Is There a Relationship between Self-Enhancement, Conservation and Personal Tax Culture?

Abstract

:1. Introduction

2. Literature Review

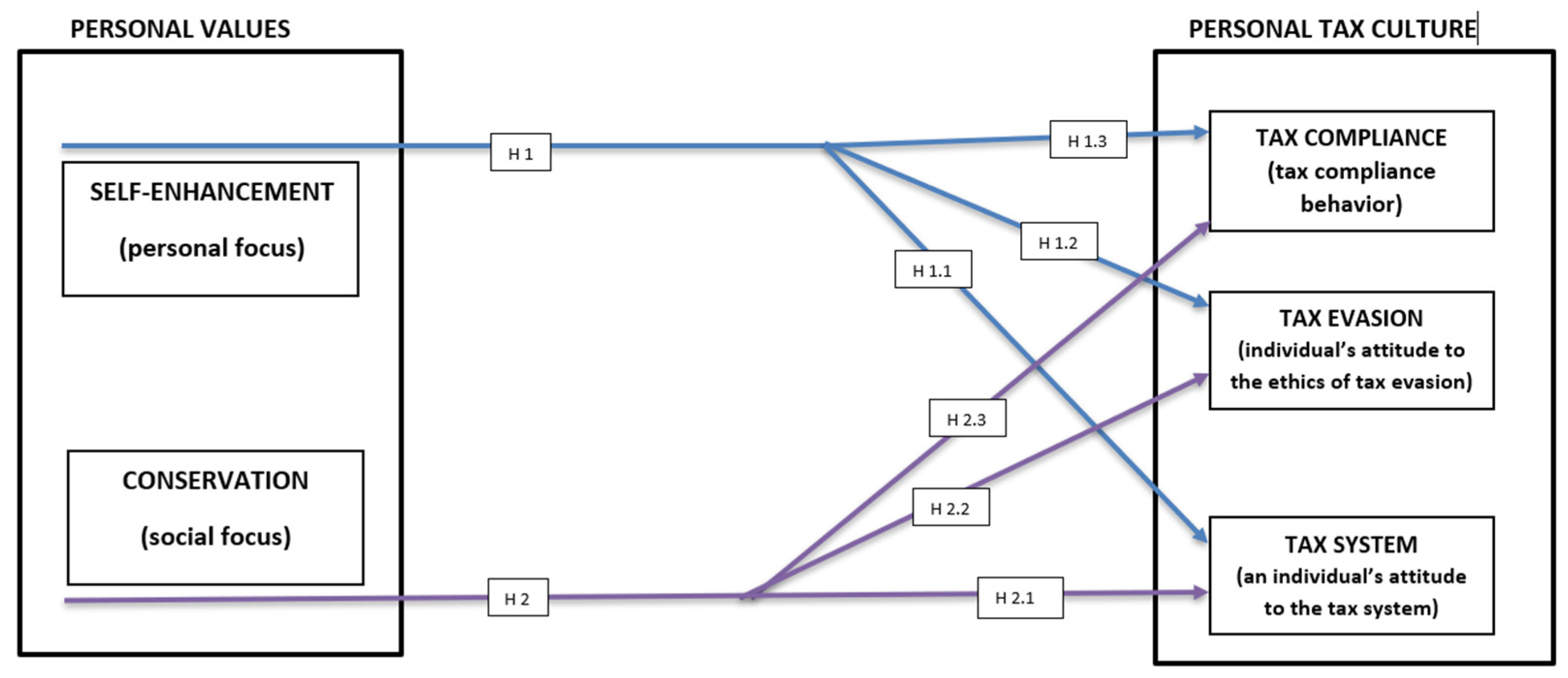

3. Framework and Hypotheses Development

- Conservation—The group of conservation personal values includes personal values such as tradition, security and conformity and expresses the individual’s behaviour in accordance with expectations and motivation for self-discipline [14].

- Personal tax culture—A set of tax-compliant behaviour and attitudes towards the ethics of tax evasion and the individual’s attitude towards the tax system.

- Tax compliance—Was measured with the variable of the individual’s tax compliance behaviour, with tax compliance being understood as the level of readiness of the individual to voluntarily fulfil their tax obligations.

- Tax evasion—Was measured with the variable of attitudes towards the ethics of tax evasion. Tax evasion generally comprises illegal arrangements where tax liability is hidden or ignored, i.e., taxpayers pays less taxes than they are legally required to pay by hiding income or information from the tax authorities [55].

- Tax system—Was measured with the variable of the individual’s attitude towards the tax system. Tax systems should be efficient, transparent, measurable and distributable and represent the integrity of tax forms in a given country with the aim of meeting fiscal, economic and social goals [77].

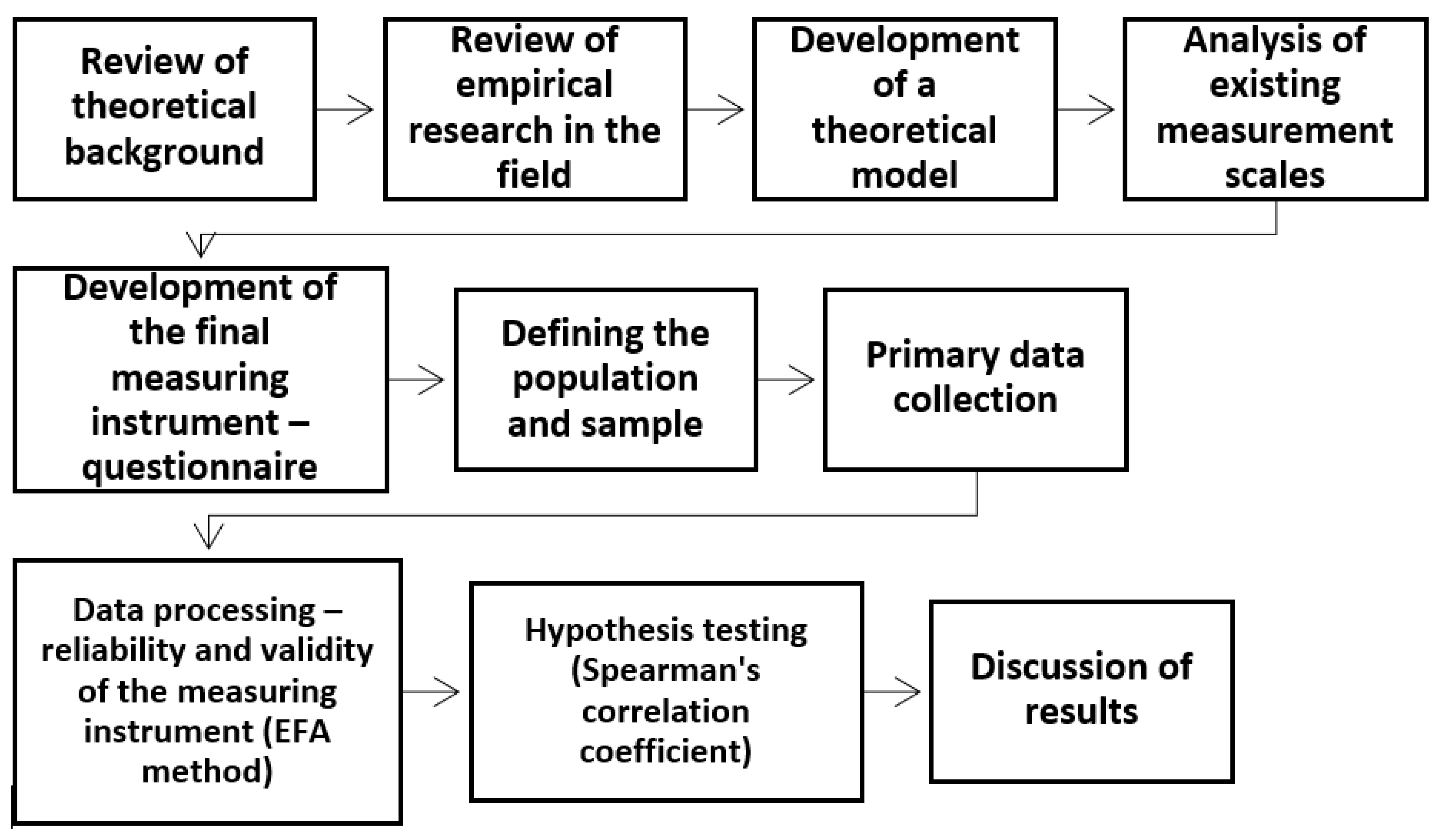

4. Materials and Methods

4.1. Sample Data

4.2. Measures

4.3. Methodology

4.4. Sample Adequacy

4.5. Data Processing Method—Exploratory Factor Analysis (EFA)

4.5.1. EFA Results for Personal Values

4.5.2. EFA Results for Personal Tax Culture

5. Results

6. Discussion

7. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Transforming Our World: The 2030 Agenda for Sustainable Development. Available online: https://sdgs.un.org/2030agenda (accessed on 14 February 2023).

- Roman, T.; Marcu, N.; Rusu, V.D.; Doacă, E.M.; Siriteanu, A.A. The Culture of Taxation: Definition and Con. Sustainability 2023, 15, 927. [Google Scholar] [CrossRef]

- Konstantinos, K.; Lazaros, N.; Panagiotis, D.; Ratten, V. Sustainable Entrepreneurship and Marketing Strategy: Exploring the Consumer “Attitude–Behavioural Intention”, Gap in the Sport Sponsorship Context. In Entrepreneurial Innovation: Strategy and Competition Aspects; Ratten, V., Ed.; Springer Nature: Singapore, 2022; pp. 53–61. [Google Scholar]

- Van de Vijver, A.; Cassimon, D.; Engelen, P.-J. A Real Option Approach to Sustainable Corporate Tax Behavior. Sustainability 2020, 12, 5406. [Google Scholar] [CrossRef]

- Saka, C.; Oshika, T.; Jimichi, M. Does Tax Avoidance Diminish Sustainability? SSRN 2017. [Google Scholar] [CrossRef]

- Issah, O.; Rodrigues, L.L. Corporate Social Responsibility and Corporate Tax Aggressiveness: A Scientometric Analysis of the Existing Literature to Map the Future. Sustainability 2021, 13, 6225. [Google Scholar] [CrossRef]

- Janová, J.; Hampel, D.; Nerudová, D. Design and validation of a tax sustainability index. Eur. J. Oper. Res. 2019, 278, 916–926. [Google Scholar] [CrossRef]

- OECD—Organisation for Economic Cooperation and Development. What Drives Tax Morale? Available online: https://www.oecd.org/ctp/tax-global/what-drives-tax-morale.pdf (accessed on 10 February 2023).

- OECD—Organisation for Economic Cooperation and Development. Boosting Tax Morale—So People and Businesses Pay Tax. Available online: https://www.oecd.org/tax/boosting-tax-morale-so-people-and-businesses-pay-tax.htm (accessed on 10 February 2023).

- Ilies, A.; Grama, V. The External Western Balkan Border of the European Union and Its Borderland: Premises for Building Functional Transborder Territorial Systems, in Annales; Zalozba Annales: Koper, Slovenia, 2010; Volume 20, pp. 457–469. [Google Scholar]

- Rickaby, M.A.; Glass, J.; Fernie, S. Conceptualizing the Relationship between Personal Values and Sustainability—A TMO Case Study. Adm. Sci. 2020, 10, 15. [Google Scholar] [CrossRef] [Green Version]

- Tóth-Nagy, G.; Utasi, A.; Neumanné, V.I.; Sebestyén, V. Data-driven supporting of Schwartz attitude model for a deeper understanding of sustainability awareness in Eastern European countries. Environ. Sustain. Indic. 2023, 17, 100226. [Google Scholar] [CrossRef]

- Bardi, A.; Schwartz, S.H. Values and Behavior: Strength and Structure of Relations. Personal. Soc. Psychol. Bull. 2003, 29, 1207–1220. [Google Scholar] [CrossRef] [PubMed]

- Schwartz, S.H. Universals in the Content and Structure of Values: Theoretical Advances and Empirical Tests in 20 Countries. Adv. Exp. Soc. Psychol. 1992, 25, 1–65. [Google Scholar] [CrossRef]

- Feldman, G.; Chao, M.M.; Farh, J.L.; Bardi, A. The motivation and inhibition of breaking rules: Personal values structures predict unethicality. J. Res. Personal. 2015, 59, 69–80. [Google Scholar] [CrossRef] [Green Version]

- Miles, A.; Yeh, C. Do demographic predictors of personal values vary by context? A test of Schwartz′s value development theory. Soc. Sci. Humanit. Open 2022, 5, 100264. [Google Scholar] [CrossRef]

- Rokeach, M. The Nature of Human Values; Free Press: New York, NY, USA, 1973. [Google Scholar]

- Schwartz, S.H.; Bilsky, W. Toward a universal psychological structure of human values. J. Personal. Soc. Psychol. 1987, 53, 550–562. [Google Scholar] [CrossRef]

- Allport, G.W.; Vernon, P.E.; Lindzey, G. Study of Values; Houghton-Mifflin: Boston, MA, USA, 1936. [Google Scholar]

- Pogačnik, V. LV, Lestvica Individualnih Vrednot: Priročnik; Zavod SR Slovenije za Produktivnost dela, Center za Psihodiagnostična Sredstva: Ljubljana, Slovenia, 1987. [Google Scholar]

- Saroglou, V.; Delpierre, V.; Dernelle, R. Values and religiosity: A meta-analysis of studies using Schwartz’s model. Personal. Individ. Differ. 2004, 37, 721–734. [Google Scholar] [CrossRef]

- Ahmad, W.; Kim, W.G.; Anwer, Z.; Zhuang, W. Schwartz personal values, theory of planned behavior and environmental consciousness: How tourists’ visiting intentions towards eco-friendly destinations are shaped? J. Bus. Res. 2020, 110, 228–236. [Google Scholar] [CrossRef]

- Hofstede, G. Culture′s Consequences: International Differences in Work Related Values; Sage Publications: London, UK; Beverly Hills, CA, USA, 1980; p. 475. [Google Scholar]

- Hofstede, G.H.; McCrae, R.R. Personality and Culture Revisited: Linking Traits and Dimensions of Culture. Cross-Cult. Res. 2004, 38, 52–88. [Google Scholar] [CrossRef] [Green Version]

- Schwartz, S.H. Universalism Values and the Inclusiveness of Our Moral Universe. J. Cross-Cult. Psychol. 2007, 38, 711–728. [Google Scholar] [CrossRef]

- Bogilović, S. Vpliv Usklajenosti Posameznikovih in Organizacijskih Vrednot na Ustvarjalnost Pri Delu. Ph.D. Thesis, Univerza v Ljubljani, Ljubljana, Slovenia, 2011. [Google Scholar]

- Schumpeter, J.A. Ökonomie und Soziologie der Einkommensteuer. Der Dtsch. Volkswirt 1929, 4, 380–385. [Google Scholar]

- Malogorski, D. Davčna Kultura v Sloveniji. Ph.D. Thesis, Zavod SR Slovenije za Produktivnost dela, Center za Psihodiagnostična Sredstva: Ljubljana, Slovenia, Ljubljana, 2004. [Google Scholar]

- Spitaler, A. Die gegenseitige Annäheurung der Steuersysteme der Kulturstaaten. In Probleme des Finanz—Und Steuerrechts—Festschrift für Ottmar Bühler. Hg.v. A. Spitaler; Dr.Otto Schmidt: Köln, Germany, 1954. [Google Scholar]

- Korostelkina, I.; Dedkova, E.; Varaksa, N.; Korostelkin, M. Models of tax relations: Improving the tax culture and discipline of taxpayers in the interests of sustainable development. E3S Web Conf. 2020, 159, 06014. [Google Scholar] [CrossRef] [Green Version]

- Richardson, G. The relationship between culture and tax evasion across countries: Additional evidence and extensions. J. Int. Account. Audit. Tax. 2008, 17, 67–78. [Google Scholar] [CrossRef]

- Nerré, B. The Concept of Tsx Culture. Intereconomics 2006, 41, 189–194. [Google Scholar] [CrossRef] [Green Version]

- Nerré, B. The Concept of Tax Culture. In Proceedings of the Annual Conference on Taxation and Minutes of the Annual Meeting of the National Tax Association, Baltimore, MD, USA, 8–10 November 2001. [Google Scholar]

- Chuenjit, P. The Culture of Taxation: Definition and Conceptual Approaches for Tax Administration. J. Popul. Soc. Stud. 2014, 22, 14–34. [Google Scholar] [CrossRef]

- Kirchler, E.; Hoelzl, E.; Wahl, I. Enforced versus voluntary tax compliance: The “slippery slope” framework. J. Econ. Psychol. 2008, 29, 210–225. [Google Scholar] [CrossRef]

- Batrancea, L.M.; Kudła, J.; Błaszczak, B.; Kopyt, M. Differences in tax evasion attitudes between students and entrepreneurs under the slippery slope framework. J. Econ. Behav. Organ. 2022, 200, 464–482. [Google Scholar] [CrossRef]

- Vincent, R.C. Vertical taxing rights and tax compliance norms. J. Econ. Behav. Organ. 2023, 205, 443–467. [Google Scholar] [CrossRef]

- Palil, M.R. Tax Knowledge and Tax Compliance Determinants in Self Assessment System in Malaysia. Ph.D. Thesis, The University of Birmingham, Birmingham, UK, 2010. [Google Scholar]

- Chan, C.W.; Troutman, C.S.; O’Bryan, D. An expanded model of taxpayer compliance: Empirical evidence from the United States and Hong Kong. J. Int. Account. Audit. Tax. 2000, 9, 83–103. [Google Scholar] [CrossRef]

- Kirchler, E. Strengthening Tax Compliance by Balancing Authorities’ Power and Trustworthiness; Van Rooij, B., Sokol, D., Eds.; Cambridge University Press: Cambridge, UK, 2021. [Google Scholar]

- Agbetunde, L.E.; Adegbie Enyi, F.F. Effect of Sentiment, Norms and Values on Tax Compliance of Self-Employed Taxpayers in South-West Nigeria. Int. J. Manag. Technol. Eng. 2019, 9, 3294–3303. [Google Scholar]

- Subramaniam, M. Sociology of Individual Voluntary Tax Compliance. Int. J. Psychosoc. Rehabil. 2020, 24, 907–917. [Google Scholar] [CrossRef]

- Kirchler, E. The Economic Psychology of Tax Behaviour; Cambridge University Press: Cambridge, UK, 2007. [Google Scholar]

- Loo, E.C. The Influence of the Introduction of Self Assessment on Compliance Behaviour of Individual Taxpayers in Malaysia; The University of Sydney: Sydney, Australia, 2006. [Google Scholar]

- Deb, R.; Chakraborty, S. Tax Perception and Tax Evasion. IIM Kozhikode Soc. Manag. Rev. 2017, 6, 174–185. [Google Scholar] [CrossRef]

- Devos, K. Tax Evasion Behaviour and Demographic Factors: An Exploratory Study in Australia. Revenue Law J. 2008, 18, 1–43. [Google Scholar] [CrossRef]

- Torgler, B.; Schneider, F. Does Culture Influence Tax Morale? Evidence from Different European Countries; Working Paper No. 2004-17; Center for Research in Economics, Management and the Arts (CREMA): Basel, Switzerland, 2004. [Google Scholar]

- McGee, R.W.; Tyler, M. Evasion and Ethics: A Demographic Study of 33 Countries; Andreas School of Business Working Paper. SSRN 2006. [Google Scholar] [CrossRef]

- Muehlbacher, S.; Kirchler, E.; Schwarzenberger, H. Voluntary versus enforced tax compliance: Empirical evidence for the “slippery slope” framework. Eur. J. Law Econ. 2011, 32, 89–97. [Google Scholar] [CrossRef]

- Kurniawan, D. The Influence of Tax Education in Higher Education on Tax Knowledge and Its Effect on Personal Tax Compliance. J. Indones. Econ. Bus. 2020, 35, 57–72. [Google Scholar] [CrossRef] [Green Version]

- Richardson, G. Determinants of tax evasion: A cross-country investigation. J. Int. Account. Audit. Tax. 2006, 15, 150–169. [Google Scholar] [CrossRef]

- Mangoting, Y.; Ganis, S.E.; Rosidi, N. Developing a Model of Tax Compliance from Social Contract Perspective: Mitigating the Tax Evasion. Procedia Soc. Behav. Sci. 2015, 211, 966–971. [Google Scholar] [CrossRef] [Green Version]

- Ma, Y.; Jiang, H.; Xiao, W. Tax evasion, audits with memory, and portfolio choice. Int. Rev. Econ. Financ. 2021, 71, 896–909. [Google Scholar] [CrossRef]

- Alstadsæter, A.; Johannesen, N.; Zucman, G. Tax Evasion and Inequality. Am. Econ. Rev. 2019, 109, 2073–2103. [Google Scholar] [CrossRef] [Green Version]

- European Commission. Accompanying the Communication from the Commission to the European Parliament and the Council—An Action Plan to Strengthen the Fight against Tax Fraud and Tax Evasion. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52012SC0404&from=SL (accessed on 15 February 2023).

- Chohan, U.W. Tax Evasion & Whistleblowers: Curious Policy or Durable Strategy? CASS Work. Pap. Econ. Natl. Aff. 2020. [Google Scholar] [CrossRef]

- Amoh, J.K.; Ali-Nakyea, A. Does corruption cause tax evasion? Evidence from an emerging economy. J. Money Laund. Control 2019, 22, 217–232. [Google Scholar] [CrossRef]

- Khalil, S.; Sidani, Y. Personality traits, religiosity, income, and tax evasion attitudes: An exploratory study in Lebanon. J. Int. Account. Audit. Tax. 2022, 47, 100469. [Google Scholar] [CrossRef]

- McGee, R.W. Three Views on the Ethics of Tax Evasion. J. Bus. Ethics 2006, 67, 15–35. [Google Scholar] [CrossRef]

- Torgler, B. Tax Morale: Theory and Empirical Analysis of Tax Compliance; Universität Basel: Basel, Switzerland, 2003. [Google Scholar]

- Alm, J. Measuring, explaining, and controlling tax evasion: Lessons from theory, experiments, and field studies. Int. Tax Public Financ. 2012, 19, 54–77. [Google Scholar] [CrossRef] [Green Version]

- Hauptman, L. The attitude of business students toward the ethics of tax evasion. Our Econ. 2014, 60, 40–48. [Google Scholar] [CrossRef] [Green Version]

- Hauptman, L.; Milfelner, B. Fairness, discrimination and personal benefits shape the attitude to ethics of tax evasion in Slovenia. In Proceedings of the 6th Global Conference on Managing in Recovering Markets, Maribor, Slovenia, 18–19 May 2015; pp. 301–315. [Google Scholar]

- Khalil, S.; Sidani, Y. The influence of religiosity on tax evasion attitudes in Lebanon. J. Int. Account. Audit. Tax. 2020, 40, 1–14. [Google Scholar] [CrossRef]

- Jackson, B.; Milliron, V. Tax Compliance Research: Findings, Problems and Prospects. J. Account. Lit. 1986, 5, 125–165. [Google Scholar]

- McGee, R.W. (Ed.) Four Views on the Ethics of Tax Evasion. In The Ethics of Tax Evasion; Springer: New York, NY, USA, 2012; pp. 3–33. [Google Scholar]

- Sidani, Y.M.; Ghanem, A.J.; Rawwas, M.Y. When idealists evade taxes: The influence of personal moral philosophy on attitudes to tax evasion—A Lebanese study. Bus. Ethics: A Eur. Rev. 2014, 23, 183–196. [Google Scholar] [CrossRef]

- Braithwaite, J.; Makkai, T. Trust and compliance. Polic. Soc. 1994, 4, 9964679. [Google Scholar] [CrossRef]

- Braithwaite, V.; Reinhart, M.; Mearns, M.; Graham, R. Preliminary Findings from the Community Hopes, Fears and Actions Survey; Working Paper No. 3; Australian National University: Canberra, Australia, 2001. [Google Scholar]

- Murphy, K.; Byng, K. Preliminary Findings from the Australian Tax System Survey of Tax Scheme Investors; Australian National University: Canberra, Australia, 2002. [Google Scholar]

- Cristea, L.A.; Voda, A.D.; Ungureanu, D.M. Tax Culture: Approached as a new constituent element of the fiscal system. Ann. “Constantin Brâncuşi” Univ. Târgu Jiu Econ. Ser. 2021, 2, 124–132. [Google Scholar]

- Schwartz, S.H. Basic Values: How They Motivate and Inhibit Prosocial Behavior. In Prosocial Motives, Emotions, and Behavior: The Better Angels of Our Nature; American Psychological Association: Washington, DC, USA, 2010; pp. 221–241. [Google Scholar]

- McGee, R.W.; Lingle, C. Tax Evasion and Business Ethics: A Comparative Study of Guatemala and the USA. SSRN Electron. J. 2006, 56, 892323. [Google Scholar] [CrossRef]

- Pulfrey, C.; Butera, F. Why neoliberal values of self-enhancement lead to cheating in higher education: A motivational account. Psychol. Sci. 2013, 24, 2153–2162. [Google Scholar] [CrossRef] [Green Version]

- Gruenfeld, D.H.; Inesi, M.E.; Magee, J.C.; Galinsky, A. Power and the objectification of social targets. J. Personal. Soc. Psychol. 2008, 95, 111–127. [Google Scholar] [CrossRef] [Green Version]

- Piff, P.K.; Stancato, D.M.; Cote, S.; Mendoza-Denton, R.; Keltner, D. Higher social class predicts increased unethical behavior. Proc. Natl. Acad. Sci. 2012, 109, 4086–4091. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Richardson, G. The influence of culture on tax systems internationally: A Theoretical and empirical analysis. J. Int. Account. Res. 2007, 6, 57–79. [Google Scholar] [CrossRef]

- Dragan, I.M.; Isaic-Maniu, A. Snowball Sampling Completion. J. Stud. Soc. Sci. 2013, 5, 160–177. [Google Scholar]

- Dragan, I.M.; Isaic-Maniu, A. An Original Solution for Completing Research through Snowball Sampling—Handicapping Method. Adv. Appl. Sociol. 2022, 12, 729–746. [Google Scholar] [CrossRef]

- Watkins, M.W. Exploratory Factor Analysis: A Guide to Best Practice. J. Black Psychol. 2018, 44, 219–246. [Google Scholar] [CrossRef]

- Shrestha, N. Factor Analysis as a Tool for Survey Analysis. Am. J. Appl. Math. Stat. 2021, 9, 4–11. [Google Scholar] [CrossRef]

- Fávero, L.P.; Belfiore, P. Chapter 12—Principal Component Factor Analysis. Data Sci. Bus. Decis. Mak. 2019, 2019, 383–438. [Google Scholar] [CrossRef]

- Janssens, W.; Wijnen, K.; De Pelsmacker, P.; Van Kenhove, P. Marketing Research With SPSS; Pearson Education: London, UK, 2008; p. 441. [Google Scholar]

- Bastič, M. Metode Raziskovanja; MariEkonomsko-Poslovna Fakulteta: Maribor, Slovenia, 2006. [Google Scholar]

- Yong, A.G.; Pearce, S. A Beginner’s Guide to Factor Analysis: Focusing on Exploratory Factor Analysis. Tutor. Quant. Methods Psychol. 2013, 9, 79–94. [Google Scholar] [CrossRef] [Green Version]

- Guadagnoli, E.; Velicer, W.E. Relation of sample size to the stability of component patterns. Psychol. Bull. 1988, 103, 265–275. [Google Scholar] [CrossRef]

- Field, A. Discovering Statistics Using SPSS; Sage: London, UK, 2009. [Google Scholar]

- Streiner, D.L. Figuring Out Factors: The Use and Misuse of Factor Analysis. Can. J. Psychiatry 1994, 39, 135–140. [Google Scholar] [CrossRef]

- Dancey, C.P.; Reidy, J. Statistics Without for Psychology; Pearson Education Limited: London, UK, 2007. [Google Scholar]

- Gauthier, T. Detecting Trends Using Spearman’s Rank Correlation Coefficient. Environ. Forensics 2001, 2, 359–362. [Google Scholar] [CrossRef]

- Schwartz, S.H. An Overview of the Schwartz Theory of Basic Values. Online Read. Psychol. Cult. 2012, 2, 294. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Cornerstones | Variables | Authors | Numbers of Used Questions from an Existing Questionnaire (Prior Research) |

|---|---|---|---|

| Tax evasion | an individual’s attitude to the ethics of tax evasion | McGee and Lingle, 2006 [73] | 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 17, 18 (15/18) |

| Tax system | an individual’s attitude to the tax system | Murphy and Byng, 2002 [70] | 1, 2, 4, 5, 8, 11, 12, 13, 15, 22, 27, 36, 42, 47, 49 (15/52) |

| Tax compliance | tax compliance behaviour | Palil, 2010 [38] | 36, 37, 38, 41, 42, 44, 45, 46, 48, 49, 50, 52, 54, 55, 56 (15/23) |

| Personal values | scale of personal values (21 PVQ) | Schwartz, 1992 [14] | all 21 PVQ (21/21) |

| Criterion | Level of Acceptance | Authors |

|---|---|---|

| Bartlett’s Test of Sphericits (BTS) | Chi-Square; p < 0.05 | Yong and Pearce, 2013 [85] |

| Kaiser-Meyer-Olkin Measure of Sampling Adequacy (KMO) | >0.05 | Yong and Pearce, 2013 [85] |

| Communalities values | >0.04 | Guadagnoli and Velicer, 1988 [86] |

| Factor loadings | >0.05 | Field, 2009 [87] |

| Total variance explained | at least 50% | Streiner, 1994 [88] |

| Cronbach’s Alpha | >0.06 | Janssens et al., 2008 [83] |

| Construct | Kaiser-Meyer-Olkin Measure of Sampling Adequacy | Bartlett’s Test of Sphericits; Chi-Square; p Value |

|---|---|---|

| Personal values | 0.781 | 0.000 |

| Personal tax culture (Tax compliance + tax evasion + tax system) | 0.886 | 0.000 |

| Variable Label | Variable | Communalities | Factor Loadings Factor JCS | |||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |||

| PV_4_01 | It is very important to him to help people around him. He wants to care for other people. | 0.634 | 0.782 | |||

| PV_4_02 | It is important to him to be loyal to his friends. He wants to devote himself to people close to him. | 0.782 | 0.874 | |||

| PV_4_03 | He thinks it is important that every person in the world be treated equally. He wants justice for everybody, even for people he does not know. | 0.619 | 0.751 | |||

| PV_4_04 | It is important to him to listen to people who are different from him. Even when he disagrees with them, he still wants to understand them. | 0.445 | 0.579 | |||

| PV_4_06 | Thinking up new ideas and being creative is important to him. He likes to do things in his own original way. | 0.527 | 0.699 | |||

| PV_4_07 | It is important to him to make his own decisions about what he does. He likes to be free to plan and to choose his activities for himself. | 0.606 | 0.720 | |||

| PV_4_08 | He likes surprises and is always looking for new things to do. He thinks it is important to do lots of different things in life. | 0.671 | 0.809 | |||

| PV_4_09 | He looks for adventures and likes to take risks. He wants to have an exciting life. | 0.613 | 0.555 | |||

| PV_4_10 | Having a good time is important to him. He likes to “spoil” himself. | 0.539 | 0.645 | |||

| PV_4_11 | He seeks every chance he can to have fun. It is important to him to do things that give him pleasure. | 0.586 | 0.578 | |||

| PV_4_12 | It is very important to him to show his abilities. He wants people to admire what he does. | 0.706 | 0.831 | |||

| PV_4_13 | Being very successful is important to him. He likes to impress other people. | 0.718 | 0.823 | |||

| PV_4_14 | It is important to him to be rich. He wants to have a lot of money and expensive things. | 0.620 | 0.742 | |||

| PV_4_15 | It is important to him to be in charge and tell others what to do. He wants people to do what he says. | 0.662 | 0.767 | |||

| PV_4_16 | It is important to him to live in secure surroundings. He avoids anything that might endanger his safety. | 0.523 | 0.646 | |||

| PV_4_17 | It is very important to him that his country be safe from threats from within and without. He is concerned that social order be protected. | 0.531 | 0.663 | |||

| PV_4_18 | He believes that people should do what they are told. He thinks people should always follow rules, even when no-one is watching. | 0.512 | 0.709 | |||

| PV_4_19 | It is important to him always to behave properly. He wants to avoid doing anything people would say is wrong. | 0.692 | 0.824 | |||

| Number of Items | 19 | |||||

| Total Variance Explained for Construct | 61.036 | |||||

| Cronbach’s Alpha for Self-Enhancement | 0.844 | |||||

| Cronbach’s Alpha for Conservation | 0.718 | |||||

| Variable Label | Variable | Communalities | Factor Loadings Factor JCS | ||

|---|---|---|---|---|---|

| 1 | 2 | 3 | |||

| C_1_08 | I wish not to comply with tax laws because the penalty rates are very low, and I can afford to pay the penalty. | 0.550 | −0.613 | ||

| C_1_09 | I wish not to comply with tax laws because I believe that the penalty is lower than my tax saving due to not comply with taw laws. | 0.492 | −0.590 | ||

| C_1_13 | I wish not to comply with tax laws because my friends do not comply, and they have never been penalised. | 0.514 | −0.605 | ||

| C_1_14 | I wish not to comply with tax laws because my parents do not comply, and they have never been penalised. | 0.624 | −0.686 | ||

| C_1_15 | I wish not to comply with tax laws because my relatives do not comply, and they have never been penalised. | 0.668 | −0.710 | ||

| C_3_01 | If tax rates are too high, is tax evasion… | 0.636 | 0.774 | ||

| C_3_02 | Even if tax rates are not too high, is tax evasion… | 0.452 | 0.541 | ||

| C_3_03 | If tax system is unfair, is tax evasion… | 0.661 | 0.781 | ||

| C_3_04 | If a large portion of the money collected is wasted, is tax evasion… | 0.619 | 0.777 | ||

| C_3_05 | Even if most of the money collected is spent wisely, is tax evasion… | 0.435 | 0.594 | ||

| C_3_06 | Even if a large portion of the money collected is spent on worthy projects, is tax evasion… | 0.480 | 0.632 | ||

| C_3_07 | If a large portion of the money collected is spent on projects that do not benefit me, is tax evasion… | 0.628 | 0.789 | ||

| C_3_08 | Even if a large portion of the money collected is spent on projects that do benefit me, is tax evasion… | 0.576 | 0.703 | ||

| C_3_09 | If everyone is doing it, is tax evasion… | 0.591 | 0.716 | ||

| C_3_10 | If a significant portion of the money collected winds up in the pockets of corrupt politicians or their families and friends, is tax evasion… | 0.502 | 0.706 | ||

| C_3_11 | If the probability of getting caught is low, is tax evasion… | 0.715 | 0.812 | ||

| C_3_12 | If some of the proceeds go to support a war that I consider to be unjust, is tax evasion… | 0.548 | 0.724 | ||

| C_3_13 | If I can’t afford to pay, is tax evasion… | 0.531 | 0.720 | ||

| C_3_14 | If the government discriminates against me because of my religion, race or ethnic background, is tax evasion… | 0.627 | 0.788 | ||

| C_3_15 | If the government imprisons people for their political opinions, is tax evasion… | 0.659 | 0.809 | ||

| C_5_05 | The Tax Office listens to powerful interest groups, not to ordinary citizens. | 0.456 | 0.669 | ||

| C_5_07 | The Tax Office is more concerned about making their job easier than making it easier for taxpayers. | 0.677 | 0.821 | ||

| C_5_10 | The Tax Office is more interested in catching you for doing the wrong thing than helping you do the right thing. | 0.672 | 0.818 | ||

| C_5_12 | The Tax Office’s decisions are too influenced by political pressures. | 0.537 | 0.709 | ||

| C_5_13 | The Tax Office is generally honest in the way it deals with people. | 0.619 | 0.779 | ||

| C_5_14 | The Tax Office tries to be fair when making their decisions. | 0.607 | 0.769 | ||

| C_5_15 | The tax system may not be perfect, but it works well enough for most citizens. | 0.546 | 0.732 | ||

| Number of Items | 27 | ||||

| Total Variance Explained for Construct | 57.137 | ||||

| Cronbach’s Alpha for Construct Tax Evasion (1) | 0.941 | ||||

| Cronbach’s Alpha for Construct Tax Compliance (2) | 0.879 | ||||

| Cronbach’s Alpha for Construct Tax System (3) | 0.813 | ||||

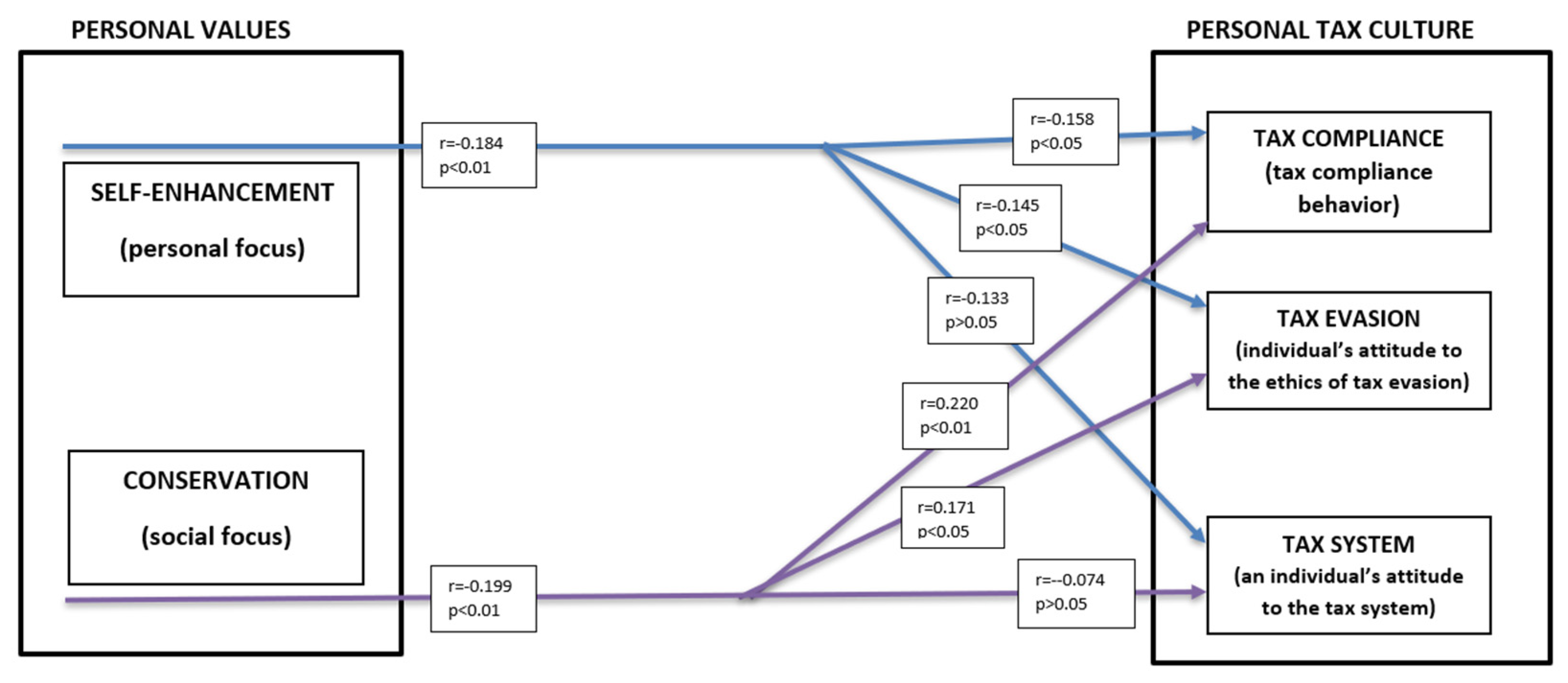

| Hypothesis | Spearman’s Rho Correlation Coefficient (r) | Sig. (2-Tailed) |

|---|---|---|

| H1 | −0.184 | p < 0.01 |

| H1.1 | −0.133 | p > 0.05 |

| H1.2 | −0.145 | p < 0.05 |

| H1.3 | −0.158 | p < 0.05 |

| H2 | 0.199 | p < 0.01 |

| H2.1 | −0.074 | p > 0.05 |

| H2.2 | 0.171 | p < 0.05 |

| H2.3 | 0.220 | p < 0.01 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hlastec, A.; Mumel, D.; Hauptman, L. Is There a Relationship between Self-Enhancement, Conservation and Personal Tax Culture? Sustainability 2023, 15, 5797. https://doi.org/10.3390/su15075797

Hlastec A, Mumel D, Hauptman L. Is There a Relationship between Self-Enhancement, Conservation and Personal Tax Culture? Sustainability. 2023; 15(7):5797. https://doi.org/10.3390/su15075797

Chicago/Turabian StyleHlastec, Aleksandra, Damijan Mumel, and Lidija Hauptman. 2023. "Is There a Relationship between Self-Enhancement, Conservation and Personal Tax Culture?" Sustainability 15, no. 7: 5797. https://doi.org/10.3390/su15075797