Improving the Efficiency of Hedge Trading Using Higher-Order Standardized Weather Derivatives for Wind Power

Abstract

:1. Introduction

2. Methods

2.1. Market Trading Model

2.2. Minimum Variance Hedging Problem

2.3. Non-Parametric Derivatives

2.4. Standardized Derivatives

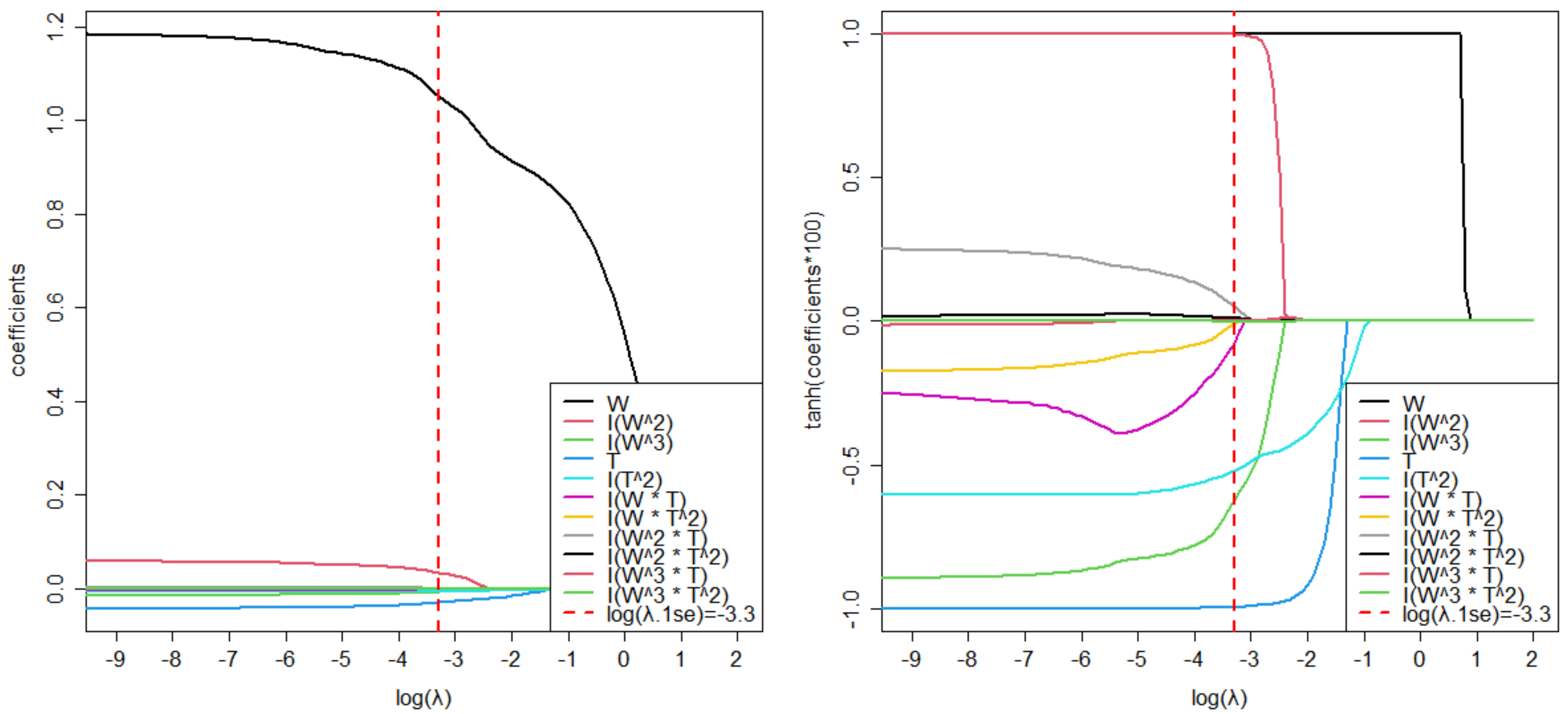

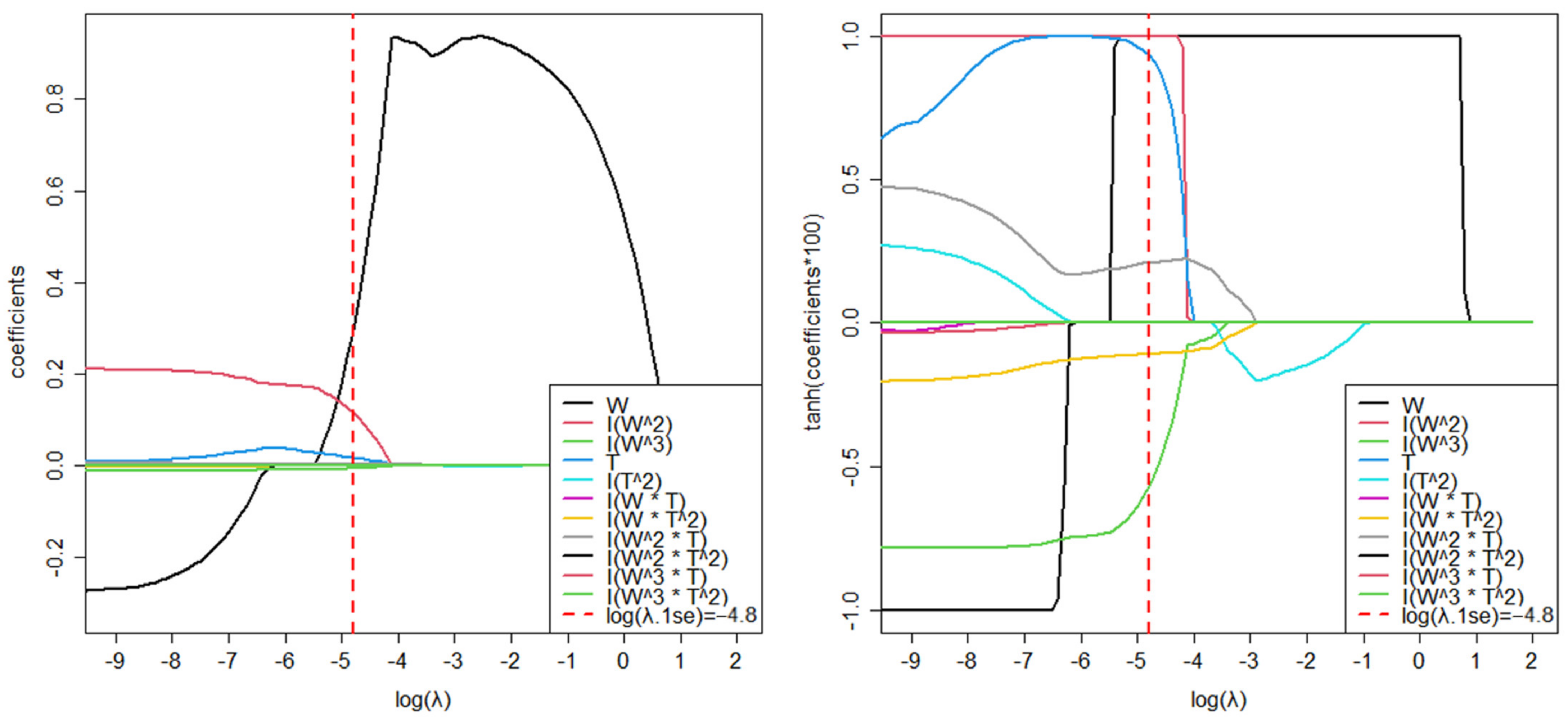

2.5. Hedge Trading Strategy Using LASSO Regression

3. Results

- Wind power generation [MWh]: actual power generation in Eastern Denmark (DK2) (downloaded from https://www.nordpoolgroup.com/en/Market-data1/, accessed on 11 January 2021)

- Wind speed [m/s] and temperature [°C]: observed values at Copenhagen Airport (downloaded from http://rp5.ru/metar.php?metar=EKCH, accessed on 11 January 2021)

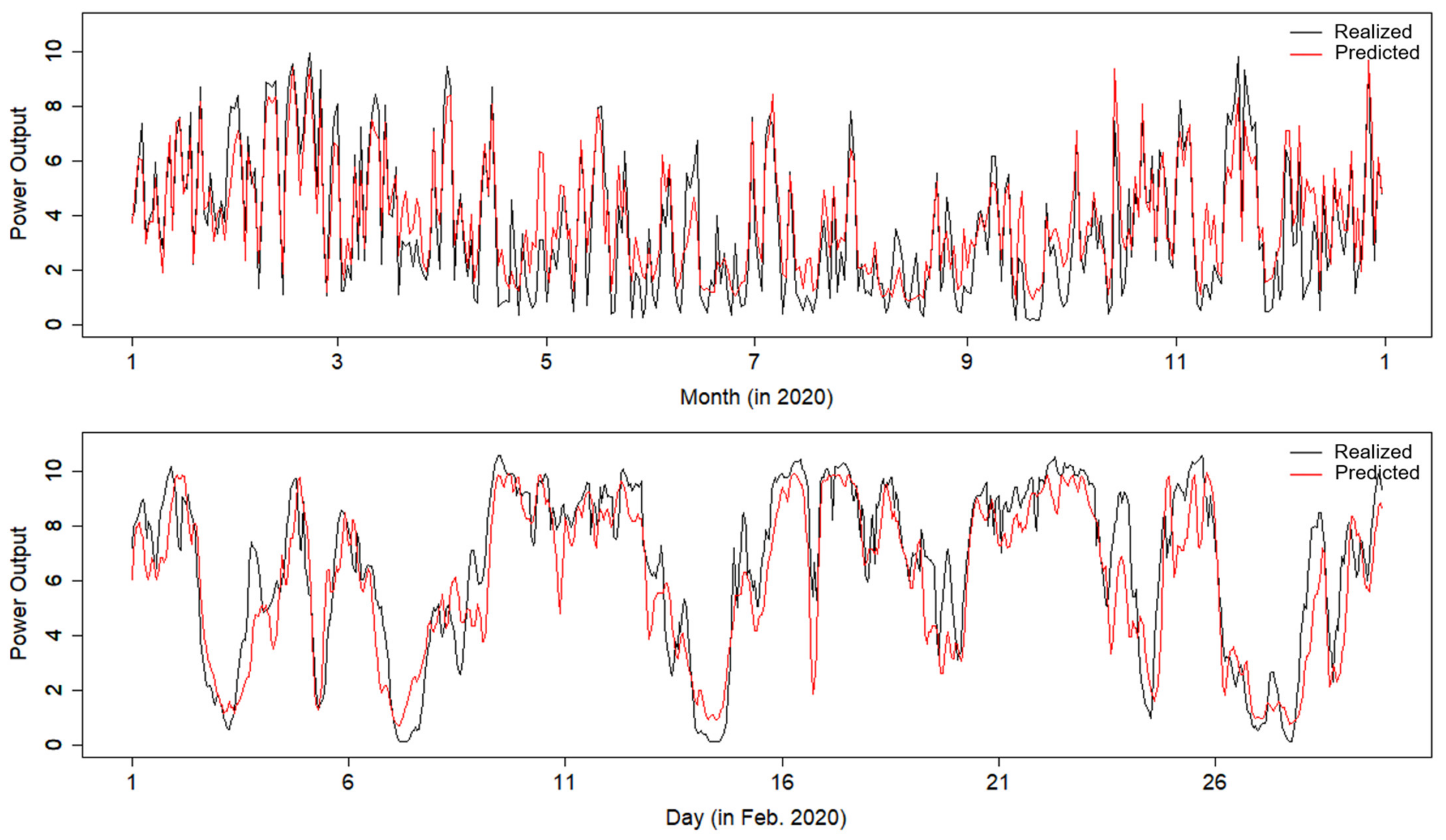

3.1. Estimated Trend (Non-Parametric Derivatives)

3.2. Measurement of Hedge Effects

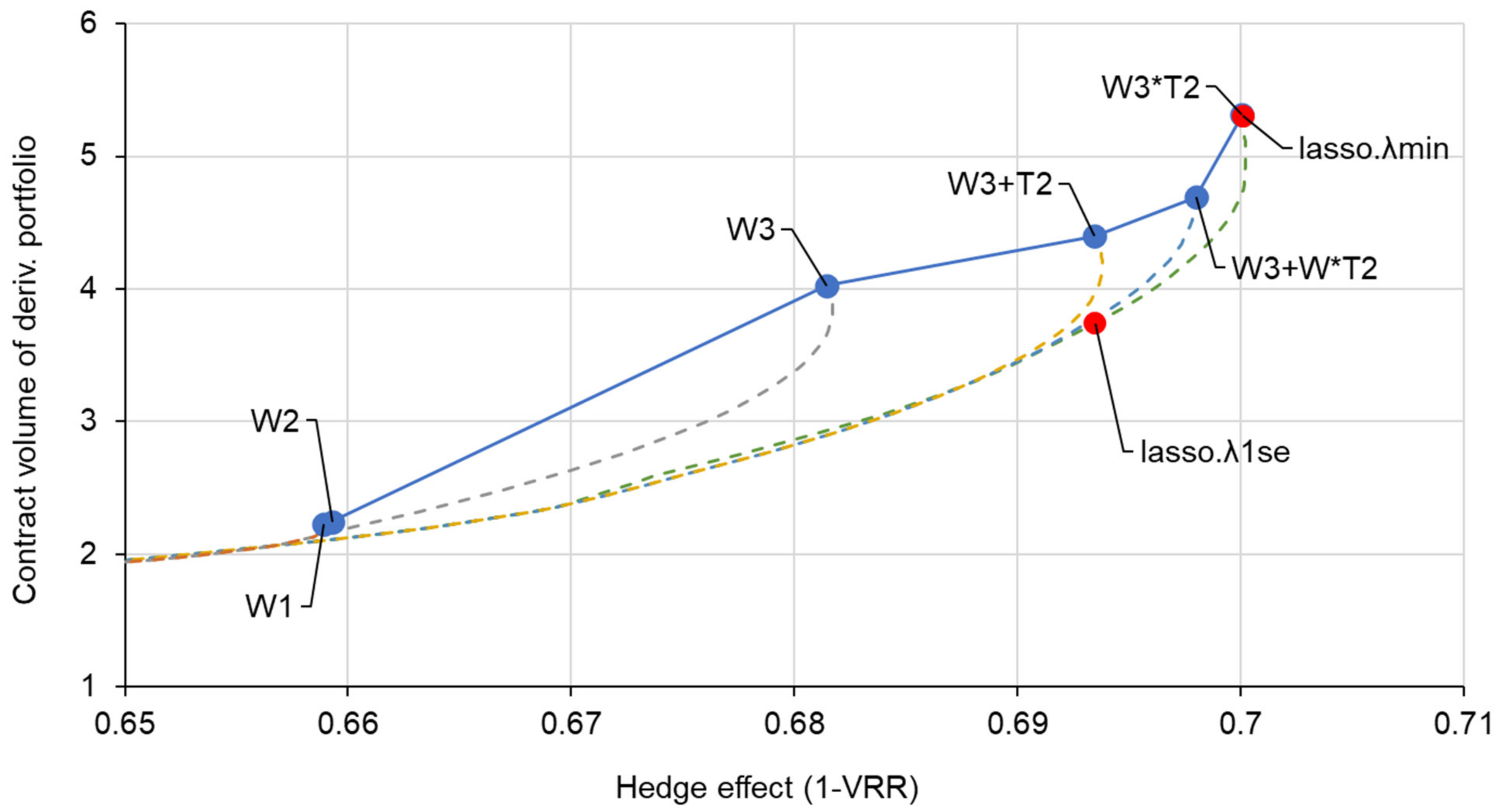

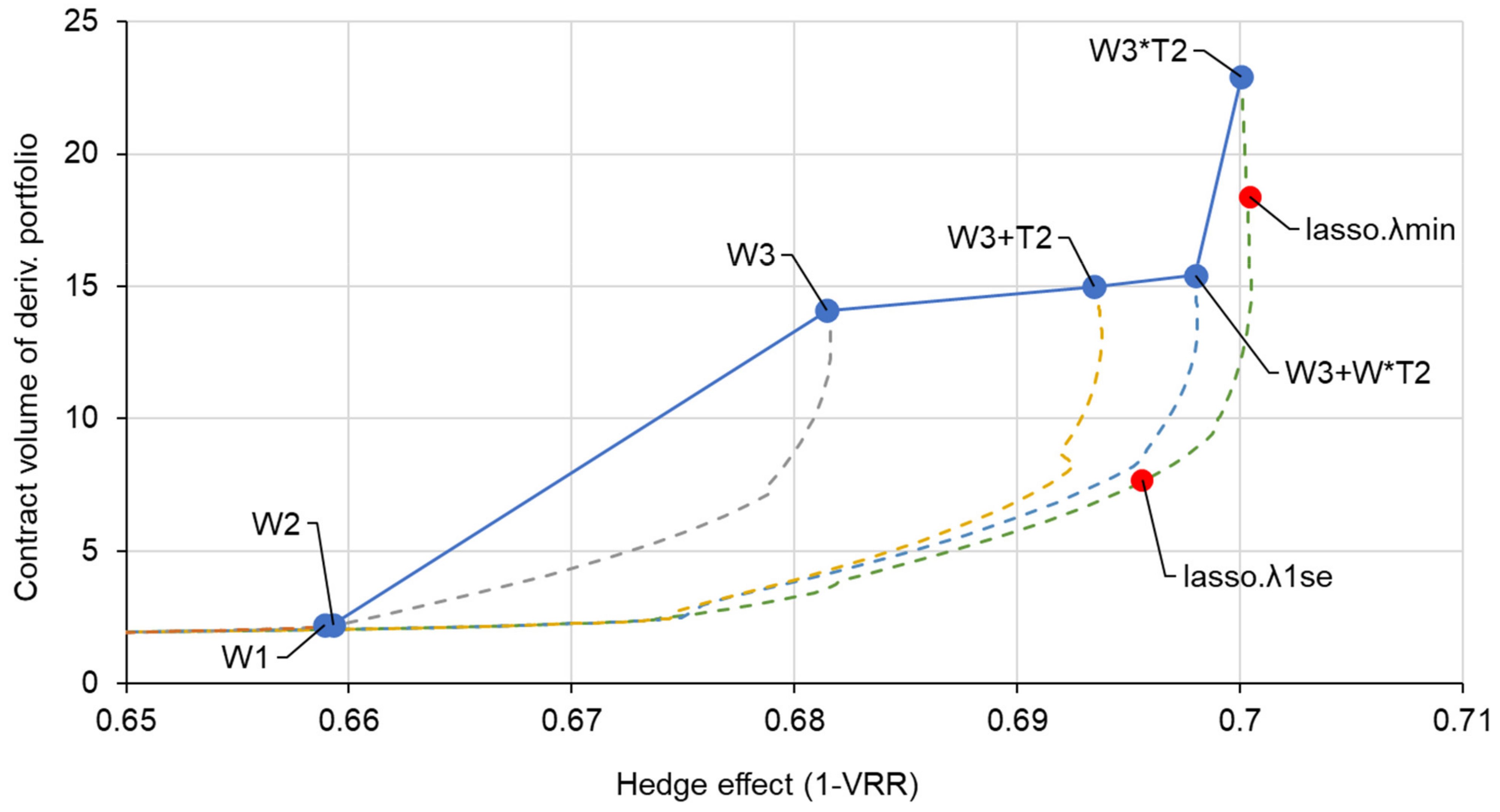

3.3. Trading Efficiency Using LASSO Regression

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Research on Wind Power Output Forecasting

Appendix B. Verification of Non-Linearity by Ramsey’s RESET Test

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Model | Diagnostic Variables | F-Statistic | p-Value |

|---|---|---|---|

| V ~ W | squares, cubes | 264.97 | |

| V ~ T | squares | 305.21 | |

| V ~ W + T | squares, cubes | 294.66 |

Appendix C. Hedge Trading Related Costs That Can Depend on Trading Volume

Appendix D. The Case of Using Derivatives with No Average Value Correction for the Underlying Index

References

- IEA. Renewables 2021 Analysis and Forecast to 2026. Available online: https://www.iea.org/reports/renewables-2021 (accessed on 15 June 2022).

- Market Research Future. Small Wind Power Market. Available online: https://www.marketresearchfuture.com/reports/small-wind-power-market-4568 (accessed on 15 June 2022).

- Botterud, A.; Wang, J.; Bessa, R.; Keko, H.; Miranda, V. Risk management and optimal bidding for a wind power producer. In IEEE PES General Meeting; IEEE: Minneapolis, MN, USA, 2010; pp. 1–8. [Google Scholar] [CrossRef]

- Bathurst, G.; Weatherill, J.; Strbac, G. Trading wind generation in short term energy markets. IEEE Trans. Power Syst. 2002, 17, 782–789. [Google Scholar] [CrossRef]

- Yamada, Y. Optimal Hedging of Prediction Errors Using Prediction Errors. Asia-Pacific Financ. Mark. 2008, 15, 67–95. [Google Scholar] [CrossRef] [Green Version]

- Eydeland, A.; Wolyniec, K. Energy and Power Risk Management: New Developments in Modeling, Pricing, and Hedging; John Wiley & Sons: Hoboken, NJ, USA, 2002; Volume 97. [Google Scholar]

- Deng, S.; Oren, S. Electricity derivatives and risk management. Energy 2006, 31, 940–953. [Google Scholar] [CrossRef]

- Benth, F.E.; Pircalabu, A. A non-Gaussian Ornstein–Uhlenbeck model for pricing wind power futures. Appl. Math. Financ. 2018, 25, 36–65. [Google Scholar] [CrossRef] [Green Version]

- Gersema, G.; Wozabal, D. An equilibrium pricing model for wind power futures. Energy Econ. 2017, 65, 64–74. [Google Scholar] [CrossRef]

- Benth, F.E.; Di Persio, L.; Lavagnini, S. Stochastic Modeling of Wind Derivatives in Energy Markets. Risks 2018, 6, 56. [Google Scholar] [CrossRef] [Green Version]

- Rodríguez, Y.; Pérez-Uribe, M.; Contreras, J. Wind Put Barrier Options Pricing Based on the Nordix Index. Energies 2021, 14, 1177. [Google Scholar] [CrossRef]

- Kanamura, T.; Homann, L.; Prokopczuk, M. Pricing analysis of wind power derivatives for renewable energy risk management. Appl. Energy 2021, 304, 117827. [Google Scholar] [CrossRef]

- Christensen, T.S.; Pircalabu, A. On the spatial hedging effectiveness of German wind power futures for wind power generators. J. Energy Mark. 2018, 11, 71–96. [Google Scholar] [CrossRef]

- Masala, G.; Micocci, M.; Rizk, A. Hedging Wind Power Risk Exposure through Weather Derivatives. Energies 2022, 15, 1343. [Google Scholar] [CrossRef]

- Hastie, T.; Tibshirani, R. Generalized Additive Models; Chapman & Hall: Boca Raton, FL, USA, 1990. [Google Scholar]

- Yamada, Y. Valuation and hedging of weather derivatives on monthly average temperature. J. Risk 2007, 10, 101–125. [Google Scholar] [CrossRef] [Green Version]

- Matsumoto, T.; Yamada, Y. Cross Hedging Using Prediction Error Weather Derivatives for Loss of Solar Output Prediction Errors in Electricity Market. Asia-Pacific Financ. Mark. 2018, 26, 211–227. [Google Scholar] [CrossRef]

- Matsumoto, T.; Yamada, Y. Simultaneous hedging strategy for price and volume risks in electricity businesses using energy and weather derivatives. Energy Econ. 2021, 95, 105101. [Google Scholar] [CrossRef]

- Matsumoto, T.; Yamada, Y. Customized yet Standardized Temperature Derivatives: A Non-Parametric Approach with Suitable Basis Selection for Ensuring Robustness. Energies 2021, 14, 3351. [Google Scholar] [CrossRef]

- Wood, S.N. Generalized Additive Models: An Introduction with R; Chapman and Hall: New York, NY, USA, 2017. [Google Scholar]

- Oum, Y.; Oren, S.; Deng, S. Hedging quantity risks with standard power options in a competitive wholesale electricity market. Nav. Res. Logist. 2006, 53, 697–712. [Google Scholar] [CrossRef]

- Oum, Y.; Oren, S.S. Optimal Static Hedging of Volumetric Risk in a Competitive Wholesale Electricity Market. Decis. Anal. 2010, 7, 107–122. [Google Scholar] [CrossRef] [Green Version]

- Brik, R.I.; Roncoroni, A. Static mitigation of volumetric risk. J. Energy Mark. 2016, 9, 111–150. [Google Scholar] [CrossRef]

- Carr, P.; Madan, D. Optimal positioning in derivative securities. Quant. Financ. 2001, 1, 19–37. [Google Scholar] [CrossRef]

- Matsumoto, T.; Yamada, Y. Multivariate Weather Derivatives for Wind Power Risk Management: Standardization Scheme and Trading Strategy. Energy Rep. 2023, in press. [Google Scholar]

- Yamada, Y.; Matsumoto, T. Construction of Mixed Derivatives Strategy for Wind Power Producers; University of Tsukuba: Tokyo, Japan, 2023; manuscript in preparation. [Google Scholar]

- Ederington, L.H. The hedging performance of the new futures markets. J. Financ. 1979, 34, 157–170. [Google Scholar] [CrossRef]

- Zainudin, A.D.; Mohamad, A. Cross hedging with stock index futures. Q. Rev. Econ. Finance 2021, 82, 128–144. [Google Scholar] [CrossRef]

- Ong, T.S.; Tan, W.F.; Teh, B.H. Hedging effectiveness of crude palm oil futures market in Malaysia. World Appl. Sci. J. 2012, 19, 556–565. [Google Scholar]

- Woo, C.-K.; Horowitz, I.; Hoang, K. Cross hedging and forward-contract pricing of electricity. Energy Econ. 2001, 23, 1–15. [Google Scholar] [CrossRef]

- Sant’Anna, L.R.; Caldeira, J.F.; Filomena, T.P. Lasso-based index tracking and statistical arbitrage long-short strategies. N. Am. J. Econ. Finance 2020, 51, 101055. [Google Scholar] [CrossRef] [Green Version]

- Chen, Q.-A.; Hu, Q.; Yang, H.; Qi, K. A kind of new time-weighted nonnegative lasso index-tracking model and its application. N. Am. J. Econ. Financ. 2022, 59, 101603. [Google Scholar] [CrossRef]

- Ketterer, J.C. The impact of wind power generation on the electricity price in Germany. Energy Econ. 2014, 44, 270–280. [Google Scholar] [CrossRef] [Green Version]

- Yamada, Y.; Matsumoto, T. Going for Derivatives or Forwards? Minimizing Cashflow Fluctuations of Electricity Transactions on Power Markets. Energies 2021, 14, 7311. [Google Scholar] [CrossRef]

- Mosquera-López, S.; Uribe, J.M. Pricing the risk due to weather conditions in small variable renewable energy projects. Appl. Energy 2022, 322, 119476. [Google Scholar] [CrossRef]

- RE-Source. Risk Mitigation for Corporate Renewable PPAs. 2017. Available online: https://resource-platform.eu/wp-content/uploads/files/statements/RE-Source%203.pdf (accessed on 3 February 2022).

- Ko, W.; Hur, D.; Park, J.-K. Correction of wind power forecasting by considering wind speed forecast error. J. Int. Counc. Electr. Eng. 2015, 5, 47–50. [Google Scholar] [CrossRef] [Green Version]

- Ramsey, J.B. Tests for Specification Errors in Classical Linear Least-Squares Regression Analysis. J. R. Stat. Soc. Ser. B (Methodol.) 1969, 31, 350–371. [Google Scholar] [CrossRef]

- Tibshirani, R. Regression Shrinkage and Selection Via the Lasso. J. R. Stat. Soc. Ser. B 1996, 58, 267–288. [Google Scholar] [CrossRef]

- Hastie, T.; Tibshirani, R.; Friedman, J.H.; Friedman, J.H. The Elements of Statistical Learning: Data Mining, Inference, and Prediction; Springer: New York, NY, USA, 2009; Volume 2, pp. 1–758. [Google Scholar]

- Friedman, J.; Hastie, T.; Tibshirani, R.; Narasimhan, B.; Tay, K.; Simon, N.; Qian, J. Package ‘glmnet’. CRAN R Repositary. Available online: https://cran.r-project.org/web/packages/glmnet/index.html (accessed on 15 June 2022).

- Krstajic, D.; Buturovic, L.J.; Leahy, D.E.; Thomas, S. Cross-validation pitfalls when selecting and assessing regression and classification models. J. Cheminform. 2014, 6, 10. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Alladi, T.; Chamola, V.; Rodrigues, J.J.P.C.; Kozlov, S.A. Blockchain in Smart Grids: A Review on Different Use Cases. Sensors 2019, 19, 4862. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Foley, A.M.; Leahy, P.G.; Marvuglia, A.; McKeogh, E.J. Current methods and advances in forecasting of wind power generation. Renew. Energy 2012, 37, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Hanifi, S.; Liu, X.; Lin, Z.; Lotfian, S. A Critical Review of Wind Power Forecasting Methods—Past, Present and Future. Energies 2020, 13, 3764. [Google Scholar] [CrossRef]

- Chaurasiya, P.K.; Kumar, V.K.; Warudkar, V.; Ahmed, S. Evaluation of wind energy potential and estimation of wind turbine characteristics for two different sites. Int. J. Ambient Energy 2021, 42, 1409–1419. [Google Scholar] [CrossRef]

- Chaurasiya, P.K.; Ahmed, S.; Warudkar, V. Wind characteristics observation using Doppler-SODAR for wind energy applications. Resour.-Effic. Technol. 2017, 3, 495–505. [Google Scholar]

- Werapun, W.; Tirawanichakul, Y.; Waewsak, J. Wind shear coefficients and their effect on energy production. Energy Procedia 2017, 138, 1061–1066. [Google Scholar] [CrossRef]

- Marčiukaitis, M.; Žutautaitė, I.; Martišauskas, L.; Jokšas, B.; Gecevičius, G.; Sfetsos, A. Non-linear regression model for wind turbine power curve. Renew. Energy 2017, 113, 732–741. [Google Scholar] [CrossRef]

- Aksoy, B.; Selbaş, R. Estimation of Wind Turbine Energy Production Value by Using Machine Learning Algorithms and Development of Implementation Program. Energy Sources Part A Recover. Util. Environ. Eff. 2019, 43, 692–704. [Google Scholar] [CrossRef]

- Bilal, B.; Ndongo, M.; Adjallah, K.H.; Sava, A.; Kébé, C.M.; Ndiaye, P.A.; Sambou, V. Wind turbine power output prediction model design based on artificial neural networks and climatic spatiotemporal data. In Proceedings of the 2018 IEEE International Conference on Industrial Technology, Buenos Aires, Argentina, 26–28 February 2020; pp. 1085–1092. [Google Scholar]

- De Giorgi, M.G.; Ficarella, A.; Tarantino, M. Assessment of the benefits of numerical weather predictions in wind power forecasting based on statistical methods. Energy 2011, 36, 3968–3978. [Google Scholar] [CrossRef]

- Vaona, A. Spatial autocorrelation or model misspecification? The help from RESET and the curse of small samples. Lett. Spat. Resour. Sci. 2009, 2, 53–59. [Google Scholar] [CrossRef]

- Hothorn, T.; Zeileis, A.; Farebrother, R.W.; Cummins, C.; Millo, G.; Mitchell, D.; Zeileis, M.A. Package ‘lmtest’. Testing Linear Regression Models. Available online: https://cran.r-project.org/web/packages/lmtest/lmtest.pdf (accessed on 3 February 2023).

- Wooldridge, J.M. Introductory Econometrics: A Modern Approach; Cengage learning: Boston, MA, USA, 2015. [Google Scholar]

- Demsetz, H. The Cost of Transacting. Q. J. Econ. 1968, 82, 33–53. [Google Scholar] [CrossRef]

- Lobo, M.S.; Fazel, M.; Boyd, S. Portfolio optimization with linear and fixed transaction costs. Ann. Oper. Res. 2006, 152, 341–365. [Google Scholar] [CrossRef]

- Georgiev, K.; Kim, Y.S.; Stoyanov, S. Periodic portfolio revision with transaction costs. Math. Methods Oper. Res. (ZOR) 2015, 81, 337–359. [Google Scholar] [CrossRef]

- Chen, F.Y.; Yano, C.A. Improving Supply Chain Performance and Managing Risk Under Weather-Related Demand Uncertainty. Manag. Sci. 2010, 56, 1380–1397. [Google Scholar] [CrossRef] [Green Version]

- Bunn, D.W.; Chen, D. The forward premium in electricity futures. J. Empir. Financ. 2013, 23, 173–186. [Google Scholar] [CrossRef]

- Longstaff, F.A.; Wang, A.W. Electricity Forward Prices: A High-Frequency Empirical Analysis. J. Financ. 2004, 59, 1877–1900. [Google Scholar] [CrossRef] [Green Version]

- Gagliardini, P.; Ossola, E.; Scaillet, O. Time-Varying Risk Premium in Large Cross-Sectional Equity Data Sets. Econometrica 2016, 84, 985–1046. [Google Scholar] [CrossRef] [Green Version]

- Woodard, J. Options and the Volatility Risk Premium; Pearson Education: London, UK, 2011. [Google Scholar]

- Batchelor, R.A.; Alizadeh, A.H.; Visvikis, I.D. The relation between bid–ask spreads and price volatility in forward markets. Deriv. Use Trading Regul. 2005, 11, 105–125. [Google Scholar] [CrossRef]

- Bryant, H.L.; Haigh, M.S. Bid–ask spreads in commodity futures markets. Appl. Financ. Econ. 2004, 14, 923–936. [Google Scholar] [CrossRef]

- Yoo, J.; Maddala, G.S. Risk premia and price volatility in futures markets. J. Futur. Mark. 1991, 11, 165–177. [Google Scholar] [CrossRef]

| Standardized Derivatives Model | Non-Parametric Derivatives Model | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| W1 | W2 | W3 | W3+T2 | W3+W*T2 | W3*T2 | Wd | Wd+Td | Wd*Td | ||

| Standardized derivatives | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||

| ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| ✓ | ✓ | ✓ | ✓ | |||||||

| ✓ | ✓ | ✓ | ||||||||

| ✓ | ✓ | |||||||||

| ✓ | ||||||||||

| Non-parametric derivatives | ✓ | ✓ | ||||||||

| ✓ | ||||||||||

| ✓ | ||||||||||

| Monthly Hedge Effect | All Period | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | |||

| Hedge effect (1-VRR) | W1 | 68.6% | 76.1% | 65.4% | 59.1% | 58.7% | 40.9% | 66.3% | 15.4% | 63.5% | 62.8% | 72.8% | 60.9% | 65.9% |

| W3 | 67.5% | 79.4% | 72.3% | 59.9% | 59.5% | 43.9% | 69.1% | 25.3% | 68.8% | 62.5% | 75.9% | 60.3% | 68.1% | |

| W3*T2 | 68.6% | 80.7% | 71.5% | 59.2% | 61.1% | 46.9% | 74.0% | 33.0% | 68.8% | 63.8% | 76.0% | 59.8% | 69.3% | |

| Improvement rate (to “W1”) | W3 | −1.6% | 4.4% | 10.6% | 1.4% | 1.4% | 7.2% | 4.3% | 64.2% | 8.3% | −0.4% | 4.2% | −1.1% | 3.4% |

| W3*T2 | 0.0% | 6.1% | 9.3% | 0.2% | 4.0% | 14.7% | 11.6% | 114.6% | 8.4% | 1.7% | 4.4% | −1.8% | 5.2% | |

| W1 | W2 | W3 | W3+T2 | W3+W*T2 | W3*T2 | Stdev of Payoffs | ||||

|---|---|---|---|---|---|---|---|---|---|---|

| Contract volumes of each derivative (absolute values of coefficients) | ||||||||||

| W | 0.98465 | 0.97895 | 1.13905 | 1.11814 | 1.16114 | 1.18486 | 1.18426 | 1.05063 | 2.3 | |

| I(W^2) | - | 0.00378 | 0.06930 | 0.06541 | 0.06286 | 0.05867 | 0.05820 | 0.03367 | 8.3 | |

| I(W^3) | - | - | 0.01406 | 0.01369 | 0.01376 | 0.01460 | 0.01455 | 0.00728 | 62.3 | |

| T | - | - | - | 0.03324 | 0.03283 | 0.04237 | 0.04244 | 0.03022 | 6.4 | |

| I(T^2) | - | - | - | 0.00569 | 0.00613 | 0.00694 | 0.00697 | 0.00579 | 46.3 | |

| I(W * T) | - | - | - | - | 0.00355 | 0.00246 | 0.00229 | 0.00080 | 13.8 | |

| I(W * T^2) | - | - | - | - | 0.00113 | 0.00180 | 0.00177 | 0.00006 | 128.2 | |

| I(W^2 * T) | - | - | - | - | - | 0.00258 | 0.00262 | 0.00051 | 56.3 | |

| I(W^2 * T^2) | - | - | - | - | - | 0.00016 | 0.00017 | 0.00011 | 428.9 | |

| I(W^3 * T) | - | - | - | - | - | 0.00015 | 0.00017 | . | 361.8 | |

| I(W^3 * T^2) | - | - | - | - | - | 0.00004 | 0.00004 | 0.00003 | 2651.4 | |

| Contract volumes of derivatives portfolio | ||||||||||

| Simple sum | 0.98465 | 0.98273 | 1.22241 | 1.23617 | 1.28140 | 1.31463 | 1.31348 | 1.12909 | ||

| Weighted sum | 2.22805 | 2.24632 | 4.02585 | 4.40015 | 4.69229 | 5.31285 | 5.30554 | 3.74113 | ||

| Hedge effects of derivatives portfolio | ||||||||||

| 1-VRR | 0.65892 | 0.65929 | 0.68146 | 0.69343 | 0.69797 | 0.70006 | 0.70009 | 0.69348 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Matsumoto, T.; Yamada, Y. Improving the Efficiency of Hedge Trading Using Higher-Order Standardized Weather Derivatives for Wind Power. Energies 2023, 16, 3112. https://doi.org/10.3390/en16073112

Matsumoto T, Yamada Y. Improving the Efficiency of Hedge Trading Using Higher-Order Standardized Weather Derivatives for Wind Power. Energies. 2023; 16(7):3112. https://doi.org/10.3390/en16073112

Chicago/Turabian StyleMatsumoto, Takuji, and Yuji Yamada. 2023. "Improving the Efficiency of Hedge Trading Using Higher-Order Standardized Weather Derivatives for Wind Power" Energies 16, no. 7: 3112. https://doi.org/10.3390/en16073112