(Not So) Stranded: The Case of Coal in Poland

Economics Department, Kozminski University, 03-301 Warsaw, Poland

*

Author to whom correspondence should be addressed.

†

PhD candidate.

Energies 2021, 14(24), 8476; https://doi.org/10.3390/en14248476

Submission received: 8 November 2021

/

Revised: 29 November 2021

/

Accepted: 9 December 2021

/

Published: 15 December 2021

(This article belongs to the Collection Feature Papers in Energy, Environment and Well-Being)

Abstract

:This paper provides an evaluation of the stranding risks of coal in Poland. Combining an industrial organization and financial analysis approach, we assess the current economic situation of companies operating within the coal industry and draft forecasts for the future. Based on the global economic outlook for coal, we claim that phasing-out coal will take at least two decades, due to the slow transformation of the energy sector and increasing energy demand. The financial evaluation of coal-dependent companies revealed sound financial conditions due to favorable trends in coal prices in international markets. Therefore, instead of prioritizing a rapid phasing-out of coal, we pledge to make more technological investments that would make burning coal less harmful for the planet and thus efficiently mitigate the negative effects of climate change.

1. Introduction

In the context of climate urgency, it is necessary to implement decarbonization policies all over the planet. In the aftermath of the Paris Agreement, policy responses to the negative effects of climate change have mainly been focused on efforts to curb CO2 emissions. Limiting the increase in global temperature to “well below 2, preferably to 1.5 degrees Celsius (1.5 °C), compared to pre-industrial levels” [1] will require a significant and rapid fossil fuel phase-out. However, the path toward a post-carbon future is hindered by challenges arising from a large variety of transition risks, which have the potential to seriously disrupt the global economy and induce profound societal changes. Among these risks, the issue of “stranded assets”—resources exposed to decreases in value—has recently loomed larger and remains highly relevant in the context of transforming the energy sector, which has historically been dependent on fossil resources.

Poland has become one of the champions of economic transition over the past few decades, and efficient decarbonization paths are linked to one of the most profound disruptions in the country’s history: the transformation of its energy sector, heavily dependent on coal, with this resource becoming a strong “stranded asset” candidate. Therefore, to meet transformation goals, a shrewd set of actions must be fulfilled to reconcile the goal of carbon neutrality and the protection of the environment, without compromising economic growth and its fruits, in the form of sustainable and inclusive development.

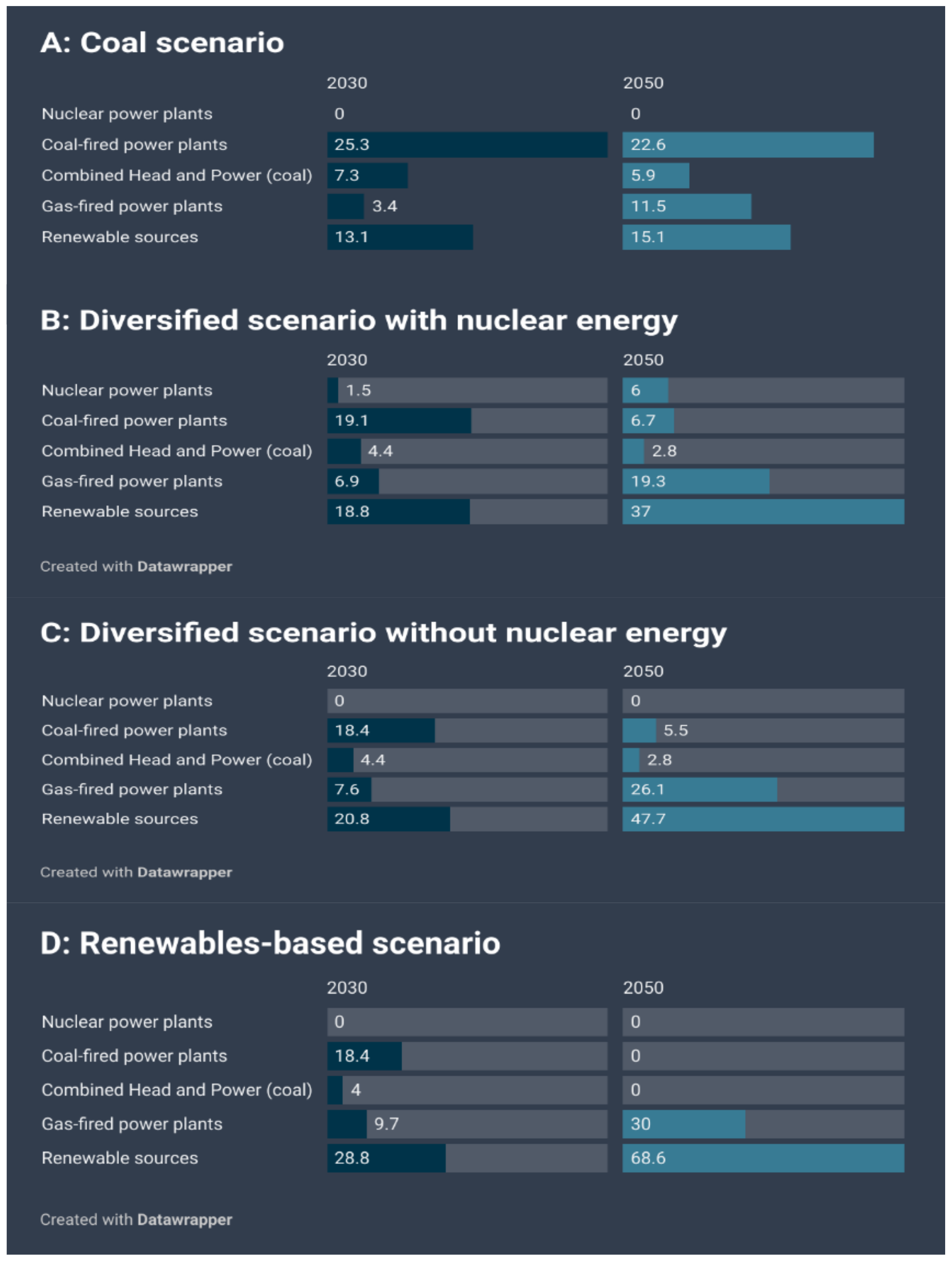

Some actions have already been announced by the Polish government. First, in February 2021, Poland endorsed its strategy for energy policies extending to 2040, with a target of attaining 23% of final energy consumption from renewable sources by 2030. The aim is to improve energy efficiency, diversify the power mix with nuclear and renewables, reduce power generation emissions, and develop competition. Poland also announced the closure of all coal mines by 2049. These fierce pledges are ambitious and necessary; nevertheless, the central question remains, “the coal question” (This refers to the seminal work of W.S. Jevons, The Coal Question), and in the scenario analysis of energy transition, this fossil fuel has not completely disappeared, as depicted in Figure 1.

Although there have been studies analyzing the possible scenarios of environmental transitions for coal mining and energy sectors worldwide, the majority of them prioritize macroeconomic, simulation-based investigation methods. In this paper, we propose an alternative, industrial organization (IO) approach, focusing on market design for the Polish coal sector from a global, macroeconomic perspective. The novelty of our approach therefore lies in offering microeconomic foundations for the Polish coal industry, as well as evaluating its financial condition with reference to international peers. We claim that given the inevitable “sunset industry” fate for the future of coal, the current global political and economic situation may lengthen the green transition, thus attenuating the stranding of coal assets. Therefore, the goal of this paper is to provide evidence of stranding risks for the Polish coal industry and to evaluate the financial condition of companies operating within it. Additionally, it also aims to provide a global economic outlook for the coal industry.

This article is structured as follows. The literature review section outlines the concept of stranded assets and stranding risks. Then, the next section briefly details the study materials and investigation methods. The subsequent section presents the results, which are further discussed in the light of possible policy designs.

2. Literature Review

The concept of “stranded assets” is not considered a new phenomenon, and therefore does not relate only to climate change transition risks and impacts. Stranded assets are defined as assets that suffer from unanticipated or premature write-downs, devaluations, or conversions to liabilities [2]. However, within the context of environmental concerns and climate change, this purely financial definition is rather insufficient to encompass the complex reality. Therefore, all natural resource endowments, investments in infrastructure and means of production and distribution, and other tangible or intangible assets that may become obsolete due to a transition to a greener economy or physical damage are classified as “stranded” [3]. This situation could arise from: (a) environmental challenges (e.g., direct, indirect, and induced impacts of climate change, e.g., increased incidences of weather events and natural disasters, air pollution, and health status, respectively); (b) changes in resource compositions (e.g., shale gas abundance); (c) government and international regulations (e.g., national or pan-national policy agreements on measures taken to mitigate climate change, such as carbon pricing or emission trading schemes); (d) changes in technology (e.g., falling prices of clean technologies such as photovoltaics); (e) changes in consumer and investor preferences (e.g., shifts in the consumption of electric cars); and (f) litigation (e.g., carbon liability) and changing statutory interpretations (e.g., fiduciary duties and disclosure requirements).

Although there has been a substantial shift in the amount of literature devoted to stranding phenomena, papers on stranded resources have scarcely considered the impacts of climate change [4]. Moreover, the literature stream that targets this research angle is also recent because the topic of stranded assets in the context of environmental risks was first brought up and publicly discussed in the journal Nature [5], in 2009. Furthermore, it is important to note that analyses of stranding assets have mobilized both academic and non-academic institutions, including, among others, the World Resources Institute and the United Nations Environment Programme Finance Initiative, the International Renewable Energy Agency, Oxford University, and Bloomberg. However, as noted in [6], academic studies of stranding phenomena, including financial evaluations and scenario analyses of assets exposed to stranding risks, remain relatively scarce. Indeed, most research is based on literature reviews, with only a few papers building on the application of assessment tools.

Most articles on stranded assets apply to natural gas and oil resources, with emphasis on their underutilization [7] due to technological and logistic complications, cost, and political constraints (e.g., liquefaction technologies for natural gas [8], high extraction costs [7,9,10], and political instability [11]). Interestingly, non-fossil fuel resources may also be stranded due to similar technological and logistical constraints such as oil and gas (e.g., wind farms frequently being situated offshore, far away from the existing grid [12,13]), but most importantly, they often become economically unsustainable because of seasonal characteristics (e.g., solar installations receive less radiation in winter).

Despite the relevance of the resource, the devaluation of coal has received less attention in the literature, and the empirical evidence remains fragmented and dispersed through different research areas. Nevertheless, the reality of the climate emergency has drawn the attention of scientists investigating both the material and financial aspects of coal divestment and its phasing-out.

Referring to the material risk category, some studies have been devoted to the evaluation of coal reserves and providing figures on the desired level of coal that must remain unburnt to meet the target of a maximum global temperature rise of 2 °C [14]. Some papers also rank countries according to the proportion of coal reserves stranded, with the United States, Russia, and Australia at the top of the list [15]. Within the same category of material risks, some articles focus on coal power capacities. For instance, the IRENA study describes the possibility of increasing coal-fueled power generation capacities in developing countries with collateral in the form of stranding risk beyond 2030 due to decarbonization targets [16]. Another interesting study [17] indicated that even if the entire development pipeline of power plants was cancelled, roughly 20% of the global capacity would need to be stranded to meet the climate goals set out in the Paris Agreement. Interestingly, 80% of this stranded capacity refers to coal-fired powers plants located in Asia. Indeed, numerous studies provide evidence of the rather recent and abundant coal-fueled power generation plant infrastructure in Asia, emphasizing some crucial challenges ahead of green transition, such as overcapacity and excessive investments in Chinese coal-fueled power generation infrastructure [18]. When related to forecasts on coal demand, this asset has a high chance of becoming “stranded” just because of a slower pace of retirement of mines compared to declining demand for coal itself. It is worth noting that scientific work on coal most frequently simulates a series of coal phase-out scenarios presented by regional or country splits and coal types [19]. Compared to the “business-as-usual” path, macroeconomic models enable the simulation of different environmental or climate change-related goals [15,20,21].

Referring to the financial dimension, we may distinguish two research perspectives. The first one seeks to understand the possible impacts climate change might have on the stability of financial systems, and if so, how to mitigate it by providing adequate responses from central banks and regulators [22,23,24]. Interestingly, the issue of the sovereign debt of countries exposed to climate change risks also falls under this category umbrella. The second perspective privileges investor exposure to stranded assets and efficient management strategies for financial portfolios exposed to environmental or climate change-related risks [25].

In summary, the literature on stranding phenomena concentrates on material risks and the impacts of the devaluation of fossil fuels; however, coal has received less attention compared to oil and gas. Additionally, financial approaches to the stranding of coal are rare, especially when referring to microeconomic analyses. To this extent, our paper sheds additional light on the financial conditions of companies in a coal-dependent economy.

3. Materials and Methods

The evaluation of coal as a “stranded asset” candidate is based on two methods. First, we proceed with a global outlook on the coal industry. Collecting data on coal reserves, production, use, and prices, we draw conclusions about the future of this fossil fuel. Secondly, building upon these conclusions, we proceed with the assessment of coal-intensive Polish companies (from the coal mining and energy sectors) from the market-design perspective and through a financial analysis lens. In turn, this enables us to voice proposals in terms of economic policy related to the future of coal in Poland and to open a dialogue about ongoing and planned policy orientations in that matter.

4. Results

4.1. Global Perspectives on Coal

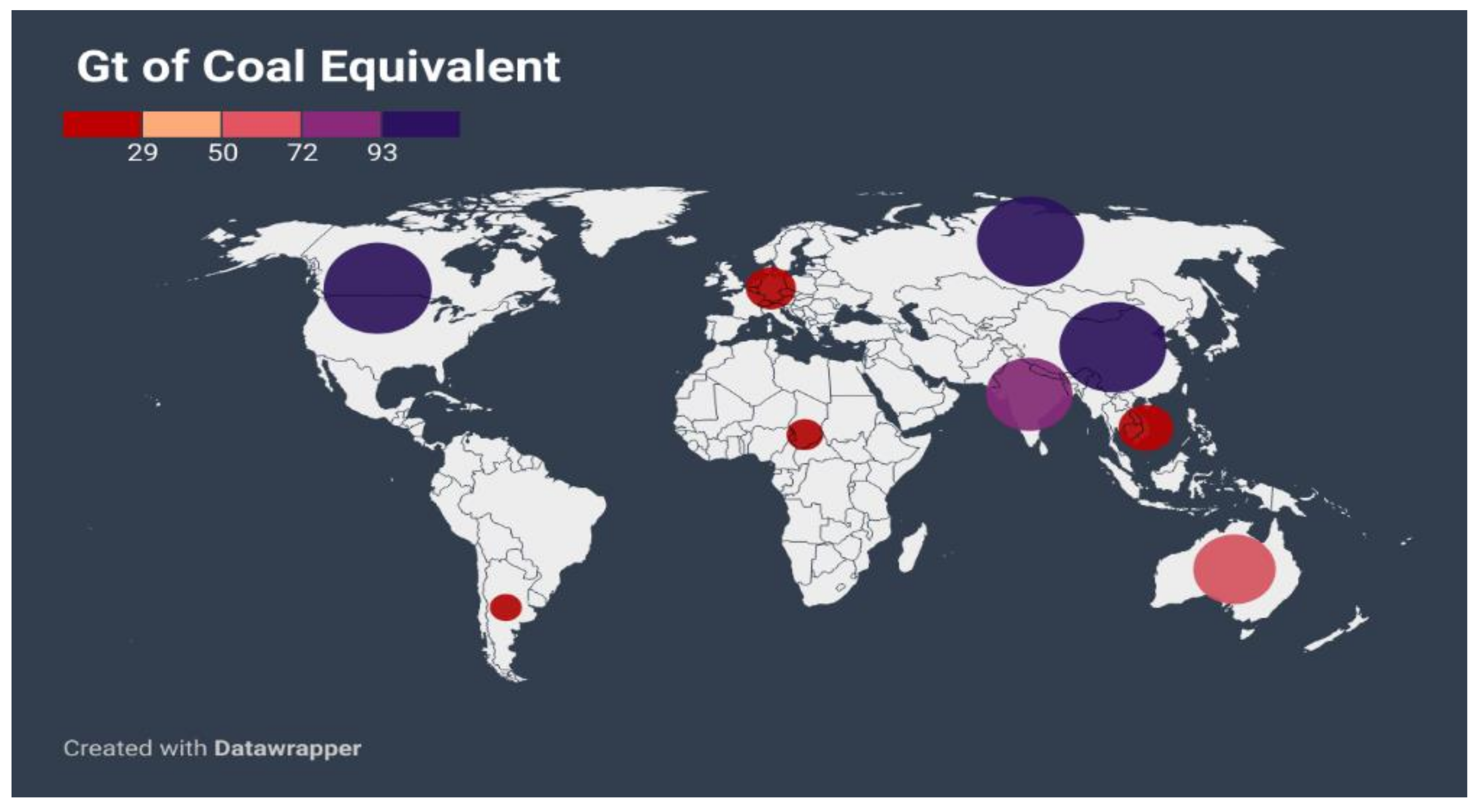

Reserves of coal and lignite are estimated to be 17,489 billion tonnes of coal equivalent (Gtce), of which only 1.2% has been extracted since 1950. The most important coal ores are located in North America, followed by regions of the Commonwealth of Independent States and China (Figure 2).

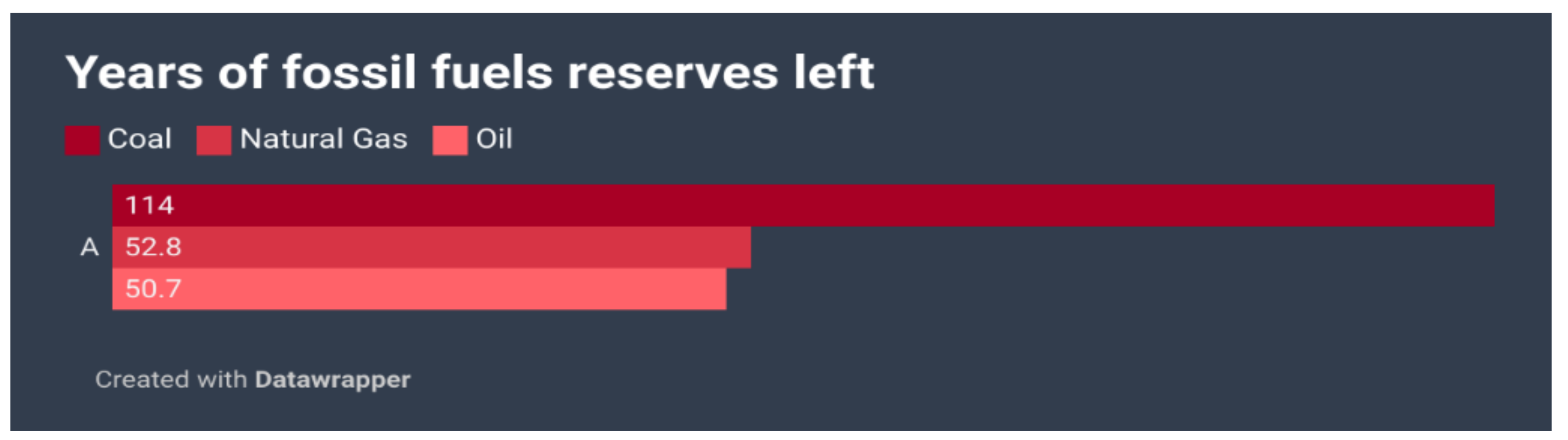

Coal is still abundant compared to reserves of oil and natural gas (Figure 3).

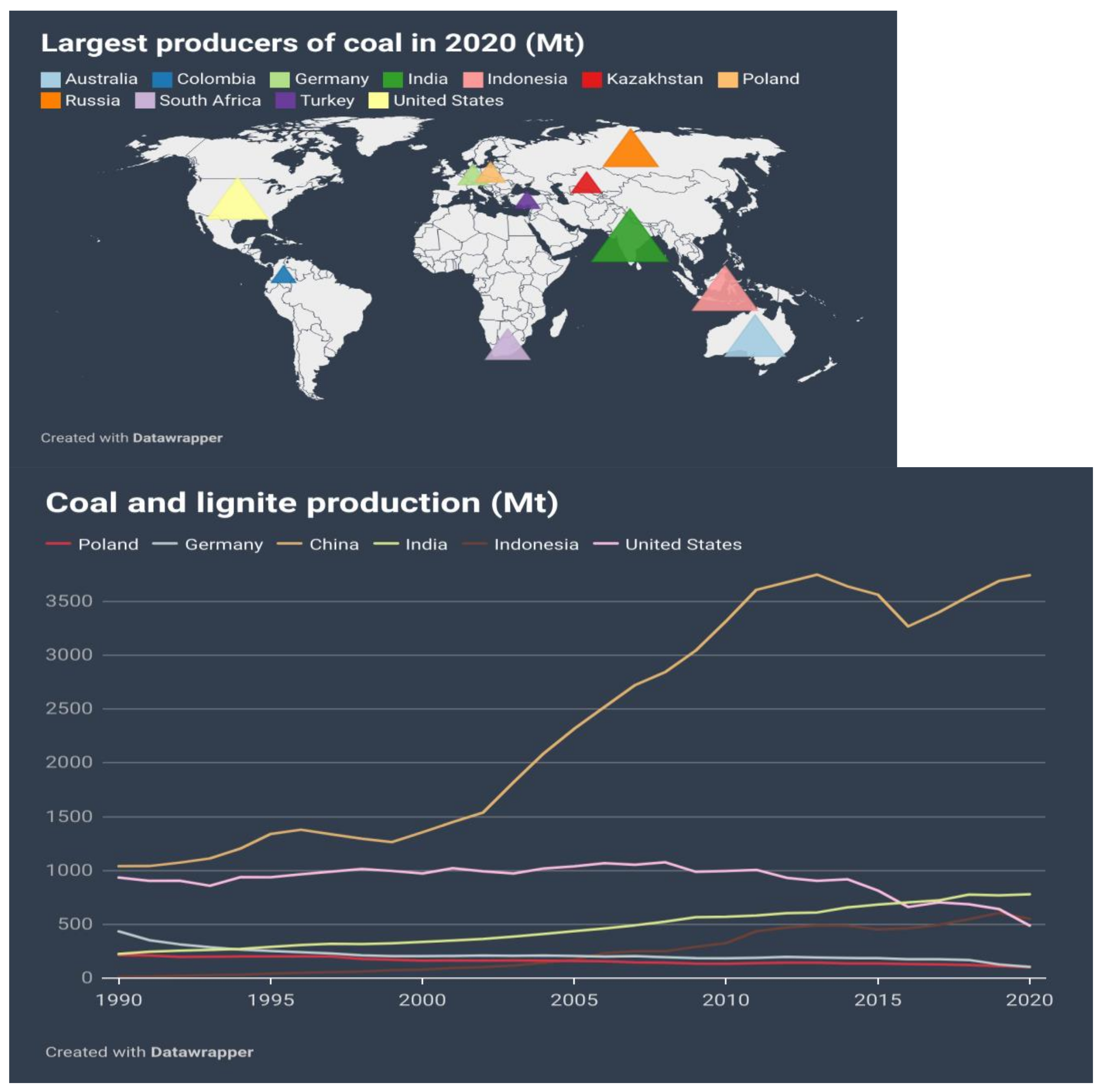

Moreover, coal reserves account for over half of all non-renewable energy reserves and are distributed more equally than those of oil and gas. The largest coal producers in 2020 were China and India, followed by Indonesia and the United States, as shown in Figure 4. Poland was the tenth largest global producer and the second largest in the European Union, behind Germany.

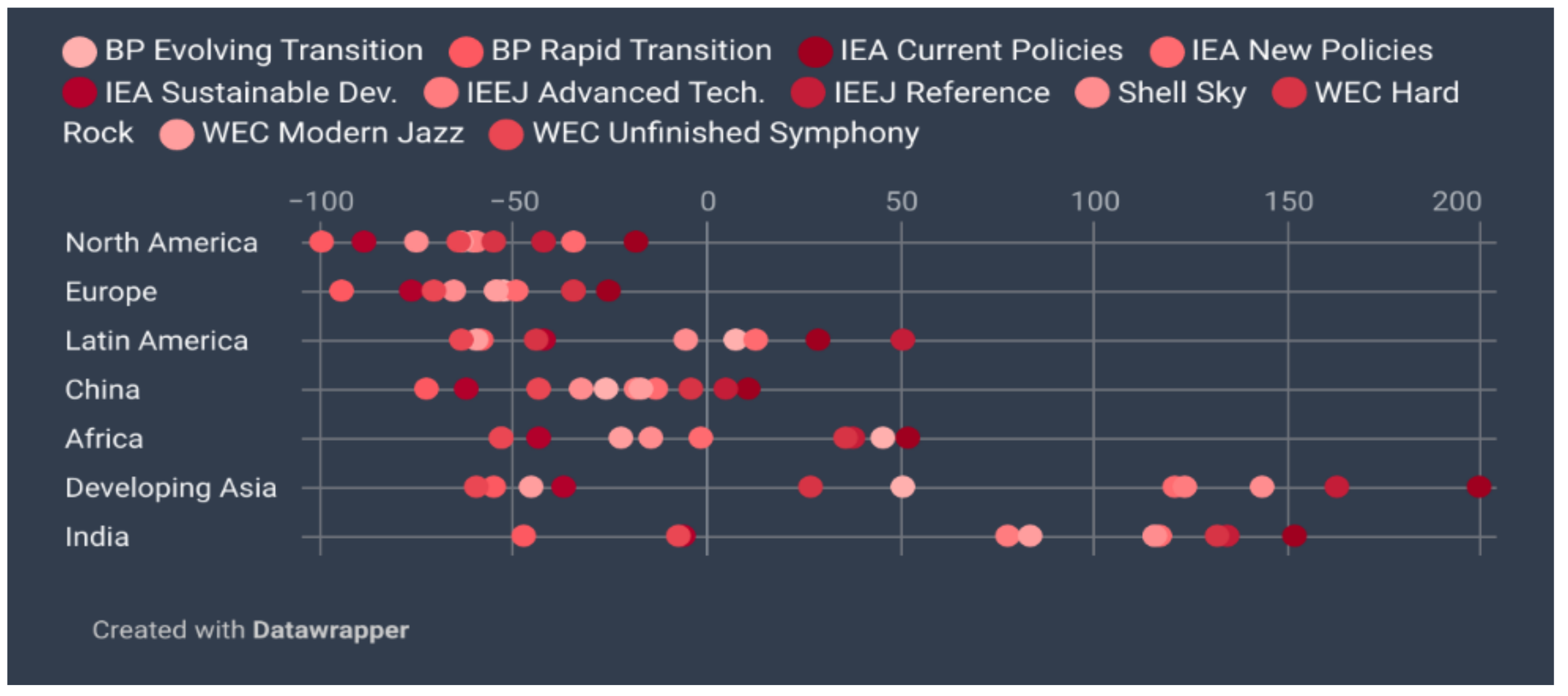

When considering recent studies evaluating the future demand for coal with regard to different transition scenarios, we may observed large forecast differentials and even divergences, as depicted in Figure 5.

Although we expect a pronounced drop in the consumption of coal in Northern America, Europe, Africa, and China (70% on average) in the next two decades, forecasts are less conclusive for Asia and Latin America. However, these scenarios remain highly dependent on the level of environmental goals and are subject to modifications in relation to the implementation of climate-related policy tools.

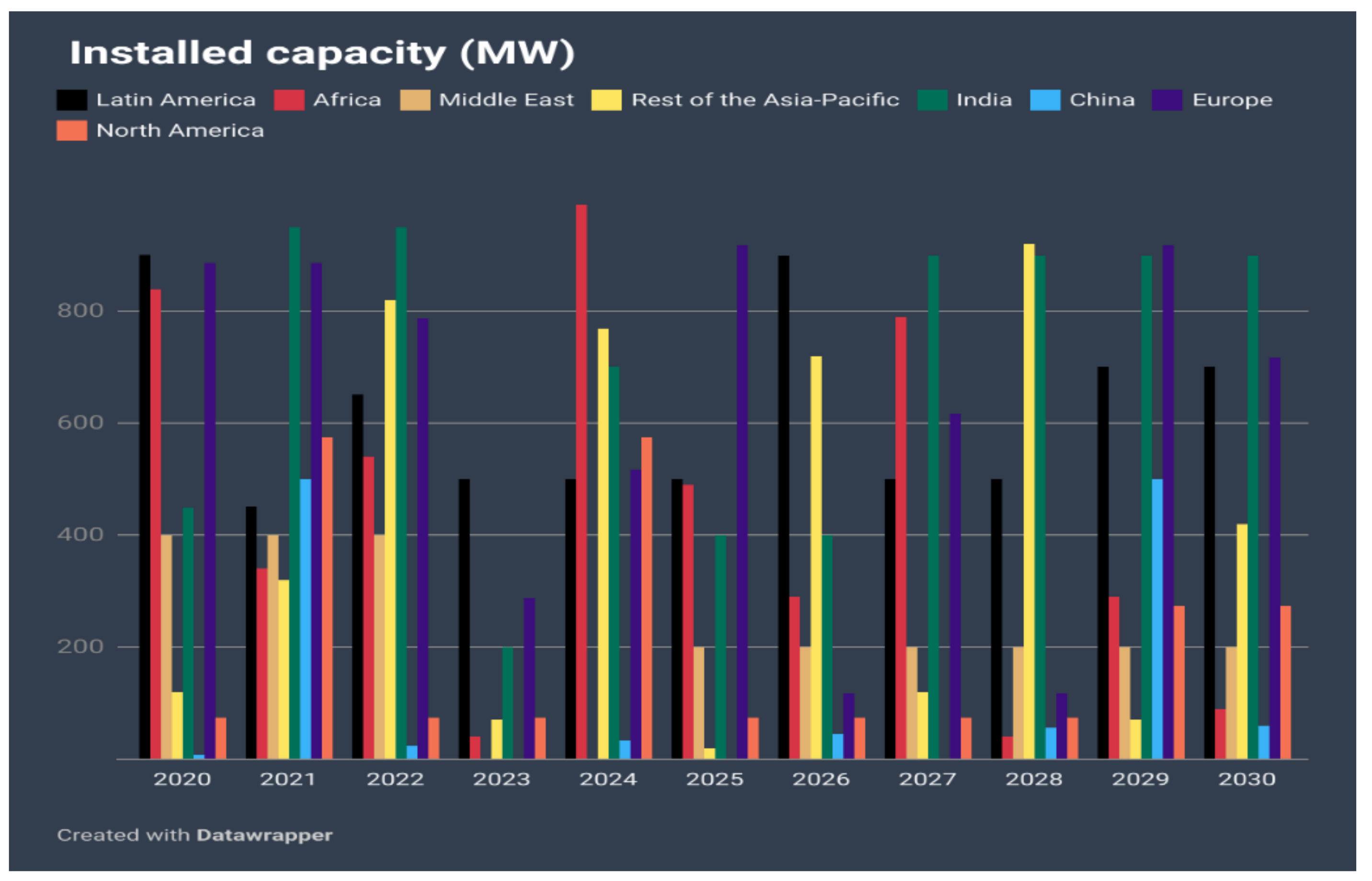

Concerning coal-fired energy production, 2021 is forecast to be the peak year for this fossil fuel resource, with global installed capacity projected to decline by slightly more than 10% over the next decade (Figure 6).

This trend will be accompanied by decreasing utilization rates. China, which accounts for approximately half of the global installed capacity, will reach its peak in coal usage in 2025 and will decline afterwards as energy from renewable resources meets more of the country’s supply requirements. In India, despite its increasing investments in renewable sources of energy, the phasing-out of coal seems to be slower than elsewhere, due to increasing demand for energy and the impossibility of satisfying the nation’s energy needs without coal-fueled stations. Coal-fired energy capacities are likely to halve in North America, with Canada closing all plants. Interestingly, closure rates in the United States will be higher than those in Europe, where most Western European countries will be coal-free, except Germany. In Central and Eastern Europe, the Balkans, and Turkey, coal should remain a substantial part of the fuel mix.

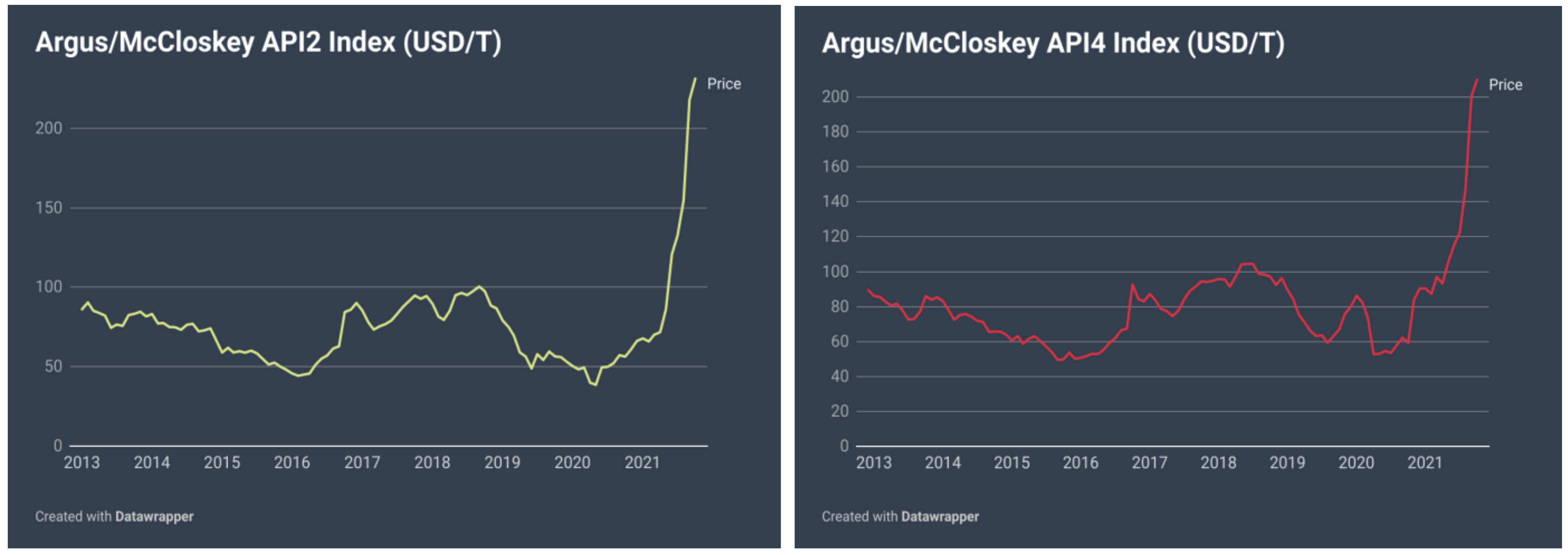

Currently, in late 2021, the global demand for coal has recovered strongly from earlier COVID-19-related impacts. At the same time, record highs in gas prices have made coal more competitive (coal and gas prices, in particular, have risen sharply, reaching their highest levels in over a decade). Recently, the global supply of coal has suffered from disruption due to extraordinary events affecting the trade. Multiple port fires in Russia and South Africa, damaged Australian shiploaders, torrential rains constraining coal extraction in Indonesia, as well as multiple strikes at production sites in Colombia have amplified the rise in coal prices. For example, the API 2 index prices for hard coal has more than doubled, from just under 70 USD/tonne at the beginning of 2021 to over 200 USD/tonne in September 2021 (see Figure 7).

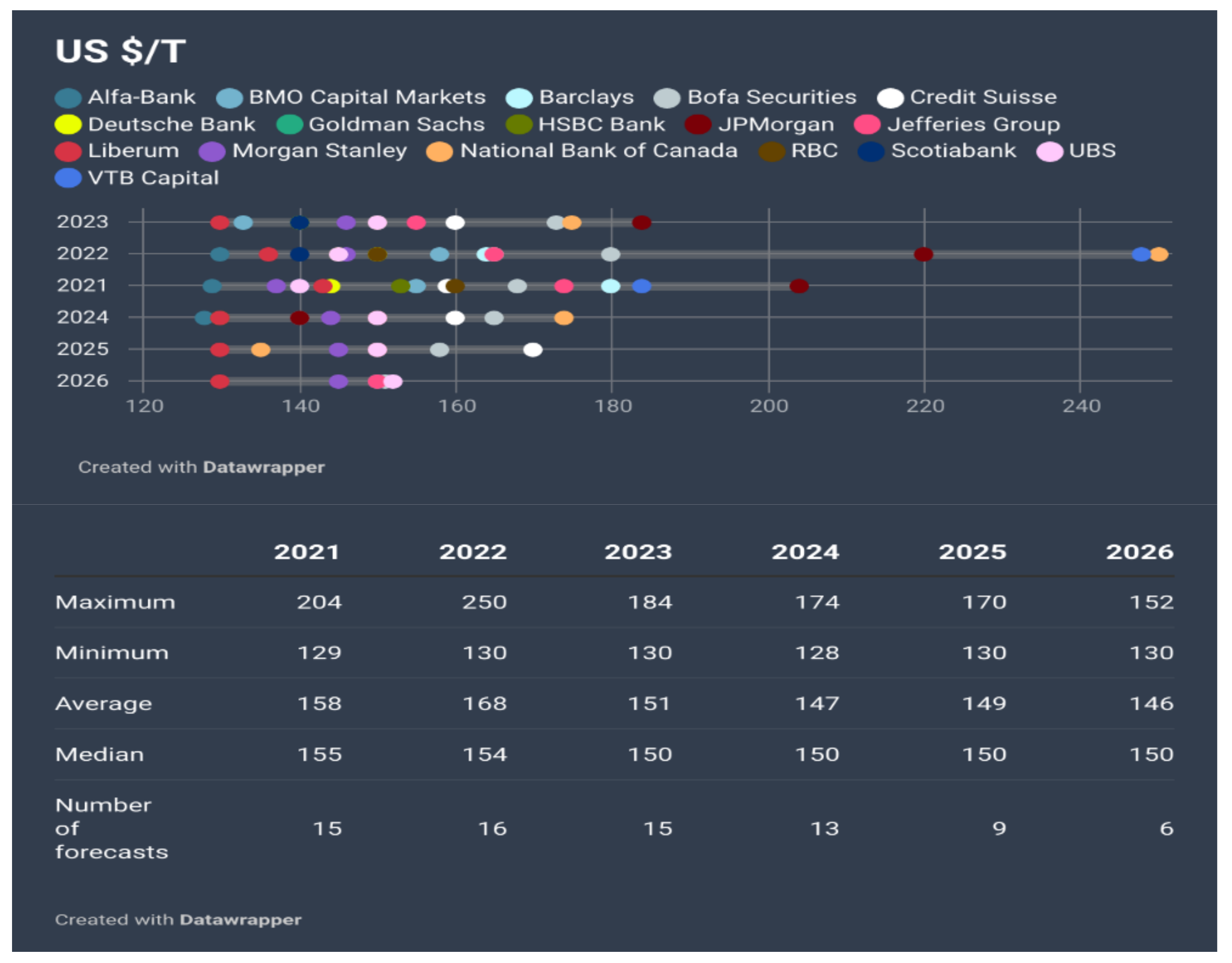

In the near future, previous forecasts of rapid gas-to-coal switching will need to be adjusted negatively due to the increased demand for energy in Europe, resulting in coal-fired generation nearing full capacity. Figure 8 summarizes the projections for coal prices elaborated by major investment banks. This outlook forecasts a steady price for coal in the coming years, at an average of USD 150 per tonne.

However, the rebound in global demand for coal has been a major driver of the upward pressure on coal prices seen since late 2020. Therefore, this upward trend in coal prices is expected to persist due to loose monetary policies and expansionary fiscal policies around the world, leading to further expansions in coal demand beyond early 2022. According to recent scenarios, coal may reach new heights in 2022, at USD 250/tonne.

4.2. Coal in Poland

Historically, Poland has been heavily dependent on coal. This stems from the fact that coal, along with copper, was one of few, relatively abundant natural resources in the country; therefore, its use for energy generation for decades seemed to be a necessity. Indeed, the country is poorly endowed with natural gas, and geopolitical factors make it difficult to import it at a reasonable scale. The hydrological position of Poland, with lowland rivers, does not enable the country to expand into hydroelectric power generation. Additionally, the country experiences too few sunny days, which does not allow for the extensive use of solar energy. The Baltic Sea theoretically represents an opportunity for offshore wind generation in the northern part of the country; however, the demand for electricity is highest in the south. Finally, to date, Poland has not built a single nuclear power generation plant, which makes the country an exception among other post-socialist-bloc EU members such as the Czech Republic and Hungary.

In the 20th century, Poland, together with the United States, Soviet Union, United Kingdom, and Germany, was among the top global producers of coal. However, the implementation of central planning during the post-World War II period left the coal sector dysfunctional. The falling efficiency of collieries and lack of access to global markets were the main reasons for its catastrophic condition in the 1980s. During an economic transition, large industrial companies underwent restructuring. Some mines were shut down, whereas the remaining became privatized or commercialized. After thirty years, the coal sector and its strategic position for energy generation and energy security still make it sensitive to changes, especially in the context of internal (mainly societal) and external (environmental and regulatory) pressures.

As already mentioned in the introduction, Poland recently approved its new national energy policy. This is based on four main elements: (1) the rapid diversification and growth of energy generation from low-carbon resources aimed at achieving a 50% reduction in CO2 emissions in the electricity sector by 2040; (2) decreasing the share of coal in electricity production to around 60% by 2030, which is meant to almost halve the amount of coal-generated energy from 130 TWh in 2020 to 75 TWh in 2040; (3) grow renewable energy sources in the total electricity production to 27% within a decade; and (4) the construction of the first nuclear power plant is planned for 2033, and six more nuclear units are scheduled by 2043. The current situation of coal and its future are not only dependent on the implementation of this strategy, but are also bound by global constraints, such as the energy supply constraints discussed in the previous section and the international harmonization of environmental policies. Additionally, the realization of this ambitious policy will require high investment outlays in the energy sector, as well as the profound transformation of Poland’s mining industry. To secure the plan financially, Poland submitted an official recovery and resilience plan to the European Commission, requesting a total of EUR 23.9 billion in grants under the Recovery and Resilience Facility, and EUR 12.1 billion in loans. The country is also seeking financial aid to realize its policy targets within Multinational Financial Framework negotiations and compensation mechanisms related to the revised EU Emission Trading System (ETS Directive), as well as supporting the EU Just Transition Fund for energy.

The situation of coal in Poland is structured by the country’s high dependence on this resource for energy generation. Therefore, the industrial organization of the coal industry results from the overlaps between mining companies and power generation firms. This interdependence is visible in the ownership structure of firms operating within these two sectors of the coal industry.

4.2.1. Coal Mining Sector

The Polish coal mining industry, which is largely state-owned, is restructuring to improve profitability in the context of falling production and high operation costs. The restructuration process is being implemented through mine transfers, as well as company mergers and liquidations. SRK (Spółka Restrukturyzacji Kopalń) was created in 2000 to take over unviable mines. PGG (Polska Grupa Górnicza) was created in 2016 to integrate 11 mines and 4 processing plants from Kompania Węglowa (the largest coal mining company liquidated in 2015). PGG took over KHW (Katowicki Holding Węglowy, a state-owned coal producer) in 2017. PGG produced 24 Mt of coal in 2020. The company plans to shut down the “Pokój” and “Wujek” mines in 2021. It is important to note that energy sector moguls (e.g., PGNiG, Węglokoks, PGE, and Energa) are minority shareholders of PGG. Finally, JSW (Jastrzębska Spółka Węglowa) is a major producer of high-quality hard coking coal and coke, with an annual output of 14 Mt in 2020. Notably, the closure of coal mines is a sensitive matter due to its significant social costs. Therefore, with the last shutdowns scheduled for 2049, Poland needs to secure funds to support regions exposed to coal phase-outs, especially Silesia. However, the good news is that an agreement with unions on transition terms was reached in April 2021.

4.2.2. Energy Sector

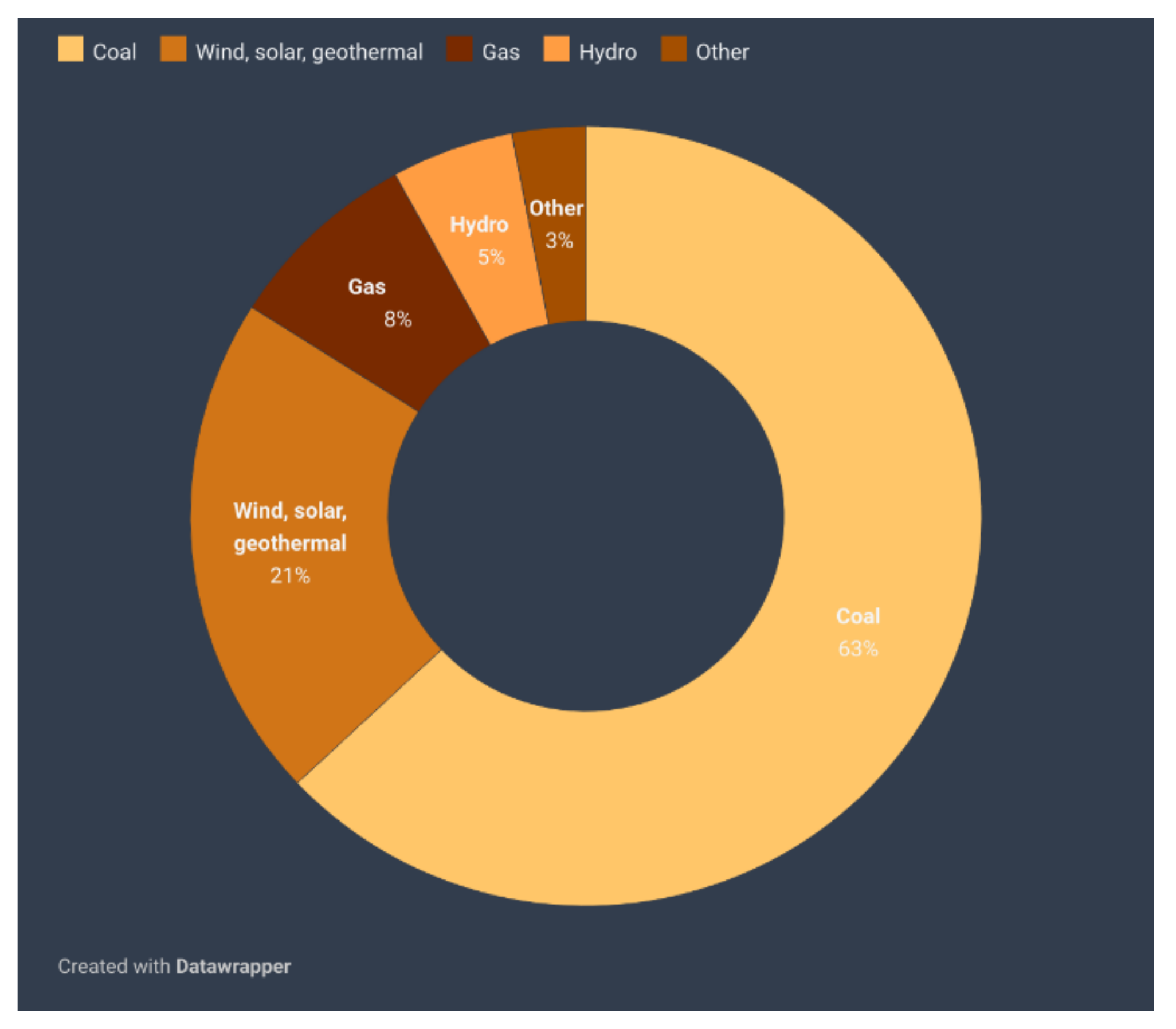

Poland has a capacity of around 49.3 GW, of which 63% is coal-dependent, as illustrated in Figure 9.

This sector also faces massive restructuring processes. In terms of market structure, energy generation is susceptible to oligopoly, with three large companies dominating the market: PGE, Tauron Polska Energia, and ENEA. These entities account for 64% of the total power generation in Poland. PGE (57.4% state-owned) is the largest of the three, with 58 TWh of electricity produced in 2020. Back in 2017, this company acquired thermal power assets from Électricité de France (EDF), and the company currently supervises eight distributors, six retail companies, and three lignite mines. In turn, ENEA (51.5% state-owned) generated 22.5 TWh in 2020 due to increases in capacity enabled by the acquisition of the Polianec coal-fired plant from Engie, and the commissioning of a 1075 MW coal-fired plant in Kozienice. Finally, Tauron Polska Energia (51.5% owned by the State Treasury, 10.4% owned by KGHM Plska Miedź and in 5.1% by Nationale Nederlanden) generated 12.5 TWh in 2020. The remaining electricity production is secured by ZE PAK and Energa (4.9 TWh and 3.2 TWh, respectively). There is also a dedicated, state-owned company, PSE (Polskie Sieci Energetyczne), which is responsible for the power transmission grid. By late 2020, it operated a 15,300-km long transmission grid. Currently, three distribution companies account for 75% of the power distribution: Tauron, PGE, and Energa. Interestingly, PGNiG, the national gas company, sells electricity to industrial customers.

4.2.3. Market Situation

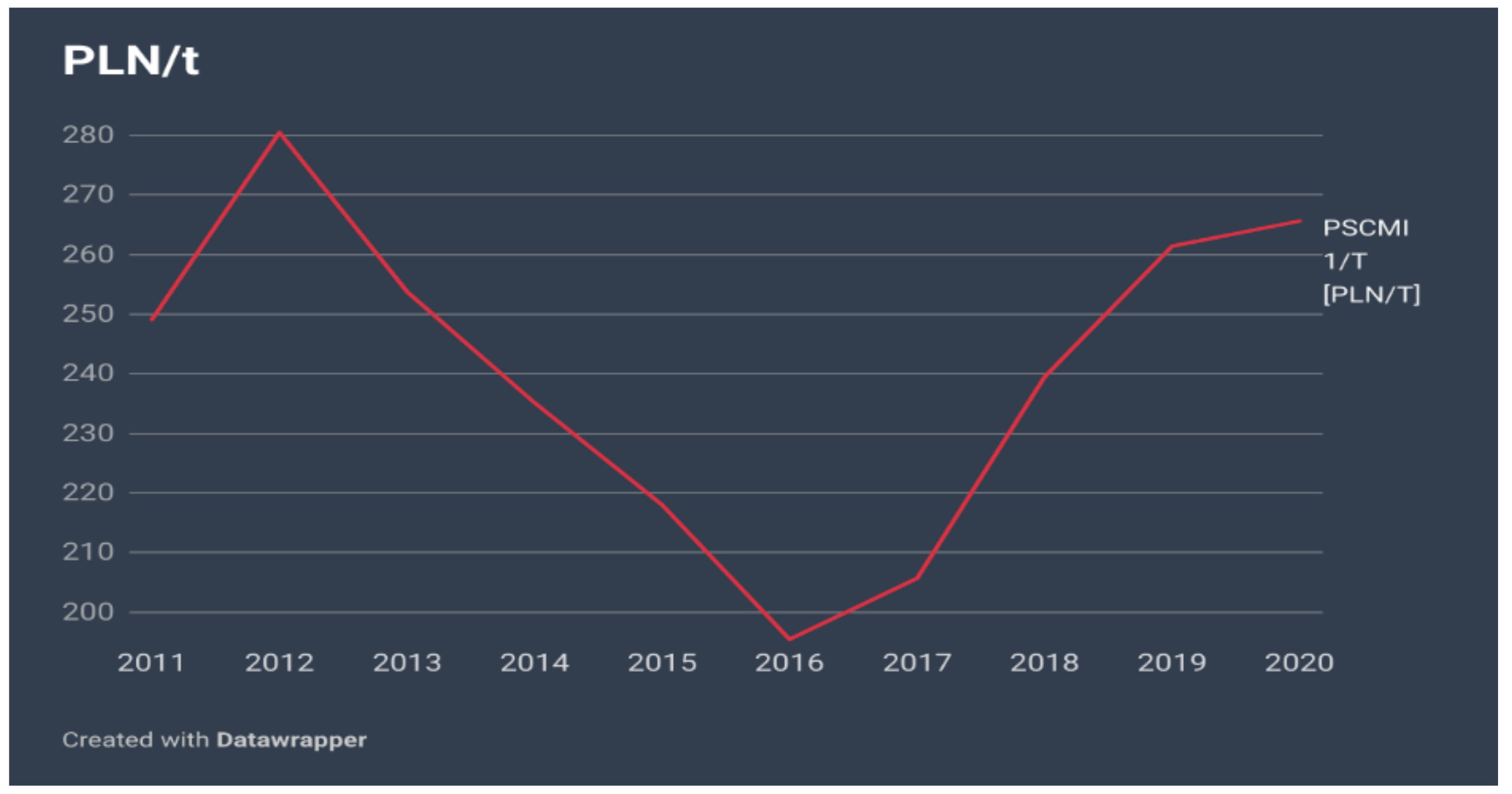

As already described, there are very close ties between coal producers and energy producers running on coal (the latter often own or have stakes in coal mining companies). The fluctuations of coal prices in the domestic market is described by the Polish Steam Coal Market Index (PSCMI® 1) reflecting the price of steam coal fines in sales to electricity producers (public power plants and industrial power plants). As displayed in Figure 10, after years of decline, the price of coal is increasing and follows the upward trend, remaining in line with the European benchmark.

4.2.4. Financials

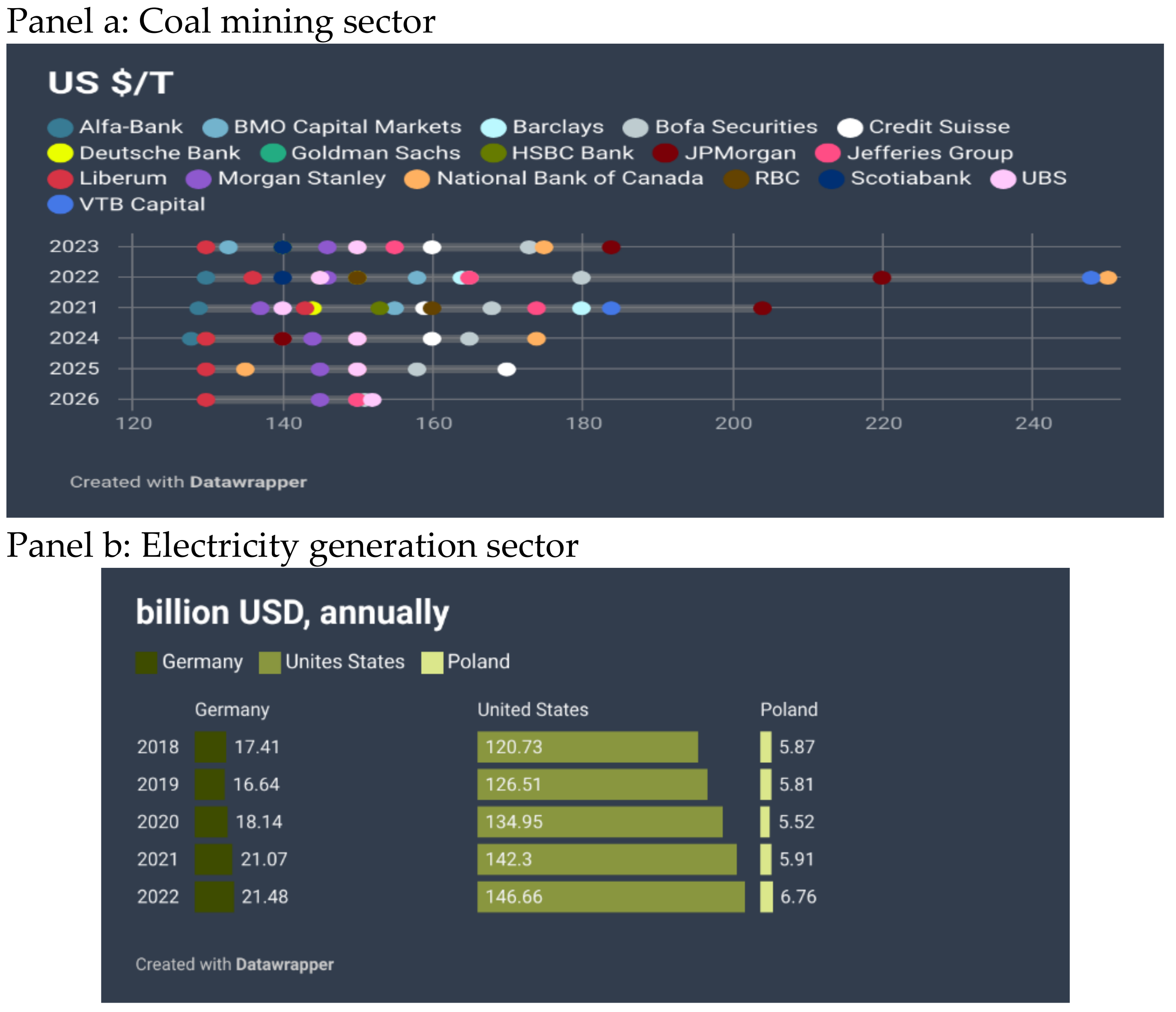

The financial evaluation of companies within the coal industry in Poland began with international benchmarking. Comparing operating surpluses of firms across a series of countries, Polish mining companies display rather comfortable revenue figures, especially when compared to Germany (Figure 11, panel a). This metric changes when it comes to the electricity generation sector, where the margins for Polish firms are substantially lower compared to peers (Figure 11, panel b). The operating revenue differentials with Germany in the energy generation and distribution sectors are because electricity prices in Poland are around 35% below the EU average, and 20% below for corporate clients.

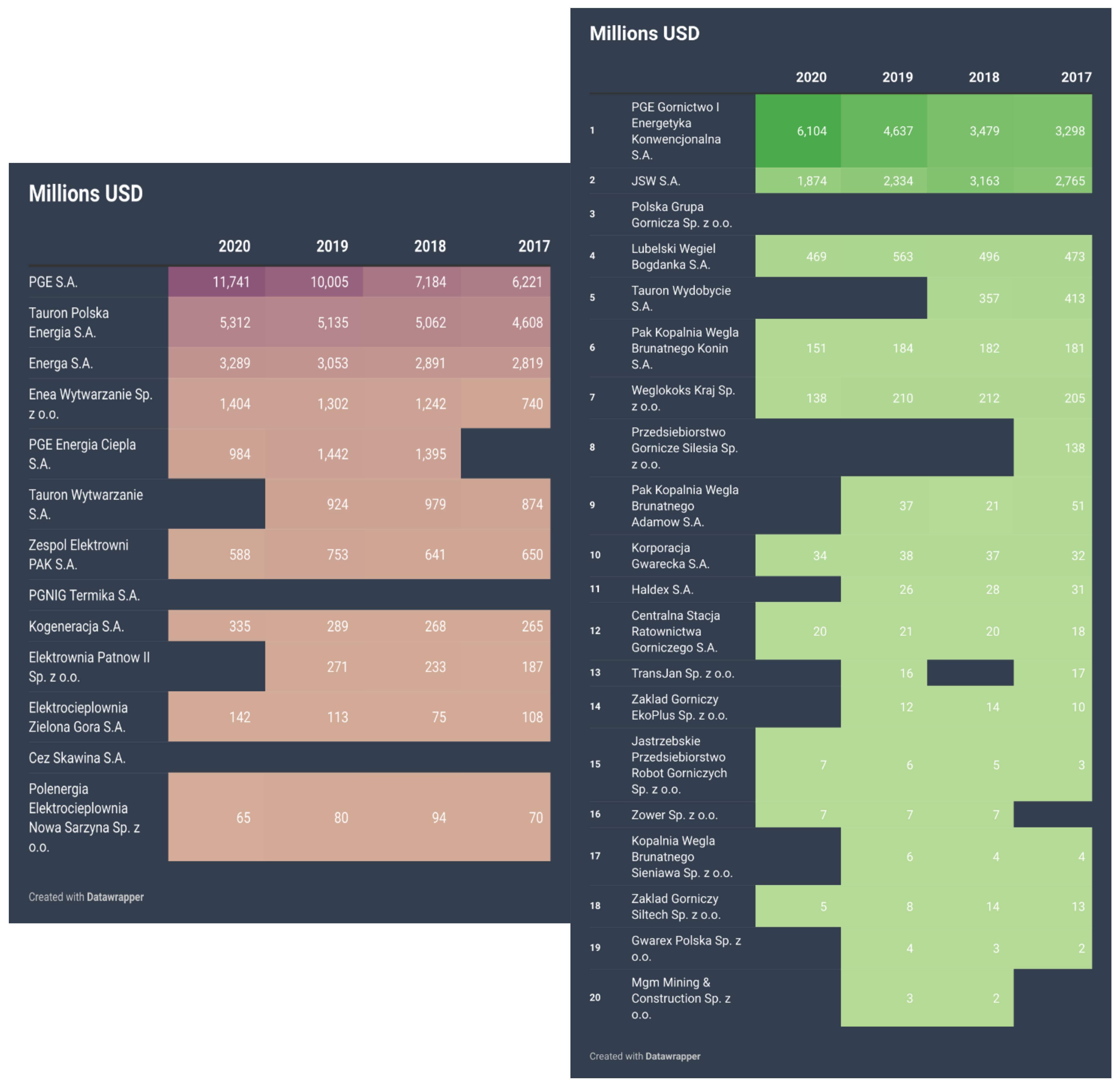

A query about EMIS and Refinitiv EIKON data returned information on a number of companies currently in operation according to North American Industry Classification System (NAICS) primary industry codes. By December 2020, there were 73 firms and companies active in the coal sector, but only a few of these were in the business of coal extraction. With reference to the energy generation and distribution sectors, there were 14 companies. Figure 12 benchmarks companies from these two sectors by operating revenue.

This analysis yielded two interesting findings. First, there is a strong size effect visible for leading companies in both sectors, mostly due to the partly achieved and ongoing restructuration and concentration of companies. These integration processes are occurring horizontally (as in the coal mining sector, where JSW conglomerates several mining plants) and vertically (energy producers take control over entire value chain—from resources through generation and distribution to financial services—as in the case of PGE, S.A). Second, there has been an upward trend in the revenue levels of the largest holdings. Surprisingly, the revenues also increased in 2020, regardless of economic slow-down, as an impact of the COVID-19 pandemic.

In order to assess the financial condition of companies, we proceeded with valuation multiples analysis (Table 1). Data on leading companies from the energy generation and coal mining sectors have been benchmarked against sector peers. In analyzing enterprise value metrics, we observed that two companies outperformed the average enterprise value both within and beyond their core sectors. This result is an interesting one; the EV:EBITDA (The enterprise value (EV) of the earnings before interest, taxes, depreciation, and amortization (EBITDA)) ratio shows that investors are willing to invest in these companies because their incremental profit units are covered by larger enterprise values compared to the sector’s average. This held even for PGE S.A., a company that displayed a drop in earnings per share, which can be seen as an indicator of lower profits, meaning that investors are not discouraged by short-term results. Overall, the sound condition of Polish companies operating in coal-intensive sectors is acknowledged by the StarMine Refinitiv valuation model, which combines the most important multiples into one clear valuation measure. Currently, PGE. S.A displays a score of 97/100, and JSW S.A. scores 80/100 among all companies in emerging markets.

Currently, large players in the Polish energy and coal-mining sectors are back on track after quickly recovering from the pandemic. A brief examination of the financial results for these companies exceeded expectations. For instance, JSW S.A. displayed an adjusted EBITDA that was 38% higher than forecasted for the second quarter of 2021, mainly due to lower-than-expected coke conversion costs. The trend in coal prices suggests a very positive outlook for late 2021 and early 2022. Profitability also increased among energy production and distribution companies, regardless of the increased investments.

5. Discussion

Having analyzed the global situation for coal mining and coal-dependent industries, such as the energy generation sector, it seems that coal still has at least two decades of value ahead. This is due to its relative abundancy and price competitiveness compared to non-fossil fuels. Indeed, the phasing-out of coal is inevitable in the context of negative climate change scenarios; however, it will happen gradually because the switch to non-fossil fuels is expected to be extended, especially in the developing world. Indeed, our analysis shows that many countries are still heavily dependent on coal in fulfilling their energy needs. Interestingly, this is not only the case in developing countries; countries such as the United States and Germany are still large consumers of coal, despite their ambitious plans for ecological transitions. The geopolitical situation does not make the situation easier, especially with the shortages of natural gas on the global market and increasing security concerns over its supply. Unsatisfied needs for energy have increased coal prices to record highs, despite the constant raise in carbon prices and ETS settlement requirements. Finally, the decrease in new investments in coal-related infrastructure is not sufficient to shorten the life cycle of existing plants (many of them are still relatively new, so premature closure would be unsustainable both technically and financially).

Our analysis also shows how coal extraction sectors are intertwined with energy generation sectors. This is precisely the case in Poland, a country that has historically and geologically been dependent on coal. Despite the reforms which commenced at the dawn of its economic transition, the country is still facing important challenges associated with profound transformation of its coal mining and energy generation reforms. Already, concentration movements are visible in both sectors, which is being accompanied by the closure of mining sites. Our analysis acknowledges that, currently, the financial situation of companies operating within coal industry is sound, and that the global macroeconomic perspectives on coal prices may help them to invest this financial surplus in restructuring and modernization efforts. Indeed, the successive closure of coal mines may lead to dramatic increases in unemployment; therefore, a solid financial back-up will be needed to compensate for the disappearing jobs. At the same time, firms from the energy generation sector must develop their coal phase-out strategies. There are some promising plans for that matter. Recently, the Polish government unveiled plans to separate coal mines from PGE, ENEA, and Tauron, and to sell them to the State Treasury in 2022. These would then be consolidated within the new National Energy Security Agency, which is responsible for gradually phasing them out. The transition strategies will also necessarily involve substantial investments in new energy generation power plants, as well as rehabilitation projects for existing facilities. With the ever-increasing electricity demand, power generation companies will need to shift their capacities, involving the development of nuclear power generation sites. For this, Poland is considering the development of its nuclear program through a specially purposed vehicle, in which PGE, Tauron, ENEA, as well as KGHM will have stakes. Finally, for the time being, the impacts of the European New Green Deal policy on the Polish energy sector remain unclear, due to high uncertainties over energy-mix composition.

6. Conclusions

In this article, we provide evidence that coal, although undoubtedly a strong stranded asset candidate, is still a very valuable resource, and this situation is not projected to evolve much in the next twenty years. Coal dependence is forecasted to persist due to projected increases in the global demand for energy, which will not be satisfied with non-fossil fuels alone. Therefore, in the context of climate emergency, efforts in making coal less harmful seem to be a sensible step, especially when enabling technologies exist, and their cost is decreasing. Reducing CO2 emissions from the coal-fired power sector in Poland will be essential for achieving mitigation targets. Technological advancements such as carbon capture and storage (CCS) facilities could be a solution to decarbonizing the coal-fired power sector in Poland. However, costs related to CCS technology are still creating a barrier for the introduction of this technology into the Polish coal sector, which could significantly reduce CO2 emissions.

The UN Climate COP26 in Glasgow brought some important conclusions and declarations for the future of the coal not only in Poland, but globally. Poland, along with twenty more countries, including Vietnam and Morocco, committed to halting investments in new coal plants, continuing similar commitments announced in the past year by Pakistan, Malaysia, and the Philippines and joining the initiative No New Coal Power Compact. This initiative, started by a diverse group of developing and developed countries, aims to stop the construction of new coal-fired power plants to keep the 1.5 °C goal within reach. The Glasgow climate summit almost succeeded in pledging to end coal-fueled power, but members failed to agree on a call to “phase out” the use of coal, which was softened to a “phase down” after the intervention of India and China, which weakens the commitment to eliminating the combustion of coal. Poland has backtracked from the COP26 declaration to cease from burning coal by 2030, just hours after signing it, and the Polish Climate and Environment Minister has confirmed that Poland is planning to phase out coal by 2049.

Author Contributions

Conceptualization, W.K. and A.G.; methodology, W.K.; investigation, W.K.; data curation, W.K.; writing—original draft preparation, W.K. and A.G. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Data supporting this research are available at: Mendeley Data, V1, doi: 10.17632/kj8tpdsc9f.1.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Horowitz, C.A. Paris Agreement. Int. Leg. Mater. 2016, 55, 740–755. [Google Scholar] [CrossRef]

- Caldecott, B.; Howarth, N.; McSharry, P. Stranded Assets in Agriculture: Protecting Value from Environment-Related Risks. 2013. Available online: https://www.smithschool.ox.ac.uk/publications/reports/stranded-assets-agriculture-report-final.pdf (accessed on 1 November 2021).

- Parker, E.; Krustins, K. Climate Change ‘Stranded Assets’ Are a Long-Term Risk for Some Sovereigns; Fitch Ratings: New York, NY, USA, 2021. [Google Scholar]

- Bos, K.; Gupta, J. Stranded assets and stranded resources: Implications for climate change mitigation and global sustainable development. Energy Res. Soc. Sci. 2019, 56, 101215. [Google Scholar] [CrossRef]

- Meinshausen, M.; Meinshausen, N.; Hare, W.; Raper, S.C.B.; Frieler, K.; Knutti, R.; Frame, D.J.; Allen, M.R. Greenhouse-gas emission targets for limiting global warming to 2 °C. Nature 2009, 458, 1158–1162. [Google Scholar] [CrossRef] [PubMed]

- Breitenstein, M.; Anke, C.-P.; Nguyen, D.K.; Walther, T. Stranded Asset Risk and Political Uncertainty: The Impact of the Coal Phase-out on the German Coal Industry; Social Science Research Network: Rochester, NY, USA, 2020. [Google Scholar]

- USGS Open-File Report 2013–1044: Role of Stranded Gas in Increasing Global Gas Supplies. Available online: https://pubs.usgs.gov/of/2013/1044/ (accessed on 7 November 2021).

- Economides, M.J.; Wood, D.A. The state of natural gas. J. Nat. Gas Sci. Eng. 2009, 1, 1–13. [Google Scholar] [CrossRef]

- Bergbauer, S.; Maerten, L. Unlocking stranded resources in naturally fractured reservoirs using a novel approach to structural reconstructions and palaeostress field modelling: An example from the hoton field, Southern North Sea, UKCS. Geol. Soc. Lond. 2015, 421, 245–261. [Google Scholar] [CrossRef]

- Ball, M.; Wietschel, M. The future of hydrogen—Opportunities and challenges. Int. J. Hydrogen Energy 2009, 34, 615–627. [Google Scholar] [CrossRef]

- Dong, L.; Wei, S.; Tan, S.; Zhang, H. GTL or LNG: Which is the best way to monetize “stranded” natural gas? Pet. Sci. 2008, 5, 388–394. [Google Scholar] [CrossRef] [Green Version]

- Hunter, T. The role of regulatory frameworks and state regulation in optimising the extraction of petroleum resources: A Study of Australia and Norway. Extr. Ind. Soc. 2014, 1, 48–58. [Google Scholar] [CrossRef]

- Leighty, W.C.; Holbrook, J.H. Alternatives to electricity for transmission, firming storage, and supply integration for diverse, stranded, renewable energy resources: Gaseous hydrogen and anhydrous ammonia fuels via underground pipelines. Energy Procedia 2012, 29, 332–346. [Google Scholar] [CrossRef] [Green Version]

- McGlade, C.; Ekins, P. The geographical distribution of fossil fuels unused when limiting global warming to 2 °C. Nature 2015, 517, 187–190. [Google Scholar] [CrossRef] [PubMed]

- Auger, T.; Trüby, J.; Balcombe, P.; Staffell, I. The future of coal investment, trade, and stranded assets. Joule 2021, 5, 1462–1484. [Google Scholar] [CrossRef]

- Gielen, D. Global Energy Transformation: A Roadmap to 2050; IRENA: Abu Dhabi, United Arab Emirates, 2019. [Google Scholar]

- Pfeiffer, A.; Hepburn, C.; Vogt-Schilb, A.; Caldecott, B. Committed emissions from existing and planned power plants and asset stranding required to meet the paris agreement. Environ. Res. Lett. 2018, 13, 054019. [Google Scholar] [CrossRef] [Green Version]

- Spencer, T.; Berghmans, N.; Sartor, O. Coal transitions in China’s power sector: A plant-level assessment of stranded assets and retirement pathways. Coal Transit. 2017, 1–26. [Google Scholar]

- Diluiso, F.; Walk, P.; Manych, N.; Cerutti, N.; Chipiga, V.; Workman, A.; Ayas, C.; Cui, R.Y.; Cui, D.; Song, K.; et al. Coal transitions—Part 1: A systematic map and review of case study learnings from regional, national, and local coal phase-out experiences. Environ. Res. Lett. 2021, 16, 113003. [Google Scholar] [CrossRef]

- Antosiewicz, M.; Nikas, A.; Szpor, A.; Witajewski-Baltvilks, J.; Doukas, H. Pathways for the transition of the polish power sector and associated risks. Environ. Innov. Soc. Transit. 2020, 35, 271–291. [Google Scholar] [CrossRef]

- Heinrichs, H.U.; Schumann, D.; Vögele, S.; Biß, K.H.; Shamon, H.; Markewitz, P.; Többen, J.; Gillessen, B.; Gotzens, F.; Ernst, A. Integrated assessment of a phase-out of coal-fired power plants in Germany. Energy 2017, 126, 285–305. [Google Scholar] [CrossRef]

- Campiglio, E. Beyond carbon pricing: The role of banking and monetary policy in financing the transition to a low-carbon economy. Ecol. Econ. 2016, 121, 220–230. [Google Scholar] [CrossRef] [Green Version]

- Caldecott, B.; Tilbury, J.; Carey, C. Stranded Assets and Scenarios: Discussion Paper; Smith School of Enterprise and the Environment, University of Oxford: Oxford, UK, 2014. [Google Scholar]

- Feridun, M.; Güngör, H. Climate-related prudential risks in the banking sector: A review of the emerging regulatory and supervisory practices. Sustainability 2020, 12, 5325. [Google Scholar] [CrossRef]

- Bolton, P.; Kacperczyk, M. Do investors care about carbon risk? J. Financ. Econ. 2021, 142, 517–549. [Google Scholar] [CrossRef]

Figure 1.

Energy generation capacities in the Polish energy mix according to different forecast scenarios: 2030 versus 2050 (in GWe). Authors’ elaboration based on Forum Energii data (forum-energii.eu).

Figure 1.

Energy generation capacities in the Polish energy mix according to different forecast scenarios: 2030 versus 2050 (in GWe). Authors’ elaboration based on Forum Energii data (forum-energii.eu).

Figure 2.

Global reserves of coal. Bubbles represent North America, Latin America, Europe, Africa, CIS, India, China, Australia, and other Asian countries. Authors’ elaboration based on (International Energy Agency) IEA and EUROCOAL data.

Figure 2.

Global reserves of coal. Bubbles represent North America, Latin America, Europe, Africa, CIS, India, China, Australia, and other Asian countries. Authors’ elaboration based on (International Energy Agency) IEA and EUROCOAL data.

Figure 3.

Years of global coal, oil, and natural gas left, reported as the reserves-to-product (R:P) ratio, which measures the number of years of production left based on the known reserves and annual production levels in 2015. Note that these values can change with time based on the discovery of new reserves and changes in annual production. Authors’ elaboration based on the BP Statistical Review of World Energy 2016.

Figure 3.

Years of global coal, oil, and natural gas left, reported as the reserves-to-product (R:P) ratio, which measures the number of years of production left based on the known reserves and annual production levels in 2015. Note that these values can change with time based on the discovery of new reserves and changes in annual production. Authors’ elaboration based on the BP Statistical Review of World Energy 2016.

Figure 4.

Global production of coal. Upper panel presents the largest coal producers in 2020, whereas the lower panel depicts the evolution of coal production for the top global producers since 1990. Authors’ elaboration, based on Enerdata.

Figure 4.

Global production of coal. Upper panel presents the largest coal producers in 2020, whereas the lower panel depicts the evolution of coal production for the top global producers since 1990. Authors’ elaboration, based on Enerdata.

Figure 5.

Trends in future demand for coal according to different climate scenarios. Authors’ elaboration based on [16] and publicly available data in ZENODO available at: https://doi.org/10.5281/zenodo.4629991 (accessed on 20 October 2021).

Figure 5.

Trends in future demand for coal according to different climate scenarios. Authors’ elaboration based on [16] and publicly available data in ZENODO available at: https://doi.org/10.5281/zenodo.4629991 (accessed on 20 October 2021).

Figure 6.

Installed coal power capacity forecast by region, global, 2019–2030. Authors’ elaboration based on Frost and Sullivan, 2021.

Figure 6.

Installed coal power capacity forecast by region, global, 2019–2030. Authors’ elaboration based on Frost and Sullivan, 2021.

Figure 7.

Evolution of coal price indexes for coal futures contracts settlements based upon the price of coal delivered into Amsterdam, the Rotterdam region in the Netherlands, and the Antwerp region in Belgium (Argus/McCloskey API 2 Index), or loaded at the Richards Bay Coal Terminal in South Africa (Argus/McCloskey API 4 Index). Authors’ elaboration based on Refinitiv EIKON data.

Figure 7.

Evolution of coal price indexes for coal futures contracts settlements based upon the price of coal delivered into Amsterdam, the Rotterdam region in the Netherlands, and the Antwerp region in Belgium (Argus/McCloskey API 2 Index), or loaded at the Richards Bay Coal Terminal in South Africa (Argus/McCloskey API 4 Index). Authors’ elaboration based on Refinitiv EIKON data.

Figure 8.

Annual contract price forecasts for hard coking coal (USD/tonne), FOB Australia. Forecast accurate as of September 2021. Authors’ elaboration based on Refinitiv EIKON data.

Figure 8.

Annual contract price forecasts for hard coking coal (USD/tonne), FOB Australia. Forecast accurate as of September 2021. Authors’ elaboration based on Refinitiv EIKON data.

Figure 9.

Installed electric capacity by source (2020, %). Authors’ elaboration based on Enerdata.

Figure 10.

Quotations of the PSCMI 1/T of the Polish Power Coal Market Index 1 for sale to commercial and industrial power plants. Authors’ elaboration based on Agencja Rozwoju Przemysłu S.A. data.

Figure 10.

Quotations of the PSCMI 1/T of the Polish Power Coal Market Index 1 for sale to commercial and industrial power plants. Authors’ elaboration based on Agencja Rozwoju Przemysłu S.A. data.

Figure 11.

Operating surpluses for coal mining sector (panel a) and energy generation and distribution sector (panel b). Figures in nominal USD billions, forecasts for 2021 and 2022. Authors’ elaboration based on Oxford Economics/EMIS data.

Figure 11.

Operating surpluses for coal mining sector (panel a) and energy generation and distribution sector (panel b). Figures in nominal USD billions, forecasts for 2021 and 2022. Authors’ elaboration based on Oxford Economics/EMIS data.

Figure 12.

Operating revenue of companies operating within the coal industry in Poland. The left panel presents the heatmap for the energy generation and distribution sectors; the right panel benchmarks firms in the coal-mining sector. Authors’ elaboration based on EMIS data.

Figure 12.

Operating revenue of companies operating within the coal industry in Poland. The left panel presents the heatmap for the energy generation and distribution sectors; the right panel benchmarks firms in the coal-mining sector. Authors’ elaboration based on EMIS data.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Valuation multiples for Polish companies operating within the coal industry.

| PGE S.A. | 12-Month Average | 12-Month Average—Utilities | 12-Month Average Electric Utilities and IPPs |

| EV/Sales | 0.5 | 8.3 | 1.1 |

| EV/EBITDA | 4.1 | 2.4 | 3.4 |

| P/E | 15.1 | 0.9 | 10.0 |

| Price/Cash flow | 3.1 | 0.9 | 2.9 |

| Price/Book | 0.4 | −0.2 | 0.5 |

| Earnings per share: 5-year historic growth | −11.70% | 9.50% | |

| Revenue: 5-year historic growth | 9.90% | 4.80% | |

| JSW S.A. | 12-Month Average | 12-Month Average—Energy Sector | 12-Month Average Coal Sector |

| EV/Sales | 0.7 | 1.1 | 0.5 |

| EV/EBITDA | 4 | 3.4 | 2.6 |

| P/E | 15.1 | 10 | 6.6 |

| Price/Cash flow | 3.1 | 4.1 | 2.9 |

| Price/Book | 0.5 | 0.5 | |

| Earnings per share: 5-year historic growth | 100.1% | 41.3% | |

| Revenue: 5-year historic growth | 0.2% | −0.21% |

Authors’ elaboration, based on Refinitiv-EIKON data.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Karpa, W.; Grginović, A. (Not So) Stranded: The Case of Coal in Poland. Energies 2021, 14, 8476. https://doi.org/10.3390/en14248476

AMA Style

Karpa W, Grginović A. (Not So) Stranded: The Case of Coal in Poland. Energies. 2021; 14(24):8476. https://doi.org/10.3390/en14248476

Chicago/Turabian StyleKarpa, Waldemar, and Antonio Grginović. 2021. "(Not So) Stranded: The Case of Coal in Poland" Energies 14, no. 24: 8476. https://doi.org/10.3390/en14248476

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.