. The estimator can also use linear processes to analyze the unrestricted error correction model. Since endogenous problems cannot alter the size and power features of the Bounds test, ARDL limits can be determined in the short run and the long run utilizing an asymptotic threshold of Monte Carlo simulations.

A long-run cointegration relationship may be discovered utilizing the Fourier ADL cointegration techniques, as seen in

Table 6, where the t-statistical value is significant at 10% and indicates a cointegration relationship among the variables. With this outcome, there is a sense of long-run linkage between LCO

2, LGDP, LPEC, RE, and LFRI. The Fourier ARDL estimator is then used in the current study to quantify the individual or collective effect of LCO

2, LGDP, LPEC, RE, and LFRI on LCO

2 in Poland. Consideration is given to LGDP, LPEC, and RE, which were controlled to accomplish this paper.

The Fourier ARDL Long Run Form (

Table 7) estimates indicate that the coefficients of LPEC and LGDP are positive and significant. Moreover, the estimated coefficients of RE and FRI are negative but significant.

These indicate that a 1% increase in both LPEC and LGDP encourages a positive effect on LCO

2 by approximately 72.68% and 66.96, respectively. These Fourier ARDL Long Run Form estimation outcomes validate the hypothesis on both variables established for this study (i.e., Hypotheses 3 and 4). The results support [

60]. It must be emphasized that, theoretically, rising economic growth affects environmental degradation due to increasing demand for natural resources and energy consumption. Depending on the models for such assessment, there is always an initial phase of environmental destruction before environmental regulatory and technology effects set in, which is popularly known as the EKC curve. This has been demonstrated extensively by all growth models, including the Source-and-Sink framework [

67]; Solow model; and Smulders and Stokey’s AK theoretical model.

GDP growth over the last decade in Poland has been phenomenal and has undoubtedly caused carbon emissions to rise. The Polish economy has witnessed some level of deterioration due to the war in Ukraine in 2022, despite a strong post-COVID-19 rebound of 5.9% rise in real GDP growth in 2021. Economic activity has seen cooling supply-chain disruptions worsened by rising input costs—a direct outcome of globally surging energy prices. Over the last two decades, despite the historical records of rising growth and increasing carbon emissions, the current pent-up consumer-level spending and strong investment action with support from Next Generation EU funds, experts forecast a further projected rise in carbon emissions in Poland.

For primary energy consumption (i.e., fossil fuels, nuclear energy, and renewable sources of energy), Poland recorded 1.95% in 1996 to 8.79% in 2021. In nominal terms, the country saw a rise in primary energy consumption, from 19 Twh in 1990 to 44 Twh in 2021. The country recorded 79% in 2021 consumption of coal and lignite to maintain its power plants, with only an industrial share of a marginal 5%. The domination of coal in the power sector of Poland makes it the largest source of greenhouse gas emissions. It is not a wonder that one percentage change in primary energy use in Poland caused a whopping 7.26% upward adjustment in carbon emissions for the period, an outcome that validates the hypothesis established for this paper. This outcome supports [

68], who found a similar trend and recommended that in Poland, carbon emissions from road transport could be significantly lowered by prioritizing renewable energy sourcing.

Additionally, the Fourier ARDL Long Run Form estimates indicate that a 1% rise in both LFRI and RE exerts a negative effect on environment degradation by 0.0008% and 13.55%, respectively. These estimates confirm hypotheses 1 and 2 established for this paper in the literature review process. The results support [

5]. In their study, [

12] revealed that rising financial risk helps reduce carbon dioxide emissions directly and could similarly have an indirect negative effect on carbon emissions through the facilitation of technological advancement. However, they also found the effect of financial risk on carbon emissions to be heterogeneous across the globe. In Poland, the Polish business environment is not too much at risk, despite perceived weakening recently. The proprietary environmental sustainability index of Allianz International Corporation places Poland at 54 out of 210 global economies. This reflects the strengths of Poland over energy consumption and CO

2 emissions (per GDP), water crisis, and general vulnerability to climate change.

For the case of renewable energy use, the outcome of the Fourier ARDL long form indicated reducing carbon emissions by −0.008785 percent, given a unit change in primary energy consumption in Poland. This outcome supports earlier findings by [

69] and validates the hypothesis established in this study on renewable energy use in Poland. In his study, ref. [

69] assessed costs and the potential of reducing greenhouse gas emissions in Poland by replacing fossil fuels using renewable energy technologies. The outcome indicated a fall in carbon dioxide emissions with reducing the cost of investment. The findings also validated the historical work of [

69], who evaluated renewable energy sourcing and its effect on CO

2 emission in Poland. The outcomes of their investigations indicated renewable energy’s potential to reduce CO

2 emissions in Poland by about 40 million tonnes annually.

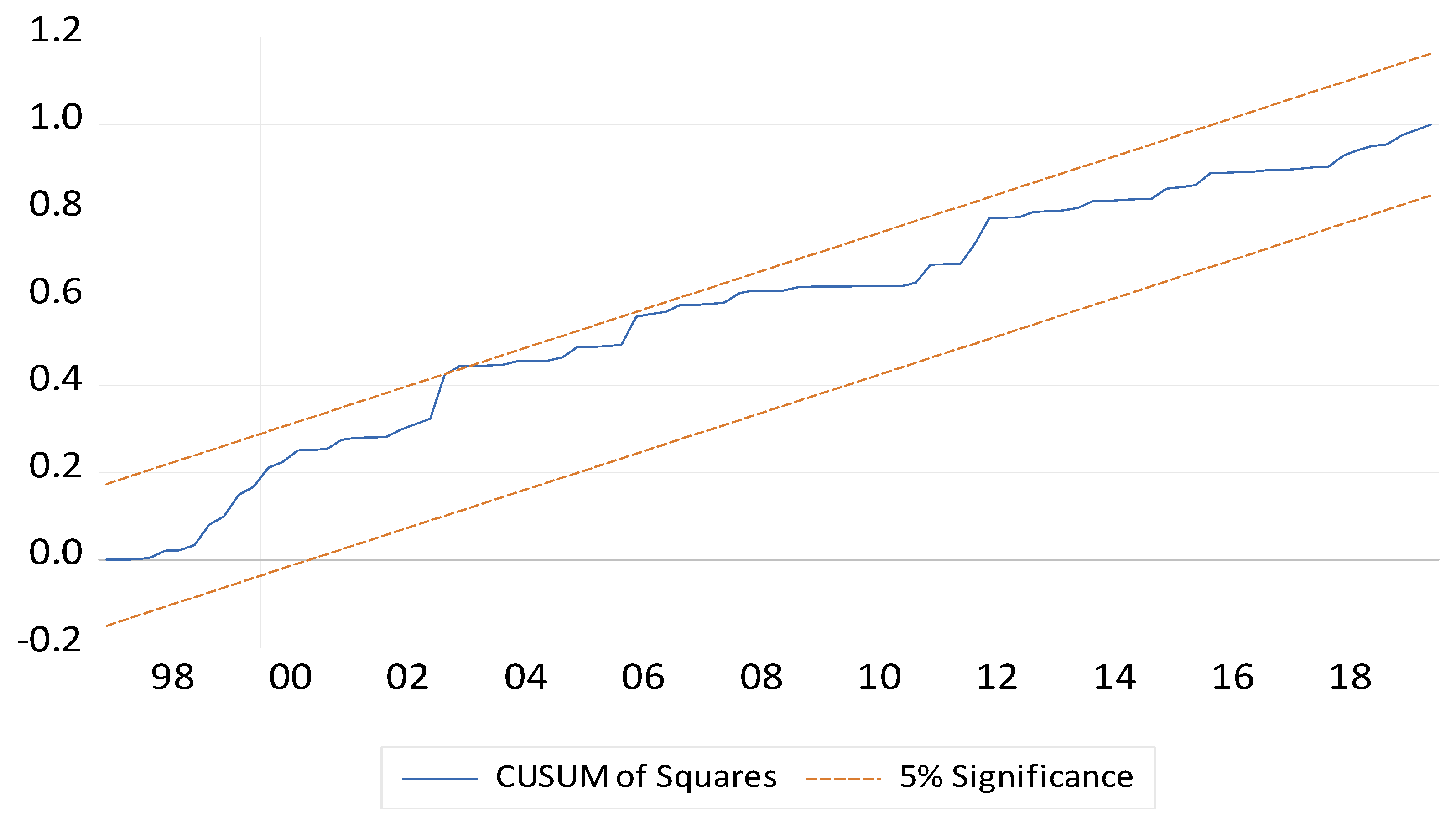

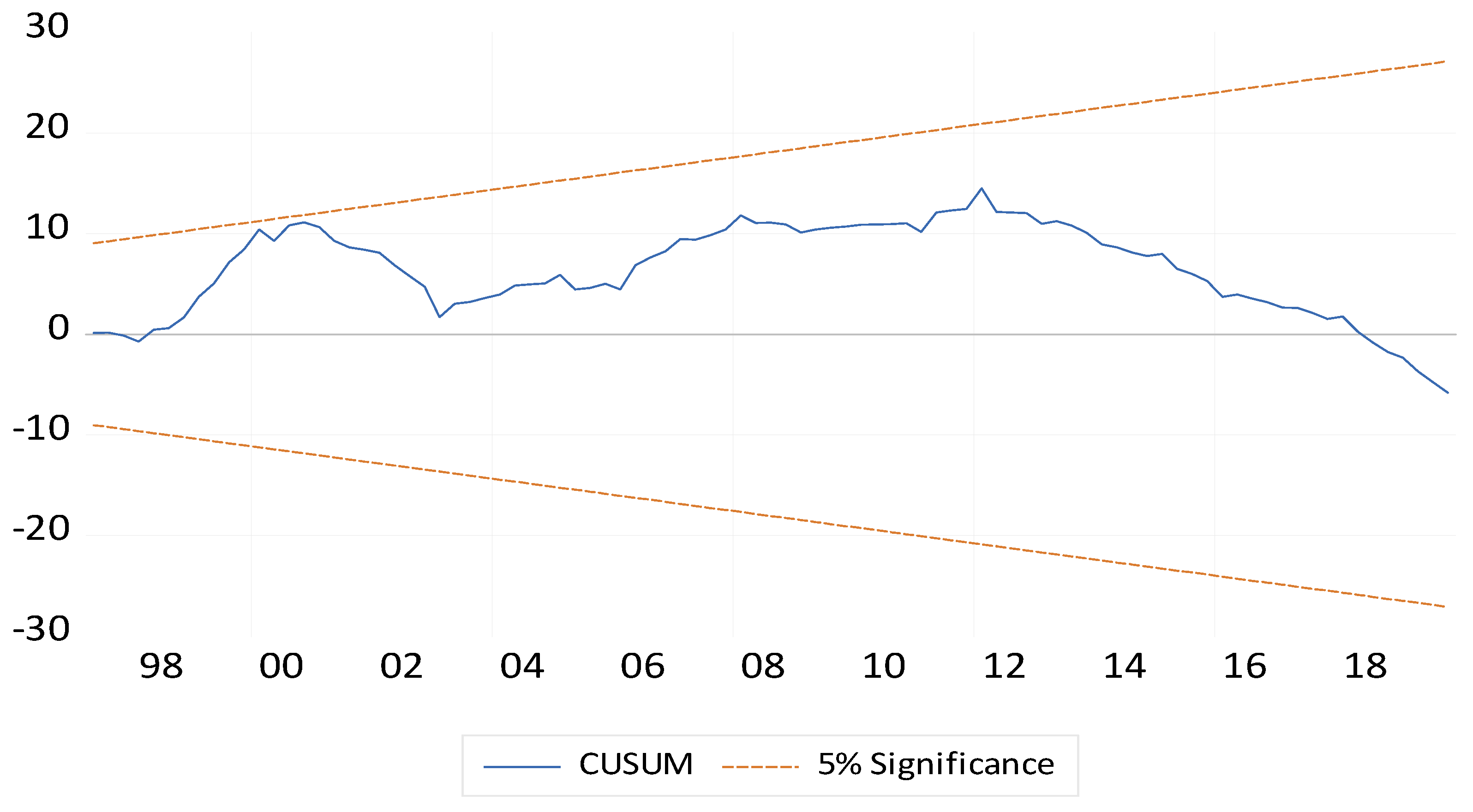

For reliable outcomes, this paper uses CUSUM and CUSUM of squares, Breusch-Godfrey serial correlation LM Test, and residual diagnostic test approaches, respectively, to capture the stability of the model and so the model is free from heteroskedasticity and serial correlation issues. In empirical evaluation, model stability and residual diagnostic tests are essential. To reduce LCO2E, the coefficients in the error-correction model must be stable to serve as a guide for policy decisions on financial development, economic output, primary energy use, and the use of renewable energy sources for the case of Poland.

Figure 4 and

Figure 5 illustrate the outcomes of cumulative stability test, while

Table 8 and

Table 9 demonstrate outcomes of both the Breusch-Godfrey serial correlation LM Test, and the residual diagnostic test, respectively. The CUSUM and CUSUM of squares results in Numbers 4 and 5 indicate that the statistical figures are within acceptable limits. This indicates that the error-correction model’s coefficients are stable and can inform policy choices regarding renewable energy consumption, primary energy use, economic output, and financial risk to lower carbon dioxide emissions in Poland.

For better policy recommendations, it is vital—and a sufficient condition—to estimate the mutual causal linkages among the variables of interest. The Fourier TY Causality Test (

Table 10) was used to assess the model. The outcome of the Fourier TY Causality Test indicates both LFRI and RE have a one direction causal effect on LCO

2, and there is no rebound action (

Figure 6).

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}