Seaports’ Role in Ensuring the Availability of Alternative Marine Fuels—A Multi-Faceted Analysis

Abstract

:1. Introduction

- The GHG emissions expressed in CO2 increased by 9.6% from 977 million tonnes in 2012 to 1076 million tonnes in 2018;

- CO2 emissions alone in 2012 accounted for 962 million tonnes, while in 2018, total CO2 emissions increased by 9.3% to 1056 million tonnes (with 708 mt from international shipping). In 2021, international shipping was responsible for 667 mt of CO2 emissions [2];

- International shipping contributes to global anthropogenic emissions; this contribution increased from 2.76% in 2012 to 2.89% in 2018, and experts say it could reach 17 percent or more by 2050, as global trade is expanding and other industries are reducing their fossil fuel consumption [5].

- “a reduction of the average carbon intensity of international shipping by at least 40% by 2030, pursuing efforts towards 70% by 2050, as compared to 2008 levels; and,

- a reduction of total annual GHG emissions from shipping by at least 50% by 2050 compared to 2008, while pursuing efforts towards phasing them out entirely within this century”.

- To provide an overview of some of the emerging alternative fuel technologies that are being used or tested for further use in maritime transport, as well as their availability;

- To analyse the bunkering and storage infrastructure available at seaports worldwide;

- To assess the level of advancement of Polish ports in relation to the bunkering of alternative fuels by ships and to explore the ports’ plans in this regard.

2. Literature Review

3. Alternative Fuels for International Shipping

3.1. Characteristics of Selected Alternative Fuels

3.1.1. LNG

3.1.2. LPG

3.1.3. Hydrogen

3.1.4. Ammonia

3.1.5. Methanol

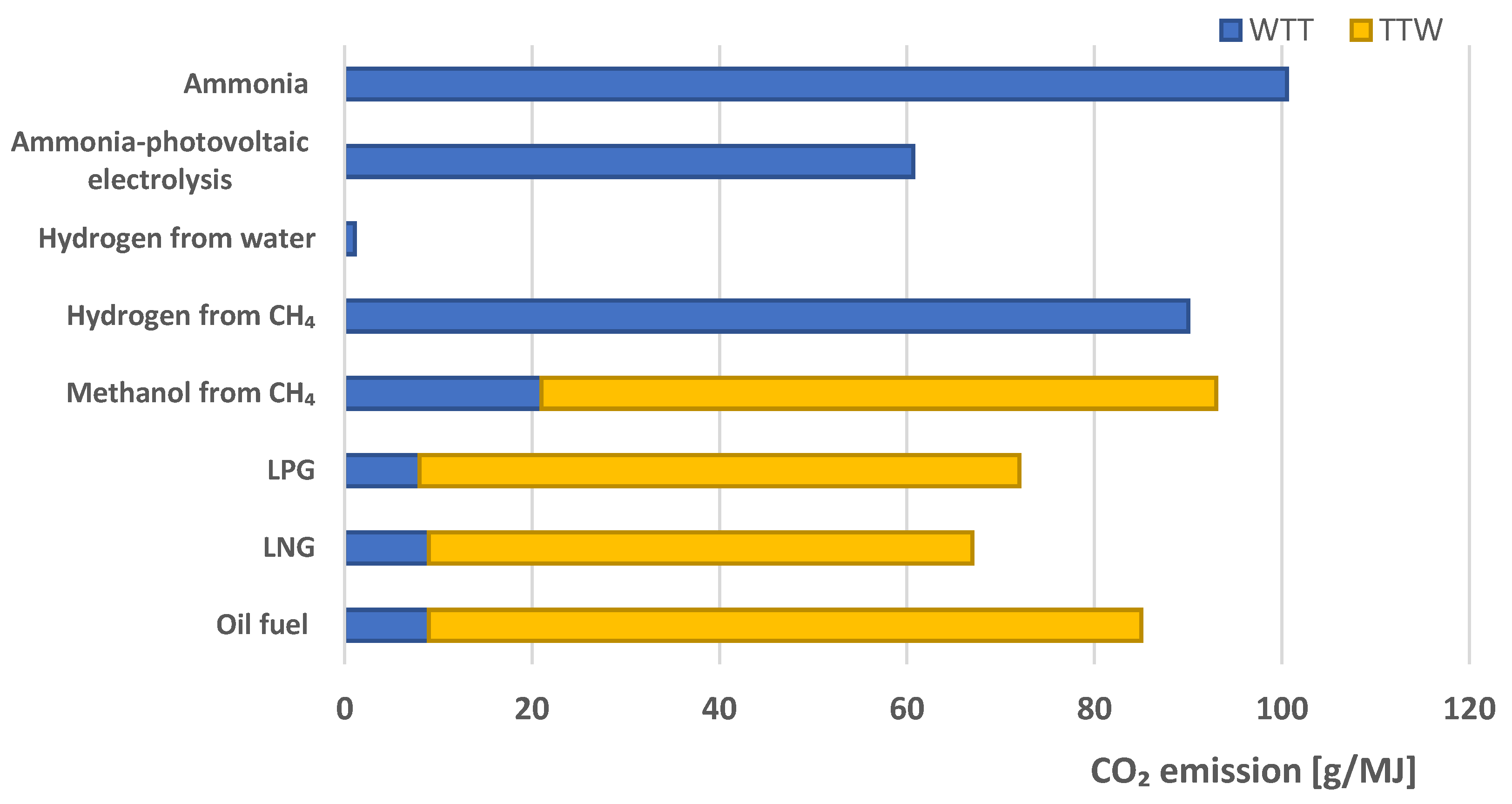

3.2. Lifecycle of Marine Fuels

- Increasing the availability of marine alternative fuels in ports to provide bunkering options for shipowners;

- Introducing market-based measures to reduce the price differential between the marine alternative fuels and conventional fuels;

- Establishing a mechanism to fund both research and development (R&D), incentivize the “first movers”, and ensure a fair and equitable fuel transition.

4. Development of Alternative Fuel Infrastructure in Ports

4.1. Ports on the Path to Decarbonising Shipping

- Incentive schemes for ships (e.g., differentiation of port dues) [87];

- More automated and effective cargo-handling operations; e.g., [88];

- Improved coordination and synchronization between ships and ports [87], such as just-in-time arrival for ships;

- On-shore power supply for ships;

- Reduced turnaround times at berth [89];

- Implementation of incentive programmes that facilitate fuel savings within the port area [90];

- Investment in green handling technologies and handling equipment, such as cranes, straddles, and truck trailers [91];

- Development of intermodal connections to and from the hinterland [85].

4.2. Existing and Planned Alternative Fuel Bunkering Infrastructure

4.2.1. Research Methodology

4.2.2. Research Findings

- Ship-to-ship (STS);

- Truck-to-ship (TTS);

- Port-to-ship (PTS).

4.2.3. LNG Bunkering Infrastructure

4.2.4. LPG Bunkering Infrastructure

4.2.5. Methanol Bunkering Infrastructure

4.2.6. Hydrogen Bunkering Infrastructure

4.2.7. Ammonia Bunkering Infrastructure

5. Level of Advancement of Polish Ports in Bunkering Alternative Fuels for Ships

5.1. Research Methodology

5.2. Results and Discussion

5.2.1. Current State and Plans (Code One)

5.2.2. Bunkering Methods (Code Two)

5.2.3. Demand Analysis (Code Three)

5.2.4. Funds (Code Four)

5.2.5. Uncertainty (Code Five)

- Uncertainty about what fuel will become the fuel of the future in shipping;

- Uncertainty about the availability of fuel if competition for it with other sectors of the economy begins;

- Uncertainty about the international and national regulations and the timing of the implementation of the requirements contained therein;

- Uncertainty about the economic and political situation in the country, which could make it difficult to raise funds for the construction of the necessary bunkering infrastructure;

- Uncertainty about the safety associated with the use of alternative fuels (in particular, hydrogen and ammonia).

5.2.6. Safety (Code Six)

5.2.7. Cooperation (Code Seven)

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

- (1)

- Has the port carried out an analysis of shipowners’ demand for alternative fuels, taking into account the specific type of fuel such as e.g., methanol, hydrogen, ammonia, LNG, LPG or other?

- (2)

- Which shipowners have expressed interest in the availability of alternative fuels at the port? (If shipowners cannot be named, please indicate the scope of their activities: ferry and ro-ro shipping, short sea container shipping, ocean shipping, tramp shipping).

- (3)

- What type of fuel would potential shipowners be interested in and what would guide their choice?

- (4)

- Have there been discussions or consultations with shipowners and representatives of other ports concerning the so-called Green Corridors or route activities?

- (1)

- Are discussions taking place with possible suppliers of alternative fuels? Will the chosen fuel be produced in Poland or will it be imported from abroad?

- (2)

- Are potential suppliers of these fuels at all interested in cooperating with the port?

- (1)

- What solutions for the supply and storage of a particular type of alternative fuel are being considered by the port?

- (2)

- What was the rationale behind the choice of a particular fuel bunkering method (ship-to-ship, track loading, bunker vessel loading, local storage, tank-to-ship, other)?

- (3)

- How does the Port plan to manage the risks associated with alternative fuel bunkering (safety issues related to transport, possible storage, and the bunkering process itself)?

- (4)

- When are the technical facilities for the bunkering of alternative fuels planned to be realised?

- (1)

- What are the sources of funding for bunkering infrastructure (in the context of alternative fuels) and related R&D: Port Authority’s own funds, funds of an external investor (infrastructure operator, PPP, EU funds)?

- (2)

- Which institutions and onshore companies are involved in the development of infrastructure for alternative fuels (State Treasury companies, private companies)?

References

- United Nations. UNCTAD Review of Maritime Transport 2022; UN: Geneva, Switzerland, 2022. [Google Scholar]

- IEA. International Shipping; IEA: Paris, France, 2022; Available online: https://www.iea.org/reports/international-shipping (accessed on 10 October 2022).

- Tan, E.C.D.; Hawkins, T.R.; Lee, U.; Tao, L.; Meyer, P.A.; Wang, M.; Thompson, M. Techno-Economic Analysis and Life Cycle Assessment of Greenhouse Gas and Criteria Air Pollutant Emissions for Biobased Marine Fuels. Available online: https://www.maritime.dot.gov/innovation/meta/techno-economic-analysis-and-life-cycle-assessment-greenhouse-gas-and-criteria-air (accessed on 1 November 2022).

- Faber, J.; Hanayama, S.; Zhang, S.; Pereda, P.; Comer, B.; Hauerhof, E.; van der Loeff, W.S.; Smith, T.; Zhang, Y.; Kosaka, H.; et al. Reduction of GHG Emissions from Ships—Fourth IMO GHG Study 2020—Final Report; International Maritime Organization (IMO): London, UK, 2020. [Google Scholar]

- Smith, T.W.P.; Jalkanen, J.P.; Anderson, B.A.; Corbett, J.J.; Faber, J.; Hanayama, S.; O’Keeffe, E.; Parker, S.; Johansson, L.; Aldous, L.; et al. Third IMO GHG Study 2014; International Maritime Organization (IMO): London, UK, 2015. [Google Scholar]

- European Commission. 2020 Annual Report from the European Commission on CO2 Emissions from Maritime Transport; COM(2021) 6022 Final; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- UNFCCC. The Paris Agreement. Available online: https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement (accessed on 29 May 2020).

- IMO. Resolution MEPC.203(62) Amendments to the Annex of the Protocol of 1997 to Amend the International Convention for the Prevention of Pollution from Ships, 1973, as Modified by the Protocol of 1978 Relating Thereto—(Adopted on 15 July 2011) (Inclusion of Regulations on Energy Efficiency for Ships in MARPOL Annex VI); International Maritime Organization (IMO): London, UK, 2011. [Google Scholar]

- IMO. Resolution MEPC.350(78) Guidelines on the Method of Calculation of the Attained Energy Efficiency Existing Ships Index (EEXI) (Adopted on 10 June 2022); International Maritime Organization (IMO): London, UK, 2022. [Google Scholar]

- IMO. Resolution MEPC.304(72) Initial IMO Strategy on Reduction of GHG Emissions from Ships, Adopted on 13 April 2018; International Maritime Organization (IMO): London, UK, 2018. [Google Scholar]

- IMO. Resolution MEPC. 328(76), Amendments to the Annex of the Protocol of 1997 to Amend the International Convention for the Prevention of Pollution from Ships, 1973, as Modified by the Protocol of 1978 (Revised MARPOL Annex VI); International Maritime Organization (IMO): London, UK, 2021. [Google Scholar]

- EU. Regulation 2021/1119 of the European Parliament and of the Council of 30 June 2021 establishing the framework for achieving climate neutrality and amending Regulations (EC) No 401/2009 and (EU) 2018/1999 (‘European Climate Law’). Off. J. Eur. Union 2021, L 243/1, 1–17. [Google Scholar]

- The US Clean Shipping Act 202. Available online: https://lowenthal.house.gov/sites/lowenthal.house.gov/files/ASL-Clean-Shipping-Act-2022.pdf) (accessed on 14 October 2022).

- IMO. Introducing Lifecycle Guidelines to Estimate Well-to-Wake Greenhouse Gas (GHG) Emissions of Sustainable Alternative Fuels to Incentivize Their Uptake at Global Level; ISWG-GHG 9/2 (EU); International Maritime Organization (IMO): London, UK, 2021. [Google Scholar]

- Percić, M.; Vladimir, N.; Fan, A. Life-cycle cost assessment of alternative marine fuels to reduce the carbon footprint in short-shipping: A case study of Croatia. Appl. Energy 2020, 279, 115848. [Google Scholar] [CrossRef]

- Percić, M.; Vladimir, N.; Fan, A. Techno-economic assessment of alternative marine fuels for inland shipping in Croatia. Renew. Sustain. Energy Rev. 2021, 148, 111363. [Google Scholar] [CrossRef]

- Calderón, M.; Illinf, D.; Veiga, J. Facilities for bunkering of liquefied natural gas in ports. Trans. Res. Proc. 2016, 14, 2431–2440. [Google Scholar] [CrossRef] [Green Version]

- Foretich, A.; Zaimes, G.G.; Hawkins, T.R.; Newes, E. Challenges and opportunities for alternative fuels in the maritime sector. Marit. Transp. Res. 2021, 2, 100033. [Google Scholar] [CrossRef]

- Svanberg, M.; Ellis, J.; Lundgren, J.; Landälv, I. Renewable methanol as a fuel for the shipping industry. Renew. Sustain. Energy Rev. 2018, 94, 1217–1228. [Google Scholar] [CrossRef]

- Aneziris, O.; Koromila, J.; Nivolianitou, Z. A systematic literature review on LNG safety at ports. Saf. Sci. 2020, 124, 104595. [Google Scholar] [CrossRef]

- Ashrafi, M.; Lister, J.; Gillen, D. Toward harmonization of sustainability criteria for alternative marine fuels. Marit. Transp. Res. 2022, 3, 100052. [Google Scholar] [CrossRef]

- KPGM International. The Pathway to Green Shipping; KPGM: Berlin, Germany, 2021. [Google Scholar]

- DNV-GL Maritime. Assessment of Selected Alternative Fuel and Technologies; DNV: Bærum, Norway, 2018. [Google Scholar]

- Andersson, K.; Salazar, C.M. Methanol as a Marine Fuel Report; Methanol Institute: Alexandria, VA, USA, 2015. [Google Scholar]

- Ellis, J.; Tanneberger, K. Study on the Use of Ethyl and Methyl Alcohol as Alternative Fuels in Shipping; European Maritime Safety Agency: Gothenburg, Sweden, 2015. [Google Scholar]

- Prussi, M.; Scarlat, N.; Acciaro, M.; Kosmos, V. Potential and limiting factors in the use of alternative fuels in the European maritime sector. J. Clean. Prod. 2021, 291, 125849. [Google Scholar] [CrossRef]

- BPO. Alternative Fuels’ Infrastructure for Ships in the Baltic Ports—Current Status and Outlook—Report; BPO: Tallinn, Estonia, 2020. [Google Scholar]

- ABS. Methanol as Marine Fuel—Sustainability Whitepaper; ABS: London, UK, 2021. [Google Scholar]

- IAE. Net Zero by 2050: Roadmap for the Global Energy Sector; IAE Publications: Paris, France, 2021. [Google Scholar]

- Al-Enazi, A.; Okonkwo, E.; Bicer, Y.; Al-Ausari, T. A review of cleaner alternative fuels for maritime transport. Energy Rep. 2021, 7, 1962–1985. [Google Scholar] [CrossRef]

- Stanĉin, H.; Mikulcić, H.; Wang, X.; Duić, N. A review on alternative fuels in future energy system. Renew. Sustain. Energy Rev. 2020, 128, 109927. [Google Scholar] [CrossRef]

- Bicer, Y.; Dincer, I. Clean Fuel options with hydrogen for see transportation: A life cycle approach. Int. J. Hydrog. Energy 2018, 42, 1179–1193. [Google Scholar] [CrossRef]

- Moradi, R.; Groth, K.M. Hydrogen storage and delivery: Review of the state of art technologies and risk and reliability analysis. Int. J. Hydrogen Energy 2019, 44, 12254–12269. [Google Scholar] [CrossRef]

- Wang, H.; Dautidis, P.; Zhang, Q. Ammonia-based green corridors for sustainable maritime transportation. Dig. Chem. Eng. 2023, 6, 100082. [Google Scholar] [CrossRef]

- Solakivi, T.; Paimander, A.; Ojala, L. Cost competitiveness of alternative maritime fuels in the new regulatory framework. Transp. Res. D Transp. Environ. 2022, 113, 103500. [Google Scholar] [CrossRef]

- Hansson, J.; Brynolf, S.; Fridell, E.; Letveer, M. The potential role of ammonia as marine fuel-based on energy system modelling and multi-criteria decision analysis. Sustainability 2020, 12, 3265. [Google Scholar] [CrossRef] [Green Version]

- Al-Booasi, F.Y.; El-Halwagi, M.M.; Moore, M.; Nielsen, R.B. Renewable ammonia as an alternative fuel for the shipping industry. Curr. Opin. Chem. Eng. 2021, 31, 100670. [Google Scholar] [CrossRef]

- Ershov, M.A.; Savelenko, V.D.; Makhmudova, A.E.; Rekhletskaya, E.S.; Makhova, U.A.; Kapustin, V.M.; Mukhina, D.Y.; Abdellatief, T.M.M. Technological Potential Analysis and Vacant Technology Forecasting in Properties and Composition of Low-Sulfur Marine Fuel Oil (VLSFO and ULSFO) Bunkered in Key World Ports. J. Mar. Sci. Eng. 2022, 10, 1828. [Google Scholar] [CrossRef]

- Abdellatief, T.M.M.; Ershov, M.A.; Kapustin, V.M.; Abdelkareem, M.A.; Kamil, M.; Olabi, A.G. Recent trends for introducing promising fuel components to enhance the anti-knock quality of gasoline: A systematic review. Fuel 2021, 291, 120112. [Google Scholar] [CrossRef]

- Abdellatief, T.M.M.; Ershov, M.A.; Kapustin, V.M.; Chernysheva, E.A.; Savelenko, V.D.; Salameh, T.; Abdelkareem, M.A.; Olabi, A.G. Novel promising octane hyperboosting using isoolefinic gasoline additives and its application on fuzzy modelling. Int. J. Hydrog. Energy 2022, 47, 4932–4941. [Google Scholar] [CrossRef]

- Ershov, M.A.; Potanin, D.A.; Tarazanov, S.V.; Abdellatief, T.M.M.; Kapustin, V.M. Blending characteristics of isooctane, MTBE, and TAME as gasoline components. Energy Fuels 2020, 34, 2816–2823. [Google Scholar] [CrossRef]

- Baresic, D.; Palmer, K. Climate Action in Shipping. Progress towards Shipping’s 2030 Breakthrough; Report of UMAS and UN Climate Change High Level Champions; Global Maritime Forum: Copenhagen, Denmark, 2022; Available online: https://www.globalmaritimeforum.org/getting-to-zero-coalition/resources-page (accessed on 25 September 2022).

- Smith, T.; Baresic, D.; Fahnestock, J.; Galbraith, C.; Perico, C.V.; Rojon, I.; Shaw, A. A Strategy for the Transition to Zero-Emission Shipping, An Analysis of Transition Pathways, Scenarios, and Levers for Change; UMAS: London, UK, 2021. [Google Scholar]

- EU. Proposal for a Regulation of the European Parliament and of The Council on the Use of Renewable and Low-Carbon Fuels in Maritime Transport and Amending Directive 2009/16/EC); COM(2021) 562 Final; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- ISO. Guidelines for Systems and Installations for Supply of LNG as Fuel to Ships; ISO: Geneva, Switzerland, 2015. [Google Scholar]

- Wang, Y.; Wright, L.A. A Comparative Review of alternative fuels for the Maritime Sector: Economic, Technology, and Policy Challenges for Clean energy Implementation. World 2021, 2, 456–481. [Google Scholar] [CrossRef]

- Jeong, B.; Lee, B.S.; Zhou, P.; Ha, S.M. Evaluation pf safety exclusion zone for bunkering station of LNG-fuelled ships. J. Mar. Eng. Technol. 2017, 16, 121–144. [Google Scholar] [CrossRef] [Green Version]

- Thinkstep. Life Cycle GHG Emission Study on the Use of LNG as Marine Fuel; Thinkstep: Leinfelden-Echterdingen, Germany, 2019. [Google Scholar]

- Le Fevre, C. A Review of Demand Prospects for LNG as a Marine Transport Fuel; Oxford Institute for Energy Studies: Oxford, UK, 2018. [Google Scholar] [CrossRef]

- Al-Breiki, M.; Bicer, Y. Comparative life cycle assessment of sustainable energy carriers including production, storage, overseas transport and utilization. J. Clean. Prod. 2021, 279, 123481. [Google Scholar] [CrossRef]

- Linstad, E.; Eskeland, G.S.; Rialland, A.; Valland, A. Decarbonizing Maritime Transport: The importance of Engine Technology and Regulations for LNG to Serve as a Transition Fuel. Sustainability 2020, 12, 8793. [Google Scholar] [CrossRef]

- DVN GL. Comparison of Alternative Marine Fuels; DVN GL: Høvik, Norway, 2019. [Google Scholar]

- IMO. Amendments to the IGF Code and Development of Guidelines for Low-Flashpoint Fuels; CCC 8/3; International Maritime Organization (IMO): London, UK, 2022. [Google Scholar]

- UN. United Nations Environmental Program (UNEP); UN: New York, NY, USA, 2006. [Google Scholar]

- Deniz, C.; Zincir, B. Environmental and economical assessment of alternative marine fuel. J. Clean. Prod. 2016, 13, 438–448. [Google Scholar] [CrossRef]

- McKinlay, C.J.; Turnock, S.R.; Hudson, D.A. A Comparison of Hydrogen and Ammonia for Future Long Distance Shipping Fuels; The Royal Institution of Naval Architects LNG/LPG and Alternative Fuels: London, UK, 2020. [Google Scholar]

- Goldmann, A.; Sauter, W.; Oettinger, M.; Kluge, T.; Schröder, U.; Seume, J.R.; Friedrichs, J.; Dinkelacker, F. A Study on Electrofuels in Aviation. Energies 2018, 11, 392. [Google Scholar] [CrossRef] [Green Version]

- Acar, C.; Dincer, I. Review and evaluation of hydrogen production options for better environment. J. Clean. Prod. 2019, 218, 835–849. [Google Scholar] [CrossRef]

- IMO. Amendments to the IGF Code and Development of Guidelines for Low-Flashpoint Fuels; CCC 7/3/9; International Maritime Organization (IMO): London, UK, 2021. [Google Scholar]

- IMO. Development of Guidelines for the Safety of Ships Using Ammonia as Fuel; CCC 8/13/1; International Maritime Organization (IMO): London, UK, 2022. [Google Scholar]

- Yapicioglu, A.; Dincer, I. A review on clean ammonia as a potential fuel for power generators. Renew. Sustain. Energy Rev. 2019, 103, 96–108. [Google Scholar] [CrossRef]

- Kim, K.; Roh, G.; Kim, W.; Chun, K. A preliminary study on an alternative ship propulsion system fueled by ammonia, Environmental and Economic assessments. J. Mar. Sci. Eng. 2020, 8, 183. [Google Scholar] [CrossRef] [Green Version]

- Interreg North-West Europe H2SHIPS. Comparative Report on Alternative Fuels for Ships Propulsion; Interreg: Lille, France, 2020. [Google Scholar]

- Jiang, L.; Kronbak, J.; Christensen, L. The costs and benefits of sulphur reduction measures: Sulphur scrubbers versus marine gas oil. Transp. Res. Part D Transp. Environ. 2014, 28, 19–27. [Google Scholar] [CrossRef]

- Corvus Energy. Case Study: Norled AS, MF Ampere, Ferry. Available online: http://files7.webydo.com/42/421998/UploadedFiles/a4465574-14ff-4689-a033-08ac32adada1.pdf (accessed on 10 November 2022).

- IMO. A Study on the Transportation Cost of a Liquefied Hydrogen Carrier Using Boil-Off-Gas as a Fuel; CCC 8/INF. 17; International Maritime Organization (IMO): London, UK, 2022. [Google Scholar]

- Frei, M.S.; Mondelli, C.; García-Muelas, R.; Kley, K.S.; Puértolas, B.; López, N.; Safonova, O.V.; Stewart, J.A.; Ferré, D.C.; PérezRamírez, J. Atomic-scale engineering of indium oxide promotion by palladium for methanol production via CO2 hydrogenation. Nat. Commun. 2019, 10, 3377. [Google Scholar] [CrossRef] [Green Version]

- Patel, S.K.S.; Gupta, R.K.; Kalia, V.C.; Lee, J. Integrating anaerobic digestion of potato peels to methanol production by methanotrophs immobilized on banana leaves. Bioresour. Technol. 2021, 323, 124550. [Google Scholar] [CrossRef] [PubMed]

- Zincir, B.; Deniz, C.; Tuner, M. Investigation of environmental, operational and economic performance of methanol partially premixed combustion at slow speed operation of a marine engine. J. Clean. Prod. 2019, 235, 1006–1019. [Google Scholar] [CrossRef]

- Wei, L.; Yao, C.; Wang, Q.; Pan, W.; Han, G. Combustion and emission characteristics of a turbocharger diesel engine using high premixed ratio pf methanol and diesel fuel. Fuel 2015, 140, 156–163. [Google Scholar] [CrossRef]

- Kang, W.C.; Myongho, K.; Jae-Jung, H. Development of a Marine LPG-Fueled High-Speed Engine for Electric Propulsion Systems. J. Mar. Sci. Eng. 2022, 10, 1498. [Google Scholar] [CrossRef]

- Andrews, J.; Shabani, B. Where does hydrogen fit in a sustainable energy economy? Procedia Eng. 2012, 49, 15–25. [Google Scholar] [CrossRef] [Green Version]

- IMO. Development of Guidelines for the Safety of Ships Using Ammonia as Fuel; CCC 8/13/2; International Maritime Organization (IMO): London, UK, 2022. [Google Scholar]

- Chen, C.; Yao, A.; Yao, C.; Wang, B.; Lu, H.; Feng, J.; Feng, L. Study of the characteristics of PM and the correlation of soot and smoke opacity on the diesel methanol dual fuel engine. Appl. Therm. Eng. 2019, 148, 391–403. [Google Scholar] [CrossRef]

- ISO 14040:2006; Environment Management-Life Cycle Assessment-Principles and Framework. ISO: Geneva, Switzerland, 2006.

- Linstad, E.; Lagemann, B.; Rialland, A.; Ganlem, G.; Valland, A. Reduction of maritime GHG emissions and potential role of E-fuels. Transp. Res. Part D 2021, 101, 103075. [Google Scholar] [CrossRef]

- Bengtsson, S.; Andersson, K.; Fridell, E. A comparative life cycle assessment of marine fuels: Liquefied natural gas and three other fossil fuels. Proc. Inst. Mech. Eng. Part M J. Eng. Marit. Environ. 2011, 225, 97–110. [Google Scholar] [CrossRef]

- Lind, M.; Pettersson, S.; Karlsson, J.; Steijaert, B.; Hermansson, P.; Haraldson, S.; Axell, M.; Zerem, A. Sustainable Ports as Energy Hubs, The Maritime Executive. 2020. Available online: https://www.maritime-executive.com/editorials/sustainable-ports-as-energy-hubs (accessed on 2 December 2021).

- Puig, M.; Wooldridge, C.; Darbra, M. ESPO Environmental Report 2022; ESPO Secretariat: Dublin, Ireland, 2022. [Google Scholar]

- Gibbs, D.; Rigot-Muller, P.; Mangan, J.; Lalwani, C. The role of sea ports in end-to-end maritime transport chain emissions. Energy Policy 2014, 64, 337–348. [Google Scholar] [CrossRef] [Green Version]

- Urbanyi-Popiołek, I.; Klopott, M. Container Terminals and Port City Interface—A Study of Gdynia and Gdańsk Ports. Transp. Res. Procedia 2016, 16, 517–526. [Google Scholar] [CrossRef] [Green Version]

- Klopott, M. Restructuring of Environmental Management of Baltic Ports—Case of Poland. Marit. Policy Manag. 2013, 40, 439–450. [Google Scholar] [CrossRef]

- Winnes, H.; Styhre, L.; Fridell, E. Reducing GHG emissions from ships in port areas. Res. Transp. Bus. Manag. 2015, 17, 73–82. [Google Scholar] [CrossRef] [Green Version]

- Notteboom, T.; van der Lugt, L.; van Saase, N.; Sel, S.; Neyens, K. The Role of Seaports in Green Supply Chain Management: Initiatives, Attitudes, and Perspectives in Rotterdam, Antwerp, North Sea Port, and Zeebrugge. Sustainability 2020, 12, 1688. [Google Scholar] [CrossRef] [Green Version]

- Klopott, M. Port as a link in the green supply chain—The example of the Port of Gdynia. In Maritime Transport IV; Rodriguez-Martos Dauer, R., Ed.; Universitat Politècnica de Catalunya: Barcelona, Spain, 2009. [Google Scholar]

- An, J.; Lee, K.; Park, H. Effects of a Vessel Speed Reduction Program on Air Quality in Port Areas: Focusing on the Big Three Ports in South Korea. J. Mar. Sci. Eng. 2021, 9, 407. [Google Scholar] [CrossRef]

- Mjelde, A.; Endresen, Ø.; Bjørshol, E.; Gierløff, C.W.; Husby, E.; Solheim, J.; Mjøs, N.; Eide, M.S. Differentiating on port fees to accelerate the green maritime transition. Mar. Pollut. Bull. 2019, 149, 110561. [Google Scholar] [CrossRef] [PubMed]

- Alamoush, A.S.; Ölçer, A.I.; Ballini, F. Ports’ role in shipping decarbonisation: A common port incentive scheme for shipping greenhouse gas emissions reduction. Clean. Logist. Supply Chain. 2022, 3, 100021. [Google Scholar] [CrossRef]

- Styhre, L.; Winnes, H.; Black, J.; Lee, J.; Le-Griffin, H. Greenhouse gas emissions from ships in ports—Case studies in four continents. Transp. Res. Part D Transp. Environ. 2017, 54, 212–224. [Google Scholar] [CrossRef]

- Acciaro, M.; Ghiara, H.; Cusano, M.I. Energy management in seaports: A new role for port authorities. Energy Policy 2014, 71, 4–12. [Google Scholar] [CrossRef]

- Densberger, N.L.; Bachkar, L. Towards accelerating the adoption of zero emissions cargo handling technologies in California ports: Lessons learned from the case of the Ports of Los Angeles and Long Beach. J. Clean. Prod. 2022, 347, 131255. [Google Scholar] [CrossRef]

- European Commission. Communication on a New Approach for a Sustainable Blue Economy in the EU; COM(2021) 240 Final; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- IMO. Reduction of GHG Emissions from Ships. Ports’ Perspective on Key Considerations Regarding the Decarbonization of Shipping, Submitted by IAPH; MEPC 79/7/19; International Maritime Organization (IMO): London, UK, 2022. [Google Scholar]

- IMO. Resolution MEPC.323(74) on Invitation to Member States to Encourage Voluntary Cooperation between the Port and Shipping Sectors to Contribute to Reducing GHG Emissions from Ships; International Maritime Organization (IMO): London, UK, 2019. [Google Scholar]

- European Commission. Proposal for a Regulation of the European Parliament and of The Council on the Deployment of Alternative Fuels Infrastructure, and Repealing Directive 2014/94/EU of the European Parliament and of the Council; COM(2021) 559 Final; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- IRENA. A Pathway to Decarbonize the Shipping Sector by 2050; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2021. [Google Scholar]

- Gucma, M.; Bąk, A.; Chłopińska, E. Concept of LNG transfer and bunkering model of vessels at South Baltic sea area. Annu. Navig. 2018, 25, 79–91. [Google Scholar] [CrossRef] [Green Version]

- Sharples, J. LNG Supply Chains and the Development of LNG as a Shipping Fuel in Northern Europe; The Oxford Institute for Energy Studies: Oxford, UK; Available online: https://www.oxfordenergy.org/wpcms/wp-content/uploads/2019/01/LNG-supply-chains-and-the-development-of-LNG-as-a-shipping-Fuel-in-Northern-Europe-NG-140.pdf (accessed on 27 October 2022).

- DNV. Alternative Fuels Insight Platform. Available online: https://afi.dnv.com/statistics/DDF10E2B-B6E9-41D6-BE2F-C12BB5660103 (accessed on 17 November 2022).

- SEA-LNG. Global Fleet. Available online: https://sea-lng.org/why-lng/global-fleet (accessed on 12 November 2022).

- ShippaxMarket 22. The 2021 Ferry, Cruise, Ro-Ro and High-Speed Year in Review with Analyses and Statistics; Shippax: Halmstad, Sweden, 2022. [Google Scholar]

- SEA-LNG. A Fuel in Transition. A View from the Bridge, SEA-LNG.ORG Report 2022. Available online: https://sea-lng.org/2022/01/sea-lng-2021-22-a-view-from-the-bridge/.pdf (accessed on 22 October 2022).

- DNV. Orders for LNG-Fueled Ships at Record Pace. Available online: https://maritime-executive.com/article/dnv-orders-for-lng-fueled-ships-at-record-pace (accessed on 12 October 2022).

- Conversion of LNG Terminals for Liquid Hydrogen or Ammonia. Fraunhofer Institute for Systems and Innovation Research ISI. Available online: https://www.google.com/Report_Conversion_of_LNG_Terminals_for_Liquid_Hydrogen_or_Ammonia.pdf (accessed on 2 January 2023).

- World LPG Association (WLPGA). LPG Bunkering Guide for LPG Marine Fuel Supply. Available online: https://www.google.com/FLPG-Bunkering-2019.pdf (accessed on 2 January 2023).

- Nektarios, A.M.; Konstantinos, D.M. Geopolitical Risk and the LNG-LPG Trade. Peace Econ. Peace Sci. Public Policy 2022, 28, 243–265. [Google Scholar] [CrossRef]

- Methanol Vessels on the Water and On the Way. Available online: https://www.methanol.org/wp-content/uploads/2022/07/Final-On-the-Water-and-on-the-Way.pdf (accessed on 11 October 2022).

- Methanol Institute. Ports with Available Methanol Storage Capacity. Available online: https://www.methanol.org/marine/ (accessed on 15 November 2022).

- Report on Methanol Supply, Bunkering Guidelines, and Infrastructure. Available online: https://www.fastwater.eu/images/fastwater/news/FASTWATER_D71.pdf (accessed on 18 October 2022).

- Methanol Dual-Fuel Chemical Tanker Takaroa Sun Conducts World’s First Barge-to-Ship Methanol Bunkering. Available online: https://www.nyk.com/english/news/2021/20210513_01.html (accessed on 15 October 2022).

- Stena Germanica First Non-Tanker Vessel in the World to be Ship-to-Ship Bunkered with Methanol. Available online: https://www.shippax.com/en/news/stena-germanica-first-non-tanker-vessel-in-the-world-to-be-ship-to-ship-bunkered-with-methanol-.aspx (accessed on 6 January 2023).

- Stena and Oljola Join Hands for a Dedicated Methanol Bunker Vessel. Available online: https://www.fleetmon.com/maritime-news/2022/40145/stena-and-oljola-join-hands-dedicated-methanol-bun/ (accessed on 19 November 2022).

- Ustolin, F.; Campari, A.; Taccani, R. An Extensive Review of Liquid Hydrogen in Transportation with Focus on the Maritime Sector. J. Mar. Sci. Eng. 2022, 10, 1222. [Google Scholar] [CrossRef]

- Hydrogen Bunkering Starts at Dutch Port, Offshore Wind Vessel First to Fuel Up. Available online: https://www.offshorewind.biz/2022/08/11/hydrogen-bunkering-starts-at-dutch-port-offshore-wind-vessel-first-to-fuel-up/ (accessed on 19 November 2022).

- Port of Amsterdam, Partners Push ahead with Plans for Large-Scale Hydrogen Import Facilities. Available online: https://www.offshore-energy.biz/port-of-amsterdam-partners-push-ahead-with-plans-for-large-scale-hydrogen-import-facilities/ (accessed on 30 October 2022).

- Hydrogen as a Marine Fuel. Sustainability White Paper. ABS. 2021. Available online: https://safety4sea.com/new-paper-examines-projected-role-of-hydrogen-as-marine-fuel/ (accessed on 2 October 2022).

- DNV. Smells Like Sustainability: Harnessing Ammonia as Ship Fuel. Available online: https://www.dnv.com/expert-story/maritime-impact/Harnessing-ammonia-as-ship-fuel.html (accessed on 20 November 2022).

- Laval, A.; Hafnia; Topsoe, H.; Vestas; Gamesa, S. Ammonfuel—An Industrial View of Ammonia as a Marine Fuel; Hafnia: Hellerup, Denmark, 2020. [Google Scholar]

- Prause, F.; Prause, G.; Philipp, R. Inventory Routing for Ammonia Supply in German Ports. Energies 2022, 15, 6485. [Google Scholar] [CrossRef]

- Ash, N.; Scarbrough, T. Sailing on Solar: Could Green Ammonia Decarbonize International Shipping? Environmental Defence Fund: London, UK, 2019. [Google Scholar]

- Green Fuel Alliance Plans Green Ammonia Facility for Bunkering at Suez Canal. Available online: https://www.offshore-energy.biz/green-fuel-alliance-plans-green-ammonia-facility-for-bunkering-at-suez-canal/ (accessed on 2 October 2022).

- AZANE. Fuel Solutions. Available online: https://www.econnectenergy.com/articles/azane-fuel-solutions (accessed on 12 November 2022).

- Adams, W.C. Conducting Semi-Structured Interviews. In Handbook of Practical Program Evaluation, 4th ed.; Wholey, J., Hatry, H., Newcomer, K., Eds.; Jossey-Bass: San Francisco, CA, USA, 2015. [Google Scholar] [CrossRef]

- Moller, A.P. Maersk Continues Green Transformation with Six Additional Large Container Vessels. Available online: https://www.maersk.com/news/articles/2022/10/05/maersk-continues-green-transformation (accessed on 7 October 2022).

- Angelopoulos, J.; Sahoo, S.; Visvikis, I.D. Commodity and Transportation Economic Market Interactions Revisited: New Evidence from a Dynamic Factor Model. Transp. Res. E Logist. Transp. Rev. 2020, 133, 101836. [Google Scholar] [CrossRef]

- Building Transparency for Investment in Alternative Fuel Infrastructure. Available online: https://www.dredging.org/news/101/building-transparency-for-investment-in-alternative-fuel-infrastructure (accessed on 8 July 2022).

- Getting to Zero Coalition, the Next Wave Green Corridors—A Special Report. 2021. Available online: https://www.globalmaritimeforum.org/content/2021/11/The-Next-Wave-Green-Corridors.pdf (accessed on 21 February 2022).

- COP26: Clydebank Declaration for Green Shipping Corridors; Policy Paper. Available online: https://www.gov.uk/government/publications/cop-26-clydebank-declaration-for-green-shipping-corridors/cop-26-clydebank-declaration-for-green-shipping-corridors (accessed on 3 April 2022).

{kind=link}

| Fuel | Challenges and Opportunities in Bunkering Alternative Fuels | Reference |

|---|---|---|

| LNG | The authors indicated the main challenges related to bunkering LNG: “investment costs and the lack of LNG infrastructure” “the investment costs, the required infrastructure and safety issues are major limitations” “if no effective infrastructure planning is implemented carefully” “the lack of LNG infrastructure in ports” “Investing in LNG infrastructure in the near term” “must be a global network of bunkering facilities for the fuel” The authors point to the opportunities associated with bunkering LNG: “the application of LNG leads to lower operating costs” “will increase the number of ports providing LNG bunkering services” “The fuelling infrastructure has widely developed beyond just a handful of key bunkering ports in recent times” “upscaling of bunkering infrastructure for LNG is growing” “the LNG bunkering infrastructure for ships is improving quite rapidly” | [15,16,17,18,19,20,21,22,23,24] |

| Methanol | The authors indicated the main challenges related to bunkering methanol: “further development of the bunkering infrastructure and distribution chains of methanol are required” “it is thought that several more terminals will be needed” “there may be a need for additional terminals for ship fuel” | [19,24,25,26,27,28,29] |

| The authors point to the opportunities associated with bunkering methanol: “the infrastructure for methanol available today is based on the worldwide distribution of methanol” “best alternative fuel, use of existing infrastructure” “potential investments in methanol bunkering infrastructure are reasonably low, and retrofitting of currently functioning infrastructure is a possibility” | ||

| Hydrogen | The authors indicated the main challenges related to bunkering hydrogen: “found a lack of reliable infrastructure” “infrastructure and bunkering facilities for hydrogen are not yet in place” “ammonia and hydrogen require the most new or modified infrastructure” “widespread utilization of clean fuels such as hydrogen and ammonia can be obstructed or delayed due to issues related to the underdeveloped infrastructure” “there is no distribution or bunkering infrastructure for ships” “hydrogen does not have a standardized design and fuelling procedure for ships and its bunkering infrastructure” “new infrastructure would costs over several billion dollars in the coming decade” “ammonia and hydrogen require the most new or modified infrastructure” | [18,23,26,27,28,29,30,31,32,33] |

| Ammonia | The authors indicated the main challenges related to ammonia: “found a lack of reliable infrastructure for the use of methanol, hydrogen ammonia and hydrogen require the most new or modified infrastructure” “Widespread utilization of clean fuels such as hydrogen and ammonia can be obstructed or delayed due to issues related to the underdeveloped infrastructure” “the existing bunkering and fuel infrastructure is not sufficient” “the development of bunkering infrastructure remains a barrier for the application of ammonia as a marine fuel” “ammonia and hydrogen require the most new or modified infrastructure” | [18,21,27,30,34,35,36,37] |

| The authors point to the opportunities associated with ammonia: “a well-established global ammonia storage and distribution infrastructure” “ammonia has existing global logistics infrastructure for transport and handling” |

| Advantages | Disadvantages |

|---|---|

| The cleanest fossil fuel available today | 40% lower volumetric energy density than diesel; increases injection time when used in internal combustion engines |

| No SOx emissions, particle emissions are very low | Twice the volume compared to the same energy stored in the form of HFO; requires more fuel tanks |

| The NOx emissions are lower than those of MGO or HFO | The storage temperature is −160 °C; requires an additional cryogenic plant |

| High energy density: approximately 18% higher than that of HFO | Risk of fire and explosion |

| The technology required to use LNG as a ship fuel is readily available | Methane release (slip); requires the installation of an additional ventilation system |

| Available worldwide and investments are underway in many places to make LNG available to ships | Reduction in CO2 is limited; limits the decrease in the Energy Efficiency Design Index |

| Bunkering infrastructure for ships is improving quite rapidly | Treated as a short-term solution, especially when targeting zero-emission shipping |

| Advantages | Disadvantages |

|---|---|

| More expensive than LNG but cheaper than traditional marine fuel (HFO) | Fuel tanks are larger than oil tanks due to the lower density of LPG Lack of bunkering infrastructure |

| Relatively easy to develop bunkering infrastructure at existing LPG storage locations or terminals by adding distribution installations | Reduction in CO2 is limited |

| Fuel supply system is technically simple, so the construction costs are relatively low compared to those of LNG | Formation of flammable atmosphere Risk of autoignition |

| Methane release (slip); requires the installation of an additional ventilation system |

| Advantages | Disadvantages |

|---|---|

| No emission of CO2, particulate matter (PM) or SOx | Low volumetric energy density, large fuel volume |

| High energy content per unit of mass | No distribution or bunkering infrastructure for ships |

| Suitable for relatively short distances | High flammability |

| NOx emission during combustion |

| Advantages | Disadvantages |

|---|---|

| No emission of CO2 | Low volumetric energy density, large fuel volume |

| Already produced in substantial amounts | Release of high levels of NOx during combustion of ammonia |

| Handling issues in maritime transport are already well-understood | N2O emission |

| Highly toxic and requires careful handling | |

| Strongly corrosive in its liquid state |

| Advantages | Disadvantages |

|---|---|

| Liquid at ambient temperature | 40% lower volumetric energy density than diesel oil |

| Easy to store and handle | Methanol fuel tanks have sizes approximately 2.5 times larger than oil tanks for the same energy content |

| Lower emissions of NO2 and CO2 than the corresponding emissions with oil-based fuels | Low-flashpoint fuel that represents fire risk |

| Minor modifications to existing storage and bunkering facilities needed | Toxic when inhaled |

| Already available in some port bunkering infrastructures | |

| Readily biodegradable |

| Type of Fuel | No. of Ships | Fuel Availability | Bunkering Method Currently Used | Port Infrastructure Availability | Location | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Active | In Order | Sea Terminals | STS | PTS | TTS | Existing | Planned | Existing | Planned | |

| LNG | 320 | 518 | High | Y | Y | Y | Y | Y | W | W |

| LPG | 28 | 93 | High | Y | Y | Y | Y | Y | W | W |

| Methanol | 22 | 58 | Limited | Y | N | Y | Y | Y | NE | E/SA |

| Hydrogen | 6 | 19 | Limited | N | N | Y | Y | Y | NE | NE |

| Ammonia | 0 | 0 | Limited | N | Y | N | Y | Y | NE | MED, NE |

| Port of Gdańsk | Port of Szczecin-Świnoujście | Port of Gdynia | |

|---|---|---|---|

| Surface area (land) | 1092 ha | 679 ha | 973 ha |

| Total length of quays | 23.7 km | 11.1 km | 11.2 km |

| Total turnover | 68.2 M tonnes | 36.8 M tonnes | 28.2 M tonnes |

| Container turnover | 2.07 million TEU | 75,381 TEU | 986,000 TEU |

| Max. draught | 17 m (outer port), 10.2 m (inner port) | 13.5 m | 13 m |

| Port of Gdańsk | Port of Szczecin-Świnoujście | Port of Gdynia | |

|---|---|---|---|

| LNG | Planned in 2027: regasification LNG terminal (FSRU); capacity up to 6.1 billion m3 per year | LNG import terminal; two cryogenic LNG storage tanks with a capacity of 160,000 m³ each | - |

| LPG | LPG terminal (import and export) on the territory of the northern port in Gdańsk; 16 diked tanks with a total storage capacity of 13,200 tonnes | - | LPG terminal; 12 storage tanks with a total capacity of approx. 1500 tonnes |

| Methanol | Possible | Not yet discussed | Not yet discussed |

| Ammonia | Not yet discussed | Not yet discussed | Not yet discussed |

| Hydrogen | Not yet discussed | Not yet discussed | Under consideration |

| Port of Gdańsk | Port of Szczecin-Świnoujście | Port of Gdynia | |

|---|---|---|---|

| Ship-to-ship | Under consideration | Under consideration | Under consideration |

| Truck-to-ship | In operation | In operation | In operation |

| Port-to-ship | Not yet discussed | Under consideration (ferry terminal) | Under consideration (ferry terminal) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Klopott, M.; Popek, M.; Urbanyi-Popiołek, I. Seaports’ Role in Ensuring the Availability of Alternative Marine Fuels—A Multi-Faceted Analysis. Energies 2023, 16, 3055. https://doi.org/10.3390/en16073055

Klopott M, Popek M, Urbanyi-Popiołek I. Seaports’ Role in Ensuring the Availability of Alternative Marine Fuels—A Multi-Faceted Analysis. Energies. 2023; 16(7):3055. https://doi.org/10.3390/en16073055

Chicago/Turabian StyleKlopott, Magdalena, Marzenna Popek, and Ilona Urbanyi-Popiołek. 2023. "Seaports’ Role in Ensuring the Availability of Alternative Marine Fuels—A Multi-Faceted Analysis" Energies 16, no. 7: 3055. https://doi.org/10.3390/en16073055