Efficiency of Polish Energy Companies in the Context of EU Climate Policy

Abstract

:1. Introduction

- Embedding considerations at the company level, while most studies on the impact of EU climate policy look at entire economies or sectors;

- To conduct an analysis of the strategic behavior and financial performance of energy companies forced by the need to purchase carbon allowances—such studies are not a common subject of consideration in the energy economics stream;

- To make an indirect assessment of the effectiveness of the introduction and tightening of emissions trading on the activities of energy companies in reducing greenhouse gas emissions.

- Empirical conclusions on Polish energy companies’ adaptation strategies to EU climate policy;

- Observations on the financial impact of the introduction and increase in the price of emission allowances in the operations of Polish energy companies;

- Sectoral and economic recommendations aimed at developing low-carbon energy while maintaining national energy security in Poland.

2. Literature Studies

2.1. CO2 Allowances as a Climate Policy Instrument

- (1)

- (2)

- The original launch phase (2008–2012) and a slow reduction in the allocation of free emission allowances;

- (3)

- (4)

- The tightening regulations phase (2021-present) oriented towards reaching a zero-carbon economy in 2050.

- The Solidarity Mechanism, which allocates 10% of all auction allowances to countries having difficulty adapting to climate policy (16 countries use it, including Poland to the greatest extent);

- The Modernization Fund, which covers 2% of emissions of all allowances and is ear-marked for climate projects in the least prosperous EU countries (Poland is the largest beneficiary of this fund).

2.2. Impact of CO2 on the Functioning of the Economy and Its Participants

3. Materials and Methods

3.1. Characteristics of the Sector and the Companies Surveyed

3.2. Research Stages and Methods

- (a)

- Net margin on sales:

- (b)

- Operating margin on sales:

- (a)

- Coverage of fixed assets with fixed capital:

- (b)

- Financial debt-to-equity ratio:

- (c)

- Total debt-to-total-assets ratio:

- (d)

- Financial debt-to-total-assets ratio:

4. Results

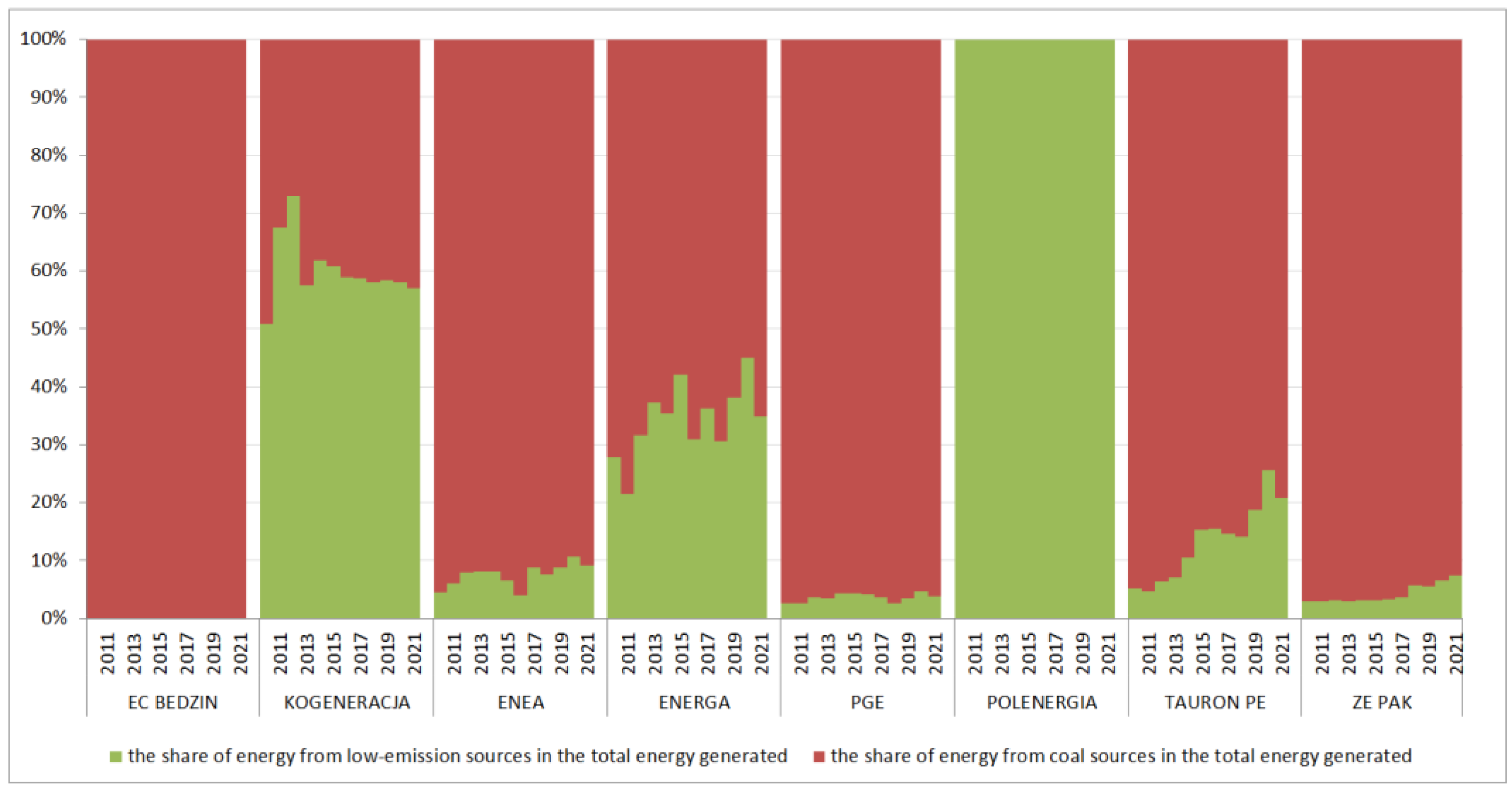

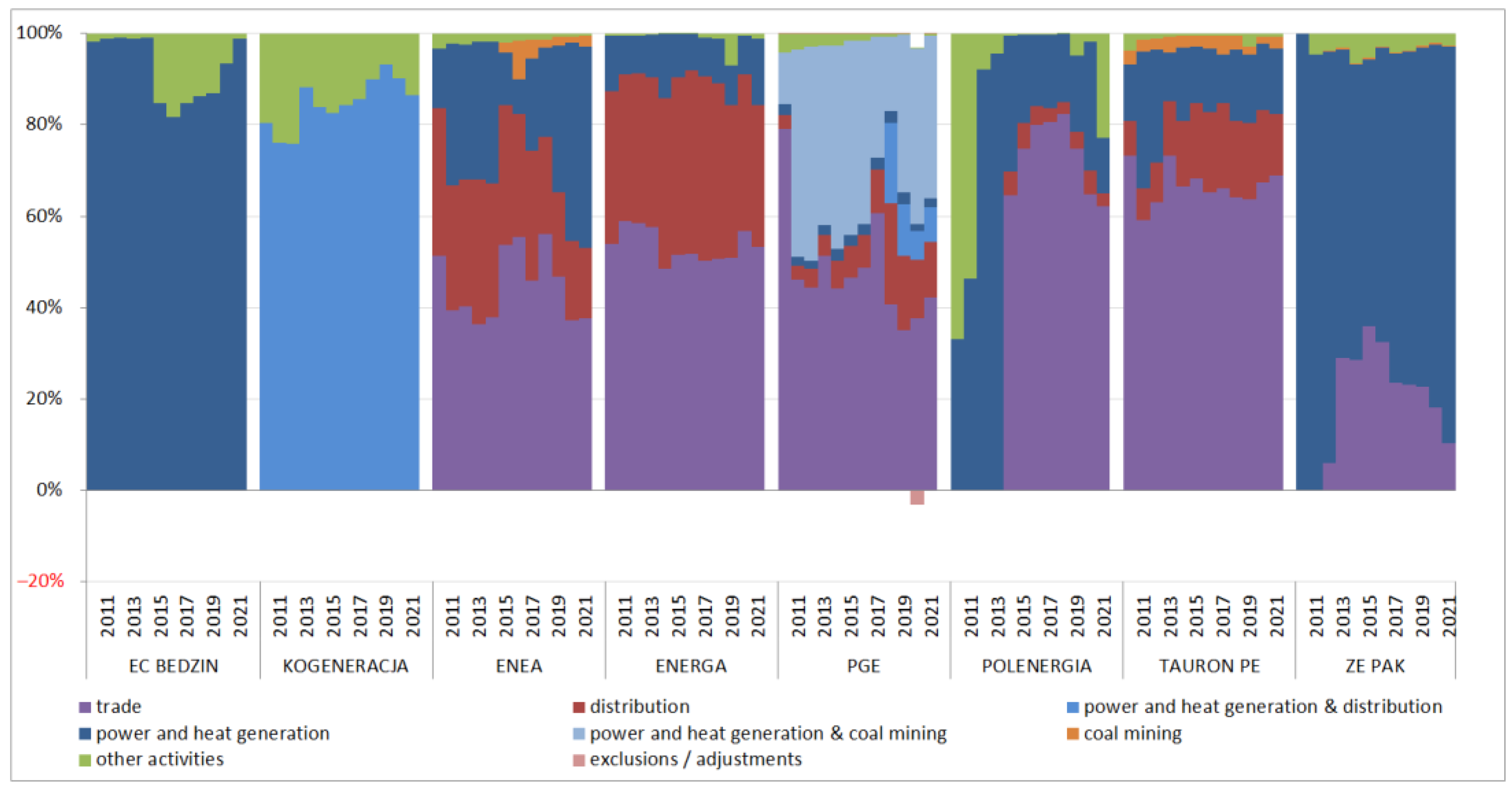

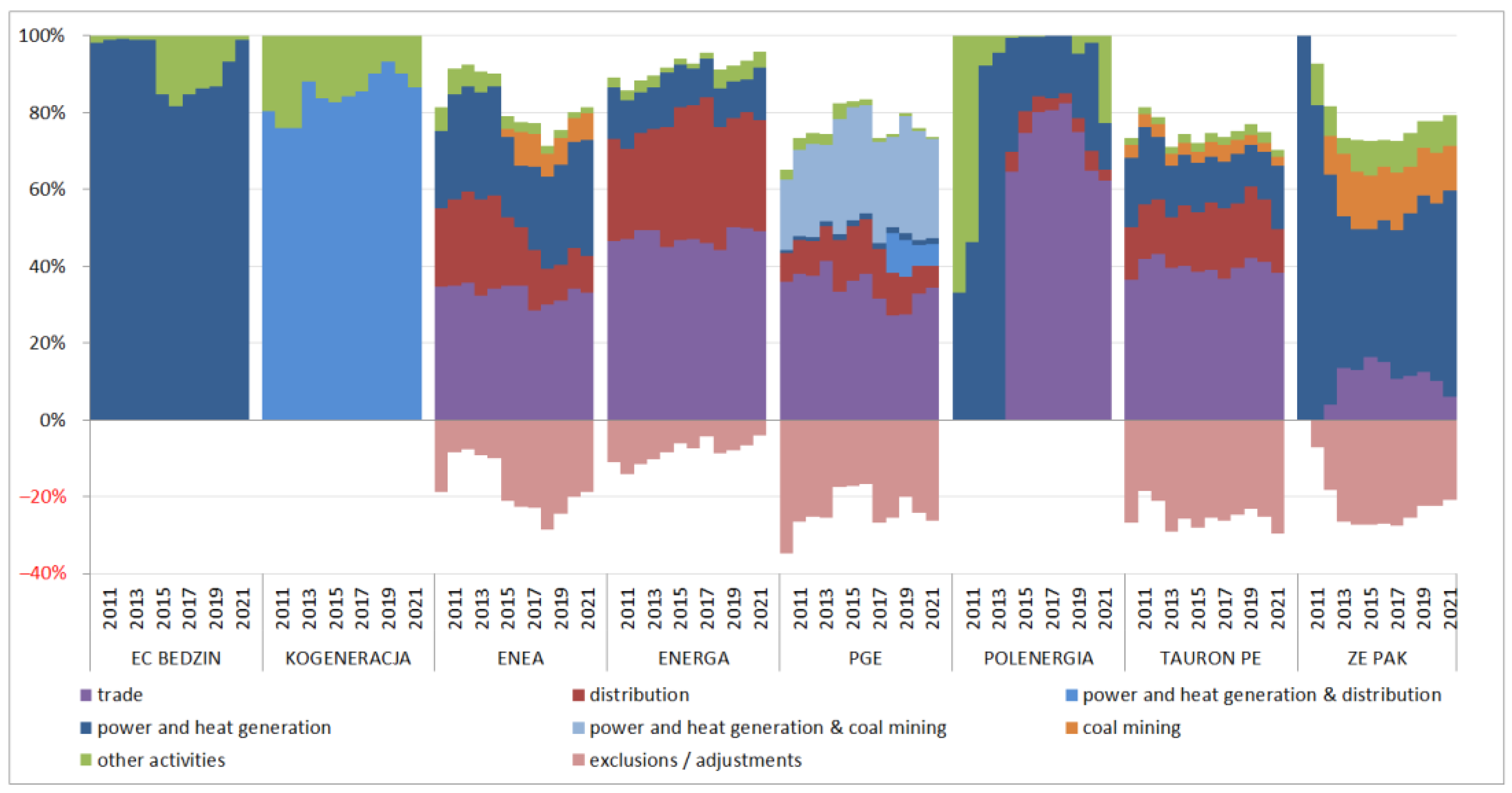

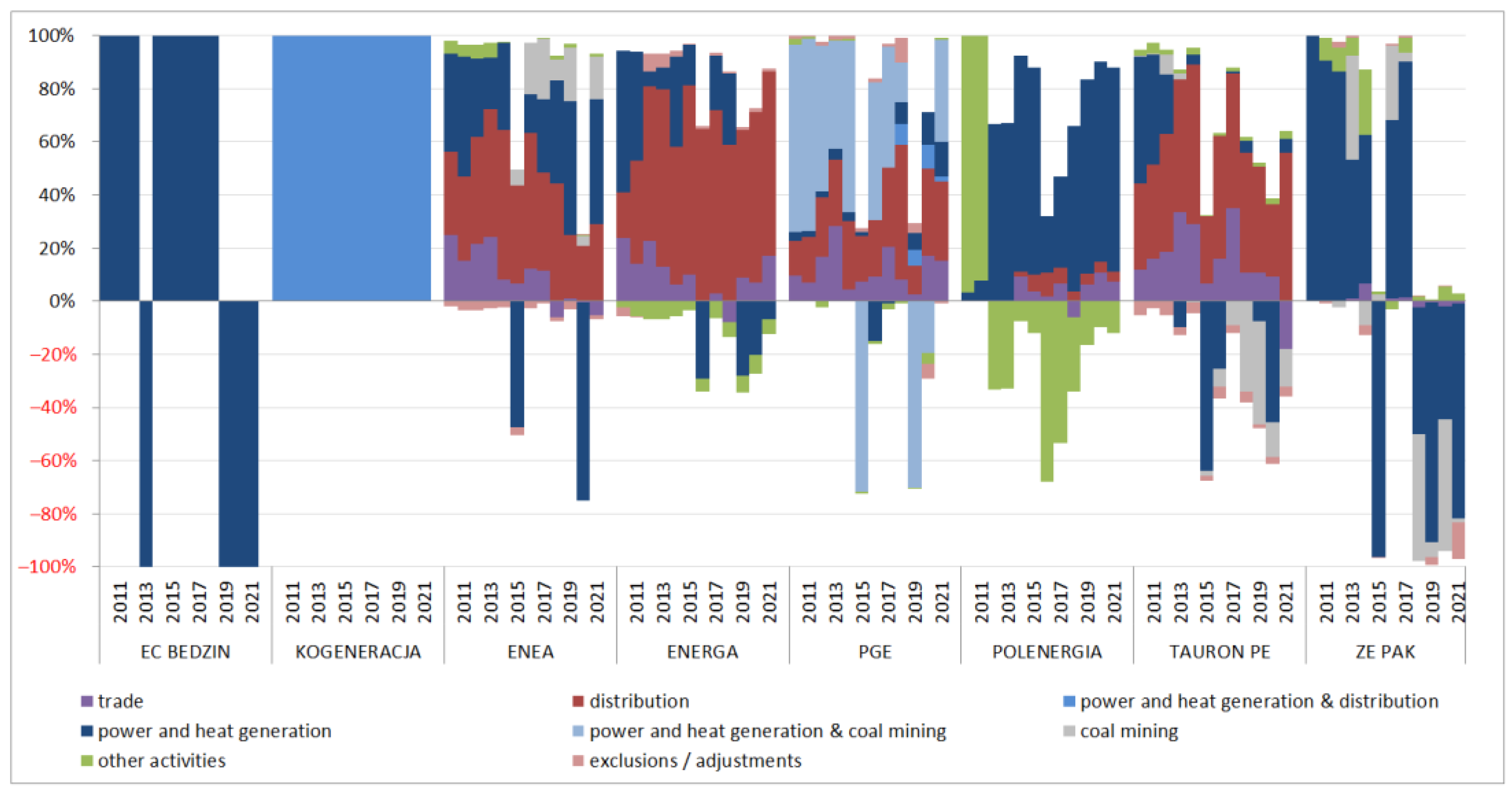

4.1. Characteristics of Power Generation Sources and Business Segments in the Surveyed Companies

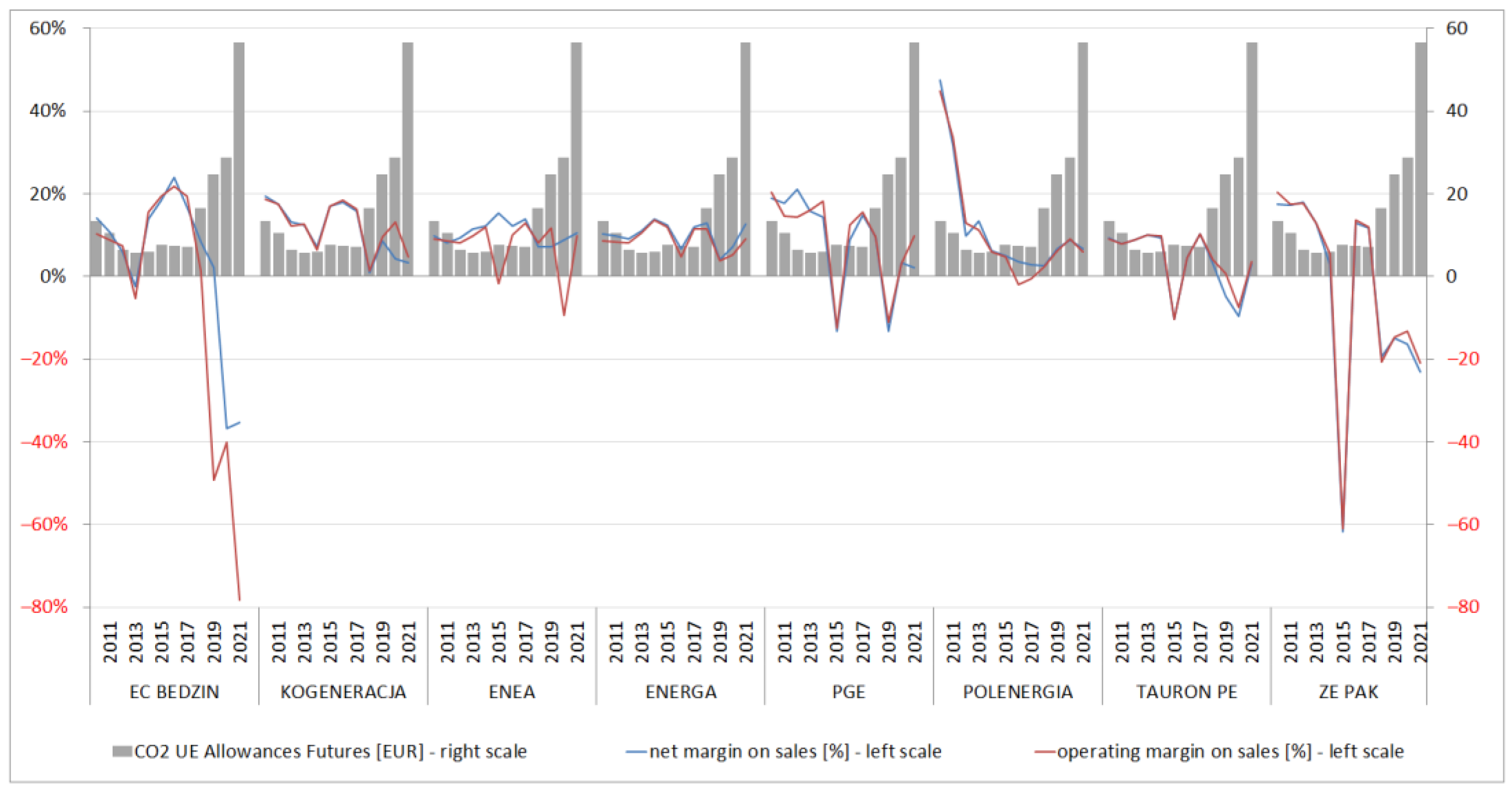

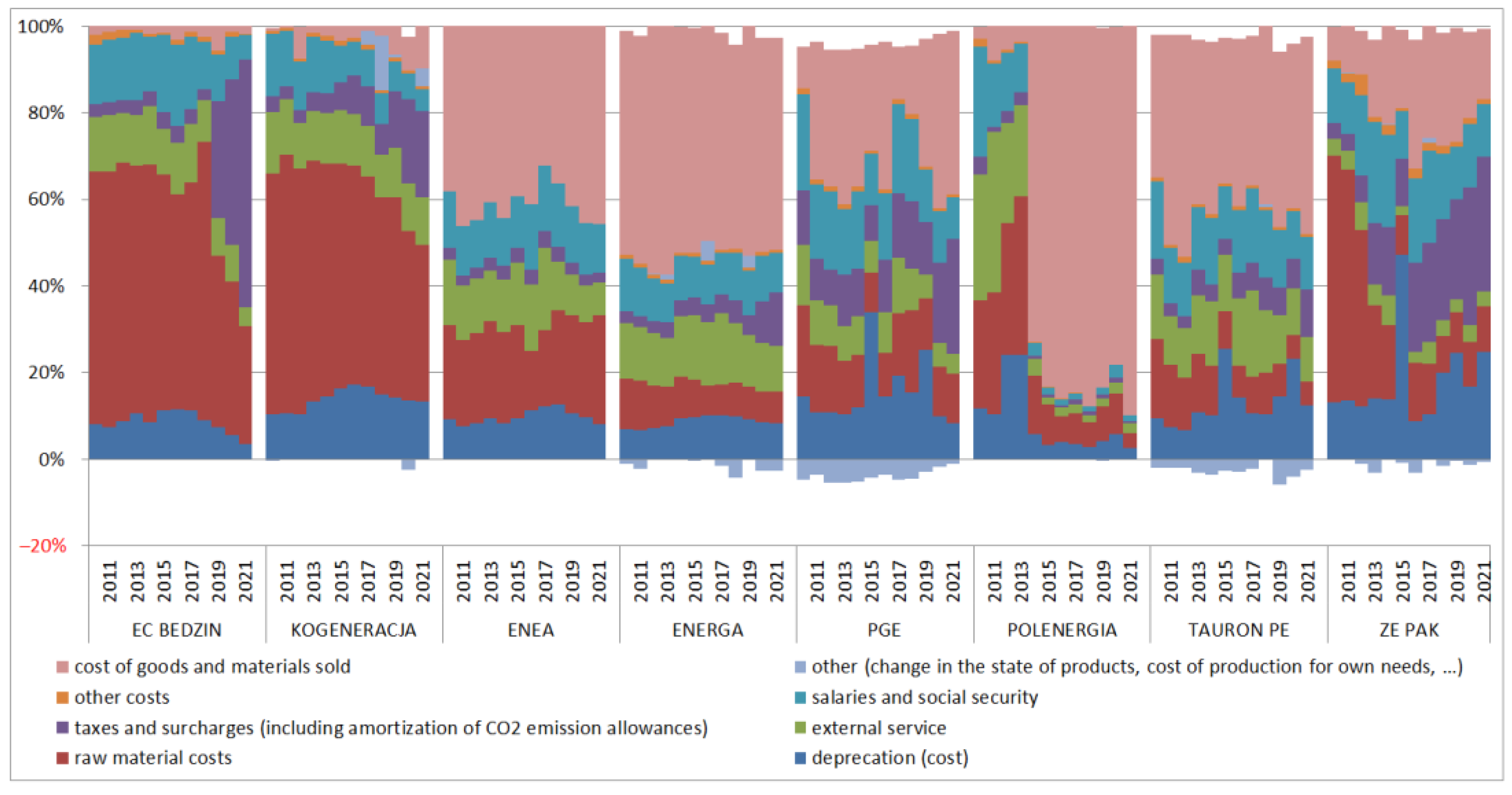

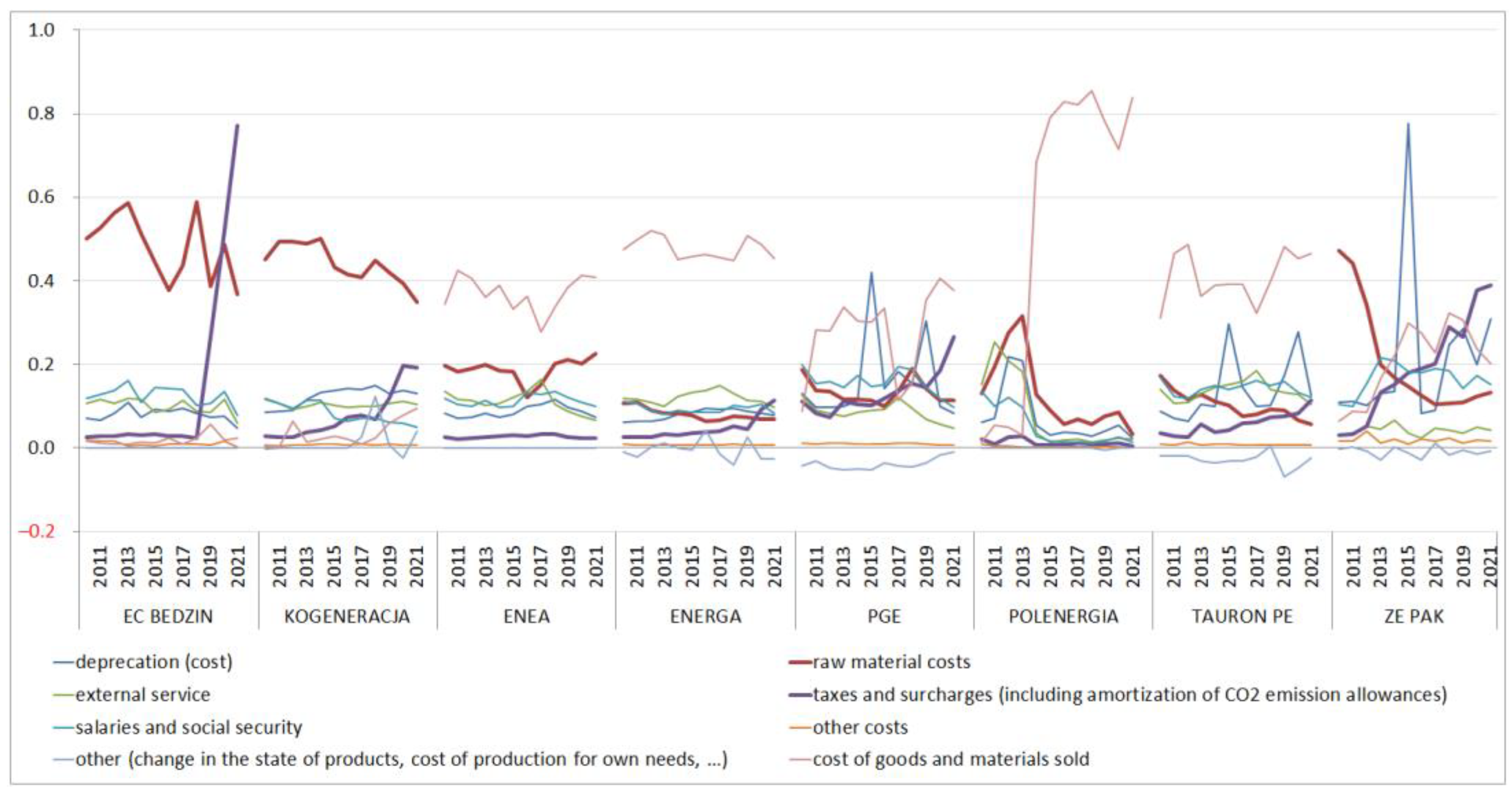

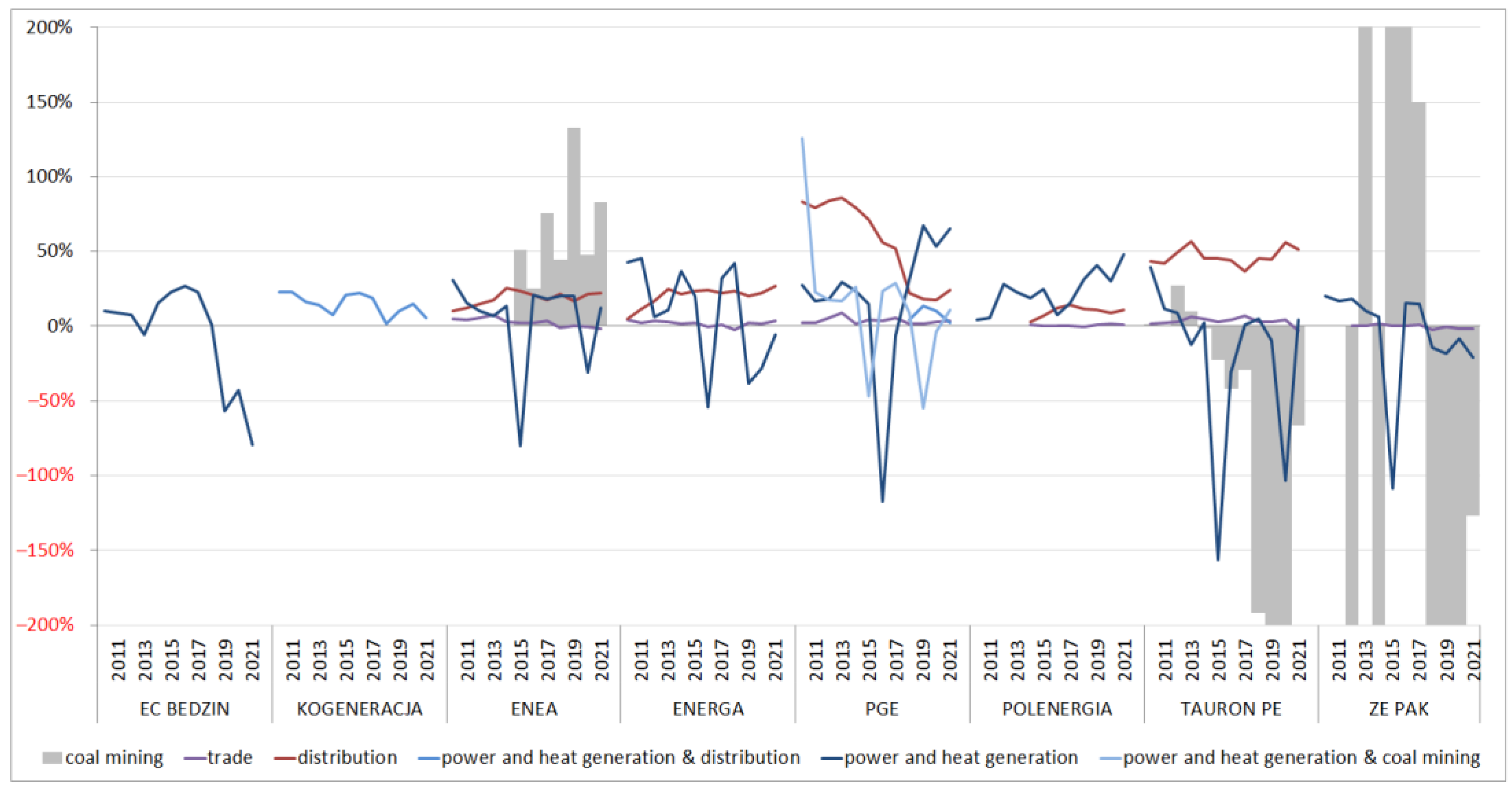

4.2. Analysis of the Financial Performance of the Surveyed Energy Companies—Current Perspective

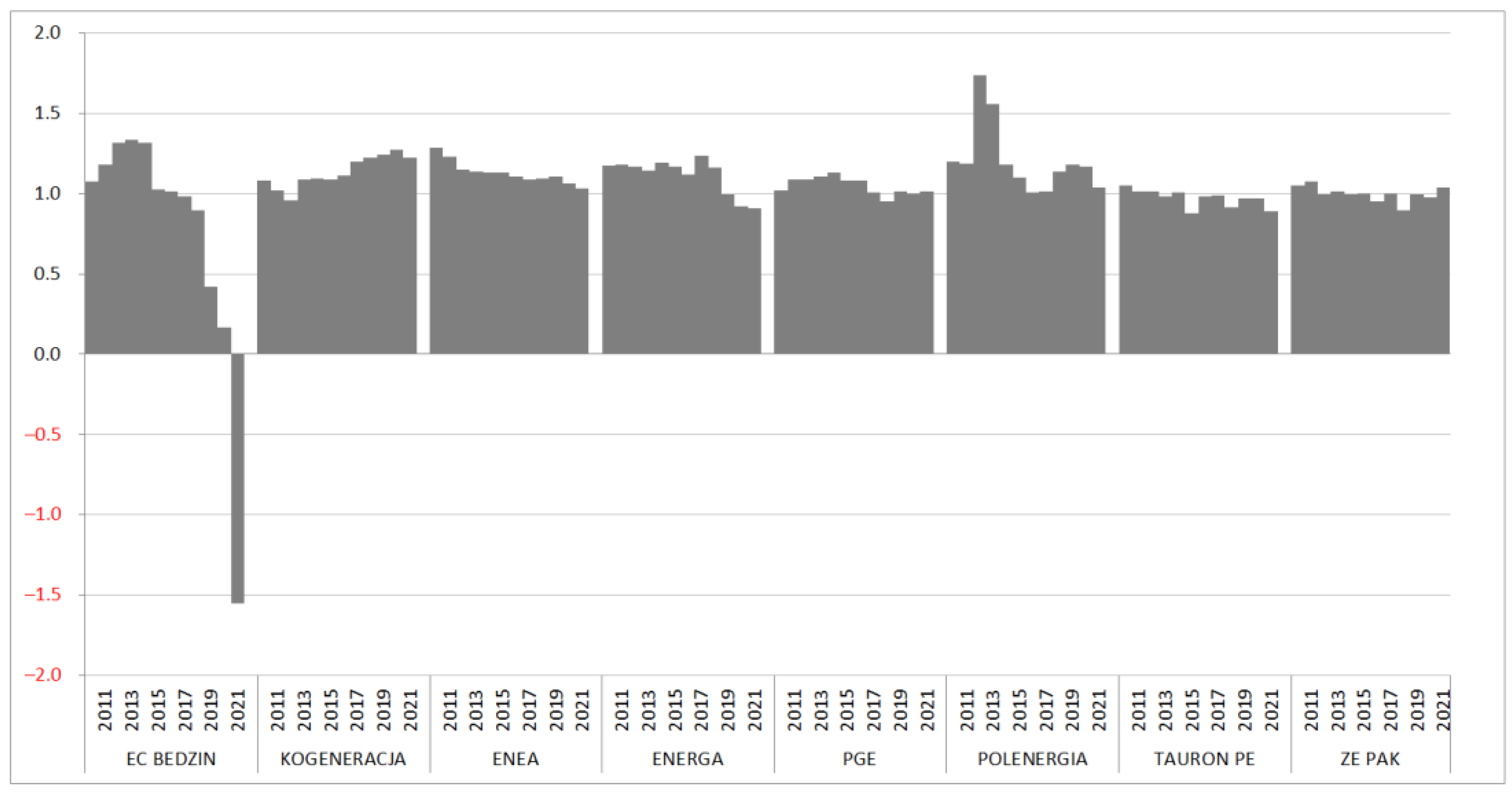

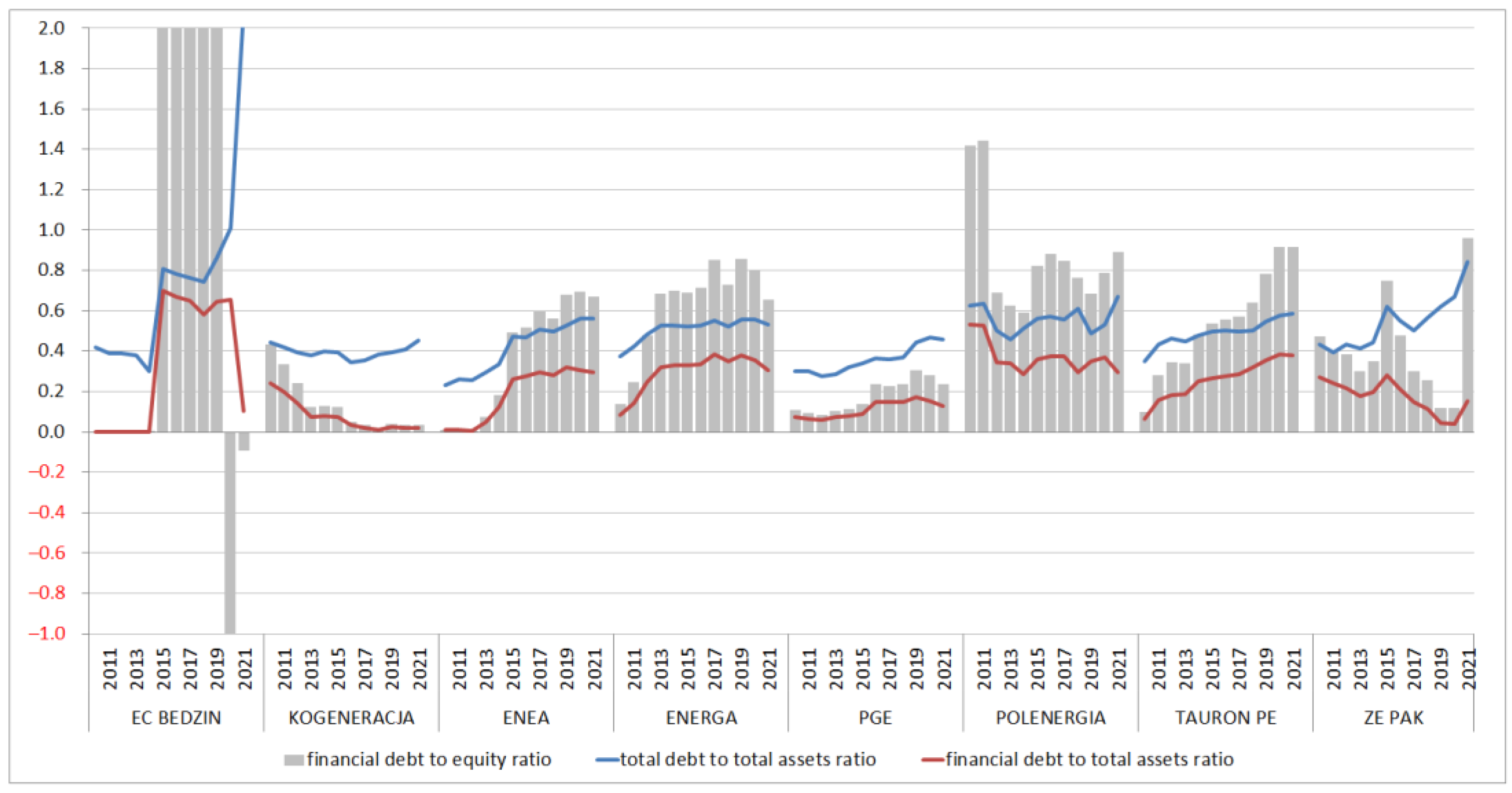

4.3. Analysis of the Capital Structure and Debt of the Surveyed Companies—A Long-Term Perspective

5. Discussion

- Systematically increasing the share of low-carbon sources in the generation segment regardless of its share in total revenues;

- Monitoring and forecasting the economic situation in terms of the ability to maintain current sales and operating margins in the distribution and trading segments;

- Implementing green innovations that can become the basis for strengthening competitiveness and survival in the future;

- Establishing cooperation with research entities to raise funds for innovative research in the area of the low-carbon economy, creating conditions for full adaptation to EU climate policy.

- Monitor the changes and effects of the European Union’s climate policy and its impact on companies;

- Step up efforts to make effective use of EU funds related to the emission allowance system;

- Identify the impact of the price of emission allowances on the behavior and financial situation of enterprises in order to negotiate with the EU the extent to which they are regulated and to prevent undesirable side effects with reference to the optimal price formation mechanism also described by Wei et al. (2022) [43].

6. Conclusions

- (1)

- The increase in the price of CO2 emission allowances was most pronounced at EC Będzin SA, a company focused on power and heat generation using coal, which was directly reflected in an increase in operating costs and a deterioration in financial performance, including sales and operating margins. The poor current performance situation translated into an increase in debt and the collapse of the capital and asset structure at this company.

- (2)

- ZE PAK SA was also affected by the effect of the increase in the price of carbon emission allowances, although to a lesser extent than in Będzin SA (increase in operating costs, deterioration of financial results, and increase in debt). The reasons for this are similar to Będzin SA’s power generation structure (coal-based) and poor diversification of business segments (dominance of generation).

- (3)

- In the other companies surveyed, the increase in the price of carbon allowances did not cause a significant financial impact. This is due to the diversification of operations and the offsetting of potential increases in power generation costs (related to the purchase of CO2 allowances) from segments related to energy distribution and trading (favorable sales and operating margins).

- The restrictiveness of the European Union’s climate policy, as expressed in the introduction, and tightening of the rules for the operation of carbon allowances, has the strongest impact on companies that do not diversify their operations in the energy sector and do not use low-carbon energy sources.

- In the long term, companies following the above strategy are at risk of bankruptcy due to rising costs, deteriorating financial performance, and a collapse of the capital structure.

- Thus, in the context of the above statements, it can be concluded that the instruments of financial repression for environmental abuses are effective because they force energy companies to change the energy mix they use and, in extreme cases, can even threaten their continued operation.

- Diversification of operations in the energy sector (combining generation, distribution, trading) and maximizing the use of low-carbon sources (gas + renewables) can be an effective way to increase the resilience of companies to the increase in market risk associated with rising CO2 prices.

- Nevertheless, the above method must not take the extreme form of reducing the business to trading and distribution, as it will then only mean a form of avoiding overexposure to market risk associated with the need to purchase emission rights.

- It is also worth adding that the focus of domestic energy companies only or mainly on energy trading and distribution may pose a threat to the security and stability of the Polish energy system, as it may lead to a situation in which there is a shortage of energy producers and domestic sources are replaced by energy imports.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Khan, S.A.R.; Ibrahim, R.L.; Al-Amin, A.Q.; Yu, Z. An Ideology of Sustainability under Technological Revolution: Striving towards Sustainable Development. Sustainability 2022, 14, 4415. [Google Scholar] [CrossRef]

- Potrč, S.; Čuček, L.; Martin, M.; Kravanja, Z. Sustainable renewable energy supply networks optimization—The gradual transition to a renewable energy system within the European Union by 2050. Renew. Sustain. Energy Rev. 2021, 146, 111186. [Google Scholar] [CrossRef]

- Afshan, S.; Ozturk, I.; Yaqoob, T. Facilitating renewable energy transition, ecological innovations and stringent environmental policies to improve ecological sustainability: Evidence from MM-QR method. Renew. Energy 2022, 196, 151–160. [Google Scholar] [CrossRef]

- Dall-Orsoletta, A.; Romero, F.; Ferreira, P. Open and collaborative innovation for the energy transition: An exploratory study. Technol. Soc. 2022, 69, 101955. [Google Scholar] [CrossRef]

- Heffron, R.J. Applying energy justice into the energy transition. Renew. Sustain. Energy Rev. 2022, 156, 111936. [Google Scholar] [CrossRef]

- Chen, B.; Xiong, R.; Li, H.; Sun, Q.; Yang, J. Pathways for sustainable energy transition. J. Clean. Prod. 2019, 228, 1564–1571. [Google Scholar] [CrossRef]

- Hu, W.; Wang, D. How does environmental regulation influence China’s carbon productivity? An empirical analysis based on the spatial spillover effect. J. Clean. Prod. 2020, 257, 120484. [Google Scholar] [CrossRef]

- Bublyk, M.; Kowalska-Styczeń, A.; Lytvyn, V.; Vysotska, V. The Ukrainian Economy Transformation into the Circular Based on Fuzzy-Logic Cluster Analysis. Energies 2021, 14, 5951. [Google Scholar] [CrossRef]

- Grosse, T.G. Low Carbon Economy Policy in Poland: An Example of the Impact of Europeanisation. Equilibrium 2011, 6, 9–39. [Google Scholar] [CrossRef]

- Lin, C.; Zhang, L.; Zhang, Z. The impact of the rise of emerging economies on global industrial CO2 emissions: Evidence from emerging economies in Regional Comprehensive Economic Partnership. Resour. Conserv. Recycl. 2022, 177, 106007. [Google Scholar] [CrossRef]

- Kumar, S. Pakistan’s Energy Security: Challenges and Options. Strat. Anal. 2010, 34, 912–924. [Google Scholar] [CrossRef]

- Nguyen, C.P.; Schinckus, C.; Su, T.D. Economic integration and CO2 emissions: Evidence from emerging economies. Clim. Dev. 2020, 12, 369–384. [Google Scholar] [CrossRef]

- Hadfield, P.; Cook, A. Financing the Low-Carbon City: Can Local Government Leverage Public Finance to Facilitate Equitable Decarbonisation? Urban Policy Res. 2019, 37, 13–29. [Google Scholar] [CrossRef]

- Shepard, J.U.; van Ruijven, B.J.; Zakeri, B. Impacts of Trade Friction and Climate Policy on Global Energy Trade Network. Energies 2022, 15, 6171. [Google Scholar] [CrossRef]

- Księżopolski, K.; Maśloch, G. Time Delay Approach to Renewable Energy in the Visegrad Group. Energies 2021, 14, 1928. [Google Scholar] [CrossRef]

- Famulska, T.; Kaczmarzyk, J.; Grząba-Włoszek, M. Environmental Taxes in the Member States of the European Union—Trends in Energy Taxes. Energies 2022, 15, 8718. [Google Scholar] [CrossRef]

- Quaranta, E.; Aggidis, G.; Boes, R.M.; Comoglio, C.; De Michele, C.; Patro, E.R.; Georgievskaia, E.; Harby, A.; Kougias, I.; Muntean, S.; et al. Assessing the energy potential of modernizing the European hydropower fleet. Energy Convers. Manag. 2021, 246, 114655. [Google Scholar] [CrossRef]

- Quaranta, E.; Bódis, K.; Kasiulis, E.; McNabola, A.; Pistocchi, A. Is There a Residual and Hidden Potential for Small and Micro Hydropower in Europe? A Screening-Level Regional Assessment. Water Resour. Manag. 2022, 36, 1745–1762. [Google Scholar] [CrossRef]

- Beal, C.M.; King, C.W. The zero-emissions cost of energy: A policy concept. Prog. Energy 2022, 3, 023001. [Google Scholar] [CrossRef]

- Guo, Z.; Liu, H. The impact of carbon tax policy on energy consumption and CO2 emission in China. Energy Sources Part B Econ. Plan. Policy 2016, 11, 725–731. [Google Scholar] [CrossRef]

- Wolde-Rufael, Y.; Weldemeskel, E.M. Environmental policy stringency, renewable energy consumption and CO2 emissions: Panel cointegration analysis for BRIICTS countries. Int. J. Green Energy 2020, 17, 568–582. [Google Scholar] [CrossRef]

- Mu, H.; Pei, Z.; Wang, H.; Li, N.; Duan, Y. Optimal Strategy for Low-Carbon Development of Power Industry in Northeast China Considering the ‘Dual Carbon’ Goal. Energies 2022, 15, 6455. [Google Scholar] [CrossRef]

- Segura, S.; Ferruz, L.; Gargallo, P.; Salvador, M. EU ETS CO2 emissions constraints and business performance: A quantile regression approach. Appl. Econ. Lett. 2014, 21, 129–134. [Google Scholar] [CrossRef]

- Swain, R.B.; Karimu, A.; Gråd, E. Sustainable development, renewable energy transformation and employment impact in the EU. Int. J. Sustain. Dev. World Ecol. 2022, 29, 695–708. [Google Scholar] [CrossRef]

- Hillebrand, R. Climate protection, energy security, and Germany’s policy of ecological modernisation. Environ. Politics 2013, 22, 664–682. [Google Scholar] [CrossRef]

- Kastanaki, E.; Giannis, A. Energy decarbonisation in the European Union: Assessment of photovoltaic waste recycling potential. Renew. Energy 2022, 192, 1–13. [Google Scholar] [CrossRef]

- Biresselioglu, M.E.; Demir, M.H.; Kaplan, M.D.; Solak, B. Individuals, collectives, and energy transition: Analysing the motivators and barriers of European decarbonisation. Energy Res. Soc. Sci. 2020, 66, 101493. [Google Scholar] [CrossRef]

- European Commission. Communication from the Commission: Europe 2020: A Strategy for Smart, Sustainable and Inclusive Growth, Brussels; European Commission: Brussel, Belgium, 2009.

- European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions: A Policy Framework for Climate and Energy in the Period from 2020 to 2030; European Commission: Brussel, Belgium, 2014.

- Kruse-Andersen, P.K.; Sørensen, P.B. Optimal carbon taxation in EU frontrunner countries: Coordinating with the EU ETS and addressing leakage. Clim. Policy 2022. [Google Scholar] [CrossRef]

- Demailly, D.; Quirion, P. CO2 abatement, competitiveness and leakage in the European cement industry under the EU ETS: Grandfathering versus output-based allocation. Clim. Policy 2006, 6, 93–113. [Google Scholar] [CrossRef]

- Hill, M.R. The European Union’s Emissions Trading Scheme: A Policy Response to the Kyoto Protocol. J. Contemp. Eur. Stud. 2006, 14, 393–410. [Google Scholar] [CrossRef]

- Fitch-Roy, O.; Fairbrass, J.; Benson, D. Ideas, coalitions and compromise: Reinterpreting EU-ETS lobbying through discursive institutionalism. J. Eur. Public Policy 2020, 27, 82–101. [Google Scholar] [CrossRef]

- Garcia-Torea, N.; Giordano-Spring, S.; Larrinaga, C.; Rivière-Giordano, G. Accounting for Carbon Emission Allowances: An Empirical Analysis in the EU ETS Phase 3. Soc. Environ. Account. J. 2022, 42, 93–115. [Google Scholar] [CrossRef]

- Available online: https://climate.ec.europa.eu/eu-action/eu-emissions-trading-system-eu-ets_en (accessed on 1 November 2022).

- Adamczewski, T. Forum Energii Po co Jest EU-ETS Ijaka Reforma nas Czeka? Available online: https://www.forum-energii.eu/pl/blog/ets-reforma (accessed on 20 November 2022).

- Nielsen, H.; Warde, P.; Kander, A. East versus West: Energy intensity in coal-rich Europe, 1800–2000. Energy Policy 2018, 122, 75–83. [Google Scholar] [CrossRef]

- Pérez, M.D.L.E.M.; Scholten, D.; Stegen, K.S. The multi-speed energy transition in Europe: Opportunities and challenges for EU energy security. Energy Strat. Rev. 2019, 26, 100415. [Google Scholar] [CrossRef]

- Balezentis, T. Shrinking ageing population and other drivers of energy consumption and CO2 emission in the residential sector: A case from Eastern Europe. Energy Policy 2020, 140, 111433. [Google Scholar] [CrossRef]

- Zhang, Y.-J.; Wang, A.-D.; Tan, W. The impact of China’s carbon allowance allocation rules on the product prices and emission reduction behaviors of ETS-covered enterprises. Energy Policy 2015, 86, 176–185. [Google Scholar] [CrossRef]

- Zhi, H.; Ni, L.; Zhu, D. The impact of emission trading system on clean energy consumption of enterprises: Evidence from a quasi-natural experiment in China. J. Environ. Manag. 2022, 318, 115613. [Google Scholar] [CrossRef] [PubMed]

- Wang, W.; Xie, P.; Wang, W.; Zhao, D. Overview and evaluation of the mitigation efficiency for China’s seven pilot ETS. Energy Sources Part A Recovery Util. Environ. Eff. 2022, 44, 1798–1812. [Google Scholar] [CrossRef]

- Wei, Y.; Zhu, R.; Tan, L. Emission trading scheme, technological innovation, and competitiveness: Evidence from China’s thermal power enterprises. J. Environ. Manag. 2022, 320, 115874. [Google Scholar] [CrossRef]

- He, M.; Zhu, X.; Li, H. How does carbon emissions trading scheme affect steel enterprises’ pollution control performance? A quasi natural experiment from China. Sci. Total. Environ. 2023, 858, 159871. [Google Scholar] [CrossRef]

- Park, H. Factors to enhance reduction technology development through ETS. Energy Strat. Rev. 2020, 29, 100489. [Google Scholar] [CrossRef]

- Yang, L.; Li, F.; Zhang, X. Chinese companies’ awareness and perceptions of the Emissions Trading Scheme (ETS): Evidence from a national survey in China. Energy Policy 2016, 98, 254–265. [Google Scholar] [CrossRef]

- Chen, Z.; Zhang, X.; Chen, F. Do carbon emission trading schemes stimulate green innovation in enterprises? Evidence from China. Technol. Forecast. Soc. Chang. 2021, 168, 120744. [Google Scholar] [CrossRef]

- He, Y.; Wei, Y.; Fang, Y.; Cao, Y. Booming or sinking: How does an emission trading scheme affect enterprise value? Chin. J. Popul. Resour. Environ. 2022, 20, 227–236. [Google Scholar] [CrossRef]

- Paramati, S.R.; Mo, D.; Gupta, R. The effects of stock market growth and renewable energy use on CO2 emissions: Evidence from G20 countries. Energy Econ. 2017, 66, 360–371. [Google Scholar] [CrossRef]

- Wang, W.; Zhang, Y.-J. Does China’s carbon emissions trading scheme affect the market power of high-carbon enterprises? Energy Econ. 2022, 108, 105906. [Google Scholar] [CrossRef]

- Spassov, Y.; Krustev, A.; Nikolovska, V. Lowest-cost Abatement in Light of the EU ETS and Renewable Feed-in Tariffs in the Electricity Sector in Bulgaria. J. Energy Nat. Resour. Law 2011, 29, 281–303. [Google Scholar] [CrossRef]

- Howie, P.; Atakhanova, Z. Assessing initial conditions and ETS outcomes in a fossil-fuel dependent economy. Energy Strategy Rev. 2022, 40, 100818. [Google Scholar] [CrossRef]

- Joltreau, E.; Sommerfeld, K. Why does emissions trading under the EU Emissions Trading System (ETS) not affect firms’ competitiveness? Empirical findings from the literature. Clim. Policy 2019, 19, 453–471. [Google Scholar] [CrossRef] [Green Version]

- De Beule, F.; Schoubben, F.; Struyfs, K. The pollution haven effect and investment leakage: The case of the EU-ETS. Econ. Lett. 2022, 215, 110536. [Google Scholar] [CrossRef]

- Mularczyk, A.; Zdonek, I.; Turek, M.; Tokarski, S. Intentions to Use Prosumer Photovoltaic Technology in Poland. Energies 2022, 15, 6300. [Google Scholar] [CrossRef]

- Ober, J.; Karwot, J. Pro-Ecological Behavior: Empirical Analysis on the Example of Polish Consumers. Energies 2022, 15, 1690. [Google Scholar] [CrossRef]

- Wolniak, R.; Skotnicka-Zasadzień, B. Development of Photovoltaic Energy in EU Countries as an Alternative to Fossil Fuels. Energies 2022, 15, 662. [Google Scholar] [CrossRef]

- Zdonek, I.; Tokarski, S.; Mularczyk, A.; Turek, M. Evaluation of the Program Subsidizing Prosumer Photovoltaic Sources in Poland. Energies 2022, 15, 846. [Google Scholar] [CrossRef]

- Jonek-Kowalska, I. Multi-criteria evaluation of the effectiveness of energy policy in Central and Eastern European countries in a long-term perspective. Energy Strategy Rev. 2022, 44, 100973. [Google Scholar] [CrossRef]

- Jonek-Kowalska, I. Towards the reduction of CO2 emissions. Paths of pro-ecological transformation of energy mixes in European countries with an above-average share of coal in energy consumption. Resour. Policy 2022, 77, 102701. [Google Scholar] [CrossRef]

- Jonek-Kowalska, I.; Nawrocki, T.L. Holistic fuzzy evaluation of operational risk in polish mining enterprises in a long-term and sectoral research perspective. Resour. Policy 2019, 63, 101464. [Google Scholar] [CrossRef]

- Gajdzik, B.; Wolniak, R.; Grebski, W.W. An Econometric Model of the Operation of the Steel Industry in Poland in the Context of Process Heat and Energy Consumption. Energies 2022, 15, 7909. [Google Scholar] [CrossRef]

- Midor, K.; Ivanova, T.N.; Molenda, M.; Biały, W.; Zakharov, O.V. Aspects of Energy Saving of Oil-Producing Enterprises. Energies 2022, 15, 259. [Google Scholar] [CrossRef]

- Nawrocki, T.L.; Jonek-Kowalska, I. Assessing operational risk in coal mining enterprises—Internal, industrial and international perspectives. Resour. Policy 2016, 48, 50–67. [Google Scholar] [CrossRef]

- Janik, A.; Ryszko, A.; Szafraniec, M. Determinants of the EU Citizens’ Attitudes towards the European Energy Union Priorities. Energies 2021, 14, 5237. [Google Scholar] [CrossRef]

- Jonek-Kowalska, I. How do turbulent sectoral conditions sector influence the value of coal mining enterprises? Perspectives from the Central-Eastern Europe coal mining industry. Resour. Policy 2018, 55, 103–112. [Google Scholar] [CrossRef]

- Król, K.; Zdonek, D. Local Government Website Accessibility—Evidence from Poland. Adm. Sci. 2020, 10, 22. [Google Scholar] [CrossRef]

- Available online: https://www.money.pl/ (accessed on 1 November 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Enterprise | Business Description |

|---|---|---|

| 1 | EC Będzin SA | The company’s core business is the generation of heat and electricity. It is the main source of heat for heating, hot water, and process heat for the Dąbrowa Basin. Customers are industrial, municipal, and service sector entities and households. |

| 2 | Kogeneracja SA | Manufacturer of electricity and heat generated in cogeneration. It consists of three power plants: EC Wrocław, EC Czechnica, and EC Zawidawie. It is part of PGE Energia Ciepła, a PGE Group Company. |

| 3 | Enea SA | The group is a vertically integrated structure that covers with its activity five basic areas on the energy market: electric and thermal energy production (e.g., Kozienice Power Station and Połaniec Power Station), trade in electrical energy, distribution of electrical energy, distribution of heat, as well as mining and enriching hard coal (Lubelski Węgiel Bogdanka). The group provides energy for 2.5 million customers, and the distribution network covers 1/5 of the country. |

| 4 | Energa SA | The core activity of the company involves production, distribution, and trade in electric and thermal energy. The total installed electrical capacity of the group’s power plants is about 1.4 GW. The company’s generating capacity includes a system power plant in Ostrołęka, 2 thermal power plants, 47 hydroelectric power plants, a pumped storage power plant in Żydów, as well as 5 wind farms and 2 photovoltaic farms. The distribution network of the group covers 1/4 of the country. |

| 5 | PGE SA | It is a vertically integrated entity, participating in the entire electricity value chain. It is one of the biggest electricity sector companies in Poland. The group is involved in lignite extraction, production of electrical energy out of fossil fuels (lignite, hard coal, natural gas) and from renewable energy sources (water power plants, wind farms, biomass), and distribution and sale of electrical energy to end customers. |

| 6 | Polenergia SA | It is Poland’s first private energy group consisting of vertically integrated companies operating in the areas of power generation from renewable and low-carbon gas sources, distribution and trading, and sale of electricity to retail and business customers. |

| 7 | Tauron PE SA | This group is one of the leading energy concerns in Poland, covering with its scope 18% of the country’s territory. It is the biggest distributor in the country and the second biggest seller and manufacturer of electrical energy. The basic areas of the group’s activities that create the energy value chain are the extraction of hard coal, production, distribution, and sale of electrical energy and heat. |

| 8 | ZE PAK SA | The group generates energy from conventional sources and by burning and co-firing biomass. The generation assets include four lignite-fired power plants located in central Poland, in the Wielkopolskie Province (Pątnów II Power Plant, which is equipped with a supercritical power unit, Konin Power Plant, and two power plants additionally equipped with biomass co-firing facilities: Pątnów I Power Plant and Adamów Power Plant). |

| Specification | Years | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | |

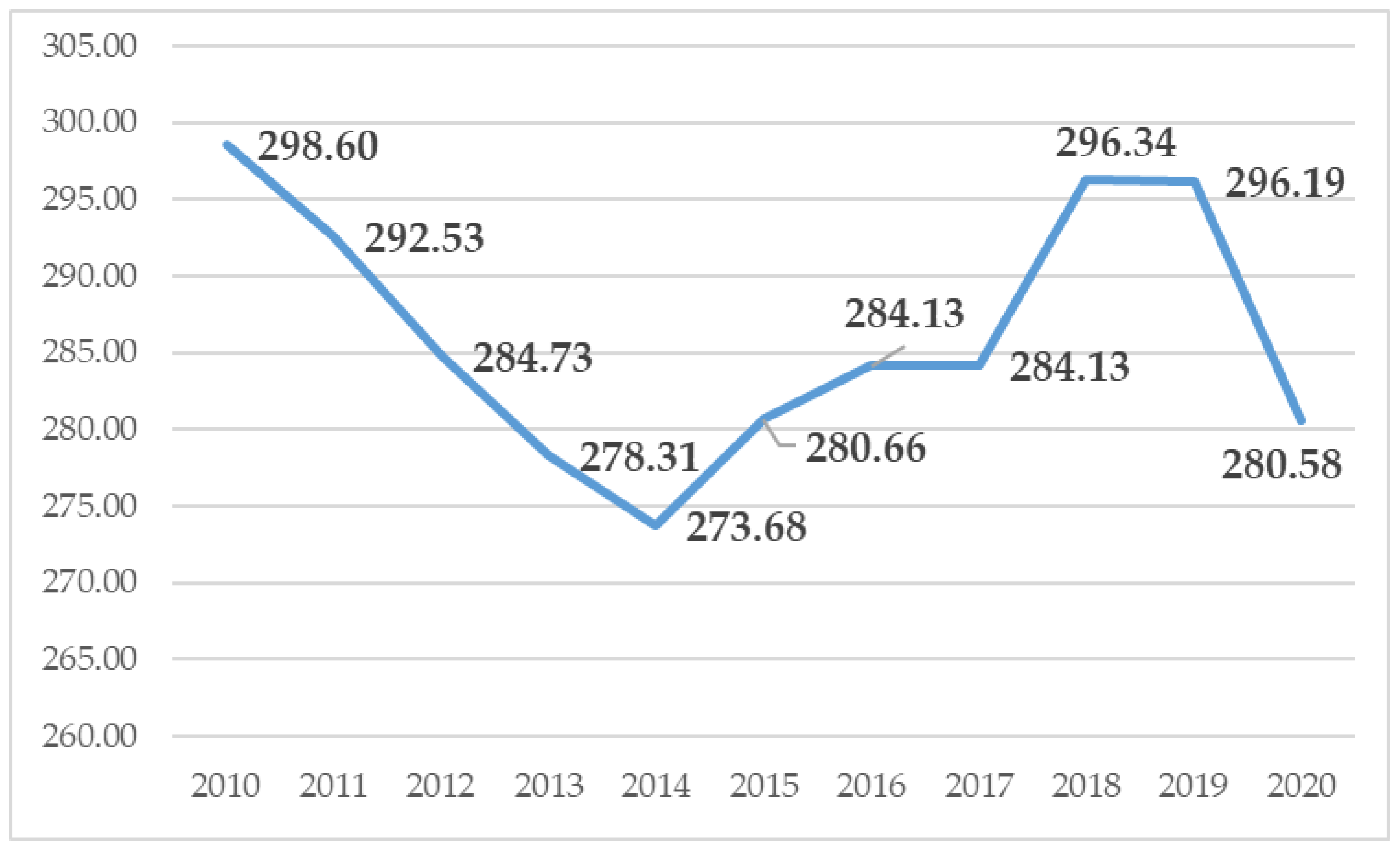

| Price | 13.47 | 10.59 | 6.53 | 5.68 | 6.06 | 7.65 | 7.38 | 7.12 | 16.46 | 24.72 | 28.68 | 56.68 |

| Price dynamics (previous year = 100%) | 100% | 79% | 62% | 87% | 107% | 126% | 97% | 96% | 231% | 150% | 116% | 198% |

| Price dynamics (2010 = 100%) | 100% | 79% | 48% | 42% | 45% | 57% | 55% | 53% | 122% | 184% | 213% | 421% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nawrocki, T.L.; Jonek-Kowalska, I. Efficiency of Polish Energy Companies in the Context of EU Climate Policy. Energies 2023, 16, 826. https://doi.org/10.3390/en16020826

Nawrocki TL, Jonek-Kowalska I. Efficiency of Polish Energy Companies in the Context of EU Climate Policy. Energies. 2023; 16(2):826. https://doi.org/10.3390/en16020826

Chicago/Turabian StyleNawrocki, Tomasz L., and Izabela Jonek-Kowalska. 2023. "Efficiency of Polish Energy Companies in the Context of EU Climate Policy" Energies 16, no. 2: 826. https://doi.org/10.3390/en16020826