The Influence of Green Supply Chain Management Practices on Corporate Sustainability Performance

1

College of Business Administration, University of Business and Technology, Jeddah 21448, Saudi Arabia

2

College of Advertising, University of Business and Technology, Jeddah 23435, Saudi Arabia

*

Author to whom correspondence should be addressed.

Sustainability 2023, 15(6), 5459; https://doi.org/10.3390/su15065459

Submission received: 21 January 2023

/

Revised: 12 March 2023

/

Accepted: 15 March 2023

/

Published: 20 March 2023

(This article belongs to the Special Issue Multiple Criteria Decision-Making Techniques in Sustainable Supply Chains and Logistics Management)

Abstract

:Sustainability is a major concern for several industries in Saudi Arabia, especially those in the industrial sector. By using green methods, many businesses intend to become sustainable. Green practices provide staff with instructions regarding how to maintain business sustainability while performing necessary production tasks. Accordingly, the purpose of this study was to investigate how green practices affect the sustainability performance of businesses. Partial least squares (PLS) analysis was used to examine data from 250 sets of completed onnaires. Our findings showed that green practices significantly impact corporate sustainability performance.

1. Introduction

Rapid globalization and industrialization in the last ten years have had negative impacts on the environment, contributing to issues such as global warming, air and water pollution, and chemical and hazardous explosions [1]. In recent years, researchers, the government, NGOs, consumers, and industries have all adopted green supply chain management (GSCM) as a sustainability pillar in response to growing environmental consciousness [2]. Researchers have long addressed the advantages of GSCM techniques [3], including their ability to enhance economic performance, enhance organizational competitiveness, and reduce environmental impacts [4].

As a result of its adverse impacts on the environment, global warming has generated widespread alarm [5] as environmental challenges such as rapid resource depletion, pollution, and losses in species diversity have deteriorated the ecological equilibrium [6].

The pressing task facing governments worldwide is to reduce this largely human-caused negative environmental impact [5]. Due to growing environmental awareness, businesses face even larger obstacles than in years past [7], as their human impacts on the climate include supply chains. Consequently, manufacturers are the primary focus of all energy-conservation and pollution-reduction regulations and programs [8]. Therefore, it is vital to regulate industrial supply chain operations so that they do not negatively affect the environment [9]. Environmental concerns and government globalization policies have driven many manufacturing enterprises to adopt specific tactics that will aid in the adoption of sustainability [10]. Green supply chain management (GSCM) refers to the activities undertaken to achieve this objective. GSCM broadens the standard notion of supply chain management within the context of more eco-friendly management [11].

Both primary and secondary stakeholders demand that businesses implement policies and strategies to address the adverse effects of their operations on the environment and societal safety due to the environmental concerns raised by their engagement in business activities. These demands have encountered resistance since some scholars and academics argue that a firm’s primary role is to increase shareholders’ profits and that the government is responsible for social and environmental issues [12].

The Earth’s sustainability and humanity’s existence are jeopardized due to supply chain operations, particularly logistics activities, which are among the crucial tasks performed by businesses. These activities increase energy consumption, waste, and hazardous gas emissions into the environment. Ineffective logistics management may result in increased energy use, waste use, and greenhouse gas emissions, resulting in excessive pollution [13]. Since the 1970s, there has been a noticeable increase of 90% in global carbon emissions [14], with industrialization and the combustion of fossil fuels responsible for around 78% of these emissions [15].

Many organizations have implemented eco-friendly techniques into their logistics services, resulting in the formation of green logistics management techniques to meet stakeholders’ environmental demands and enhance societal safety. Environmental practitioners and researchers are currently investigating the success of environmental measures in protecting the environment while also sustaining enterprises by increasing profitability and shareholder value [12]. This research has produced contradictory findings about the effect of environmentally friendly supply chain approaches on environmental and financial performance [16]. More research is necessary to contribute to the continuing discussion to help managers make informed decisions about adopting green practices that might ensure enhanced performance and sustainability.

The majority of existing work has been conducted in specific industries, particularly manufacturing enterprises [17], at the expense of other businesses that considerably contribute to environmental degradation, which limits the generalization of currently available results [12]. The impact of GSCM on all elements of sustainability performance and their interconnections has received little attention, particularly in Saudi Arabia. Additional research is required to fill the identified severe gaps, thus motivating this study.

Manufacturers are required by law in many industrialized nations in North America and Europe to collect, recover, and/or dispose of used goods and packaging, which has sparked the development of concepts (or terms) such as “reverse logistics”, “closed-loop supply chains”, and “green supply chains” [18]. Industries, governments, and consumers are becoming more aware of the need to protect the environment and reduce pollution [8]. However, according to [19], the demand for GSCM adoption is stronger in the less environmentally conscious companies of developing countries (such as India, China, and Brazil). These countries are competing for quicker economic growth, and their economies are expanding due to rapid industrialization [20]. Accordingly, they are already emerging as the world’s leading polluters of the future [19]. Regarding the environmental damage caused by industrial development, China has been at the forefront among developing nations [21]. Saudi Arabia has not demonstrated much regard for environmental protection while pursuing economic expansion [22,23,24]. Companies in Saudi Arabia are reluctant to commit to sustainability issues unless they are legally required to do so. As a result, GSCM, which has already matured in some rich countries, is still a relatively new idea in India and other emerging nations [25]. We were encouraged by this fact to consider Saudi Arabian manufacturers as our study object.

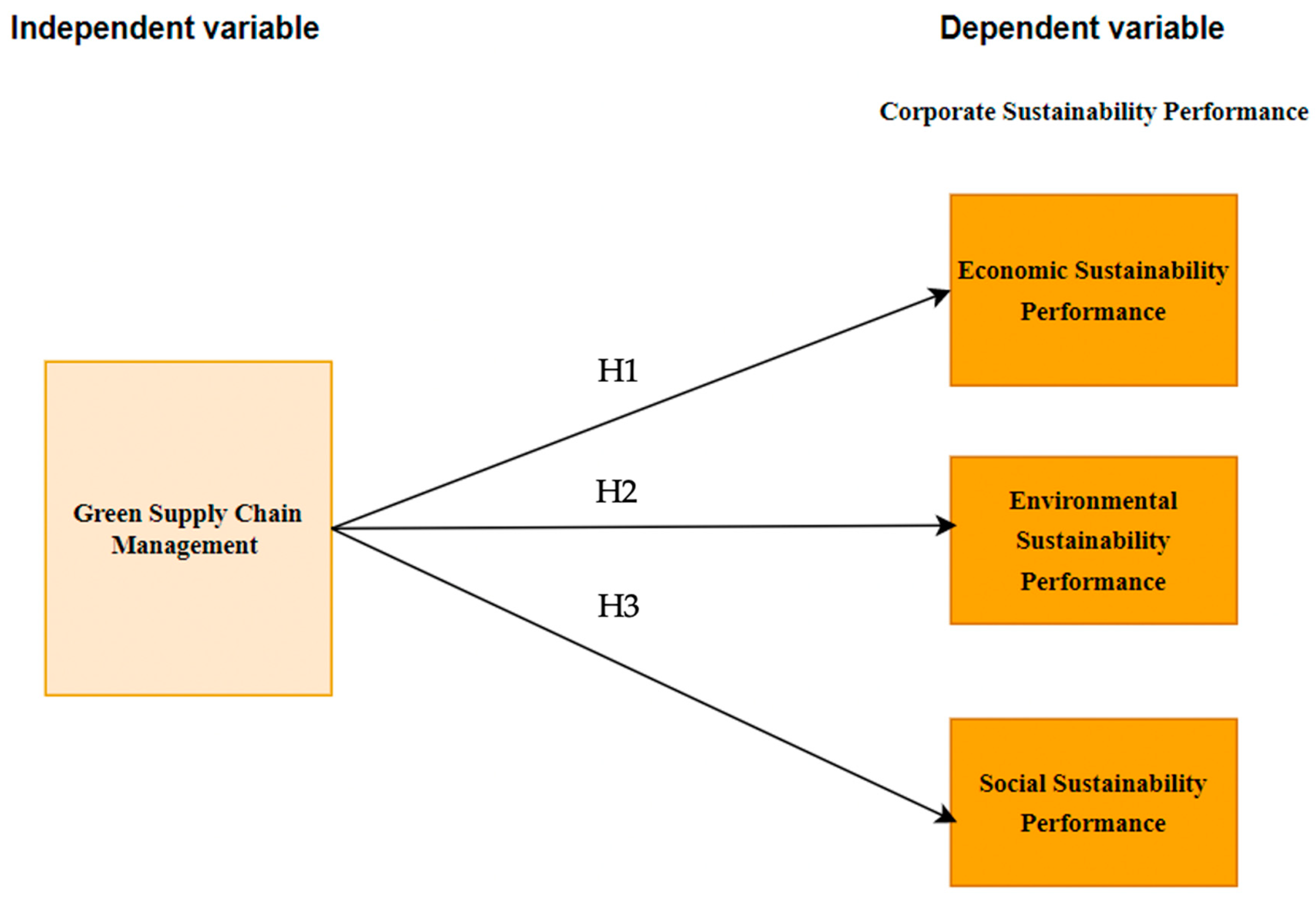

Considering the significant gaps in the existing literature and the need to broaden its scope regarding small and medium-sized firms in Saudi Arabia, this study was conducted to evaluate the efficacy of green supply chain practices in achieving higher levels of environmental, social, and economic performance in manufacturing industries. In this study, we created a complete model (shown in Figure 1) that describes how green supply chain strategies affect social, environmental, and economic performance. The results of this study contribute to industry managers’ jobs and add to the existing body of knowledge on sustainability performance.

To test our proposed hypotheses, we surveyed Saudi Arabian manufacturing firms to ascertain the extent of the adoption of green supply chain management techniques and their impact on corporate performance. The study was primarily focused on employees responsible for each organization’s ISO paperwork or environmental management system. The sampling strategy employed in the study was cluster sampling. Of the 540 surveys distributed via electronic mail, 250 were returned to the authors by respondents. The findings demonstrated that using green supply chain management techniques favors and significantly influences economic, social, and environmental performance.

The rest of the paper is structured as follows. Section 2 describes the related literature; Section 3 provides hypotheses development; Section 4 presents methodology; Section 5 reports data analysis and results; Section 6 describes discussion; and finally, Section 7 provides conclusions, limitations, and future work outlooks.

2. Literature Review

2.1. Green Supply Chain Management (GSCM) Practices

GSCM has attracted much corporate attention during the past three decades [26]. Various characteristics of GSCM practices have been described in earlier studies [27]. According to [28], GSCM techniques are fundamentally green initiatives that focus on minimizing, reusing, and recycling materials and energy to enhance environmental impacts at every phase of the manufacturing process, including design, procurement, production, distribution, and product recovery [29].

According to [30], GSCM refers to the distribution of goods and services from suppliers and manufacturers to end users while accounting for monetary, informational, and material flows in the environment. GSCM integrates an environmental viewpoint with SCM, spanning material sourcing and selection, product design, manufacturing processes, finished item distribution to clients, and product disposal after expiration [31]. Due to consumer demands and legal requirements, monitoring and assessing environmental management comprise the initial stage of GSCM, which culminates in the adoption of proactive measures involving several reverse activities such as refurbishing, recycling, reworking, reusing, and remanufacturing [32].

GSCM can also be categorized as a collaboration and monitoring-based set of procedures for achieving economic and environmental objectives [33].

All organizational departments and upstream and downstream supply chain partners must work in unison to accomplish these goals [2].

There has been a rise in interest in GSCM approaches from many supply chain and operational management practitioners and scholars. Expanding environmental deterioration through losses in raw material resources, overflows of waste sites, and population increases, among other processes, is the primary driver of GSCM’s growing significance [34]. However, the use of GSCM is aimed to increase returns, improve business sense, and offer environmentally sustainable products, i.e., to improve an organization’s business value performance [33,34]. Companies must integrate environmental standards throughout the whole supply chain for sustainable performance since they are held liable and charged for the environmental liabilities of their suppliers.

We identified three GSCM techniques after conducting a thorough analysis of the literature: internal environmental management (IEM), eco-design (ED), and customer cooperation (CC).

Internal environmental management (IEM) is the process of integrating global sustainability and corporate social responsibility (GSCR) into an organization’s strategy and proving their commitment through top management vision, middle management involvement, and the development of cross-functional teams [35]. Proactive businesses have highlighted IEM as the cornerstone of the GSCM transformation process. Eco-design (ED) is used to build a product with the least possible environmental impact through product life-cycle analysis [36]. Eco-design provides pollution prevention compliance during a product’s life cycle and comprises a proactive approach to environmental degradation. It also helps reduce potential future repair expenses [37]. This strategy considers the environment from the conception of ideas to the design of items that consume fewer resources, consume less energy, and emit fewer dangerous gases, all of which can improve both environmental and economic performance [38].

Businesses must adapt to the present environment and consider customers valuable partners in collaborative efforts to address environmental concerns. Customer service and green training for eco-design, green manufacturing, and green packaging are examples of customer cooperation (CC) activities [39]. CC engages people in everything from eco-design to distribution, packaging, and product returns [40]. To exchange real-time information and effectively carry out all of the above-mentioned procedures, it is necessary to maintain a long-term, trust-based relationship [41].

2.2. Corporate Sustainability Performance (CSP)

Measuring organizational performance is an important step in obtaining crucial details about a company’s goals and its level of accomplishment [42]. Companies that operate well may attract investors who often evaluate an organization’s entire performance before considering any investment-related choices, such as whether to begin, continue, or discontinue investments [42].

The phrase “corporate sustainability” is not well-defined [43]. Corporate sustainability can refer to the company strategies and investment models that use business methods to satisfy and stabilize the requirements of present and future shareholders, according to the UN General Assembly (1987). Similarly, [44] defined corporate sustainability as meeting current stakeholder requirements while preserving an organization’s capacity to meet future stakeholder needs. According to [45], the process through which firms manage their financial, ecological, and social–commercial risks, obligations, and possibilities is known as sustainability in the business world. Corporate sustainability is broadly and similarly defined [46] as the practice of conducting operations in order to meet present requirements without risking future generations’ demands while evaluating how company operations affect community well-being. “Business sustainability” is the capacity to engage in commerce to protect the health of the economy, the ecosystem, and society [47].

Corporate sustainability is critical for realizing an organization’s vision without jeopardizing its market advantage while meeting the demands of economic growth, environmentalism, and social responsibilities [43]. An organization’s transition to a sustainable future must be realized through the effort and responsibility of executives, stakeholders, and employees [48]. In this context, corporate sustainability performance refers to an organization’s capacity to effectively and efficiently utilize its limited resources over time, such as by minimizing waste and considering economic, environmental, and social sustainability performance [42]. In short, the triple bottom line (as shown in Figure 2), which incorporates social, environmental, and economic sustainability performance, means “business sustainability performance” [49,50].

According to previous research on the triple bottom line idea, business sustainability sits at the crossroads of economic, environmental, and social performance [51,52]. According to [53], corporate sustainability performance refers to how well a company integrates governance, social, environmental, and economic concerns into its operations and their effects on the organization and society. Corporate sustainability requires the collaboration of an organization’s stakeholders regarding present and future economic, social, and environmental demands [54]. An organization with a high CSP has competitive benefits that boost efficiency, revenues, and savings, providing advantages over rivals [48]. It can be difficult for organizations to simultaneously advance social and human welfare, lessen their influence on the environment, and guarantee the successful accomplishment of their goals [55].

2.3. Descriptions of the CSP Triple Bottom Line

2.3.1. Economic Sustainability Performance

The primary purpose of a business is to generate stakeholder value via financial sustainability performance [56]. The primary focuses from an economic viewpoint are the production and distribution of goods and services in relation to wants and desires [48], as well as how businesses manage their cash flow [45]. According to [57], an organization’s economic performance reflects its influence on the economic condition of its stakeholders and the economic system at the domestic, national, or international level. Economic performance at the organizational level represents the impact of a company on the economic condition of stakeholders and the domestic and international sustainability to remain competitive in the market [57], [58] as economic sustainability adds to the fulfillment of shareholders and the organization itself.

2.3.2. Environmental Sustainability Performance

Environmental difficulties such as global warming, climate change, and sustainability concerns have been the principal focuses of study for the past two decades. They are now the foremost focuses of many organizations [42]. Environmental sustainability must be incorporated into strategic planning and models for firms to effectively compete in the international market [56].

Like other types of capital, the environment offers critical inputs for both consumption and production; this could be called natural capital [59]. Ref. [60] established a link between long-term environmental quality and sustainability. Recycling, emission reduction, and waste treatment programs are examples of sustainable organizational practices [61].

Green supply chain management is often used to achieve the environmental goals of company sustainability by controlling energy usage and exhaustible resources, reducing manufacturing waste output, and adopting safe and legal disposal strategies [58]. Environmental performance represents an organization’s capacity to minimize water pollution, air pollution, and soil degradation; its capacity to implement appropriate waste management practices and avoid or lessen the use of toxic and dangerous materials; and its capacity to implement any advancements aimed at reducing the regularity of environmental disasters and accomplishing energy savings [25].

2.3.3. Social Sustainability Performance

The social side of corporate sustainability is concerned with protecting or improving future generations’ social well-being [58]. The impact of corporate behavior on society is measured in terms of social performance [62]. In essence, social performance or the social bottom line is the accomplishment of an organization’s social mission in terms of societal interests through the incorporation of recognized social ideals and the fulfillment of social obligations [56].

Social sustainability in human capital is exemplified in behaviors such as maintaining and providing a safe workplace environment, employment practices, benefits, salary, and development and training [58]. Employees’ well-being is typically assessed based on whether they obtain a basic wage and properly functioning benefits (such as medical benefits, annual leave, clean drinking water, and a safe workplace) specified by labor legislation, as well as whether they are subjected to ill treatment, bullying, or violence at work [62]. Beyond what is required by law, socially responsible organizations link their operational activities with social, ethical, and environmental challenges, perhaps resulting in a better quality of life for the majority of stakeholders [42].

3. Development of the Hypotheses

Green Logistics/Supply Chain Management Impact on Sustainable Performance

Going green fundamentally means seeking information, pursuits, and lifestyles that improve environmental well-being. Green practices are eco-friendly activities [61], and green business techniques help organizations become more competitive while enhancing their financial and environmental performance [63]. Green practices are widely recognized to improve an organization’s brand image, save costs [64], and increase competitiveness by enabling expansion into new markets and the achievement of complete compliance with existing standards [65]. Basically, greater investment in environmental practices favors an organization’s competitive edge and improves its operational performance [66]. According to several studies, environmental management or performance and business performance are positively correlated [67]. Organizations can significantly reduce costs by using green practices, resulting in cost advantages over rivals [68]. Consequently, adopting green practices can demonstrate a commitment to environmental sustainability [69].

Ref. [32] evaluated the efficacy of green practices in the context of the Indian manufacturing industry. They discovered that green techniques such as lowering particulate matter emissions, specific effluent discharge, carbon dioxide intensity, and water consumption minimized environmental harm while improving company performance. In another study, adopting green manufacturing processes, purchasing energy-efficient products and equipment, working with suppliers to guarantee uniform packaging, and engaging in reverse logistics by accepting customer returns all demonstrated beneficial effects on the study’s sample of chemical manufacturing enterprises [70]. According to the authors’ findings, green practices (such as green purchasing) had favorable and significant impacts on the performance of large chemical manufacturing enterprises in Kenya [70].

According to [71], a strong and favorable correlation exists between green business practices and company sustainability performance. In addition, [72] evaluated the application of green practices in the Brazilian electrical and electronics industry and discovered that green practices, specifically those related to green strategy and green innovation, influence competitiveness in the sector by minimizing environmental impacts. Moreover, [73] successfully demonstrated how green practices affect an organization’s social and environmental sustainability performance. Ref. [63] Studied the effectiveness of green practices in the context of the Indian manufacturing sector [32] and found that green practices lessened environmental harm and enhanced business performance, as evidenced by lower emissions of particulate matter, specific effluent discharge, carbon dioxide intensity, and water consumption. In another study, [74] showed that green practices benefited the operational performance of Brazilian industrial organizations and that businesses could benefit from green practices by working with upstream providers of environmentally friendly production technologies (such as by sharing environmental information) and considering green customers’ preferences when conducting business.

Moreover, [65] conducted empirical research that reinforced the significance of green practices for Chinese manufacturing companies’ environmental performance. Organizations are more likely to perform better to improve their corporate sustainability responsibility image for their stakeholders when they adhere to the environmental aspect of sustainability [65].

We developed inquiry statements in response to the following problem question: What connection exists between green business practices and the sustainability performance of corporations? We assumed that green supply chain management has a favorable effect on social, economic, and environmental performance, and we formulated three hypotheses as follows:

H1:

Green supply chain management has a positive impact on economic sustainability performance.

H2:

Green supply chain management has a positive impact on environmental sustainability performance.

H3:

Green supply chain management has a positive impact on social sustainability performance.

4. Methodology

To test the given hypotheses, this study relied on a survey of Saudi Arabian manufacturing companies to determine the level of adoption of green supply chain management methods and their effects on corporate performance. The development of the survey instrument, data collection methods, respondent profiles, data collation methods, and reliability and validity analyses are described here.

We used cluster sampling in this study. The sample size was established using the five methods recommended by [75]. The population, or the total number of enterprises, was first identified. The size of the population sample was then calculated using the table created by Krejcie and Morgan in 1970 [76]. As one of the most potent statistical tools in social research, SEM allows for the simultaneous testing of several associations [77]. Even though earlier studies were primarily focused on covariance-based approaches (CB-SEM) such as SMART PLS [77], a variance-based approach (or PLS-SEM), with a unique methodological feature, was chosen as a viable alternative. We sent a total of 540 questionnaire forms via electronic mail to operational and production managers of manufacturing companies with operations in Saudi Arabia. The study specifically concentrated on the staff members in charge of or accountable for the organization’s environmental management system or ISO documentation. Out of the 540 questionnaires, respondents returned 250 surveys to the study authors.

The survey questionnaire’s items (GSCM practices and performance) and scales were modified from the existing literature [35] to fit the Saudi Arabian context. A five-point Likert scale was used to evaluate each response as indicated in Table A1.

The sample comprised manufacturing facilities that were randomly chosen from a list of 500 known manufacturing businesses that may have used GSCM techniques. This list was created using a database of all Saudi Arabian manufacturing companies after checking each company’s website. The manufacturing sector was then divided into four main areas.

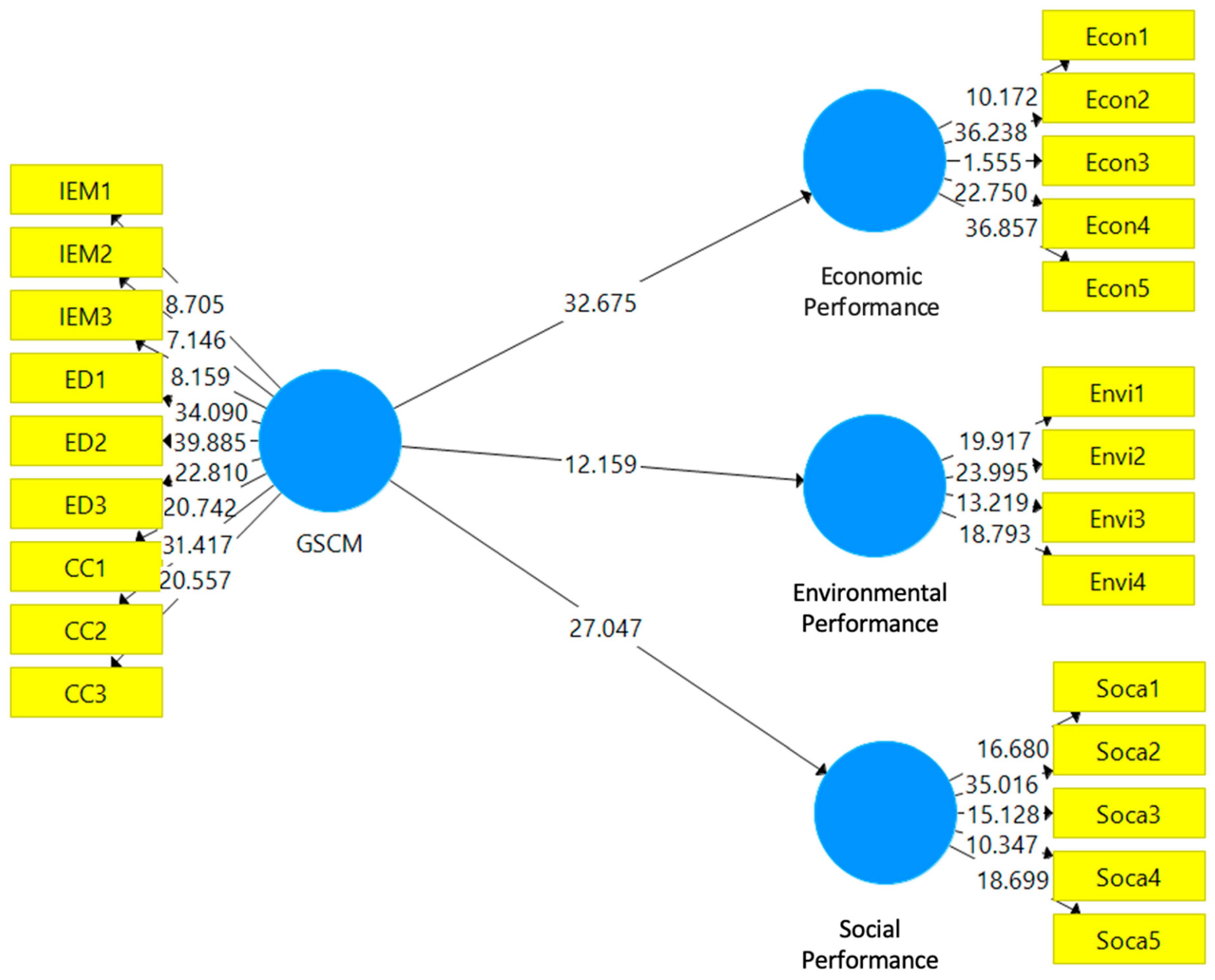

Factor analysis, confirmatory factor analysis, and structural equation modeling (SEM) were used to examine the obtained data. The study’s constructs’ validity and dependability were evaluated with exploratory factor analysis (EFA). In order to evaluate construct reliability, convergent and discriminant validity, and the overall fit of the measurement model, a confirmatory factor analysis (CFA) was also conducted. To test the proposed hypotheses, structural equation modeling was used. Software-wise, smart PLS v.3 was utilized for SEM and confirmatory factor analysis (CFA) while SPSS 22 was used for exploratory factor analysis (EFA).

5. Data Analysis and Results

Examining the construct reliability, convergent validity, and discriminant validity allowed for the evaluation of the measurement model [77]. We first evaluated the construct’s composite reliability and Cronbach’s alpha to gauge the model’s dependability. Our measurements showed that the first-order construct’s composite reliability ranged from 0.858 to 0.927 (Table 1). Second, the convergent validity was evaluated using the average variance extracted (AVE) measure [24]. All of the construct’s AVE values were found to be above the threshold value of >0.50 and within the range of 0.564 to 0.644, indicating that our model’s convergent validity was acceptable [77]. Additionally, the Cronbach’s alpha range was above the threshold value of 0.7, specifically between 0.792 and 0.910, indicating that our measurement model design was trustworthy and appropriate for the model [77].

Furthermore, the cross-loading matrix (Table 2) and [78]’s criterion were employed to assess the test’s discriminant validity. To pass a cross-loading test, the outer loadings of the measurement items on a linked construct must be greater than all of their outer loadings on other constructions. According to our study’s cross-loading matrix data, all assessment items had higher loadings on their target constructs. According to [78]’s criterion, the square root of each construct’s AVE should be greater than its highest correlation with any other construct [24]. The FornellLarcker criterion was satisfied in our study because the square root of the AVE, which served as a diagonal element, was greater than the off-diagonal correlation in the rows and columns. Consequently, the combined findings of the cross-loading and Fornell–Larcker criteria demonstrated that the data’s discriminant validity was fulfilled.

Discriminate validity, developed by Fornell and Larcker, is a potent and frequently used metric that measures the interrelationship between reflective variables and their indicators. With this metric, the operationalization of a collection of variables that are connected or unconnected to a case study is estimated, and a reliability index’s value should ideally be greater than 0.70. Cross-loadings differ if there is a correlation between constructs, but our study’s cross-loading values matched the outer loadings. Therefore, as indicated in Table 3, we evaluated our study’s discriminatory validity.

Our next step was to evaluate the structured relationships among the variables after examining the instrument’s reliability and validity. The advantage of SEM-PLS over other algorithms is that it can be used to examine all assembled relations at once compared to other algorithms that compute them separately. As a result, we examined both direct and indirect impacts in our structural equation model. Figure 3 shows the structural model of the current study. To determine the significance of the claimed association, a bootstrapping procedure was applied to 1000 observations; p-values were considered during this process (as shown in Table 4). The significance of the hypotheses was examined using p-values with a threshold level of 0.05. The findings revealed that all hypotheses had p-values of less than 0.05. Therefore, H1, H2, and H3 were acceptable.

6. Discussion

Regarding the Malaysian manufacturing sector, [79] discovered that green practices improved corporate sustainability performance. Moreover, [80] sent out self-administered surveys and received responses from 178 significant ISO14001-certified manufacturers in Malaysia; according to their study, adopting green practices improved firms’ sustainability performance in terms of their economic, environmental, and social sustainability. Additionally, [32,64,70,71,73,79,81] concluded that green practices help organizations perform well in terms of sustainability. Organizations are more likely to improve their corporate sustainability responsibility reputation for their customers when they are devoted to the environmental aspect of sustainability according to [64], who used empirical evidence to show the value of green practices for Chinese manufacturing companies’ environmental performance. Finally, our findings also showed that green supply chain management practices have positive impacts on environmental, social, and economic performance. In short, many empirical studies have validated the beneficial relationship between green practices and corporate sustainability performance at the organizational level.

In this study, we developed inquiry statements in response to the following problem question: What connection exists between green business practices and the sustainability performance of corporations? We assumed that green supply chain management positively affects social, economic, and environmental performance, and our hypotheses were ultimately validated.

7. Conclusions, Limitations, and Future Work

In an effort to encourage Saudi Arabian manufacturing companies to maintain environmental friendliness while consistently working to improve social, economic, and environmental corporate performance, we aimed to illuminate the green supply chain management practices currently used by these companies and their impact on corporate sustainability performance in this study. According to this study’s findings, eco-design, corporate environmental management, and customer participation are all examples of green supply chain management methods.

Items (GSCM practices and performance) and scales from our survey questionnaire were adjusted based on previously published research to fit the Saudi Arabian context. Each response was scored on a five-point Likert scale. Our sample comprised manufacturing facilities that were randomly chosen from a list of 500 known manufacturing businesses that may have used GSCM techniques. This list was created using a database of all Saudi Arabian manufacturing companies after checking each company’s website. The manufacturing sector was then divided into four main areas.

Global scholars and practitioners have been seriously concerned about sustainability, particularly regarding the importance of green company development [82]. Our findings demonstrate how green supply chain management techniques greatly impact economic, environmental, and social performance. Our measurements of sustainable performance that consider social, environmental, and economic factors are significant theoretical contributions to the body of available knowledge on the green practices and corporate sustainability performance of Saudi Arabian manufacturing organizations.

Despite its importance in the business setting, the connection between green practices and corporate sustainability performance has only been researched by a small number of studies [79]. In the context of the industrial sector, this study offers empirical support for the relationship between GSCM and sustainability. The Saudi Arabian industrial sector and the manufacturing industries of other emerging and developed countries (particularly the managers of manufacturing organizations) are anticipated to benefit from the thorough understanding of the linkages between green practices and corporate sustainability performance described in this study. For organizations to remain competitive, they must consider the impact of their environmental activities on sustainable global supply chain management [83], as manufacturing businesses can save significant amounts of money by successfully implementing green practices, which will eventually boost operational performance. Moreover, a high level of environmental performance or management is linked to better corporate performance, and green habits can demonstrate a dedication to environmental sustainability. Ultimately, our study’s conclusions and findings are anticipated to guide workers in industrial organizations to favorably regard green operations as a crucial duty.

Employing workers as participants in our study had benefits and drawbacks. On the one hand, employees are regarded as a practical sample that can produce initial and generalizable results. On the other hand, employees could display carelessness and a lack of focus on a study’s objectives. This problem is most obvious in studies when participants can self-administer surveys at their own convenience; individuals might not carefully read the information or answer questions, especially at the end of extensive questionnaires. Monitoring how long it takes each respondent to complete a questionnaire and removing any responses that took much less time than anticipated are two ways to lessen this type of impact. The cutoff point for completion should differ depending on the instrument and subject groups, and it was established using standard deviation and average completion time values in the current study. Another disadvantage of using an employee sample in our study was the differing level of GSCM understanding shown by participants depending on their education or experiences.

To accurately represent levels of green practice and corporate sustainability performance, we recommend that future studies consider manufacturing organizations in other countries and expand their number of samples to ensure the generalizability of results. Following these practices will allow researchers to provide further insights into how green practices affect businesses’ sustainability performance while establishing and maintaining competitive advantages.

Author Contributions

Conceptualization, M.T.H.; Methodology, M.T.H.; Investigation, B.A.B.; Resources, B.A.B.; Writing—review & editing, A.B. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

Table A1.

Questionnaire.

| Environmental Performance | Strongly Disagree | Disagree | Neutral | Agree | Strongly Agree |

|---|---|---|---|---|---|

| The company reduction of solid wastes | |||||

| The company reduced waste and emissions from the operations | |||||

| The company decreased consumption of hazardous/harmful/toxic materials | |||||

| The company decreased of frequency environmental accidents | |||||

| The company’s improvement of an enterprise’s environmental situation | |||||

| Economic Performance | Strongly Disagree | Disagree | Neutral | Agree | Strongly Agree |

| The company decreased the cost of materials purchasing | |||||

| The company decreased the cost of energy consumption | |||||

| The company decreased of fee for waste treatment | |||||

| The company decreased of fee for waste discharge | |||||

| Social Performance | Strongly Disagree | Disagree | Neutral | Agree | Strongly Agree |

| The company improved health and safety for employees or the community. | |||||

| The company protected the claims and rights of aboriginal people or localCommunity. | |||||

| The company showed concern for the visual aspects of the organization‘s facilities and operations | |||||

| The company communicated the organizational environmental impactsand risks to the general public. | |||||

| The company considered the interests of stakeholders in investment decisionsby creating a formal dialogue. | |||||

| Green Supply Chain Management Practices | Strongly Disagree | Disagree | Neutral | Agree | Strongly Agree |

| The company Commitment of GSCM from senior managers (IEM1) | |||||

| The company has a support for GSCM from mid-level managers (IEM2) | |||||

| In the company, there are environmental compliance and auditing programs (IEM3) | |||||

| In the company there is cooperation with customers for eco-design (CC1) | |||||

| In the company, there is cooperation with customers for cleaner production (CC2) | |||||

| In the company, there is cooperation with customers for green packaging (CC3) | |||||

| In the company, there is design of products for reduced consumption of material/energy (ED1) | |||||

| In the company, there is the Design of products for reuse, recycling, recovery of material, and parts (ED2) | |||||

| In the company, there is Design of products to avoid or reduce the use of hazardous products and/or theirthe manufacturing process (ED3) |

References

- Geng, R.; Mansouri, S.A.; Aktas, E. The Relationship between Green Supply Chain Management and Performance: A Meta-Analysis of Empirical Evidences in Asian Emerging Economies. Int. J. Prod. Econ. 2017, 183, 245–258. [Google Scholar] [CrossRef] [Green Version]

- Saeed, A.; Jun, Y.; Nubuor, S.; Priyankara, H.; Jayasuriya, M. Institutional Pressures, Green Supply Chain Management Practices on Environmental and Economic Performance: A Two Theory View. Sustainability 2018, 10, 1517. [Google Scholar] [CrossRef] [Green Version]

- Green, K.W.; Zelbst, P.J.; Meacham, J.; Bhadauria, V.S. Green Supply Chain Management Practices: Impact on Performance. Supply Chain. Manag. Int. J. 2012, 17, 290–305. [Google Scholar]

- Khan, S.A.R.; Dong, Q.; Zhang, Y.; Khan, S.S. The Impact of Green Supply Chain on Enterprise Performance: In the Perspective of China. J. Adv. Manuf. Syst. 2017, 16, 263–273. [Google Scholar] [CrossRef]

- Sharma, S.; Gandhi, M.A. Exploring Correlations in Components of Green Supply Chain Practices and Green Supply Chain Performance. Compet. Rev. 2016, 26, 332–368. [Google Scholar] [CrossRef]

- Çankaya, S.; Sezen, B. Effects of Green Supply Chain Management Practices on Sustainability Performance. J. Clean. Prod. 2019, 209, 1565–1578. [Google Scholar]

- Al-Sheyadi, A.; Muyldermans, L.; Kauppi, K. The Complementarity of Green Supply Chain Management Practices and the Impact on Environmental Performance. J. Environ. Manag. 2019, 242, 186–198. [Google Scholar] [CrossRef]

- Zhu, Q.; Qu, Y.; Geng, Y.; Fujita, T. A Comparison of Regulatory Awareness and Green Supply Chain Management Practices among Chinese and Japanese Manufacturers. Bus. Strategy Environ. 2017, 26, 18–30. [Google Scholar] [CrossRef]

- Zaid, A.A.; Jaaron, A.A.M.; Bon, A.T. The impact of green human resource management and green supply chain management practices on sustainable performance: An empirical study. J. Clean. Prod. 2018, 201, 939–951. [Google Scholar] [CrossRef]

- Han, Z.; Huo, B. The Impact of Green Supply Chain Integration on Sustainable Performance. Ind. Manag. Data Syst. 2020; ahead-of-print. [Google Scholar]

- Walker, P.H.; Seuring, P.S.; Sarkis, P.J.; Klassen, P.R. Sustainable Operations Management: Recent Trends and Future Directions. Int. J. Oper. Prod. Manag. 2014, 34. [Google Scholar] [CrossRef]

- Baah, C.; Jin, Z.; Tang, L. Organizational and Regulatory Stakeholder Pressures Friends or Foes to Green Logistics Practices and Financial Performance: Investigating Corporate Reputation as a Missing Link. J. Clean. Prod. 2020, 247, 119125. [Google Scholar] [CrossRef]

- Demir, E.; Huang, Y.; Scholts, S.; Van Woensel, T. A Selected Review on the Negative Externalities of the Freight Transportation: Modeling and Pricing. Transp. Res. Part E Logist. Transp. Rev. 2015, 77, 95–114. [Google Scholar] [CrossRef]

- Herold, D.M.; Lee, K.-H. Carbon management in the logistics and transportation sector: An overview and new research directions. Carbon Manag. 2017, 8, 1–19. [Google Scholar] [CrossRef]

- IPCC Climate. Mitigation of Climate Change Promotion of Climate Change Policies in Turkey LIFE05/TCY/TR164 LAND-USE CHANGE and FORESTRY Transportation Air Quality Management Congestion Management Sustainable Development in the Sector Methane Emissions from Energy and Waste Recycling of Wastes; Pubmed Publishers: Ankara, Turkey, 2014; Available online: https://www.google.com.hk/search?q=Mitigation+of+Climate+Change+Promotion+of+Climate+Change+Policies+in+Turkey+LIFE05%2FTCY%2FTR164+LAND-USE+CHANGE+and+FORESTRY+Transportation+Air+Quality+Management+Congestion+Management+Sustainable+Development+in+the+Sector+Methane+Emissions+from+Energy+and+Waste+Recycling+of+Wastes&ei=BwUYZOfPN-7j2roPk6OtuAw&ved=0ahUKEwin74-W-On9AhXusVYBHZNRC8cQ4dUDCA4&uact=5&oq=Mitigation+of+Climate+Change+Promotion+of+Climate+Change+Policies+in+Turkey+LIFE05%2FTCY%2FTR164+LAND-USE+CHANGE+and+FORESTRY+Transportation+Air+Quality+Management+Congestion+Management+Sustainable+Development+in+the+Sector+Methane+Emissions+from+Energy+and+Waste+Recycling+of+Wastes&gs_lcp=Cgxnd3Mtd2l6LXNlcnAQAzIICAAQogQQsAMyCAgAEKIEELADSgQIQRgBUN8BWN8BYJYKaAFwAHgAgAEAiAEAkgEAmAEAoAECoAEByAECwAEB&sclient=gws-wiz-serp (accessed on 20 January 2023).

- Agyabeng-Mensah, Y.; Afum, E.; Ahenkorah, E. Exploring Financial Performance and Green Logistics Management Practices: Examining the Mediating Influences of Market, Environmental and Social Performances. J. Clean. Prod. 2020, 258, 120613. [Google Scholar] [CrossRef]

- Evangelista, P. Environmental Sustainability Practices in the Transport and Logistics Service Industry: An Exploratory Case Study Investigation. Res. Transp. Bus. Manag. 2014, 12, 63–72. [Google Scholar] [CrossRef]

- Mitra, S.; Datta, P.P. Adoption of Green Supply Chain Management Practices and Their Impact on Performance: An Exploratory Study of Indian Manufacturing Firms. Int. J. Prod. Res. 2013, 52, 2085–2107. [Google Scholar] [CrossRef]

- Scur, G.; Barbosa, M.E. Green Supply Chain Management Practices: Multiple Case Studies in the Brazilian Home Appliance Industry. J. Clean. Prod. 2017, 141, 1293–1302. [Google Scholar] [CrossRef]

- Mathivathanan, D.; Kannan, D.; Haq, A.N. Sustainable Supply Chain Management Practices in Indian Automotive Industry: A Multi-Stakeholder View. Resour. Conserv. Recycl. 2018, 128, 284–305. [Google Scholar] [CrossRef]

- Namagembe, S.; Ryan, S.; Sridharan, R. Green Supply Chain Practice Adoption and Firm Performance: Manufacturing SMEs in Uganda. Manag. Environ. Qual. Int. J. 2019, 30, 5–35. [Google Scholar] [CrossRef]

- Kouaib, A. Corporate Sustainability Disclosure and Investment Efficiency: The Saudi Arabian Context. Sustainability 2022, 14, 13984. [Google Scholar] [CrossRef]

- Kouaib, A.; Amara, I. Corporate Social Responsibility Disclosure and Investment Decisions: Evidence from Saudi Indexed Companies. J. Risk Financ. Manag. 2022, 15, 495. [Google Scholar] [CrossRef]

- Singh, H.P.; Singh, A.; Alam, F.; Agrawal, V. Impact of Sustainable Development Goals on Economic Growth in Saudi Arabia: Role of Education and Training. Sustainability 2022, 14, 14119. [Google Scholar] [CrossRef]

- Choudhary, K.; Sangwan, K.S. Adoption of Green Practices throughout the Supply Chain: An Empirical Investigation. Benchmarking Int. J. 2019, 26, 1650–1675. [Google Scholar] [CrossRef]

- Zhao, R.; Liu, Y.; Zhang, N.; Huang, T. An Optimization Model for Green Supply Chain Management by Using a Big Data Analytic Approach. J. Clean. Prod. 2017, 142, 1085–1097. [Google Scholar] [CrossRef]

- Habib, M.A.; Bao, Y.; Ilmudeen, A. The Impact of Green Entrepreneurial Orientation, Market Orientation and Green Supply Chain Management Practices on Sustainable Firm Performance. Cogent Bus. Manag. 2020, 7, 1743616. [Google Scholar] [CrossRef]

- Masudin, I.; Wastono, T.; Zulfikarijah, F. The Effect of Managerial Intention and Initiative on Green Supply Chain Management Adoption in Indonesian Manufacturing Performance. Cogent Bus. Manag. 2018, 5, 1485212. [Google Scholar] [CrossRef]

- Tippayawong, K.; Niyomyat, N.; Sopadang, A.; Ramingwong, S. Factors Affecting Green Supply Chain Operational Performance of the Thai Auto Parts Industry. Sustainability 2016, 8, 1161. [Google Scholar] [CrossRef] [Green Version]

- Zhu, Q.; Sarkis, J.; Lai, K. Examining the Effects of Green Supply Chain Management Practices and Their Mediations on Performance Improvements. Int. J. Prod. Res. 2012, 50, 1377–1394. [Google Scholar] [CrossRef]

- Srivastava, S.K. Green Supply-Chain Management: A State-of-The-Art Literature Review. Int. J. Manag. Rev. 2007, 9, 53–80. [Google Scholar] [CrossRef]

- Ali, A.; Haseeb, M. Radio Frequency Identification (RFID) Technology as a Strategic Tool towards Higher Performance of Supply Chain Operations in Textile and Apparel Industry of Malaysia. Uncertain Supply Chain. Manag. 2019, 7, 215–226. [Google Scholar] [CrossRef]

- Chu, S.; Yang, H.; Lee, M.; Park, S. The Impact of Institutional Pressures on Green Supply Chain Management and Firm Performance: Top Management Roles and Social Capital. Sustainability 2017, 9, 764. [Google Scholar] [CrossRef] [Green Version]

- Wilkerson, T. Environmental life cycle. ACS ChemWorx 2005, 45, 4570–4578. [Google Scholar]

- Zhu, Q.; Sarkis, J.; Lai, K. Confirmation of a Measurement Model for Green Supply Chain Management Practices Implementation. Int. J. Prod. Econ. 2008, 111, 261–273. [Google Scholar] [CrossRef]

- Al-Ghwayeen, W.S.; Abdallah, A.B. Green Supply Chain Management and Export Performance. J. Manuf. Technol. Manag. 2018, 29, 1233–1252. [Google Scholar] [CrossRef]

- Zailani, S.; Jeyaraman, K.; Vengadasan, G.; Premkumar, R. Sustainable Supply Chain Management (SSCM) in Malaysia: A Survey. Int. J. Prod. Econ. 2012, 140, 330–340. [Google Scholar] [CrossRef]

- Zsidisin, G.A.; Siferd, S.P. Environmental Purchasing: A Framework for Theory Development. Eur. J. Purch. Supply Manag. 2001, 7, 61–73. [Google Scholar] [CrossRef]

- Vijayvargy, L.; Thakkar, J.; Agarwal, G. Green Supply Chain Management Practices and Performance. J. Manuf. Technol. Manag. 2017, 28, 299–323. [Google Scholar] [CrossRef]

- Bouzon, M.; Govindan, K.; Rodriguez, C.M.T. Evaluating Barriers for Reverse Logistics Implementation under a Multiple Stakeholders’ Perspective Analysis Using Grey Decision Making Approach. Resour. Conserv. Recycl. 2018, 128, 315–335. [Google Scholar] [CrossRef]

- Marshall, D.; McCarthy, L.; Heavey, C.; McGrath, P. Environmental and Social Supply Chain Management Sustainability Practices: Construct Development and Measurement. Prod. Plan. Control 2014, 26, 673–690. [Google Scholar] [CrossRef]

- Shad, M.K.; Lai, F.-W.; Fatt, C.L.; Klemeš, J.J.; Bokhari, A. Integrating Sustainability Reporting into Enterprise Risk Management and Its Relationship with Business Performance: A Conceptual Framework. J. Clean. Prod. 2019, 208, 415–425. [Google Scholar] [CrossRef]

- KOÇ, S.; Durmaz, V. Future Oriented Corporate Leadership Model. J. Glob. Strateg. Manag. 2015, 1, 52. [Google Scholar] [CrossRef]

- Wu, Y.; Su, G.; Tang, S.; Liu, W.; Ma, Z.; Zheng, X.; Liu, H.; Yu, H. The combination of in silico and in vivo approaches for the investigation of disrupting effects of tris (2-chloroethyl) phosphate (TCEP) toward core receptors of zebrafish. Chemosphere 2017, 168, 122–130. [Google Scholar] [CrossRef]

- Jan, A.; Marimuthu, M.; Mat Isa, M.P. bin M. The Nexus of Sustainability Practices and Financial Performance: From the Perspective of Islamic Banking. J. Clean. Prod. 2019, 228, 703–717. [Google Scholar] [CrossRef]

- Compact, U.G. Transforming Care Is Everyone’s Business. Nurs. Stand. 2015, 29, 3. [Google Scholar]

- Hassini, E.; Surti, C.; Searcy, C. A Literature Review and a Case Study of Sustainable Supply Chains with a Focus on Metrics. Int. J. Prod. Econ. 2012, 140, 69–82. [Google Scholar] [CrossRef]

- Desjardins, R.L.; Sivakumar, M.V.K. Foreword. Agric. For. Meteorol. 2007, 142, 88–89. [Google Scholar] [CrossRef]

- Mdolo, A.; Banda, R.; Phiri, A.; Sambala, E.Z.; Wiyeh, A.B.; Wiysonge, C.S. Burden of Seasonal Influenza in Sub-Saharan Africa: A Systematic Review Protocol. BMJ Open 2018, 8, e022949. [Google Scholar]

- Nguyen, M.; Phan, A.; Matsui, Y. Contribution of Quality Management Practices to Sustainability Performance of Vietnamese Firms. Sustainability 2018, 10, 375. [Google Scholar] [CrossRef] [Green Version]

- Seth, D.; Shrivastava, R.L.; Shrivastava, S. An Empirical Investigation of Critical Success Factors and Performance Measures for Green Manufacturing in Cement Industry. J. Manuf. Technol. Manag. 2016, 27, 1076–1101. [Google Scholar] [CrossRef]

- Elkington, J. Partnerships from Cannibals with Forks: The Triple Bottom Line of 21st-Century Business. Environ. Qual. Manag. 1998, 8, 37–51. [Google Scholar] [CrossRef]

- Artiach, T.; Lee, D.; Nelson, D.; Walker, J. The Determinants of Corporate Sustainability Performance. Account. Financ. 2010, 50, 31–51. [Google Scholar] [CrossRef]

- Liern, V.; Pérez-Gladish, B. Ranking Corporate Sustainability: A Flexible Multidimensional Approach Based on Linguistic Variables. Int. Trans. Oper. Res. 2017, 25, 1081–1100. [Google Scholar] [CrossRef] [Green Version]

- Sharma, A.K. Biofertilizers for Sustainable Agriculture; Updesh Purohit for Agrobios: Jodhpur, India, 2003; pp. 41–46. [Google Scholar]

- Brockett, A.; Zabihollah, R. Corporate Sustainability; John Wiley & Sons: Hoboken, NJ, USA, 2012. [Google Scholar]

- Orlitzky, M.; Swanson, D.L. Corporate Social and Financial Performance: An Integrative Review. In Toward Integrative Corporate Citizenship; Palgrave Macmillan: London, UK, 2008; pp. 83–120. [Google Scholar]

- Aktin, T.; Gergin, Z. Mathematical Modelling of Sustainable Procurement Strategies: Three Case Studies. J. Clean. Prod. 2016, 113, 767–780. [Google Scholar] [CrossRef]

- Hallegatte, S.; Heal, G.; Fay, M.; Treguer, D. From Growth to Green Growth—A Framework; NBER: Cambridge, MA, USA, 2023. [Google Scholar]

- Pero, M.; Moretto, A.; Bottani, E.; Bigliardi, B. Environmental Collaboration for Sustainability in the Construction Industry: An Exploratory Study in Italy. Sustainability 2017, 9, 125. [Google Scholar] [CrossRef] [Green Version]

- Abdul Aziz, N.; Ong, T.; Foong, S.; Senik, R.; Attan, H. Green Initiatives Adoption and Environmental Performance of Public Listed Companies in Malaysia. Sustainability 2018, 10, 2003. [Google Scholar] [CrossRef] [Green Version]

- Tsoi, J. Stakeholders’ Perceptions and Future Scenarios to Improve Corporate Social Responsibility in Hong Kong and Mainland China. J. Bus. Ethics 2009, 91, 391–404. [Google Scholar] [CrossRef]

- Saedi, A.M.; Majid, A.A.; Isa, Z. Evaluation of Safety Climate Differences among Employees’ Demographic Variables: A Cross-Sectional Study in Two Different-Sized Manufacturing Industries in Malaysia. Int. J. Occup. Saf. Ergon. 2019, 27, 714–727. [Google Scholar] [CrossRef]

- Yang, M.X.; Li, J.; Yu, I.Y.; Zeng, K.J.; Sun, J. Environmentally Sustainable or Economically Sustainable? The Effect of Chinese Manufacturing Firms’ Corporate Sustainable Strategy on Their Green Performances. Bus. Strategy Environ. 2019, 28, 989–997. [Google Scholar] [CrossRef]

- Chiou, T.-Y.; Chan, H.K.; Lettice, F.; Chung, S.H. The Influence of Greening the Suppliers and Green Innovation on Environmental Performance and Competitive Advantage in Taiwan. Transp. Res. Part E Logist. Transp. Rev. 2011, 47, 822–836. [Google Scholar] [CrossRef]

- Schoenherr, T. The Role of Environmental Management in Sustainable Business Development: A Multi-Country Investigation. Int. J. Prod. Econ. 2012, 140, 116–128. [Google Scholar] [CrossRef]

- Molina-Azorín, J.F.; Claver-Cortés, E.; Pereira-Moliner, J.; Tarí, J.J. Environmental Practices and Firm Performance: An Empirical Analysis in the Spanish Hotel Industry. J. Clean. Prod. 2009, 17, 516–524. [Google Scholar] [CrossRef]

- Hart, S.L. A Natural-Resource-Based View of the Firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef] [Green Version]

- Sharma, S.; Aragón-Correa, J.A.; Rueda-Manzanares, A. The Contingent Influence of Organizational Capabilities on Proactive Environmental Strategy in the Service Sector: An Analysis of North American and European Ski Resorts. Can. J. Adm. Sci./Rev. Can. Des Sci. De L’administration 2007, 24, 268–283. [Google Scholar] [CrossRef]

- Ochieng, B.E. Effect of Green Purchasing Practices on Performance of Large Chemical Manufacturing Firms in Nairobi County Kenya. J. Innov. Bus. Manag. 2019, 11, 89–103. [Google Scholar]

- Halbusi, H.A.; Tehseen, S. Supply Chain Management and Practices of Firm Performance: A Review Paper. J. Hum. Dev. Educ. Spec. Res. (JHDESR) 2018, 4, 11–20. [Google Scholar]

- Sellitto, M.A.; Hermann, F.F. Influence of Green Practices on Organizational Competitiveness: A Study of the Electrical and Electronics Industry. Eng. Manag. J. 2019, 31, 98–112. [Google Scholar] [CrossRef]

- Thong, K.-C.; Wong, W.-P. Pathways for Sustainable Supply Chain Performance—Evidence from a Developing Country, Malaysia. Sustainability 2018, 10, 2781. [Google Scholar] [CrossRef] [Green Version]

- Santos, H.; Lannelongue, G.; Gonzalez-Benito, J. Integrating Green Practices into Operational Performance: Evidence from Brazilian Manufacturers. Sustainability 2019, 11, 2956. [Google Scholar] [CrossRef] [Green Version]

- Gay, L.R.; Diehl, P.L. Research Methods for Business and Management; Mc. Millan Publishing Company: New York, NY, USA, 1992. [Google Scholar]

- Krejcie, R.V.; Morgan, D.W. Determining Sample Size for Research Activities. Educ. Psychol. Meas. 1970, 30, 607–610. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Sarstedt, M.; Matthews, L.M.; Ringle, C.M. Identifying and Treating Unobserved Heterogeneity with FIMIX-PLS: Part I—Method. Eur. Bus. Rev. 2016, 28, 63–76. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Abdul-Rashid, S.H.; Sakundarini, N.; Raja Ghazilla, R.A.; Thurasamy, R. The Impact of Sustainable Manufacturing Practices on Sustainability Performance. Int. J. Oper. Prod. Manag. 2017, 37, 182–204. [Google Scholar] [CrossRef]

- Foo, B. The State of Food and Agriculture 2018: Migration, Agriculture and Rural Development; Food and Agriculture Organization of the United Nations: Rome, Italy, 2018. [Google Scholar]

- Maghsoudi, A.; Zailani, S.; Ramayah, T.; Pazirandeh, A. Coordination of Efforts in Disaster Relief Supply Chains: The Moderating Role of Resource Scarcity and Redundancy. Int. J. Logist. Res. Appl. 2018, 21, 407–430. [Google Scholar] [CrossRef]

- Luthra, S.; Mangla, S.K.; Xu, L.; Diabat, A. Using AHP to Evaluate Barriers in Adopting Sustainable Consumption and Production Initiatives in a Supply Chain. Int. J. Prod. Econ. 2016, 181, 342–349. [Google Scholar] [CrossRef]

- Brunnermeier, M.K.; Pedersen, L.H. Market Liquidity and Funding Liquidity. Rev. Financ. Stud. 2009, 22, 2201–2238. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Proposed model.

Figure 2.

Triple bottom line for corporate sustainability performance.

Figure 3.

Structural model.

Table 1.

Confirmatory factor analysis (CFA).

| Cronbach’s Alpha | rho_A | Composite Reliability | Average Variance Extracted (AVE) | |

|---|---|---|---|---|

| Economic Performance | 0.792 | 0.856 | 0.858 | 0.564 |

| Environment Performance | 0.817 | 0.823 | 0.878 | 0.644 |

| GSCM | 0.910 | 0.919 | 0.927 | 0.590 |

| Social Performance | 0.821 | 0.832 | 0.874 | 0.583 |

Table 2.

Cross-loading matrix.

| Economic Performance | Environment Performance | GSCM | Social Performance | |

|---|---|---|---|---|

| CC1 | 0.719 | 0.588 | 0.801 | 0.641 |

| CC2 | 0.738 | 0.651 | 0.849 | 0.680 |

| CC3 | 0.701 | 0.540 | 0.780 | 0.792 |

| ED1 | 0.708 | 0.490 | 0.854 | 0.686 |

| ED2 | 0.744 | 0.508 | 0.875 | 0.712 |

| ED3 | 0.720 | 0.560 | 0.821 | 0.664 |

| Econ1 | 0.719 | 0.440 | 0.595 | 0.615 |

| Econ2 | 0.853 | 0.566 | 0.764 | 0.673 |

| Econ3 | 0.362 | 0.183 | 0.217 | 0.241 |

| Econ4 | 0.826 | 0.559 | 0.725 | 0.639 |

| Econ5 | 0.872 | 0.526 | 0.783 | 0.696 |

| Envi1 | 0.508 | 0.814 | 0.574 | 0.544 |

| Envi2 | 0.507 | 0.827 | 0.548 | 0.561 |

| Envi3 | 0.433 | 0.775 | 0.431 | 0.474 |

| Envi4 | 0.573 | 0.793 | 0.597 | 0.640 |

| IEM1 | 0.526 | 0.409 | 0.637 | 0.529 |

| IEM2 | 0.515 | 0.452 | 0.596 | 0.512 |

| IEM3 | 0.593 | 0.457 | 0.640 | 0.519 |

| Soca1 | 0.678 | 0.482 | 0.701 | 0.744 |

| Soca2 | 0.690 | 0.560 | 0.760 | 0.828 |

| Soca3 | 0.558 | 0.557 | 0.565 | 0.757 |

| Soca4 | 0.503 | 0.500 | 0.533 | 0.697 |

| Soca5 | 0.569 | 0.576 | 0.592 | 0.785 |

Table 3.

Discriminant validity.

| Economic Performance | Environment Performance | GSCM | Social Performance | |

|---|---|---|---|---|

| Economic Performance | 0.751 | |||

| Environment Performance | 0.636 | 0.802 | ||

| GSCM | 0.870 | 0.678 | 0.768 | |

| Social Performance | 0.795 | 0.698 | 0.838 | 0.763 |

Table 4.

Hypothesis testing results.

| Original Sample (O) | Sample Mean (M) | Standard Deviation (STDEV) | T Statistics (|O/STDEV|) | p-Values | |

|---|---|---|---|---|---|

| GSCM -> Economic | 0.870 | 0.875 | 0.027 | 32.675 | 0.000 |

| GSCM -> Environment | 0.678 | 0.681 | 0.056 | 12.159 | 0.000 |

| GSCM -> Social | 0.838 | 0.837 | 0.031 | 27.047 | 0.000 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hejazi, M.T.; Al Batati, B.; Bahurmuz, A. The Influence of Green Supply Chain Management Practices on Corporate Sustainability Performance. Sustainability 2023, 15, 5459. https://doi.org/10.3390/su15065459

AMA Style

Hejazi MT, Al Batati B, Bahurmuz A. The Influence of Green Supply Chain Management Practices on Corporate Sustainability Performance. Sustainability. 2023; 15(6):5459. https://doi.org/10.3390/su15065459

Chicago/Turabian StyleHejazi, Mohammed Taj, Bader Al Batati, and Ahmed Bahurmuz. 2023. "The Influence of Green Supply Chain Management Practices on Corporate Sustainability Performance" Sustainability 15, no. 6: 5459. https://doi.org/10.3390/su15065459

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.