Strategies of Energy Suppliers and Consumer Awareness in Green Energy Optics

Abstract

:1. Introduction

2. Renewable Energy Sources—Problem Statement Part I

3. Dominant Strategy in Companies—USA, Canada, UK, Australia, Poland—Problem Statement Part II

- increasing dependence on inherently high-cost and remote resources (although natural gas in North America is a perhaps temporary exception to this trend);

- the need for reinvestment in aging energy infrastructure;

- the inevitable costs of higher environmental and social standards;

- and the emerging cost of carbon mitigation.

- A resource approach, where resources are at the heart of these organizations and build value through the ability to find and exploit unique resources. Competition for access to deposits, in addition to key know-how, knowledge, competencies, and experience of employees in the field of deposit exploitation, as well as access to technology. These are only a few selected examples characterizing the strategies of energy and utilities companies in the field of the resource approach.

- A positional approach, resulting in a shaping of the competitive position in the sector of differentiating the Chamberlin’s rent. Aggressive competition between entities in the sector is caused by, for example, the homogeneity of the product, building new barriers to entering the sector, as well as ensuring that exit from it is not simple. These are the selected tools for shaping their position by competing energy production companies. Other schools’ innovative-entrepreneurial and network approaches in this sector do not play a significant role.

4. Willingness to Pay for Green Energy—Problem Statement Part III

- (a)

- ratio of households to wind power in Sweden [65];

- (b)

- the impact of green energy projects (wind turbines) on the national landscape and how to reduce this impact as much as possible—Scotland [66];

- (c)

- identification of factors influencing the growth of the renewable energy market, as well as recommendations for the area in Germany [67]; the authors emphasised the role of state policy, and market liberalisation, which creates a window of opportunity;

- (d)

- (e)

- the use of the CV model to estimate willingness to pay in Korea [70];

- (f)

- mechanisms for potential investments in renewable energy using green energy tariffs and the Renewable Obligation Certificate (ROC) scheme [71], as well as the use of mixed logit models, which estimate the distribution of utility coefficients in the UK [72]; results from these studies suggest that although the adoption of renewable energy is valued by households, the value is not large enough to cover the individual costs of domestic investment;

- (g)

- the implementation of bioenergy programmes using biomass in Spain [73], which, according to studies, would result in an increase in the welfare of society;

- (h)

- identifying willingness to pay for support of increased R&D to replace fossil fuels in the USA [74];

- (i)

- Green energy prices by three groups of payers: “concerned”, “protest”, and “willing to pay”in Australia [75];

- (j)

- specific conditions of the downstream environment—a study conducted one year after the Fukushima tragedy, in two groups of consumers in the USA and Japan, in relation to two alternative energy sources: nuclear and renewable energy; for the Japanese population, a significant aversion to nuclear energy was shown [24];

- (k)

- the social acceptance of green energy in light of the policy implications and health consequences for residents of polluted countries, using the example of Greece [55]; in this research, it is particularly noteworthy to highlight the impact of a prolonged economic recession on the increased motivation of residents to make cost-effective energy choices (solar and wind energy);

- (l)

- the different demographic characteristics of the Turkish population [76].

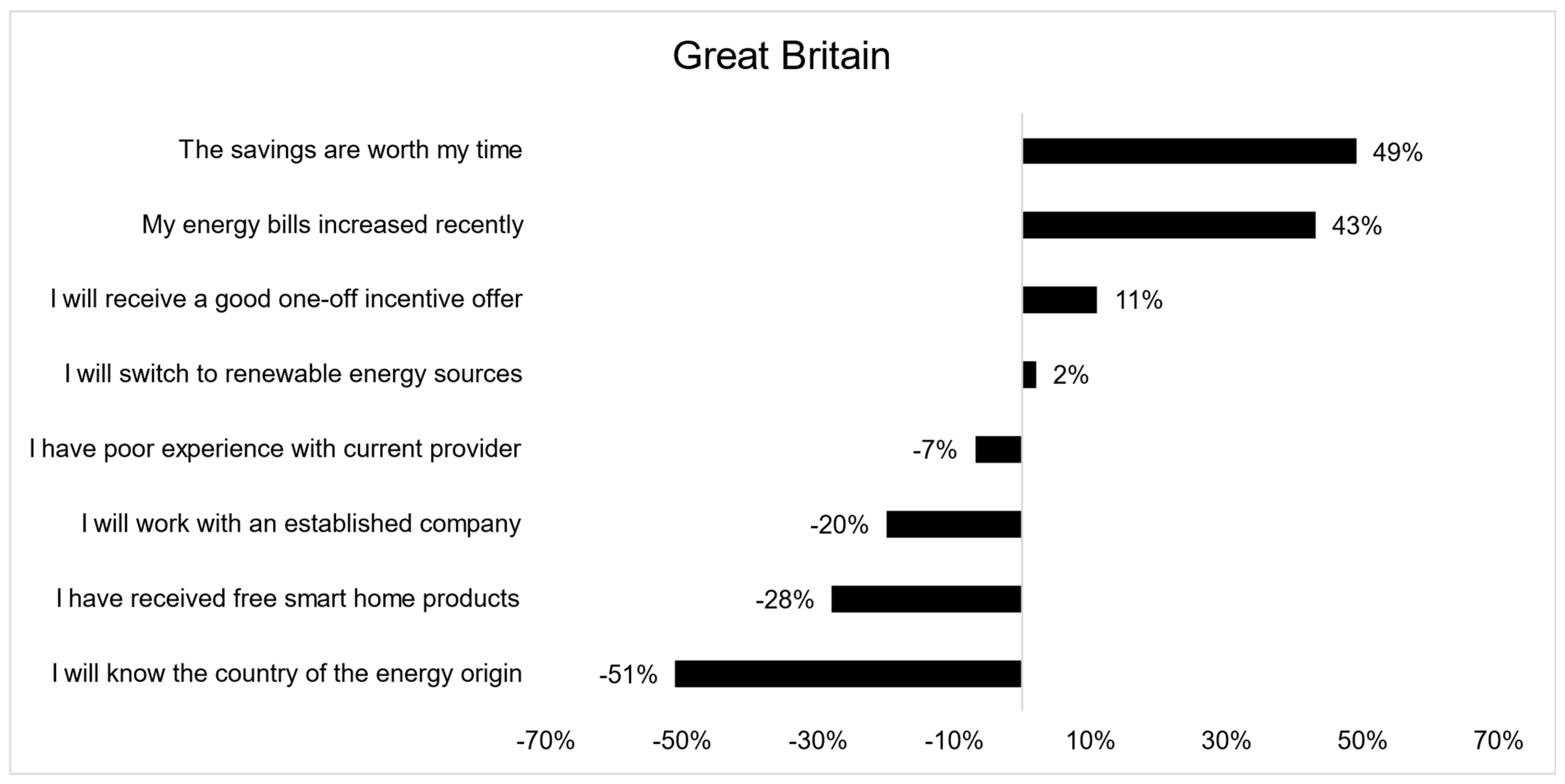

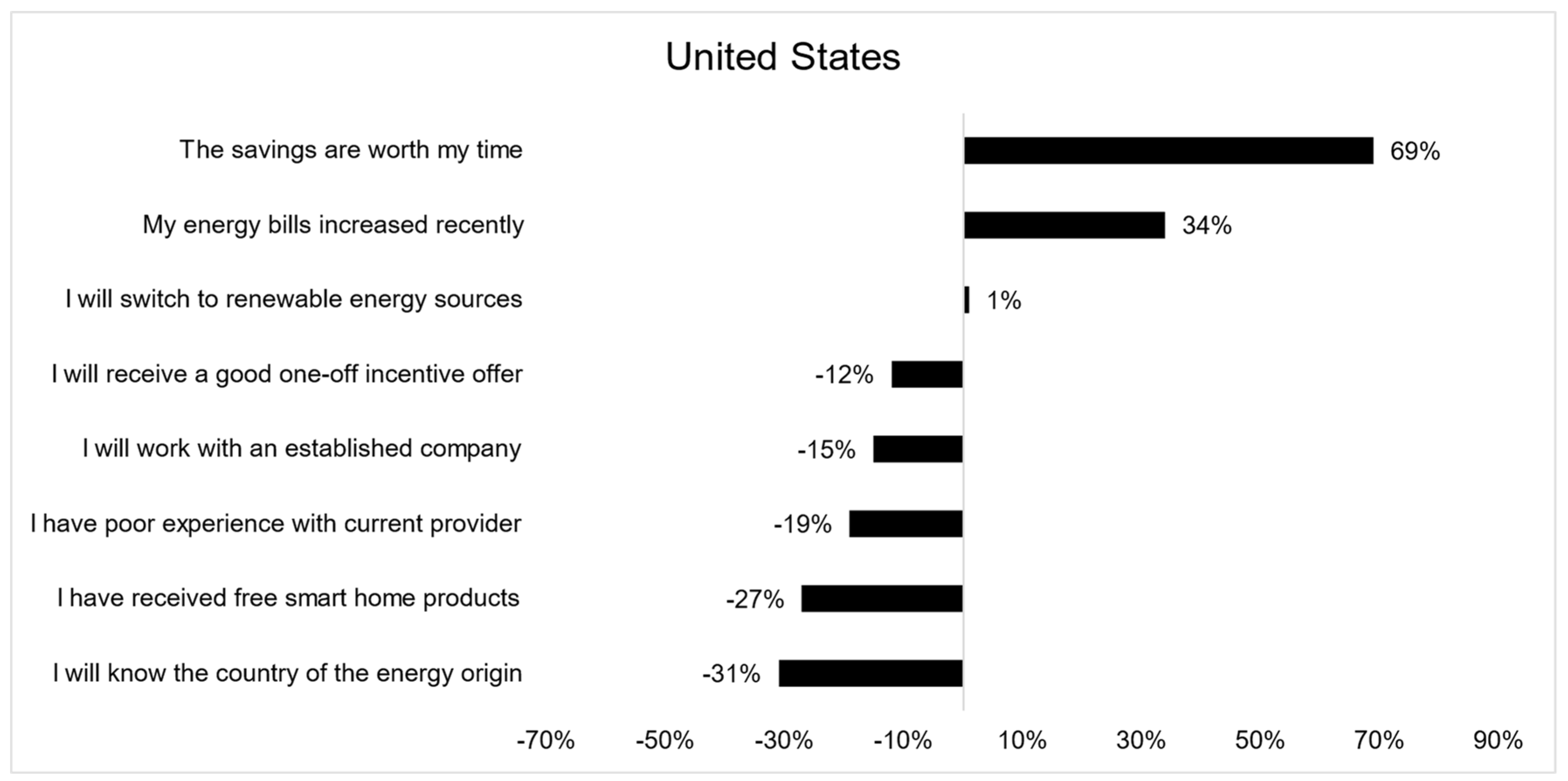

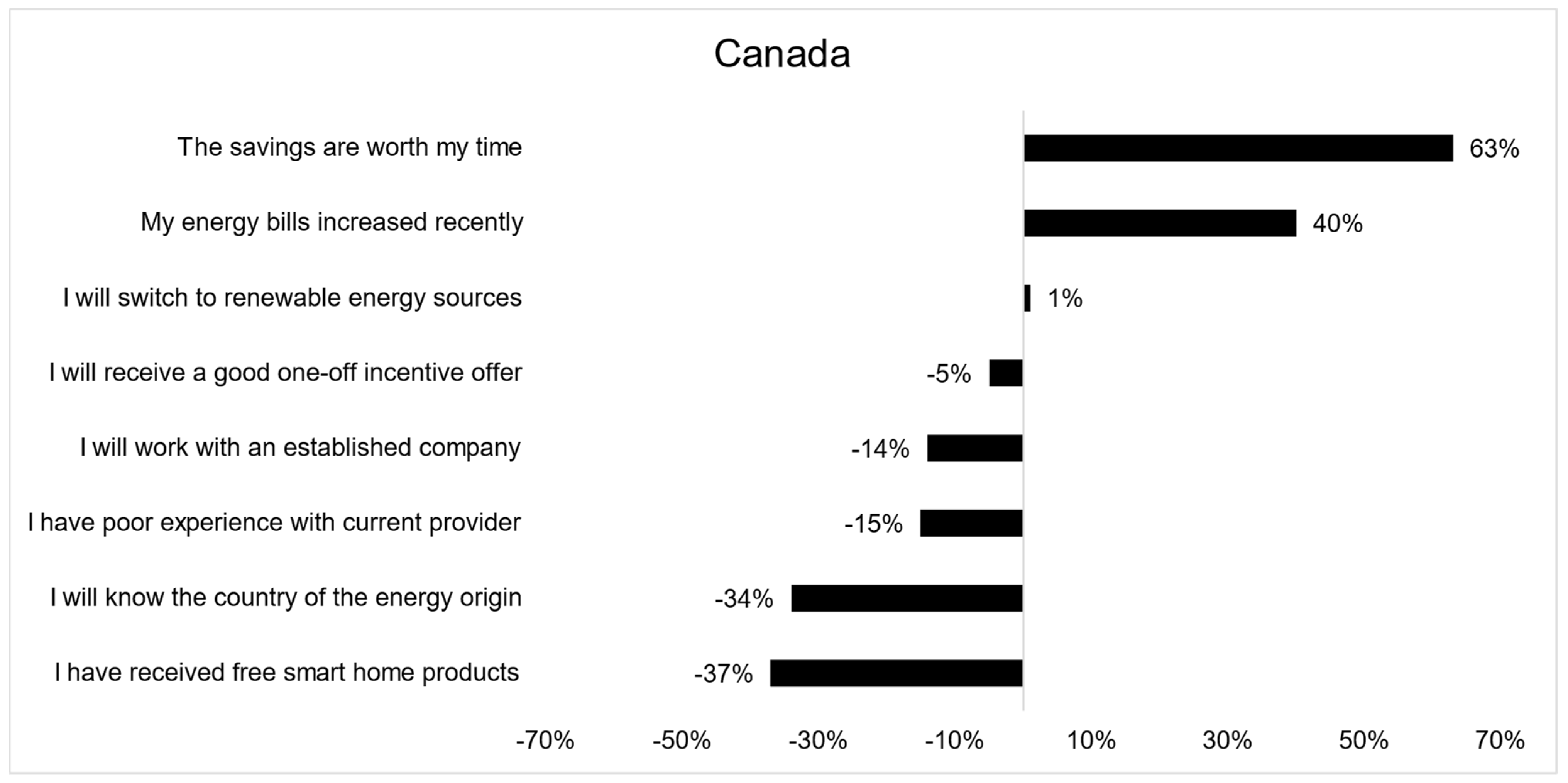

5. Research Methodology: Description of the Research Procedure and Research Sample

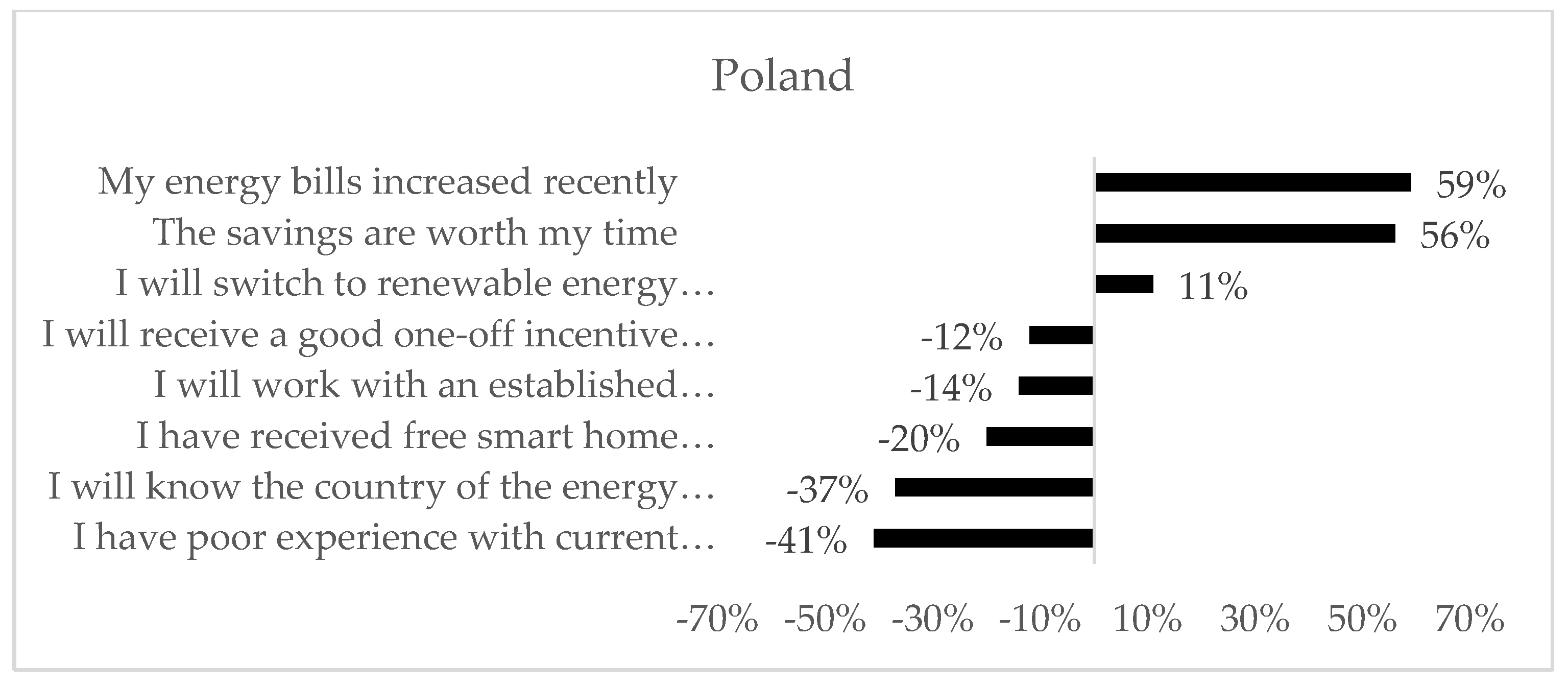

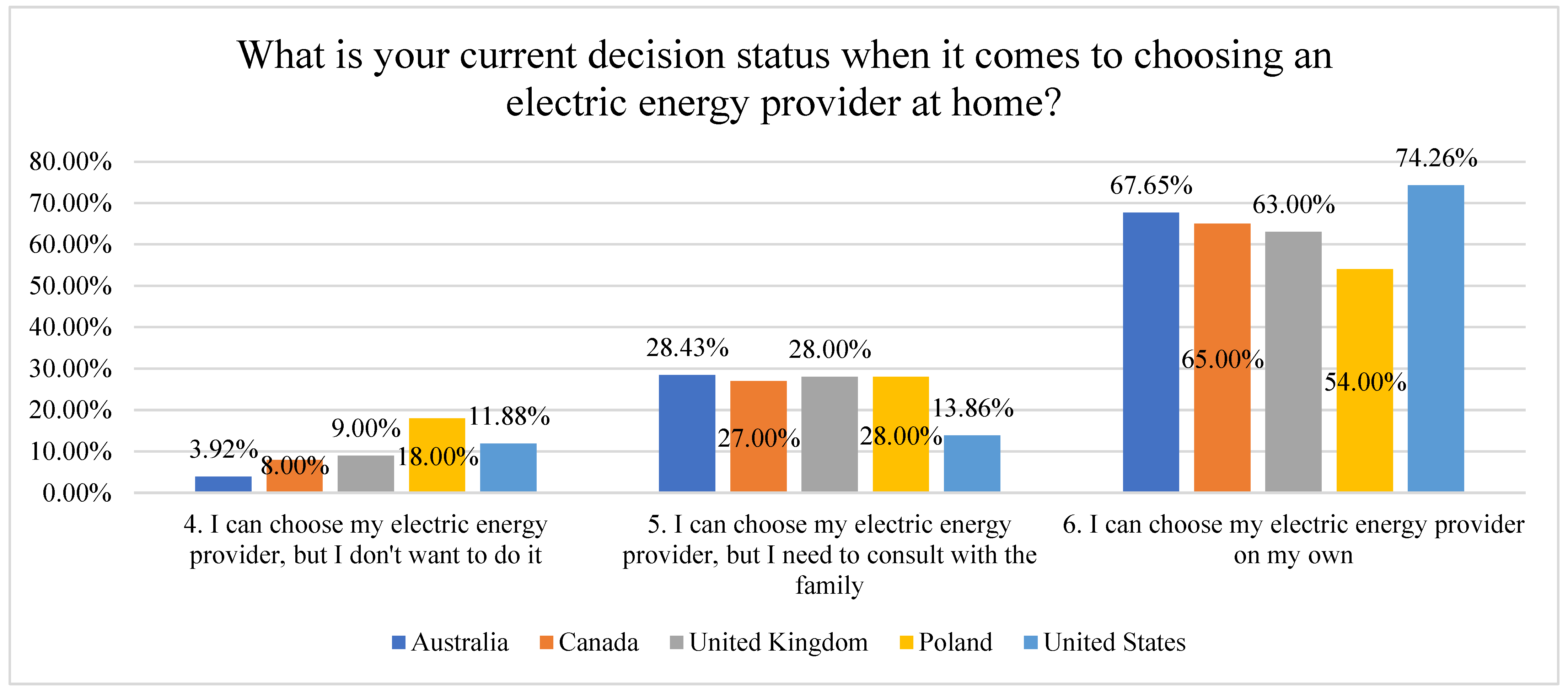

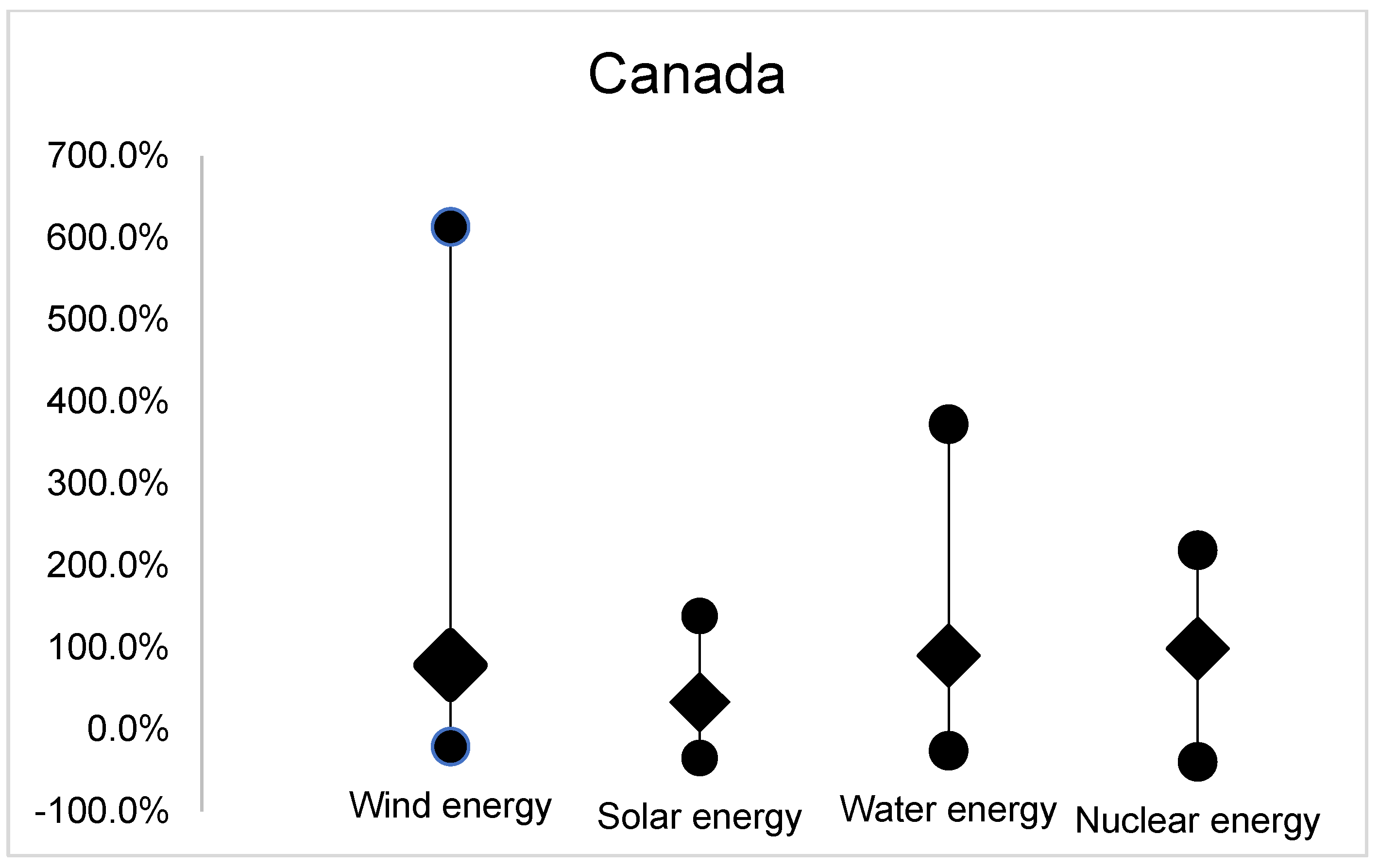

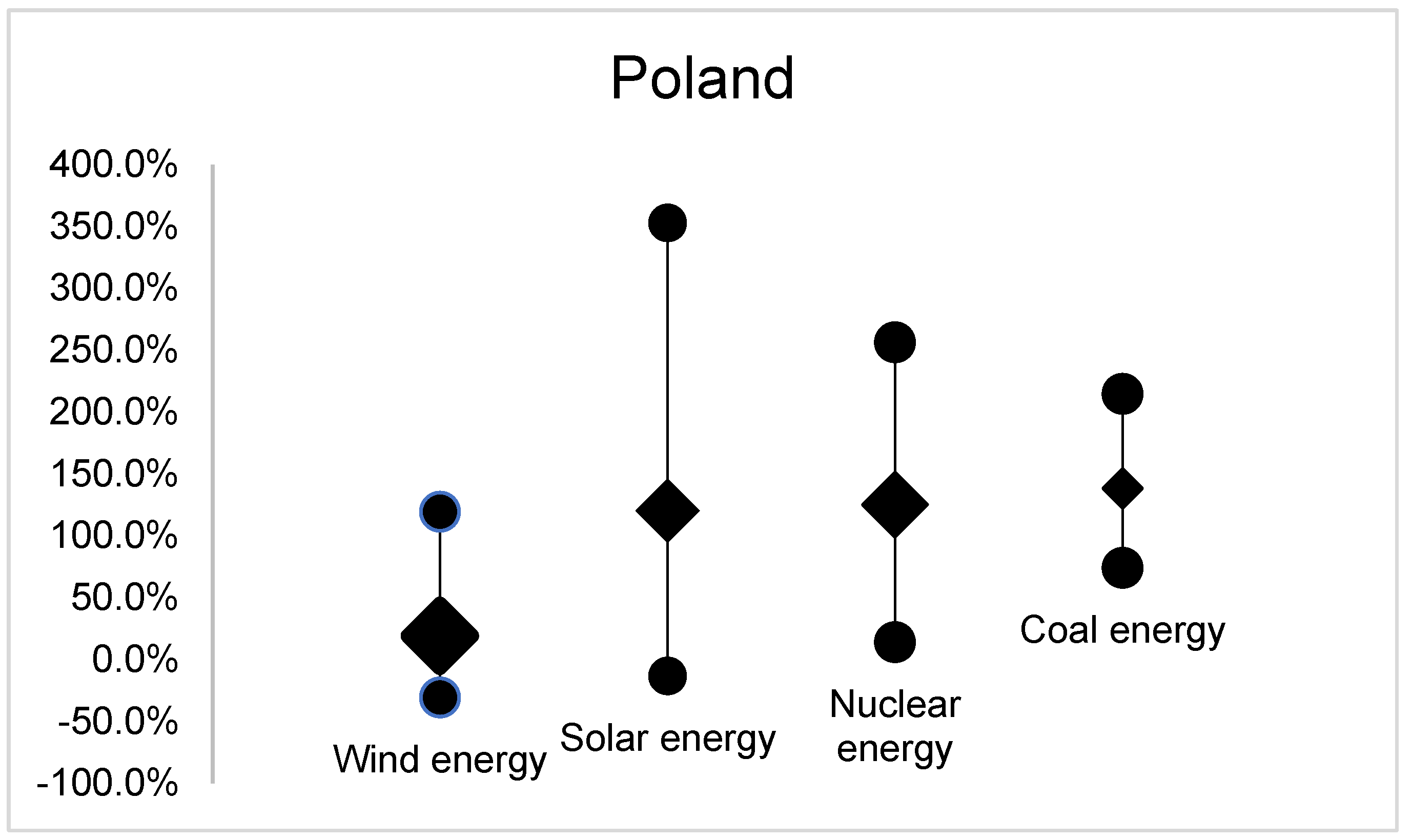

6. Results

- “1. I cannot choose the electric energy provider; my landlord does it for me”

- “2. I cannot choose the electric energy provider; someone in my family does it for me”

- “3. I cannot choose the electric energy provider due to contracts I already have”

7. Discussion & Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| CAP (MW) | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

| Hydropower | ||||||||||

| USA | 101,107 | 101,589 | 102,162 | 102,240 | 102,692 | 102,703 | 102,801 | 102,649 | 105,767 | 101,894 |

| Canada | 75,537 | 75,511 | 75,474 | 79,405 | 80,304 | 80,831 | 81,396 | 81,399 | 81,404 | 82,740 |

| Australia | 8271 | 8271 | 8271 | 8271 | 8271 | 8271 | 8523 | 8523 | 8523 | 8523 |

| UK | 4437 | 4453 | 4474 | 4677 | 4733 | 4770 | 4773 | 4773 | 4775 | 4793 |

| Poland | 2351 | 2355 | 2364 | 2370 | 2385 | 2390 | 2391 | 2397 | 2400 | 2384 |

| Renewable hydropower (including mixed plants) | ||||||||||

| USA | 82,442 | 82,903 | 83,386 | 83,374 | 83,665 | 83,644 o | 83,722 | 83,624 | 83,797 o | 79,982 o |

| Canada | 75,363 | 75,337 | 75,300 | 79,231 | 80,130 | 80,657 | 81,222 | 81,222 | 81,227 u | 82,563 u |

| Australia | 7461 | 7461 | 7461 | 7461 | 7461 | 7461 | 7713 o | 7713 o | 7713 o | 7713 o |

| UK | 1993 | 2009 | 2030 | 2077 | 2133 | 2170 e | 2173 | 2173 o | 2175 o | 2193 o |

| Poland | 945 | 949 | 958 | 964 | 972 | 967 | 968 | 974 e | 977 e | 1164 |

| Pure pumped storage | ||||||||||

| USA | 18,665 | 18,686 | 18,776 | 18,866 | 19,027 | 19,059 | 19,079 | 19,025 | 21,969 o | 21 912 o |

| Canada | 174 | 174 | 174 | 174 | 174 o | 174 e | 174 e | 177 | 177 e | 177 e |

| Australia | 810 | 810 | 810 | 810 | 810 | 810 | 810 | 810 o | 810 o | 810 o |

| UK | 2444 | 2444 | 2444 | 2600 | 2600 | 2600 | 2600 | 2600 o | 2600 o | 2600 o |

| Poland | 1406 | 1406 | 1406 | 1406 | 1413 | 1423 | 1423 | 1423 e | 1423 e | 1220 o |

| Marine energy | ||||||||||

| USA | - | 0 u | 0 e | 0 u | 0 u | 0 o | - | - | - | - |

| Canada | 20 | 20 | 20 | 20 | 20 | 20 | 20 e | 20 e | 20 e | 20 e |

| Australia | 1 | 1 | 1 | 1 | 1 | 1 e | 1 e | 1 o | 1 e | 1 e |

| UK | 9 | 8 | 9 | 9 | 9 | 13 | 18 | 20 | 22 o | 22 o |

| Poland | - | - | - | - | - | - | - | - | - | - |

| Wind energy 1 | ||||||||||

| USA | 59,075 | 59,973 | 64,232 | 72,573 | 81,286 | 87,597 | 94,516 | 104,052 | 118,732 | 132,738 |

| Canada | 6201 | 7801 | 9694 | 11,214 | 11,973 | 12,250 | 12,816 | 13,413 | 13,627 | 14,304 |

| Australia | 2561 | 3221 | 3797 | 4181 | 4324 | 4812 | 5442 | 6279 | 8603 | 8951 |

| UK | 9030 | 11,282 | 13,074 | 14,306 | 16,126 | 19,585 | 21,767 | 24,095 | 24,485 | 27,130 |

| Poland | 2564 | 3429 | 3836 | 4886 | 5747 | 5759 | 5766 | 5837 | 6298 | 6958 |

| Onshore wind energy | ||||||||||

| USA | 59,075 | 59,973 | 64,232 | 72,573 | 81,257 | 87,568 | 94,487 | 104,023 o | 118,703 o | 132,696 o |

| Canada | 6201 | 7801 | 9694 | 11,214 | 11,973 | 12,250 | 12,816 u | 13,413 u | 13,627 | 14,304 |

| Australia | 2561 | 3221 | 3797 | 4181 | 4324 | 4812 | 5442 | 6279 | 8603 o | 8951 o |

| UK | 6035 | 7586 | 8573 | 9212 | 10,833 | 12,597 | 13,551 | 14,125 | 14,102 o | 14,430 u |

| Poland | 2564 | 3429 | 3836 | 4886 | 5747 | 5759 | 5766 | 5837 | 6298 | 6958 u |

| Offshore wind energy | ||||||||||

| USA | - | - | 0 u | 0 u | 29 | 29 | 29 o | 29 o | 29 o | 42 o |

| Canada | - | - | - | - | - | - | - | - | - | - |

| Australia | - | - | - | - | - | - | - | - | - | - |

| UK | - | - | - | - | - | - | - | - | - | - |

| Poland | - | - | - | - | - | - | - | - | - | - |

| Solar energy 2 | ||||||||||

| USA | 8613 | 13,045 | 17,651 | 23,442 | 34,716 | 43,115 | 51,570 | 60,826 | 75,562 | 95,209 |

| Canada | 766 | 1210 | 1843 | 2519 | 2665 | 2932 | 3095 | 3327 | 3342 | 3630 |

| Australia | 3799 | 4568 | 5287 | 5946 | 6689 | 7354 | 8625 | 12,969 | 17,344 | 19,076 |

| UK | 1753 | 2937 | 5528 | 9601 | 11,914 | 12,760 | 13,073 | 13,346 | 13,462 | 13,689 |

| Poland | 1 | 2 | 27 | 108 | 187 | 287 | 562 | 1539 | 3955 | 6257 |

| Solar photovoltaic | ||||||||||

| USA | 8137 | 11,759 | 15,984 | 21,684 | 32,958 | 41,357 | 49,812 | 59,068 | 73,814 o | 93,713 o |

| Canada | 766 | 1210 | 1843 | 2519 | 2665 | 2932 | 3095 | 3327 | 3342 | 3630 |

| Australia | 3796 | 4565 | 5284 | 5943 | 6686 | 7352 | 8623 | 12,967 | 17,342 o | 19,074 o |

| UK | 1753 | 2937 | 5528 | 9601 | 11,914 | 12,760 | 13,073 | 13,346 | 13,462 o | 13,689 o |

| Poland | 1 | 2 | 27 | 108 | 187 | 287 | 562 | 1539 | 3955 | 6257 |

| Concentrated solar power | ||||||||||

| USA | 476 | 1286 | 1667 | 1758 | 1758 | 1758 o | 1758 o | 1758 o | 1748 o | 1496 o |

| Canada | - | - | - | - | - | - | - | - | - | - |

| Australia | 3 | 3 | 3 | 3 | 3 | 2 | 2 | 2 o | 2 e | 2 e |

| UK | - | - | - | - | - | - | - | - | - | - |

| Poland | - | - | - | - | - | - | - | - | - | - |

| Bioenergy | ||||||||||

| USA | 11,321 | 12,392 | 12,526 | 13,115 | 13,049 | 12,985 | 12,774 | 12,267 | 12,271 | 13,574 |

| Canada | 2013 | 2041 | 2497 | 2473 | 2540 | 2642 | 2654 | 2410 | 2416 | 2416 |

| Australia | 827 | 817 | 824 | 826 | 864 | 864 | 864 | 864 | 875 | 876 |

| UK | 3117 | 3791 | 4254 | 4808 | 5251 | 5514 | 6997 | 7165 | 7243 | 7259 |

| Poland | 583 | 735 | 816 | 961 | 974 | 968 | 1004 | 1010 | 1045 | 1045 |

| Solid biofuels and renewable waste | ||||||||||

| USA | 9015 o | 9966 o | 9977 o | 10,590 o | 10,519 o | 10,404 o | 10,159 o | 9841 o | 9840 o | 11,140 o |

| Canada | 1897 | 1925 | 2381 | 2357 | 2424 | 2503 | 2515 e | 2271 e | 2271 e | 2271 e |

| Australia | 597 | 597 | 598 | 598 | 674 o | 674 e | 674 e | 674 e | 678 e | 678 e |

| UK | 1742 | 2377 | 2723 | 3180 | 3477 | 3695 | 5161 | 5333 | 5405 o | 5418 o |

| Poland | 455 | 582 | 629 | 745 | 749 | 738 | 778 | 777 | 784 | 784 e |

| Renewable municipal waste | ||||||||||

| USA | 1205 o | 1222 o | 1222 o | 1270 o | 1270 o | 1270 o | 1270 o | 1270 o | 1270 o | 1270 o |

| Canada | 39 | 39 | 39 | 39 | 39 | 38 | 38 e | 38 e | 38 e | 38 e |

| Australia | - | - | - | - | - | - | - | - | - | 0 o |

| UK | 257 | 273 | 340 | 465 | 514 | 545 | 568 | 661 | 723 o | 733 o |

| Poland | - | - | - | 8 | 22 | 30 | 43 | 45 | 50 | 50 e |

| Biogas | ||||||||||

| USA | 2102 | 2271 | 2394 | 2370 | 2375 | 2416 | 2379 | 2303 | 2308 o | 2310 o |

| Canada | 116 | 116 | 116 | 116 | 116 | 139 | 139 e | 139 | 145 u | 145 u |

| Australia | 230 | 220 | 226 | 228 | 190 o | 190 o | 190 o | 190 | 197 o | 198 o |

| UK | 1375 o | 1414 o | 1531 o | 1628 o | 1774 o | 1819 o | 1836 o | 1832 o | 1838 o | 1841 o |

| Poland | 128 o | 153 o | 187 o | 216 o | 225 o | 229 e | 225 e | 233 e | 261 e | 261 e |

| Renewable energy share of electricity capacity | ||||||||||

| USA | 15.4 | 16.0 | 16.8 | 18.2 | 19.8 | 20.9 | 21.9 | 23.3 | 25.3 | 27.5 |

| Canada | 63.3 | 64.6 | 65.5 | 66.3 | 66.4 | 66.8 | 67.1 | 67.1 | 66.8 | 68.3 |

| Australia | 22.5 | 24.3 | 25.5 | 26.9 | 28.8 | 30.8 | 32.9 | 37.8 | 42.2 | 42.8 |

| UK | 16.6 | 21.4 | 25.8 | 32.0 | 35.9 | 38.2 | 40.7 | 44.6 | 45.1 | 46.5 |

| Poland | 11.6 | 14.3 | 15.7 | 18.5 | 20.7 | 18.6 | 19.3 | 21.5 | 24.9 | 29.9 |

References

- Aktar, M.A.; Alam, M.M.; Al-Amin, A.Q. Global Economic Crisis, Energy Use, CO2 Emissions, and Policy Roadmap amid COVID-19. Sustain. Prod. Consum. 2021, 26, 770–781. [Google Scholar] [CrossRef] [PubMed]

- Hojnik, J.; Ruzzier, M.; Fabri, S.; Klopčič, A.L. What You Give Is What You Get: Willingness to Pay for Green Energy. Renew. Energy 2021, 174, 733–746. [Google Scholar] [CrossRef]

- Halkos, G.E.; Gkampoura, E.-C. Evaluating the Effect of Economic Crisis on Energy Poverty in Europe. Renew. Sustain. Energy Rev. 2021, 144, 110981. [Google Scholar] [CrossRef]

- Brouwer, R.; Brander, L.; van Beukering, P. A Convenient Truth: Air Travel Passengers’ Willingness to Pay to Offset Their CO2 Emissions. Clim. Chang. 2008, 90, 299–313. [Google Scholar] [CrossRef]

- Niemczyk, J.; Borowski, K.; Trzaska, R.; Trzaska, M.; Sus, A.; Matuszewski, M. Identification of the Strategy of the Energy and Utilities Sector from the G7 Group Countries, from the Perspective of a Dominant Strategy Approach. Energies 2022, 15, 8562. [Google Scholar] [CrossRef]

- Sulich, A.; Sołoducho-Pelc, L. Renewable Energy Producers’ Strategies in the Visegrád Group Countries. Energies 2021, 14, 3048. [Google Scholar] [CrossRef]

- Loučanová, E.; Olšiaková, M.; Štofková, J. Open Business Model of Eco-Innovation for Sustainability Development: Implications for the Open-Innovation Dynamics of Slovakia. J. Open Innov. Technol. Mark. Complex. 2022, 8, 98. [Google Scholar] [CrossRef]

- Senkus, P.; Glabiszewski, W.; Wysokińska-Senkus, A.; Cyfert, S.; Batko, R. The Potential of Ecological Distributed Energy Generation Systems, Situation, and Perspective for Poland. Energies 2021, 14, 7966. [Google Scholar] [CrossRef]

- Tomaszewski, K.; Sekściński, A. Odnawialne Źródła Energii w Polsce—Perspektywa Lokalna i Regionalna. Rynek Energii 2020, 4, 10–19. [Google Scholar]

- Streimikiene, D.; Balezentis, T.; Alisauskaite-Seskiene, I.; Stankuniene, G.; Simanaviciene, Z. A Review of Willingness to Pay Studies for Climate Change Mitigation in the Energy Sector. Energies 2019, 12, 1481. [Google Scholar] [CrossRef]

- Rohdin, P.; Thollander, P. Barriers to and Driving Forces for Energy Efficiency in the Non-Energy Intensive Manufacturing Industry in Sweden. Energy 2006, 31, 1836–1844. [Google Scholar] [CrossRef] [Green Version]

- Bertoldi, P.; Rezessy, S.; Vine, E. Energy Service Companies in European Countries: Current Status and a Strategy to Foster Their Development. Energy Policy 2006, 34, 1818–1832. [Google Scholar] [CrossRef]

- Qin, Y.; Xu, Z.; Wang, X.; Škare, M. Green Energy Adoption and Its Determinants: A Bibliometric Analysis. Renew. Sustain. Energy Rev. 2022, 153, 111780. [Google Scholar] [CrossRef]

- Kahouli, B.; Hamdi, B.; Nafla, A.; Chabaane, N. Investigating the Relationship between ICT, Green Energy, Total Factor Productivity, and Ecological Footprint: Empirical Evidence from Saudi Arabia. Energy Strategy Rev. 2022, 42, 100871. [Google Scholar] [CrossRef]

- Pawłowski D Kryzys Energetyczny 2022–Przyczyny, Wzrost Cen. Jak Sobie Poradzić? Available online: https://magazynprzedsiebiorcy.pl/kryzys-energetyczny (accessed on 21 October 2022).

- Dietz, T.; Ostrom, E.; Stern, P.C. The Struggle to Govern the Commons. Science 2003, 302, 1907–1912. [Google Scholar] [CrossRef]

- Kosoy, N.; Brown, P.G.; Bosselmann, K.; Duraiappah, A.; Mackey, B.; Martinez-Alier, J.; Rogers, D.; Thomson, R. Pillars for a Flourishing Earth: Planetary Boundaries, Economic Growth Delusion and Green Economy. Curr. Opin. Environ. Sustain. 2012, 4, 74–79. [Google Scholar] [CrossRef]

- Niemczyk, J.; Sus, A.; Borowski, K.; Jasiński, B.; Jasińska, K. The Dominant Motives of Mergers and Acquisitions in the Energy Sector in Western Europe from the Perspective of Green Economy. Energies 2022, 15, 1065. [Google Scholar] [CrossRef]

- Daniel Tang, K.H. Climate Change Policies of the Four Largest Global Emitters of Greenhouse Gases: Their Similarities, Differences and Way Forward. J. Energy Res. Rev. 2022, 10, 19–35. [Google Scholar] [CrossRef]

- Kulkarni, S.S.; Wang, L.; Venetsanos, D. Managing Technology Transfer Challenges in the Renewable Energy Sector within the European Union. Wind 2022, 2, 150–174. [Google Scholar] [CrossRef]

- Del Río, P.; Peñasco, C.; Mir-Artigues, P. An Overview of Drivers and Barriers to Concentrated Solar Power in the European Union. Renew. Sustain. Energy Rev. 2018, 81, 1019–1029. [Google Scholar] [CrossRef]

- Cheng, D.; Shi, X.; Yu, J. The Impact of the Green Energy Infrastructure on Firm Productivity: Evidence from the Three Gorges Project in the People’s Republic of China; Asian Development Bank Institute: Tokyo, Japan, 2020. [Google Scholar] [CrossRef]

- Michalak, D.; Rosiek, K.; Szyja, P. Gospodarka Niskoemisyjna–Gospodarka Cyrkularna–Zielona Gospodarka; Uwarunkowania i Wzajemne Powiazania; Wydawnictwo Uniwersytetu Łódzkiego: Łódź, Poland, 2020. [Google Scholar]

- Murakami, K.; Ida, T.; Tanaka, M.; Friedman, L. Consumers’ Willingness to Pay for Renewable and Nuclear Energy: A Comparative Analysis between the US and Japan. Energy Econ. 2015, 50, 178–189. [Google Scholar] [CrossRef]

- Green productivity: An Approach to Sustainable Development Green Productivity. Available online: https://www.apo-tokyo.org/wp-content/uploads/2014/07/ind_gp_aasd-2002.pdf (accessed on 21 November 2022).

- Tuttle, T.; Heap, J. Green Productivity: Moving the Agenda. Int. J. Prod. Perform. Manag. 2008, 57, 93–106. [Google Scholar] [CrossRef]

- Porter, M.E.; der Linde, C. Toward a New Conception of the Environment-Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Rexhäuser, S.; Rammer, C. Environmental Innovations and Firm Profitability: Unmasking the Porter Hypothesis. Environ. Resour. Econ. 2014, 57, 145–167. [Google Scholar] [CrossRef]

- Zhang, D. Green Credit Regulation, Induced R&D and Green Productivity: Revisiting the Porter Hypothesis. Int. Rev. Financ. Anal. 2021, 75, 101723. [Google Scholar]

- Wu, W.; Huang, M.; Lv, H.; Wang, W.; Zhang, M. Does the Air Pollution Joint Prevention and Control Policy Possess the Porter Effect in China-Evidence from Two Perspectives. Environ. Impact Assess. Rev. 2021, 91, 106678. [Google Scholar] [CrossRef]

- Cudmore, B.A. Sustainable Energy: The Importance of Consumer Awareness, Acceptance, and Action. Int. J. Sustain. Dev. 2011, 14, 154–174. [Google Scholar] [CrossRef]

- Rośnie Świadomość Ekologiczna Polaków. Available online: https://biznes.newseria.pl/biuro-prasowe/energetyka/rosnie-swiadomosc,b1038027711 (accessed on 2 January 2023).

- Czarnecka, M.; Kinelski, G.; Stefańska, M.; Grzesiak, M.; Budka, B. Social Media Engagement in Shaping Green Energy Business Models. Energies 2022, 15, 1727. [Google Scholar] [CrossRef]

- Chomać-Pierzecka, E.; Sobczak, A.; Urbańczyk, E. RES Market Development and Public Awareness of the Economic and Environmental Dimension of the Energy Transformation in Poland and Lithuania. Energies 2022, 15, 5461. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Strategy: Techniques for Analyzing Industries and Competitors. Rev. Inteligência Compet. 2012, 2, 47–77. [Google Scholar]

- Obłój, K. O Definicji Strategii Raz Jeszcze. Prz. Organ. 2009, 5, 3–5. [Google Scholar] [CrossRef]

- Nag, R.; Hambrick, D.C.; Chen, M.-J. What Is Strategic Management, Really? Inductive Derivation of a Consensus Definition of the Field. Strateg. Manag. J. 2007, 28, 935–955. [Google Scholar] [CrossRef]

- Rumelt, R.P. Strategy in a Structural Break. McKinsey Q. 2009, 1, 35–42. [Google Scholar]

- Obłój, K.; Obłój, T. Dominujaca Logika Skutecznych Strategii–Wyniki Badań Jakościowych. Koncepcja Dominujacej Logiki. Prz. Organ. 2006, 4, 9–12. [Google Scholar]

- Drucker, P.F. Zarzadzanie XXI Wieku-Wyzwania; New Media Srl Aliberti Editore: Warsaw, Poland, 2010. [Google Scholar]

- Ludwicki, T. Świat Strategii. Prz. Organ. 1995, 4, 13–16. [Google Scholar] [CrossRef]

- Szczerbowski, R. Polityka Energetyczna Wybranych Krajów Europejskich a Strategia Energetyczna Polski. Polityka Energetyczna 2015, 18, 5–14. [Google Scholar]

- Moore, M. An Energy Strategy for Canada; Canadian Global Affairs Institute: Ottawa, ON, Canada, 2015. [Google Scholar]

- Krog, L.; Sperling, K. A Comprehensive Framework for Strategic Energy Planning Based on Danish and International Insights. Energy Strategy Rev. 2019, 24, 83–93. [Google Scholar] [CrossRef]

- Nagy, K.; Körmendi, K. Use of Renewable Energy Sources in Light of the “New Energy Strategy for Europe 2011–2020”. Appl. Energy 2012, 96, 393–399. [Google Scholar] [CrossRef]

- Winston, A.; Favaloro, G.; Healy, T. Energy Strategy for the C-Suite. Harv. Bus. Rev. 2017, 95, 139–146. [Google Scholar]

- Ralston, B. How to Develop a Customized Corporate Energy Strategy. Strategy Leadersh. 2008, 36, 30–39. [Google Scholar] [CrossRef]

- Galani, D.; Gravas, E.; Stavropoulos, A. Company Characteristics and Environmental Policy. Bus. Strategy Environ. 2012, 21, 236–247. [Google Scholar] [CrossRef]

- Christoffersen, L.B.; Larsen, A.; Togeby, M. Empirical Analysis of Energy Management in Danish Industry. J. Clean Prod. 2006, 14, 516–526. [Google Scholar] [CrossRef]

- Rudberg, M.; Waldemarsson, M.; Lidestam, H. Strategic Perspectives on Energy Management: A Case Study in the Process Industry. Appl Energy 2013, 104, 487–496. [Google Scholar] [CrossRef]

- Borchers, A.M.; Duke, J.M.; Parsons, G.R. Does Willingness to Pay for Green Energy Differ by Source? Energy Policy 2007, 35, 3327–3334. [Google Scholar] [CrossRef]

- Zografakis, N.; Sifaki, E.; Pagalou, M.; Nikitaki, G.; Psarakis, V.; Tsagarakis, K.P. Assessment of Public Acceptance and Willingness to Pay for Renewable Energy Sources in Crete. Renew. Sustain. Energy Rev. 2010, 14, 1088–1095. [Google Scholar] [CrossRef]

- Kostakis, I.; Sardianou, E. Which Factors Affect the Willingness of Tourists to Pay for Renewable Energy? Renew Energy 2012, 38, 169–172. [Google Scholar] [CrossRef]

- Ma, C.; Rogers, A.A.; Kragt, M.E.; Zhang, F.; Polyakov, M.; Gibson, F.; Chalak, M.; Pandit, R.; Tapsuwan, S. Consumers’ Willingness to Pay for Renewable Energy: A Meta-Regression Analysis. Resour. Energy Econ. 2015, 42, 93–109. [Google Scholar] [CrossRef]

- Ntanos, S.; Kyriakopoulos, G.; Chalikias, M.; Arabatzis, G.; Skordoulis, M. Public Perceptions and Willingness to Pay for Renewable Energy: A Case Study from Greece. Sustainability 2018, 10, 687. [Google Scholar] [CrossRef]

- le Gall-Ely, M. Definition, Measurement and Determinants of the Consumer’s Willingness to Pay: A Critical Synthesis and Avenues for Further Research. Rech. Et Appl. En Mark. 2009, 24, 91–112. [Google Scholar] [CrossRef]

- Nemet, G.F.; Johnson, E. Willingness to Pay for Climate Policy: A Review of Estimates; Working Paper Series, La Follette School Working Paper No. 2010-011; University of Wisconsin-Madison: Madison, WI, USA, 2010. [Google Scholar]

- Reynolds, T.; Kolodinsky, J.; Murray, B. Consumer Preferences and Willingness to Pay for Compact Fluorescent Lighting: Policy Implications for Energy Efficiency Promotion in Saint Lucia. Energy Policy 2012, 41, 712–722. [Google Scholar] [CrossRef]

- Biswas, A.; Roy, M. A Study of Consumers’ Willingness to Pay for Green Products. J. Adv. Manag. Sci. 2016, 4, 211–215. [Google Scholar] [CrossRef]

- Miller, K.; Hofstetter, R.; Krohmer, H.; Zhang, J. Measuring Consumers’ Willingness to Pay. Which Method Fits Best? GfK Mark. Intell. Rev. 2012, 4, 42–49. [Google Scholar] [CrossRef]

- Breidert, C.; Hahsler, M.; Reutterer, T. A Review of Methods for Measuring Willingness-to-Pay. Innov. Mark. 2006, 2, 8–32. [Google Scholar]

- Soliño, M.; Farizo, B.A.; Campos, P. The Influence of Home-Site Factors on Residents’ Willingness to Pay: An Application for Power Generation from Scrubland in Galicia, Spain. Energy Policy 2009, 37, 4055–4065. [Google Scholar] [CrossRef]

- Sardianou, E.; Genoudi, P. Which Factors Affect the Willingness of Consumers to Adopt Renewable Energies? Renew Energy 2013, 57, 1–4. [Google Scholar] [CrossRef]

- Bollino, C.A. The Willingness to Pay for Renewable Energy Sources: The Case of Italy with Socio-Demographic Determinants. Energy J. 2009, 30, 81–96. [Google Scholar]

- Ek, K. Public and Private Attitudes towards “Green” Electricity: The Case of Swedish Wind Power. Energy Policy 2005, 33, 1677–1689. [Google Scholar] [CrossRef]

- Bergmann, A.; Hanley, N.; Wright, R. Valuing the Attributes of Renewable Energy Investments. Energy Policy 2006, 34, 1004–1014. [Google Scholar] [CrossRef]

- Wüstenhagen, R.; Bilharz, M. Green Energy Market Development in Germany: Effective Public Policy and Emerging Customer Demand. Energy Policy 2006, 34, 1681–1696. [Google Scholar] [CrossRef]

- Wang, H.; Mullahy, J. Willingness to Pay for Reducing Fatal Risk by Improving Air Quality: A Contingent Valuation Study in Chongqing, China. Sci. Total Environ. 2006, 367, 50–57. [Google Scholar] [CrossRef] [PubMed]

- Zhang, L.; Sun, C.; Liu, H.; Zheng, S. The Role of Public Information in Increasing Homebuyers’ Willingness-to-Pay for Green Housing: Evidence from Beijing. Ecol. Econ. 2016, 129, 40–49. [Google Scholar] [CrossRef]

- Yoo, S.-H.; Kwak, S.-Y. Willingness to Pay for Green Electricity in Korea: A Contingent Valuation Study. Energy Policy 2009, 37, 5408–5416. [Google Scholar] [CrossRef]

- Diaz-Rainey, I.; Ashton, J.K. Stuck between a ROC and a Hard Place? Barriers to the Take up of Green Energy in the UK. Energy Policy 2008, 36, 3053–3061. [Google Scholar] [CrossRef]

- Scarpa, R.; Willis, K. Willingness-to-Pay for Renewable Energy: Primary and Discretionary Choice of British Households’ for Micro-Generation Technologies. Energy Econ. 2010, 32, 129–136. [Google Scholar] [CrossRef]

- Solino, M.; Vazquez, M.X.; Prada, A. Social Demand for Electricity from Forest Biomass in Spain: Does Payment Periodicity Affect the Willingness to Pay? Energy Policy 2009, 37, 531–540. [Google Scholar] [CrossRef]

- Li, H.; Jenkins-Smith, H.C.; Silva, C.L.; Berrens, R.P.; Herron, K.G. Public Support for Reducing US Reliance on Fossil Fuels: Investigating Household Willingness-to-Pay for Energy Research and Development. Ecol. Econ. 2009, 68, 731–742. [Google Scholar] [CrossRef]

- Ivanova, G.A. Consumers’ Willingness to Pay for Electricity from Renewable Energy Sources, Queensland, Australia. Int. J. Renew. Energy Res. 2013, 2, 758–766. [Google Scholar]

- Muhammad, I.; Shabbir, M.S.; Saleem, S.; Bilal, K.; Ulucak, R. Nexus between Willingness to Pay for Renewable Energy Sources: Evidence from Turkey. Environ. Sci. Pollut. Res. 2021, 28, 2972–2986. [Google Scholar] [CrossRef]

- van Westendorp, P.H. NSS Price Sensitivity Meter (PSM)—A New Approach to Study Consumer Perception of Prices. In Proceedings of the 29th ESOMAR Congress, Venice, Italy, 5–9 September 1976; Volume 139167. [Google Scholar]

- Stefan, A.; Paul, L. Does It Pay to Be Green? A Systematic Overview. Acad. Manag. Perspect. 2008, 22, 45–62. [Google Scholar] [CrossRef] [Green Version]

- KPRM Czysta Energia, Czyste Powietrze. Available online: https://www.gov.pl/web/polski-lad/czysta-energia-czyste-powietrze (accessed on 21 January 2023).

- Mitchell, C.; Connor, P. Renewable Energy Policy in the UK 1990–2003. Energy Policy 2004, 32, 1935–1947. [Google Scholar] [CrossRef]

- Mundaca, L.; Richter, J.L. Assessing ‘Green Energy Economy’Stimulus Packages: Evidence from the US Programs Targeting Renewable Energy. Renew. Sustain. Energy Rev. 2015, 42, 1174–1186. [Google Scholar] [CrossRef]

- Liming, H.; Haque, E.; Barg, S. Public Policy Discourse, Planning and Measures toward Sustainable Energy Strategies in Canada. Renew. Sustain. Energy Rev. 2008, 12, 91–115. [Google Scholar] [CrossRef]

- Zahedi, A. Australian Renewable Energy Progress. Renew. Sustain. Energy Rev. 2010, 14, 2208–2213. [Google Scholar] [CrossRef]

| CAP (MW) | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|---|---|---|---|

| USA | 263,279 | 272,622 | 286,380 | 308,002 | 331,723 | 348,336 | 367,056 | 388,933 | 419,978 | 457,857 |

| Canada | 84,363 | 86,409 | 89,354 | 95,457 | 97,328 | 98,501 | 99,807 | 100,392 | 100,632 | 102,932 |

| Australia | 14,649 | 16,068 | 17,370 | 18,415 | 19,339 | 20,492 | 22,645 | 27,826 | 34,536 | 36,617 |

| UK | 15,902 | 20,027 | 24,895 | 30,800 | 35,433 | 40,043 | 44,028 | 46,800 | 47,387 | 50,293 |

| Poland | 4094 | 5116 | 5638 | 6919 | 7881 | 7982 | 8301 | 9360 | 12,275 | 15,424 |

| Scenario | Scenario 1: Roller Coaster | Scenario 2: Stuck on Carbon |

|---|---|---|

| Future Energy Markets: | Shift to Alternatives | Abundant Hydrocarbons |

| Global Climate Changes: | Abrupt Effects | Incremental Effects |

| Global Environmental Values and Priorities: | Global Agreement; National Discords | Global Disagreement; National Accords |

| World Economic Growth: | Developing Global Economy | Economic Nationalism |

| Selected Approaches to Strategy | Name of the Strategy Approach | Basic Cognitive Assumptions of Selected Approaches to the Strategy | Keywords for Selected Approaches to the Strategy |

|---|---|---|---|

| Classic approaches to strategy (1950–2008) | planning | The implementation of the Ricardian rent. The guideline for action is to focus on the economies of scale and scope. | economy scale, Ansoff |

| positional | The implementation of the Chamberlin’s rent. The guideline for action is to build the structure of market shares in order to take a privileged competitive position. | industry analysis, Porter, portfolio, matrix, value chain | |

| resource | The implementation of the Ricardian rent. The guideline for action is to build value for shareholders based on the RBV on the basis of a bundle of key competences. | Resources Based View, core competences, competences | |

| Modern approaches to strategy | innovative | Realization of the Schumpeter’s rent. The guideline for action is to focus on breakthrough innovations also achieved in open innovation systems. | Schumpeter, disruptive innovation, open innovation |

| (2008–2020) | network | The realization of the rent resulting from the network effect. The guideline for action is to build a network of dependencies in a way that allows for synergy. | network, network effect |

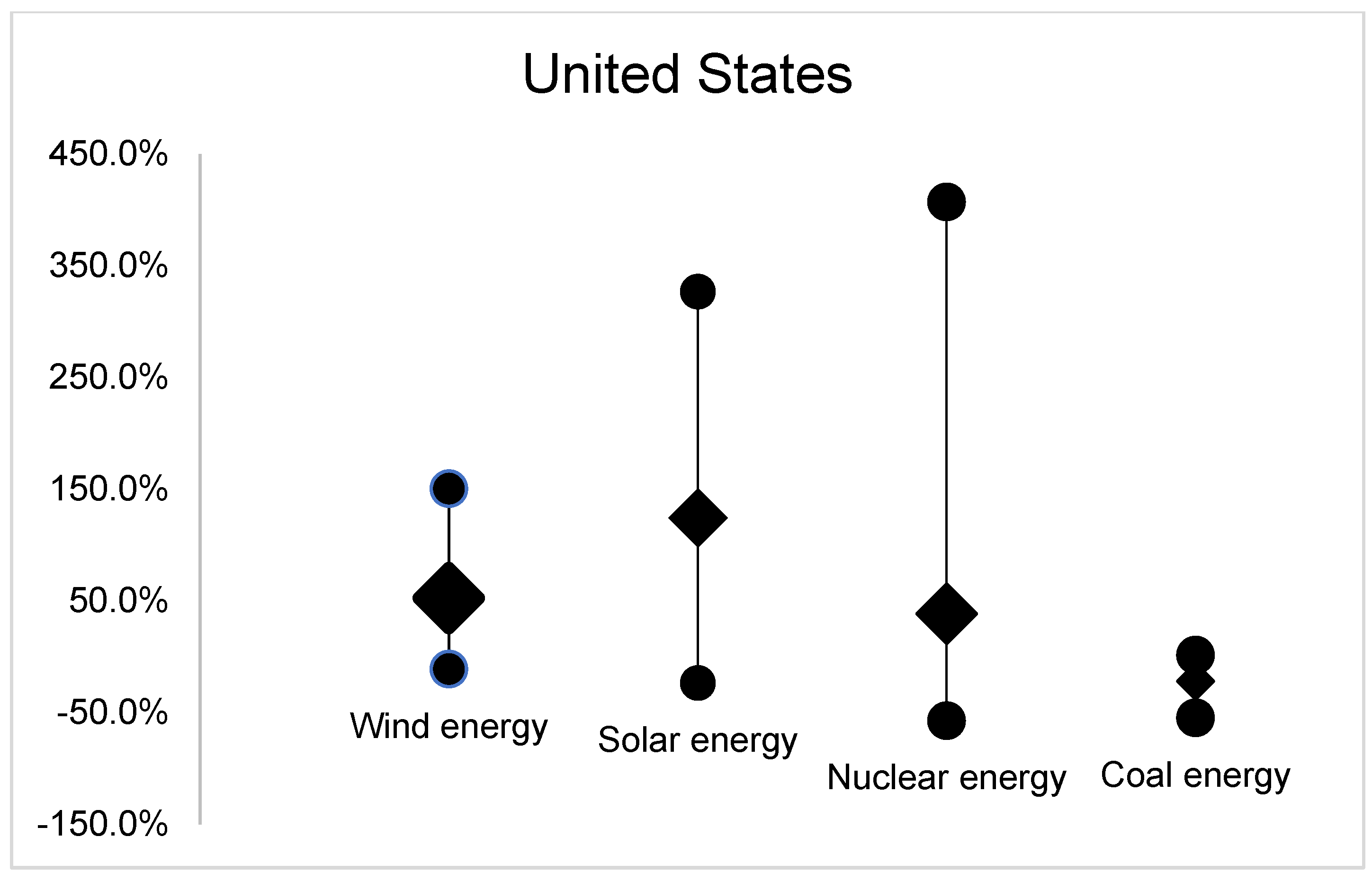

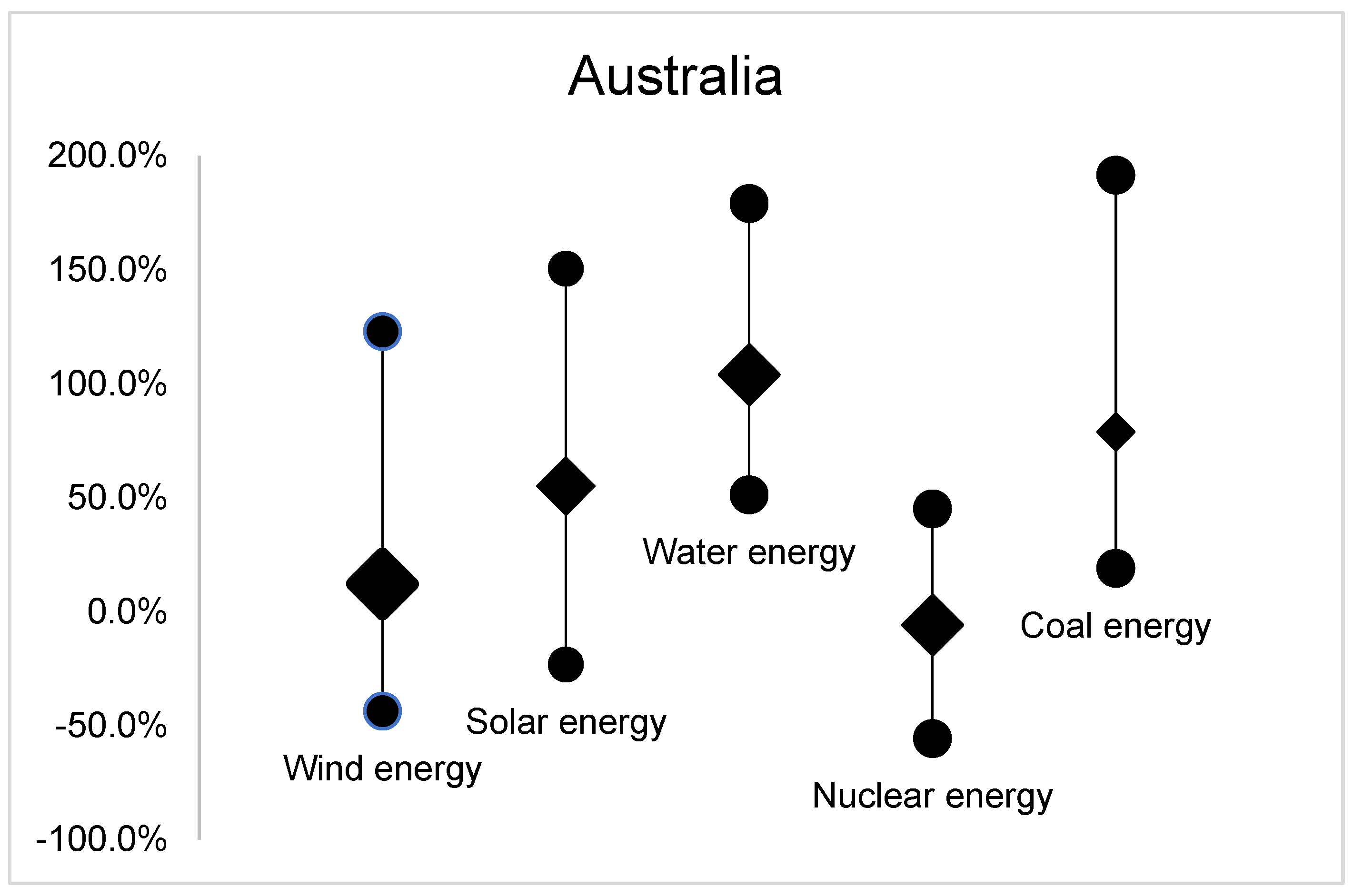

| Wind Energy | Solar Energy | Water Energy | Nuclear Energy | Coal Energy | Sum | |

|---|---|---|---|---|---|---|

| GB | 23 | 55 | 5 | 16 | 1 | 100 |

| US | 8 | 71 | 4 | 11 | 7 | 101 |

| AU | 8 | 76 | 5 | 5 | 6 | 100 |

| PL | 9 | 62 | 1 | 14 | 11 | 97 |

| CA | 10 | 39 | 28 | 16 | 4 | 97 |

| Sum | 58 | 303 | 43 | 62 | 29 | 495 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sus, A.; Trzaska, R.; Wilczyński, M.; Hołub-Iwan, J. Strategies of Energy Suppliers and Consumer Awareness in Green Energy Optics. Energies 2023, 16, 1613. https://doi.org/10.3390/en16041613

Sus A, Trzaska R, Wilczyński M, Hołub-Iwan J. Strategies of Energy Suppliers and Consumer Awareness in Green Energy Optics. Energies. 2023; 16(4):1613. https://doi.org/10.3390/en16041613

Chicago/Turabian StyleSus, Aleksandra, Rafał Trzaska, Maciej Wilczyński, and Joanna Hołub-Iwan. 2023. "Strategies of Energy Suppliers and Consumer Awareness in Green Energy Optics" Energies 16, no. 4: 1613. https://doi.org/10.3390/en16041613