Does the Mixed-Ownership Reform Affect the Innovation Strategy Choices of Chinese State-Owned Enterprises?

Abstract

:1. Introduction

2. Theoretical Background and Hypothesis Development

2.1. Types and Implications of Innovation Strategies

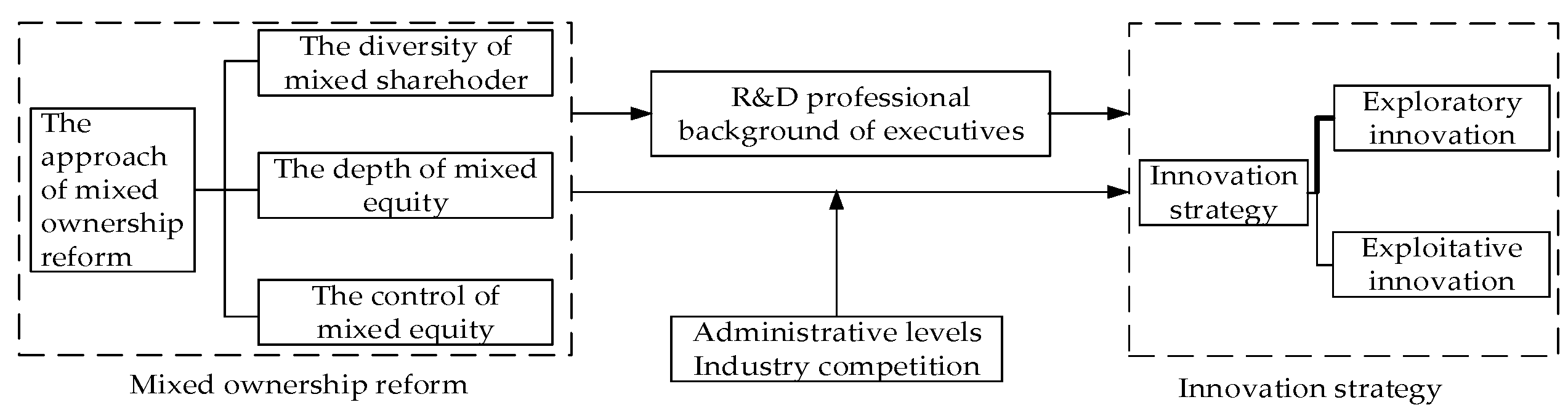

2.2. The Approach of Mixed-Ownership Reform

2.3. Hypothesis Development

3. Materials and Methods

3.1. Sample Selection and Data Sources

3.2. Model Construction and Variable Definition

4. Results

4.1. Descriptive Statistics and Correlation Analysis

4.2. Basic Regression Results of Mixed-Ownership Reform and Innovation Strategy Choices of SOEs

4.3. Basic Regression Results of Heterogeneous Shareholder Holdings and the Innovation Strategy Choices of SOEs

4.4. Basic Regression Results of the Moderation Effect of Administrative Levels and Industry Competition

4.4.1. The Moderation Effect of Administrative Levels

4.4.2. The Moderation Effect of Industry Competition

4.5. Endogenous Test

4.6. Other Robustness Test

4.6.1. Replacement Measurement Index of Innovation Strategy

4.6.2. Replacement Measurement Index of Mixed-Ownership Reform Degree of SOEs

4.6.3. Robustness with the Modified Sample Size

5. Further Analysis: Mechanism Analysis of the Impact of Mixed-Ownership Reform on the Innovation Strategies of SOEs

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Solow, R.M. Technical change and the aggregate production function. Rev. Econ. Stat. 1957, 39, 312–320. [Google Scholar] [CrossRef] [Green Version]

- Cadil, J.; Mirosnik, K.; Petkovova, L.; Mirvald, M. Public Support of Private R&D–Effects on Economic Sustainability. Sustainability 2018, 10, 4612. [Google Scholar] [CrossRef] [Green Version]

- March, J.G. Exploration and exploitation in organizational learning. Organ. Sci. 1991, 2, 71–87. [Google Scholar] [CrossRef]

- Tang, Q.Q.; Li, H.W. The choice of innovation mode of Chinese enterprises-based on the perspective of corporate governance. Contemp. Econ. Manag. 2011, 33, 23–31. [Google Scholar]

- Li, Y.H. Corporate governance and heterogeneous R&D innovation of enterprises-An empirical study based on GEM listed companies of strategic emerging industries. Secur. Mark. Her. 2014, 26–31. [Google Scholar]

- Wang, Y.X.; Sun, Y.Y. The impact of corporate governance on innovation strategy-An empirical study based on R&D expenditure heterogeneity. Res Financ. Econ. Issues 2018, 5, 113–121. [Google Scholar]

- Zhu, L.; Xu, X.T.; Wang, C.Y. Industrial environment, tenure of managers and ambidexterity innovation investment of enterprises-empirical data from GEM. Secur. Mark. Her. 2017, 6, 4–11. [Google Scholar]

- Zhai, S.P.; Bi, X.F. Environmental uncertainty, management confidence and ambidexterity innovation investment of enterprises. J. Zhongnan Univ. Econ. Law 2016, 91–100. [Google Scholar] [CrossRef]

- Li, C.; Pervaiz, K.; Khan, M.A.; Ur Rehman, F.; Oláh, J. On the Asymmetries of Sovereign Credit Rating Announcements and Financial Market Development in the European Region. Sustainability 2019, 11, 6636. [Google Scholar] [CrossRef] [Green Version]

- Sun, J.J.; Zhang, Y. Financial development, agency cost and innovation strategy of enterprises. Res Financ. Econ. Issues 2019, 50–59. [Google Scholar] [CrossRef]

- Li, W.G.; Yu, M.G. Ownership structure and innovation of private enterprises. Manag. World 2015, 112–125. [Google Scholar] [CrossRef]

- Wang, Y.W.; Chen, L. Does mixed ownership reform promote enterprise innovation? Res. Econ. Manag. 2017, 38, 112–121. [Google Scholar]

- Yuan, J.G.; Hou, Q.S.; Cheng, C. The curse effect of enterprise political resources-Based on the investigation of political connection and enterprise technological innovation. Manag. World 2015, 139–155. [Google Scholar] [CrossRef]

- Ren, S.M.; Li, X.Q.; Wang, Y.L.; Han, Y.Q. Private equity participation, institutional environment and enterprise innovation. R D Manag. 2019, 31, 59–71. [Google Scholar]

- Zhang, J.D.; Liu, S.H. Viewing the choice of strategic investors from China Unicom’s mixed ownership reform. Account. Res. 2018, 28–34. [Google Scholar] [CrossRef]

- Gavetti, G.; Levinthal, D. Looking forward and looking backward: Cognitive and experiential search. Adm. Sci. Q. 2000, 45, 113–137. [Google Scholar] [CrossRef] [Green Version]

- Green, S.G.; Gavin, M.B.; Aiman-Smith, L. Assessing a multidimensional measure of radical technological innovation. IEEE Trans. Eng. Manag. 1995, 42, 203–214. [Google Scholar] [CrossRef]

- Levinthal, D.A.; March, J.G. The myopia of learning. Strateg. Manag. J. 1993, 14, 95–112. [Google Scholar] [CrossRef]

- Brickley, J.A.; Lease, R.C.; Smith, C.J. Ownership structure and voting on antitakeover amendments. J. Financ. Econ. 1988, 20, 267–291. [Google Scholar] [CrossRef]

- Lu, J.C.; Jiang, G.S. Mixed ownership and cash dividend distribution of state-owned enterprises. Econ. Manag. 2018, 40, 5–20. [Google Scholar]

- Bennedsen, M.; Wolfenzon, D. The Balance of Power in Closely Held Corporations. Soc. Sci. Electron. Publ. 2001, 58, 113–139. [Google Scholar] [CrossRef] [Green Version]

- Ma, L.F.; Wang, L.L.; Zhang, Q. The priority choice of mixed ownership: The logic of market. China’s Ind. Econ. 2015, 5–20. [Google Scholar] [CrossRef]

- Wang, Y. Mergers and acquisitions of mixed ownership and innovation-driven development-A longitudinal case study of “hanlan environment” of local state-owned enterprises in guangdong province from 2001 to 2015. Manag. World 2016, 150–163. [Google Scholar] [CrossRef]

- Luo, F.K.; Pang, T.Y.; Wang, J. Does the mixed ownership reform affect the R&D investment of enterprises?-Based on the empirical evidence of A-share listed companies in China. R D Manag. 2019, 31, 56–66. [Google Scholar]

- Wu, C.Q.; Li, T.K. Enterprise behavior in mixed market. Donyue Trib. 2005, 38–47. [Google Scholar] [CrossRef]

- Choi, S.B.; Lee, S.H.; Williams, C. Ownership and firm innovation in a transition economy: Evidence from China. Res. Policy 2011, 40, 441–452. [Google Scholar] [CrossRef]

- Faber, J.; Hesen, A.B. Innovation capabilities of European nations: Cross-national analyses of patents and sales of product innovations. Res. Policy 2004, 33, 193–207. [Google Scholar] [CrossRef]

- Porta, R.L.; Lopez-De-Silanes, F.; Shleifer, A. Corporate Ownership Around the World. J. Financ. 1999, 54, 471–517. [Google Scholar] [CrossRef]

- Li, Z.Q.; Sun, Z.; Wang, Z.W. “Tunneling” and ownership arrangement-Empirical evidence from capital occupation of major shareholders of listed companies in China. Account. Res. 2004, 25, 3–13. [Google Scholar]

- Pagano, M.; Röell, A.A. The choice of stock ownership structure: Agency costs, monitoring, and the decision to go public. Q. J. Econ. 1998, 113, 187–225. [Google Scholar] [CrossRef]

- Jin, Y.C.; Jin, Q.L.; Xuan, Y. “Inaction” or “eager expression”: The political motivation in enterprise investment. Econ. Res. J. 2016, 51, 126–139. [Google Scholar]

- Li, H.J.; Liu, S.Y. Bank credit, ownership nature and enterprise innovation. Stud. Sci. Sci. 2015, 33, 1089–1099. [Google Scholar]

- Aghion, P.; Reenen, J.V.; Zingales, L. Innovation and Institutional Ownership. Am. Econ. Rev. 2013, 103, 277–304. [Google Scholar] [CrossRef] [Green Version]

- Richardson, S. Over-investment of free cash flow. Rev. Account. Stud. 2006, 11, 159–189. [Google Scholar] [CrossRef]

- Chen, G.; Zhang, J.J.; Pifer, N.D. Corporate Governance Structure, Financial Capability, and the R&D Intensity in Chinese Sports Sector: Evidence from Listed Sports Companies. Sustainability 2019, 11, 6810. [Google Scholar] [CrossRef] [Green Version]

- Zhou, J.; Xue, Y.Z. The impact of corporate internal governance mechanism on R&D investment-An empirical study based on the shareholding of the general manager and the structure of the board of directors. R D Manag. 2008, 20, 1–9. [Google Scholar]

- Bi, X.F.; Zhai, S.P.; Jiang, B.Q. The impact of government subsidy and financial redundancy on ambidexterity innovation of high-tech enterprises. Account. Res. 2017, 46–52. [Google Scholar] [CrossRef]

- Tang, Q.Q.; Xiao, H.L. Financing constraints and innovation investment-cash flow sensitivity- Based on the perspective of R&D heterogeneity. South China J. Econ. 2012, 11, 40–54. [Google Scholar]

- Hao, Y.; Gong, L.T. Mixed participation of state-owned and private shareholders and improvement of corporate performance. Econ. Res. J. 2017, 52, 122–135. [Google Scholar]

- Yang, X.Q.; Yin, X.Q. How does the mixed ownership reform of state-owned enterprises affect the company’s cash holding? Manag. World 2018, 34, 93–107. [Google Scholar]

- Wei, M.H.; Cai, G.L.; Liu, J.H. Research on classified governance of state-owned listed companies in China. J. Sun Yatsen Univ. Soc. Sci. Ed. 2017, 57, 175–192. [Google Scholar]

- Cai, G.L.; Liu, J.H.; Ma, X.X. Governance of non-state-owned shareholders and executive compensation incentive in state-owned enterprises. Manag. World 2018, 34, 137–149. [Google Scholar]

- Newman, K.L. Organizational transformation during institutional upheaval. Acad. Manag. Rev. 2000, 25, 602–619. [Google Scholar] [CrossRef]

- Liu, Y.G.; Zheng, Q.; Cai, G.L. Does non-state-owned shareholders improve the quality of internal control of state-owned enterprises?-Evidence from state-owned listed companies. Account. Res. 2016, 11, 61–68. [Google Scholar]

- Liu, Q.L.; Luo, L.; He, W.F.; Chen, H.W. Nature of property rights, institutional environment and internal control. Account. Res. 2012, 4, 52–61. [Google Scholar]

- Xia, L.J.; Fang, Y.Q. Government control, governance environment and corporate value: Empirical evidence from China’s securities market. Econ. Res. J. 2005, 5, 40–51. [Google Scholar]

- Yue, X.M.; Li, S.; Shi, T.L. Discussion on the high income problem of monopoly industry. Soc. Sci. China 2010, 3, 77–93. [Google Scholar]

- Chen, C.M.; Sun, J.H. Background characteristics of entrepreneur population and diversification strategy choice: An empirical study based on panel data of Chinese listed companies. Manag. World 2008, 5, 124–133. [Google Scholar]

- Wang, F.S.; Sun, H.X. Ultimate controller, diversification strategy and cash holding level. Manag. World 2012, 7, 124–136. [Google Scholar]

- Peng, H.X.; Mao, X.S. Government innovation subsidy, corporate executives’ background and R&D investment: Empirical evidence from China’s high-tech industry. Financ. Trade Econ. 2017, 38, 147–161. [Google Scholar]

- Han, Z.X.; Cui, J.W.; Wang, S. Do technology executives improve the technical efficiency of enterprises? Stud. Sci. Sci. 2014, 32, 559–568. [Google Scholar]

- Baron, R.M.; Kenny, D.A. The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical consideration. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

{kind=link}

| Classification | Definition |

|---|---|

| State-owned shareholders | Shareholders formed by the state through direct control of government departments (Ministry of Finance, state-owned assets supervision and administration commission (SASAC), etc.) or through controlling industrial enterprises and government-owned management enterprises |

| Private shareholders | Shareholders formed by the investment of non-state-owned legal persons in China |

| Foreign shareholders | Shareholders formed by the investment of overseas legal persons, overseas natural persons, and foreign-invested enterprises |

| Natural person shareholders | Shareholders formed by the investment of natural persons or families in China |

| Institutional investors | Shareholders (Listed Open-ended Fund, Qualified Foreign Institutional Investor, insurance, fund, securities enterprises, financial institutions, etc.) formed by the securities investment of legal persons in the financial market |

| Others | Shareholders other than the above five categories |

| Type of Variable | Variable | Variable Symbol | Measurement of Variable |

|---|---|---|---|

| Explained variable | Exploratory innovation investment | Research expensed expenditure/Total assets at the fiscal year-begin × 100%. | |

| Exploitative innovation investment | Research capitalized expenditure/Total assets at the fiscal year-begin × 100%. | ||

| Explanatory variable | Diversity of mixed shareholders | The types of heterogeneous shareholders included in the top ten shareholders. If only one kind of shareholder is involved in the enterprise, the value of is 1; the value of two kinds is 2. By analogy, there can be at most five types of shareholders, where the value of is 5. | |

| Depth of mixed equity | The sum of the four non-state-owned shareholding ratios of private, foreign, and natural persons as well as institutional investors among the top ten shareholders. | ||

| Control of mixed equity | The proportion of directors, supervisors, and executives appointed by non-state-owned shareholders in the top ten shareholders. | ||

| The shareholding ratio of private shareholders | The sum of the shareholding ratios of private shareholders in the top ten shareholders. | ||

| The shareholding ratio of foreign shareholders | The sum of the shareholding ratios of foreign shareholders in the top ten shareholders. | ||

| The shareholding ratio of natural persons | The sum of the shareholding ratios of natural persons in the top ten shareholders. | ||

| The shareholding ratio of institutional investors | The sum of the shareholding ratios of institutional investors in the top ten shareholders. | ||

| Control variable | Company size | Natural logarithm value of total assets at the fiscal year-end. | |

| Leverage | The company’s total liabilities/Total assets at the fiscal year-end. | ||

| Growth | Percentage change in operating revenue over the fiscal year. | ||

| Profitability | The company’s total profits/Total assets at the fiscal year-end. | ||

| Free cash flow | Free cash flow scaled/Total assets at the fiscal year-end. | ||

| The scale of the board | Natural logarithm of the number of directors on the board. | ||

| The proportion of independent directors | The number of independent directors/The number of directors on the board. | ||

| Duality | Dummy variable, if the chairman concurrently serves as the general manager, take 1, otherwise, take 0. | ||

| Age of listed companies | Age of the company at the year of IPO. | ||

| Year | Year dummy variable | ||

| Industry | Industry dummy variable. |

| Variable | mean | sd | 1 | 2 | 3 | 4 | 5 | 6 |

| 1. | 1.148 | 1.672 | 1 | |||||

| 2. | 0.120 | 0.408 | 0.236 *** | 1 | ||||

| 3. | 2.918 | 1.033 | 0.021 | 0.004 | 1 | |||

| 4. | 0.114 | 0.106 | 0.046 *** | 0.030 ** | 0.342 *** | 1 | ||

| 5. | 0.021 | 0.057 | 0.135 *** | 0.081 *** | 0.063 *** | 0.374 *** | 1 | |

| 6. | 22.820 | 1.381 | −0.149 *** | −0.012 | 0.288 *** | 0.124 *** | −0.131 *** | 1 |

| 7. | 0.509 | 0.202 | −0.145 *** | −0.042 *** | 0.007 | −0.032 ** | −0.145 *** | 0.431 *** |

| 8. | 0.081 | 0.270 | 0.060 *** | 0.071 *** | 0.050 *** | 0.096 *** | 0.090 *** | 0.047 *** |

| 9. | 0.050 | 0.051 | 0.033 ** | 0.014 | 0.144 *** | 0.101 *** | 0.134 *** | 0.071 *** |

| 10. | 0.044 | 0.070 | 0.020 | −0.054 *** | 0.133 *** | 0.033 ** | 0.017 | 0.092 *** |

| 11. | 0.023 | 0.002 | −0.040 *** | 0.000 | 0.094 *** | 0.087 *** | 0.031 ** | 0.184 *** |

| 12. | 0.369 | 0.053 | −0.012 | 0.016 | 0.049 *** | −0.020 | −0.099 *** | 0.160 *** |

| 13. | 0.096 | 0.294 | −0.011 | −0.006 | 0.005 | 0.019 | 0.038 ** | −0.040 *** |

| 14. | 18.76 | 5.043 | −0.035 ** | −0.041 *** | 0.019 | 0.018 | 0.007 | −0.098 *** |

| Variable | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

| 7. | 1 | |||||||

| 8. | 0.022 | 1 | ||||||

| 9. | −0.303 *** | 0.214 *** | 1 | |||||

| 10. | −0.192 *** | 0.035 ** | 0.378 *** | 1 | ||||

| 11. | 0.060 *** | −0.008 | 0.019 | 0.068 *** | 1 | |||

| 12. | 0.077 *** | −0.009 | −0.048 *** | −0.022 | −0.384 *** | 1 | ||

| 13. | 0.004 | −0.006 | 0.017 | 0.007 | −0.079 *** | 0.061 *** | 1 | |

| 14. | 0.009 | 0.042 *** | 0.027 * | −0.031 ** | −0.032 ** | −0.073 *** | 0.025 * | 1 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 0.074 *** | 0.0001 | |||||

| (3.39) | (0.01) | |||||

| 0.476 ** | 0.028 | |||||

| (2.34) | (0.50) | |||||

| 2.313 *** | 0.365 *** | |||||

| (6.13) | (3.48) | |||||

| SIZE | −0.120 *** | 0.011 ** | −0.109 *** | 0.011 ** | −0.093 *** | 0.013 ** |

| (−5.96) | (2.04) | (−5.53) | (2.03) | (−4.77) | (2.39) | |

| −0.232 * | −0.024 | −0.248 * | −0.023 | −0.223 * | −0.017 | |

| (−1.72) | (−0.65) | (−1.84) | (−0.62) | (−1.66) | (−0.46) | |

| 0.298 *** | 0.098 *** | 0.288 *** | 0.097 *** | 0.270 *** | 0.093 *** | |

| (3.62) | (4.29) | (3.49) | (4.24) | (3.29) | (4.07) | |

| 1.554 *** | 0.318 ** | 1.590 *** | 0.314 ** | 1.341 *** | 0.269** | |

| (3.19) | (2.35) | (3.26) | (2.32) | (2.75) | (1.99) | |

| 0.461 | −0.480 *** | 0.549 | −0.479 *** | 0.605 * | −0.468 *** | |

| (1.36) | (−5.10) | (1.62) | (−5.09) | (1.79) | (−4.98) | |

| −9.512 | 1.125 | −8.840 | 1.012 | −9.393 | 0.733 | |

| (−0.69) | (0.29) | (−0.64) | (0.26) | (−0.68) | (0.19) | |

| −0.459 | 0.114 | −0.401 | 0.115 | −0.239 | 0.141 | |

| (−1.02) | (0.92) | (−0.89) | (0.92) | (−0.53) | (1.13) | |

| −0.081 | 0.0002 | −0.083 | −0.0001 | −0.100 | −0.003 | |

| (−1.13) | (0.01) | (−1.16) | (−0.00) | (−1.35) | (−0.14) | |

| −0.016 *** | −0.004 *** | −0.015 *** | −0.0036 *** | −0.014 *** | −0.004 *** | |

| (−3.51) | (−2.94) | (−3.43) | (−2.94) | (−3.29) | (−2.87) | |

| 3.501 *** | 0.306 | 3.331 *** | 0.311 | 2.784 *** | 0.234 | |

| (4.72) | (1.49) | (4.51) | (1.52) | (3.77) | (1.14) | |

| Control | control | control | control | control | control | |

| Control | control | control | control | control | control | |

| 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | |

| 0.296 | 0.091 | 0.295 | 0.091 | 0.300 | 0.094 | |

| 0.291 | 0.085 | 0.291 | 0.085 | 0.296 | 0.088 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 0.027 *** | 0.008 ** | |||||

| (4.24) | (2.35) | |||||

| 1.092 ** | −0.019 | |||||

| (2.53) | (−1.44) | |||||

| 0.332 ** | −0.096 | |||||

| (2.29) | (−0.52) | |||||

| SIZE | −0.474 *** | −0.049 *** | −0.492 *** | −0.048 *** | −0.473 *** | −0.048 *** |

| (−2.72) | (−4.13) | (−2.75) | (−4.01) | (−2.71) | (−3.88) | |

| −0.207 ** | 0.055 | −0.036 | 0.052 | −0.206 ** | 0.054 | |

| (−2.06) | (1.34) | (−0.37) | (1.30) | (−2.04) | (1.29) | |

| 0.116 * | 0.006 | 0.101 | 0.008 | 0.118 * | 0.008 | |

| (1.75) | (0.24) | (1.46) | (0.30) | (1.76) | (0.31) | |

| −0.180 | 0.106 ** | −0.154 | 0.105 ** | −0.196 | 0.109 ** | |

| (−0.65) | (2.16) | (−0.60) | (2.19) | (−0.71) | (2.20) | |

| 0.137 | −0.027 | 0.149 | −0.0230 | 0.158 | −0.025 | |

| (1.08) | (−0.88) | (1.16) | (−0.71) | (1.24) | (−0.91) | |

| −35.940 ** | −5.048 * | −36.220 ** | −4.663 | −34.760 ** | −4.680 | |

| (−2.41) | (−1.68) | (−2.35) | (−1.56) | (−2.40) | (−1.56) | |

| −0.703 * | −0.002 | −0.644 | 0.0004 | −0.680 * | −0.002 | |

| (−1.73) | (−0.02) | (−1.64) | (0.00) | (−1.71) | (−0.02) | |

| −0.054 * | −0.039 *** | −0.049 * | −0.039 *** | −0.052 * | −0.039 *** | |

| (−1.91) | (−3.35) | (−1.74) | (−3.34) | (−1.86) | (−3.33) | |

| 0.137 *** | 0.011 *** | 0.138 *** | 0.012 *** | 0.139 *** | 0.011 *** | |

| (9.12) | (6.74) | (9.30) | (6.69) | (9.47) | (7.68) | |

| 10.320 *** | 1.106 *** | 10.570 *** | 1.095 *** | 10.290 *** | 1.102 *** | |

| (2.60) | (3.34) | (2.63) | (3.28) | (2.59) | (3.31) | |

| 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | |

| 989 | 989 | 989 | 989 | 989 | 989 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| −1.199 | 0.211 | |||||||

| (−1.53) | (0.97) | |||||||

| 0.904 *** | −0.087 | |||||||

| (2.89) | (−1.00) | |||||||

| 1.450 ** | 0.273 | |||||||

| (2.40) | (1.63) | |||||||

| 1.160 ** | 0.536 *** | |||||||

| (2.27) | (3.81) | |||||||

| −0.105 *** | 0.012 ** | −0.121 *** | 0.013 ** | −0.092 *** | 0.014 ** | −0.108 *** | 0.009 * | |

| (−5.36) | (2.19) | (−5.89) | (2.32) | (−4.58) | (2.44) | (−5.49) | (1.67) | |

| −0.273 ** | −0.024 | −0.238 * | −0.027 | −0.269 ** | −0.024 | −0.267 ** | −0.023 | |

| (−2.02) | (−0.63) | (−1.76) | (−0.73) | (−2.00) | (−0.64) | (−1.98) | (−0.63) | |

| 0.313 *** | 0.096 *** | 0.309 *** | 0.097 *** | 0.285 *** | 0.094 *** | 0.297 *** | 0.095 *** | |

| (3.78) | (4.20) | (3.75) | (4.27) | (3.45) | (4.12) | (3.60) | (4.17) | |

| 1.685 *** | 0.311 ** | 1.670 *** | 0.316 ** | 1.627 *** | 0.313 ** | 1.570 *** | 0.281 ** | |

| (3.46) | (2.30) | (3.43) | (2.34) | (3.34) | (2.33) | (3.22) | (2.09) | |

| 0.516 | −0.478 *** | 0.495 | −0.477 *** | 0.587 * | −0.467 *** | 0.550 | −0.469 *** | |

| (1.52) | (−5.08) | (1.46) | (−5.07) | (1.73) | (−4.98) | (1.62) | (−5.02) | |

| −5.703 | 0.918 | −8.118 | 1.245 | −6.638 | 1.123 | −6.722 | 1.153 | |

| (−0.41) | (0.24) | (−0.59) | (0.32) | (−0.48) | (0.29) | (−0.48) | (0.30) | |

| −0.406 | 0.114 | −0.407 | 0.114 | −0.399 | 0.114 | −0.398 | 0.117 | |

| (−0.90) | (0.92) | (−0.91) | (0.92) | (−0.89) | (0.92) | (−0.89) | (0.95) | |

| −0.075 | −0.0003 | −0.081 | 0.0006 | −0.083 | −0.0008 | −0.079 | −0.0002 | |

| (−1.04) | (−0.01) | (−1.13) | (0.03) | (−1.15) | (−0.04) | (−1.09) | (−0.01) | |

| −0.015 *** | −0.004 *** | −0.015 *** | −0.004 *** | −0.015 *** | −0.004 *** | −0.015 *** | −0.003 *** | |

| (−3.40) | (−2.93) | (−3.49) | (−2.90) | (−3.37) | (−2.91) | (−3.32) | (−2.81) | |

| 3.318 *** | 0.293 | 3.631 *** | 0.269 | 2.955 *** | 0.253 | 3.275 *** | 0.322 | |

| (4.49) | (1.43) | (4.84) | (1.29) | (3.95) | (1.23) | (4.44) | (1.58) | |

| control | control | Control | control | control | control | control | control | |

| control | control | Control | control | control | control | control | control | |

| 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | |

| 0.295 | 0.092 | 0.296 | 0.092 | 0.295 | 0.092 | 0.295 | 0.095 | |

| 0.290 | 0.086 | 0.291 | 0.086 | 0.291 | 0.086 | 0.290 | 0.089 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 0.217 *** | 0.012 | |||||

| (4.95) | (0.52) | |||||

| 1.905 *** | −0.082 | |||||

| (4.78) | (−0.36) | |||||

| 3.537 *** | 1.621 *** | |||||

| (4.84) | (3.84) | |||||

| −0.220 *** | −0.077 *** | −0.190 *** | −0.073 *** | −0.149 *** | −0.066 *** | |

| (−5.62) | (−3.27) | (−5.00) | (−3.17) | (−3.95) | (−2.91) | |

| −0.162 | −0.219 | −0.255 | −0.227 | −0.258 | −0.194 | |

| (−0.59) | (−1.47) | (−0.93) | (−1.52) | (−0.94) | (−1.30) | |

| 0.244 | 0.324 *** | 0.216 | 0.328 *** | 0.149 | 0.314 *** | |

| (1.45) | (3.66) | (1.28) | (3.69) | (0.88) | (3.55) | |

| 3.601 *** | 0.375 | 3.483 *** | 0.410 | 3.320 *** | 0.163 | |

| (3.99) | (0.67) | (3.85) | (0.74) | (3.66) | (0.29) | |

| 0.884 | 0.486 | 1.283 * | 0.494 | 1.235 * | 0.532 | |

| (1.33) | (1.29) | (1.93) | (1.31) | (1.86) | (1.41) | |

| 50.530 * | −30.740 ** | 48.240 * | −29.760 ** | 51.120 * | −32.660 ** | |

| (1.73) | (−2.04) | (1.65) | (−1.98) | (1.75) | (−2.18) | |

| 0.347 | −0.799 | 0.537 | −0.786 | 0.582 | −0.660 | |

| (0.41) | (−1.55) | (0.63) | (−1.53) | (0.69) | (−1.29) | |

| 0.283 * | −0.130 * | 0.258 | −0.128 * | 0.247 | −0.141 * | |

| (1.68) | (−1.76) | (1.53) | (−1.74) | (1.46) | (−1.91) | |

| −0.025 *** | −0.002 | −0.024 *** | −0.0015 | −0.021 ** | −0.001 | |

| (−2.69) | (−0.33) | (−2.65) | (−0.31) | (−2.33) | (−0.29) | |

| 5.324 *** | 2.889 *** | 5.007 *** | 2.831 *** | 4.027 *** | 2.671 *** | |

| (4.33) | (4.60) | (4.09) | (4.52) | (3.29) | (4.28) | |

| control | control | control | control | control | control | |

| control | control | control | control | control | control | |

| 1534 | 3016 | 1534 | 3016 | 1534 | 3016 | |

| 0.322 | 0.278 | 0.321 | 0.278 | 0.321 | 0.282 | |

| 0.308 | 0.271 | 0.308 | 0.271 | 0.308 | 0.275 | |

| central | local | central | local | central | local |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 0.073 | 0.069 *** | |||||

| (1.61) | (2.92) | |||||

| 0.252 | 0.467 ** | |||||

| (0.51) | (2.13) | |||||

| −0.447 | 2.344 *** | |||||

| (−0.41) | (5.83) | |||||

| −0.053 | −0.125 *** | −0.038 | −0.115 *** | −0.036 | −0.099 *** | |

| (−1.43) | (−5.52) | (−1.06) | (−5.19) | (−1.02) | (−4.51) | |

| −0.098 | −0.266 * | −0.115 | −0.279 * | −0.136 | −0.254 * | |

| (−0.35) | (−1.79) | (−0.41) | (−1.88) | (−0.48) | (−1.72) | |

| 0.037 | 0.317 *** | 0.036 | 0.306 *** | 0.045 | 0.288 *** | |

| (0.19) | (3.57) | (0.18) | (3.45) | (0.23) | (3.26) | |

| 1.039 | 1.458 *** | 1.063 | 1.486 *** | 1.045 | 1.215 ** | |

| (0.80) | (2.79) | (0.82) | (2.84) | (0.80) | (2.32) | |

| −1.089 | 0.548 | −0.965 | 0.631 * | −1.028 | 0.666 * | |

| (−1.18) | (1.51) | (−1.05) | (1.74) | (−1.10) | (1.84) | |

| 45.920 * | −15.690 | 52.320 ** | −15.700 | 54.780 ** | −16.660 | |

| (1.72) | (−1.02) | (1.97) | (−1.02) | (2.08) | (−1.09) | |

| 2.222 ** | −0.758 | 2.373 ** | −0.709 | 2.389 ** | −0.532 | |

| (2.22) | (−1.56) | (2.38) | (−1.46) | (2.40) | (−1.09) | |

| 0.071 | −0.084 | 0.092 | −0.088 | 0.098 | −0.105 | |

| (0.51) | (−1.06) | (0.66) | (−1.11) | (0.71) | (−1.33) | |

| −0.040 *** | −0.014 *** | −0.038 *** | −0.014 *** | −0.039 *** | −0.013 *** | |

| (−3.59) | (−2.91) | (−3.48) | (−2.86) | (−3.48) | (−2.75) | |

| 0.074 | 4.394 *** | −0.314 | 4.268 *** | −0.371 | 3.720 *** | |

| (0.07) | (5.47) | (−0.31) | (5.33) | (−0.37) | (4.64) | |

| control | control | control | control | control | control | |

| control | control | control | control | control | control | |

| 506 | 4044 | 506 | 4044 | 506 | 4044 | |

| 0.333 | 0.282 | 0.329 | 0.281 | 0.329 | 0.286 | |

| 0.309 | 0.276 | 0.306 | 0.276 | 0.306 | 0.281 | |

| monopoly | competitive | monopoly | competitive | monopoly | competitive |

| 0.169 *** | −0.005 | ||||||||

| (2.78) | (−0.34) | ||||||||

| 1.382 *** | 0.201 ** | ||||||||

| (4.07) | (2.45) | ||||||||

| 3.566 *** | 0.794 *** | ||||||||

| (5.40) | (4.97) | ||||||||

| 0.471 *** | 0.797 *** | 0.758 *** | |||||||

| (31.78) | (82.05) | (80.89) | |||||||

| 0.125 *** | −0.212 *** | 0.003 | 0.004 *** | −0.191 *** | −0.00126 | −0.0002 | −0.162 *** | 0.004 | |

| (9.42) | (−7.42) | (0.38) | (4.98) | (−7.59) | (−0.21) | (−0.44) | (−6.54) | (0.64) | |

| −0.179 ** | −0.550 *** | −0.109 *** | −0.016 *** | −0.557 *** | −0.096 ** | −0.007 ** | −0.560 *** | −0.092 ** | |

| (−2.04) | (−3.20) | (−2.62) | (−2.64) | (−3.27) | (−2.34) | (−2.10) | (−3.31) | (−2.24) | |

| 0.139 ** | 0.479 *** | 0.126 *** | 0.012 *** | 0.456 *** | 0.120 *** | 0.005 *** | 0.446 *** | 0.114 *** | |

| (2.54) | (4.54) | (4.96) | (3.11) | (4.31) | (4.69) | (2.77) | (4.23) | (4.49) | |

| 1.307 *** | −0.290 | 0.172 | 0.041 * | −0.083 | 0.148 | 0.022* | −0.309 | 0.090 | |

| (3.89) | (−0.44) | (1.08) | (1.78) | (−0.13) | (0.95) | (1.82) | (−0.48) | (0.58) | |

| 0.538 ** | 0.0419 | −0.475 *** | −0.032 ** | 0.212 | −0.472 *** | −0.003 | 0.233 | −0.464 *** | |

| (2.35) | (0.09) | (−4.43) | (−2.01) | (0.48) | (−4.42) | (−0.38) | (0.53) | (−4.35) | |

| 20.118 ** | −11.42 | 4.718 | −0.272 | −11.50 | 3.858 | 0.126 | −9.984 | 3.815 | |

| (2.12) | (−0.62) | (1.06) | (0.41) | (−0.62) | (0.87) | (0.37) | (−0.55) | (0.86) | |

| 0.384 | 0.334 | 0.108 | 0.021 | 0.423 | 0.104 | −0.017 | 0.660 | 0.156 | |

| (1.24) | (0.56) | (0.75) | (0.97) | (0.71) | (0.72) | (−1.52) | (1.11) | (1.08) | |

| 0.054 | −0.166 * | 0.010 | −0.003 | −0.166 * | 0.008 | −0.001 | −0.175 * | 0.005 | |

| (1.09) | (−1.74) | (0.44) | (−0.97) | (−1.75) | (0.34) | (−0.35) | (−1.86) | (0.21) | |

| 0.005 | −0.022 *** | −0.005 *** | 0.0003 | −0.022 *** | −0.005 *** | 0.0001 | −0.020 *** | −0.005 *** | |

| (1.57) | (−3.94) | (−3.40) | (1.55) | (−3.85) | (−3.58) | (0.57) | (−3.64) | (−3.45) | |

| −1.971 *** | 6.401 *** | 0.078 | −0.077 *** | 6.207 *** | 0.150 | 0.012 | 5.490 *** | 0.020 | |

| (−5.64) | (9.12) | (0.46) | (−3.19) | (9.17) | (0.92) | (0.99) | (8.19) | (0.12) | |

| control | control | control | control | control | control | control | control | control | |

| control | control | control | control | control | control | control | control | control | |

| 3566 | 3566 | 3566 | 3566 | 3566 | 3566 | 3566 | 3566 | 3566 | |

| 0.314 | 0.041 | 0.017 | 0.670 | 0.042 | 0.017 | 0.663 | 0.051 | 0.024 | |

| 0.312 | 0.038 | 0.015 | 0.669 | 0.039 | 0.014 | 0.662 | 0.048 | 0.021 | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 0.087 ** | 0.001 | |||||

| (2.30) | (0.07) | |||||

| 1.034 *** | 0.178 | |||||

| (2.71) | (1.53) | |||||

| 6.105 *** | 0.828 *** | |||||

| (9.36) | (4.15) | |||||

| −0.154 *** | 0.029 *** | −0.147 *** | 0.027 *** | −0.107 *** | 0.033 *** | |

| (−4.38) | (2.74) | (−4.27) | (2.60) | (−3.19) | (3.19) | |

| −1.909 *** | −0.127 * | −1.912 *** | −0.121 * | −1.832 *** | −0.111 | |

| (−8.13) | (−1.78) | (−8.15) | (−1.70) | (−7.88) | (−1.57) | |

| 0.433 *** | 0.188 *** | 0.407 *** | 0.183 *** | 0.353 ** | 0.177 *** | |

| (3.03) | (4.34) | (2.84) | (4.21) | (2.49) | (4.07) | |

| −0.827 | 0.270 | −0.840 | 0.250 | −1.527 * | 0.161 | |

| (−0.98) | (1.05) | (−0.99) | (0.97) | (−1.81) | (0.63) | |

| −1.287 ** | −1.089 *** | −1.165 ** | −1.081 *** | −1.007 * | −1.061 *** | |

| (−2.18) | (−6.07) | (−1.98) | (−6.04) | (−1.72) | (−5.94) | |

| 2.754 | −2.627 | 2.004 | −3.260 | −0.762 | −3.497 | |

| (0.11) | (−0.36) | (0.08) | (−0.44) | (−0.03) | (−0.48) | |

| −0.717 | 0.149 | −0.645 | 0.151 | −0.211 | 0.209 | |

| (−0.92) | (0.63) | (−0.83) | (0.64) | (−0.27) | (0.88) | |

| −0.062 | 0.021 | −0.072 | 0.018 | −0.108 | 0.014 | |

| (−0.49) | (0.55) | (−0.58) | (0.48) | (−0.87) | (0.37) | |

| −0.029 *** | −0.006 ** | −0.029 *** | −0.006 *** | −0.027 *** | −0.006 ** | |

| (−3.84) | (−2.58) | (−3.78) | (−2.59) | (−3.61) | (−2.50) | |

| 5.753 *** | 0.480 | 5.619 *** | 0.506 | 4.237 *** | 0.312 | |

| (4.46) | (1.23) | (4.38) | (1.30) | (3.32) | (0.80) | |

| control | control | control | control | control | control | |

| control | control | control | control | control | control | |

| 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | |

| 0.304 | 0.090 | 0.304 | 0.090 | 0.317 | 0.093 | |

| 0.299 | 0.084 | 0.300 | 0.084 | 0.312 | 0.087 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 0.313 * | −0.014 | |||||

| (1.92) | (−0.32) | |||||

| 0.217 *** | 0.080 *** | |||||

| (2.75) | (3.69) | |||||

| 0.274 *** | 0.009 | |||||

| (4.78) | (0.55) | |||||

| −0.102 *** | 0.011 ** | −0.103 *** | 0.011 ** | −0.096 *** | 0.012 ** | |

| (−5.24) | (2.12) | (−5.28) | (2.10) | (−4.91) | (2.16) | |

| −0.258* | −0.024 | −0.253 * | −0.018 | −0.246 * | −0.023 | |

| (−1.91) | (−0.65) | (−1.88) | (−0.49) | (−1.83) | (−0.62) | |

| 0.301 *** | 0.097 *** | 0.278 *** | 0.088 *** | 0.280 *** | 0.097 *** | |

| (3.66) | (4.28) | (3.36) | (3.87) | (3.40) | (4.24) | |

| 1.665 *** | 0.316 ** | 1.601 *** | 0.300 ** | 1.426 *** | 0.310 ** | |

| (3.42) | (2.36) | (3.29) | (2.23) | (2.92) | (2.30) | |

| 0.519 | −0.478 *** | 0.565 * | −0.465 *** | 0.558* | −0.477 *** | |

| (1.53) | (−5.11) | (1.67) | (−4.97) | (1.65) | (−5.10) | |

| −8.429 | 1.146 | −8.809 | 0.366 | −9.265 | 1.000 | |

| (−0.61) | (0.30) | (−0.63) | (0.10) | (−0.67) | (0.26) | |

| −0.424 | 0.114 | −0.426 | 0.106 | −0.255 | 0.118 | |

| (−0.94) | (0.92) | (−0.95) | (0.86) | (−0.57) | (0.95) | |

| −0.077 | 0.0002 | −0.091 | −0.005 | −0.091 | −0.0002 | |

| (−1.08) | (0.01) | (−1.27) | (−0.25) | (−1.27) | (−0.01) | |

| −0.015 *** | −0.004 *** | −0.016 *** | −0.004 *** | −0.015 *** | −0.004 *** | |

| (−3.44) | (−2.92) | (−3.53) | (−3.12) | (−3.46) | (−2.94) | |

| 3.087 *** | 0.315 | 3.126 *** | 0.264 | 2.876 *** | 0.296 | |

| (4.16) | (1.54) | (4.23) | (1.30) | (3.89) | (1.45) | |

| control | control | control | control | control | Control | |

| control | control | control | control | control | Control | |

| 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | |

| 0.295 | 0.092 | 0.296 | 0.094 | 0.298 | 0.092 | |

| 0.290 | 0.086 | 0.291 | 0.088 | 0.293 | 0.086 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| 0.120 *** | 0.009 | |||||

| (4.67) | (1.32) | |||||

| 0.503 ** | 0.058 | |||||

| (2.11) | (0.91) | |||||

| 1.797 *** | 0.117 | |||||

| (4.02) | (0.98) | |||||

| −0.159 *** | −0.001 | −0.135 *** | 0.001 | −0.120 *** | 0.002 | |

| (−6.74) | (−0.16) | (−5.88) | (0.10) | (−5.25) | (0.31) | |

| 0.150 | −0.059 | 0.101 | −0.062 | 0.119 | −0.062 | |

| (0.89) | (−1.33) | (0.60) | (−1.40) | (0.71) | (−1.39) | |

| 0.247 ** | 0.124 *** | 0.248 ** | 0.123 *** | 0.242 ** | 0.124 *** | |

| (2.40) | (4.52) | (2.39) | (4.47) | (2.35) | (4.51) | |

| 1.587 *** | 0.232 | 1.688 *** | 0.238 | 1.512 ** | 0.228 | |

| (2.67) | (1.46) | (2.83) | (1.50) | (2.53) | (1.44) | |

| 0.746 * | −0.494 *** | 0.883 ** | −0.483 *** | 0.901 ** | −0.483 *** | |

| (1.83) | (−4.55) | (2.16) | (−4.45) | (2.21) | (−4.46) | |

| −20.730 | 0.111 | −17.240 | 0.288 | −16.750 | 0.428 | |

| (−1.29) | (0.03) | (−1.07) | (0.07) | (−1.04) | (0.10) | |

| −0.806 | 0.003 | −0.692 | 0.011 | −0.538 | 0.021 | |

| (−1.54) | (0.02) | (−1.32) | (0.08) | (−1.02) | (0.15) | |

| −0.092 | −0.042* | −0.091 | −0.042* | −0.092 | −0.042 * | |

| (−1.02) | (−1.75) | (−1.00) | (−1.75) | (−1.02) | (−1.74) | |

| −0.013 ** | −0.003 ** | −0.012 ** | −0.003 ** | −0.012 ** | −0.003 ** | |

| (−2.43) | (−2.41) | (−2.35) | (−2.40) | (−2.25) | (−2.36) | |

| 5.650 *** | 0.111 | 5.199 *** | 0.083 | 4.797 *** | 0.049 | |

| (6.60) | (0.49) | (6.10) | (0.37) | (5.65) | (0.22) | |

| control | control | control | control | control | Control | |

| control | control | control | control | control | Control | |

| 3148 | 3148 | 3148 | 3148 | 3148 | 3148 | |

| 0.321 | 0.099 | 0.317 | 0.099 | 0.319 | 0.099 | |

| 0.314 | 0.091 | 0.310 | 0.090 | 0.313 | 0.090 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

|---|---|---|---|---|---|---|---|---|---|

| 0.074 *** | 0.004 ** | 0.064 *** | |||||||

| (3.39) | (2.03) | (3.03) | |||||||

| 2.591 *** | |||||||||

| (14.58) | |||||||||

| 0.478 ** | 0.037 ** | 0.381 * | |||||||

| (2.17) | (2.07) | (1.77) | |||||||

| 2.598 *** | |||||||||

| (14.61) | |||||||||

| 2.313 *** | 0.161 *** | 1.905 *** | |||||||

| (6.13) | (5.21) | (5.15) | |||||||

| 2.537 *** | |||||||||

| (14.27) | |||||||||

| −0.120 *** | −0.003 ** | −0.112 *** | −0.109 *** | −0.003 * | −0.101 *** | −0.093 *** | −0.002 | −0.088 *** | |

| (−5.96) | (−2.09) | (−5.65) | (−5.52) | (−1.90) | (−5.23) | (−4.77) | (−1.20) | (−4.62) | |

| −0.232 * | −0.010 | −0.206 | −0.250 * | −0.010 | −0.223 * | −0.223 * | −0.009 | −0.201 | |

| (−1.72) | (−0.91) | (−1.56) | (−1.85) | (−0.94) | (−1.69) | (−1.66) | (−0.78) | (−1.53) | |

| 0.298 *** | 0.007 | 0.279 *** | 0.288 *** | 0.006 | 0.271 *** | 0.270 *** | 0.005 | 0.257 *** | |

| (3.62) | (1.09) | (3.47) | (3.49) | (0.95) | (3.36) | (3.29) | (0.79) | (3.19) | |

| 1.554 *** | 0.141 *** | 1.189 ** | 1.591 *** | 0.141 *** | 1.225 ** | 1.341 *** | 0.124 *** | 1.026 ** | |

| (3.19) | (3.53) | (2.50) | (3.26) | (3.54) | (2.57) | (2.75) | (3.11) | (2.15) | |

| 0.461 | −0.049 * | 0.588 * | 0.549 | −0.044 | 0.664 ** | 0.605 * | −0.041 | 0.708 ** | |

| (1.36) | (−1.77) | (1.77) | (1.62) | (−1.60) | (2.00) | (1.79) | (−1.47) | (2.14) | |

| −9.512 | 6.355 *** | −25.980 * | −8.664 | 6.345 *** | −25.150 * | −9.393 | 6.309 *** | −25.400 * | |

| (−0.69) | (5.60) | (−1.91) | (−0.62) | (5.59) | (−1.85) | (−0.68) | (5.58) | (−1.87) | |

| −0.459 | −0.063 * | −0.295 | −0.402 | −0.060 * | −0.245 | −0.239 | −0.049 | −0.114 | |

| (−1.02) | (−1.73) | (−0.67) | (−0.90) | (−1.65) | (−0.56) | (−0.53) | (−1.34) | (−0.26) | |

| −0.081 | −0.010 * | −0.054 | −0.084 | −0.011 * | −0.056 | −0.097 | −0.012 ** | −0.067 | |

| (−1.13) | (−1.77) | (−0.77) | (−1.17) | (−1.82) | (−0.80) | (−1.35) | (−1.97) | (−0.96) | |

| −0.016 *** | −0.003 *** | −0.008 * | −0.015 *** | −0.003 *** | −0.008 * | −0.014 *** | −0.003 *** | −0.007 * | |

| (−3.51) | (−7.91) | (−1.86) | (−3.41) | (−7.86) | (−1.77) | (−3.29) | (−7.77) | (−1.70) | |

| 3.501 *** | 0.040 | 3.396 *** | 3.322 *** | 0.034 | 3.233 *** | 2.784 *** | −0.004 | 2.794 *** | |

| (4.72) | (0.67) | (4.69) | (4.50) | (0.56) | (4.48) | (3.77) | (−0.07) | (3.87) | |

| control | control | control | control | control | control | control | control | control | |

| control | control | control | control | control | control | control | control | control | |

| 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | 4550 | |

| 0.296 | 0.240 | 0.328 | 0.295 | 0.240 | 0.327 | 0.300 | 0.244 | 0.330 | |

| 0.291 | 0.235 | 0.323 | 0.290 | 0.235 | 0.322 | 0.296 | 0.239 | 0.326 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, C.; Yuan, R.; Khan, M.A.; Pervaiz, K.; Sun, X. Does the Mixed-Ownership Reform Affect the Innovation Strategy Choices of Chinese State-Owned Enterprises? Sustainability 2020, 12, 2587. https://doi.org/10.3390/su12072587

Li C, Yuan R, Khan MA, Pervaiz K, Sun X. Does the Mixed-Ownership Reform Affect the Innovation Strategy Choices of Chinese State-Owned Enterprises? Sustainability. 2020; 12(7):2587. https://doi.org/10.3390/su12072587

Chicago/Turabian StyleLi, Chunling, Runsen Yuan, Muhammad Asif Khan, Khansa Pervaiz, and Xiaoran Sun. 2020. "Does the Mixed-Ownership Reform Affect the Innovation Strategy Choices of Chinese State-Owned Enterprises?" Sustainability 12, no. 7: 2587. https://doi.org/10.3390/su12072587