Comparative Study of Service Quality on VIP Customer Satisfaction in Internet Banking: South Korea Case

Abstract

:1. Introduction

2. Theoretical Background

2.1. VIP Internet Banking Services

2.2. Service Quality in Internet Banking

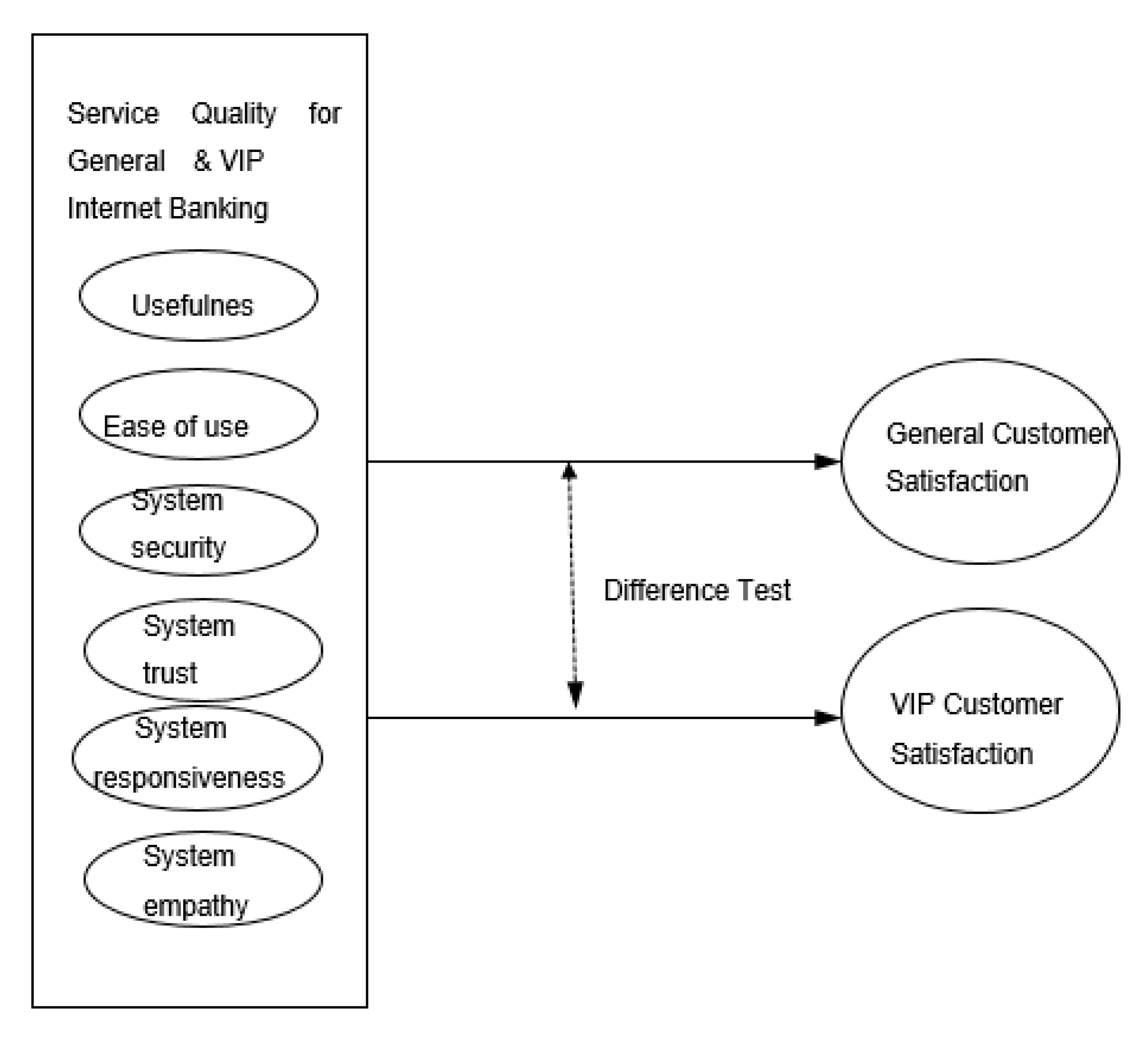

3. Research Model

4. Research Methods

Data Collection

5. Results

5.1. Measurement Properties

5.2. Results and Discussion

6. Conclusions

6.1. Summary of Findings

6.2. Implications for Research

6.3. Implications for Practice

Author Contributions

Conflicts of Interest

References

- Goh, K.H.; Kauffman, R.J. Firm strategy and the Internet in U.S. commercial banking. J. Manag. Inf. Syst. 2013, 30, 9–40. [Google Scholar] [CrossRef]

- Liu, D.-Y.; Chen, S.-W.; Chou, T.-C. Resource fit in digital transformation. Manag. Decis. 2011, 49, 1728–1742. [Google Scholar] [CrossRef]

- Keller, K.L. Managing the growth tradeoff: Challenges and opportunities in luxury branding. J. Brand Manag. 2009, 16, 290–301. [Google Scholar] [CrossRef]

- Tynan, C.; McKechnie, S.; Chhuon, C. Co-creating value for luxury brands. J. Bus. Res. 2010, 63, 1156–1163. [Google Scholar] [CrossRef]

- Im, I.; Hong, S.; Kang, M.S. An international comparison of technology adoption: Testing the UTAUT model. Inf. Manag. 2011, 48, 1–8. [Google Scholar] [CrossRef]

- Lee, K.-W.; Tsai, M.-T.; Lanting, M.C.L. From marketplace to marketspace: Investigating the consumer switch to online banking. Electron. Commer. Res. Appl. 2011, 10, 115–125. [Google Scholar] [CrossRef]

- Lee, M.-C. Factors influencing the adoption of internet banking: An integration of TAM and TPB with perceived risk and perceived benefit. Electron. Commer. Res. Appl. 2009, 8, 130–141. [Google Scholar] [CrossRef]

- Martins, C.; Oliveira, T.; Popovič, A. Understanding the Internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. Int. J. Inf. Manag. 2014, 34, 1–13. [Google Scholar] [CrossRef]

- Montazemi, A.R.; Qahri-Saremi, H. Factors affecting adoption of online banking: A meta-analytic structural equation modeling study. Inf. Manag. 2015, 52, 210–226. [Google Scholar] [CrossRef]

- Riffai, M.M.M.A.; Grant, K.; Edgar, D. Big TAM in Oman: Exploring the promise of on-line banking, its adoption by customers and the challenges of banking in Oman. Int. J. Inf. Manag. 2012, 32, 239–250. [Google Scholar] [CrossRef]

- Takieddine, S.; Sun, J. Internet banking diffusion: A country-level analysis. Electron. Commer. Res. Appl. 2015, 14, 361–371. [Google Scholar] [CrossRef]

- Tassabehji, R.; Kamala, M.A. Evaluating biometrics for online banking: The case for usability. Int. J. Inf. Manag. 2012, 32, 489–494. [Google Scholar] [CrossRef]

- Yoon, C. Antecedents of customer satisfaction with online banking in China: The effects of experience. Comput. Hum. Behav. 2010, 26, 1296–1304. [Google Scholar] [CrossRef]

- Yoon, H.S.; Steege, L.M.B. Development of a quantitative model of the impact of customers’ personality and perceptions on Internet banking use. Comput. Hum. Behav. 2013, 29, 1133–1141. [Google Scholar] [CrossRef]

- Al-Ajam, A.S.; Nor, K.M. Challenges of adoption of internet banking service in Yemen. Int. J. Bank Mark. 2015, 33, 178–194. [Google Scholar] [CrossRef]

- Amin, M. Internet banking service quality and its implication on e-customer satisfaction and e-customer loyalty. Int. J. Bank Mark. 2016, 34, 280–306. [Google Scholar] [CrossRef]

- Marafon, D.L.; Basso, K.; Espartel, L.B.; Barcellos, M.D.; Eduardo Rech, E. Perceived risk and intention to use internet banking: The effects of self confidence and risk acceptance. Int. J. Bank Mark. 2018, 36, 277–289. [Google Scholar] [CrossRef]

- Namahoot, K.S.; Laohavichien, T. Assessing the intentions to use internet banking: The role of perceived risk and trust as mediating factors. Int. J. Bank Mark. 2018, 36, 256–276. [Google Scholar] [CrossRef]

- Patel, K.J.; Patel, H.J. Adoption of internet banking services in Gujarat: An extension of TAM with perceived security and social influence. Int. J. Bank Mark. 2018, 36, 147–169. [Google Scholar] [CrossRef]

- Rawashdeh, A. Factors affecting adoption of internet banking in Jordan: Chartered accountant’s perspective. Int. J. Bank Mark. 2015, 33, 510–529. [Google Scholar] [CrossRef]

- Yadav, R.; Chauhan, V.; Pathak, G.S. Intention to adopt internet banking in an emerging economy: A perspective of Indian youth. Int. J. Bank Mark. 2015, 33, 530–544. [Google Scholar] [CrossRef]

- Choi, E.; Ko, E.; Kim, A.J. Explaining and predicting purchase intentions following luxury-fashion brand value co-creation encounters. J. Bus. Res. 2016, 69, 5827–5832. [Google Scholar] [CrossRef]

- Cristini, H.; Kauppinen-Räisänen, H.; Barthod-Prothade, M.; Woodside, A. Toward a general theory of luxury: Advancing from workbench definitions and theoretical transformations. J. Bus. Res. 2017, 70, 101–107. [Google Scholar] [CrossRef]

- Kang, Y.-J.; Park, S.-Y. The perfection of the narcissistic self: A qualitative study on luxury consumption and customer equity. J. Bus. Res. 2016, 69, 3813–3819. [Google Scholar] [CrossRef]

- Shukla, P.; Banerjee, M.; Singh, J. Customer commitment to luxury brands: Antecedents and consequences. J. Bus. Res. 2016, 69, 323–331. [Google Scholar] [CrossRef] [Green Version]

- Hanafizadeh, P.; Keating, B.W.; Khedmatgozar, H.R. A systematic review of Internet banking adoption. Telemat. Inform. 2014, 31, 492–510. [Google Scholar] [CrossRef]

- Leonardi, P.M.; Bailey, D.E.; Diniz, E.H.; Sholler, D.; Nardi, B. Multiplex appropriation in complex systems implementation: The case of Brazil’s correspondent banking system. MIS Q. 2016, 40, 461–474. [Google Scholar] [CrossRef]

- Kuo, T.H. The antecedents of customer relationship in e-banking industry. J. Comput. Inf. Syst. 2011, 51, 57–66. [Google Scholar]

- Shukla, P. Status consumption in cross-national context: Socio-psychological, brand and situational antecedents. Int. Mark. Rev. 2010, 27, 108–129. [Google Scholar] [CrossRef]

- Wiedmann, K.P.; Hennigs, N.; Siebels, A. Value-based segmentation of luxury consumption behavior. Psychol. Mark. 2009, 26, 625–651. [Google Scholar] [CrossRef]

- Kastanakis, M.N.; Balabanis, G. Between the mass and the class: Antecedents of the “bandwagon” luxury consumption behavior. J. Bus. Res. 2012, 65, 1399–1407. [Google Scholar] [CrossRef]

- Shukla, P. Impact of interpersonal influences, brand origin and brand image on luxury purchase intentions: Measuring interfunctional interactions and a cross-national comparison. J. World Bus. 2011, 46, 242–252. [Google Scholar] [CrossRef]

- Bazi, S.; Filieri, R.; Gorton, M. Customers’ motivation to engage with luxury brands on social media. J. Bus. Res. 2020, 112, 223–235. [Google Scholar] [CrossRef]

- Li, G.; Liu, H.; Li, G. Payment willingness for VIP subscription in social networking sites. J. Bus. Res. 2014, 67, 2179–2184. [Google Scholar] [CrossRef]

- Cheng, T.C.E.; Lam, D.Y.C.; Yeung, A.C.L. Adoption of internet banking: An empirical study in Hong Kong. Decis. Support Syst. 2006, 42, 1558–1572. [Google Scholar] [CrossRef] [Green Version]

- Shah, M.H.; Siddiqui, F.A. Organisational critical success factors in adoption of e-banking at the Woolwich bank. Int. J. Inf. Manag. 2006, 26, 442–456. [Google Scholar] [CrossRef]

- Vatanasombut, B.; Igbaria, M.; Stylianou, A.C.; Rodgers, W. Information systems continuance intention of web-based applications customers: The case of online banking. Inf. Manag. 2008, 45, 419–428. [Google Scholar] [CrossRef]

- Liao, Z.; Cheung, M.T. Measuring consumer satisfaction in Internet banking: A core framework. Commun. ACM 2008, 51, 47–51. [Google Scholar] [CrossRef]

- Compeau, D.R.; Wilson, T.D. Computer self-efficacy: Development of a measure and initial test. MIS Q. 1995, 19, 189–211. [Google Scholar] [CrossRef] [Green Version]

- Lee, K.C.; Jung, N. Exploring antecedents of behavior intention to use Internet banking in Korea: Adoption perspective. Int. J. E Adopt. 2009, 1, 30–47. [Google Scholar] [CrossRef]

- Chauhan, V.; Yadav, R.; Choudhary, V. Analyzing the impact of consumer innovativeness and perceived risk in internet banking adoption: A study of Indian consumers. Int. J. Bank Mark. 2019, 37, 323–339. [Google Scholar] [CrossRef]

- Asian Banker, Mobile Banking Seen to Overtake Internet Banking. Available online: http://www.theasianbanker.com/updates-and-articles/mobile-banking-seen-to-overtake-internet-banking (accessed on 3 August 2020).

- Internet Banking Transactions at New Record High in 2019. Available online: http://www.koreaherald.com/view.php?ud=20200412000286 (accessed on 3 August 2020).

- Joseph, I.N.; Rajendran, C.; Kamalanabhan, T.J. An instrument for measuring total quality management implementation in manufacturing-based business units in India. Int. J. Prod. Res. 1999, 37, 2201–2215. [Google Scholar] [CrossRef]

- Liao, C.-H.; Yen, H.R.; Li, E.Y. The effect of channel quality inconsistency on the association between e-service quality and customer relationships. Int. Res. 2011, 21, 458–478. [Google Scholar] [CrossRef] [Green Version]

- Carlson, J.; O’Cass, A. Developing a framework for understanding e-service quality, its antecedents, consequences, and mediators. Manag. Serv. Qual. 2011, 21, 264–286. [Google Scholar] [CrossRef]

- Thaichon, P.; Lobo, A.; Mitsis, A. An empirical model of home internet services quality in Thailand. Asia Pac. J. Mark. Logist. 2014, 26, 190–210. [Google Scholar] [CrossRef]

- Dospinescu, O.; Anastasiei, B.; Dospinescu, N. Key factors determining the expected benefit of customers when using bank cards: An analysis on millennials and generation Z in Romania. Symmetry 2019, 11, 1449. [Google Scholar] [CrossRef] [Green Version]

- Dospinescu, O. E-Wallet. A new technical approach. Acta Univ. Danub. 2012, 11, 84–94. [Google Scholar]

- Bontis, N.; Booker, L.D.; Serenko, A. The mediating effect of organizational reputation on customer loyalty and service recommendation in the banking industry. Manag. Decis. 2007, 45, 1426–1445. [Google Scholar] [CrossRef] [Green Version]

- Elliot, S.; Li, G.; Choi, C. Understanding service quality in a virtual travel community environment. J. Bus. Res. 2013, 66, 1153–1160. [Google Scholar] [CrossRef]

- Rha, J.-Y. Customer satisfaction and qualities in public service: An intermediary customer perspective. Serv. Ind. J. 2012, 32, 1883–1900. [Google Scholar] [CrossRef]

- Zhao, Y.L.; Benedetto, C.A.D. Designing service quality to survive: Empirical evidence from Chinese new ventures. J. Bus. Res. 2013, 66, 1098–1107. [Google Scholar] [CrossRef]

- Parasuraman, A.; Zeithaml, V.A.; Berry, L.L. A conceptual model of service quality and its implications for future research. J. Mark. 1985, 49, 41–50. [Google Scholar] [CrossRef]

- Parasuraman, A.; Zeithaml, V.A.; Berry, L.L. Refinement and reassessment of the SERVQUAL scale. J. Retail. 1991, 67, 420–450. [Google Scholar]

- George, A.; Kumar, G.S.G. Impact of service quality dimensions in internet banking on customer satisfaction. Decision 2014, 41, 73–85. [Google Scholar] [CrossRef]

- Zhu, Y.-Q.; Chen, H.-G. Service fairness and customer satisfaction in internet banking: Exploring the mediating effects of trust and customer value. Int. Res. 2012, 22, 482–498. [Google Scholar] [CrossRef]

- Zhang, L.; Zhu, J.; Liu, Q. A meta-analysis of mobile commerce adoption and the moderating effect of culture. Comput. Hum. Behav. 2012, 28, 1902–1911. [Google Scholar] [CrossRef]

- McLean, G. Examining the determents and outcomes of mobile app engagement—A longitudinal perspective. Comput. Hum. Behav. 2018, 84, 392–403. [Google Scholar] [CrossRef] [Green Version]

- Akter, S.; D’Ambra, J.; Ray, P. Development and validation of an instrument to measure user perceived service quality of mHealth. Inf. Manag. 2013, 50, 181–195. [Google Scholar] [CrossRef] [Green Version]

- Agarwal, R.; Karahanna, E. Time flies when you’re having fun: Cognitive absorption and beliefs about information technology usage. MIS Q. 2000, 24, 665–694. [Google Scholar] [CrossRef]

- Kang, J.-Y.M.; Mun, J.M.; Johnson, K.K.P. In-store mobile usage: Downloading and usage intention toward mobile location-based retail apps. Comput. Hum. Behav. 2015, 46, 210–217. [Google Scholar] [CrossRef]

- De Wulf, K.; Schillewaert, N.; Muylle, S.; Rangarajan, D. The role of pleasure in web site success. Inf. Manag. 2006, 43, 434–446. [Google Scholar] [CrossRef]

- Yoo, J.; Park, M. The effects of e-mass customization on consumer perceived value, satisfaction, and loyalty toward luxury brands. J. Bus. Res. 2016, 69, 5775–5784. [Google Scholar] [CrossRef]

- Kastanakis, M.N.; Balabanis, G. Explaining variation in conspicuous luxury consumption: An individual differences’ perspective. J. Bus. Res. 2014, 67, 2147–2154. [Google Scholar] [CrossRef]

- Choi, J.; Kim, S. Is the smartwatch an IT product or a fashion product? A study on factors affecting the intention to use smartwatches. Comput. Hum. Behav. 2016, 63, 777–786. [Google Scholar] [CrossRef]

- Chen, J.V.; Cheng, H.K.; Hsiao, H.J.V. Loyalty and profitability of VIP and non-VIP customers in the banking service industry. Serv. Sci. 2016, 8, 19–36. [Google Scholar] [CrossRef]

- Vanani, I.R. Designing a predictive analytics for the formulation of intelligent decision making policies for vip customers investing in the bank. J. Inf. Technol. Manag. 2017, 9, 477–511. [Google Scholar]

- Thomson, M.; MacInnis, D.J.; Park, C.W. The ties that bind: The strength of consumers’ emotional attachments to brands. J. Consum. Psychol. 2005, 15, 77–91. [Google Scholar] [CrossRef]

- McKinney, V.; Yoon, K.; Zahedi, F.M. The measurement of Web-consumer satisfaction: An expectation and disconfirmation approach. Inf. Syst. Res. 2002, 13, 296–315. [Google Scholar] [CrossRef]

- Kohli, R.; Devaraj, S.; Mahmood, A. Understanding determinants of online consumer satisfaction: A decision process perspective. J. Manag. Inf. Syst. 2004, 21, 115–135. [Google Scholar] [CrossRef]

- Doll, W.J.; Deng, X.; Raghunathan, T.S.; Torkzadeh, G.; Xia, W. The meaning and measurement of user satisfaction: A multigroup invariance analysis of the end-user computing satisfaction instrument. J. Manag. Inf. Syst. 2004, 21, 227–262. [Google Scholar] [CrossRef]

- Lederer, A.L.; Maupin, D.J.; Sena, M.P.; Zhuang, Y. The technology acceptance model and the World Wide Web. Decis. Support Syst. 2000, 29, 269–282. [Google Scholar] [CrossRef]

- Buellingen, F.; Woerter, M. Development perspectives, firm strategies and applications in mobile commerce. J. Bus. Res. 2004, 57, 1402–1408. [Google Scholar] [CrossRef]

- O’Cass, A.; Fenech, T. Web retailing adoption: Exploring the nature of Internet users Web retailing behavior. J. Retail. Consum. Serv. 2003, 10, 81–94. [Google Scholar] [CrossRef]

- Ranganathan, C.; Ganapathy, S. Key dimensions of business-to-consumer websites. Inf. Manag. 2002, 39, 457–465. [Google Scholar] [CrossRef]

- Barnes, S.J.; Vidgen, R.T. An evaluation of cyber-bookshops:The WebQualTM method. Int. J. Electron. Commer. 2001, 6, 11–30. [Google Scholar] [CrossRef]

- Kim, S.; Stoel, L. Dimensional hierarchy of retail website quality. Inf. Manag. 2004, 41, 619–633. [Google Scholar] [CrossRef]

- O’cass, A.; McEwen, H. Exploring consumer status and conspicuous consumption. J. Consum. Behav. 2004, 4, 25–39. [Google Scholar] [CrossRef]

- Shukla, P.; Purani, K. Comparing the importance of luxury value perceptions in cross-national contexts. J. Bus. Res. 2012, 65, 1417–1424. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modeling. In Modern Methods for Business Research; Marcoulides, G.A., Ed.; Edison Lawrence Erlbaum Associates: Hillsdale, NJ, USA, 1998; pp. 295–336. [Google Scholar]

- Howel, J.M.; Higgins, C.A. Champion of technological innovation. Adm. Sci. Q. 1990, 35, 317–341. [Google Scholar] [CrossRef]

- Lai, P.C. The literature review of technology adoption models and theories for the novelty technology. J. Inf. Syst. Technol. Manag. 2017, 14, 21–38. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Variables | Items | Sources |

|---|---|---|

| Usefulness | The usage goals are always accomplished using Internet banking of this bank. | [54,55,73] |

| The value of using Internet banking of this bank is high. | ||

| Productivity is greatly improved using Internet banking of this bank. | ||

| The Internet banking of this bank provides much saving in time. | ||

| The financial information provided in the Internet banking of this bank is very useful. | ||

| The Internet banking of this bank provides much saving in the transaction fee. | ||

| Ease of use | It is easy to use various functions through Internet banking of this bank. | [55,73] |

| The usage procedures of Internet banking of this bank is very clear. | ||

| It easy to become a skillful user of Internet banking of this bank. | ||

| The Internet banking sites of this bank are composed of very user-friendly menus. | ||

| I can easily search wanted service items in the Internet banking sites of this bank. | ||

| It is very easy to move into other menus in the Internet banking sites of this bank. | ||

| System security | Internet banking maintains rapid and reliable access to the site. | [74,75,76] |

| Any transactions in the Internet banking of this bank are processed one time without errors or system breakdown. | ||

| The Internet banking site of this bank well protects users’ transaction account information. | ||

| The Internet banking of this bank maintains accuracy and protection of transaction data. | ||

| System trust | Users can trustfully use the Internet banking of this bank. | [55,77] |

| The Internet banking of this bank can accurately perform the intended services by customers. | ||

| The exposure of personal information is not believed to occur. | ||

| Users believe that the Internet banking of this bank ensures reliability. | ||

| System responsiveness | When I use the Internet banking of this bank, there is little waiting time between my actions and the website’s response. | [55,77,78] |

| The Internet banking of this bank enables fast processing of transactions. | ||

| The Internet banking of this bank enables fast responding to customers’ complaints. | ||

| The Internet banking of this bank enables prompt processing with customers’ requests. | ||

| The Internet banking of this bank instantly provides service to customers. | ||

| Empathy | Internet banking is much interested in individual customer. | [29,79,80] |

| Internet banking much understands and reflects customer requirements. | ||

| Internet banking solves customer with attention. | ||

| Internet banking provides a differentiated service. | ||

| I am attached to the Internet banking of this bank. | ||

| I am bonded by the Internet banking of this bank. | ||

| I am connected with the Internet banking of this bank. | ||

| Satisfaction | Overall, I am satisfied with this Internet banking experience of this bank. | [71] |

| I strongly recommend the Internet banking of this bank to others. | ||

| I am likely to further use the Internet banking of this bank | ||

| I am satisfied with the Internet banking of this bank after being compared with others. |

| Categories | General Customers | VIP Customers | Total | ||||

|---|---|---|---|---|---|---|---|

| Frequency | Percentage | Frequency | Percentage | Frequency | Percentage | ||

| Gender | Male | 397 | 30.8 | 441 | 34.2 | 838 | 65.0 |

| Female | 248 | 19.2 | 204 | 15.8 | 452 | 35.0 | |

| Total | 645 | 50.0 | 645 | 50.0 | 1290 | 100 | |

| Age | Below 20 | 12 | 0.9 | 0 | 0 | 12 | 0.9 |

| 21-30 | 241 | 18.7 | 52 | 4 | 293 | 22.7 | |

| 31-40 | 237 | 18.4 | 258 | 20 | 495 | 38.4 | |

| 41-50 | 106 | 8.2 | 211 | 16.4 | 317 | 24.6 | |

| Over 51 | 49 | 3.8 | 124 | 9.1 | 173 | 13.4 | |

| Total | 645 | 50.0 | 645 | 50 | 1290 | 100 | |

| Education | Middle or High school graduated | 92 | 7.1 | 64 | 5.0 | 156 | 12.1 |

| College student | 106 | 8.2 | 57 | 4.4 | 163 | 12.6 | |

| College graduated | 356 | 27.6 | 377 | 29.2 | 733 | 56.8 | |

| Master or PhD degree | 91 | 7.1 | 147 | 11.4 | 238 | 18.4 | |

| Total | 645 | 50.0 | 645 | 50.0 | 1290 | 100.0 | |

| Jobs | Students | 63 | 4.9 | 10 | 0.8 | 73 | 5.7 |

| Housewives | 61 | 4.7 | 82 | 6.3 | 143 | 11.2 | |

| Private | 317 | 24.6 | 299 | 23.2 | 616 | 47.8 | |

| Public | 34 | 2.6 | 33 | 2.5 | 67 | 5.2 | |

| Owner of Business | 42 | 3.3 | 80 | 6.2 | 122 | 9.5 | |

| Specialty job | 84 | 6.5 | 99 | 7.7 | 183 | 14.2 | |

| Others | 44 | 3.4 | 42 | 3.3 | 86 | 6.7 | |

| Total | 645 | 50.0 | 645 | 50.0 | 1290 | 100.0 | |

| Class | General Customers | VIP Customers | Total | ||||

|---|---|---|---|---|---|---|---|

| Frequency | Percentage | Frequency | Percentage | Frequency | Percentage | ||

| Period of | Less than 6 months | 47 | 3.6 | 10 | 0.8 | 57 | 4.4 |

| using | 6 months–one year | 105 | 8.1 | 24 | 1.9 | 129 | 10.0 |

| Internet | One year–two years | 128 | 9.9 | 43 | 3.3 | 171 | 13.3 |

| banking | More than 2 years | 365 | 28.4 | 568 | 44.0 | 933 | 72.3 |

| Total | 645 | 50.0 | 645 | 50.0 | 1290 | 100 | |

| Number | 1 | 169 | 13.0 | 116 | 9.0 | 285 | 22.1 |

| of using | 2–5 | 334 | 25.9 | 301 | 23.3 | 635 | 49.2 |

| Internet | 6–10 | 88 | 6.8 | 131 | 10.2 | 219 | 17.0 |

| banking | 11–15 | 23 | 1.8 | 41 | 3.2 | 64 | 5.0 |

| per week | More than 15 | 31 | 2.5 | 56 | 4.3 | 87 | 6.7 |

| Total | 645 | 50.0 | 645 | 50.0 | 1290 | 100 | |

| Hours | Less than 30 minutes | 57 | 4.4 | 92 | 7.1 | 149 | 11.6 |

| spent | 30 min–1 h | 83 | 6.4 | 111 | 8.6 | 194 | 15.0 |

| using | 1–2 h | 211 | 16.4 | 199 | 15.4 | 410 | 31.8 |

| Internet | More than 2 h | 294 | 22.8 | 243 | 18.9 | 537 | 41.6 |

| per day | Total | 645 | 50.0 | 645 | 50.0 | 1,290 | 100 |

| (a) Subsample of General Customers | ||||

| Variables | Item | Factor Loading | Eigen Value | Percent of Variance Explained |

| Usefulness (1) | USF1 | 0.702 | 2.12 | 52.9 |

| USF2 | 0.840 | |||

| USF3 | 0.565 | |||

| USF4 | 0.773 | |||

| Ease of use (2) | EOU1 | 0.826 | 2.95 | 73.8 |

| EOU2 | 0.893 | |||

| EOU3 | 0.875 | |||

| EOU4 | 0.839 | |||

| System security (3) | SS1 | 0.825 | 2.80 | 70.1 |

| SS2 | 0.813 | |||

| SS3 | 0.867 | |||

| SS4 | 0.842 | |||

| System trust (4) | ST1 | 0.877 | 2.98 | 74.4 |

| ST2 | 0.787 | |||

| ST3 | 0.872 | |||

| ST4 | 0.909 | |||

| System responsiveness (5) | SR1 | 0.666 | 2.98 | 74.5 |

| SR2 | 0.915 | |||

| SR3 | 0.942 | |||

| SR4 | 0.902 | |||

| System empathy (6) | SE1 | 0.932 | 3.39 | 84.6 |

| SE2 | 0.946 | |||

| SE3 | 0.925 | |||

| SE4 | 0.876 | |||

| Customer satisfaction (7) | CS1 | 0.905 | 3.13 | 78.2 |

| CS2 | 0.905 | |||

| CS3 | 0.901 | |||

| CS4 | 0.823 | |||

| (b) Subsample of VIP Customers | ||||

| Variables | Item | Factor Loading | Eigen Value | Percent of Variance Explained |

| Usefulness (1) | USF1 | 0.741 | 2.01 | 50.3 |

| USF2 | 0.700 | |||

| USF3 | 0.652 | |||

| USF4 | 0.740 | |||

| Ease of use (2) | EOU1 | 0.853 | 3.12 | 77.9 |

| EOU2 | 0.911 | |||

| EOU3 | 0.895 | |||

| EOU4 | 0.869 | |||

| System security (3) | SS1 | 0.834 | 2.96 | 74.0 |

| SS2 | 0.860 | |||

| SS3 | 0.885 | |||

| SS4 | 0.862 | |||

| System trust (4) | ST1 | 0.896 | 3.07 | 76.6 |

| ST2 | 0.799 | |||

| ST3 | 0.904 | |||

| ST4 | 0.899 | |||

| System responsiveness (5) | SR1 | 0.710 | 3.11 | 77.7 |

| SR2 | 0.932 | |||

| SR3 | 0.945 | |||

| SR4 | 0.918 | |||

| System empathy (6) | SE1 | 0.927 | 3.30 | 82.6 |

| SE2 | 0.935 | |||

| SE3 | 0.912 | |||

| SE4 | 0.858 | |||

| Customer satisfaction (7) | CS1 | 0.920 | 3.17 | 79.3 |

| CS2 | 0.916 | |||

| CS3 | 0.896 | |||

| CS4 | 0.826 | |||

| (c) Total Sample | ||||

| Variables | Item | Factor Loading | Eigen Value | Percent of Variance Explained |

| Usefulness (1) | USF1 | 0.721 | 2.06 | 51.5 |

| USF2 | 0.780 | |||

| USF3 | 0.605 | |||

| USF4 | 0.753 | |||

| Ease of use (2) | EOU1 | 0.840 | 3.03 | 75.8 |

| EOU2 | 0.902 | |||

| EOU3 | 0.884 | |||

| EOU4 | 0.854 | |||

| System security (3) | SS1 | 0.830 | 2.88 | 72.0 |

| SS2 | 0.837 | |||

| SS3 | 0.876 | |||

| SS4 | 0.852 | |||

| System trust (4) | ST1 | 0.886 | 3.02 | 75.4 |

| ST2 | 0.792 | |||

| ST3 | 0.887 | |||

| ST4 | 0.905 | |||

| System responsiveness (5) | SR1 | 0.687 | 3.04 | 76.1 |

| SR2 | 0.923 | |||

| SR3 | 0.944 | |||

| SR4 | 0.910 | |||

| System empathy (6) | SE1 | 0.929 | 3.35 | 83.6 |

| SE2 | 0.941 | |||

| SE3 | 0.919 | |||

| SE4 | 0.867 | |||

| Customer satisfaction (7) | CS1 | 0.912 | 3.15 | 78.7 |

| CS2 | 0.910 | |||

| CS3 | 0.899 | |||

| CS4 | 0.825 | |||

| Variables | Composite Reliability | Cronbach Alpha | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

|---|---|---|---|---|---|---|---|---|---|

| (a) The subsample of general customers and VIP customers | |||||||||

| Usefulness (1) | 0.829 | 0.87 | 0.748 | ||||||

| Ease of use (2) | 0.933 | 0.91 | 0.638 | 0.776 | |||||

| System security (3) | 0.914 | 0.88 | 0.568 | 0.697 | 0.726 | ||||

| System trust (4) | 0.931 | 0.92 | 0.566 | 0.609 | 0.788 | 0.770 | |||

| System responsiveness (5) | 0.928 | 0.91 | 0.632 | 0.683 | 0.753 | 0.718 | 0.765 | ||

| System empathy (6) | 0.949 | 0.91 | 0.499 | 0.566 | 0.61 | 0.575 | 0.75 | 0.823 | |

| Customer satisfaction (7) | 0.950 | 0.92 | 0.587 | 0.679 | 0.742 | 0.702 | 0.71 | 0.592 | 0.826 |

| (b) The subsample of general customers and VIP customers | |||||||||

| Variables | Composite Reliability | Cronbach Alpha | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| Usefulness (1) | 0.801 | 0.88 | 0.702 | ||||||

| Ease of use (2) | 0.934 | 0.90 | 0.659 | 0.779 | |||||

| System security (3) | 0.919 | 0.87 | 0.568 | 0.679 | 0.740 | ||||

| System trust (4) | 0.928 | 0.90 | 0.518 | 0.603 | 0.79 | 0.763 | |||

| System responsiveness (5) | 0.932 | 0.89 | 0.578 | 0.685 | 0.738 | 0.669 | 0.774 | ||

| System empathy (6) | 0.950 | 0.94 | 0.53 | 0.617 | 0.633 | 0.586 | 0.73 | 0.825 | |

| Customer satisfaction (7) | 0.938 | 0.93 | 0.624 | 0.698 | 0.718 | 0.672 | 0.709 | 0.636 | 0.793 |

| (c) Total sample | |||||||||

| Variables | Composite Reliability | Alpha | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| Usefulness (1) | 0.917 | 0.87 | 0.827 | ||||||

| Ease of use (2) | 0.933 | 0.90 | 0.650 | 0.778 | |||||

| System security (3) | 0.917 | 0.88 | 0.571 | 0.690 | 0.734 | ||||

| System trust (4) | 0.930 | 0.90 | 0.546 | 0.608 | 0.790 | 0.767 | |||

| System responsiveness (5) | 0.930 | 0.90 | 0.609 | 0.685 | 0.747 | 0.695 | 0.770 | ||

| System empathy (6) | 0.949 | 0.93 | 0.516 | 0.594 | 0.624 | 0.582 | 0.741 | 0.825 | |

| Customer satisfaction (7) | 0.945 | 0.92 | 0.606 | 0.689 | 0.732 | 0.689 | 0.710 | 0.614 | 0.811 |

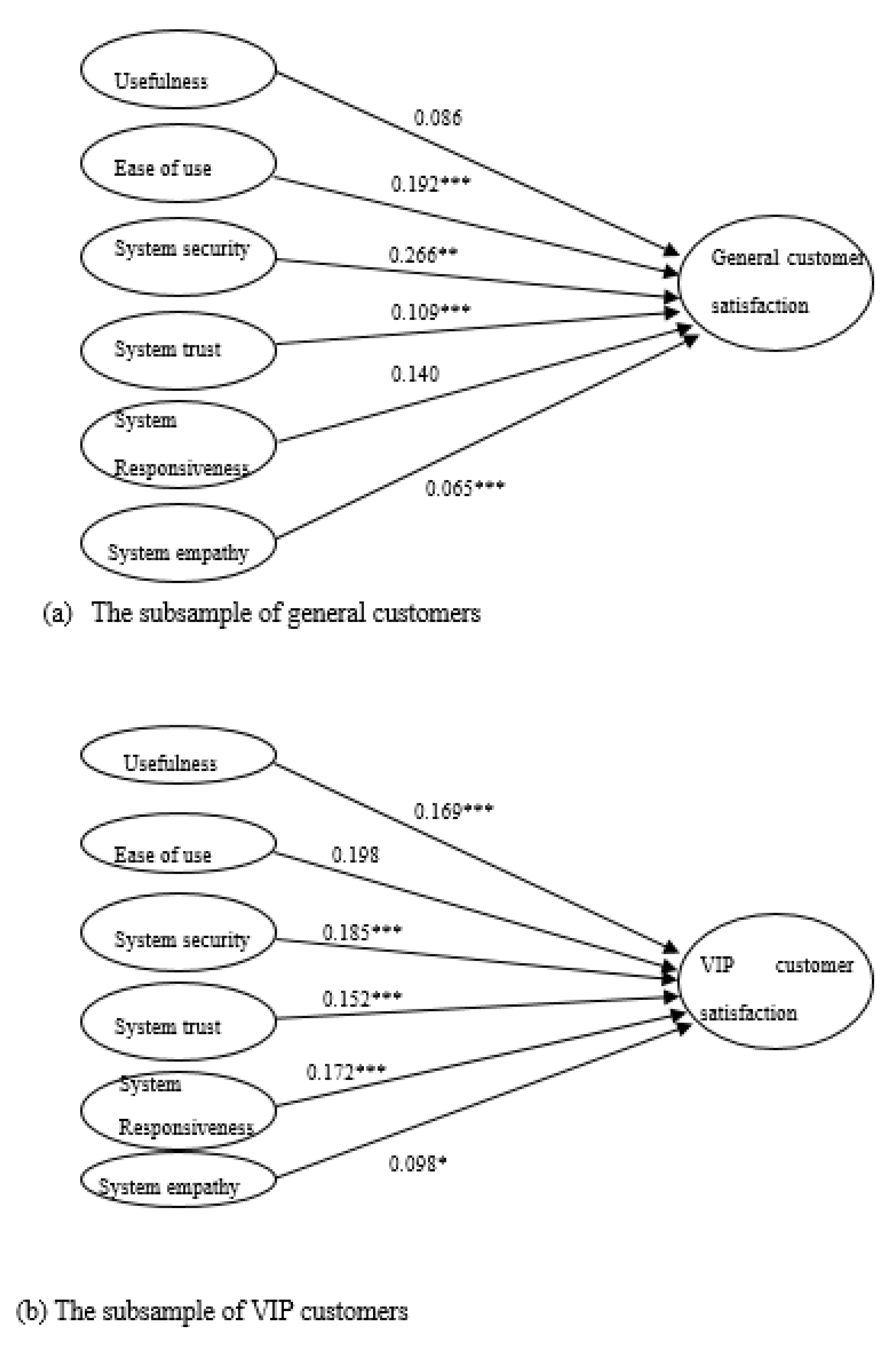

| Path | Estimates | General Customers | VIP Customers |

|---|---|---|---|

| Usefulness → customer | Path coefficient | 0.086 | 0.169 |

| satisfaction | Standard deviation | 0.074 | 0.054 |

| Size of subsample | 645 | 645 | |

| t-value of path difference | 20.24 *** | ||

| Ease of use → customer | Path coefficient | 0.192 | 0.198 |

| satisfaction | Standard deviation | 0.073 | 0.057 |

| Size of subsample | 645 | 645 | |

| t-value of path difference | 1.65 * | ||

| System security → customer | Path coefficient | 0.266 | 0.185 |

| satisfaction | Standard deviation | 0.075 | 0.074 |

| Size of subsample | 645 | 645 | |

| t-value of path difference | 21.28 *** | ||

| System trust → | Path coefficient | 0.109 | 0.152 |

| customer satisfaction | Standard deviation | 0.065 | 0.061 |

| Size of subsample | 645 | 645 | |

| t-value of path difference | 11.61 *** | ||

| System responsiveness → | Path coefficient | 0.140 | 0.172 |

| customer satisfaction | Standard deviation | 0.087 | 0.068 |

| Size of subsample | 645 | 645 | |

| t-value of path difference | 7.85 *** | ||

| System empathy → | Path coefficient | 0.065 | 0.098 |

| customer satisfaction | Standard deviation | 0.077 | 0.056 |

| Size of subsample | 645 | 645 | |

| t-value of path difference | 8.80 *** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, S.; Lee, K.C. Comparative Study of Service Quality on VIP Customer Satisfaction in Internet Banking: South Korea Case. Sustainability 2020, 12, 6365. https://doi.org/10.3390/su12166365

Lee S, Lee KC. Comparative Study of Service Quality on VIP Customer Satisfaction in Internet Banking: South Korea Case. Sustainability. 2020; 12(16):6365. https://doi.org/10.3390/su12166365

Chicago/Turabian StyleLee, Sangjae, and Kun Chang Lee. 2020. "Comparative Study of Service Quality on VIP Customer Satisfaction in Internet Banking: South Korea Case" Sustainability 12, no. 16: 6365. https://doi.org/10.3390/su12166365