Influence of Digital Accounting System Usage on SMEs Performance: The Moderating Effect of COVID-19

,

,  ,

,  ,

,  ,

,  ,

,

Abstract

:1. Introduction

2. Literature Review

3. Theoretical Understanding and Foundation

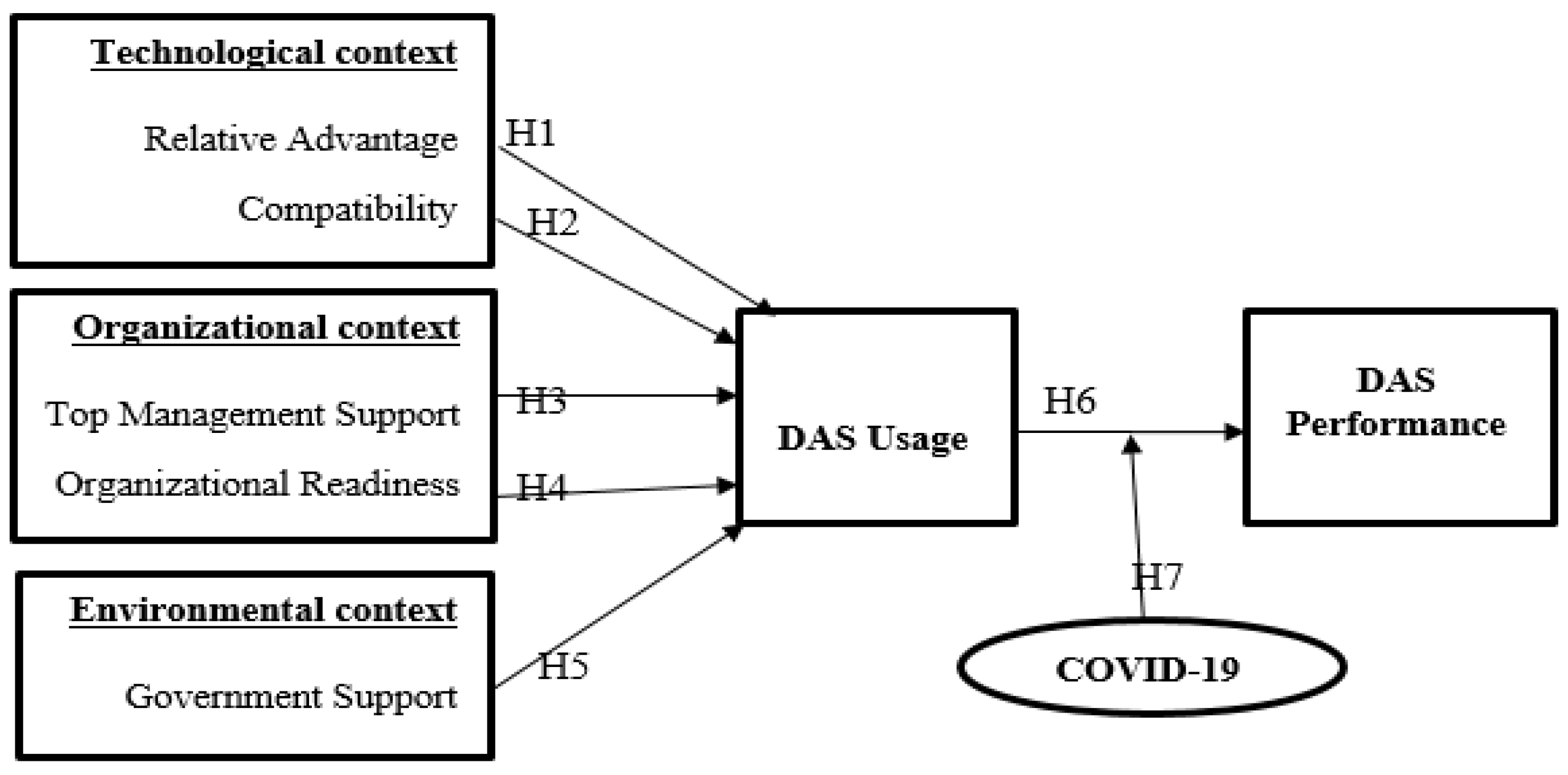

4. The Research Model and Hypotheses

4.1. Technological Factors and DAS Usage

4.2. Organizational Factors and DAS Usage

4.3. Environmental Factors and DAS Usage

4.4. DAS Usage and DAS Performance

4.5. Moderating Effect of COVID-19 on the Relationship between DAS Usage and DAS Performance

5. Methodology

6. Data Analysis

7. Results and Interpretation

7.1. Assessment of Measurement Model

7.2. Assessment of the Structural Model

7.2.1. Direct Relationship Model

7.2.2. Moderating Relationship Model

8. Discussion

9. Implications

10. Limitations and Recommendations for Future Studies

11. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

| Measurement Items | Source |

| DAS Usage Our business use DAS Our business intends to use DAS in regular bases in the future. Our business would highly recommend DAS for others to adopt. | [23] |

| Relative advantage DAS enables our business to appropriately manage supply chain risks. DAS enables our business to provide useful information to make decisions. DAS would enable our business to respond faster than competitors to changing environments. DAS would enable our business to reduce our operation cost. DAS would enable our business to reduce our operation time. | [47] |

| Top Management Support Our top management promotes the use of DAS in the business. Our top management creates support for DAS initiatives within the business. Our top management promotes DAS as a strategic priority within the business. Our top Management is interested in the news about DAS adoption. Our top Management overcome the hurdles present due to natural resistance to technology usage. | [47] |

| Organizational Readiness Lacking capital/financial resources has prevented my business from fully exploit BD. Lacking needed IT infrastructure has prevented my business from exploiting BD. Lacking analytics capability prevent the business fully exploit BD. Lacking skilled resources prevent the business fully exploit BD. | [23] |

| Government Support The governmental policies encourage our business to adopt new ITs (e.g., BDA). The government provides incentives for adopting BD. Government procurements and contracts such as offering technical support, training, and funding for BD adoption. Standards or laws support adoption of BD technologies. Adequate legal protection supports BD technology adoption. There are some business laws to deal with the security and privacy concerns over the BD technologies. | [47] |

| DAS Performance DAS is a processing system to generate information for decision managers. DAS minimize uncertainty in decision-making and improve the ability to plan and control activities. DAS supports our business growth in terms of sales, revenue and customers provide information to internal and external audiences. DAS improve user satisfaction, reduce errors, and improve information availability. DAS reduce costs reduce time, save human resources for businesses to use. DAS is a connection tool for management systems and operational systems. | [47] |

| COVID-19 COVID-19 has had an adverse impact on our organization. COVID-19 has made daily work even more challenging. COVID-19 has added to concerns about their future development. COVID-19 has inspired our organization to take the initiative to expand business. COVID-19 has caused me to work longer hours. COVID-19 has made work more demanding. | [100] |

| Compatibility Using DAS is compatible with our business culture. Using DAS is compatible with our business values. Using DAS is compatible with our preferred work practices. | [23] |

References

- Almaiah, M.A.; Ayouni, S.; Hajjej, F.; Lutfi, A.; Almomani, O.; Awad, A.B. Smart Mobile Learning Success Model for Higher Educational Institutions in the Context of the COVID-19 Pandemic. Electronics 2022, 11, 1278. [Google Scholar] [CrossRef]

- Alsmadi, A.A.; Alzoubi, M. Green Economy: Bibliometric Analysis Approach. Int. J. Energy Econ. Policy 2022, 12, 282–289. [Google Scholar] [CrossRef]

- Alsyouf, A.; Lutfi, A.; Al-Bsheish, M.; Jarrar, M.; Al-Mugheed, K.; Almaiah, M.A.; Alhazmi, F.N.; Masa’deh, R.; Anshasi, R.J.; Ashour, A. Exposure Detection Applications Acceptance: The Case of COVID-19. Int. J. Environ. Res. Public Health 2022, 19, 7307. [Google Scholar] [CrossRef] [PubMed]

- Janssen, M.; van der Voort, H.; Wahyudi, A. Factors influencing big data decision-making quality. J. Bus. Res. 2017, 70, 338–345. [Google Scholar] [CrossRef]

- Alshira’h, A.F.; Abdul-Jabbar, H.; Samsudin, R.S. Sales tax compliance model for the Jordanian small and medium enterprises research. J. Adv. Res. Soc. Behav. Sci. 2018, 10, 115–130. [Google Scholar]

- Lohapan, N. Digital accounting implementation and audit performance: An empirical research of tax auditors in Thailand. J. Asian Financ. Econ. Bus. 2021, 8, 121–131. [Google Scholar]

- AlNasrallah, W.; Saleem, F. Determinants of the Digitalization of Accounting in an Emerging Market: The Roles of Organizational Support and Job Relevance. Sustainability 2022, 14, 6483. [Google Scholar] [CrossRef]

- Hasbolah, F.; Rosli, M.H.; Hamzah, H.; Omar, S.A.; Bhuiyan, A.B. The digital accounting entrepreneurship competency for sustainable performance of the rural Micro, Small and Medium Enterprises (MSMES): An empirical review. Int. J. Small Medium Enterp. 2021, 4, 12–25. [Google Scholar]

- Cokins, G.; Oncioiu, I.; Türkeș, M.C.; Topor, D.I.; Căpuşneanu, S.; Paștiu, C.A.; Deliu, D.; Solovăstru, A.N. Intention to use accounting platforms in Romania: A quantitative study on sustainability and social influence. Sustainability 2020, 12, 6127. [Google Scholar] [CrossRef]

- Apriyanti, H.W.; Yuvitasari, E. The role of digital utilization in accounting to enhance MSMEs’ performance during COVID-19 pandemic: Case study in Semarang, Central Java, Indonesia. In Conference on Complex, Intelligent, and Software Intensive Systems; Springer: Cham, Switzerland, 2021; pp. 495–504. [Google Scholar]

- Ashraf, M.; Watto, W.A.; Alrawad, M. Do Uncertainty and Financial Development Influence the FDI Inflow of a Developing Nation? A Time Series ARDL Approach. Sustainability 2022, 14, 12609. [Google Scholar] [CrossRef]

- Bani-Khalid, T.; Alshira’h, A.F.; Alshirah, M.H. Determinants of Tax Compliance Intention among Jordanian SMEs: A Focus on the Theory of Planned Behavior. Economies 2022, 10, 30. [Google Scholar] [CrossRef]

- Alsyouf, A.; Masa’deh, R.; Albugami, M.; Al-Bsheish, M.; Lutfi, A.; Alsubahi, N. Risk of Fear and Anxiety in Utilising Health App Surveillance Due to COVID-19: Gender Differences Analysis. Risks 2021, 9, 179. [Google Scholar] [CrossRef]

- Oudat, M.S.; Alsmadi, A.A.; Alrawashdeh, N.M. Foreign direct investment and economic growth in Jordan: An empirical research using the bounds test for cointegration. Rev. Finanz. Y Politica Econ. 2019, 11, 55–63. [Google Scholar] [CrossRef]

- Son, D.D.; Marriot, N.; Marriot, P. Users’ perceptions and uses of financial reports of small and medium companies in transitional economies: Qualitative evidence from Vietnam. Qual. Res. Account. Manag. 2006, 3, 218–235. [Google Scholar] [CrossRef]

- Alshirah, M.H.; Rahman, A.A.; Mustapa, I.R. Board of directors’ characteristics and corporate risk disclosure: The moderating role of family ownership. EuroMed J. Bus. 2020, 7, 423–440. [Google Scholar] [CrossRef]

- Ali, A.; Rahman, M.; Ismail, W. Predicting continuance intention to use accounting information systems among SMEs in Terengganu, Malaysia. Int. J. Econ. Manag. 2012, 6, 295–320. [Google Scholar]

- Alghusin, N.; Alsmadi, A.A.; Alkhatib, E.; Alqtish, A.M. The impact of financial policy on economic growth in Jordan (2000–2017): An ardl approach. Ekon. Pregl. 2020, 71, 97–108. [Google Scholar] [CrossRef]

- Hameed, M.A.; Counsell, S. Establishing relationships between innovation characteristics and IT innovation adoption in organizations: A meta-Analysis Approach. Int. J. Innov. Manag. 2014, 18, 1450007. [Google Scholar] [CrossRef]

- Owoseni, A.; Twinomurinzi, H. Mobile apps usage and dynamic capabilities: A structural equation model of SMEs in Lagos, Nigeria. Telemat. Inform. 2018, 35, 2067–2081. [Google Scholar] [CrossRef]

- Wang, Y.; Shi, X. Thrive, not just survive: Enhance dynamic capabilities of SMEs through IS competence. J. Syst. Inf. Technol. 2011, 13, 200–222. [Google Scholar] [CrossRef]

- Elbashir, M.Z.; Collier, P.A.; Sutton, S.G. The role of organizational absorptive capacity in strategic use of business intelligence to support integrated management control systems. Account. Rev. 2011, 86, 155–184. [Google Scholar] [CrossRef]

- Lutfi, A.A.; Idris, K.M.; Mohamad, R. The influence of technological, organizational and environmental factors on accounting information system usage among Jordanian small and medium-sized enterprises. Int. J. Econ. Financ. Issues 2016, 6, 240–248. [Google Scholar] [CrossRef]

- Alrawashdeh, N.; Alsmadi, A.A.; Anwar, A.L. FinTech: A Bibliometric Analysis for the Period of 2014–2021. Qual. Access Success 2022, 23, 176–188. [Google Scholar]

- Almaiah, M.A.; Alfaisal, R.; Salloum, S.A.; Al-Otaibi, S.; Shishakly, R.; Shishakly, R.; Alrawad, M.; Mulhem, A.A.; Al-Maroof, R.S. Integrating Teachers’ TPACK Levels and Students’ Learning Motivation, Technology Innovativeness, and Optimism in an IoT Acceptance Model. Electronics 2022, 11, 3197. [Google Scholar] [CrossRef]

- Al-Khasawneh, A.L.; Almaiah, M.A.; Alsyouf, A.; Alrawad, M. Business Sustainability of Small and Medium Enterprises during the COVID-19 Pandemic: The Role of AIS Implementation. Sustainability 2022, 14, 5362. [Google Scholar] [CrossRef]

- Alsyouf, A. Self-efficacy and personal innovativeness influence on nurses beliefs about EHRS usage in Saudi Arabia: Conceptual model. Int. J. Manag. (IJM) 2021, 12, 1049–1058. [Google Scholar]

- Dyt, R.; Halabi, A.K. Empirical evidence examining the accounting information systems and accounting reports of small and micro business in Australia. Small Enterp. Res. 2007, 15, 1–9. [Google Scholar] [CrossRef]

- Alshir’ah, A.F.; Abdul Jabbar, H.; Samsudin, R.S. Determinants of sales tax compliance in small and medium enterprises in Jordan: A call for empirical research. World J. Manag. Behav. Stud. 2016, 4, 41–46. [Google Scholar]

- Ismail, N.A.; King, M. Factors influencing the alignment of accounting information systems in small and medium sized Malaysian manufacturing firms. J. Inf. Syst. Small Bus. 2007, 1, 1–20. [Google Scholar]

- Smirat, B.Y.A. The use of accounting information by small and medium enterprises in south district of Jordan, (An empirical study). Res. J. Financ. Account. 2013, 4, 169–175. [Google Scholar]

- Khassawneh, A.A.L. The influence of organizational factors on Accounting Information Systems (AIS) effectiveness: A study of Jordanian SMEs. Int. J. Mark. Technol. 2014, 4, 36–46. [Google Scholar]

- Ismail, N.A.; Mat Zin, R. Usage of accounting information among Malaysian Bumiputra small and medium non-manufacturing firms. J. Enterp. Resour. Plan. Stud. 2009, 2009, 101113. [Google Scholar]

- Ismail, W.; Ali, A. Conceptual model for examining the factors that influence the likelihood of Computerized Accounting Information System (CAIS) adoption among Malaysian SMEs. Int. J. Inf. Technol. Bus. Manag. 2013, 15, 122–151. [Google Scholar]

- Ahmad, M.; Ayasra, A.; Zawaideh, F. Issues and problems related to data quality in AIS implementation. Int. J. Latest Res. Sci. Technol. 2013, 2, 17–20. [Google Scholar]

- Idris, K.M.; Mohamad, R. AIS usage factors and impact among Jordanian SMEs: The moderating effect of environmental uncertainty. J. Adv. Res. Bus. Manag. Stud. 2017, 6, 24–38. [Google Scholar]

- Alsmadi, A.A.; Sha’ban, M.; Al-Ibbini, O.A. The relationship between E-banking services and bank profit in Jordan for the period of 2010–2015. Pervasive Health: Pervasive computing technologies for healthcare. In Proceedings of the 2019 5th International Conference on E-Business and Applications, Bangkok, Thailand, 25–28 February 2019; pp. 70–74. [Google Scholar]

- Bruwer, J.P.; Smit, Y. Accounting Information Systems—A value-adding phenomenon or a mere trend? The situation in Small and Medium financial service organizations in the Cape Metropolis. Expert J. Bus. Manag. 2015, 3, 38–52. [Google Scholar]

- Alamin, A.; Yeoh, W.; Warren, M.; Salzman, S. An empirical study of factors influencing accounting information systems adoption. In Proceedings of the 23rd European Conference on Information Systems, ECIS, Münster, Germany, 26–29 May 2013; Available online: http://dro.deakin.edu.au/eserv/DU:30073613/yeoh-anempiricalstudy-2015.pdf (accessed on 14 August 2022).

- Melville, N.; Kraemer, K.; Gurbaxani, V. Review: Information technology and organizational performance: An integrative model of IT business value. MIS Q. 2004, 28, 283–322. [Google Scholar] [CrossRef] [Green Version]

- Wade, M.; Hulland, J. Review: The resource-based view and information systems research: Review, extension, and suggestions for future research. MIS Q. 2004, 28, 107–142. [Google Scholar] [CrossRef]

- Sila, I. Do organizational and environmental factors moderate the effects of Internet-based Interorganizational systems on firm performance quest? Eur. J. Inf. Syst. 2010, 19, 581–600. [Google Scholar] [CrossRef]

- Thuan, P.Q.; Khuong, N.V.; Anh, N.D.C.; Hanh, N.T.X.; Thi, V.H.A.; Tram, T.N.B.; Han, C.G. The Determinants of the Usage of Accounting Information Systems toward Operational Efficiency in Industrial Revolution 4.0: Evidence from an Emerging Economy. Economies 2022, 10, 83. [Google Scholar] [CrossRef]

- Devaraj, S.; Kohli, R. Performance impacts of information technology: Is actual usage the missing link. Manag. Sci. 2003, 49, 273–289. [Google Scholar] [CrossRef] [Green Version]

- Mishra, A.N.; Konana, P.; Barua, A. Antecedents and consequences of internet use in procurement: An empirical investigation of US manufacturing firms. Inf. Syst. Res. 2007, 18, 103–120. [Google Scholar] [CrossRef]

- Henderson, D.; Sheetz, S.D.; Trinkle, B.S. The determinants of inter-organizational and internal in-house adoption of XBRL: A structural equation model. Int. J. Account. Inf. Syst. 2012, 13, 109–140. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Okaily, M.; Alsyouf, A.; Alsaad, A.; Taamneh, A. The Impact of AIS Usage on AIS Effectiveness among Jordanian SMEs: A Multi Group Analysis of the Role of Firm Size. Glob. Bus. Rev. 2020, 21, 0972150920965079. [Google Scholar] [CrossRef]

- Lutfi, A. Understanding the Intention to Adopt Cloud-based Accounting Information System in Jordanian SMEs. Int. J. Digit. Account. Res. 2022, 22, 47–70. [Google Scholar] [CrossRef]

- Lutfi, A. Factors Influencing the Continuance Intention to Use Accounting Information System in Jordanian SMEs from the Perspectives of UTAUT: Top Management Support and Self-Efficacy as Predictor Factors. Economies 2022, 10, 75. [Google Scholar] [CrossRef]

- Alsmadi, A.; Alrawashdeh, N.; Al-Dweik, A.; Al-Assaf, M. Cryptocurrencies: A bibliometric analysis. Int. J. Data Netw. Sci. 2022, 6, 619–628. [Google Scholar] [CrossRef]

- Ismail, N.A. Factors influencing AIS effectiveness among manufacturing SMEs: Evidence from Malaysia. Electron. J. Inf. Syst. Dev. Ctries. 2009, 38, 1–19. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al-Otaibi, S.; Lutfi, A.; Almomani, O.; Awajan, A.; Alsaaidah, A.; Alrawad, M.; Awad, A.B. Employing the TAM Model to Investigate the Readiness of M-Learning System Usage Using SEM Technique. Electronics 2022, 11, 1259. [Google Scholar] [CrossRef]

- Alraja, M.N.; Imran, R.; Khashab, B.M.; Shah, M. Technological innovation, sustainable green practices and SMEs sustainable performance in times of crisis (COVID-19 pandemic). Inf. Syst. Front. 2022, 1–25. [Google Scholar] [CrossRef]

- Tornatzky, L.G.; Fleischer, M. The Processes of Technological Innovation; Lexiton Books: Lexiton, MA, USA, 1990. [Google Scholar]

- Rogers, E.M. Diffusion of Innovations, 5th ed.; Free Press: New York, NY, USA, 2003. [Google Scholar]

- Zhu, K.; Kraemer, L. Post-adoption variations in usage and value of e-business by organizations: Cross-country evidence from retail industry. Inf. Syst. Res. 2005, 16, 61–84. [Google Scholar] [CrossRef] [Green Version]

- Picoto, W.N.; Bélanger, F.; Palma-dos-Reis, A. An organizational perspective on m-business: Usage factors and value determination. Eur. J. Inf. Syst. 2014, 23, 571–592. [Google Scholar] [CrossRef]

- Ramanathan, R.; Ramanathan, U.; Hsiao, H.L. The impact of e-commerce on Taiwanese SMEs: Marketing and operations effects. Int. J. Prod. Econ. 2012, 140, 934–943. [Google Scholar] [CrossRef]

- Maroufkhani, P.; Ismail WK, W.; Ghobakhloo, M. Big data analytics adoption model for small and medium enterprises. J. Sci. Technol. Policy Manag. 2020, 11, 483–513. [Google Scholar] [CrossRef]

- Zhu, K. The complementarity of information technology infrastructure and e-commerce capability: A resource-based assessment of their business value. J. Manag. Inf. Syst. 2004, 21, 167–202. [Google Scholar] [CrossRef]

- Garg, A.K.; Choeu, T. The adoption of electronic commerce by small and medium enterprises in Pretoria East. Electron. J. Inf. Syst. Dev. Ctries. 2015, 68, 1–23. [Google Scholar] [CrossRef]

- Shanmugam, J.K. The Impact of Information Technology (IT) Adoption towards Small Medium Enterprises (SMEs) Performance in Malaysia: The Role of IT Governance as Moderator. 2016. Available online: https://www.researchgate.net/publication/305865357_The_Impact_of_Information_Technology_IT_Adoption_Towards_Small_Medium_Enterprises_SMEs_Performance_In_Malaysia_The_Role_of_IT_ Goverance_as_Moderator (accessed on 3 September 2022).

- Hossain, M.B.; Wicaksono, T.; Nor, K.M.; Dunay, A.; Illes, C.B. E-commerce adoption of small and medium-sized enterprises during COVID-19 pandemic: Evidence from South Asian Countries. J. Asian Financ. Econ. Bus. 2022, 9, 291–298. [Google Scholar]

- Cruz-Jesus, F.; Pinheiro, A.; Oliveira, T. Understanding CRM adoption stages: Empirical analysis building on the TOE framework. Comput. Ind. 2019, 109, 1–13. [Google Scholar] [CrossRef]

- Al-Omoush, K.S.; Al Attar, M.K.; Saleh, I.H.; Alsmadi, A.A. The drivers of E-banking entrepreneurship: An empirical study. Int. J. Bank Mark. 2020, 38, 485–500. [Google Scholar] [CrossRef]

- Căpușneanu, S.; Mateș, D.; Tűrkeș, M.C.; Barbu, C.M.; Staraș, A.I.; Topor, D.I.; Stoenică, L.; Fűlöp, M.T. The impact of force factors on the benefits of digital transformation in Romania. Appl. Sci. 2021, 11, 2365. [Google Scholar] [CrossRef]

- Mcmahon, R.G.P. Growth and performance of manufacturing SMEs: The influence of financial management characteristics. Int. Small Bus. J. 2001, 19, 10–28. [Google Scholar] [CrossRef]

- Rahayu, R.; Day, J. Determinant factors of E-commerce adoption by SMEs in developing country: Evidence from Indonesia. Procedia-Soc. Behav. Sci. 2015, 195, 142–150. [Google Scholar] [CrossRef] [Green Version]

- Al-Alawi, A.I.; Al-Ali, F.M. Factors affecting E-commerce adoption in SMEs in GCC: An empirical study of Kuwait. Res. J. Inf. Technol. 2015, 7, 1–21. [Google Scholar] [CrossRef]

- Kim, S.; Baek, T.H. Examining the antecedents and consequences of mobile app engagement. Telemat. Inform. 2018, 35, 148–158. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Hajjej, F.; Al-Khasawneh, A.; Shehab, R.; Al-Otaibi, S.; Alrawad, M. Explaining the Factors Affecting Students’ Attitudes to Using Online Learning (Madrasati Platform) during COVID-19. Electronics 2022, 11, 973. [Google Scholar] [CrossRef]

- Meri, A.; Hasan, M.; Danaee, M.; Jaber, M.; Jarrar, M.; Safei, N.; Dauwed, M.; Abd, S.K.; Al-Bsheish, M. Modelling the utilization of cloud health information systems in the Iraqi public healthcare sector. Telemat. Inform. 2019, 36, 132–146. [Google Scholar] [CrossRef]

- Thong, J.Y.; Yap, C.S.; Raman, K.S. Top management support, external expertise and information systems implementation in small businesses. Inf. Syst. Res. 1996, 7, 248–267. [Google Scholar] [CrossRef]

- Mehrtens, J.; Cragg, P.B.; Mills, A.M. A model of Internet adoption by SMEs. Inf. Manag. 2001, 39, 165–176. [Google Scholar] [CrossRef]

- Chwelos, P.; Benbasat, I.; Dexter, A.S. Research report: Empirical test of an EDI adoption model. Inf. Syst. Res. 2001, 12, 304–321. [Google Scholar] [CrossRef] [Green Version]

- Al-Khasawneh, A.L.; Barakat, H.J. The role of the Hashemite leadership in the development of human resources in Jordan: An analytical study. Int. Rev. Manag. Mark. 2016, 6, 654–667. [Google Scholar]

- Alsyouf, A.; Ishak, A.K.; Alhazmi, F.N.; Al-Okaily, M. The Role of Personality and Top Management Support in Continuance Intention to Use Electronic Health Record Systems among Nurses. Int. J. Environ. Res. Public Health 2022, 19, 11125. [Google Scholar] [CrossRef]

- Al-Khasawneh, A.L.; Al-Zoubi, M.R.; Alnajjar, F.J. Quality between the contemporary management & Islamic thought perspectives: Comparative study. J. Emerg. Trends Econ. Manag. Sci. 2013, 4, 281–290. [Google Scholar]

- Lutfi, A. Investigating the moderating effect of Environment Uncertainty on the relationship between institutional factors and ERP adoption among Jordanian SMEs. J. Open Innov. Technol. Mark. Complex. 2022, 6, 91. [Google Scholar] [CrossRef]

- Alrawad, M.; Alyatama, S.; Elshaer, I.A.; Almaiah, M.A. Perception of Occupational and Environmental Risks and Hazards among Mineworkers: A Psychometric Paradigm Approach. Int. J. Environ. Res. Public Health 2022, 19, 3371. [Google Scholar] [CrossRef]

- Verkijika, S.F. Factors influencing the adoption of mobile commerce applications in Cameroon. Telemat. Inform. 2018, 35, 1665–1674. [Google Scholar] [CrossRef]

- Lutfi, A. Understanding Cloud Based Enterprise Resource Planning Adoption among SMEs in Jordan. J. Theor. Appl. Inf. Technol. 2021, 99, 5944–5953. [Google Scholar]

- Esmeray, A. The Impact of Accounting Information Systems (AIS) on Firm Performance: Empirical Evidence in Turkish Small and Medium Sized Enterprises. Int. Rev. Manag. Mark. 2016, 6, 233–236. [Google Scholar]

- DeLone, W.H.; McLean, E.R. Information systems success: The quest for the dependent variable. Inf. Syst. Res. 1992, 3, 60–95. [Google Scholar] [CrossRef] [Green Version]

- De Guinea, A.O.; Kelley, H.; Hunter, M.G. Information systems effectiveness in small businesses: Extending a Singaporean model in Canada. J. Glob. Inf. Manag. 2005, 13, 55–79. [Google Scholar] [CrossRef] [Green Version]

- Tan, L.F.; Seetharaman, S. Preventing the spread of COVID-19 to nursing homes: Experience from a Singapore geriatric centre. J. Am. Geriatr. Soc. 2020, 68, 942. [Google Scholar] [CrossRef]

- Kraus, S.; Clauss, T.; Breier, M.; Gast, J.; Zardini, A.; Tiberius, V. The economics of COVID-19: Initial empirical evidence on how family firms in five European countries cope with the corona crisis. Int. J. Entrep. Behav. Res. 2020, 26, 1067–1092. [Google Scholar] [CrossRef]

- Montani, F.; Staglianò, R. Innovation in times of pandemic: The moderating effect of knowledge sharing on the relationship between COVID-19-induced job stress and employee innovation. RD Manag. 2022, 52, 193–205. [Google Scholar] [CrossRef]

- Miroshnychenko, I.; Strobl, A.; Matzler, K.; de Massis, A. Absorptive capacity, strategic flexibility, and business model innovation: Empirical evidence from Italian SMEs. J. Bus. Res. 2021, 130, 670–682. [Google Scholar] [CrossRef]

- McKinsey, G.L.; Lizama, C.O.; Keown-Lang, A.E.; Niu, A.; Santander, N.; Larpthaveesarp, A.; Chee, E.; Gonzalez, F.F.; Arnold, T.D. A new genetic strategy for targeting microglia in development and disease. eLife 2020, 9, e54590. [Google Scholar] [CrossRef] [PubMed]

- Lodge, M.; Boin, A. Great easing? Leaders face a tragic dilemma but they should not hide behind the backs of experts. LSE COVID-19 Blog, 14 May 2020; 1–3. [Google Scholar]

- Amman Chamber of Industry. 2014. Available online: http://www.aci.org.jo/development/en/ (accessed on 1 March 2022).

- Alshira’h, A.; Alsqour, M.; Alsyouf, A.; Alshirah, M. A Socio-Economic Model of Sales Tax Compliance. Economies 2020, 8, 88. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, J.G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); SAGE Publications: Newbury Park, CA, USA, 2014. [Google Scholar]

- Almaiah, M.A.; Hajjej, F.; Shishakly, R.; Amin, A.; Awad, A.B. The Role of Quality Measurements in Enhancing the Usability of Mobile Learning Applications during COVID-19. Electronics 2022, 11, 1951. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sinkovics, R.R. The use of partial least squares path modeling in international marketing. In New Challenges to International Marketing; Emerald Group Publishing Limited: Bingley, UK, 2009; pp. 277–319. [Google Scholar]

- Saad, M.; Almaiah, M.A.; Alsaad, A.; Al-Khasawneh, A.; Alrawad, M.; Alsyouf, A.; Al-Khasawneh, A.L. Actual Use of Mobile Learning Technologies during Social Distancing Circumstances: Case Study of King Faisal University Students. Sustainability 2022, 14, 7323. [Google Scholar] [CrossRef]

- Henseler, J.; Fassott, G. Testing moderating affects in PLS path models: An illustration of available procedures. In Handbook of Partial Least Squares; Springer: Berlin/Heidelberg, Germany, 2010; pp. 713–735. [Google Scholar]

- Alkhater, N.; Walters, R.; Wills, G. An empirical study of factors influencing cloud adoption among private sector organisations. Telemat. Inform. 2018, 35, 38–54. [Google Scholar] [CrossRef]

- Song, J.; Xia, S.; Vrontis, D.; Sukumar, A.; Liao, B.; Li, Q.; Tian, K.; Yao, N. The Source of SMEs’ Competitive Performance in COVID-19: Matching Big Data Analytics Capability to Business Models. Inf. Syst. Front. 2022, 1–21. [Google Scholar] [CrossRef]

- Lan, N.T.N.; Yen, L.L.; Ha, N.T.T.; Van, P.T.N.; Huy, D.T.N. Enhancing Roles Of Management Accounting And Issues Of Applying Ifrs For Sustainable Business Growth: A Case Study. J. Secur. Sustain. Issues 2020, 10, 709–720. [Google Scholar]

- Phuong, N.T.T.; Huy, D.T.N.; van Tuan, P. The evaluation of impacts of a seven factor model on nvb stock price in commercial banking industry in vietnam-and roles of Discolosure of Accounting Policy In Risk Management. Int. J. Entrep. 2020, 24, 1–13. [Google Scholar]

- Almaiah, M.A.; Al Mulhem, A. Thematic analysis for classifying the main challenges and factors influencing the successful implementation of e-learning system using NVivo. Int. J. Adv. Trends Comput. Sci. Eng. 2020, 9, 142–152. [Google Scholar] [CrossRef]

{kind=link}

| Innovations | Innovations Impacts | Author (s) |

|---|---|---|

| ERP Adoption | ERP performance | [27] |

| Mobile Business Use | M-Business Value | [57] |

| E-commerce Usage | E-commerce impact | [58] |

| AIS Implementation | Business Sustainability | [26] |

| E-commerce usage | Business performance | [43] |

| Big Data (BD) Adoption | BD Impact | [59] |

| Internet usage | Procurement- process performance | [45] |

| E-Business (EB) Usage | EB value | [56] |

| AIS Usage | AIS Effectiveness | [47] |

| Characteristic | Frequency | Percent | |

|---|---|---|---|

| Position | CEOs | 88 | 48.1% |

| Senior managers | 49 | 26.8% | |

| Managers | 47 | 25.1% | |

| Experience | 3 years or less | 48 | 26.2% |

| 4–7 years | 42 | 22.9% | |

| 8–11 years | 49 | 26.8% | |

| More than 11 | 44 | 24.1% | |

| Gender | Male | 105 | 57.4% |

| Female | 78 | 42.6% | |

| Age | 20–29 years | 39 | 21.3% |

| 30–39 years | 46 | 25.1% | |

| 40–49 years | 66 | 36.1% | |

| 50 years and above | 32 | 17.5% | |

| Education | Diploma or below | 29 | 15.8% |

| Bachelor degree | 81 | 44.3% | |

| Master’s degree | 59 | 32.2% | |

| PhD | 14 | 7.6% | |

| Number of Years Using DAS | 2 years or less | 72 | 39.3% |

| 3–5 years | 62 | 33.9% | |

| 6–8 years | 33 | 18.1% | |

| More than 8 years | 16 | 8.7% |

| Latent Construct | Item | Item Loading | Cronbach’s Alpha | Composite Reliability | AVE |

|---|---|---|---|---|---|

| >0.4 | >0.7 | >0.7 | >0.5 | ||

| DAS Performance (DASP) | DASP1 | 0.873 | 0.837 | 0.879 | 0.553 |

| DASP2 | 0.799 | ||||

| DASP3 | 0.734 | ||||

| DASP4 | 0.751 | ||||

| DASP5 | 0.692 | ||||

| DASP6 | 0.567 | ||||

| DAS Use (DASU) | DASU1 | 0.647 | 0.719 | 0.826 | 0.545 |

| DASU2 | 0.772 | ||||

| DASU3 | 0.698 | ||||

| DASU4 | 0.822 | ||||

| Relative Advantage (RA) | RA1 | 0.503 | 0.836 | 0.874 | 0.541 |

| RA2 | 0.707 | ||||

| RA3 | 0.803 | ||||

| RA4 | 0.796 | ||||

| RA5 | 0.816 | ||||

| RA6 | 0.741 | ||||

| Compatibility (CO) | CO1 | 0.756 | 0.717 | 0.835 | 0.631 |

| CO2 | 0.901 | ||||

| CO3 | 0.713 | ||||

| Top Management Support (TMS) | TMS 1 | 0.830 | 0.853 | 0.894 | 0.627 |

| TMS 2 | 0.844 | ||||

| TMS 3 | 0.842 | ||||

| TMS 4 | 0.725 | ||||

| TMS 5 | 0.709 | ||||

| Organizational Readiness (OR) | OR1 | 0.653 | 0.849 | 0.893 | 0.628 |

| OR2 | 0.836 | ||||

| OR3 | 0.877 | ||||

| OR4 | 0.853 | ||||

| OR5 | 0.720 | ||||

| COVID-19 (COV) | COV1 | 0.455 | 0.767 | 0.845 | 0.538 |

| COV2 | 0.511 | ||||

| COV4 | 0.801 | ||||

| COV5 | 0.888 | ||||

| COV6 | 0.889 | ||||

| Government Support (GS) | GS1 | 0.719 | 0.810 | 0.866 | 0.523 |

| GS2 | 0.605 | ||||

| GS3 | 0.838 | ||||

| GS4 | 0.825 | ||||

| GS5 | 0.734 | ||||

| GS6 | 0.576 |

| DAS P | DAS U | Co | COV | RA | GS | TMS | OR | |

|---|---|---|---|---|---|---|---|---|

| DAS P | 0.743 | |||||||

| DAS U | 0.383 | 0.738 | ||||||

| Co | 0.451 | 0.347 | 0.794 | |||||

| COV | 0.288 | 0.386 | 0.317 | 0.733 | ||||

| R A | 0.261 | 0.371 | 0.211 | 0.305 | 0.828 | |||

| G S | 0.146 | 0.160 | 0.196 | 0.025 | 0.128 | 0.723 | ||

| TMS | 0.372 | 0.306 | 0.247 | 0.659 | 0.280 | 0.088 | 0.832 | |

| O R | 0.086 | 0.277 | 0.165 | 0.425 | 0.603 | 0.061 | 0.293 | 0.793 |

| Hypothesis No. | Relationship | Path Coefficient | T-Value | p-Value | Decision |

|---|---|---|---|---|---|

| H1 | RA → DAS U | 0.009 | 0.110 | 0.457 | Not Supported |

| H2 | CO → DAS U | 0.194 | 2.588 | 0.013 ** | Supported |

| H3 | TMS → DAS U | 0.095 | 1.450 | 0.088 * | Supported |

| H4 | OR → DAS U | 0.127 | 1.816 | 0.049 ** | Supported |

| H5 | GS → DAS U | 0.089 | 1.394 | 0.096 * | Supported |

| H6 | DAS U → DAS P | 0.383 | 6.977 | 0.000 *** | Supported |

| Hypothesis No. | Relationship | Path Coefficient | T-Value | p-Value | Decision |

|---|---|---|---|---|---|

| H9 | DASU * COVID-19 → DASP | 0.202 | 2.132 | 0.028 ** | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lutfi, A.; Alkelani, S.N.; Al-Khasawneh, M.A.; Alshira’h, A.F.; Alshirah, M.H.; Almaiah, M.A.; Alrawad, M.; Alsyouf, A.; Saad, M.; Ibrahim, N. Influence of Digital Accounting System Usage on SMEs Performance: The Moderating Effect of COVID-19. Sustainability 2022, 14, 15048. https://doi.org/10.3390/su142215048

Lutfi A, Alkelani SN, Al-Khasawneh MA, Alshira’h AF, Alshirah MH, Almaiah MA, Alrawad M, Alsyouf A, Saad M, Ibrahim N. Influence of Digital Accounting System Usage on SMEs Performance: The Moderating Effect of COVID-19. Sustainability. 2022; 14(22):15048. https://doi.org/10.3390/su142215048

Chicago/Turabian StyleLutfi, Abdalwali, Saleh Nafeth Alkelani, Malak Akif Al-Khasawneh, Ahmad Farhan Alshira’h, Malek Hamed Alshirah, Mohammed Amin Almaiah, Mahmaod Alrawad, Adi Alsyouf, Mohamed Saad, and Nahla Ibrahim. 2022. "Influence of Digital Accounting System Usage on SMEs Performance: The Moderating Effect of COVID-19" Sustainability 14, no. 22: 15048. https://doi.org/10.3390/su142215048