1. Introduction

Over the last decades, the electricity sector has experienced critical changes in composition and operation, changing from natural monopolies to liberalized structures [

1]. The integrated markets of Portugal and Spain form the Iberian electricity market, known as MIBEL, which has been operating since 2007. Within the different markets composing MIBEL, the day-ahead market is by far the most important, where almost all electrical energy is traded.

With the recent increase in renewable energy sources (RES) and their expected integration into electricity markets, some questions have arisen. One of the most important is related to future electricity prices, which are expected to decrease with the increase in RES, greatly exacerbating the so-called “missing money” problem [

2,

3,

4]. This problem occurs when the suppliers’ revenues are not sufficient to cover all their costs, forcing market participants and future investors to change their trading strategies. Management, decision-making, and strategic planning are crucial activities in every modern business, and even more important in uncertain environments, such as the electricity market [

5,

6]. Therefore, it is vital to have the right forecasting tools to perform these tasks properly.

Considering the change that is expected to occur in the Iberian energy mix from today until 2030, with a projected sharp increase in the share of renewable generation, from 40% to 80–90% of the total electricity generation [

7], it is important to predict how day-ahead market prices will be affected.

In this paper, a methodology is proposed concerning the development of forecasting models to assess the influence of the increasing penetration of renewable power on MIBEL spot prices for the year 2030. The results of this analysis can provide important information about future electricity market prices for both present and future investors, allowing them to make rational and thoughtful investment decisions.

A common approach when developing forecasting models, especially for short periods of time, is to use previous values of the variable under prediction, in this case, the electricity price, as input, to improve accuracy. However, this is not a feasible solution when assessing electricity prices for 2030. Therefore, a different approach was adopted, with models using only explanatory variables of the underlying process, for instance, the production of generation technologies, demand, and variable costs of fossil fuel technologies.

In the literature, different models have been proposed to perform electricity price forecasts. Weron [

8] conducted an extensive and complete state-of-the-art review on the topic, evaluating the strengths and weaknesses of a variety of models and methods.

Statistical and artificial Intelligence (AI) techniques are by far the most frequently used techniques for electricity price forecasting [

9,

10]. With the liberalization of electricity markets in several countries, future electricity prices have become difficult to assess, and some traditional statistical methods have been considered incomplete and insufficient. The literature shows that AI algorithms, such as feedforward neural networks (FFNNs), are simple yet capable of mapping any non-linear function [

10,

11], making them a powerful and robust tool [

8,

12]. Artificial neural networks (ANNs) are frequently considered the most accurate forecasting tool when compared with traditional forecasting techniques, especially for nonstationary, nonlinear, discontinuous, and complex problems [

13]. Such algorithms can easily handle nonlinear, noisy, or incomplete data due to their learning characteristics, making them a natural tool for electrical markets, considering the characteristics of electricity prices [

14]. For these reasons, AI algorithms, more precisely ANNs, were used in this study.

With the increasing demand for AI models targeted at the forecasting of electricity prices, new and more sophisticated techniques have arisen. Most recently, new advancements were made regarding ANN forecasting techniques for electricity prices and stock prices, especially in the field of hybrid models. In [

15], the authors proposed a hybrid kernel-based model with advanced optimization, called a kernel-based extreme learning machine. The authors used a variational-mode decomposition process to decompose the original data into its various components and a chaotic sine cosine algorithm for optimization purposes. In [

16], the authors used a hybrid variational mode decomposition approach and a stacked gated recurrent unit model to predict stock prices, showing that individual stock price information/predictors are much more important than industry environment information. In [

17], the authors used an empirical wavelet transform attention-based LSTM algorithm. This algorithm decomposes the initial time series into several components through the empirical wavelet transform, and then that information is processed by the attention-based and LSTM components, from which the final predictions are obtained. In [

18], a whole new approach was provided. Instead of a hybrid model, the authors proposed a technique called transfer learning. A pre-trained model, from a given problem, can be optimized and used to predict electricity prices, thus increasing the model’s accuracy. However, these techniques are more suitable for shorter forecasting periods, in which the degree of uncertainty is lower than for longer time periods. More sophisticated models tend to demand more sophisticated and refined data, which is not the case for long time periods.

Electricity price forecasts can be divided into short-, medium-, and long-term, with extremely different methodologies used to address each of these time ranges. Considering the problem under consideration, and the definition provided in [

8], in this study we focused on long-term electricity price forecasts.

The literature is not extensive for this particular time range, containing a relatively small number of papers and studies. One explanation for this is the uncertainty about price-driven factors in the long run, such as fuel prices, regulatory policies, political intervention, technological changes, the energy mix, grid developments, etc. Electricity price behavior in the long term is highly dependent on investments made in the power system, and on political interventions [

19]. Even so, different authors have presented different methodologies and considerations when modeling and forecasting long-term electricity prices. For such a time range, more important than the model itself is the selection of the correct variables, which allow the process to be described over the long term. Several studies have proposed sets of variables and considerations that are believed to accurately describe electricity prices in the long term.

Some authors have focused more on the physical properties of the electrical market, considering variables such as the generation of energy using conventional and non-conventional technologies, imports and exports, demand, etc., and including few considerations related to the economic and social components of the market [

20,

21,

22].

Other authors have also considered, in addition to this information, the price elasticity of electricity, gross domestic product, information about households, consumption expenditure, population data, grid connections/restrictions, new capacity installed in the future, old capacity dismissed in the future, fuel costs, CO

2 allowances, the efficiency of technologies, inflation, etc. [

23,

24,

25].

As previously stated, the literature on electricity price forecasting in the long run is scarce, providing insufficient options to correctly assess future scenarios in which the energy mix is expected to be substantially different. To address this research gap, in this study we proposed a methodology using complex forecasting models, specifically, ANNs, with the ability to extract complex relationships from the data provided, incorporating explanatory variables that can accurately describe real market behavior and, more importantly, explanatory variables that can be extrapolated into the future and forecasted. Following this methodology, it is possible to assess future electricity prices with larger time horizons.

For that purpose, two deep learning-based ANNs, namely, feedforward neural networks (FFNNs) and long short-term memory (LSTM), were used to assess and forecast the day-ahead market prices resulting from future renewable power penetration scenarios. The use of two different forecast models allowed us to compare the experimental results and draw conclusions about their accuracy. If both models presented similar results for the simulated 2030 electricity prices, then we would be able to have an extra degree of confidence in regard to the experimental results.

The chosen explanatory variables were the production of electricity generation technologies, demand, and variable costs, representing the physical and economic components of the market. Therefore, the final explanatory variables considered the daily electricity generation from solar, hydro, wind, other renewables, coal, natural gas, and nuclear technologies, as well as the associated fuel and CO2 daily costs (i.e., the variable costs) and the daily demand level.

The remainder of the paper is organized as follows. In

Section 2, the data sources and the applied methodology are described.

Section 3 presents and discusses the experimental results in detail.

Section 4 describes an ongoing study to investigate the unique challenges associated with energy markets with large-scale penetrations of renewables, placing the work described in this paper into the context of a larger goal. Finally,

Section 5 presents some relevant concluding remarks.

2. Data and Methods

Data on electricity generation, energy sources, and demand were obtained from Rede Elétrica Nacional (REN) and Red Eléctrica de España (REE), the transmission system operators (TSO) for Portugal and Spain, respectively. MIBEL market prices were obtained from OMIE, the MIBEL market operator. Coal prices were obtained from the European Association for Coal and Lignite (Euracoal) and natural gas prices were obtained from Ycharts, an investment platform with information about different market stocks and prices. Information on CO

2 allowances was obtained from the European Energy Exchange market (EEX), a European platform related to all types of energy trade and the associated factors. Nuclear variable costs were collected from the Nuclear Energy Institute, directly in euros per MWh of electricity produced. All the abovementioned data were collected for the period 2015–2019, with a daily resolution.

Table 1 summarizes the collected information concerning the yearly average prices of CO

2, natural gas, and coal. We considered both the fuel costs and CO

2 costs as variable costs.

The methodology proposed to evaluate the influence of future renewable generation on MIBEL prices comprises five steps:

Data treatment and analysis, assessing the influence of the different components of the energy mix (demand and generation) on electricity prices.

The construction of the two AI models (FFNN and LSTM) that will be used to predict electricity prices.

Training and tuning of the models.

Validation of the model.

Modelling of the 2030 energy mix, which will be used as input to the models to obtain the simulated MIBEL electricity prices for 2030.

2.1. Data Treatment and Analysis

Having collected information about the daily demand and generation of electricity from different sources, it was then necessary to compute the associated daily CO2 and fuel costs, which in this work were only related to natural gas and coal technologies.

To calculate the fuel costs, it was necessary to compute the daily primary energy used by natural gas and coal technologies to generate electricity. Such information can be obtained using the corresponding efficiencies. In the case of natural gas, different technologies are being considered, from combined-cycle and cogeneration systems to normal gas turbines. Accordingly, we considered it to have an average efficiency of 55%. For coal technologies, we considered the regular efficiency presented by this technology to be around 35%. With these values and the unitary fuel costs shown in

Table 1, it was possible to compute the daily fuel costs. The daily CO

2 costs were computed using information about the daily emissions and the unitary price of CO

2.

A correlation analysis was performed to assess the relationship between the selected variables and the electricity prices. When discussing forecasting models it is not only important to select the correct variables, but also to assess their influence on the final output. In this way, it is possible to evaluate the coherence of future results.

According to King et. al. [

26], two methods are typically used to calculate correlations between variables. If variables are normally distributed, Pearson’s correlation should be used. If not, then Spearman’s correlation should be chosen. For the specific case considered in this study, the data were not normally distributed, so Spearman’s correlation (

) was used. From

samples, this correlation ranks

and

variables independently, either in an ascending or descending order, and posteriorly calculates their differences (

). Using that information, the Spearman’s correlation between them is computed as follows:

2.2. Construction of AI Models

Attending to the evidence found in the literature, AI models such as ANNs show an enormous potential to deal with noisy, volatile, and non-linear environments, such as the prices of the electricity market. Two ANN algorithms were used here to evaluate 2030 MIBEL electricity prices. The first was a feedforward neural network (FFNN), one of the simplest algorithms. The second is called long short-term memory (LSTM), a more complex and sophisticated algorithm that integrates the group of recurrent neural networks (RNNs).

FFNNs are the basis of deep learning [

27,

28,

29]. This specific architecture is efficient and simple to use, and is widely applied in supervised learning. The “feedforward” designation comes from the information flux, which is processed in one direction only, from the input through the hidden layers until reaching the output, called the forward direction.

LSTM is a specific case of RNN and is considered a generalization of FFNN, with the upgrade of an internal memory. LSTM provides neurons with information feedback from the

previous time steps. This means that after computing the output of a given neuron, that same information flows back into the network, and therefore the algorithm can analyze, process, and use it to compute the next output. According to Hochreiter et. al. [

30], the general idea behind LSTM algorithms is to introduce the cell state, where information can be added or removed and passed to other cells. Unlike FFNN, information is propagated using unit gates (forget, input, and output gates), which are responsible for updating the cell state and computing neurons’ outputs. LSTM neurons are much more complex than the basic artificial neurons used in FFNN. According to [

31,

32], RNN structures may present some advantages when predicting stock prices, due to their repetitive nature, and having information on previous steps can be advantageous. When data exhibit auto-correlation or time dependence, RNNs are good candidates to extract their underlying patterns. However, that same ability to memorize previous steps may lead to some convergence and stability problems. As such, when predicting stock prices, RNNs seem to be a good candidate, but they may not always be the best ones.

In this study, both neural networks contained one input layer, two hidden layers, and one output layer. The number of input neurons was determined by the number of variables used to describe the process, namely, nine.

Figure 1 shows a schematic representation of a neural network, as well as its inputs and outputs. The difference between the two algorithms consisted mainly of the information flow, meaning that in the LSTM there is the previously mentioned feedback (not represented in

Figure 1).

2.3. Training the Models

In the training procedure, it is necessary to feed the models with specific data, called training data, containing predictors (or inputs) and the corresponding solutions (or targets), ensuring that they can learn, adapt, and minimize errors. Most neural networks, including the ones considered in this study, are trained by considering gradient descent techniques using the backpropagation algorithm, as described in [

33,

34].

In this paper, the training of the models was performed using previous information concerning the generation, demand, and variable costs considered in MIBEL for the period 2015–2019 (i.e., the variables presented in

Figure 1). The forecasting strategy was implemented as a one-step ahead approach, i.e., the model predicted each daily electricity price at one time, based on the corresponding daily explanatory variables. In this way, the models could adapt to previous information and (hopefully) generalize for new cases and problems. During the training procedure, and through the implementation of an exhaustive stochastic grid search, the different hyperparameters used could be optimized. The batch size, the number of epochs, the type of optimizer, the considered cost function, the type of weight initializer, and the activation function present in the neurons are summarized in

Table 2.

2.4. Validating the Models

After the construction and training of the models, it is crucial to evaluate their accuracy in generalizing for new cases (this assessment is called model validation). To perform this task, a dataset composed of predictors/inputs and targets/solutions is required, to predict and quantify the error. In this study, the plan for the validation process consisted of predicting previous MIBEL prices for each year between 2015 and 2019 and comparing the results with the known real values. When forecasting a specific year, a critical part of performing a good model validation consists in ensuring that the model cannot have access to data regarding that particular year in the training stage.

A common approach is to compare the accuracy of the models with a benchmark. In this paper, we adopted the persistence method. This method states that the value observed at time t − 1 will also occur at time t.

The error was quantified using two basic indicators: mean absolute percentage error (MAPE) and mean absolute error (MAE), as shown in (2) and (3), respectively:

where

represents the total number of samples,

is the forecasted value, and

is the real value.

Apart from these two indicators, a statistical analysis was also performed for a better understanding of the error, by calculating the associated statistical indicators, namely, the mean (), standard deviation (), and median (M).

2.5. Modeling the Energy Mix of 2030

To forecast the electricity prices for 2030, taking into account the previously described models, it was necessary to consider information about the expected 2030 energy mix in MIBEL. In [

6], the future Iberian power system was simulated using the EnergyPlan tool, following the objectives established by the European Commission and the Iberian Governments until 2040. Information about future generation technologies, electrical production, and demand is also provided in [

6].

Table 3 shows the energy mix considered for 2030, following the results of [

7], and compares it with the real energy mix from 2019.

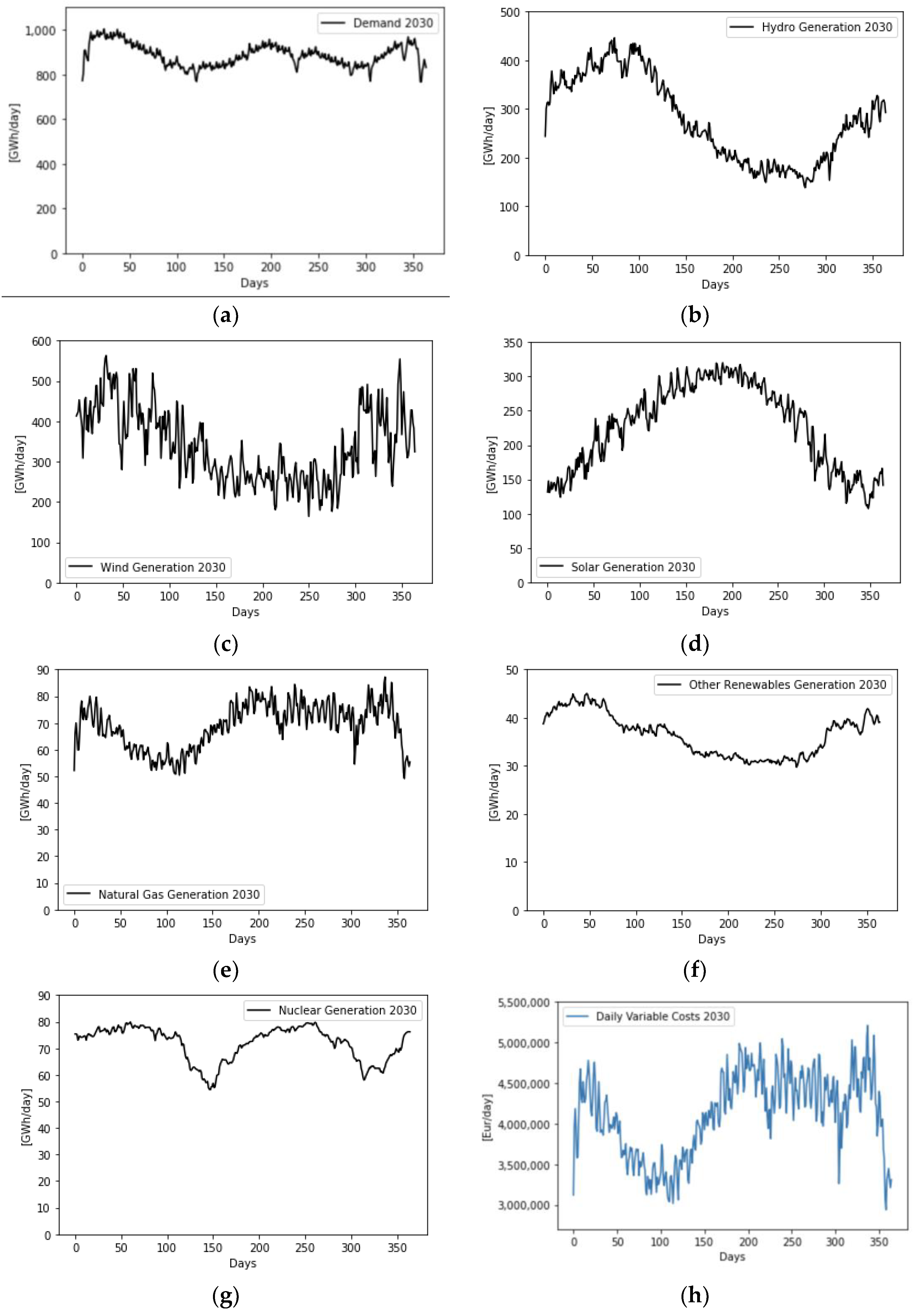

By 2030, it is clear that renewable generation will largely increase its share in MIBEL, and fossil fuel generation will be drastically reduced, with coal technologies reaching null production. For 2019, the amount of electricity originating from renewable sources, which include hydro, wind, solar, and other renewables, was around 39% of the total generation. For 2030, this percentage rises to 86%. The largest investment was observed for solar technologies, which are expected to increase their production by 707%, when compared with 2019.

The information provided in [

7] was presented on a yearly basis and this needed to be converted into the models’ predictors/inputs (i.e., on a daily basis). To overcome this issue, we decided to capture past patterns of generation and demand variables and replicate them for 2030 (assuming that the distribution of predictors in 2030 would be similar to that of today). This is a simple and natural approximation. To obtain the previous patterns, one could use a single year from the 2015–2019 period or consider an average of all years in the interval. The latter approach was preferable since any unusual event that may appear in one year could be disguised by using the average of the period. Thus, an “average year” was considered.

In the computation process for daily fuel costs, we followed the same methodology as explained for previous years (2015–2019). For the computation of daily CO2 costs, a different approach needed to be adopted, since it was not possible to access information about the daily emissions for 2030 (as was possible for previous years). To overcome this difficulty, a “natural gas emission factor” was created by dividing the total emissions from natural gas power plants by the total electricity generated for the period of 2015–2019. This allowed us to compute an average daily emission and the respective cost. This was also a simple and natural approximation which considered that the CO2 emissions of natural gas power plants would not change in the future.

Table 4 presents the CO

2 and natural gas prices, as forecasted by the Portuguese authorities in their development plans.

Figure 2 represents the used demand, generation, and variable cost distributions for the predictors in 2030.

4. Market Design and the Missing-Money Problem

Electricity markets (EMs) are built on well-established rules of transparency and competition. For the specific case of European markets, the ‘common’ design framework includes day-ahead and intra-day-markets, operating together with forward markets and complemented with balancing markets (see, e.g., [

40,

41,

42]). This framework was developed, however, when the majority of power plants were fuel-based, meaning that their production could be controllable, with a limited economic impact.

The clean energy transition creates unique challenges in the design and operation of electricity markets. Chief among these is the well-known missing-money problem—the concern that even robust EMs may not provide sufficient incentives for at least some generators to earn revenue to pay for both variable and fixed costs [

5]. In other words, the concern is that insufficient incentives for generators to build new capacity (or even maintain existing capacity) will result in insufficient installed capacity to serve the required loads, particularly during peak periods.

Most existing market designs already incorporate at least two mechanisms to meet this challenge: scarcity pricing and forward capacity markets. Scarcity pricing can be based on the value of lost load pricing, ancillary service scarcity pricing, or even emergency demand-response pricing. This allows energy prices to rise above the variable cost of the most expensive operating resources when the system is capacity-constrained. Although difficult to predict in terms of investment in capital, these prices may provide important revenue for resources to recover fixed capital costs (see, e.g., [

3]).

However, energy-only markets—that is, markets based on scarcity pricing or a similar mechanism—have been the subject of a somewhat intense debate. In particular, some industry members and researchers have made strong arguments that they cannot incentivize appropriate investments, stating the need for additional incentive mechanisms and highlighting the importance of forward capacity markets. These markets determine capacity prices depending on the current supply of capacity and predicted capacity needs. They look ahead to ensure that sufficient capacity will be available to meet load requirements, especially in peak periods, and aim to provide important incentives for new capacity to be built in locations where it is most needed (see, e.g., [

3]).

With the increasing penetration of renewable energy generation—which is likely to offer electricity at very low costs—both the average energy prices and the cleared energy levels of power plants are likely to be reduced. This, in turn, could reduce the overall revenue for generators, and therefore may (greatly) exacerbate the missing-money problem.

At present, it is unclear whether or not the ‘common’ design framework provides the right incentives to support the issues of resource adequacy and revenue sufficiency in future power systems with large-scale penetration by renewables. Accordingly, there is a pressing need to monitor the impacts of such large penetrations on existing markets to determine if the ‘common’ framework is still effective. If it leads to inefficiency, increased market power, reduced competition, or a degradation in reliability, important modifications may be required, or a new design framework may even be necessary.

In our ongoing studies, we are examining the use of an agent-based tool to help manage the unique challenges of EMs with large-scale penetration by renewables. The tool is called MATREM (for multi-agent trading in electricity markets) [

43]. In this research, we aim to investigate emerging and new market design elements to ensure that the resources needed to meet future reliability requirements have adequate opportunities to recover their costs. To this end, the feasibility of energy-only markets will be investigated, together with studies of evolving capacity mechanisms and the main new design elements.

The plan involves the use of an iterative procedure to search for operational practices in relation to market design—that is, various elements of market design will be investigated, implemented, and evaluated iteratively until a consensus emerges on specific best practices. Put differently, the MATREM system will be extended with specific market design elements and the empirical evaluation of such elements will be performed by considering a number of forward-looking scenarios (for the years 2030 and 2050). In this way, the work presented in this paper constitutes part of a larger project plan and represents an important step towards one of its major goals.

5. Conclusions

According to the information collected in this study, from 2019 until 2030, the share of renewable electricity in MIBEL is expected to increase, from 39% up to 86% of the total electrical generation, driven by the continuous increase in the installed renewable capacity. The main goal of this study was to evaluate the influence of increasing renewable power penetration on future MIBEL prices, with a special focus on 2030. The developed models based on artificial intelligence, namely, the feedforward neural network (FFNN) and long short-term memory (LSTM) algorithms, were constructed using explanatory variables of the underlying process. The chosen variables were the production of electricity generation technologies, demand, and fossil fuel variable costs, which represented the physical and economic components of the market.

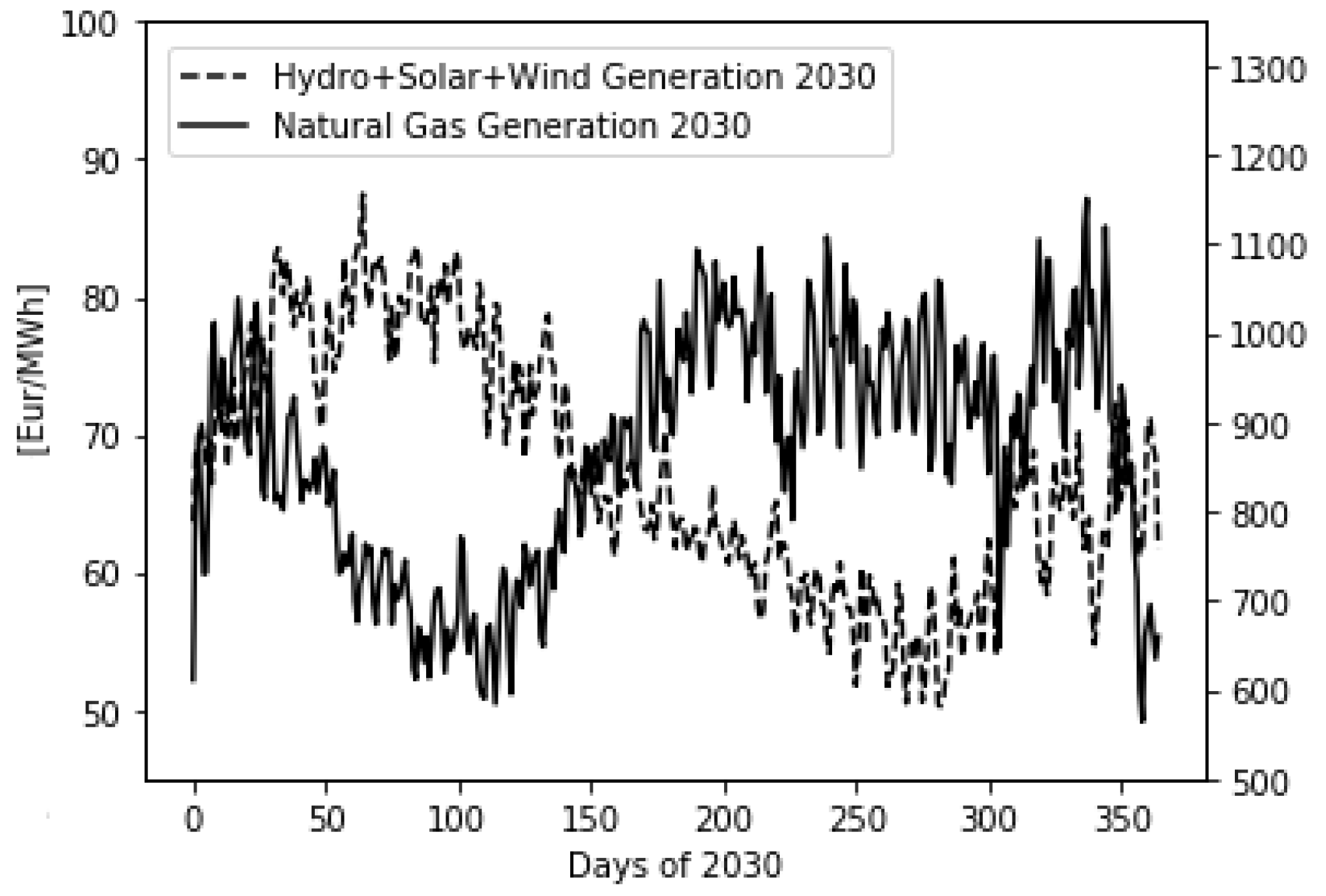

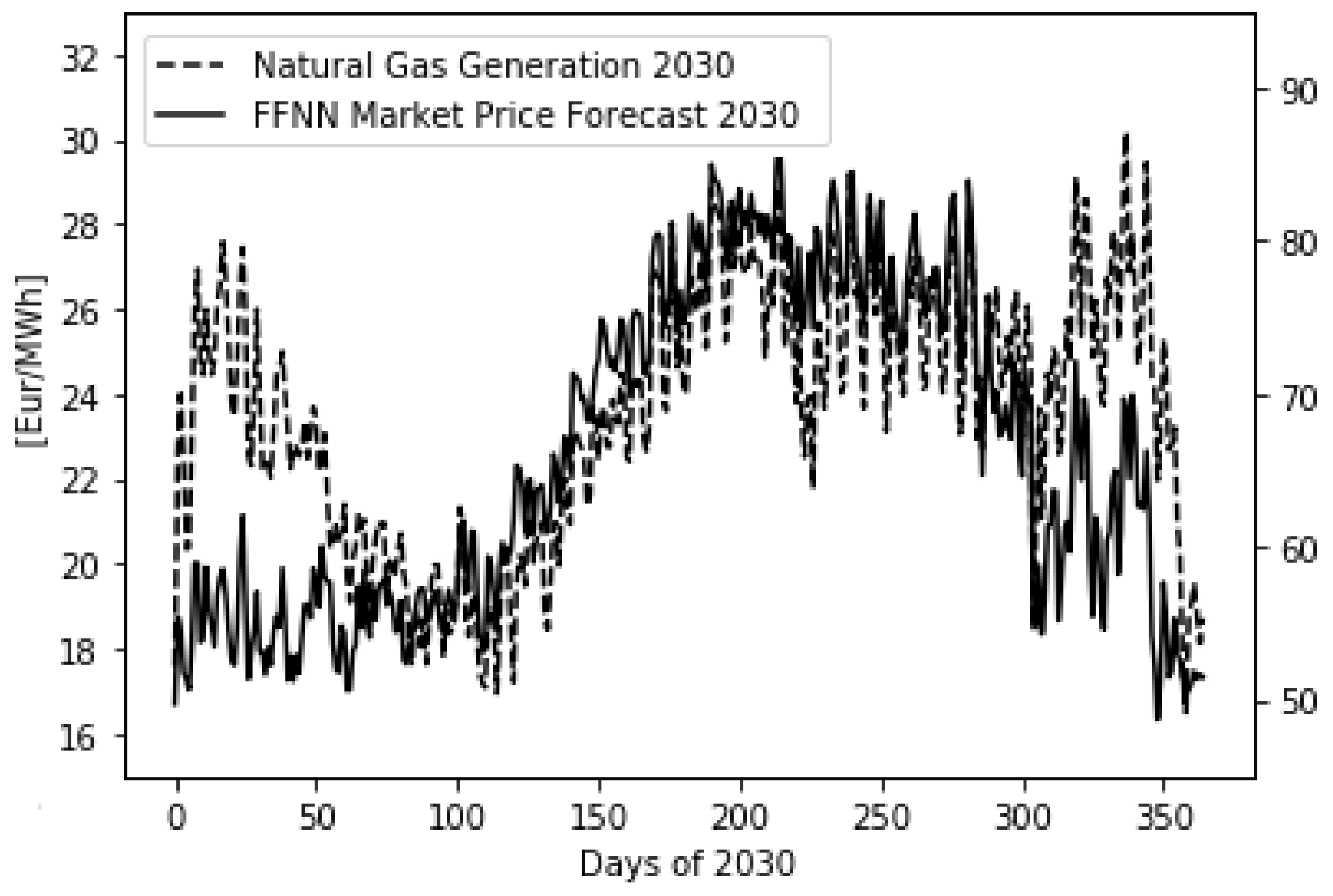

Both a daily and hourly correlation between generation, demand, and electricity prices was developed for the period 2015–2019 in order to assess their influence on electricity prices. The results showed that an increase in renewable generation tended to decrease the average daily market price and an increase in fossil fuel generation and demand levels tended to increase market prices. Moreover, hydro technologies exhibited a positive opportunity cost, represented by their positive hourly correlation with electricity prices. However, on a wider scale, an increase in hydro generation tended to decrease electricity prices, which was shown by a negative daily correlation.

To validate the models, the FFNN and LSTM algorithms were used to forecast the of MIBEL electricity prices of previous years (2015–2019), and their errors were compared with a benchmark. The results showed similarity between the two AI models and the benchmark, with MAPE and MAE values around 8–11.5% and 4.32–5.11 EUR/MWh, respectively. The similarity in the accuracy of both algorithms and the benchmark can be explained by the fact that no past electricity prices were used; rather, only explanatory variables related to the process were used. To justify this statement, another model was constructed, which, in addition to the previous inputs, also used information about the last n days of electricity prices, more precisely from the last 5 days. The results showed that these models, with the extra inputs, showed improved accuracy and outperformed the benchmark model, with MAPE and MAE values between 6.84–8.81% and 3.21–3.89 EUR/MWh, respectively. Accordingly, FFNN and LSTM provided reasonable values of accuracy and thus represented a viable solution for the problem under study.

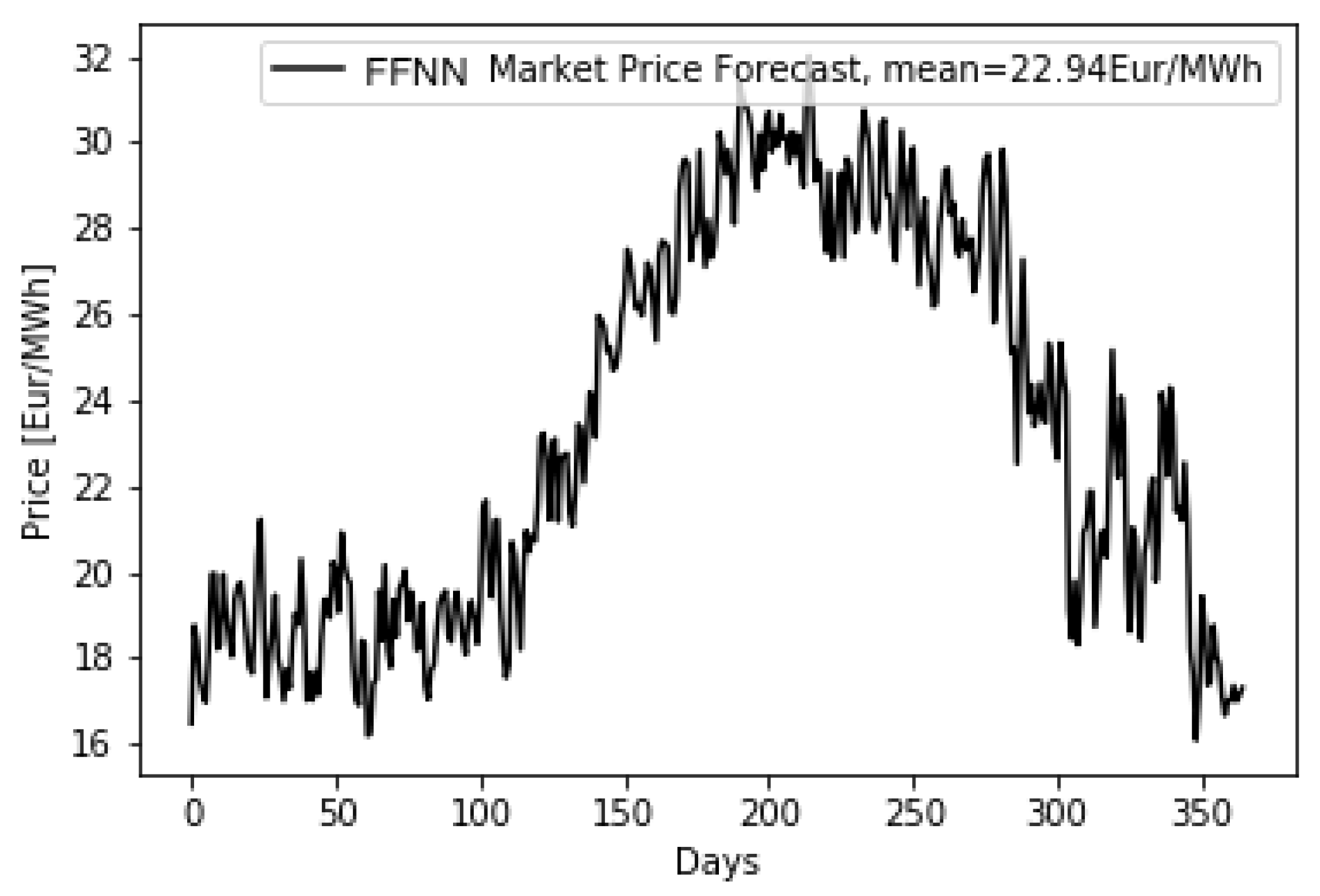

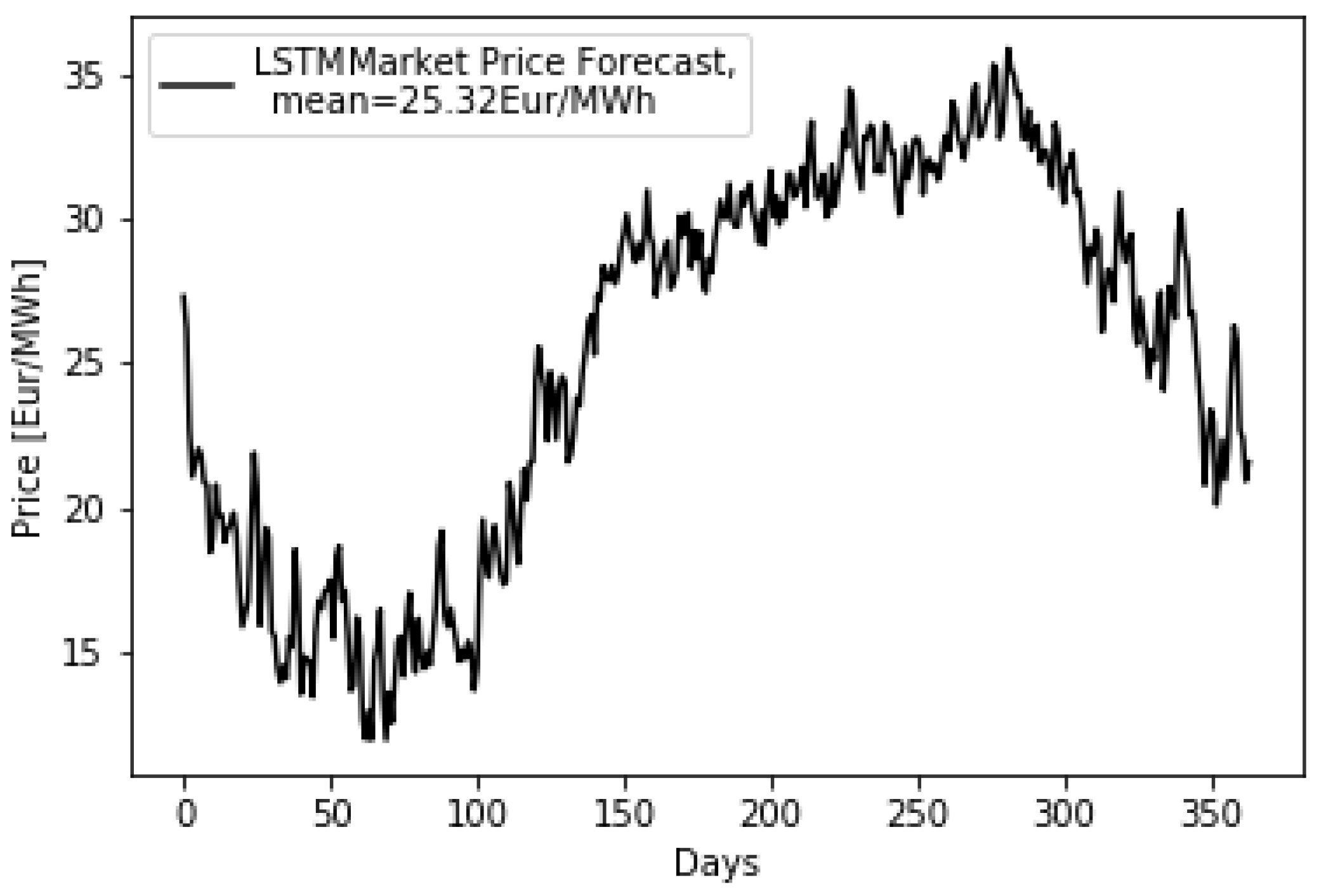

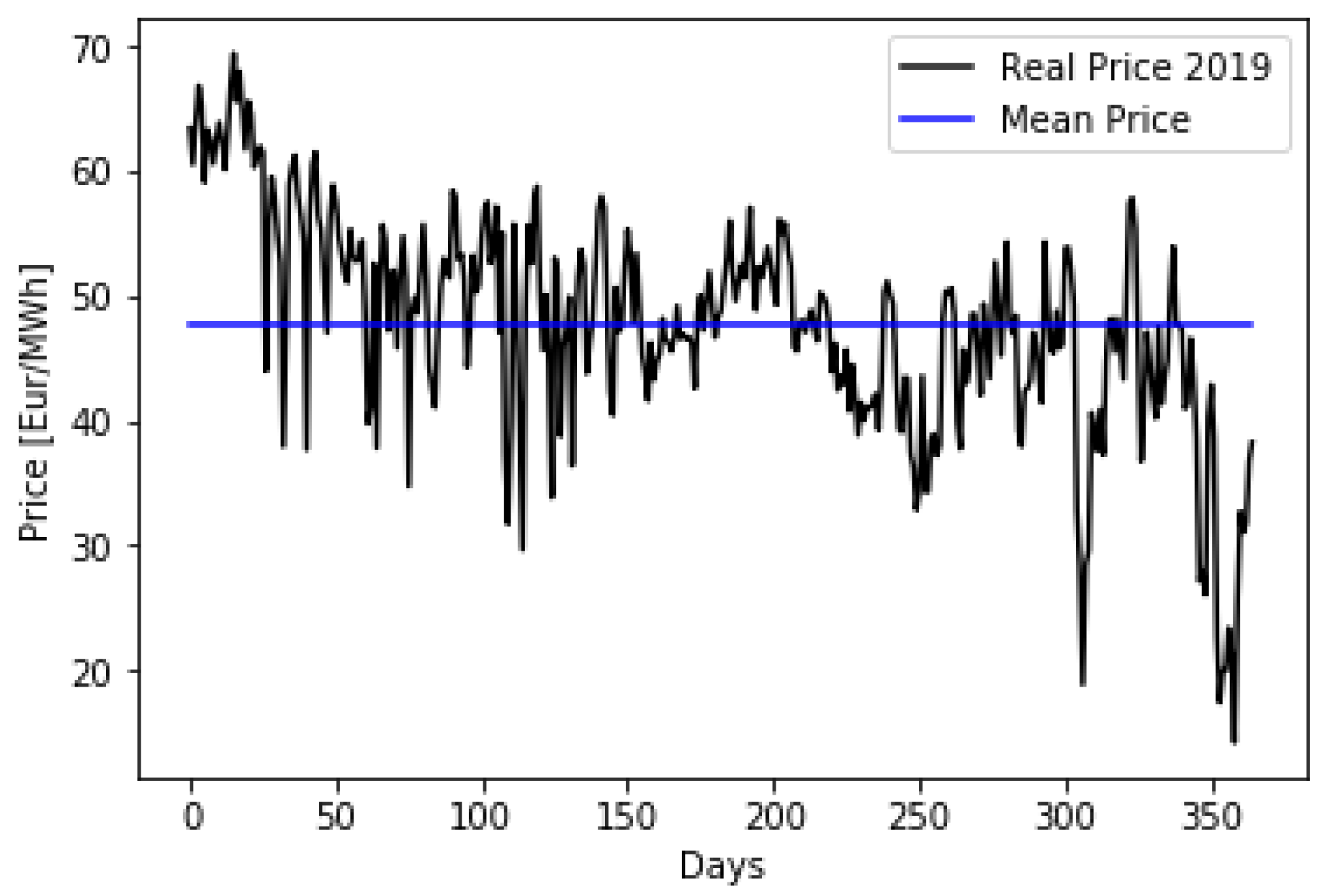

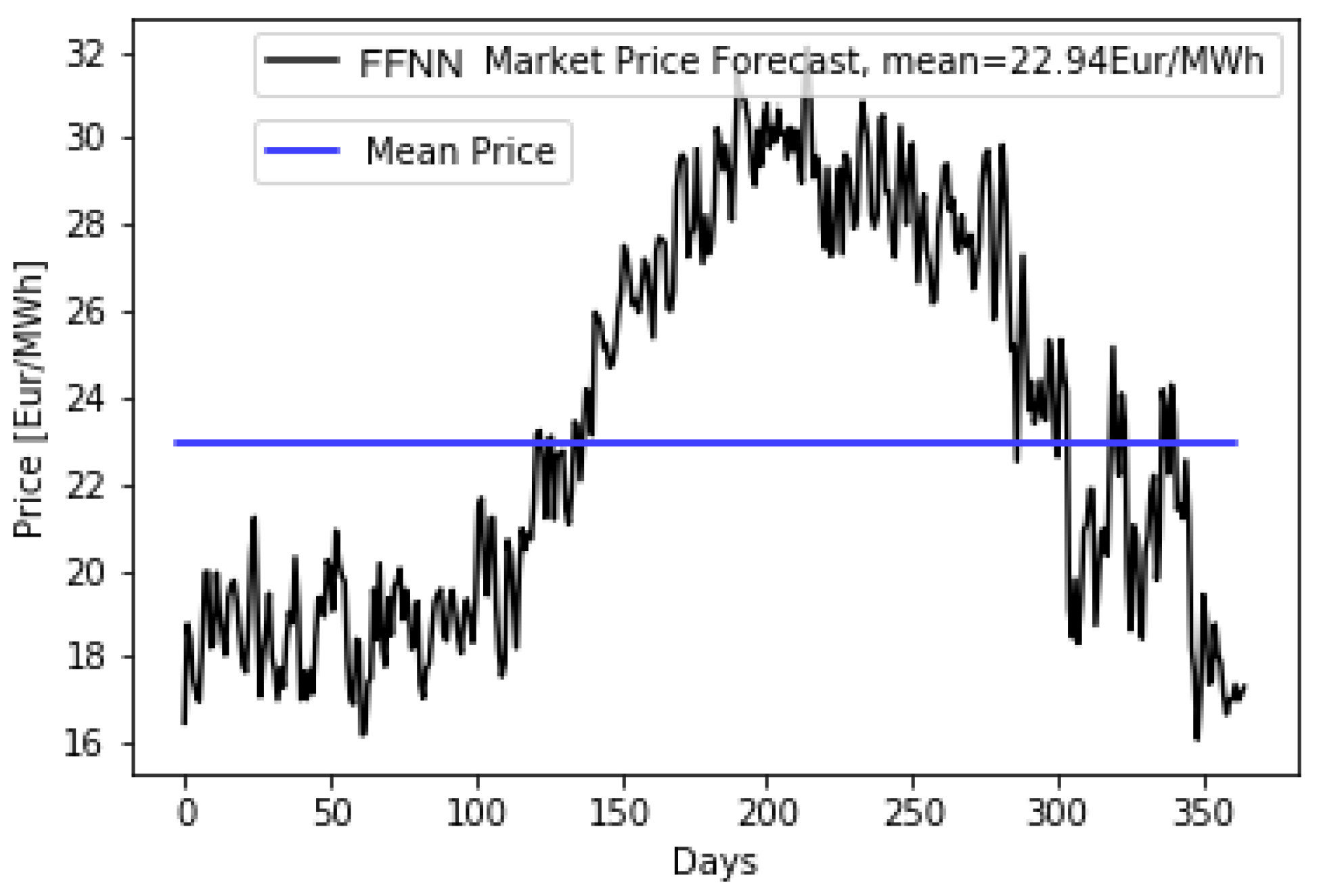

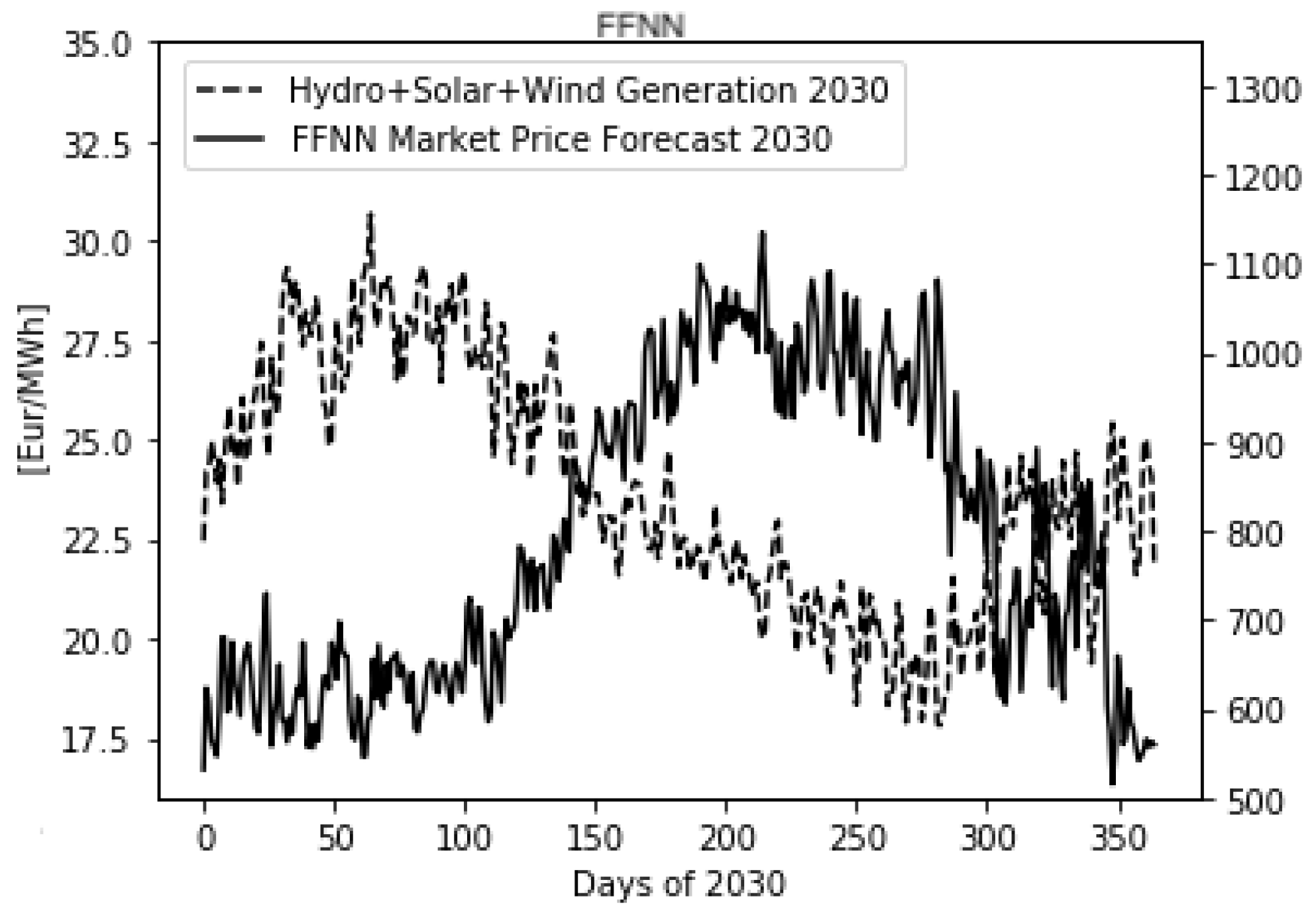

Regarding the prediction of the 2030 electricity prices in MIBEL, a large reduction in the annual average electricity price for 2030, with values of 22.94 EUR/MWh and 25.32 EUR/MWh for the FFNN and LSTM algorithms, respectively, was found. In comparison with 2019 (with an average electricity price of 47.68 EUR/MWh), the forecasted values corresponded to a relative reduction of about 50%. This is a substantial reduction, compatible with the expected high levels of renewable generation in 2030, with near-zero variable costs. Another finding was that the forecasted electricity prices presented a different pattern throughout the year, as compared with the 2019 calendar year, for instance. The effect of the drastic change in the energy mix composition predicted for 2030 was reflected in the distribution of electricity prices throughout the year, which closely followed the inverse pattern of renewable production.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}