Oil-Price Uncertainty and International Stock Returns: Dissecting Quantile-Based Predictability and Spillover Effects Using More than a Century of Data

Abstract

:1. Introduction

2. Predictive Regression Models

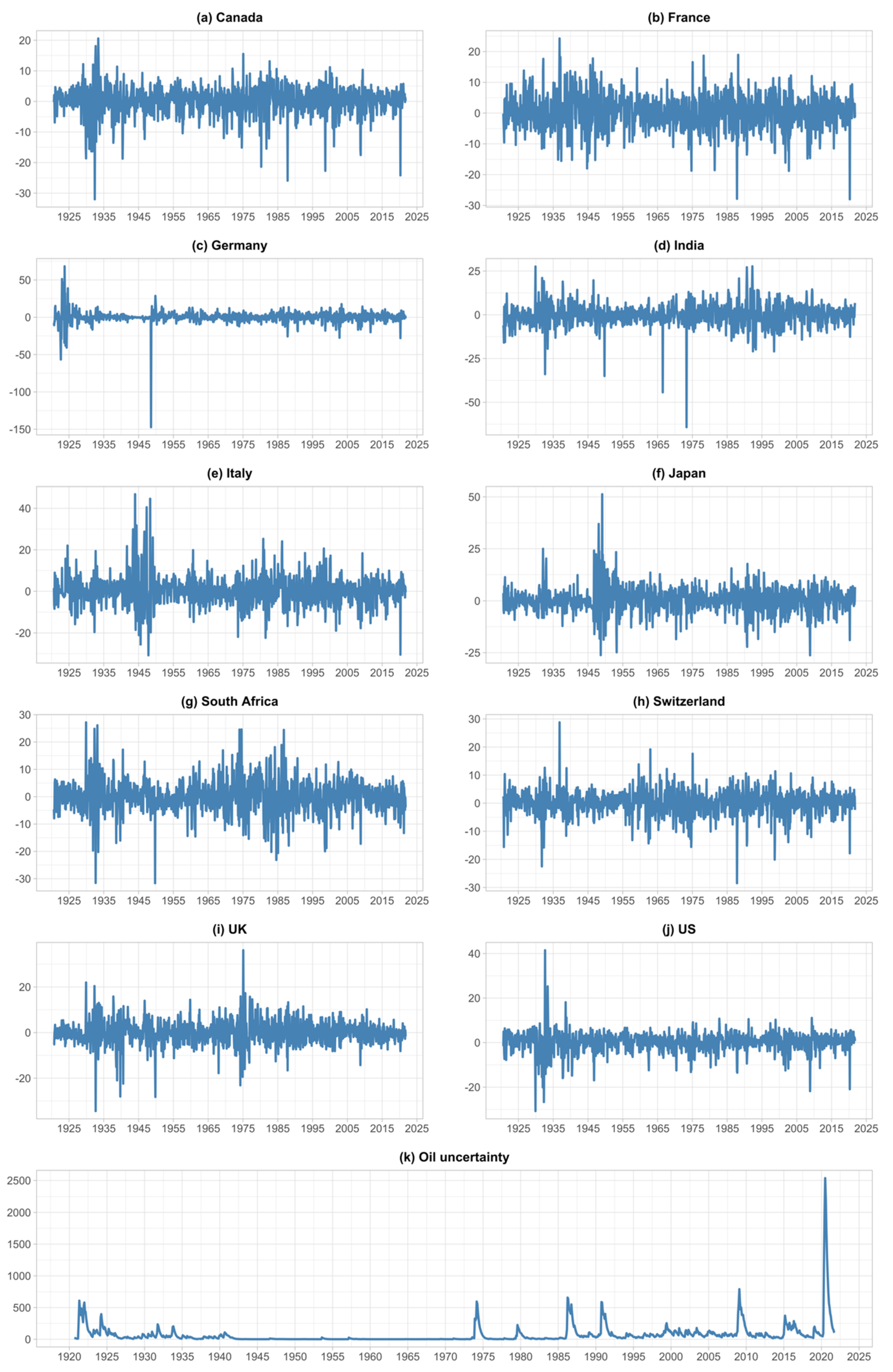

3. Data

4. Empirical Findings

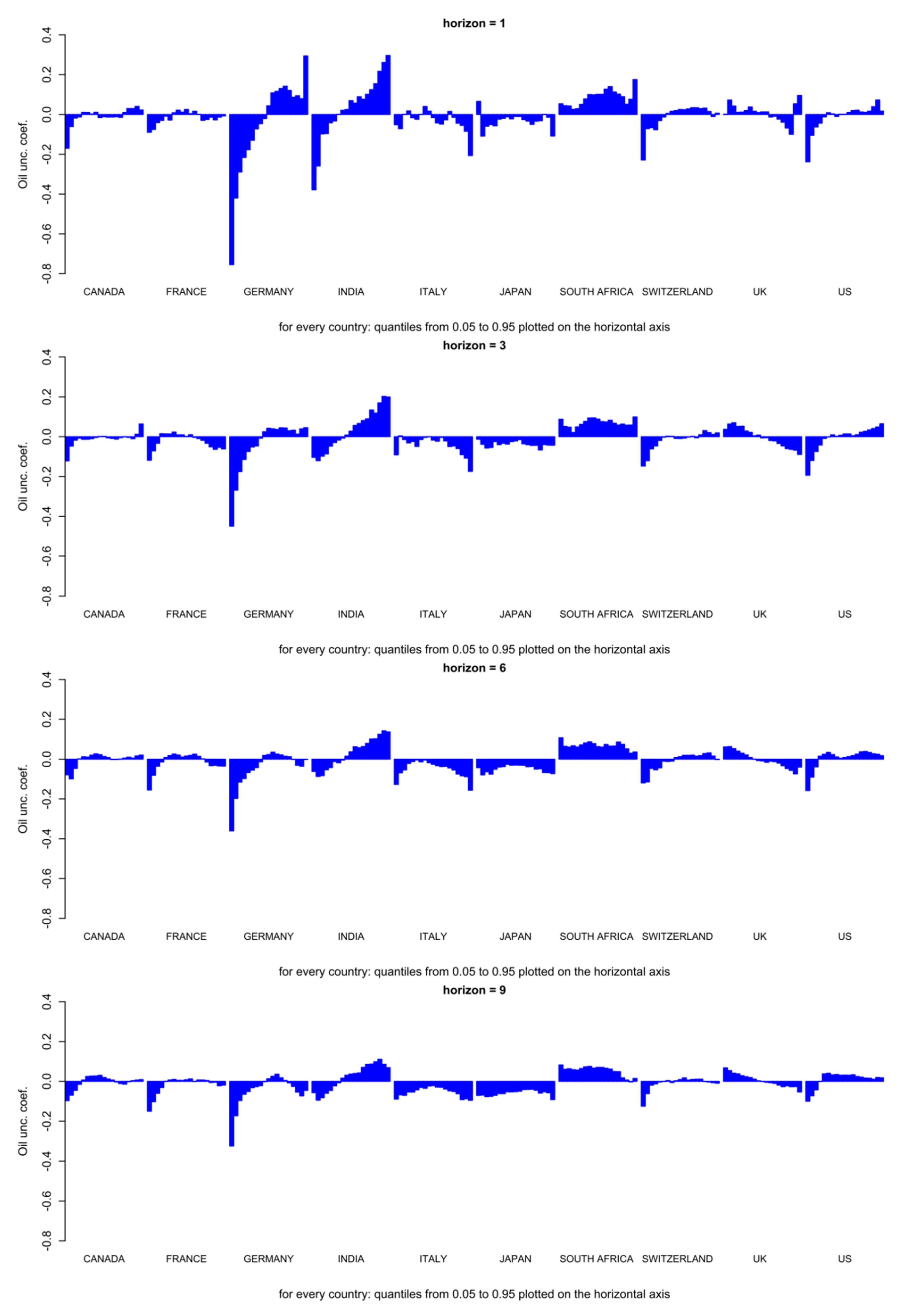

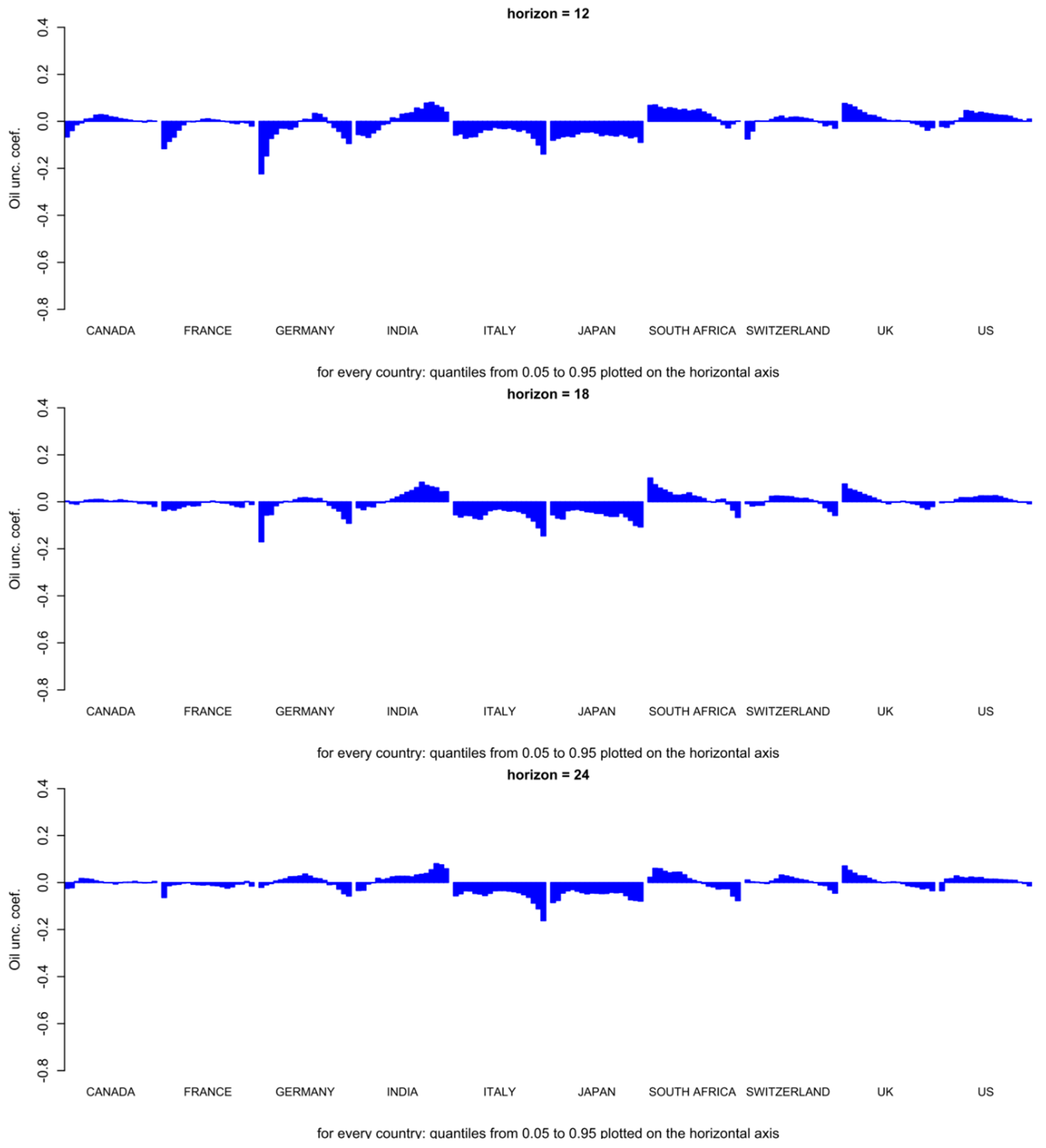

4.1. Forecasting Results

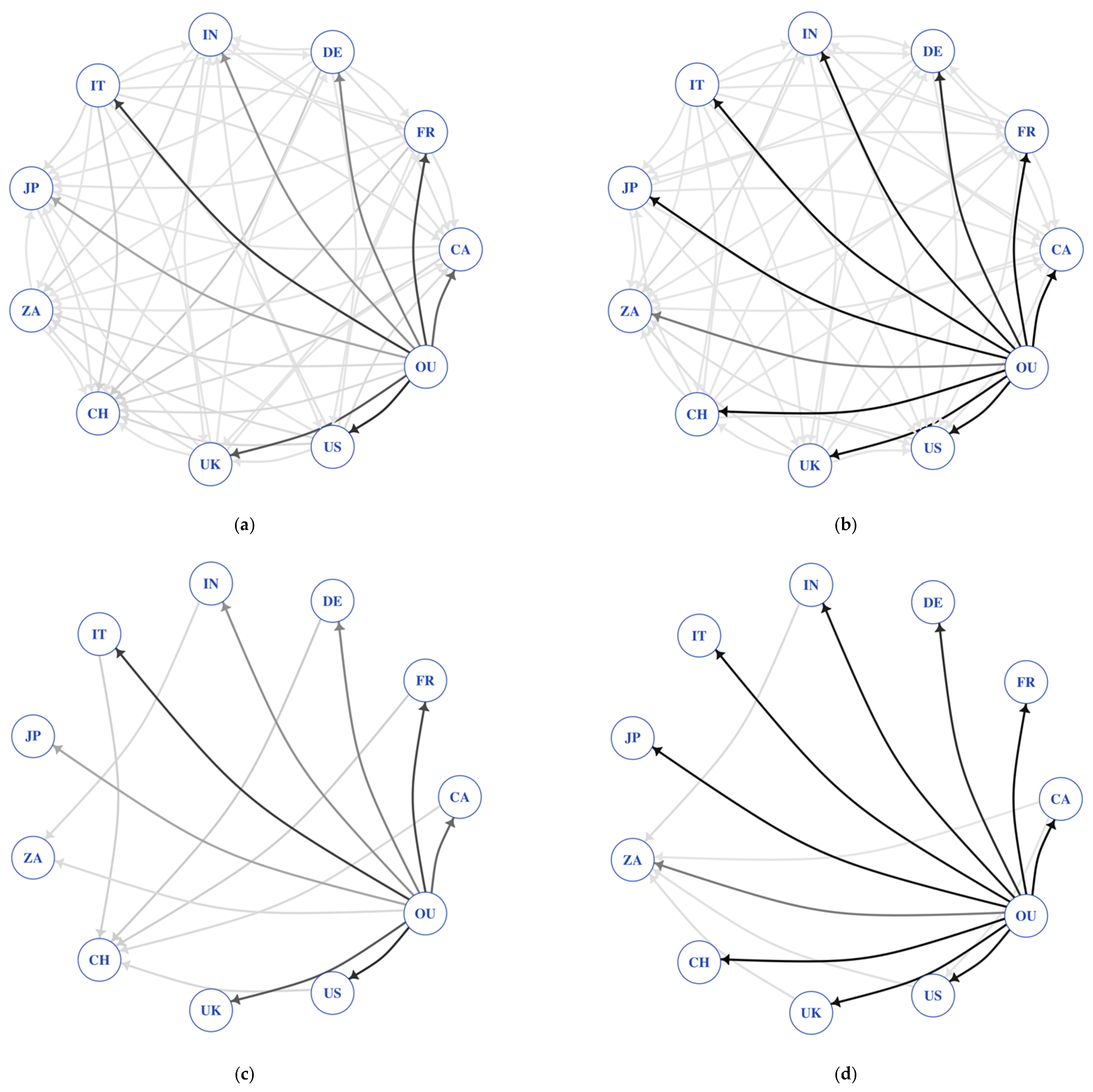

4.2. Regimes-Based Connectedness Results and Investment Implications

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Canada | France | Germany | India | Italy | Japan | |

| Statistic | CA | FR | DE | IN | IT | JP |

| Mean | 0.206 | 0.394 | 0.187 | −0.106 | 0.319 | 0.358 |

| S.D. | 4.592 | 5.503 | 8.073 | 6.253 | 7.058 | 6.034 |

| Min | −32.011 | −28.017 | −147.279 | −64.254 | −30.782 | −26.279 |

| Max | 20.589 | 24.256 | 68.264 | 27.690 | 46.811 | 51.287 |

| Skewness | −1.106 | −0.253 | −4.717 | −1.119 | 0.760 | 0.580 |

| Kurtosis | 5.618 | 1.822 | 100.959 | 13.170 | 5.591 | 7.124 |

| JB | 1852.385 *** | 182.403 *** | 521,844.876 *** | 9063.431 *** | 1706.435 *** | 2647.451 *** |

| South Africa | Switzerland | UK | US | Oil Uncertainty (OIL_UNC) | ||

| Statistic | ZA | CH | UK | US | OU | |

| Mean | 0.040 | 0.159 | 0.024 | 0.310 | 70.975 | |

| S.D. | 5.954 | 4.374 | 5.165 | 4.406 | 165.337 | |

| Min | −31.650 | −28.479 | −34.430 | −30.753 | 1.008 | |

| Max | 27.201 | 28.778 | 36.116 | 41.484 | 2536.770 | |

| Skewness | −0.048 | −0.510 | −0.178 | −0.465 | 7.922 | |

| Kurtosis | 3.156 | 4.988 | 6.059 | 11.969 | 89.223 | |

| JB | 507.507 *** | 1317.739 *** | 1872.398 *** | 7319.968 *** | 416,781.610 *** |

| Canada (CA) | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | 5.4804 *** | 7.2432 *** | 7.7305 *** | 8.0552 *** | 8.3996 *** |

| 3 | 30.0470 *** | 29.8887 *** | 30.0940 *** | 30.5043 *** | 31.2106 *** |

| 6 | 48.8757 *** | 49.5146 *** | 50.2101 *** | 51.8332 *** | 54.7206 *** |

| 9 | 59.7664 *** | 61.5225 *** | 63.5063 *** | 66.8864 *** | 71.8290 *** |

| 12 | 66.6430 *** | 69.3991 *** | 72.3594 *** | 76.7925 *** | 83.0177 *** |

| 18 | 73.4330 *** | 77.3927 *** | 81.6248 *** | 87.7516 *** | 96.1108 *** |

| 24 | 73.9455 *** | 77.8864 *** | 82.5771 *** | 89.3594 *** | 98.4716 *** |

| France (FR) | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | 6.3620 *** | 7.2471 *** | 7.9322 *** | 8.4771 *** | 9.2419 *** |

| 3 | 32.0595 *** | 31.0787 *** | 31.0264 *** | 31.4570 *** | 32.2572 *** |

| 6 | 50.4667 *** | 50.4568 *** | 50.7707 *** | 52.1863 *** | 54.5124 *** |

| 9 | 60.2360 *** | 62.0011 *** | 63.7013 *** | 66.6309 *** | 70.9955 *** |

| 12 | 71.1355 *** | 74.1394 *** | 77.2470 *** | 81.9037 *** | 88.3707 *** |

| 18 | 78.0588 *** | 82.0287 *** | 86.4896 *** | 92.8287 *** | 101.4192 *** |

| 24 | 84.1488 *** | 89.0199 *** | 94.7484 *** | 102.8983 *** | 113.8628 *** |

| Germany (DE) | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | −0.0304 | −0.0408 | −0.0489 | −0.0558 | −0.0619 |

| 3 | 22.1413 *** | 19.8431 *** | 17.8224 *** | 16.2627 *** | 15.0398 *** |

| 6 | 49.1776 *** | 49.8417 *** | 50.7371 *** | 52.9877 *** | 56.5639 *** |

| 9 | 57.4173 *** | 59.4958 *** | 61.9414 *** | 65.7028 *** | 70.9413 *** |

| 12 | 64.2860 *** | 67.0138 *** | 70.1761 *** | 75.0193 *** | 81.7098 *** |

| 18 | 65.8235 *** | 69.5390 *** | 73.6751 *** | 79.6903 *** | 87.8614 *** |

| 24 | 68.1973 *** | 72.3469 *** | 77.2291 *** | 84.2390 *** | 93.6809 *** |

| India (IN) | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | 6.6610 *** | 7.8605 *** | 8.7403 *** | 9.7294 *** | 10.8895 *** |

| 3 | 34.2447 *** | 33.4717 *** | 33.1863 *** | 33.8146 *** | 35.2266 *** |

| 6 | 55.9590 *** | 56.5965 *** | 57.3946 *** | 59.3295 *** | 62.5465 *** |

| 9 | 68.4950 *** | 70.3921 *** | 72.5318 *** | 75.9896 *** | 81.2207 *** |

| 12 | 82.4923 *** | 85.7183 *** | 89.1765 *** | 94.5480 *** | 102.2504 *** |

| 18 | 100.5006 *** | 105.5870 *** | 111.3451 *** | 119.6967 *** | 130.9977 *** |

| 24 | 101.6299 *** | 107.1692 *** | 113.8164 *** | 123.5633 *** | 136.7903 *** |

| Italy (IT) | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | 8.1219 *** | 9.9043 *** | 11.8050 *** | 12.9516 *** | 14.0496 *** |

| 3 | 31.1155 *** | 31.2116 *** | 32.0832 *** | 33.2771 *** | 34.8462 *** |

| 6 | 45.0681 *** | 46.1790 *** | 47.1035 *** | 49.0987 *** | 52.1795 *** |

| 9 | 52.6023 *** | 54.2944 *** | 56.5492 *** | 60.0800 *** | 64.952 *** |

| 12 | 58.6007 *** | 61.2763 *** | 64.2609 *** | 68.9322 *** | 75.3187 *** |

| 18 | 65.6667 *** | 68.8835 *** | 72.6163 *** | 78.1481 *** | 85.6733 *** |

| 24 | 72.3672 *** | 76.4420 *** | 81.2412 *** | 88.1203 *** | 97.4060 *** |

| Japan (JP) | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | 7.7895 *** | 10.5237 *** | 12.3909 *** | 13.5504 *** | 14.7601 *** |

| 3 | 32.6978 *** | 33.0664 *** | 33.4913 *** | 34.4981 *** | 36.0140 *** |

| 6 | 46.1696 *** | 47.9324 *** | 49.0691 *** | 51.0530 *** | 54.0522 *** |

| 9 | 56.6341 *** | 59.0716 *** | 61.5812 *** | 65.3488 *** | 70.3983 *** |

| 12 | 64.5106 *** | 67.6304 *** | 71.1540 *** | 76.2769 *** | 83.1049 *** |

| 18 | 70.9028 *** | 75.1158 *** | 79.5581 *** | 85.7982 *** | 94.2258 *** |

| 24 | 72.6994 *** | 77.0989 *** | 82.1197 *** | 89.3549 *** | 99.0218 *** |

| South Africa (ZA) | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | 8.2964 *** | 9.4845 *** | 10.8520 *** | 11.6503 *** | 12.7213 *** |

| 3 | 34.1471 *** | 33.4270 *** | 33.7088 *** | 34.5045 *** | 35.8966 *** |

| 6 | 57.9810 *** | 58.3660 *** | 58.8450 *** | 60.6053 *** | 63.7685 *** |

| 9 | 72.9328 *** | 75.2876 *** | 77.8432 *** | 81.9912 *** | 87.8248 *** |

| 12 | 80.7393 *** | 84.4037 *** | 88.4145 *** | 94.6587 *** | 103.1594 *** |

| 18 | 83.4895 *** | 88.1933 *** | 93.5529 *** | 101.3645 *** | 111.9483 *** |

| 24 | 92.3261 *** | 97.6548 *** | 103.8140 *** | 112.8047 *** | 125.0195 *** |

| Switzerland (CH) | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | 7.4940 *** | 7.8755 *** | 9.0694 *** | 9.7816 *** | 10.7581 *** |

| 3 | 31.9384 *** | 30.7749 *** | 30.6713 *** | 31.4211 *** | 32.7586 *** |

| 6 | 49.7216 *** | 50.8735 *** | 52.0055 *** | 54.1263 *** | 57.3040 *** |

| 9 | 63.0756 *** | 65.3880 *** | 67.7258 *** | 71.4613 *** | 76.8146 *** |

| 12 | 71.2159 *** | 74.5311 *** | 78.1453 *** | 83.4362 *** | 90.5305 *** |

| 18 | 83.8940 *** | 88.6358 *** | 94.0200 *** | 101.6712 *** | 111.9015 *** |

| 24 | 85.7254 *** | 90.8166 *** | 96.7568 *** | 105.1647 *** | 116.4791 *** |

| UK | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | 7.3849 *** | 9.5479 *** | 10.6744 *** | 11.9226 *** | 12.6929 *** |

| 3 | 26.9010 *** | 27.2498 *** | 27.9282 *** | 28.9153 *** | 30.2618 *** |

| 6 | 41.1060 *** | 41.7911 *** | 42.3479 *** | 43.6310 *** | 45.9965 *** |

| 9 | 48.1450 *** | 49.6972 *** | 51.4142 *** | 54.0192 *** | 57.7359 *** |

| 12 | 52.6877 *** | 54.8292 *** | 57.1575 *** | 60.8198 *** | 65.7464 *** |

| 18 | 62.3997 *** | 65.7829 *** | 69.4332 *** | 74.7400 *** | 81.8649 *** |

| 24 | 65.9381 *** | 69.7089 *** | 73.9110 *** | 79.8362 *** | 87.8560 *** |

| US | |||||

| Horizon | m | ||||

| 2 | 3 | 4 | 5 | 6 | |

| 1 | 7.2639 *** | 8.4353 *** | 9.4870 *** | 10.3174 *** | 11.2059 *** |

| 3 | 33.4457 *** | 33.8675 *** | 34.6486 *** | 35.9221 *** | 37.9822 *** |

| 6 | 50.0905 *** | 50.9738 *** | 52.1340 *** | 54.4882 *** | 58.1975 *** |

| 9 | 58.4171 *** | 60.6130 *** | 63.3531 *** | 67.6082 *** | 73.4821 *** |

| 12 | 65.5209 *** | 68.5206 *** | 71.9698 *** | 77.0623 *** | 84.1272 *** |

| 18 | 69.3140 *** | 72.9984 *** | 77.4758 *** | 83.9991 *** | 92.7723 *** |

| 24 | 71.3134 *** | 75.2479 *** | 80.0222 *** | 86.9867 *** | 96.3795 *** |

| Canada (CA) | |

| Horizon | Dates |

| 1 | 1940M12, 1956M08, 1975M01 |

| 3 | |

| 6 | |

| 9 | 1937M07, 1952M11, 1967M11, 1982M11, 2000M11 |

| 12 | 1937M09, 1957M02, 1975M08, 1990M10, 2006M09 |

| 18 | 1937M08, 1957M02, 1975M11, 1990M10, 2006M11 |

| 24 | 1937M09, 1952M07, 1967M05, 1983M08, 2001M06 |

| France (FR) | |

| Horizon | Dates |

| 1 | 1939M10, 1962M05 |

| 3 | 1939M11, 1962M06 |

| 6 | 1940M02, 1962M06 |

| 9 | 1940M04, 1960M06, 1975M06, 1990M06, 2006M10 |

| 12 | 1940M06, 1960M09, 1975M09, 1990M09, 2006M10 |

| 18 | 1940M12, 1960M12, 1975M11, 1990M10, 2006M11 |

| 24 | 1940M06, 1961M02, 1975M12, 1990M10, 2006M12 |

| Germany (DE) | |

| Horizon | Dates |

| 1 | 1935M10, 1950M12, 1966M03, 1982M09, 2000M03 |

| 3 | 1935M11, 1951M01, 1966M04, 1982M09, 2000M05 |

| 6 | 1936M02, 1951M03, 1966M04, 1982M11, 2000M06 |

| 9 | 1936M04, 1951M04, 1966M04, 1982M12, 2000M09 |

| 12 | 1936M07, 1951M07, 1966M07, 1982M12, 2000M11 |

| 18 | 1950M01, 1964M12, 1983M02, 2001M02 |

| 24 | 1950M07, 1965M05, 1982M12, 2000M11 |

| India (IN) | |

| Horizon | Dates |

| 1 | 1940M12, 1956M04, 1976M07, 1991M08, 2006M09 |

| 3 | 1940M12, 1956M05, 1976M07, 1991M08, 2006M09 |

| 6 | 1941M03, 1956M08, 1976M07, 1991M08, 2006M09 |

| 9 | 1941M06, 1956M09, 1975M10, 1990M10, 2005M10 |

| 12 | 1947M07, 1968M03, 1987M05, 2002M06 |

| 18 | 1948M01, 1969M01, 1986M04, 2002M04 |

| 24 | 1948M05, 1977M05, 1995M09 |

| Italy (IT) | |

| Horizon | Dates |

| 1 | |

| 3 | |

| 6 | 1939M06, 1961M07, 1978M05 |

| 9 | 1939M06, 1960M10, 1975M10, 1990M10, 2006M10 |

| 12 | 1939M07, 1960M10, 1975M10, 1990M10, 2006M10 |

| 18 | 1939M10, 1960M12, 1975M11, 1990M10, 2006M11 |

| 24 | 1939M11, 1962M06, 1979M02, 2001M02 |

| Japan (JP) | |

| Horizon | Dates |

| 1 | |

| 3 | |

| 6 | 1944M12, 1960M01, 1975M02, 1990M03, 2005M04 |

| 9 | 1945M04, 1960M04, 1975M04, 1990M04, 2005M05 |

| 12 | 1945M07, 1960M07, 1975M07, 1990M07, 2005M07 |

| 18 | 1947M12, 1962M11, 1989M10, 2004M09 |

| 24 | 1948M01, 1962M11, 1990M02, 2004M12 |

| South Africa (ZA) | |

| Horizon | Dates |

| 1 | 1940M06, 1974M02 |

| 3 | 1941M05, 1956M09, 1974M04, 1991M07, 2006M09 |

| 6 | 1941M05, 1961M09, 1981M01, 2000M10 |

| 9 | 1941M05, 1961M11, 1981M02, 2001M01 |

| 12 | 1947M05, 1962M05, 1981M05, 2001M03 |

| 18 | 1947M10, 1962M09, 1981M11, 2001M02 |

| 24 | 1948M06, 1963M04, 1982M02, 2000M12 |

| Switzerland (CH) | |

| Horizon | Dates |

| 1 | 1945M04, 1962M03, 1982M08, 1998M08 |

| 3 | 1945M05, 1962M04, 1982M09, 1998M08 |

| 6 | 1945M08, 1962M05, 1982M11, 1998M08 |

| 9 | 1945M09, 1962M05, 1982M11, 1998M09 |

| 12 | 1939M01, 1962M05, 1982M12, 2001M03 |

| 18 | 1939M06, 1962M07, 1983M02, 1999M07 |

| 24 | 1939M06, 1962M10, 1983M07, 2000M01 |

| UK | |

| Horizon | Dates |

| 1 | 1941M08, 1956M12, 1974M04, 1990M12, 2006M09 |

| 3 | 1941M06, 1967M05, 1982M09 |

| 6 | 1941M10, 1957M01, 1975M01, 1991M04, 2006M09 |

| 9 | 1941M10, 1956M12, 1975M01, 1991M04, 2006M10 |

| 12 | 1941M07, 1957M01, 1975M01, 1990M01, 2006M10 |

| 18 | 1941M10, 1957M03, 1975M04, 1990M03, 2006M11 |

| 24 | 1941M09, 1957M03, 1975M01, 1989M11, 2006M12 |

| US | |

| Horizon | Dates |

| 1 | |

| 3 | |

| 6 | 1937M04, 1952M05, 1967M08, 1982M09, 1999M09 |

| 9 | 1937M05, 1952M07, 1967M11, 1982M11, 2000M08 |

| 12 | 1937M06, 1952M06, 1968M01, 1983M01, 2000M04 |

| 18 | 1937M05, 1952M04, 1967M03, 1983M02, 2000M09 |

| 24 | 1937M09, 1952M07, 1967M05, 1983M04, 2000M11 |

| Canada (CA) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0096 | 1.0539 | 1.0207 | 1.0063 | 1.0056 | 1.0692 | 1.0225 | 1.0565 | 1.0541 | 1.0681 |

| 3 | 1.1653 | 0.9834 *** | 1.0260 | 1.0137 | 1.1749 | 1.1579 | 1.3767 | 1.1520 | 1.0041 | 1.1533 |

| 6 | 1.0695 | 3.6724 | 2.8853 | 1.5703 | 1.0828 | 1.0428 | 0.9909 *** | 1.0160 | 1.7642 | 2.5774 |

| 9 | 1.0097 | 1.0775 | 1.0009 | 1.0102 | 1.0289 | 1.0012 | 1.0055 | 1.0082 | 1.0198 | 1.1721 |

| 12 | 1.0426 | 1.1246 | 1.0181 | 0.9767 *** | 1.0041 | 0.9960 *** | 1.0777 | 1.0577 | 1.0481 | 1.0280 |

| 18 | 1.0415 | 0.9319 *** | 1.0219 | 0.9984 ** | 1.0093 | 1.0224 | 1.0306 | 1.0739 | 0.9909 *** | 0.9967 ** |

| 24 | 1.1414 | 1.1748 | 1.0304 | 1.2822 | 1.0970 | 1.0810 | 1.0539 | 1.0424 | 0.9874 *** | 0.9849 *** |

| France (FR) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0313 | 1.0527 | 1.0000 | 1.0215 | 1.0231 | 1.1059 | 1.0470 | 1.0838 | 1.1175 | 1.1217 |

| 3 | 1.1494 | 0.9469 *** | 0.9420 *** | 1.1186 | 1.1266 | 1.1617 | 1.1589 | 1.0852 | 1.1215 | 1.0157 |

| 6 | 1.0095 | 1.0188 | 0.9864 *** | 1.0475 | 1.0057 | 1.0044 | 1.0184 | 0.9977 ** | 0.9696 *** | 1.0002 |

| 9 | 1.0015 | 1.0973 | 1.0783 | 1.0000 | 0.9929 *** | 0.9913 *** | 1.0098 | 0.9977 ** | 0.9986 ** | 1.1446 |

| 12 | 0.9937 *** | 1.0030 | 0.9432 *** | 0.9674 *** | 1.0113 | 1.0188 | 0.9883 *** | 0.9917 *** | 1.0205 | 1.0648 |

| 18 | 1.0137 | 0.9867 *** | 1.1046 | 1.0585 | 1.0279 | 1.0175 | 1.0282 | 0.9880 *** | 1.1046 | 0.9785 *** |

| 24 | 1.3594 | 1.1084 | 1.0417 | 1.5507 | 1.3332 | 1.3228 | 1.3951 | 1.4304 | 1.2986 | 2.5698 |

| Germany (DE) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0279 | 1.1018 | 0.9898 *** | 1.0360 | 1.0204 | 1.0448 | 1.1372 | 1.0048 | 1.1026 | 1.0208 |

| 3 | 1.1151 | 0.9379 *** | 1.0549 | 1.2953 | 1.1239 | 1.1144 | 1.0876 | 1.0256 | 1.0308 | 1.0686 |

| 6 | 1.0230 | 1.0046 | 0.9894 *** | 1.0064 | 1.0024 | 1.0043 | 1.0321 | 1.0120 | 1.0740 | 1.0010 |

| 9 | 1.0030 | 1.2079 | 0.9989 * | 1.0230 | 1.0217 | 0.9938 *** | 0.9912 *** | 0.9995 | 1.0267 | 0.9872 *** |

| 12 | 0.9980 ** | 1.0389 | 0.9968 ** | 1.0012 | 0.9947 *** | 0.9985 ** | 0.9969 ** | 1.0231 | 0.9805 *** | 1.0071 |

| 18 | 1.0313 | 0.9988 * | 1.0337 | 1.0673 | 1.0675 | 1.0283 | 1.0253 | 1.0513 | 0.9915 *** | 0.9369 *** |

| 24 | 1.9997 | 1.2953 | 1.3754 | 1.6164 | 1.7809 | 2.1678 | 2.3916 | 2.3820 | 3.2277 | 4.1536 |

| India (IN) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0978 | 1.4814 | 1.0274 | 1.2574 | 1.1813 | 1.1473 | 1.1468 | 1.0286 | 1.1446 | 1.0188 |

| 3 | 1.0085 | 1.0727 | 1.0415 | 1.4281 | 1.1178 | 1.0832 | 0.9824 *** | 0.9711 *** | 1.0006 | 1.0187 |

| 6 | 1.0248 | 1.0924 | 0.9995 | 1.0007 | 1.0071 | 1.0155 | 1.0914 | 1.0631 | 1.0370 | 0.9494 *** |

| 9 | 1.0184 | 1.0396 | 1.0065 | 1.0293 | 1.0306 | 0.9973 ** | 0.9981 ** | 0.9995 | 0.9757 *** | 1.1052 |

| 12 | 0.9998 | 1.0349 | 0.9828 *** | 0.9998 | 1.0011 | 1.0048 | 1.0216 | 0.9920 *** | 0.9639 *** | 1.0069 |

| 18 | 1.0422 | 0.9695 *** | 0.9801 *** | 1.0793 | 1.1084 | 1.0888 | 1.1171 | 1.0380 | 0.9846 *** | 1.0141 |

| 24 | 1.0024 | 1.0503 | 0.9541 *** | 1.0345 | 1.0017 | 1.0018 | 1.0207 | 1.0009 | 1.0319 | 1.0166 |

| Italy (IT) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.1823 | 0.7720 *** | 1.1620 | 1.5118 | 1.4267 | 1.2264 | 1.1427 | 1.1004 | 1.1092 | 1.0123 |

| 3 | 1.1822 | 1.0281 | 1.7459 | 1.4004 | 1.3863 | 1.0002 | 1.0119 | 0.9681 *** | 1.0874 | 1.0138 |

| 6 | 1.0074 | 0.8750 *** | 1.0080 | 1.0002 | 1.0014 | 0.9872 *** | 1.0717 | 1.0194 | 1.0022 | 1.0442 |

| 9 | 1.2124 | 1.0220 | 1.1897 | 1.1015 | 1.0460 | 1.0197 | 1.1358 | 1.4979 | 1.2484 | 1.3853 |

| 12 | 1.0000 | 1.0521 | 1.0373 | 0.9943 *** | 1.0061 | 0.9979 ** | 1.0209 | 1.0349 | 1.0578 | 1.1765 |

| 18 | 1.0291 | 1.0006 | 1.0080 | 1.0531 | 1.0765 | 1.1013 | 1.0739 | 1.0585 | 1.0108 | 0.9812 *** |

| 24 | 1.0053 | 1.0635 | 1.0201 | 1.0394 | 1.0173 | 1.0704 | 1.0097 | 0.9958 *** | 1.0163 | 1.0753 |

| Japan (JP) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.2420 | 0.9940 *** | 1.2484 | 1.7484 | 1.6886 | 1.3154 | 1.1184 | 1.0560 | 1.0853 | 1.0603 |

| 3 | 1.2625 | 1.7774 | 1.7937 | 1.0878 | 1.0151 | 1.0109 | 1.0547 | 1.1246 | 1.0573 | 1.1131 |

| 6 | 1.0223 | 0.9873 *** | 1.0180 | 1.0746 | 1.0076 | 1.0391 | 1.0806 | 1.0392 | 0.9947 *** | 1.0003 |

| 9 | 1.0012 | 1.0090 | 1.0027 | 1.0031 | 1.0031 | 1.0054 | 0.9999 | 1.0020 | 1.0002 | 1.0206 |

| 12 | 0.9974 ** | 1.0620 | 1.0324 | 0.9806 *** | 1.0010 | 0.9980 ** | 1.0126 | 1.0178 | 1.0751 | 1.1429 |

| 18 | 1.0002 | 1.5033 | 1.0417 | 1.0012 | 1.0367 | 1.1547 | 1.0448 | 0.9856 *** | 0.9976 ** | 1.0058 |

| 24 | 1.0025 | 1.1077 | 1.0006 | 1.0076 | 1.1255 | 1.0761 | 1.0774 | 1.0424 | 1.0013 | 0.9898 *** |

| South Africa (ZA) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.4650 | 0.9945 *** | 1.8966 | 2.1014 | 1.9733 | 1.8073 | 1.9312 | 1.2950 | 1.0204 | 0.9817 *** |

| 3 | 1.0708 | 1.4051 | 1.3542 | 1.1024 | 0.9813 *** | 1.0104 | 1.0200 | 1.0921 | 1.0107 | 1.0261 |

| 6 | 0.9947 *** | 1.0304 | 1.0222 | 0.9977 ** | 1.0135 | 0.9369 *** | 0.9627 *** | 1.0376 | 1.0192 | 1.0136 |

| 9 | 0.9999 | 1.0205 | 1.0358 | 0.9965 *** | 1.0090 | 0.9984 ** | 1.0001 | 1.0009 | 0.9941 *** | 1.0138 |

| 12 | 1.0070 | 1.0895 | 0.9975 ** | 0.9957 *** | 0.9749 *** | 0.9918 *** | 1.0050 | 0.9994 * | 1.0011 | 0.9736 *** |

| 18 | 1.0216 | 1.0691 | 1.1364 | 1.0466 | 1.0634 | 1.0373 | 1.0168 | 1.0039 | 0.9895 *** | 1.0167 |

| 24 | 1.0402 | 1.1938 | 1.0024 | 1.0669 | 1.1141 | 1.1288 | 1.1311 | 1.1342 | 0.9889 *** | 1.0083 |

| Switzerland (CH) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0279 | 1.0496 | 1.0018 | 1.0119 | 1.0090 | 0.9998 | 1.0692 | 1.1040 | 1.1118 | 1.1047 |

| 3 | 0.9998 | 1.2222 | 1.1021 | 1.0053 | 1.0216 | 1.1108 | 1.0138 | 0.8667 *** | 1.0533 | 1.0154 |

| 6 | 1.0565 | 0.9798 *** | 1.0370 | 1.0100 | 0.9812 *** | 1.1639 | 1.1867 | 1.0328 | 1.0160 | 1.0183 |

| 9 | 1.0301 | 1.1459 | 1.0247 | 1.0025 | 1.0043 | 1.0047 | 1.0113 | 1.0100 | 1.0238 | 1.0247 |

| 12 | 1.0419 | 0.9803 *** | 0.9976 ** | 1.0122 | 1.0058 | 1.1001 | 1.0572 | 1.0242 | 1.0173 | 0.9930 *** |

| 18 | 1.0600 | 1.0691 | 1.0739 | 1.1491 | 1.0879 | 1.0784 | 1.0828 | 1.0381 | 0.9783 *** | 1.0375 |

| 24 | 1.0990 | 0.9874 *** | 0.9947 *** | 1.1388 | 1.2852 | 1.2089 | 1.1239 | 1.0596 | 1.0010 | 1.1398 |

| UK | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0434 | 1.0109 | 1.0136 | 1.0100 | 0.9996 | 1.0531 | 1.0868 | 1.2331 | 1.1611 | 1.0767 |

| 3 | 1.0323 | 1.4793 | 1.0448 | 1.0267 | 1.0649 | 1.0963 | 1.0343 | 0.9485 *** | 0.9670 *** | 0.9797 *** |

| 6 | 1.0012 | 1.2523 | 1.0781 | 1.0078 | 1.0069 | 1.0031 | 1.0022 | 0.9990 * | 1.0072 | 1.1252 |

| 9 | 1.0847 | 1.0446 | 1.0154 | 1.0109 | 1.0584 | 1.0510 | 1.0718 | 1.0722 | 1.0875 | 1.0844 |

| 12 | 1.3548 | 1.2745 | 1.2623 | 1.3162 | 1.3016 | 1.2363 | 1.2374 | 1.1294 | 1.0468 | 1.0564 |

| 18 | 1.0766 | 1.1655 | 1.0600 | 1.0944 | 1.1366 | 1.1212 | 1.0326 | 1.0043 | 1.0045 | 1.0186 |

| 24 | 1.1771 | 1.0165 | 1.4577 | 1.2638 | 1.1698 | 1.1418 | 1.2222 | 1.1263 | 1.0788 | 0.9917 *** |

| US | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0497 | 1.0348 | 1.0002 | 0.9872 *** | 0.9995 | 1.1256 | 1.0973 | 1.1177 | 1.1432 | 1.0528 |

| 3 | 1.3280 | 0.9840 *** | 1.3684 | 1.0353 | 1.0276 | 1.0337 | 1.0000 | 2.7862 | 1.4646 | 1.3231 |

| 6 | 1.0004 | 1.0385 | 0.9756 *** | 0.9718 *** | 0.9942 *** | 1.0033 | 1.0291 | 1.0555 | 1.0440 | 1.0169 |

| 9 | 1.0755 | 0.9941 *** | 0.9895 *** | 0.9877 *** | 1.0202 | 1.0466 | 1.0866 | 1.0581 | 1.0790 | 1.0206 |

| 12 | 1.0067 | 1.0155 | 1.0299 | 1.0278 | 1.0109 | 1.0037 | 0.9989 * | 0.9788 *** | 1.0072 | 1.0008 |

| 18 | 1.0942 | 1.1269 | 1.1496 | 1.1291 | 1.1904 | 1.0899 | 1.0626 | 1.0094 | 1.0057 | 1.0084 |

| 24 | 1.4691 | 1.8355 | 1.9966 | 1.5954 | 1.4648 | 1.3589 | 1.2509 | 1.2500 | 1.2216 | 1.0107 |

| Lower Regime | ||||||||||||

| CA | FR | DE | IN | IT | JP | ZA | CH | UK | US | OIL_UNC | From | |

| CA | 26.75 | 7.13 | 5.38 | 5.24 | 5.59 | 2.09 | 1.48 | 6.80 | 0.79 | 13.46 | 25.29 | 73.25 |

| FR | 3.28 | 24.97 | 4.25 | 0.44 | 5.70 | 1.71 | 0.09 | 4.20 | 0.34 | 2.06 | 52.95 | 75.03 |

| DE | 1.49 | 2.48 | 71.54 | 0.24 | 2.63 | 1.49 | 0.04 | 2.75 | 0.23 | 1.24 | 15.88 | 28.46 |

| IN | 2.16 | 0.37 | 0.35 | 36.20 | 0.33 | 0.08 | 5.44 | 0.68 | 2.73 | 3.90 | 47.76 | 63.80 |

| IT | 0.96 | 1.88 | 1.95 | 0.14 | 23.71 | 1.04 | 0.01 | 1.26 | 0.16 | 0.89 | 67.98 | 76.29 |

| JP | 1.84 | 3.31 | 2.41 | 0.16 | 5.59 | 69.87 | 0.06 | 2.48 | 0.72 | 1.15 | 12.41 | 30.13 |

| ZA | 1.63 | 0.11 | 0.09 | 11.89 | 0.04 | 0.04 | 65.67 | 0.42 | 7.13 | 6.96 | 6.03 | 34.33 |

| CH | 6.16 | 8.74 | 9.54 | 1.54 | 7.16 | 2.63 | 0.33 | 20.06 | 0.38 | 4.88 | 38.59 | 79.94 |

| UK | 0.15 | 0.45 | 0.13 | 2.85 | 0.52 | 0.48 | 4.43 | 0.06 | 21.22 | 2.26 | 67.45 | 78.78 |

| US | 4.64 | 1.53 | 1.36 | 3.52 | 1.90 | 0.47 | 2.90 | 1.71 | 1.83 | 7.59 | 72.55 | 92.41 |

| OU | 0.01 | 0.01 | 0.01 | 0.01 | 0.03 | 0.08 | 0.01 | 0.00 | 0.00 | 0.00 | 99.85 | 0.15 |

| To | 22.33 | 26.00 | 25.49 | 26.02 | 29.49 | 10.10 | 14.78 | 20.37 | 14.31 | 36.80 | 406.88 | 57.51 |

| Net | −50.91 | −49.03 | −2.97 | −37.78 | −46.80 | −20.03 | −19.55 | −59.57 | −64.47 | −55.61 | 406.73 | |

| Upper Regime | ||||||||||||

| CA | FR | DE | IN | IT | JP | ZA | CH | UK | US | OIL_UNC | From | |

| CA | 2.20 | 0.61 | 0.43 | 0.40 | 0.51 | 0.19 | 0.13 | 0.55 | 0.13 | 1.05 | 93.80 | 97.80 |

| FR | 0.48 | 3.58 | 0.55 | 0.07 | 0.89 | 0.31 | 0.01 | 0.62 | 0.10 | 0.45 | 92.96 | 96.42 |

| DE | 0.37 | 0.61 | 18.72 | 0.20 | 0.73 | 0.18 | 0.02 | 0.69 | 0.04 | 0.28 | 78.16 | 81.28 |

| IN | 0.37 | 0.09 | 0.07 | 7.21 | 0.12 | 0.02 | 0.99 | 0.14 | 0.42 | 0.69 | 89.88 | 92.79 |

| IT | 0.25 | 0.51 | 0.47 | 0.11 | 6.04 | 0.32 | 0.00 | 0.32 | 0.03 | 0.26 | 91.70 | 93.96 |

| JP | 0.16 | 0.33 | 0.36 | 0.04 | 0.49 | 6.40 | 0.00 | 0.25 | 0.05 | 0.11 | 91.80 | 93.60 |

| ZA | 0.57 | 0.09 | 0.04 | 4.87 | 0.02 | 0.03 | 27.08 | 0.20 | 2.88 | 2.70 | 61.52 | 72.92 |

| CH | 0.31 | 0.44 | 0.44 | 0.07 | 0.38 | 0.15 | 0.02 | 0.99 | 0.03 | 0.29 | 96.88 | 99.01 |

| UK | 0.01 | 0.09 | 0.04 | 0.60 | 0.08 | 0.08 | 0.82 | 0.01 | 4.53 | 0.54 | 93.20 | 95.47 |

| US | 2.03 | 0.76 | 0.62 | 1.59 | 0.98 | 0.20 | 1.34 | 0.79 | 0.79 | 3.40 | 87.51 | 96.60 |

| OU | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 100.00 | 0.00 |

| To | 4.55 | 3.53 | 3.01 | 7.95 | 4.21 | 1.46 | 3.33 | 3.55 | 4.47 | 6.36 | 877.42 | 83.62 |

| Net | −93.25 | −92.89 | −78.27 | −84.83 | −89.75 | −92.14 | −69.58 | −95.46 | −91.00 | −90.24 | 877.42 | |

| Regime 1 | ||||||||||||

| CA | FR | DE | IN | IT | JP | ZA | CH | UK | US | OIL_UNC | From | |

| CA | 83.24 | 0.21 | 0.04 | 0.07 | 0.21 | 0.01 | 0.64 | 1.47 | 0.18 | 8.58 | 5.33 | 16.76 |

| FR | 1.61 | 58.10 | 0.13 | 0.05 | 0.90 | 0.02 | 0.12 | 9.52 | 0.22 | 0.57 | 28.76 | 41.90 |

| DE | 1.16 | 0.00 | 55.40 | 0.09 | 2.67 | 0.18 | 0.54 | 0.59 | 0.62 | 1.99 | 36.77 | 44.60 |

| IN | 0.05 | 0.03 | 0.80 | 35.89 | 0.04 | 0.01 | 0.00 | 0.65 | 0.22 | 0.18 | 62.13 | 64.11 |

| IT | 1.19 | 0.00 | 0.13 | 0.01 | 88.78 | 2.07 | 0.67 | 2.13 | 0.01 | 0.22 | 4.78 | 11.22 |

| JP | 0.20 | 0.07 | 0.10 | 0.71 | 0.91 | 50.52 | 0.18 | 1.26 | 0.89 | 4.86 | 40.30 | 49.48 |

| ZA | 0.14 | 0.06 | 0.03 | 0.17 | 0.02 | 0.08 | 31.56 | 0.00 | 0.24 | 0.14 | 67.56 | 68.44 |

| CH | 1.80 | 0.03 | 0.02 | 0.10 | 0.12 | 0.00 | 0.20 | 94.26 | 0.07 | 0.82 | 2.58 | 5.74 |

| UK | 7.07 | 0.02 | 0.38 | 4.45 | 0.49 | 0.26 | 0.24 | 0.16 | 55.44 | 10.80 | 20.68 | 44.56 |

| US | 5.68 | 0.02 | 0.01 | 0.28 | 0.02 | 0.03 | 0.03 | 2.85 | 1.02 | 37.80 | 52.25 | 62.20 |

| OU | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 99.99 | 0.01 |

| To | 18.90 | 0.45 | 1.65 | 5.93 | 5.40 | 2.67 | 2.62 | 18.62 | 3.47 | 28.18 | 321.13 | 37.18 |

| Net | 2.15 | −41.45 | −42.95 | −58.18 | −5.82 | −46.81 | −65.82 | 12.88 | −41.09 | −34.02 | 321.12 | |

| Regime 2 | ||||||||||||

| CA | FR | DE | IN | IT | JP | ZA | CH | UK | US | OIL_UNC | From | |

| CA | 18.84 | 0.03 | 0.03 | 0.13 | 0.01 | 0.06 | 1.62 | 2.49 | 0.01 | 0.16 | 76.63 | 81.16 |

| FR | 0.92 | 9.37 | 0.05 | 0.01 | 0.67 | 0.21 | 0.97 | 0.17 | 0.00 | 0.48 | 87.16 | 90.63 |

| DE | 1.14 | 0.04 | 23.32 | 0.52 | 0.01 | 0.55 | 3.17 | 9.05 | 1.48 | 3.28 | 57.43 | 76.68 |

| IN | 5.83 | 0.64 | 0.06 | 49.80 | 0.14 | 0.52 | 7.67 | 0.17 | 3.49 | 14.80 | 16.89 | 50.20 |

| IT | 28.46 | 4.85 | 2.62 | 0.24 | 26.22 | 10.02 | 0.62 | 0.31 | 1.62 | 10.91 | 14.13 | 73.78 |

| JP | 3.87 | 0.56 | 4.10 | 0.38 | 0.35 | 23.42 | 1.30 | 4.52 | 0.21 | 31.14 | 30.15 | 76.58 |

| ZA | 0.34 | 0.40 | 0.00 | 0.56 | 0.02 | 0.23 | 13.32 | 0.76 | 1.62 | 2.23 | 80.51 | 86.68 |

| CH | 2.03 | 0.27 | 0.07 | 0.03 | 0.06 | 0.02 | 6.65 | 63.14 | 0.31 | 2.50 | 24.91 | 36.86 |

| UK | 19.76 | 2.31 | 0.02 | 0.31 | 0.44 | 0.05 | 4.82 | 6.48 | 34.87 | 6.61 | 24.34 | 65.13 |

| US | 6.10 | 0.03 | 0.01 | 0.11 | 0.01 | 0.52 | 2.11 | 4.74 | 1.10 | 23.65 | 61.62 | 76.35 |

| OU | 0.04 | 0.01 | 0.00 | 0.05 | 0.02 | 0.02 | 0.02 | 0.01 | 0.11 | 0.06 | 99.66 | 0.34 |

| To | 68.50 | 9.13 | 6.97 | 2.35 | 1.72 | 12.19 | 28.94 | 28.69 | 9.95 | 72.18 | 473.76 | 64.94 |

| Net | −12.66 | −81.50 | −69.71 | −47.85 | −72.06 | −64.39 | −57.74 | −8.17 | −55.18 | −4.17 | 473.42 | |

| The 0.10−th Quantile of Oil Uncertainty | ||||||||||||

| CA | FR | DE | IN | IT | JP | ZA | CH | UK | US | OIL_UNC | From | |

| CA | 43.17 | 8.03 | 2.70 | 4.29 | 3.82 | 1.88 | 1.59 | 11.86 | 0.42 | 22.18 | 0.05 | 56.83 |

| FR | 9.78 | 53.01 | 3.97 | 0.64 | 7.10 | 3.01 | 0.11 | 15.01 | 0.91 | 6.44 | 0.01 | 46.99 |

| DE | 4.42 | 5.14 | 71.77 | 0.45 | 3.66 | 1.12 | 0.07 | 9.80 | 0.13 | 3.41 | 0.02 | 28.23 |

| IN | 5.74 | 0.86 | 0.77 | 61.60 | 0.63 | 0.29 | 10.11 | 2.13 | 5.22 | 12.57 | 0.09 | 38.40 |

| IT | 5.44 | 8.40 | 3.22 | 0.44 | 64.02 | 3.63 | 0.04 | 8.80 | 0.54 | 5.43 | 0.03 | 35.98 |

| JP | 3.79 | 4.60 | 1.46 | 0.10 | 4.53 | 76.43 | 0.05 | 5.91 | 0.82 | 2.30 | 0.01 | 23.57 |

| ZA | 2.04 | 0.11 | 0.06 | 10.48 | 0.04 | 0.03 | 64.76 | 0.55 | 8.83 | 13.03 | 0.08 | 35.24 |

| CH | 12.64 | 12.41 | 5.91 | 1.78 | 6.19 | 3.21 | 0.50 | 47.34 | 0.16 | 9.79 | 0.05 | 52.66 |

| UK | 2.98 | 1.38 | 0.58 | 6.44 | 0.77 | 0.80 | 9.97 | 1.25 | 63.92 | 11.88 | 0.04 | 36.08 |

| US | 20.44 | 5.10 | 2.13 | 8.32 | 3.79 | 1.02 | 7.48 | 9.15 | 5.50 | 37.03 | 0.04 | 62.97 |

| OU | 0.05 | 0.01 | 0.00 | 0.00 | 0.05 | 0.00 | 0.01 | 0.10 | 0.05 | 0.01 | 99.73 | 0.27 |

| To | 67.32 | 46.04 | 20.80 | 32.95 | 30.58 | 15.00 | 29.93 | 64.54 | 22.59 | 87.04 | 0.42 | 37.93 |

| Net | 10.49 | −0.95 | −7.43 | −5.45 | −5.39 | −8.57 | −5.30 | 11.88 | −13.50 | 24.07 | 0.15 | |

| The 0.90−th Quantile of Oil Uncertainty | ||||||||||||

| CA | FR | DE | IN | IT | JP | ZA | CH | UK | US | OIL_UNC | From | |

| CA | 19.21 | 11.79 | 6.23 | 3.22 | 9.45 | 8.73 | 4.50 | 12.71 | 5.31 | 15.22 | 3.63 | 80.79 |

| FR5 | 11.35 | 19.54 | 6.43 | 5.14 | 10.31 | 9.16 | 6.37 | 12.89 | 7.57 | 10.16 | 1.07 | 80.46 |

| DE | 5.04 | 5.03 | 11.88 | 4.76 | 4.05 | 4.67 | 4.31 | 5.82 | 3.76 | 4.55 | 46.12 | 88.12 |

| IN | 5.39 | 6.59 | 5.57 | 21.46 | 6.29 | 7.80 | 12.03 | 6.38 | 10.03 | 3.93 | 14.52 | 78.54 |

| IT | 9.40 | 10.21 | 6.13 | 5.13 | 18.95 | 8.69 | 5.98 | 10.30 | 6.72 | 9.06 | 9.44 | 81.05 |

| JP | 9.93 | 10.31 | 6.02 | 6.41 | 9.82 | 21.70 | 7.41 | 10.61 | 7.89 | 8.99 | 0.90 | 78.30 |

| ZA | 7.73 | 8.76 | 5.81 | 11.54 | 7.36 | 8.34 | 20.16 | 8.62 | 11.05 | 5.38 | 5.26 | 79.84 |

| CH | 12.65 | 12.10 | 7.80 | 4.09 | 9.92 | 9.18 | 5.34 | 19.76 | 6.47 | 11.61 | 1.08 | 80.24 |

| UK | 6.84 | 9.25 | 4.74 | 11.06 | 8.40 | 8.80 | 12.46 | 8.07 | 24.74 | 3.11 | 2.51 | 75.26 |

| US | 16.22 | 11.41 | 6.65 | 2.64 | 9.98 | 8.82 | 3.01 | 13.25 | 3.88 | 19.57 | 4.58 | 80.43 |

| OU | 3.79 | 3.58 | 6.52 | 4.77 | 2.68 | 3.75 | 4.02 | 4.14 | 3.14 | 3.41 | 60.21 | 39.79 |

| To | 88.34 | 89.05 | 61.90 | 58.76 | 78.26 | 77.93 | 65.43 | 92.78 | 65.83 | 75.42 | 89.12 | 76.62 |

| Net | 7.55 | 8.59 | −26.22 | −19.77 | −2.79 | −0.37 | −14.41 | 12.54 | −9.43 | −5.01 | 49.33 | |

References

- Bernanke, B.S. Irreversibility, uncertainty, and cyclical investment. Q. J. Econ. 1983, 98, 85–106. [Google Scholar] [CrossRef] [Green Version]

- Pindyck, R. Irreversibility, uncertainty, and investment. J. Econ. Lit. 1991, 29, 1110–1148. [Google Scholar]

- Swaray, R.; Salisu, A.A. A firm-level analysis of the upstream-downstream dichotomy in the oil-stock nexus. Glob. Financ. J. 2018, 37, 199–218. [Google Scholar] [CrossRef]

- Demirer, R.; Jategaonkar, S.P.; Khalifa, A.A.A. Oil price risk exposure and the cross-section of stock returns: The case of net exporting countries. Energ. Econ. 2015, 49, 140–142. [Google Scholar] [CrossRef]

- Christoffersen, P.; Pan, X.N. Oil volatility risk and expected stock returns. J. Bank. Financ. 2018, 95, 5–26. [Google Scholar] [CrossRef] [Green Version]

- Sadorsky, P. Oil price shocks and stock market activity. Energ. Econ. 1999, 21, 449–469. [Google Scholar] [CrossRef]

- Masih, R.; Peters, S.; de Mello, L. Oil price volatility and stock price fluctuations in an emerging market: Evidence from South Korea. Energ. Econ. 2011, 33, 975–986. [Google Scholar] [CrossRef]

- Alsalman, Z. Oil price uncertainty and the U.S. stock market analysis based on a GARCH in mean VAR model. Energ. Econ. 2016, 59, 251–260. [Google Scholar] [CrossRef]

- Diaz, E.M.; Molero, J.C.; de Gracia, F.P. Oil price volatility and stock returns in the G7 economies. Energ. Econ. 2016, 54, 417–430. [Google Scholar] [CrossRef] [Green Version]

- Rahman, S. Oil price volatility and the US stock market. Empir. Econ. 2021, 61, 1461–1489. [Google Scholar] [CrossRef]

- Jiranyakul, K. Does oil price uncertainty transmit to the Thai stock market? J. Econ. Financ. Stud. 2014, 2, 16–25. [Google Scholar] [CrossRef]

- Aye, G.C. Does oil price uncertainty matter for stock returns in South Africa? Investig. Manag. Financ. Innov. 2015, 12, 179–188. [Google Scholar]

- Bass, A. Does oil prices uncertainty affect stock returns in Russia: A bivariate GARCH-in-mean approach. Int. J. Energ. Econ. Policy 2017, 7, 224–230. [Google Scholar]

- Benavides, D.R.; García, M.A.M.; Reyes, L.F.H. Uncertainty of the international oil price and stock returns in Mexico through an SVAR-MGARCH. Contad. Adm. 2019, 64, 1–16. [Google Scholar]

- Basher, S.A.; Sadorsky, P. Oil price risk and emerging stock markets. Glob. Financ. J. 2006, 17, 224–251. [Google Scholar] [CrossRef]

- Salisu, A.A.; Gupta, R. Oil Price Uncertainty Shocks and Global Equity Markets: Evidence from a GVAR Model. J. Risk Financ. Manag. 2022, 15, 355. [Google Scholar] [CrossRef]

- Campbell, J.Y. Viewpoint: Estimating the equity premium. Can. J. Econ. 2008, 41, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Salisu, A.A.; Pierdzioch, C.; Gupta, R. Geopolitical risk and forecastability of tail risk in the oil market: Evidence from over a century of monthly data? Energy 2021, 235, 121333. [Google Scholar] [CrossRef]

- Rapach, D.E.; Zhou, G. Forecasting stock returns. In Handbook of Economic Forecasting, 2nd ed.; (Part A); Elliott, G., Timmermann, A., Eds.; Elsevier: Amsterdam, The Netherlands, 2013; pp. 328–383. [Google Scholar]

- Stock, J.H.; Watson, M.W. Forecasting output and inflation: The tole of asset prices. J. Econ. Lit. 2003, 41, 788–829. [Google Scholar] [CrossRef]

- Rapach, D.E.; Strauss, J.K.; Zhou, G. International Stock Return Predictability: What is the Role of the United States? J. Financ. 2013, 68, 1633–1662. [Google Scholar] [CrossRef]

- Aye, G.C.; Balcilar, M.; Gupta, R. International stock return predictability: Is the role of US time-varying? Empirica 2017, 44, 121–146. [Google Scholar] [CrossRef] [Green Version]

- Gupta, R.; Majumdar, A.; Wohar, M.E. The Role of current account balance in forecasting the US equity premium: Evidence from a quantile predictive regression approach. Open Econ. Rev. 2017, 28, 47–59. [Google Scholar] [CrossRef] [Green Version]

- Gupta, R.; Huber, F.; Piribauer, P. Predicting international equity returns: Evidence from time-varying parameter vector autoregressive models. Int. Rev. Financ. Anal. 2020, 68, 101456. [Google Scholar] [CrossRef] [Green Version]

- Huber, F.; Krisztin, T.; Piribauer, P. Forecasting equity indices using large Bayesian VARs. B. Econ. Res. 2017, 69, 288–308. [Google Scholar] [CrossRef]

- Jordan, S.J.; Vivian, A.J.; Wohar, M.E. Forecasting market returns: Bagging or combining? Int. J. Forecast. 2017, 33, 102–120. [Google Scholar] [CrossRef] [Green Version]

- Jordan, S.J.; Vivian, A.J.; Wohar, M.E. Stock returns forecasting with metals: Sentiment vs. fundamentals. Eur. J. Financ. 2018, 24, 458–477. [Google Scholar] [CrossRef] [Green Version]

- Christou, C.; Gupta, R.; Jawadi, F. Does Inequality Help in Forecasting Equity Premium in a Panel of G7 Countries? N. Am. J. Econ. Financ. 2021, 57, 101456. [Google Scholar] [CrossRef]

- Salisu, A.A.; Gupta, R. Commodity prices and forecastability of international stock returns over a century: Sentiments versus fundamentals with focus on South Africa. Emerg. Mark. Financ. Trade 2022, 58, 2620–2636. [Google Scholar] [CrossRef]

- Rapach, D.E.; Zhou, G. Asset pricing: Time-series predictability. Oxf. Res. Encycl. Econ. Financ. 2022; in press. [Google Scholar]

- Narayan, P.K.; Gupta, R. Has oil price predicted stock returns for over a century? Energ. Econ. 2015, 48, 18–23. [Google Scholar] [CrossRef] [Green Version]

- Gupta, R.; Wohar, M.E. Forecasting oil and stock returns with a Qual VAR using over 150 years of data. Energ. Econ. 2017, 62, 181–186. [Google Scholar] [CrossRef] [Green Version]

- Degiannakis, S.A.; Filis, G.; Arora, V. Oil prices and stock markets: A review of the theory and empirical evidence. Energ. J. 2018, 39, 85–130. [Google Scholar] [CrossRef] [Green Version]

- Smyth, R.; Narayan, P.K. What do we know about oil prices and stock returns? Int. Rev. Financ. Anal. 2018, 57, 148–156. [Google Scholar] [CrossRef]

- Guidolin, M.; Hyde, S.; McMillan, D.; Ono, S. Non-linear predictability in stock and bond returns: When and where is it exploitable? Int. J. Forecast. 2009, 25, 373–399. [Google Scholar] [CrossRef] [Green Version]

- Gupta, R.; Majumdar, A. Incorporating Economic Policy Uncertainty in US Equity Premium Models: A Nonlinear Predictability Analysis. Financ. Res. Lett. 2016, 18, 291–296. [Google Scholar]

- Demirer, R.; Pierdzioch, C.; Zhang, H. On the Short-Term Predictability of Stock Returns: A Quantile Boosting Approach. Financ. Res. Lett. 2017, 22, 35–41. [Google Scholar] [CrossRef]

- Gupta, R.; Mwamba, J.W.M.; Wohar, M.E. The role of partisan conflict in forecasting the US equity premium: A nonparametric approach. Finance Res. Lett. 2018, 25, 131–136. [Google Scholar] [CrossRef] [Green Version]

- Gupta, R.; Pierdzioch, C.; Vivian, A.J.; Wohar, M.E. The predictive value of inequality measures for stock returns: An analysis of long-span UK data using quantile random forests. Financ. Res. Lett. 2019, 29, 315–322. [Google Scholar] [CrossRef] [Green Version]

- Koenker, R.; Bassett, G. Regression quantiles. Econometrica 1978, 46, 33–50. [Google Scholar] [CrossRef]

- Meligkotsidou, L.; Panopoulou, E.; Vrontos, I.D.; Vrontos, S.D. A Quantile Regression Approach to Equity Premium Prediction. J. Forecast. 2014, 33, 558–576. [Google Scholar] [CrossRef] [Green Version]

- Gebka, B.; Wohar, M.E. Stock return distribution and predictability: Evidence from over a century of daily data on the DJIA index. Int. Rev. Econ. Financ. 2019, 60, 1–25. [Google Scholar] [CrossRef] [Green Version]

- Das, S.; Demirer, R.; Gupta, R.; Mangisa, S. The effect of global crises on stock market correlations: Evidence from scalar regressions via functional data analysis. Struct. Chang. Econ. Dyn. 2019, 50, 132–147. [Google Scholar] [CrossRef]

- Elder, J.; Serletis, A. Oil Price Uncertainty. J. Money Credit. Bank 2010, 42, 1137–1159. [Google Scholar] [CrossRef]

- Bai, J.; Perron, P. Computation and analysis of multiple structural change models. J. Appl. Econom. 2003, 18, 1–22. [Google Scholar] [CrossRef] [Green Version]

- Brock, W.A.; Scheinkman, J.A.; Dechert, W.D.; LeBaron, B. A test for independence based on the correlation dimension. Econom. Rev. 1996, 15, 197–235. [Google Scholar] [CrossRef]

- McCracken, M.W. Asymptotics for out of sample tests of Granger causality. J. Econom. 2007, 140, 719–752. [Google Scholar] [CrossRef]

- Pierdzioch, C.; Risse, M.; Rohloff, S. The international business cycle and gold-price fluctuations. Q. Rev. Econ. Financ. 2014, 54, 292–305. [Google Scholar] [CrossRef]

- Pierdzioch, C.; Risse, M.; Rohloff, S. Fluctuations of the real exchange rate, real interest rates, and the dynamics of the price of gold in a small open economy. Empir. Econ. 2016, 51, 1481–1499. [Google Scholar] [CrossRef] [Green Version]

- Gupta, R.; Pierdzioch, C.; Do Economic Conditions of U.S. States Predict the Realized Volatility of Oil-Price Returns? A Quantile Machine-Learning Approach. Financial Innovation, Forthcoming. Available online: https://ideas.repec.org/p/pre/wpaper/202216.html (accessed on 18 August 2022).

- Ren, X.; Duan, K.; Tao, L.; Shi, Y.; Yan, C. Carbon prices forecasting in quantiles. Energ. Econ. 2022, 108, 105862. [Google Scholar] [CrossRef]

- Balcilar, M.; Ozdemir, Z.A.; Ozdemir, H.; Wohar, M.E. Fed’s unconventional monetary policy and risk spillover in the US financial markets. Q. Rev. Econ. Financ. 2020, 78, 42–52. [Google Scholar] [CrossRef]

- Balcilar, M.; Roubaud, D.; Usman, O.; Wohar, M.E. Moving out of the linear rut: A period-specific and regime-dependent exchange rate and oil price pass-through in the BRICS countries. Energ. Econ. 2021, 98, 105249. [Google Scholar] [CrossRef]

- Balcilar, M.; Roubaud, D.; Usman, O.; Wohar, M.E. Testing the asymmetric effects of exchange rate pass-through in BRICS countries: Does the state of the economy matter? World Econ. 2021, 44, 188–233. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Better to give than receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 28, 57–66. [Google Scholar] [CrossRef] [Green Version]

- Shahzad, S.J.H.; Bouri, E.; Kang, S.H.; Saeed, T. Regime specific spillover across cryptocurrencies and the role of COVID-19. Financ. Innov. 2021, 7, 5. [Google Scholar] [CrossRef] [PubMed]

- Balcilar, M.; Ozdemir, Z.A.; Ozdemir, H.; Aygun, G.; Wohar, M.E. Effectiveness of monetary policy under the high and low economic uncertainty states: Evidence from the major Asian economies. Empir. Econ. 2022, 63, 1741–1769. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Cunado, J.; Gupta, R.; Wohar, M.E. Volatility spillovers across global asset classes: Evidence from time and frequency domains. Q. Rev. Econ. Financ. 2018, 70, 194–202. [Google Scholar] [CrossRef]

- Demirer, R.; Gupta, R.; Suleman, M.T.; Wohar, M.E. Time-varying rare disaster risks, oil returns and volatility. Energ. Econ. 2018, 75, 239–248. [Google Scholar] [CrossRef] [Green Version]

- Sohag, K.; Hammoudeh, S.; Elsayed, A.H.; Mariev, O.; Safonova, Y. Do geopolitical events transmit opportunity or threat to green markets? Decomposed measures of geopolitical risks. Energ. Econ. 2022, 111, 106068. [Google Scholar] [CrossRef]

| Canada (CA) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 0.9980 ** | 1.0150 | 1.0057 | 1.0197 | 1.0074 | 0.9997 | 1.0169 | 1.0160 | 1.0164 | 1.144 |

| 3 | 1.0017 | 0.9998 | 1.0000 | 0.9846 *** | 1.0156 | 0.9980 ** | 0.9917 *** | 1.0285 | 0.9940 *** | 1.0000 |

| 6 | 0.9980 ** | 0.9621 *** | 0.9626 *** | 1.0012 | 0.9983 ** | 1.0022 | 1.0013 | 0.9873 *** | 0.9945 *** | 0.9265 *** |

| 9 | 1.0641 | 0.9761 *** | 0.9835 *** | 0.9844 *** | 1.0578 | 1.1103 | 1.0329 | 1.0675 | 1.2132 | 1.1411 |

| 12 | 1.1553 | 0.9330 *** | 0.9828 *** | 1.1089 | 1.0737 | 1.1749 | 1.1123 | 1.2327 | 1.1309 | 1.2312 |

| 18 | 1.1320 | 0.9922 *** | 0.9984 ** | 1.0484 | 1.0900 | 1.1163 | 1.1250 | 1.2039 | 1.2192 | 1.2263 |

| 24 | 1.0694 | 1.0093 | 1.0034 | 1.0020 | 1.2571 | 1.1061 | 1.0691 | 1.0192 | 1.0586 | 1.0462 |

| France (FR) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0251 | 1.1607 | 1.0457 | 1.0056 | 1.0364 | 1.0031 | 1.0711 | 1.2095 | 1.1462 | 1.0772 |

| 3 | 1.0209 | 1.1080 | 1.0099 | 1.0365 | 1.0019 | 1.0098 | 1.0517 | 1.5301 | 1.3449 | 1.0926 |

| 6 | 1.0431 | 1.2209 | 1.2231 | 1.1026 | 1.0036 | 1.1815 | 1.4462 | 1.2086 | 1.4417 | 1.0852 |

| 9 | 1.4294 | 0.8060 *** | 0.9906 *** | 1.1436 | 1.6721 | 1.7185 | 1.6809 | 1.6962 | 1.5166 | 1.2891 |

| 12 | 1.4385 | 0.8585 *** | 0.9100 *** | 1.5124 | 1.8152 | 1.5974 | 1.5176 | 1.4567 | 1.3110 | 1.2027 |

| 18 | 1.3528 | 0.9371 *** | 1.1383 | 1.3144 | 1.4495 | 1.3513 | 1.4295 | 1.0844 | 1.2531 | 1.0528 |

| 24 | 0.9941 *** | 2.0310 | 1.6327 | 1.3403 | 1.0672 | 0.9785 *** | 0.8190 *** | 0.8782 *** | 0.8927 *** | 0.9258 *** |

| Germany (DE) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.4176 | 1.1750 | 0.8222 *** | 0.9614 *** | 0.9707 *** | 1.2425 | 1.0300 | 2.4939 | 1.8366 | 1.8639 |

| 3 | 1.6517 | 1.1434 | 1.1125 | 1.0936 | 1.0243 | 2.5849 | 2.6628 | 1.7991 | 2.1421 | 1.3476 |

| 6 | 1.3142 | 3.5451 | 2.5854 | 2.2575 | 0.8455 *** | 1.6159 | 2.1308 | 3.3076 | 1.4995 | 1.2194 |

| 9 | 0.9971 ** | 1.2140 | 2.6180 | 2.6565 | 4.9158 | 1.1643 | 2.8539 | 1.6979 | 4.3362 | 1.2318 |

| 12 | 1.1267 | 2.1916 | 1.8270 | 3.4710 | 2.0924 | 1.5209 | 0.9993 * | 0.9945 *** | 2.3191 | 1.2422 |

| 18 | 2.5850 | 1.5524 | 1.8803 | 2.0956 | 2.5410 | 1.5859 | 1.3141 | 1.1005 | 0.8732 *** | 0.6903 *** |

| 24 | 1.6232 | 1.7894 | 1.6333 | 4.2118 | 2.6620 | 1.0992 | 0.9854 *** | 1.8293 | 1.1091 | 0.8259 *** |

| India (IN) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0857 | 1.7240 | 1.2149 | 1.1133 | 1.0344 | 1.0043 | 1.0015 | 1.0197 | 1.0007 | 1.1186 |

| 3 | 1.1611 | 1.0341 | 1.2258 | 1.1876 | 1.1786 | 1.0450 | 1.0725 | 1.0465 | 1.1696 | 0.9137 *** |

| 6 | 1.1925 | 1.1427 | 1.2356 | 1.0328 | 1.2058 | 1.0172 | 1.1481 | 1.2241 | 1.0290 | 0.9332 *** |

| 9 | 1.1550 | 1.0927 | 1.1351 | 1.2211 | 1.3926 | 1.1182 | 1.2946 | 1.1484 | 0.9901 *** | 1.0171 |

| 12 | 1.2437 | 1.1970 | 1.2089 | 1.3610 | 1.4850 | 1.5520 | 1.2222 | 1.0406 | 0.9842 *** | 0.9999 |

| 18 | 1.0908 | 1.0922 | 1.2128 | 1.0453 | 1.1845 | 1.2281 | 1.0832 | 0.9610 *** | 0.9610 *** | 0.9750 *** |

| 24 | 0.9516 *** | 0.8987 *** | 0.9999 | 0.9831 *** | 0.8714 *** | 0.9564 *** | 0.8902 *** | 0.8005 *** | 0.9850 *** | 1.0321 |

| Italy (IT) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0007 | 1.1022 | 0.9960 *** | 1.0354 | 1.0473 | 1.0337 | 1.0178 | 0.9939 *** | 1.0905 | 1.1920 |

| 3 | 1.0548 | 0.9328 *** | 0.9686 *** | 0.9758 *** | 0.9883 *** | 1.0203 | 1.1135 | 1.2332 | 1.1777 | 1.0167 |

| 6 | 1.0347 | 0.9772 *** | 1.0108 | 0.9904 *** | 0.9858 *** | 1.0188 | 1.0202 | 1.0450 | 1.3207 | 1.9168 |

| 9 | 1.1396 | 0.9962 *** | 0.9226 *** | 0.9622 *** | 0.9786 *** | 1.0112 | 1.0326 | 1.4797 | 3.0196 | 1.4055 |

| 12 | 1.1953 | 0.8882 *** | 0.9731 *** | 0.9525 *** | 0.9758 *** | 1.0100 | 1.0271 | 3.0478 | 1.3284 | 1.4164 |

| 18 | 1.1337 | 0.9389 *** | 0.9794 *** | 0.9742 *** | 0.9943 *** | 1.0093 | 1.0906 | 1.5868 | 1.6185 | 1.3491 |

| 24 | 1.0005 | 1.1307 | 1.0861 | 1.0323 | 1.0197 | 1.0058 | 0.9994 * | 1.1876 | 1.1627 | 1.2209 |

| Japan (JP) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0048 | 1.0090 | 1.0079 | 1.0331 | 0.9991 * | 1.0072 | 1.0055 | 1.0336 | 1.0364 | 1.2751 |

| 3 | 1.0079 | 1.0299 | 1.0359 | 1.0108 | 1.0215 | 0.9988 * | 1.0031 | 1.0409 | 1.1107 | 1.1536 |

| 6 | 1.0153 | 1.1587 | 1.0521 | 1.0689 | 1.1444 | 0.9877 *** | 1.0016 | 1.0082 | 1.0010 | 0.9019 *** |

| 9 | 1.1694 | 1.0982 | 1.1854 | 1.2222 | 1.3247 | 1.1140 | 1.0525 | 0.9935 *** | 1.0427 | 0.9210 *** |

| 12 | 1.1983 | 0.9589 *** | 1.0424 | 1.1766 | 1.3171 | 1.2843 | 1.1694 | 1.1323 | 1.0128 | 0.8732 *** |

| 18 | 1.2738 | 1.0021 | 1.1267 | 1.1001 | 1.0518 | 1.2595 | 1.2878 | 1.2550 | 1.3483 | 1.1020 |

| 24 | 0.9408 *** | 1.0542 | 0.9402 *** | 0.9130 *** | 0.9208 *** | 0.9677 *** | 0.9281 *** | 0.9435 *** | 0.9824 *** | 0.9910 *** |

| South Africa (ZA) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0079 | 0.9631 *** | 0.9473 *** | 0.9842 *** | 0.9966 ** | 1.0071 | 0.9962 *** | 0.9973 ** | 0.9929 *** | 1.0229 |

| 3 | 1.0548 | 0.8283 *** | 0.9522 *** | 0.9965 *** | 1.0026 | 1.1008 | 1.2520 | 1.2392 | 1.1127 | 1.0894 |

| 6 | 1.1171 | 0.9239 *** | 0.9334 *** | 0.9563 *** | 1.0866 | 1.1281 | 1.1792 | 1.1782 | 1.2355 | 1.2009 |

| 9 | 1.1175 | 0.8061 *** | 0.8771 *** | 0.9612 *** | 1.0510 | 1.1090 | 1.1599 | 1.2825 | 1.3334 | 1.2622 |

| 12 | 1.0696 | 0.9107 *** | 0.7970 *** | 0.9908 *** | 1.0138 | 1.1403 | 1.0709 | 1.1330 | 1.1370 | 1.0567 |

| 18 | 1.0141 | 0.9516 *** | 0.9334 *** | 0.9245 *** | 1.0573 | 1.1359 | 0.9949 *** | 0.9966 ** | 0.9986 ** | 0.9950 *** |

| 24 | 1.1456 | 1.2272 | 1.2561 | 1.3636 | 1.1097 | 1.0612 | 1.0578 | 1.0058 | 0.9954 *** | 0.9507 *** |

| Switzerland (CH) | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0204 | 0.9290 *** | 1.0315 | 1.0565 | 1.0209 | 1.0391 | 1.0068 | 0.9830 *** | 1.0074 | 1.0247 |

| 3 | 1.1437 | 0.4522 *** | 0.9962 *** | 0.9944 *** | 1.0236 | 1.0985 | 1.1754 | 1.2126 | 1.1953 | 1.1661 |

| 6 | 1.1165 | 0.6385 *** | 1.1369 | 1.0811 | 1.0535 | 1.0582 | 1.0373 | 1.0329 | 0.9838 *** | 0.7994 *** |

| 9 | 1.2423 | 0.8608 *** | 1.4216 | 1.3856 | 1.1707 | 1.0331 | 1.0175 | 1.1656 | 1.0339 | 1.0212 |

| 12 | 1.2583 | 0.9800 *** | 1.2718 | 1.2747 | 1.1303 | 1.1448 | 1.1905 | 1.3831 | 1.2275 | 1.0096 |

| 18 | 1.1429 | 1.0699 | 1.0520 | 1.0831 | 1.0031 | 1.0943 | 0.9883 *** | 1.1353 | 1.0788 | 1.3768 |

| 24 | 0.9730 *** | 1.0020 | 1.0351 | 0.9687 *** | 0.9831 *** | 0.9793 *** | 1.0097 | 0.9805 *** | 0.9869 *** | 0.9858 *** |

| UK | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 1.0023 | 1.0677 | 1.0541 | 1.0961 | 1.0016 | 1.0048 | 0.9998 | 0.9998 | 1.0236 | 1.0349 |

| 3 | 1.0013 | 1.0845 | 1.0334 | 1.0453 | 0.9901 *** | 0.9990 * | 1.0110 | 1.0461 | 1.0398 | 1.0969 |

| 6 | 0.9921 *** | 1.0180 | 1.0499 | 0.9992 * | 0.9764 *** | 0.9825 *** | 1.0146 | 1.0363 | 1.1124 | 1.2448 |

| 9 | 0.9988 * | 1.0064 | 0.9769 *** | 0.9417 *** | 0.9635 *** | 0.9891 *** | 1.0323 | 1.0542 | 1.1204 | 1.3297 |

| 12 | 1.0057 | 1.0008 | 0.9627 *** | 0.9707 *** | 0.9640 *** | 0.9785 *** | 1.0160 | 1.0703 | 1.1240 | 1.2243 |

| 18 | 0.9917 *** | 0.9910 *** | 1.0213 | 0.9817 *** | 0.9783 *** | 0.9989 * | 0.9917 *** | 0.9918 *** | 0.9985 ** | 1.0980 |

| 24 | 1.0394 | 1.3147 | 1.1081 | 1.0582 | 1.0345 | 1.0192 | 1.0107 | 1.0186 | 1.0579 | 1.0442 |

| US | ||||||||||

| Horizon | Linear | Quantile | ||||||||

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

| 1 | 0.9907 *** | 1.1334 | 1.1105 | 0.9950 *** | 1.0052 | 0.9661 *** | 0.9583 *** | 0.9518 *** | 0.9434 *** | 0.9894 *** |

| 3 | 0.9817 *** | 1.1144 | 1.1073 | 1.0307 | 0.9946 *** | 0.9811 *** | 0.9949 *** | 0.8965 *** | 0.8889 *** | 0.8665 *** |

| 6 | 0.9789 *** | 1.1636 | 1.1357 | 1.0287 | 1.0104 | 0.9926 *** | 0.9565 *** | 0.9049 *** | 0.9341 *** | 0.7939 *** |

| 9 | 1.0052 | 1.2372 | 1.1513 | 1.0293 | 1.0279 | 1.0864 | 1.1258 | 1.1438 | 1.2257 | 1.0315 |

| 12 | 1.0830 | 1.0107 | 1.0364 | 0.9209 *** | 1.5974 | 1.3401 | 1.0593 | 1.0440 | 1.0660 | 1.2161 |

| 18 | 1.1733 | 0.9291 *** | 0.9598 *** | 1.1178 | 1.3775 | 1.2569 | 1.1599 | 1.0849 | 1.1491 | 1.1675 |

| 24 | 1.4589 | 1.2233 | 1.3722 | 1.3257 | 1.2879 | 1.8856 | 1.3823 | 1.3940 | 1.3036 | 1.3293 |

| Lower Regime | ||||||||||||

| CA | FR | DE | IN | IT | JP | ZA | CH | UK | US | OIL_UNC | From | |

| CA | 14.55 | 3.86 | 2.93 | 2.88 | 3.07 | 1.18 | 0.8 | 3.68 | 0.44 | 7.31 | 59.29 | 85.45 |

| FR | 1.94 | 14.82 | 2.53 | 0.27 | 3.39 | 1.04 | 0.05 | 2.49 | 0.21 | 1.22 | 72.04 | 85.18 |

| DE | 0.91 | 1.51 | 44.01 | 0.15 | 1.64 | 0.98 | 0.02 | 1.69 | 0.14 | 0.75 | 48.2 | 55.99 |

| IN | 2.39 | 0.41 | 0.4 | 40.59 | 0.38 | 0.08 | 6.1 | 0.78 | 3.11 | 4.4 | 41.34 | 59.41 |

| IT | 0.71 | 1.37 | 1.41 | 0.11 | 17.34 | 0.77 | 0.01 | 0.92 | 0.12 | 0.65 | 76.58 | 82.66 |

| JP | 1.45 | 2.62 | 1.89 | 0.13 | 4.41 | 55.5 | 0.04 | 1.97 | 0.58 | 0.91 | 30.49 | 44.5 |

| ZA | 1.5 | 0.11 | 0.09 | 11.99 | 0.03 | 0.04 | 66.15 | 0.4 | 7.16 | 6.97 | 5.55 | 33.85 |

| CH | 9.36 | 13.39 | 14.63 | 2.41 | 11.08 | 4.02 | 0.5 | 31.03 | 0.6 | 7.51 | 5.46 | 68.97 |

| UK | 0.17 | 0.47 | 0.13 | 3.04 | 0.53 | 0.51 | 4.73 | 0.06 | 22.67 | 2.42 | 65.28 | 77.33 |

| US | 2.95 | 0.97 | 0.87 | 2.29 | 1.22 | 0.33 | 1.86 | 1.1 | 1.18 | 4.86 | 82.37 | 95.14 |

| OU | 0.02 | 0 | 0 | 0.01 | 0.02 | 0.08 | 0 | 0.01 | 0 | 0 | 99.86 | 0.14 |

| To | 21.41 | 24.72 | 24.88 | 23.27 | 25.78 | 9.03 | 14.13 | 13.1 | 13.54 | 32.14 | 486.62 | 62.60 |

| Net | −64.04 | −60.46 | −31.11 | −36.13 | −56.88 | −35.47 | −19.72 | −55.86 | −63.79 | −63 | 486.47 | |

| Upper Regime | ||||||||||||

| CA | FR | DE | IN | IT | JP | ZA | CH | UK | US | OIL_UNC | From | |

| CA | 1.85 | 0.51 | 0.36 | 0.35 | 0.44 | 0.16 | 0.12 | 0.45 | 0.11 | 0.87 | 94.79 | 98.15 |

| FR | 0.43 | 3.28 | 0.5 | 0.06 | 0.82 | 0.28 | 0 | 0.56 | 0.1 | 0.4 | 93.56 | 96.72 |

| DE | 0.31 | 0.5 | 15.4 | 0.17 | 0.61 | 0.15 | 0.02 | 0.57 | 0.04 | 0.23 | 82.01 | 84.6 |

| IN | 0.41 | 0.1 | 0.08 | 7.97 | 0.14 | 0.02 | 1.09 | 0.15 | 0.46 | 0.76 | 88.84 | 92.03 |

| IT | 0.24 | 0.48 | 0.48 | 0.11 | 5.59 | 0.31 | 0 | 0.31 | 0.02 | 0.24 | 92.22 | 94.41 |

| JP | 0.12 | 0.25 | 0.3 | 0.04 | 0.37 | 4.83 | 0 | 0.19 | 0.04 | 0.09 | 93.76 | 95.17 |

| ZA | 0.78 | 0.09 | 0.06 | 6.08 | 0.02 | 0.02 | 34.2 | 0.28 | 3.59 | 3.41 | 51.46 | 65.8 |

| CH | 0.26 | 0.38 | 0.37 | 0.06 | 0.32 | 0.13 | 0.01 | 0.82 | 0.02 | 0.24 | 97.37 | 99.18 |

| UK | 0.01 | 0.08 | 0.03 | 0.53 | 0.07 | 0.07 | 0.75 | 0.01 | 4.13 | 0.53 | 93.8 | 95.87 |

| US | 1.57 | 0.57 | 0.48 | 1.24 | 0.76 | 0.16 | 1.03 | 0.61 | 0.61 | 2.61 | 90.37 | 97.39 |

| OU | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 100 | 0 |

| To | 4.13 | 2.97 | 2.63 | 8.63 | 3.56 | 1.3 | 3.02 | 3.14 | 4.99 | 6.76 | 878.2 | 83.58 |

| Net | −94.02 | −93.74 | −81.97 | −83.4 | −90.86 | −93.87 | −62.78 | −96.05 | −90.88 | −90.63 | 878.2 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Balcilar, M.; Gupta, R.; Pierdzioch, C. Oil-Price Uncertainty and International Stock Returns: Dissecting Quantile-Based Predictability and Spillover Effects Using More than a Century of Data. Energies 2022, 15, 8436. https://doi.org/10.3390/en15228436

Balcilar M, Gupta R, Pierdzioch C. Oil-Price Uncertainty and International Stock Returns: Dissecting Quantile-Based Predictability and Spillover Effects Using More than a Century of Data. Energies. 2022; 15(22):8436. https://doi.org/10.3390/en15228436

Chicago/Turabian StyleBalcilar, Mehmet, Rangan Gupta, and Christian Pierdzioch. 2022. "Oil-Price Uncertainty and International Stock Returns: Dissecting Quantile-Based Predictability and Spillover Effects Using More than a Century of Data" Energies 15, no. 22: 8436. https://doi.org/10.3390/en15228436