1. Introduction

Indonesia is the largest economy in South East Asia [

1], and it is considered an emerging economy. However, Indonesian financial institutions and equity markets are distinctive from other emerging stock markets and financial institutions. Indonesia registered 7.9 percent growth from 2008 to 2017; such growth is higher than many major emerging economies, including those of Brazil, Russia, India, China, South Africa, Singapore, and Malaysia. In addition, Islamic features differentiate the Indonesian equity market from stock markets in other emerging countries [

2]. Moreover, the integration of the Indonesian equity market with global equity markets has increased over time. The country allowed foreign investors to buy 49 percent of new and listed shares, except bank shares, as of September 1989 [

3]. In an effort to liberalize its equity market, in July 1992, the Indonesian government ceased its control of the Jakarta Stock Exchange (JSX) and vested it as a private limited company regulated by member companies [

4]. As a result, foreign institutions’ share of total market capitalization reached 41 percent in 2007. Furthermore, Indonesia’s sustainable economic growth in the post-East Asian crisis period has further been driven by its exports [

5]. However, liberalization of trade and financial integration with the rest of the world has increased Indonesia’s vulnerability to external shocks, particularly shocks hitting the world’s large economies. This is apparent from the recent global financial crisis that hit the U.S. economy in 2008–2009,which caused a 30 percent depreciation of Indonesian currency, IDR, against the USD and a 51.1 percent decrease in the country’s stock market prices in 2008 [

6]. Hence, it is appropriate to identify linkages between the uncertainty of economic policy in the developed markets and the return of the Indonesian stock market.

A nonzero probability of changes in existing economic policies that determine the rules of the game for economic agents is called economic policy uncertainty [

7]. It is countercyclical and affects almost the entire economy. A recent surge in research interest in the effects of policy uncertainty has been due to the global financial crisis, quantification of uncertainty, and rise in computing power [

8]. It has primarily focused on the effects of uncertainty on a large set of macroeconomic variables, such as inflation and unemployment [

9], firm-level investment [

10,

11], demand for durable goods [

12] and output growth [

13,

14]. The effect of uncertainty on investment is more severe for firms with larger irreversible investments and government spending dependency [

15]. Economic policy uncertainty with firm-level uncertainty leads to economic contraction [

9,

14,

16].

Stock markets play a key role in the economic growth of a country by improving liquidity, mobilizing capital, exercising corporate control, risk pooling, and sharing services including investment levels. Stock market development augments economic growth by attracting more investment [

17]. Increased financial globalization has led to greater integration of equity markets around the world [

18]. This is apparent from a large number of studies that examine comovements among stock markets. Ref. [

19] attributes fluctuation in most of the stock market in the sample countries to a common global factor and equates it with international stock market comovements. Ref. [

20] examines the correlation among thirty-two emerging equity markets from four regions and find its significant presence within regions, across regions, and comovements with the rest of the world’s equity markets. Ref. [

21] identifies a volatility spillover across the stock markets of London, New York, and Tokyo. The U.S. is the largest equity market in the world. Due to its size, a large number of studies have focused on the U.S. equity market spillover effect. Ref. [

22] examines day-to-day linkages between the U.S. and four Asian equity market prices and finds a significant tendency among the Asian markets to follow U.S. equity market prices. Ref. [

23] shows a significant interaction between U.S. stock market uncertainty and emerging market returns. Ref. [

24] indicates that the U.S. equity market has a significant effect on the equity market returns of France, Germany, and the United Kingdom. According to [

25], the U.S. equity market skewness negatively predicts international equity market returns. Ref. [

26] identifies significant mean return and volatility spillover effects from U.S. equity markets on the stock markets of Brazil, Russia, India, China, and South Africa. Ref. [

27] indicates risk spillover between G7 and U.S. equity markets.

Ref. [

28] identifies uncertainty as a new channel for financial market contagion and stock market volatility. Government policies set the environment in which private businesses have to operate. Both real and financial markets react negatively to government-policy-related uncertainty [

7,

29]. An increase in uncertainty hampers long-run growth prospectus and equity prices [

30]. The U.S. constitutes 23.89 percent of the global economy [

31] and more than 40 percent of the world equity market. Hence, shocks hitting the U.S not only affect the U.S. economy but also spread to other countries. Ref. [

32] argues that trade-related fluctuations in the world’s largest economy (U.S.) influence financial markets around the world. Ref. [

33] identifies a negative effect of the tightening of monetary policy in the U.S. on 50 equity markets around the globe. The recent most global financial crisis that hit the U.S. financial markets also spread to other equity markets around the globe. It resulted in 27, 51, and 55 percent falls in the U.S., Europe, and Japan stock market prices, respectively. The fall in emerging market equity prices was quite large and stood at 60 percent [

34].

This paper makes at least three contributions to the empirical literature on economic policy uncertainty and stock market returns. First, there are many studies in the literature examining the interaction between economic policy uncertainty and emerging economies’ equity markets, including those of Brazil, China, India, South Korea, Malaysia, Mexico, Philippines, Russia, South Africa, Taiwan, and Thailand; see, for example, [

35,

36,

37,

38,

39,

40,

41,

42,

43,

44]. However, as far as we know, there is no previous study examining the interaction between economic policy uncertainty and the equity market for Indonesia. Thus, the first contribution of our paper is that we bridge the gap in the literature regarding the examination of the interaction between economic policy uncertainty and the equity market in Indonesia. The second contribution of our paper to the empirical literature on economic policy uncertainty and stock market returns is that our paper is the first paper employing both rolling window correlation [

45] and the dynamic conditional correlation method [

46] to examine the interaction between the Indonesian equity market and the uncertainty of economic policy in the developed markets.

Another contribution of our paper is that we observe the factors that determine the dynamic interaction between the uncertainty of economic policy in the developed markets and the return of the Indonesian stock market. Ref. [

47] identifies increased comovements in the international equity market during the recession. According to [

48], uncertainty effects are intensified during the recession in the U.S. economy. Ref. [

39] finds a negative effect of policy uncertainty on G7 stock markets in the bearish regime and a significant negative role in the bearish and bullish market of BRIC. Ref. [

38] find a negative effect of uncertainty on stock market returns during bearish regimes for both developed and emerging economies but in higher magnitude for the latter countries. Using quantile regression, ref. [

49] finds an increase in the out-of-sample predictability of economic policy uncertainty when stock market performance is poor to moderate. According to [

50], the link between policy uncertainty and equity returns increases during poor economic conditions. This means that bad economic conditions could increase the vulnerability of the stock market returns to uncertainty shock. In this paper, we expand on the above work to determine the factors that explain the time-varying-based dynamic conditional correlation between the uncertainty of economic policy in the developed markets and the return of the Indonesian stock market. Our study is based on two hypotheses: the first hypotheses

) assumes that the correlation between policy uncertainty in the global economy and return of the Indonesian market is constant; the second hypothesis

tests whether oil price shocks, macroeconomic variables, and recessionary indicators affect the dynamic conditional correlations between global economic policy uncertainty and Indonesian stock market return.

The remainder of the paper is organized as follows: A literature review is given in

Section 2 followed by a discussion on data and methodology in

Section 3. This includes data discussion in

Section 3.1 followed by a discussion on rolling window correlation, dynamic conditional correlation, and autoregressive distributed lag model in

Section 3.2.1,

Section 3.2.2 and

Section 3.2.3, respectively. The empirical analysis is provided in

Section 4, and it includes descriptive statistics, rolling window correlation, and dynamic conditional correlation; the results of the autoregressive distributed lag model are presented in

Section 4.1,

Section 4.2,

Section 4.3 and

Section 4.4. The conclusion is given in

Section 5.

2. Literature Review

There is a vast body of literature linking economic policy uncertainty and stock returns. Refs. [

51,

52,

53], and others examine the detrimental economic effects of monetary, fiscal, and regulatory policy uncertainty. However, the bulk of the literature is largely built on four channels through which policy uncertainty affects asset prices. First, firms and other economic agents may alter their consumption and savings decisions due to uncertainty. As a result, consumers increase their precautionary savings, which potentially reduces consumption expenditure [

30]. On the other hand, a high level of uncertainty impels firms to freeze prospective investment projects and hiring [

10]. Second, the uncertainty effect of demand and supply might lead to a rise in production cost and financing [

54]. Policy uncertainty not only reduces levels of investment, hiring, and consumption but also hampers economic growth, particularly in smaller but open economies. Third, to counter the negative effect of policy uncertainty, governments could adopt a protectionist policy that may further increase risk in financial markets [

29]. Lastly, due to policy uncertainty, a decrease in future cash flows or an increase in the risk-adjusted discount rate or both may affect stock prices [

55].

Several studies have been conducted on policy uncertainty, although among all, two approaches are noteworthy. The first approach is event based with respect to the date of policy implementation. Despite being well documented, an event-based approach may be artificially precise [

56]. The second approach uses government elections as a proxy for policy uncertainty [

57,

58]. The study conducted by [

59] revealed that the equity market remains volatile a month before the presidential elections. Ref. [

60] also came up with a similar conclusion that political uncertainty leads to greater market volatility but after, not before, major unexpected political outcomes such as Brexit. As is well known, when the economy is doing well, politicians stick with their old policies, but when the economy is not stirring in the right directions, politicians are tempted to experiment, consequently spurring further uncertainty [

29].

Ref. [

61] finds a negative correlation between U.S. economic policy uncertainty and returns of all high-yielding currencies, except JPY. Ref. [

7] identifies the key role of uncertainty in terms structure dynamics, which, in turn, has a major effect on countercyclical volatility of asset returns.

The effect of the economic policy uncertainty index constructed by [

7] on economic activities is much prevalent among the work of researchers [

8,

14]. Since its development, many studies follow similar techniques for evaluating the effects of policy uncertainty on different macroeconomic indicators, stock market returns, and stock market volatility.

In recent years, numerous studies have further been added to the subject, although the work of [

28,

39,

40,

41,

43,

44,

49,

56,

62,

63,

64,

65,

66,

67,

68,

69,

70,

71,

72,

73,

74,

75,

76,

77] is prominent. All of these studies relate their own country’s policy uncertainty to their own country’s stock market returns, with the exception of a few. In this regard, refs. [

28,

40,

43,

44,

64,

69,

70,

72,

76,

77] are some of the exceptions. Ref. [

43] examines the effect of U.S. economic policy uncertainty on G7 and IBSA (India, Brazil, and South Africa) countries’ stock markets. Ref. [

64] relates their own country’s economic policy uncertainty and global uncertainty (policy uncertainty in China, the European area, Japan, and the USA) to the stock market returns of Hong Kong, Malaysia, and South Korea. Results based on causality in quantile regression provide strong evidence of relevancy of one’s own country’s economic policy uncertainty and global uncertainty for Malaysian stock market returns and South Korean stock market returns and their volatility. Hong Kong stock returns appear unaffected by both kinds of uncertainties. Ref. [

39] also employs the quantile regression techniques to examine the dependence structure between economic policy uncertainty and stock market returns with respect to G7 and BRIC countries. Ref. [

44] examines their own country’s policy uncertainty and the effects of U.S. economic policy uncertainty on the stock market returns of Pacific-Rim countries (Australia, Canada, China, Japan, Korea, and the U.S.). Pooled vector autoregression results suggest a negative effect of policy uncertainty on the returns of all stock markets. However, the U.S. policy uncertainty appears an insignificant determinant of Australian stock market returns. Ref. [

40] examines volatility spillovers between U.S. economic policy uncertainty and BRIC (Brazil, Russia, India, and China) equity markets. Ref. [

70] focuses on the effect of U.S. economic policy uncertainty on China’s A/B stock markets and the U.S. stock market returns co-movement. Ref. [

69] also examines the spillover effect of U.S. economic policy uncertainty on global financial markets with respect to nineteen economies. Factor augmented vector autoregression results showed a negative spillover effect of U.S. economic policy uncertainty on all countries except the Chinese equity market. Ref. [

72] examines the importance of European and U.S. economic policy uncertainty in predicting European stock market returns represented by the stock markets of the UK, Germany, and France. The results indicate the failure of their own country’s economic policy uncertainty in improving forecast accuracy of these markets. On the other hand, U.S. economic policy uncertainty offers valuable information that enhanced the predictability of these stock market returns. Ref. [

28] investigates the effect of U.S. economic policy uncertainty, financial uncertainty, and news-implied uncertainty on the stock market volatility of six industrialized and three emerging economies. Economic policy uncertainty and news-implied uncertainty have both positive and negative effects on the returns of stock markets. Ref. [

76] identifies a negative effect of U.S. economic policy uncertainty on BRIC countries’ stock market returns, except for those of China. Ref. [

77] shows that the U.S. instead of China’s economic policy uncertainty has a key role in shaping global financial markets.

In a recent publication, ref. [

78] examines the impact of changes in economic policy uncertainty on the Japanese stock return. The results indicate that a rise in volatility creates a negative effect on stock prices, reaffirming the risk premium hypothesis. It is further stated that the degree of asymmetry of uncertainty on stock returns is significant for the Japanese market as compared with the U.S. influence. Ref. [

79] also identifies a significant volatility spillover effect from the U.S. equity market to stock markets in the southeast Asian countries.

The aforementioned studies conclude a mixture of positive and negative effects of policy uncertainty on stock returns. We further extend the discussion and attempt to pinpoint those factors that determine the dynamic linkages between the uncertainty of economic policy in the developed markets and the return of the Indonesian stock market.

5. Conclusions

Trade liberalization and financial integration in the emerging markets are at the heart of policy making and research. As is well known, a rise in international trade and financial integration could increase risk in policy uncertainty. Shocks originating from the world-leading economies are inclined to affect emerging markets. As a result, the global stock market tumbles, and the global economy is exposed to vulnerability. To understand this phenomenon, several studies have examined the relationships between trade and financial integration of emerging markets. As an illustration, ref. [

88] examined the stock market volatility of financial markets in emerging and developed countries. Likewise, ref. [

89] conducted a study on the level of stock market integration for twenty-five emerging economies.

There is no dearth of literature on policy uncertainty and stock returns. However, to date no particular study has examined the relationship between trade and financial integration for the Indonesian stock market. Thus, to bridge the gap, our study provides new evidence on the relationship between economic policy uncertainty and the stock market return of Indonesia.

In this paper, we focused on the dynamic interaction between the uncertainty of economic policy in developed markets and the return of the Indonesian stock market. The objective was to identify the nature of the correlation between the uncertainty of economic policy in the developed markets and the return of the Indonesian stock market and the factors that explain this correlation.

Our study offers a sound framework that covers both risk and uncertainty to test the effect of uncertainty of economic policy with reference to the Indonesian economy. From the perspective of investors, it is significant to comprehend the direction and nature of the correlation between the uncertainty of economic policy in the developed markets and the return of the Indonesian stock market.

In order to examine the effect of global economic policy on the return of the Indonesian stock market, we first tested whether or not the correlation between the policy uncertainty in the global economy and the return of the Indonesian stock market is constant. Afterward, we determined to what degree oil price shocks, macroeconomic variables, and recessionary indicators affect the conditional correlation between the variables. Furthermore, we examined whether our recessionary indicators, inflation, global crude oil prices, gross domestic product, and world crude oil production, are appropriate in explaining the dynamic conditional correlation between policy uncertainty in the global economy and the return of the Indonesian stock market.

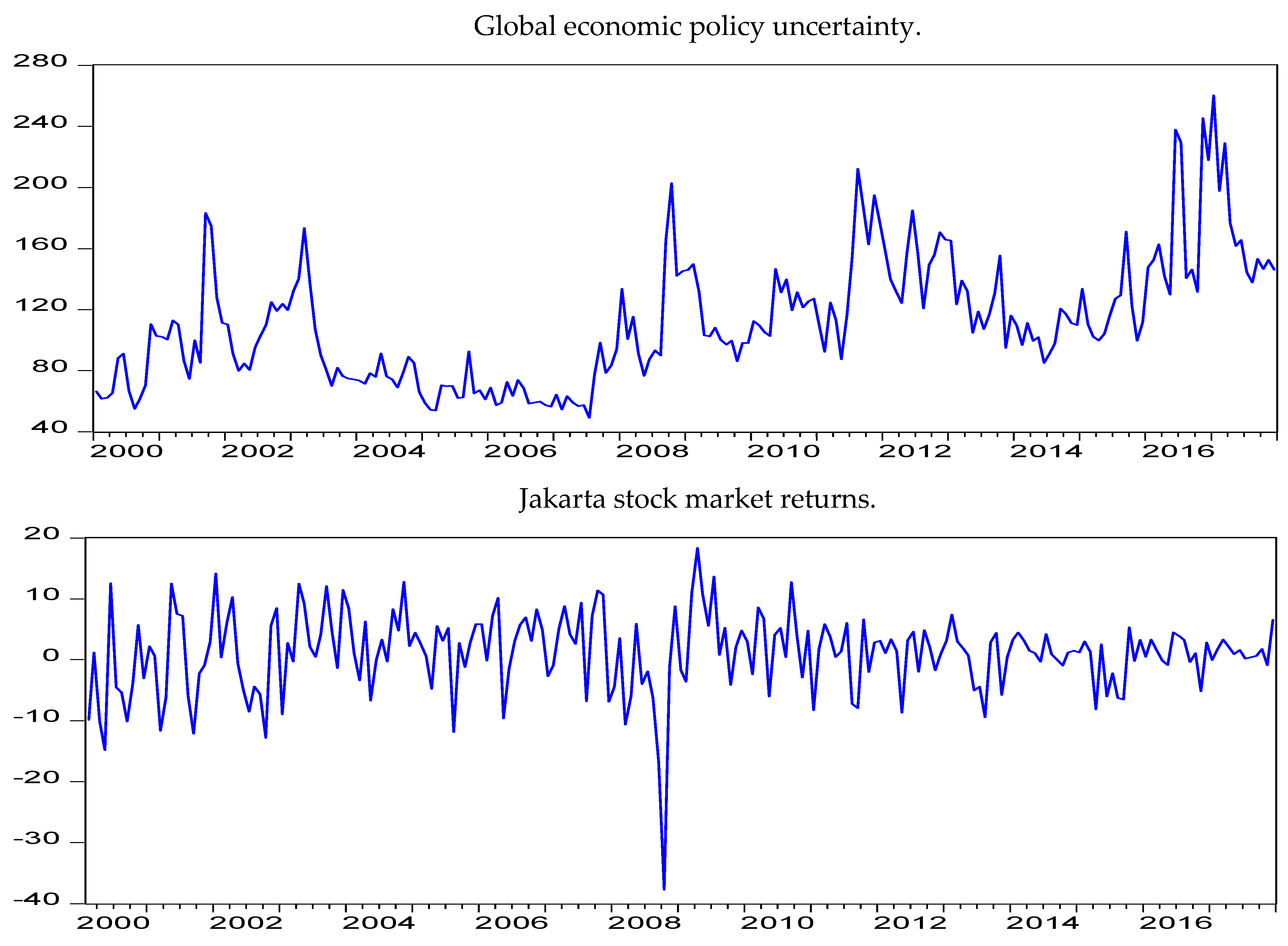

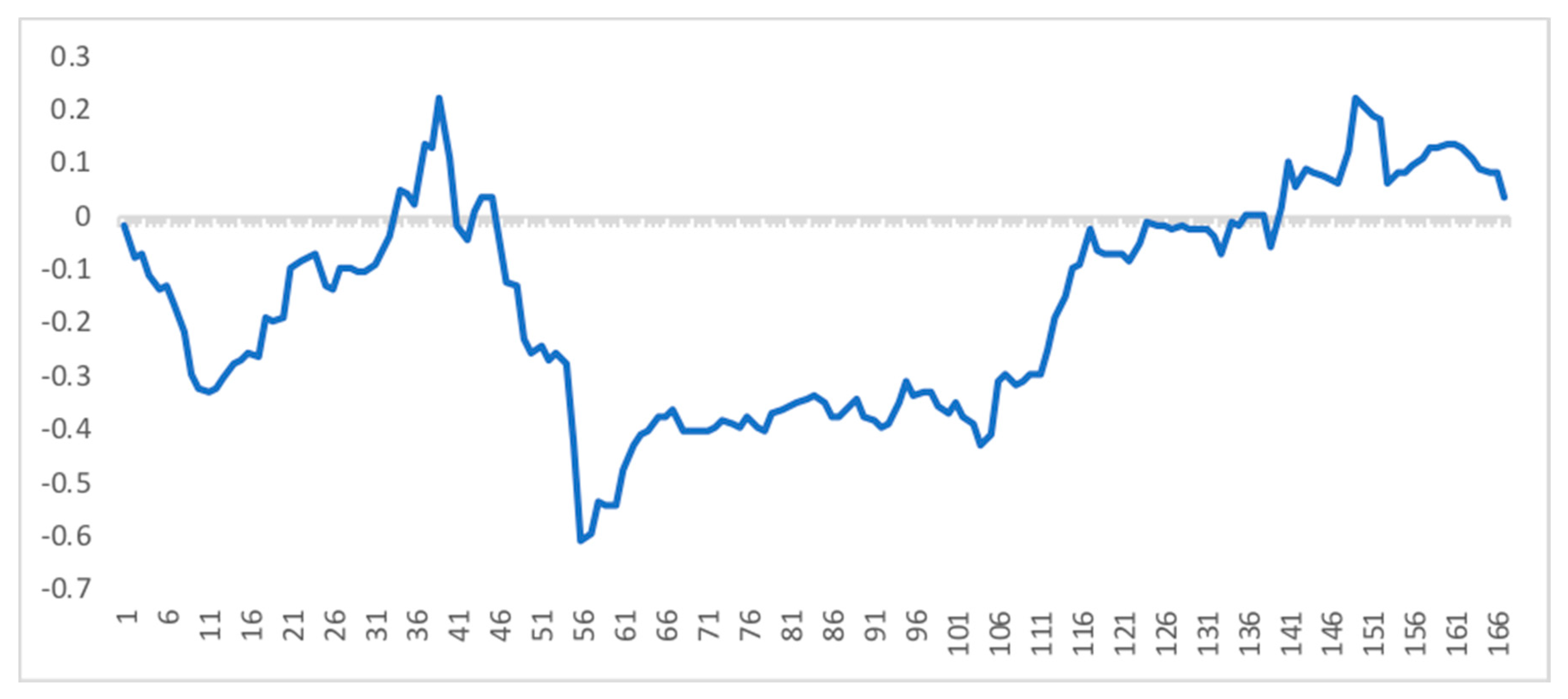

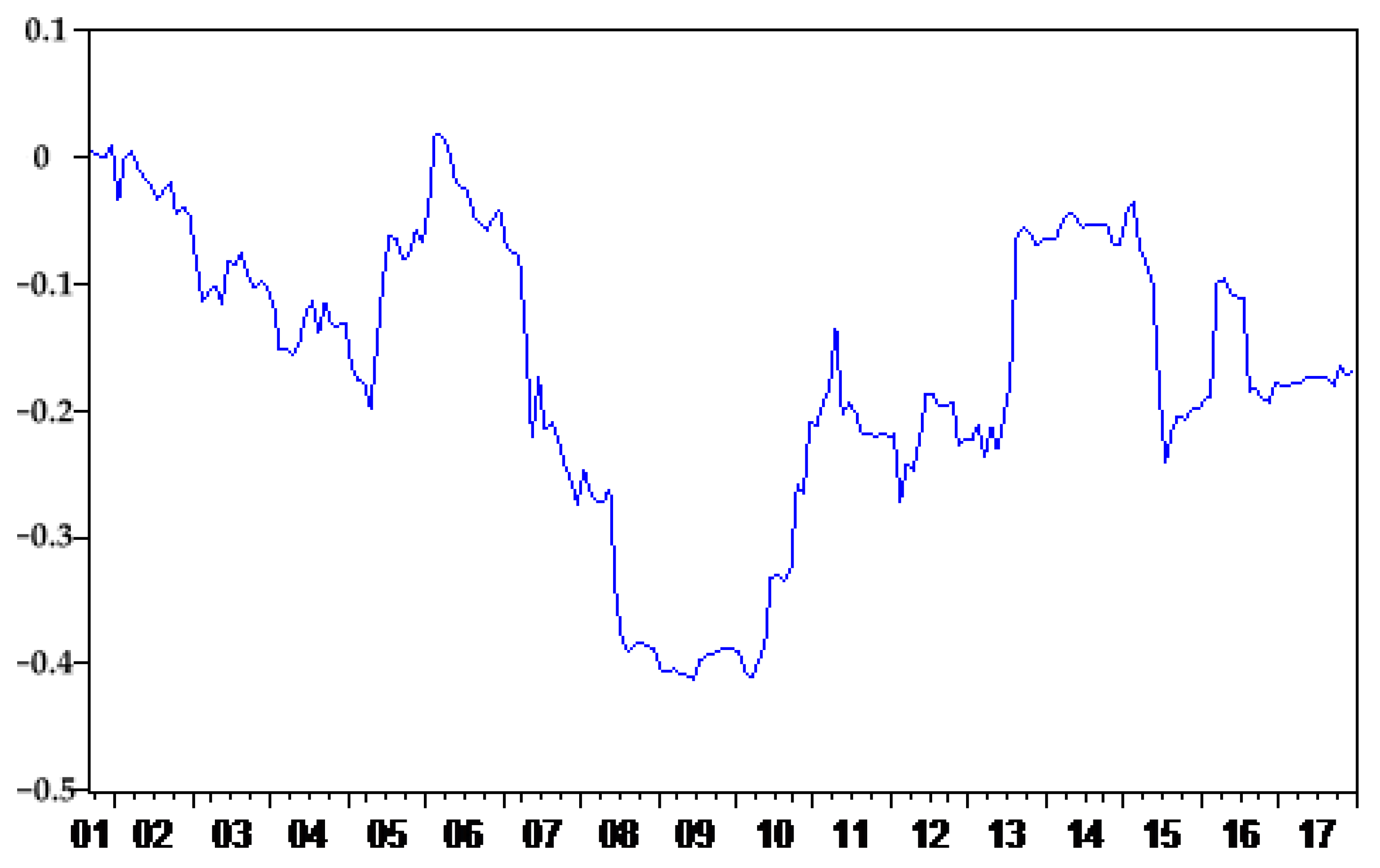

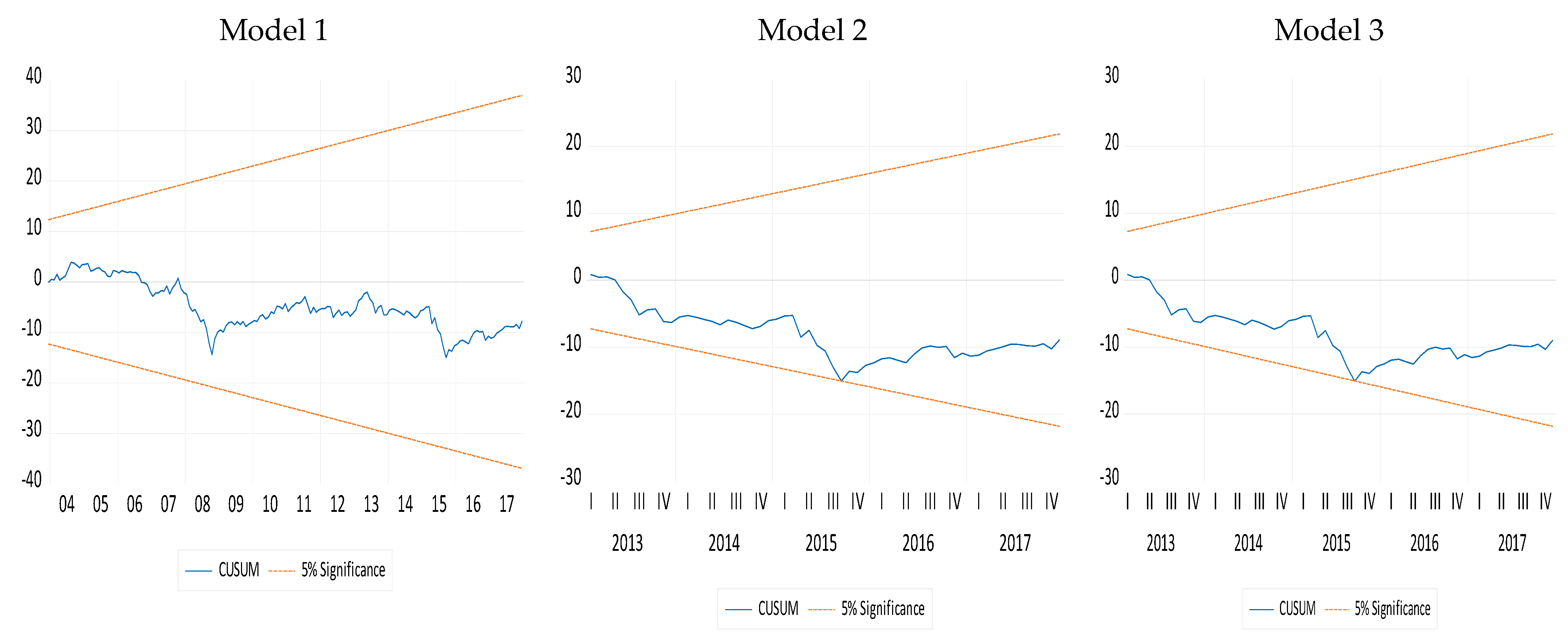

This paper employed both rolling window correlation and dynamic conditional correlation to test the first hypothesis and determine the integration, also known as co-movement, synchronization, and the correlation between the financial markets of the world-leading economies and Indonesia. It was observed that shocks hitting the global economy eventually spread to other countries, including Indonesia.

Our study presents some interesting facts. It is revealed the correlation between global policy uncertainty and the return of the Indonesian stock market is time varying with positive and negative values for separate periods. The average negative estimate of time-varying correlation indicates that when confronted with liquidity constraints in one country, investors may sell off their assets in another country and raise funds in order to meet current or future financial needs. The resulting capital outflow arising from the negative effect of policy uncertainty in the developed markets on the stock market returns also has a negative effect on the sustainable growth of Indonesia.

Several policy implications can be drawn from our research. Our empirical results suggest that the Indonesian stock market is not profitable for global investors, particularly when the global policy uncertainty is high. Regression results based on the autoregressive distributed lag method show that global crude oil prices, world crude oil production, inflation, and gross domestic product have a significant effect on the conditional correlation. Considering the above observations, it is recommended that Indonesian policymakers should closely monitor global crude oil prices and its production, inflation, and growth prospects for avoiding vulnerability of the stock market returns to global uncertainty shocks.

Like most of the studies, our research also has some limitations. First, it examines the interaction between the uncertainty of economic policy in developed markets and the return of the Indonesian stock market; second, global crude oil prices, world crude oil production, gross domestic product, consumer price index, and recessionary indicators are used as determinants of the dynamic conditional correlation.

There is plenty of room for further research. Future studies might be focused on finding out whether the correlation between the world uncertainty index for Indonesia and the return of the Indonesian stock market is constant or time-varying. This can be further extended by splitting aggregate oil price shocks into supply-side shocks, aggregate demand shocks, and oil-specific demand shocks. Such studies will be very instrumental in understanding the shocks that potentially have a significant effect on the dynamic conditional correlation between the uncertainty of economic policy in developed markets and the return of the Indonesian stock market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}