1. Introduction

Since the emergence of a finance-led growth view [

1,

2,

3,

4,

5,

6,

7,

8,

9], researchers have devoted great attention to exploring the determinants of financial development (FD) (e.g., [

10,

11,

12,

13,

14,

15,

16,

17,

18,

19,

20,

21,

22,

23]), and this debate is still evolving. The natural resource rent (NRR) as a determinant of FD has received substantial attention among research scholars, such as [

24,

25,

26,

27,

28], but they have failed to determine its role conclusively. Most of the extant literature (e.g., [

24,

25,

27,

29]) has reported a negative impact of the NRR on FD in various resource-rich countries (famously referred to as “the resource curse hypothesis” (RCH) or “the natural resource curse paradox”) [

30,

31,

32].

However, this orthodox perspective on the natural resource curse as a hurdle to development has been refuted by many scholars in previously published empirical literature; [

26,

28] for example, reported natural resources as a stimulus to FD and proved it is a blessing rather than a curse. Thus, the negative impact of the NRR on the development of the financial sector has not always existed, as reported by [

26,

28]. Various factors could help countries in obtaining benefits from resource revenue and turn the resource curse into a blessing. According to [

33], the resource curse hypothesis is attributed to the rent-seeking behavior of the public office holders entrusted with the management of economic affairs. Atkinson and Hamilton [

34] reported that the incapability of the government to manage and channel the resource revenue to sustainable development is the basic reason behind the existence of the resource course hypothesis [

33].

Therefore, the theory postulates that the presence of strong institutions mitigates the negative impact of resource revenue by controlling rent-seeking behavior (Mehlum, et al. [

35]). This issue of a potential negative impact can be mitigated by enhancing the quality of economic and political institutions [

36]. Thus, the NRR requires a high-quality institutional setup which may control misuse of resource rent and may allow a country to escape from the negative impact of the NRR and thereby enhance FD [

37]. The quality of institutions decides the impact of resource rent on FD, and whether resource abundance is a blessing or curse for any country [

38].

Surprisingly, the extant literature has generally ignored the decisive role of institutional quality in relationships of NRR and FD [

24,

25,

26,

27,

28]. Hence, the fact that the role of institutional quality in the resource-finance nexus has been overlooked has made the theme difficult to locate in the existing literature.

Moreover, the literature has largely focused on developed countries, especially American and European countries (see, for example, [

26,

39]), or developing economies such as, African countries (see, for example, [

29,

40,

41,

42]), which have different institutional and financial sector dynamics. From emerging countries perspective (such as Pakistan) the literature is scant. Pakistan is an emerging economy, blessed with huge natural resource wealth. Considering the natural resource abundance, researchers have recently focused their attention on examining the impact of the NRR on various economic indicators, mainly on economic growth (see, for example, [

43]). However, the literature has very much ignored the nexus between natural resources and FD, which is regarded as an important driver of economic growth. Recently, Asif et al. [

44] has provided the only scholarly evidence relating to the impact of the NRR on FD in Pakistan, and has documented a natural resource curse in the financial sector of Pakistan. However, their study does not consider the role of IQ in this context, which makes their findings elusive. Hence, to the best of our knowledge, this may be the first study in the context of Pakistan which captures the moderation role of IQ in the nexus of the NRR-FD.

Furthermore, it has been established in the literature that various country-specific attributes such as culture, institutional environment, development level, etc. significantly influence the relationship between the macro-economic variables of any country [

45,

46]. Therefore, the findings of these studies cannot be generalized to emerging economies such as Pakistan. Pakistan is an emerging economy that possesses a unique institutional framework and FD dynamics along with abundant natural resources which make it an important case to study. Finally, the existing literature assumes a linear relationship among the NRR, FD, and IQ, although this relationship could be non-linear (asymmetric).

Shin, et al. [

47] postulate that the economic and financial shocks/crises, restructuring programs, regional and international disparities, and abrupt shifts in policies may influence macroeconomic variables, which consequently, could engender asymmetries in their dynamic relationship. Moreover, if non-linearities exist in a relationship then linear models may fail to give reliable and consistent estimates.

Therefore, overlooking the existence of non-linearities in resource-finance nexuses may produce biased empirical results. Furthermore, through asymmetric analysis, the response of FD to both positive and negative changes to the NRR could be captured separately, which is imperative for policy formulation [

48]. The FD could respond differently to positive and negative changes to the NRR. For policy formulation, it is imperative to know the response of FD to both appreciation and depreciation in the NRR. However, to the best of our knowledge, no study has attempted to explore the asymmetric relationship between the NRR and FD.

Given the foregoing observation, the objective of this study is to answer the following two critical questions empirically. First, “In the context of the Pakistani economy, what is the long-run relationship between the NRR and FD when IQ acts as a moderator? Second, “Do asymmetrical relationships exist between the NRR and FD in Pakistan?” Our study has made an invaluable contribution by investigating the ambiguous relationship between the NRR and FD, and the role of IQ in this paradigm. The findings of this study are useful for stakeholders seeking a source to help turn the resource curse into a blessing for the financial sector.

Furthermore, unlike the existing literature, which ignores asymmetries in the resource-finance relationship, this study has applied the nonlinear autoregressive distributed lag (NARDL) cointegration approach of [

47] along with the Autoregressive Distributed Lag (ARDL) bound test to cointegration [

49], to explore potential asymmetries in the NRR and FD nexuses for the first time in the economic literature and to provide valuable insight for policymakers.

Finally, we find a single significant threshold value of 3.097 above which the relationship of the NRR and FD turns nonlinear. It is interesting to note that up to a threshold of 3.097 the coefficient is 3.228, and above this threshold, the coefficient declines slightly to 2.804. Importantly, above the identified threshold the variation explained by the NRR declines slightly. This implies that regulators should maintain at least an IQ level of up to 3.097 to experience the most desirable financial benefits of the NRR.

The rest of this study is organized as follows;

Section 2 contains the literature review,

Section 3 provides details of the research design and methods,

Section 4 discusses the empirical results, and

Section 5 outlines the conclusion and policy implications of the study.

2. Literature Review

The NRR is profit accrued from trading natural resources, after deducting the cost of such trade (payments to factors of production) and also considering the opportunity costs of production [

50]. The literature has mainly focused on the role of the NRR in the economic progress of countries and has reported mixed evidence [

51,

52,

53,

54,

55,

56,

57,

58]. The adverse effect of the NRR on economic growth is coined as a “the resource curse hypothesis”, which is widely investigated in diverse contextual settings. Classical growth theory postulates that natural resource wealth does not foster economic performance [

38,

59,

60]; low economic growth is attributed to a poor institutional environment characterized by corruption, the inefficiency of the bureaucracy and mismanagement [

57].

However, the positive role of the NRR in stimulating economic growth has also been observed by famous economists such as David Ricardo and Adam Smith. Natural resource endowment enhances economic growth by creating ample investment opportunities and markets in developing economies [

61,

62]. Brunnschweiler [

63], articulated that natural resource endowment fosters economic growth through sound institutions. Many other scholars have rejected the resource curse hypothesis, for example, [

64,

65,

66,

67], and concluded that the NRR is a blessing rather than a curse. Arin and Braunfels [

68] also rejected the resource curse view of natural resources and provided fresh evidence regarding the positive role of natural resources on growth via a sound institutional environment. Erdoğan, et al. [

69] examined the impact of natural resource exports on economic growth and the role of financial deepening in this context. They evidenced that the impact of natural resource exports on economic growth is sensitive to the level of financial deepening; when financial deepening crosses a threshold of 45% natural resource exports significantly enhance economic growth.

Likewise, considering the question of whether the NRR is a “curse” or “blessing” for the development of the financial sector, the empirical literature has produced conflicting evidence. The traditional view suggests the NRR hinders FD by influencing trade openness, Dutch diseases, rent-seeking, and corruption. Arguably, Yuxiang and Chen [

24] were the first to explore the relationship between the NRR and FD in the context of China and reported an adverse effect of the NRR on FD. They argue that the NRR has a negative impact on FD through enhancing corruption, rent-seeking, misuse of the NRR and Dutch diseases. Recently, Guan, Kirikkaleli, Bibi and Zhang [

25] also reported similar results in China. Furthermore, Mlachila and Ouedraogo [

27] investigated the resource curse hypothesis in a sample of 68 resource-rich countries and found strong evidence of the natural resource curse in the financial sector of sample countries, operating through the commodity price shocks channel.

Recently, the role of institutions in economic and financial development has been widely acknowledged [

70,

71]. Economists generally agree that the outcome of economic policies and resource abundance in an economy is sensitive to the quality of its institutions [

72]. Irrespective of how well-devised policy is, or how many resources a country has, if institutions are not supportive then the positive outcome from such policies or resources cannot be realized [

73]. Institutions are the humanly created rules of the game in a society which shape economic, political, and social interactions. They include the formal and informal standards that decide how people treat and interact with each other [

74]. Bhattacharyya and Hodler [

75], studied the mediating role of IQ between the NRR and FD and reported that in the absence of sound political institutions in a country, natural resource wealth weakens contract enforcement, which is consequently harmful for FD, ceteris paribus, while the presence of sound institutions enhances contract enforcement, which is useful in accelerating FD. Meager economic development in resource-abundant economies is attributed to corruption, the potential existence of rent-seeking and patronage [

76]. Further, [

76] recommended addressing rent-seeking behavior and patronage by enhancing IQ through focused policies along with macro-economic management in resource-abundant economies. Costa and Santos [

37], examining the role of institutions in allotting royalties from hydrocarbon resources to minimize the resource curse, reported huge misappropriation by institutions. They recommend that enhancing the quality of institutions responsible for monitoring oil rents disbursement and utilization and enhancing public participation may help to avoid the misappropriation of oil rents. Taguchi and Lar [

77] studied the natural resources curse hypothesis for two different periods in selected economies from 1980–1995 and 1995–2014. For the first period, their results validate the natural resource curse hypothesis [

33], while the results are reversed for the second period, due to a better institutional environment in the sample countries.

Rathinam and Raja [

78] studies the nexuses between IQ and FD in the Indian context and observed a causal relationship between institutional development and FD, which eventually enhances economic growth. Similarly, Khan et al. [

79] examine a long-run association between IQ and stock market development in the context of Pakistan. Recently, Dwumfour and Ntow-Gyamfi [

29] have empirically studied the relationship between resource-abundance, FD, and IQ, and evidenced that IQ reduced the negative impact of the NRR on FD. Bulte, et al. [

80] noticed that the direct influence of mineral resource rent on financial sector development is ambiguous; however, indirectly mineral resource rent positively influences FD when IQ is introduced into the analysis. Huang [

81] examined whether an improvement in the quality of political institutions enhances FD. The empirical findings revealed that IQ fosters FD in the short-run in developing economies and an increase in FD is observed following a democratic transformation in a country.

Summing up, the NRR can undermine FD by enhancing corruption, rent-seeking, misuse of resources, and Dutch diseases, and weakening contract enforcement. The literature contends that a sound institutional environment can potentially check channels through which the natural resource curse operates in the financial sector and turn the curse into a blessing. Moreover, the literature suggests that various macroeconomic variables as fundamental determinants of FD such as economic growth, economic policy uncertainty, trade openness, and capital must be taken as control variables in our model for efficient and reliable results.

The FD and economic growth relationship is a bidirectional phenomenon, i.e., a supply-leading and demand-following hypothesis. The earlier view considers economic growth as a function of FD, as a developed financial system minimizes the information asymmetry and transaction costs, which attracts domestic and foreign financial resource into the economic system [

33,

82,

83,

84]. The latter view holds that economic growth stimulates FD (banking sector and financial markets) via increased investment opportunities and demand for financial services [

13,

39,

85,

86]. Therefore, economic growth as an important determinant of FD is included as a control for FD in our analysis.

Trade openness is a stimulus to exports and—accompanied by increased demand for financial services and the scale of the financial sector—is also an important determinant of FD [

87,

88,

89]. Openness enhances FD only in the presence of sound institutions [

90]. Moreover, according to Baltagi, et al. [

91], capital account and trade openness are significant determinants of FD. Trade openness seems to have a positive impact on FD; therefore, we take openness as a control for FD in our study. [

92] defined economic risk as a risk that emerges from the uncertainty of fiscal and monetary policies devised by the government and central bank of a country.

The author argues that the government uses economic policy as a tool to shape financial markets and make frequent adjustments according to the economic conditions. Uncertainty regarding government economic policy has a profound effect on financial markets and it undermines the development process [

93,

94,

95]. Therefore, we have used the economic risk index developed by Baker et al. [

96] as a control variable in our model. Capital also significantly influences the FD; therefore, in line with [

26,

39,

97] we also incorporate capital as a control variable in our model.

Moreover, as mentioned in the introduction section the existing literature on the NRR and FD nexuses only assumes a symmetric relationship and ignores the existence of asymmetries. Abdulahi, Shu and Khan [

51] empirically investigated the links between the NRR and economic growth and found an asymmetric relationship between the NRR and economic growth, subject to a certain threshold level of IQ. When IQ crosses a certain threshold level, only then can the NRR benefit economic growth. Likewise, Tiba [

98] also found non-linearity in the relationship between the NRR and economic growth. In the same vein, Shin, Yu and Greenwood-Nimmo [

47] postulate that economic and financial shocks/crises, restructuring programs, regional and international disparities, and abrupt shifts in policies may influence the macroeconomic variables, which consequently, could engender asymmetries in their dynamic relationship. Moreover, if non-linearities exist in a relationship then linear models may fail to give reliable and consistent estimates.

Hence, based on the resource-growth experience, we have assumed non-linearity in the relationship between the NRR and FD, to be empirically verified at a later stage of the study. The literature discussed above laid down the conceptual foundations to study the impact of the NRR on FD and the role of IQ in this paradigm by controlling FD for economic growth, trade openness, economic policy uncertainty, and capital. Relying on the given literature, we postulate our hypothesis as follows;

Hypothesis (H1): Institutional quality significantly positively moderates the relationship between the NRR and FD in Pakistan.

Hypothesis (H2): The relationship between the NRR and FD is asymmetric and depends on a certain IQ threshold.

4. Results and Discussion

Table 1 shows descriptive and normality statistics (mean, standard deviation, minimum, maximum values and p-values of the Cramer von Mises, Shapiro-Wilk and Anderson Darling tests, respectively) of all variables of the study. The mean values of economic growth, economic risk, trade openness, and FD are comparatively higher. Standard deviation as relative to the rest of the variables shows a high volatility in the NRR, in economic growth and in both the series of FD. Moreover, we have tested the normality of our variables by using widely used methods of normality, i.e., Cramer von Mises [

115], Shapiro-Wilk [

116] and Anderson Darling [

117] tests and the p-values of the respective tests are reported in the last three columns of

Table 1, respectively. Yap and Sim [

118] compared various tests of normality based on their power and ranked the Shapiro-Wilk test at the top, followed by the Anderson Darling and Cramer von Mises tests.

The p-values of all the tests are greater than 0.05, which shows that we fail to reject the null hypothesis of normality in all cases, i.e., all the series are normally distributed and satisfy the presumption of normality for further empirical analysis.

Furthermore, we calculated Pearson’s correlation which is reported in

Table 2. The choice of Pearson’s correlation was decided by the normal distribution of the residual obtained by Jarque-Bera [Jarque-Bera normality test: 3.264,

p-value 0.1956].

The results in

Table 2 show that the NRR has a negative correlation with FD, economic risk, and openness. However, it is positively correlated with the rest of the variables. The IQ, economic growth, moderating term and capital show a positive correlation with FD.

As mentioned in

Section 3.4, the ARDL bounds test to cointegration can be applied only to variables with mixed integration order I(0) or I(1). Thus, we determined the stationary properties of the variables, using the Augmented Dickey-Fuller (ADF) test, proposed by Dickey and Fuller [

104,

105], and the Phillip-Peron (PP) test of Phillips and Perron [

106]; the results are presented in

Table 3. This reveals that both the series of FD, the NRR, the interactive term (meaning the interaction variable generated by multiplying IQ and the NRR to explore the moderating role of IQ), economic growth, and policy uncertainty are non-stationary at the level, although they are stationary after taking the first difference, as per ADF. The PP test also confirms ADF results, except for the NRR which is stationary both at the level and at first difference according to the PP test. The IQ, trade openness and capital are found to be stationary at both the level and first difference, and both tests affirm these findings, indicating the robustness of the unit root results. However, both the ADF and PP tests are criticized in the literature, as they do not consider any structural break in the series resulting from any abrupt policy change or natural calamity, and so may give misleading results. To overcome this drawback, the literature gives various unit root tests with the ability to consider any structural break in a series, such as [

107,

119].

Following recent literature [

113], we used the Zivot-Andrews [

107] structural break unit root test. The results of this are reported in

Table 3, which reveals that FD, the NRR, trade openness, economic growth, economic risk, and capital are non-stationary at the level; however, these variables are stationary at the first difference, while IQ is stationary at both the level and first difference. The overall results confirm a mixed integration order and importantly none of the variables is integrated at the second order.

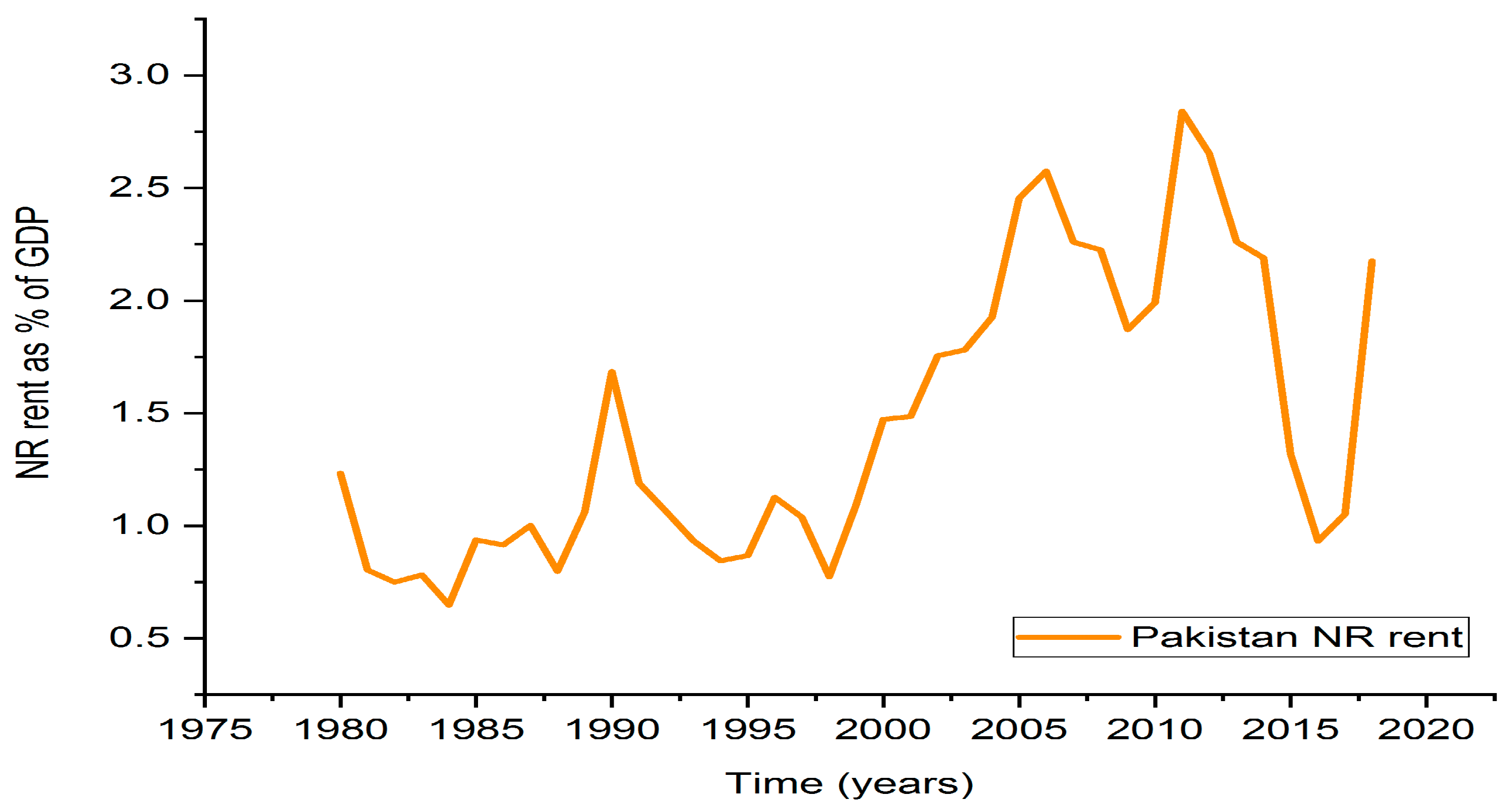

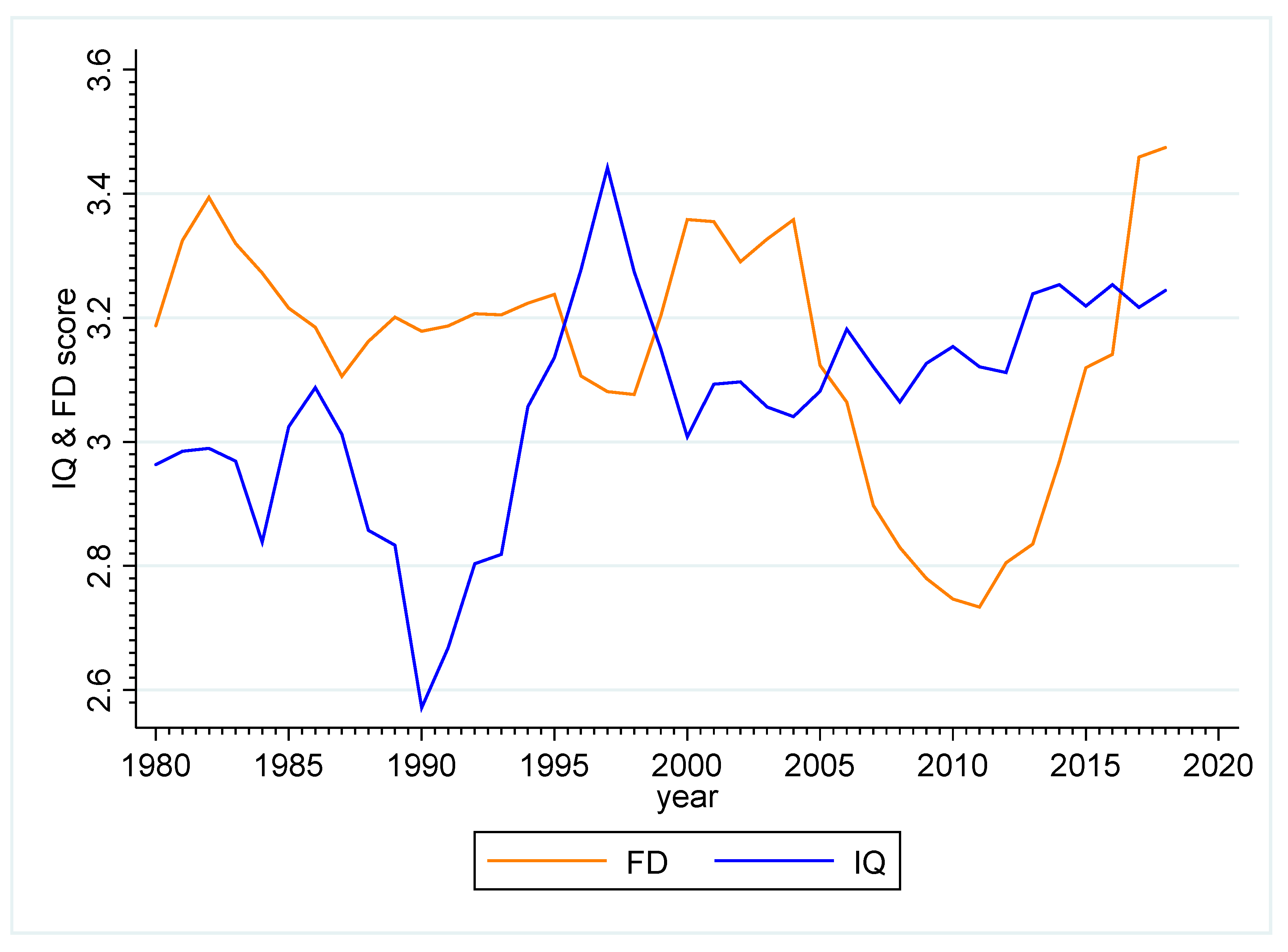

Furthermore, structural breaks represent the structural changes which appear in the individual time series. We tested the overall structural break after estimating the regression using STATA 15, which captured 2007 as a single significant structural break. This break represents a year of political instability in the country caused by a series of events, including the Seventeenth Amendment in the constitution of Pakistan, the state of emergency in 2007, the National Reconciliation Ordinance, the siege of Lal Masjid, the suspension of the Chief Justice of the Pakistan Supreme Court, Iftikhar Muhammad Chaudhry, and the movement to impeach Pervez Musharraf. These events collectively disrupted the overall economy and political institutions, as well as financial activities.

After testing the stationarity of the variables accordingly, we first applied the linear ARDL bound test to cointegration, the results of which are shown in

Table 4. These results show that ARDL F-statistics are greater than the upper bond critical values given by [

49], at all—1%, 5% and 10%—significance levels for all models from Equations (3)–(7), specified by swapping all variables as dependent variables; this verifies the existence of 7 cointegrating vectors in the above model. This proved the existence of a long-run equilibrium relationship/cointegration between the FD, the NRR, IQ, economic growth, policy uncertainty, trade openness, capital, and the interactive term for Pakistan over the period studied. Additionally, to confirm the robustness of the results, we performed diagnostic and stability tests; the result proved the robustness, reliability, and usefulness of the results obtained from the ARDL bounds test of [

49] for policy formulation.

After confirming the linear cointegration among the FD of Pakistan and its determinants, we then also estimated the Non-linear ARDL model of [

47], specified in Equation (6) above, in order to explore the presence of any protentional asymmetric long-run relationship in Pakistan among FD and its determinants. Specifically, we intended to document the response of FD to both appreciation and depreciation of the NRR and offer more comprehensive findings for policy implications. The results of the non-linear ARDL model (significant F-statistics) reported in the bottom portion of

Table 4 are in line with linear ARDL results and this proves the existence of a strong long term cointegration among variables of the study.

Having confirmed the cointegration among the variables of the study, we then proceeded to estimate the long-run and short-run coefficients.

Table 5 presents long-run and short-run parameters in the upper and bottom segment, respectively. The results revealed that the IQ, moderating term, economic growth, trade openness, and capital significantly stimulate FD in Pakistan, while economic risk has a significant negative impact on FD, and natural resource exerts no significant effect on FD in Pakistan in the short run. In the long run, IQ, moderating term, economic growth, capital, and trade openness have a significant cointegrating relationship with FD, whereas the NRR and economic risk have an adverse significant effect on FD in Pakistan. These empirical findings regarding the role of the NRR in FD are consistent with the existing body of literature on the subject compiled in different contextual settings [

24,

75]. A sound institutional environment significantly explains the FD [

120]; high-quality institutions exert pressure on policymakers to devise a policy framework that reduces uncertainty and thereby enhances the FD [

121,

122,

123]. The significant positive coefficient of IQ in both the short- and long run confirms the vital role of IQ in stimulating FD in Pakistan and supplements the existing theoretical and empirical view regarding this phenomenon.

Moreover, our results depict a statistically significant moderating term (i.e., the interaction of the NRR with IQ ) which confirms the moderating role of IQ (both in the short- and long run) in the NRR and FD nexuses in Pakistan. Kolstad and Søreide [

76] argued that to examine the real effect of the NRR on FD, the interactive role of IQ with the NRR must be taken into account. Omitting IQ from the model will lead to empirical mis-specification and result in an overestimation of results. Bhattacharyya and Hodler [

75] evidenced that in counties with weak institutions, the NRR hinders FD. Overall, our findings are consistent with the extant literature, for example [

24,

26,

39,

75,

124], which reported similar results. Furthermore, a plausible justification of our findings is the growing level of IQ, which acts as a tool to avoid the resource-curse in Pakistan. The quality of institutions has considerably improved in Pakistan due to the successful transition of back to back political regimes over the last two decades. Furthermore, after the establishment of the National Accountability Bureau (NAB), established to curb corruption in Pakistan, and its anti-corruption campaign, the level of corruption has slightly decreased (for example from June 2002 the corruption score was 1.50, which improved to 2.00 by 2008). Since 2007 the independent judiciary movement in Pakistan has led to a more independent and efficient judiciary, which is an essential part of a sound institutional framework. Law and order were rated by the ICRG at 3.00 points in 2009, which increased to 3.42 in 2010 and 3.50 in the next three years. Similarly, democratic accountability has substantially improved, as the score was only 1.00 until 2007, but then reached 4.50 in 2016. The gradual improvement in IQ appears as an important consideration for policymakers.

The policymakers in Pakistan and other resource-rich countries that are in a similar development cadre should focus on the institutional framework to avoid the negative impact of the NRR on various development indicators and to utilize natural resources as a blessing rather than a curse. Moreover, the coefficient of the error correction term (ECMt-1) is significant and negative, which further supports the existence of cointegration between FD in Pakistan and its selected determinants; it also implies that any deviation from the equilibrium relationship in the short run is corrected with a speed of approximately 65% percent annually. We found no anomaly regarding the results of the controlling variables.

As one of the objectives of this study is to investigate asymmetries in the resource-finance nexuses, to this end we separated depreciation from appreciation in the NRR and estimated the Non-linear Autoregressive Distributed Lag model (NARDL), and the results for the short- and the long run are given in

Table 6. We find a significant negative coefficient of the NRR in the long run, which indicates that the NRR significantly negatively influences the FD in Pakistan during an appreciation period, whereas in a depreciation period the NRR has a positive and statistically significant coefficient, which shows that FD responds positively to a decline in the NRR.

As both the positive and negative partial sum of natural resources rent changes have statistically significant coefficients, which are different in sign and size, this shows that the NRR changes had an asymmetric effect on FD in Pakistan, whereas in the short-run an appreciation in natural resources has no effect on FD and depreciation harms FD. Furthermore, the results of the control variables are in line with the theoretical and empirical literature and free from any incongruity.

Moreover, the is highly significant, which further supports the rationale for using the non-linear model in this context. The stability and diagnostic tests are applied to authenticate the reliability of our estimates. The insignificant RESET test confirms the correct specification of our non-linear model. The CUSUM and CUSUM Square graphs of the respective models are not reported to maintain brevity, as we have an estimated number of estimators. Other diagnostic tests confirm that our model is free from serial correlation and heteroscedasticity, and that residuals follow a normal distribution.

For robustness, we use an alternative measure of FD, i.e., domestic credit as a percentage of GDP (DC), which is also widely used in the literature. The results are reported in

Table 7 and prove the robustness of our main primary results. The results of the bound test also confirm long-run cointegration relationships among FD measures by “DC” and the NRR, IQ, moderating term, economic growth, policy uncertainty, trade openness, and capital. These results are in line with our baseline model estimates and prove the usefulness of our primary results.

We also estimated the long run and short run coefficient to confirm the robustness of our baseline model; the results are shown in

Table 8. The NRR significantly negatively influences the FD measured by DC in both the short- and long run. The IQ, the moderating term, holds significant positive coefficients, in the short- and long run, which are in line with the results of the primary model. Moreover, the results of controlling variables are in line with the literature.

Threshold Analysis

Table 9 incorporates the results of the single threshold estimation. We find a single significant threshold value of 3.097 above which the relationship of the NRR and FD turns nonlinear. It is important to note that up to a threshold of 3.097 the coefficient is 3.228, and above this threshold the coefficient declines slightly to 2.804. Importantly, above the identified threshold the variation explained by the NRR declines slightly. This implies that regulators should maintain at least an IQ level of up to 3.097 to experience the most positive financial benefits of the NRR.

5. Conclusions

This study aimed to explore the long-run relationship between the NRR and FD in Pakistan by incorporating the moderating role of IQ in this framework in both symmetric and asymmetric settings and offers valuable policy implications for stakeholders. We used the ARDL bounds test and NARDL to cointegration approaches to answer the research questions. To validate the robustness of our results, we have re-estimated our primary model by using the alternate traditional proxy of FD (i.e., DC) and the results confirm the robustness of our primary results. The empirical findings proved a long run equilibrium association between the NRR and FD and the positive moderating role of IQ in this paradigm. Specifically, the resource rent negatively influences the FD in Pakistan, IQ has a positive association with FD and the significant positive coefficient of the moderating term proves the positive moderating role of IQ in the NRR and FD nexuses in Pakistan.

Furthermore, the results of the NARDL prove the existence of asymmetries in the relationship between the NRR and FD, both in the short and long run. FD does not respond identically to both appreciation and depreciation in the NRR, as both the positive and negative significant coefficients of the NRR reveals that changes in the NRR have an asymmetric effect on FD in Pakistan.

It is worth mentioning that we find a single significant threshold value of 3.097 above which the relationship of the NRR-FD turns nonlinear—as up to this threshold the NRR explains substantial (coefficient is 3.228) in FD, which declines slightly to 2.804 above the threshold level. Based on the findings of this study we offer the following policy implication for stakeholders:

Policy attention should be directed to improve the institutional framework, in order to challenge the resource curse puzzle in the financial sector and stimulate FD by understanding and incorporating the moderating role of IQ in resource finance nexuses. IQ is an essential factor for FD [

121,

125]. On the other hand, weak institutions are a hurdle to FD [

75]. Moreover, there is a need to identify other channels through which the NRR could enhance FD, and policies should be devised to improve them in order to fully reap the benefits of the natural resource. However, this process is very complicated and needs careful attention from researchers.

The NRR may indirectly stimulate FD, potentially via a sound institutional framework. This implies that IQ prevents the misuse of the NRR and allocates it to the efficient sectors of the economy through the financial system, as the view that the NRR undermines FD [

126] is attributed to misuse of natural resource revenue. The threshold result implies that regulators should maintain at least an IQ level of up to 3.097 to experience the most lucretive financial benefits of the natural resource rent in Pakistan. Furthermore, considering the findings of this study regarding other controlling variables, policymakers should come up with policies that enhance the financial and economic development of the country.

The findings of this study are subject to a few limitations that could be addressed in future research. As FD is composed of two sub-sectors i.e., financial institutions development and financial markets development, in future an attempt to explore the impact of the NRR on these two components individually would be a great contribution to the resource-finance literature. Likewise, future studies can also investigate the role of each dimension of IQ individually in the NRR and FD relationship.

,

,

{kind=link}

{kind=link}