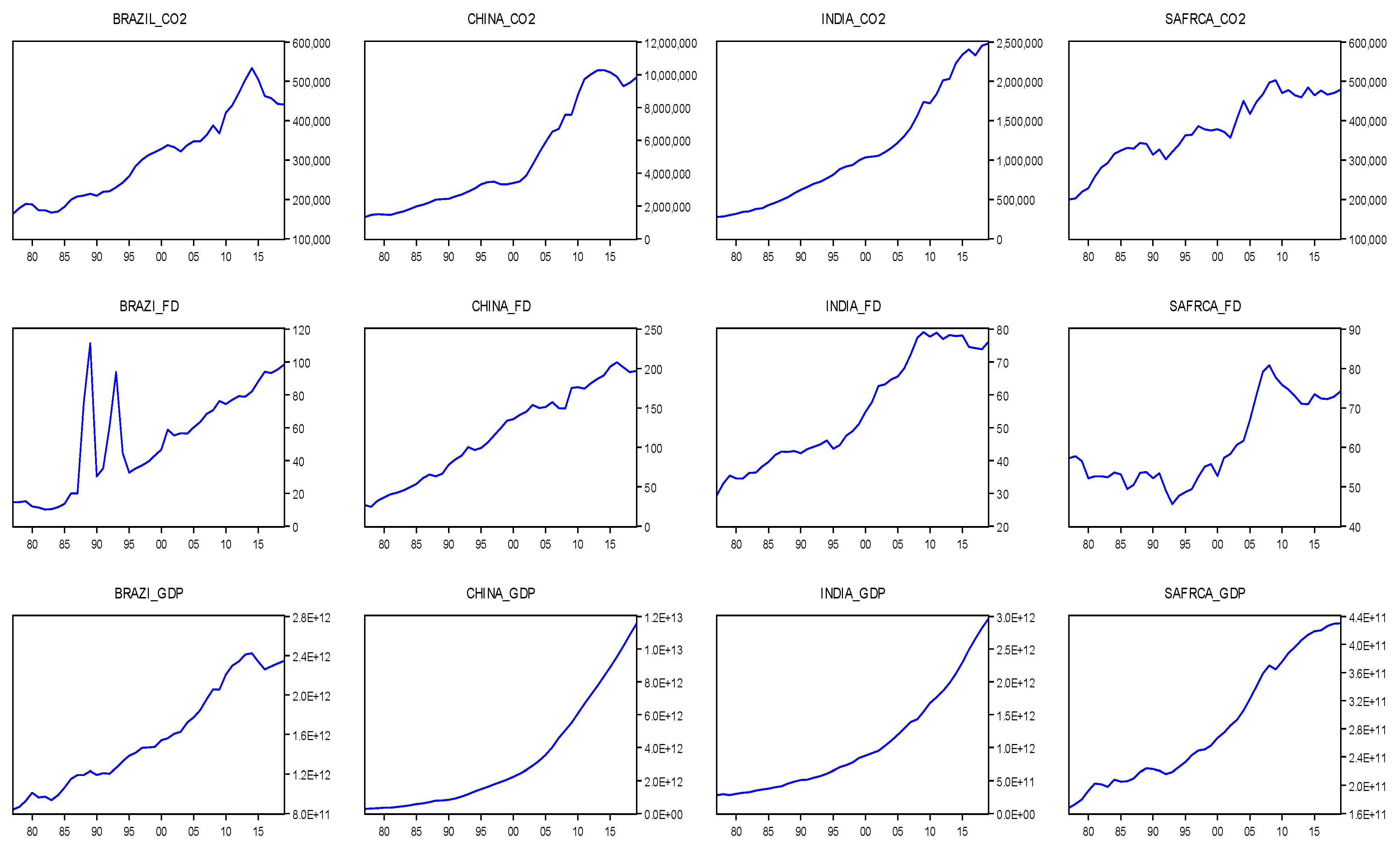

1. Introduction

The BRICS countries are Brazil, Russia, India, China, and South Africa. The abbreviation, BRICS, which was coined by Jim O’Neil of Goldman Sachs in a 2001 report, is used because of its similarity to the English word “brick”. It has been 20 years since the concept of BRICS countries was put forward. In the past 20 years, the BRICS countries have achieved rapid economic growth. According to the latest statistics, the total population of the BRICS countries is approximately 3.178 billion, accounting for approximately 41.42% of the world’s total population (The data calculated by the author comes from:

https://www.statista.com/studies-and-reports/ (assessed on 18 June 2021)). The total gross domestic product (GDP) of the BRICS countries accounts for about 22.45% of the world’s total GDP. Moreover, as countries cooperate with each other in many fields, the world economy has gradually improved.

However, rapid economic development is often accompanied by a large amount of energy consumption and CO2 emissions. CO2 emissions from human activities have become an important source of global warming, accounting for about 77% of global greenhouse gas emissions. As the world’s largest emerging economies, the BRICS countries have experienced a significant increase in CO2 emissions. In 2019, the carbon dioxide emissions of the BRICS countries amounted to 14,759 billion tons, accounting for about 43.19% of the world’s total CO2 emissions. However, the BRICS countries have made varying degrees of effort to reduce their carbon dioxide emissions. China is a responsible country; it released a plan in 2014, which projected that by 2020, it will achieve the goal of reducing its CO2 emission intensity by 40% to 45% compared to 2005. This goal has been achieved. As the CO2 emissions of the entire BRICS countries account for more than two-fifths of the world’s CO2 emissions, paying attention to the influencing factors of CO2 emissions in the BRICS countries will not only alleviate the pressure of global CO2 emission-reduction, but also help promote the sustainable development of the countries’ economies.

The economic development of a country is a prerequisite for financial development; thus, financial development is the result of a country’s economic development, and the inevitable product of the development of commodity currency. It is precisely because of the inseparable relationship between the economic development and financial development that almost every country’s macro and micro economic research mentions them almost every time. In recent years, the BRICS countries have also cooperated in the currency market and capital market, and have made considerable progress. Although there are many challenges with this system of cooperation, in today’s economic globalization, it is also a good trend to promote high-quality development through win-win cooperation.

As financial development is the core driving force of a country’s economy, it is a necessary factor to consider in achieving a low-carbon economy. For instance, financial development can improve technological innovation and reduce energy consumption, thereby reducing CO

2 emissions. However, financial development may also contribute to the deterioration of the environment and increase CO

2 emissions. Moreover, financial development makes it easier for companies to raise funds and expand reproduction, which will increase consumer consumption of household appliances and increase CO

2 emissions. In terms of the joint development of economy, finance and carbon dioxide emissions, to build a green and low-carbon circular development economic system, cultivate green and low-carbon industries, increase the demand for carbon finance, and tilt investment and financing to green projects as much as possible. Intensify efforts to adjust the economic and industrial structure, vigorously increase support for low-carbon sectors, in-depth promote technological innovation, model innovation, and management innovation, vigorously develop clean energy construction, and enhance the real economy’s market for green finance including carbon finance demand is the trend of global development, and the BRICS countries should also follow this trend for policy construction. The question this now raises is what kind of relationship exists between financial development, economic growth, and the reduction of CO

2 emissions? This paper responds to this question through empirical analysis. The remaining parts of the paper are as follows:

Section 2 is a literature review, and

Section 3 describes the financial development, economic growth, and CO

2 emissions of the BRICS countries.

Section 4 is the research method.

Section 5 is discussions and conclusions.

3. Analysis of the Economic Growth, Financial Development and CO2 Emissions of the BRICS Countries

3.1. Analysis of Economic Growth

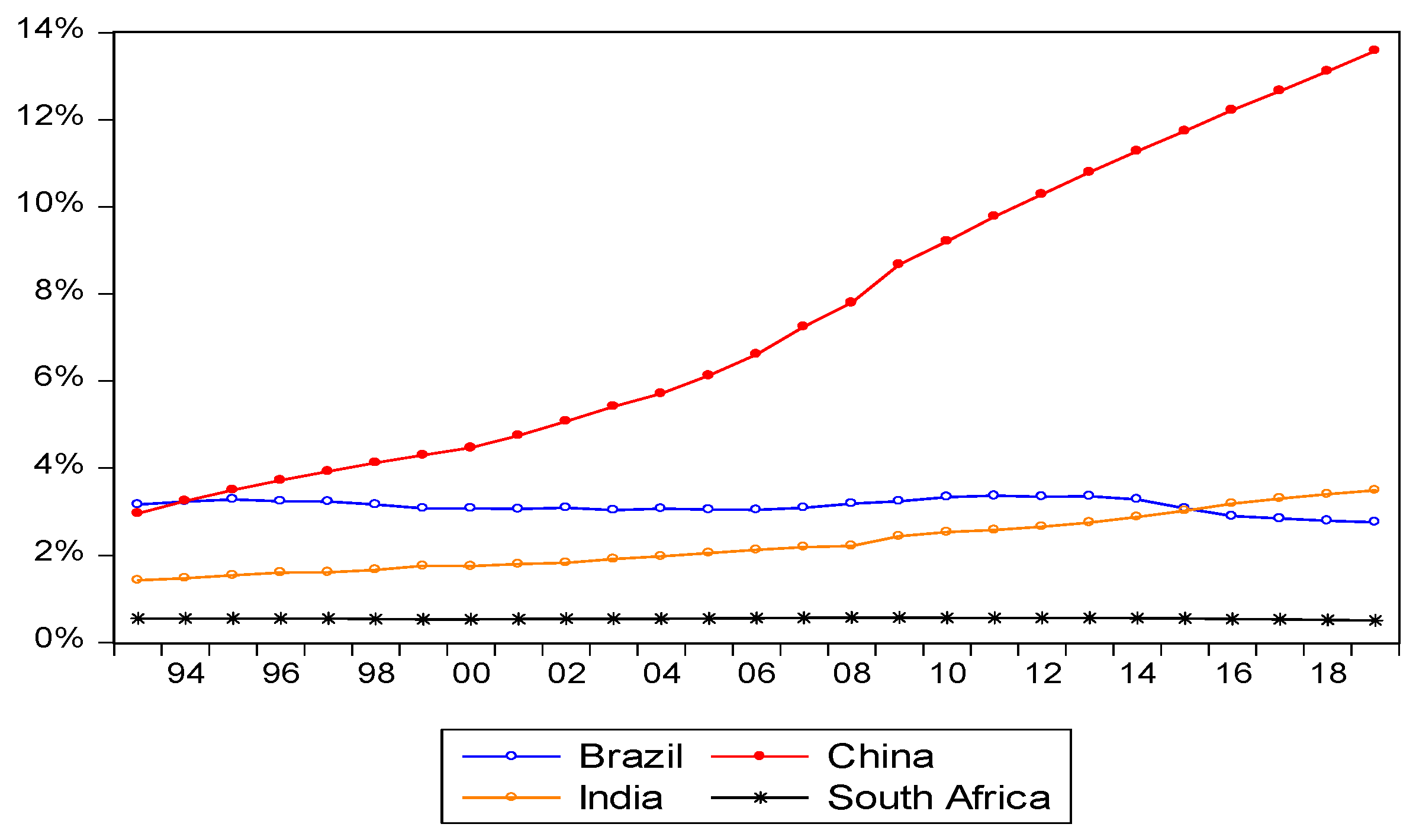

From

Figure 1, it is evident that between 1993 and 2019, the GDP of the BRICS countries accounted for approximately 22% of the world’s total GDP. Although the global financial crisis occurred in 2008, various countries around the world were affected to varying degrees. Although the BRICS countries also suffered some impacts, leading to a decline in their GDP, they recovered quickly after the crisis. In the 27 years from 1993 to 2019, the country with the largest share of the global GDP of the BRICS countries was China, followed by India. Although the economic strength of the BRICS countries continues to develop, their share of the total economy of world continues to increase. However, because different countries have different developments, China and India account for a higher proportion of GDP compared to the other three countries based on this indicator. Nevertheless, the other three countries still have a lot of room for development.

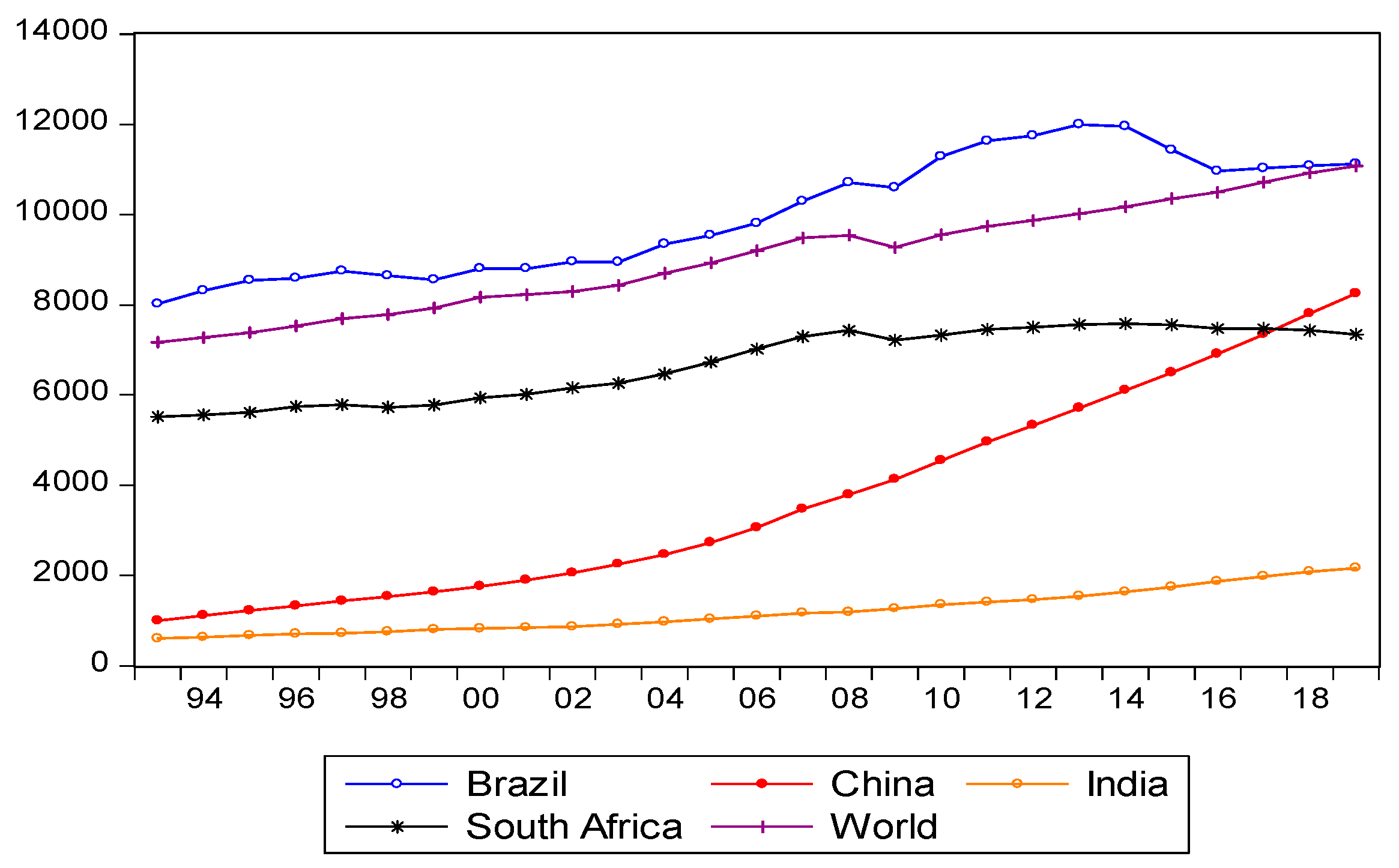

Although China and India account for a relatively large total GDP and rank high among the BRICS countries, they also have large populations. Looking at their per capita GDP, they may not be the top few. According to the per capita GDP graph in

Figure 2, Brazil ranks first, which is higher than the world average, while China only caught up with South Africa in second place in the last two years. India’s, a low-middle-income country, has a total population of over 1.35 billion. Its per capita GDP only slightly exceeds US

$2000, the lowest among the BRICS countries. The global per capita GDP is about US

$11,300 and India’s per capita is only 17% of the global per capita.

China’s per capita GDP has increased, but has not reached the global average, which is about US$9800. However, according to China’s economic growth rate and the slowdown in population growth, China’s per capita GDP is also slowly increasing, and it is likely to reach the world average level in the future. Therefore, the economic strength of the five countries can be viewed from different angles and different conclusions can be drawn.

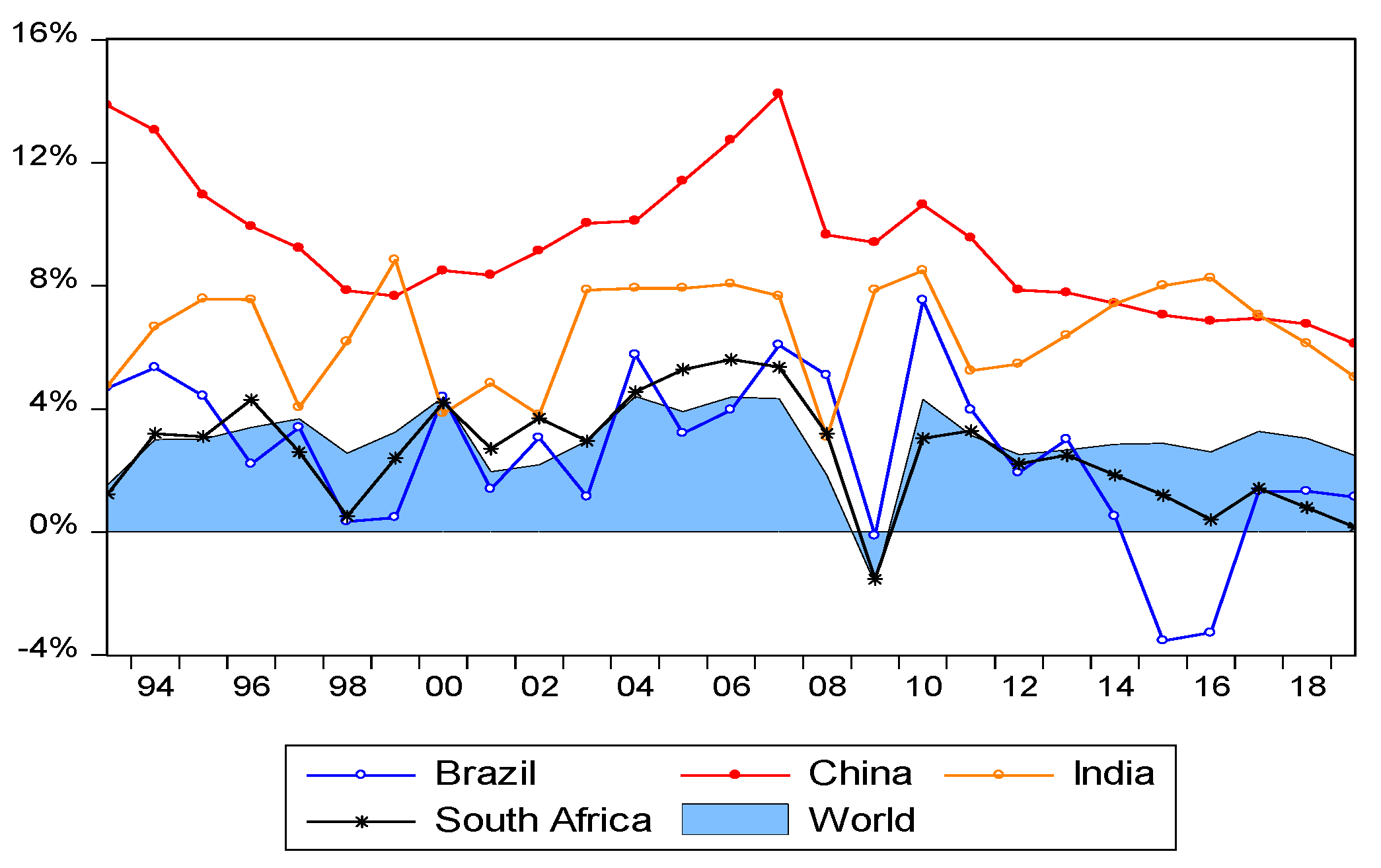

From

Figure 3,

Table 1, it can be seen that between 1993 and 2019, the average GDP growth rate of the BRICS countries was about 4.56%, which is higher than the world average GDP growth rate; this shows that the BRICS countries have indeed developed rapidly. It is worth noting that under the circumstances of the 2008 financial crisis, although the economic growth rates of various countries have declined and many countries have even experienced negative growth, China still maintains a growth rate of 9.4%. India’s growth rate at that time was also positive.

In statistics, the average value can reflect the overall data level during the time period and the standard deviation can reflect the volatility of the data. This is expressed in

Table 1 below, which combines the data from each country in

Figure 1,

Figure 2 and

Figure 3.

The average annual GDP growth rate of China is 9.37%, which is about 6.45% higher than the world’s average GDP growth rate. After 1994, the total GDP surpassed that of several other countries and became the first. More interestingly, data from the BRICS countries show that under the global financial crisis triggered by the subprime mortgage crisis in 2008, almost all the economic growth rates of the BRICS countries were negative, but the GDP growth rate of China was still positive. Although the GDP growth rate had declined in those years, the average value remained between 6% and 7%.

India’s growth rate is relatively stable, with an average growth rate of 6.51% for more than two decades due to its large population, although its per capita GDP ranks last among the BRICS countries. However, since 2009, it has also become the second largest country in terms of GDP among the BRICS countries. The average growth rate of India’s GDP is around 6.51%, which is higher than the world’s GDP growth rate. India’s GDP growth rate has the smallest fluctuation among the BRICS countries. Under the influence of the 2008 subprime mortgage crisis, although India’s growth rate declined, it was still positive. Because of the impact of the financial crisis, India’s growth rate slowly returned to the pre-financial crisis level after 2013.

Brazil’s per capita GDP ranked first among the five countries from 1993 to 2006. From 2000 to 2010, Brazil’s economy achieved rapid development with the help of its government’s active economic policies and a better international market environment. After Lula took office as president, he introduced a series of policies conducive to the development of the Brazilian market. Under the guidance of pragmatism, Brazil ushered in a new period of prosperity and development. However, Brazil’s negative economic growth in 2015 and 2016 was due to the fact that the Brazilian government did not take timely response measures to the economic situation at the time. They adjusted public financial expenditures and reduced welfare policies that were too “developed,” leading to hyperinflation, high unemployment, and social instability. Fifteen years of Brazilian political turmoil, coupled with the Brazilian government’s fiscal austerity policy and interest rate hike measures have made the economy even worse.

South Africa is the largest economy in Africa, although the total GDP is at the bottom of the five countries. However, most of the GDP per capita ranks third. It is one of the most influential countries in Africa. South Africa is an upper middle-income economy with rich mineral resources. However, due to serious flaws in South Africa’s business model based on mining and primary manufacturing, economic growth has not increased. The data also showed that the GDP growth rate is very stable. The standard deviation is second only to India. Since South Africa joined the BRICS in 2010, it has also brought new vitality to the BRICS countries, and, at the same time, has strengthened its own vitality in participating in the cooperation between the BRICS countries. After the 2008 financial crisis, South Africa stimulated its economy by rewarding interest rates. In terms of fiscal policy, the South African government increased government budget investment, and then the GDP growth rate returned to the pre-financial crisis level the following year.

3.2. Analysis of Financial Development

3.2.1. Analysis of the General Situation of Financial Development

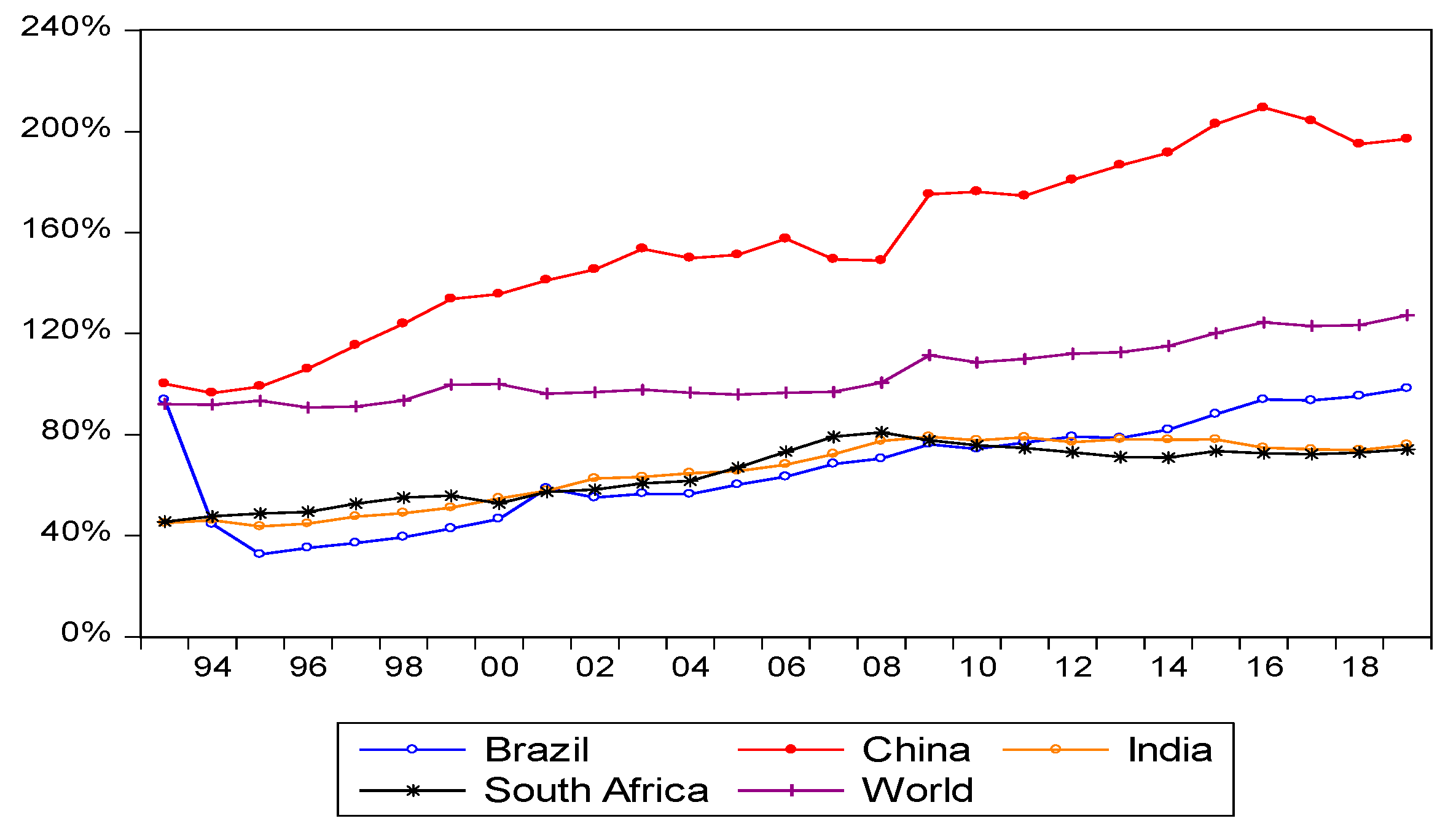

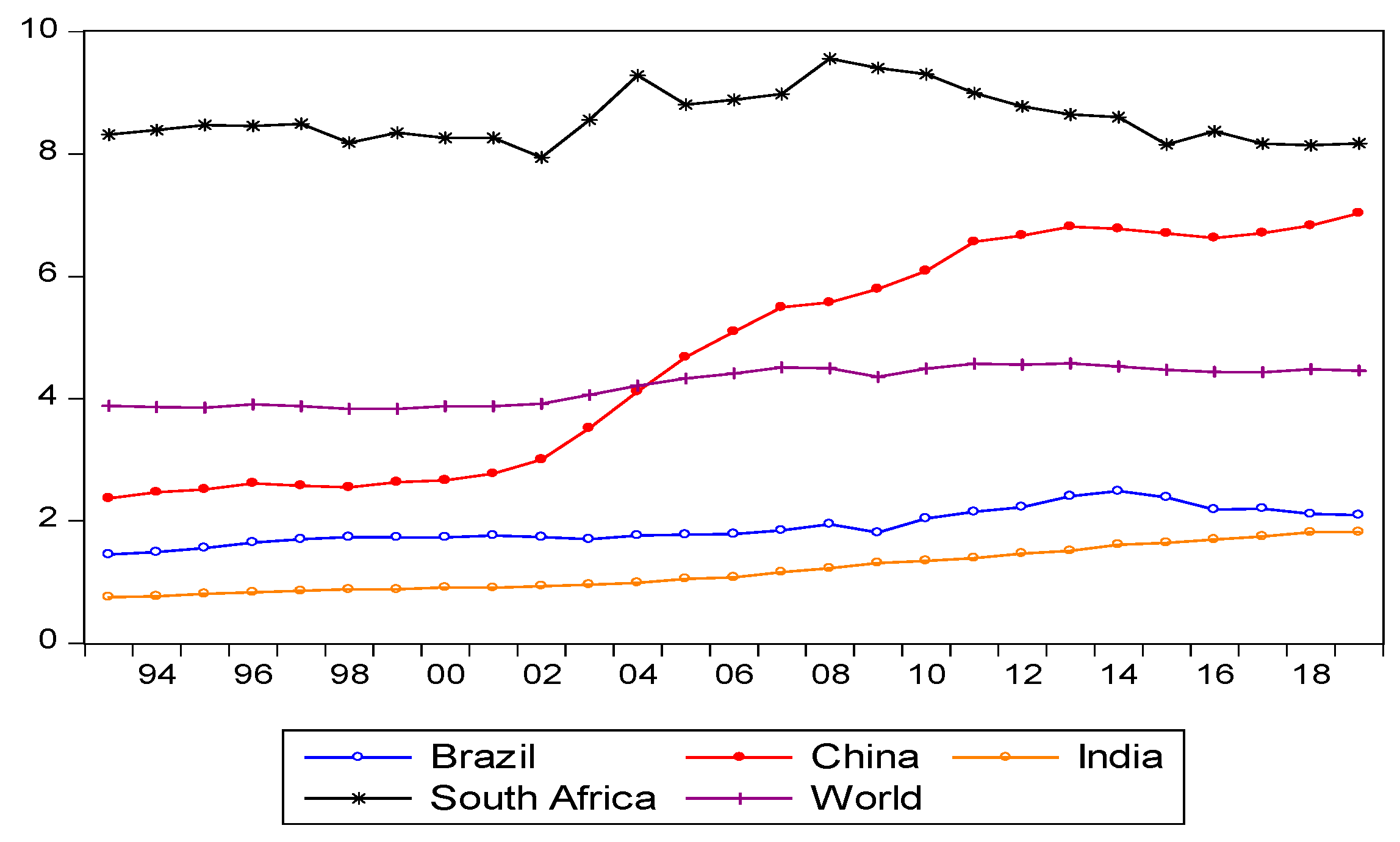

The ratio of M2/GDP is usually used to compare the degree of financial deepening, because M2 is the quantity of money and the stock and GDP is the gross domestic product, a flow concept. The ratio of the two measures the stock of money required per unit of output. It can also reflect a country’s macro level of development.

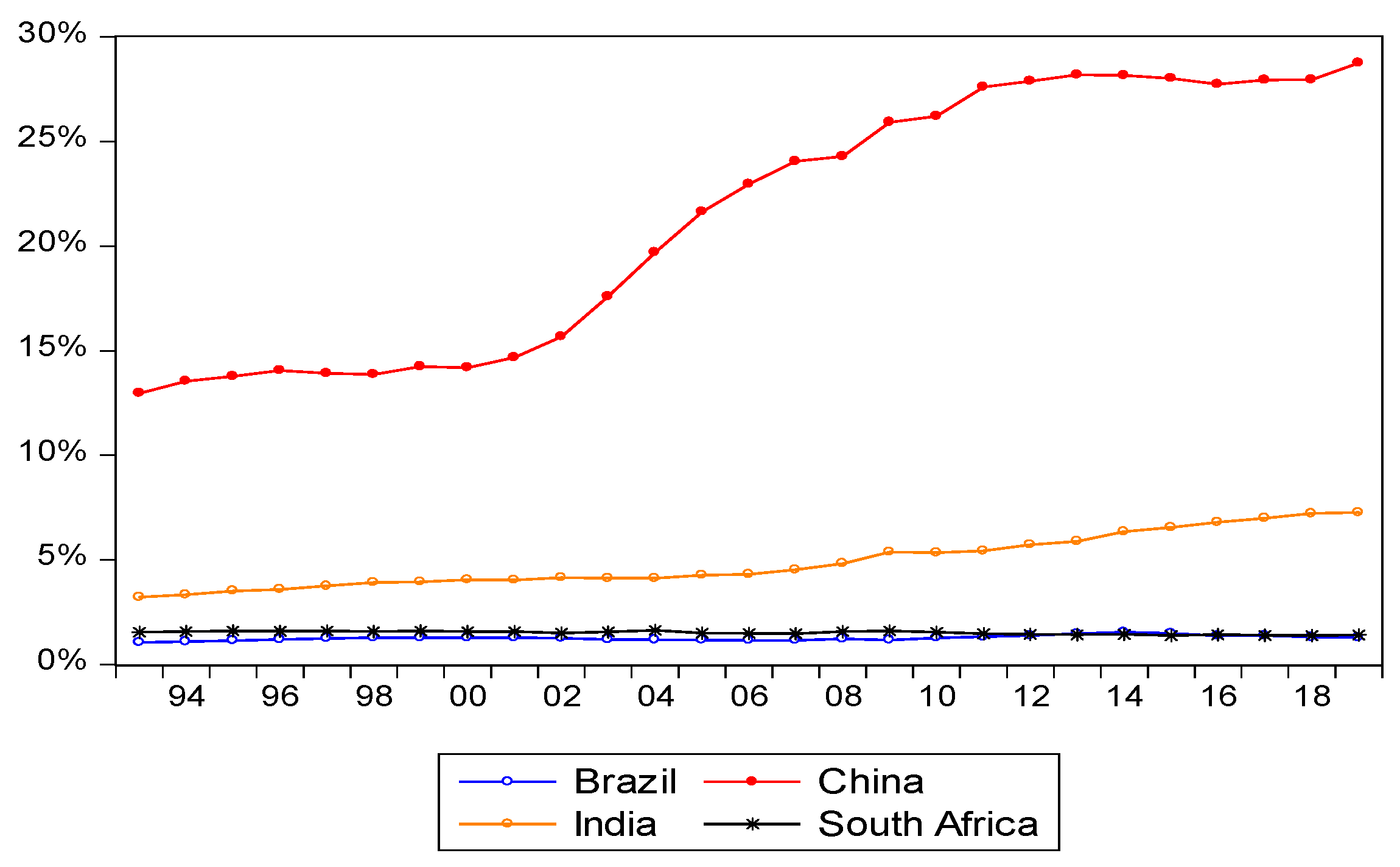

From

Figure 4, it is clear that this indicator of the BRICS countries is increasing as a whole, indicating that the macro development trend is relatively good. However, the indicator plummeted in Brazil from 1993 to 1995 because Brazil experienced hyperinflation again at that time. The Brazilian government announced the implementation of “the Real Economic Plan” in order to subdue the hyperinflation. The plan is to ensure the relative currency in circulation in the market. Regarding stability, the government has taken measures to strictly restrict currency issuance. However, looking at the number of national indicators alone, China’s indicator is the highest, which also reflects that the scale of China’s financial development is the highest among the BRICS countries and is higher than the world average. Brazil, India, and South Africa have similar levels of this indicator.

3.2.2. Analysis of the Development of the Banking Industry

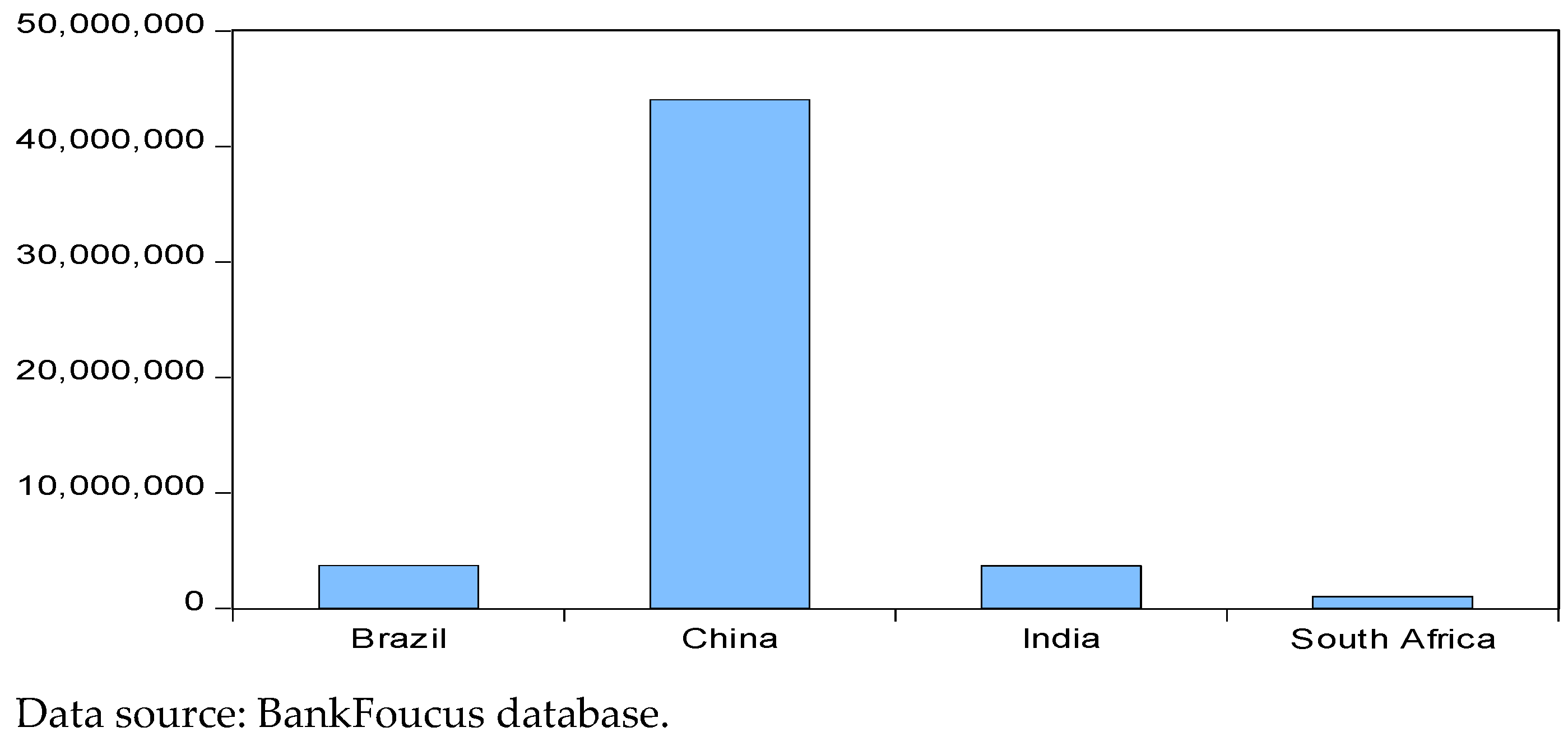

From

Figure 5, it can be seen that the total asset level of the banking industry in the BRICS countries is different, and the number of banks in each country is also different. The figure also shows that the total assets of China’s banking industry are much higher than those of the other four countries, which is also largely related to China’s population and financial industry development history.

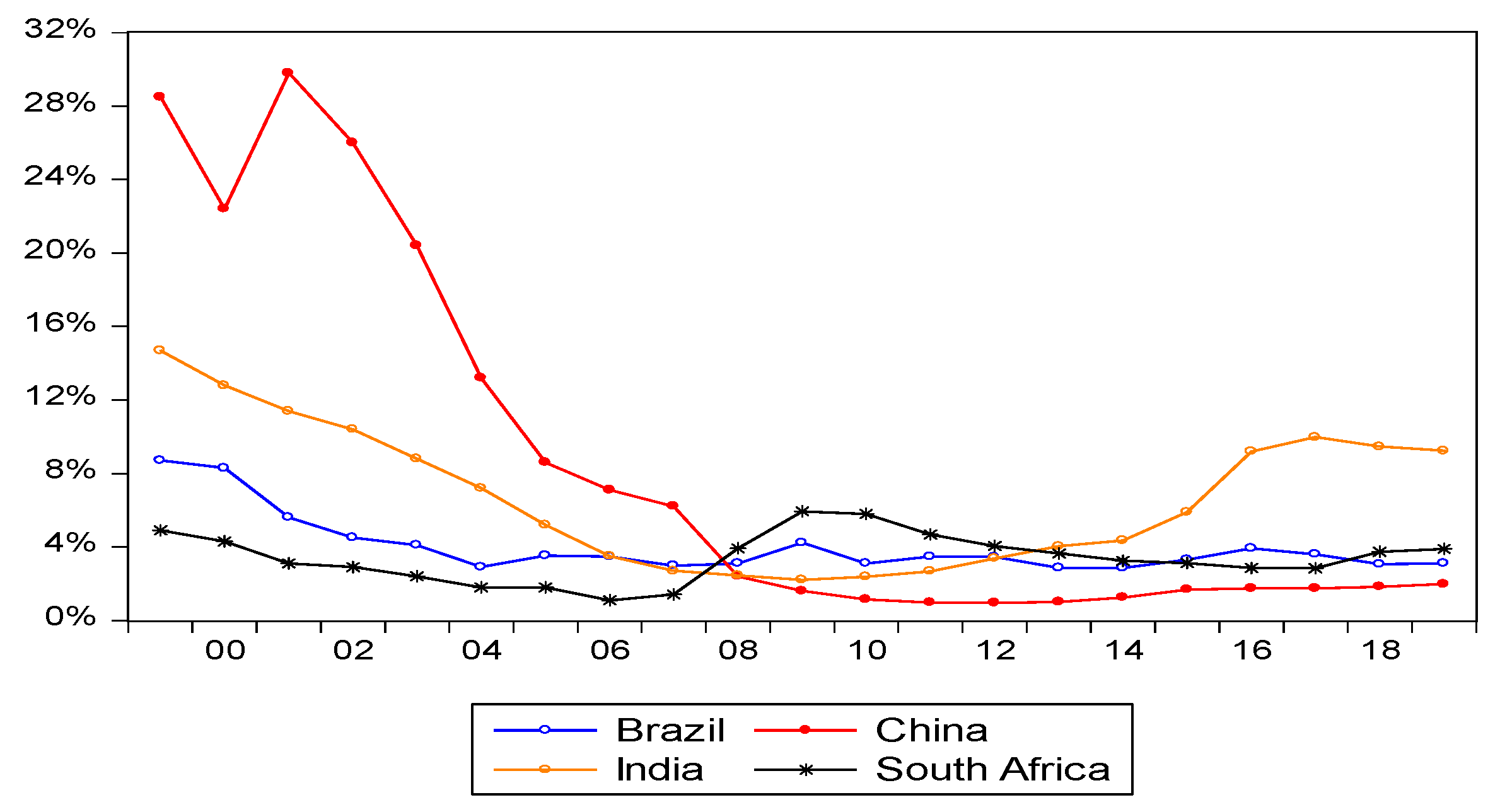

Table 2 indicates that there are many banking institutions in China. As seen in

Figure 6, China’s non-performing loan rate has not always been low. In 1999 and 2001, the non-performing loan rate was as high as about 30%. The level has a certain relationship with the national regulatory standards at that time.

Regarding the development of the banking, the Brazilian banking system was established in the 1960s. An important feature of the Brazilian banking industry is its high degree of monopoly. Over 50% of domestic commercial institutions in Brazil are almost entirely owned by Brazil’s top eight domestic commercial banks. This has also led to the low status of the remaining small and medium-sized commercial banks. With its good response to the 2007 financial crisis, the Brazilian Commercial Bank became a safe haven. After the financial crisis, Brazilian banks actively seized opportunities to cooperate with emerging markets, and at the same time encouraged private finance. The development of institutions and the development of the domestic banking industry have entered a fast lane, which is worth learning from the BRICS.

After the reform and opening up, the banking industry of China embarked on the right track of development. A modern banking system based on central banks, policy banks, and commercial banks was gradually established. Commercial banks are divided into large state-owned commercial banks and state-level commercial banks. Commercial banks, urban commercial banks, and rural credit cooperatives formed a relatively complete banking system. At the same time, there are problems in the development of the banking industry of China. Affected by the narrowing interest rate differentials and financial disintermediation, the profitability of the banking industry has decreased; the total loan and total assets have a decreasing trend, and the mismatch of the decreasing trend has aggravated the unreasonable structure of the banking industry’s assets and liabilities. China has gradually implemented “Basel III” and the requirement for capital adequacy ratio has been further increased. This is yet another challenge for the banking industry. In short, for commercial banks, the era of rapid growth has passed. With the tightening of supervision, coupled with the shortage of funds, the pressure on profits and assets, and liabilities faced by banks, banks are forced to find new outlets. However, it depends on the situation. In the final analysis, the economic recovery of China and upgrading of consumption structure provide opportunities for the transformation and development of commercial banks.

After India’s independence, the development of its banking industry can be divided into three stages: the privatization stage, the rise of nationalization, and the development of the Indian banking industry. In the 1990s, due to the Asian financial crisis in 1997, the reform of the industrial division of the Indian banking industry went through further changes. Until this day, the Indian banking industry has maintained a hierarchical banking system. A major characteristic of the Indian banking industry is its rural banking system. India is committed to providing sufficient credit funds for rural development. Therefore, it has established targeted regional rural banks and a long-standing rural cooperative financial system. The industry proposed relevant financial policies, such as the KISAN credit card plan and the recently launched “inclusive finance.” These measures have led to certain achievements at the same time they have paid a relatively high price. South Africa’s banking system is relatively developed and complete, far ahead of other emerging economies, and not inferior to developed economies. Its banking industry has introduced a complete business system covering commercial banks, merchant banks, retail banks, insurance, and securities. Electronic banking equipment is covered all over the country and Automatic Teller Machine equipment and online banking services are popularized throughout the country.

In summary, the overall development of the banking industry in the BRICS countries is relatively fast, but due to their own development history, their development is facing different difficulties. This is a problem that all countries need to solve.

3.2.3. Analysis of the Development of the Securities Market

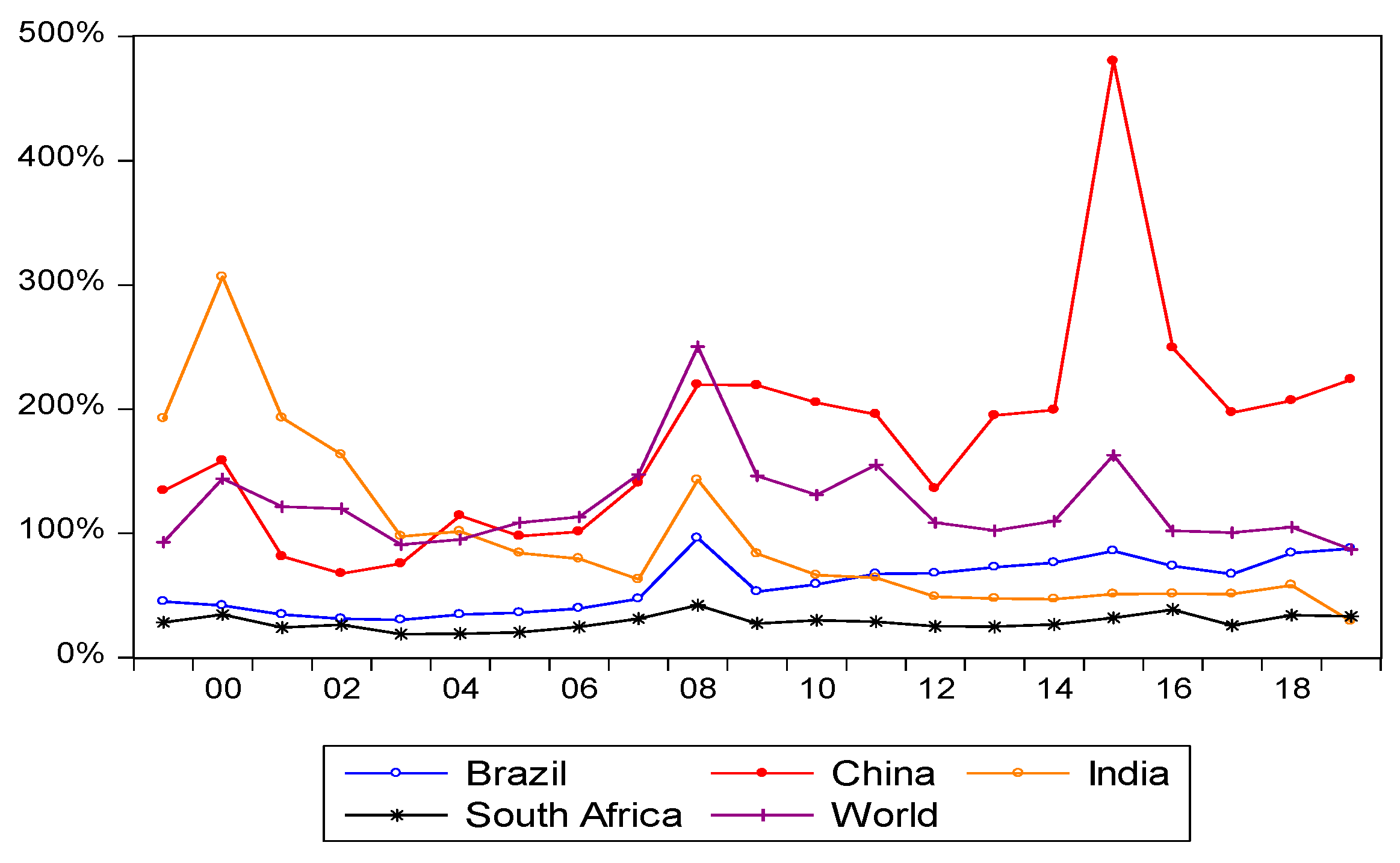

Stock transaction turnover rate refers to the total amount of stock transactions within a certain period divided by the average market value of listed companies during that period. In

Figure 7, from 2006 to 2007, the stock market was in good condition because of the bull market globally, and almost all global stock markets were rising. In 2008, the bear market was accompanied by the emergence of the financial crisis, and global stock markets fell. After the bull market in China in 2009, the stock market became volatile for five consecutive years. As the stock market had a certain linkage effect, during China’s bull market in 2015, the stock market turnover rate of other countries in the world increased accordingly. As of 2019, the stock turnover rate of the BRICS countries is higher than the world average, which shows that the stock markets of the BRICS countries are relatively active, of which China has the highest proportion, reflecting that the stock market is very active.

Because the development of the country is different, the development of the securities market in each country is also different. The development of the Brazilian securities industry can be traced back to the Brazilian Stock Exchange established in 1890. In the 1970s, in order to stimulate the development of the domestic securities market, Brazil introduced a large number of foreign investors, and its investment scale once reached 25%. However, after the financial crisis, foreign investors withdrew one after another, thereby causing violent fluctuations in the Brazilian securities market, and affected the country’s economic development. It can be seen that the economic development of a country cannot rely too much on foreign investment, and the BRICS countries should use this as a warning. Brazil Futures Exchange and Sao Paulo Stock Exchange underwent shareholding reforms in 2007 and merged into Brazil Stock Exchange. The newly established exchange has a wealth of trading varieties and adopts electronic trading methods. As of 2011, it has become the world’s twelfth largest fund-raising market with huge development potential.

The development of the securities industry of China began with the reform and opening up in 1978. The Shenzhen Stock Exchange and Shanghai Stock Exchange, established on 1 and 18 December 1990, are milestones in the development of China’s securities industry. As of May 2018, the number of companies listed on the Shenzhen Stock Exchange has reached 2112, and the total market value of A-shares has reached 335.256 billion US dollar. The number of companies listed on the Shanghai Stock Exchange has continued to grow. The number of listed companies on the Shanghai Stock Exchange reached 1423, and the total market value of A-shares reached 4730.259 billion US dollar. Yuan, far ahead of other BRICS countries: In the field of stock trading, the small and medium board of directors established in 2004 and the ChiNext board of directors established in 2009 facilitated the financing of small-sized and medium-sized enterprises and innovative companies. As of May 2018, there are 911 listed companies on the small-sized and medium-sized board and 725 listed companies on the GEM, which are indistinguishable from the mainboard market: as far as the types of transactions are concerned, not only stocks can be traded, but also funds, bonds, convertible bonds, ETFs, and warrants.

In terms of trading scope, the Shanghai–Hong Kong Stock Connect opened in 2014 and the Shenzhen–Hong Kong Stock Connect opened in 2016 and have expanded the investment scope of Chinese investors and provided international choices. At the same time, in recent years, with the increase in national income, the enthusiasm of the whole society for securities investment has gradually increased. At the same time, the regulatory agencies have taken more effective measures to regulate their development in accordance with the changes in reality.

However, it is important to note the issues affecting the development of China’s securities industry. Securities companies have a relatively simple way of making profits, mainly relying on traditional businesses such as securities brokerage and self-operation of securities. Compared with the securities industry in developed economies, the scale of China’s securities industry is small. The investment variety is too small and diversified services cannot be realized. Thus, it cannot effectively diversify risks, nor attract capital, and expand profits. With the opening of the market, the influx of international institutions, competition, and insufficient innovation capabilities, it is difficult to keep up with the market. In some gray areas, such as private equity, insufficient supervision and risk can be easily induced, stockholders are unable to make rational investments, and the phenomenon of following the trend is obvious. These problems are restricting the further development of China’s securities industry.

India is the first country in Asia to have a stock exchange. Its first stock exchange, the Bombay Stock Exchange, was established in 1875. As of 2018, the number of listed companies reached 5648, and the number of listed companies reached 5985 between 2016 and 2017 (Data sources: NSE India (National Stock Exchange of India Ltd.;

https://www.nseindia.com/ (assessed on 18 June 2021)). The National Stock Exchange of India was established in November 1992 and is another major stock exchange in India. As of May 2018, more than 1300 stocks were traded, with a trading volume of 21.468 billion US dollar and a market capitalization of 33.101 billion US dollar, making it India’s largest stock exchange and the world’s third highest trading volume. It is evident that the Indian securities industry has impressive strength and huge development potential.

The South African Stock Market was established in 1887. The stock exchange was the Johannesburg Stock Exchange. At the beginning of the establishment, the exchange was mainly to raise funds for the development of gold mines. With the development, financing models and trading products gradually changed from mining stocks to financial stocks. As the largest equity market on the African continent, the market value of companies listed on the Fort Johannesburg Stock Exchange accounted for more than 70% of the market value of listed companies in Africa.

From the foregoing, it is clear that there are still gaps in the development of the securities industry in the BRICS countries; as their characteristics differ, so do their advantages, shortcomings, and development potential.

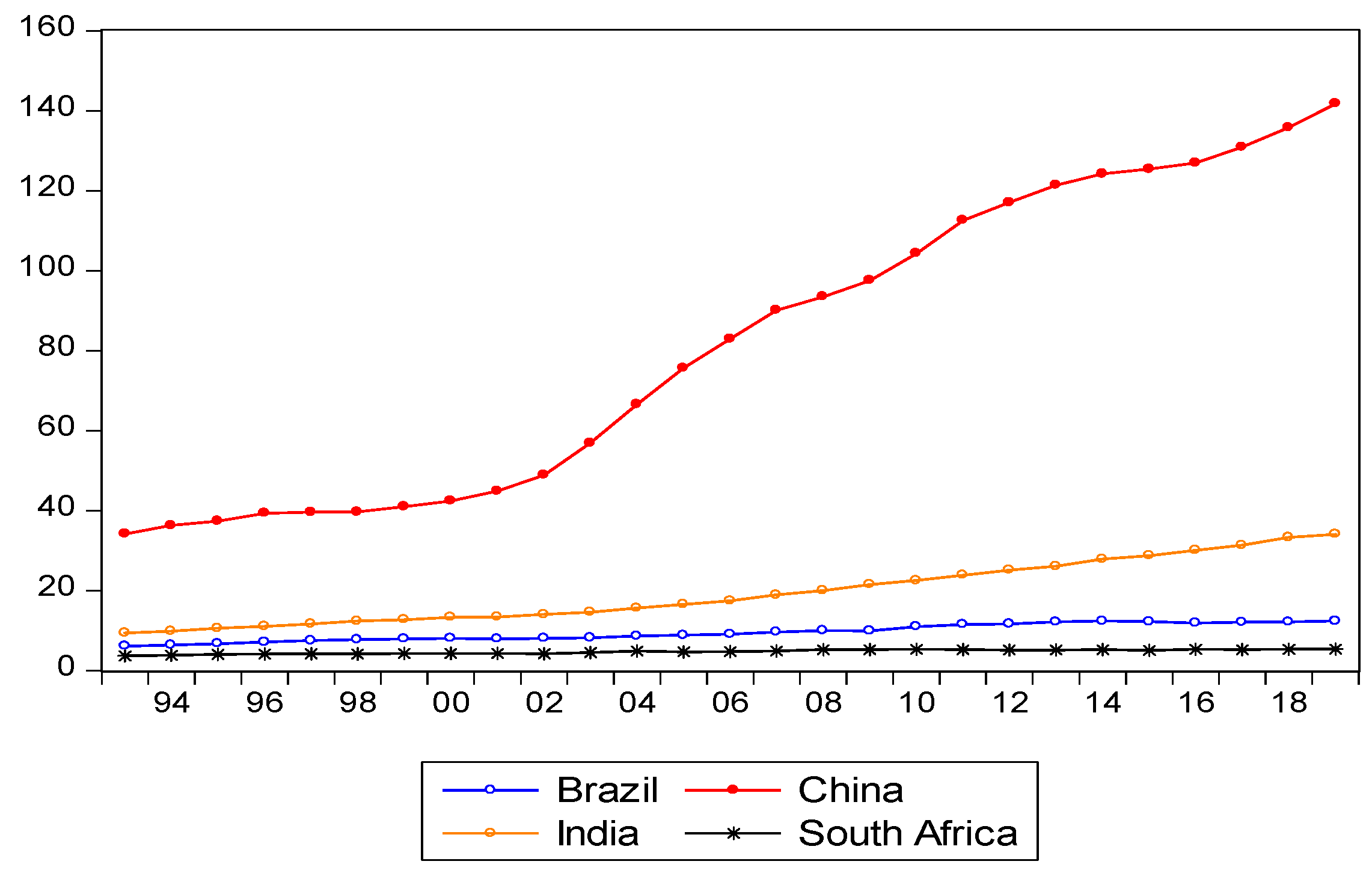

3.3. Analysis of CO2 Emissions

Economic development has brought about a large amount of waste discharge. CO

2 emissions are usually used to measure the world’s emission indicators, especially the “Kyoto Protocol” passed in Kyoto, Japan, in December 1997, which has aroused the global fanaticism about greenhouse gases (mainly CO

2). First of all, it can be seen, from

Figure 8, that from 1993 to 2019, the proportion of the BRICS countries in world CO

2 emissions increased year by year in China and India, while the changes in Brazil and South Africa were not particularly obvious. China, in particular, accounted for a relatively high proportion of CO

2 emissions in 1993. It has continued to strive for development in the course of exploration. The level of industrial development has gradually increased, and CO

2 emissions have also increased accordingly. By 2019, China’s total CO

2 emissions accounted for 28.76% of the world’s total CO

2 emissions, ranking first among the four BRICS countries. Although India’s global CO

2 emissions are much lower than China’s, it is likely to slowly increase in due course. India’s total CO

2 emissions worldwide accounted for 7.25% of the world’s total, ranking second among the BRICS countries. Compared to the other three countries, the CO

2 emissions of Brazil and South Africa are relatively small and there have been no significant changes. By 2019, South Africa’s total CO

2 emissions accounted for 1.40% of the world’s total CO

2 emissions, ranking fourth among the BRICS countries and Brazil’s total CO

2 emissions accounted for 1.29% of the world’s total emissions, ranking fifth among the BRICS countries.

The CO

2 emissions and energy use are also inextricably linked. As shown in

Figure 9, the energy consumption performance trend of the BRICS countries can be divided into two different stages according to time, the slow growth interval from 1993 to 2002 and 2004, and the range in which consumption has risen rapidly after the year. Among them, the fastest growing is China, which is also related to China’s rapid development after the 21st century. The main reason for the growth is the rapid growth of China’s energy consumption, which is consistent with the rapid development of its economy. India’s development is at a relatively steady pace and energy consumption is also relatively steady. Brazil and South Africa have slow growth in energy consumption, which is similar to the growth rate of their total CO

2 emissions.

Figure 10 shows that South Africa’s per capita carbon emissions are very high, and it has the highest per capita CO

2 emissions. South Africa has the second highest per capita CO

2 emissions account. It is rich in mineral resources; since the end of international sanctions in the early 1990s and the establishment of the new South Africa in 1994, the country’s economy has been in a state of steady growth.

China ranks third in CO2 emissions per capita. This is in line with the fluctuations in the overall increase in CO2 emissions per capita. Although China’s per capita carbon dioxide emissions in the 1990s were lower than the world average, China’s rapid development since the beginning of the 21st century after its accession to the World Trade Organization, led to the development of its manufacturing industries, resulting in rapid increases in its CO2 emissions. With China’s rapid development in the 21st century, the rise of industry and manufacturing required the support of large amounts of energy. As coal became the main energy fuel, carbon emissions increased quickly. Due to China’s large population, even if the per capita CO2 emissions are very low, the total amount would still be very large. Therefore, in recent years, China has continuously adopted energy-saving and emission-reduction measures to contribute to environmental protection.

Brazil and India ranked fourth and fifth, respectively. Brazil and India are emerging economies and their economic growth rates are relatively slow. Thus, the two countries are constantly exploring suitable development paths and striving to improve the level of development. The development process has also been accompanied by the process of urbanization and industrialization, thus, there is a large demand for energy and resources, energy consumption, and CO2 emissions. Therefore, the pressure is greater; the impact of the two countries on the environment is also worth noting.

CO2 emissions of the BRICS countries have always been an issue of concern. Countries are constantly cooperating to save energy and reduce emissions to contribute to environmental protection. Through cooperation, exchanges, and a mutually beneficial, win-win strategic policy, there will be an improvement in production, science and technology, innovative technology, optimization of energy structures, and regional economic integration, resulting in a resource-saving and environment-friendly society.

5. Discussions

The purpose of this paper is to explore the relationship between the economic growth, financial development, and CO

2 emissions of the BRICS countries. The BRICS countries have a large population, large size, and rich energy resources. In the context of energy transition, strengthening energy cooperation in various fields and giving full play to their respective advantages and strengths can contribute to the sustainable development of global energy. The energy consumption of the BRICS countries ranks 1, 3, 4, 7, and 23 in the world’s total energy consumption rankings. (Data Sources: bp “Statistical Review of World Energy 2020”. See:

https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2020-full-report.pdf, (assessed on 18 June 2021)) The BRICS countries are the world’s fastest growing and largest developing country economies. In the past 40 years, especially in the past two decades, the carbon emissions of the BRICS countries have increased greatly. While economic development has attracted attention, carbon emissions have also increased cause disputes from all parties.

Under the huge energy consumption, the total carbon emissions of the BRICS countries accounted for 41.81% of the world’s total carbon emissions, (Data Sources: bp “Statistical Review of World Energy 2020”. See:

https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2020-full-report.pdf, (assessed on 18 June 2021)) and the per capita carbon emissions far exceed the world average level, and the gap is increasing. With environmental issues receiving widespread and continuous attention, economic development is a prerequisite for financial development, and financial development is the result of a country’s economic development. From the perspective of developing countries, financial development can improve technological innovation, reduce energy consumption, and thereby reduce carbon emissions. At the same time, research on the relationship between balanced economic development, financial development, and carbon emissions has also increased, which is also the motivation of this paper.

In the early stage of financial development in the BRICS countries, the financial system was not perfect, the efficiency of resource allocation was insufficient, the financing costs for enterprises to obtain green funds were high, and the shortage of scientific research investment and education funds would hinder enterprises from achieving the transformation of green and low-carbon production, resulting in carbon increase in emissions. When the financial development reaches a certain level, the financial system will be further improved, which can alleviate the uneven distribution of financial resources among industries. At the same time, resources such as scientific research personnel and R&D investment are more abundant, and the green and low-carbon concept will also be improved. Therefore, a higher level of financial development enables enterprises to have better advantages in technology, capital, and talents, strengthen industries to promote the optimization and upgrading of traditional industries, and increase the enthusiasm of the supply of green products, thereby helping to reduce CO2 emissions. However, when financial development surpasses the “financial moderation” stage and enters the “financial excess” stage, the role of financial development in promoting carbon emission reduction may be weakened. Therefore, when the level of financial development is at different stages of development, the relationship between the two may change.

The BRICS countries have increased renewable energy sources to reduce CO

2 emissions. Renewable energy occupies an important position in Brazil’s energy structure. Among them, biofuel has always been an important feature of Brazil’s energy development. Its production and consumption are second only to the United States, ranking second in the world. In 2016, Brazil promoted the establishment of the “Biomass Future Platform”, which aims to further promote international cooperation in sustainable biofuels, consolidate Brazil’s leading position in advanced biofuel technology and promotion and application, and combine with conventional new technologies such as hydropower, wind energy, and solar energy. Energy sources form a situation of benign complementarity. It is estimated that by 2029, the proportion of renewable energy in Brazil’s primary energy structure will further increase to more than 48%, which can reduce carbon emissions. In 2019, carbon dioxide emissions per unit of GDP decreased by 18.2% and 48.1%, respectively, compared with 2015 and 2005, which exceeded the target of 40–45% reduction in 2020 and basically reversed the rapid growth of CO

2 emissions (Data Sources: Renewable Energy Policy Brief BRAZIL, the International Renewable Energy Agency (IRENA). See:

https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2015/IRENA_RE_Latin_America_Policies/IRENA_RE_La-tin_America_Policies_2015_Country_Brazil.pdf?la=en&hash=D645B3E7B7DF03BDDAF6EE4F35058B2669E132B1, (assessed on 18 June 2021)).

In 2019, China’s non-fossil energy accounted for 15.3% of primary energy consumption, an increase of 7.9 percentage points from 2005. It has also exceeded the foreign promised target of increasing to about 15% by 2020; in 2018, forest area and forest stock volume compared with 2005, 45.09 million hectares and 5.104 billion cubic meters were increased, respectively, becoming the country with the largest increase in global forest resources during the same period. The Chinese government, in 2020, promotes the accelerated transformation of the energy consumption structure of “China’s Energy Development in the New Era” to clean and low-carbon. The Chinese government has further strengthened the clean development and utilization of coal, vigorously intensified oil and gas exploration and development, and accelerated the construction of natural gas production, supply, storage, and marketing system. Accelerate the development and utilization of non-fossil energy such as wind, solar, and biomass energy; promote the replacement of high-carbon energy with low-carbon energy, and promote the replacement of fossil energy with renewable energy. China further takes the construction of a new generation of information infrastructure as an opportunity to promote the digital and intelligent development of energy, accelerate the improvement of the intelligent level of the whole energy industry chain, and promote the coordinated development of multi-source and industrialization. The interaction of energy supply and demand methods improves the overall efficiency of the energy system (Data Sources: China National Energy Strategy and Policy 2020, Chapter VII: Renewable Energy Strategy and Policy. See:

http://kigeit.org.pl/FTP/PRCIP/Literatura/049_China_National_Energy_Strategy_and_Policy_2020%20_Renewable_energy.pdf, (assessed on 18 June 2021)).

The Indian government promised to reduce greenhouse gas emissions by 33% to 35% from 2015 to 2030. India’s new energy industry plans to reach the goal of 450 million kilowatts of renewable energy installed capacity by 2030, and at the same time promote the continuous decline of the cost of solar power generation, so that the economics of solar power generation can compete with coal power under the premise of considering the cost of energy storage. In 2015, India initiated the establishment of the International Solar Energy Alliance to raise US

$1 trillion in investment to develop 1 billion kilowatts of solar energy resources globally by 2030 (Data Sources: India 2020 Energy Policy Review, International Energy Agency (IEA), See:

https://iea.blob.core.windows.net/assets/2571ae38-c895-430e-8b62-bc19019c6807/India_2020_Energy_Policy_Review.pdf, (assessed on 18 June 2021)).

The Indian government promised to reduce greenhouse gas emissions by 33% to 35% from 2015 to 2030. India’s new energy industry plans to reach the goal of 450 million kilowatts of renewable energy installed capacity by 2030, and at the same time promote the continuous decline of the cost of solar power generation so that the economics of solar power generation can compete with coal power under the premise of considering the cost of energy storage. In 2015, India initiated the establishment of the International Solar Energy Alliance to raise US

$1 trillion in investment to develop 1 billion kilowatts of solar energy resources globally by 2030 (Data Sources: Renewable Energy 2021—South Africa, The International Comparative Legal Guides (ICLG). See:

https://iclg.com/practice-areas/renewable-energy-laws-and-regulations/south-africa, (assessed on 18 June 2021)).

In terms of policy, we suggest that the BRICS countries need to adjust the industrial structure to continuously reduce the secondary industry, which accounts for a high proportion of energy consumption, reduce the use of traditional fossil energy, and increase scientific and technological research and development investment to improve energy efficiency and reduce energy consumption intensity, and carbon emission intensity, and enhance the restraining effect on the increase of carbon emission. The BRICS countries need to promote the accelerated development of the tertiary industry, focus on the driving force of high-tech industries on economic development, and reduce the dependence of economic growth on high-carbon industries. The BRICS countries should improve their emission reduction coordination mechanisms, build a fair and open cooperation platform, actively promote the flow of emission reduction funds and technology sharing, realizes multi-faceted and multi-channel joint emission reductions, and accelerates the management of CO2 emissions in the BRICS countries. The BRICS countries should focus on sustainable economic development; give full play to the active role of the financial sector in the field of structural transformation and new energy technology applications, appropriately limit loans to high-polluting enterprises, and increase financial support for clean technology research, development, application, and promotion. The BRICS countries should work hard to promote technological progress to reduce energy intensity and reduce carbon emissions. While ensuring the efficient completion of CO2 emission reduction targets, they should consider the possible impact of CO2 emission constraints on the financial stability and steady economic growth of all countries and face environmental degradation. At this time, gradual policies should be adopted to alleviate the negative impact of CO2 emission constraints on economic growth and financial stability.

In terms of financial development, BRICS countries should reasonably expand and guide their own green financial markets to provide policy support for the transformation of the green economy; Encouraging financial product innovation, providing diversified products and services for low-carbon industries, broadening the incentive mechanism for technological progress and energy structure transformation will provide more convenience for low-carbon environmental protection industries, strengthen financial development, support industrial emission reduction technologies, promote carbon financial innovation, help the industry reduce CO2 emissions, and promote the establishment of low-carbon capital market and the development of carbon trading market. The shortcoming of this paper is that it only uses the three variables of financial development, GDP and CO2 emissions to study the impact of financial development and GDP on CO2 emissions; financial development uses traditional M2/GDP as indicator variables, which cannot contribute to the development of green finance, perform deeper and more precise analysis. Future researchers can use the financial development part more as indicators for empirical research departments, which can increase the depth and breadth of research.

6. Conclusions

This paper investigated the relationship between carbon dioxide emissions, financial development, and economic growth in BRICS countries during the period 1976–2019. The Frontier Toda-Yamamoto QR with the smooth structure break and Quantile on Quantile methodologies, which were used to explore the EKC hypothesis in relation to the BRICS countries, represented the main innovative contributions of this paper.

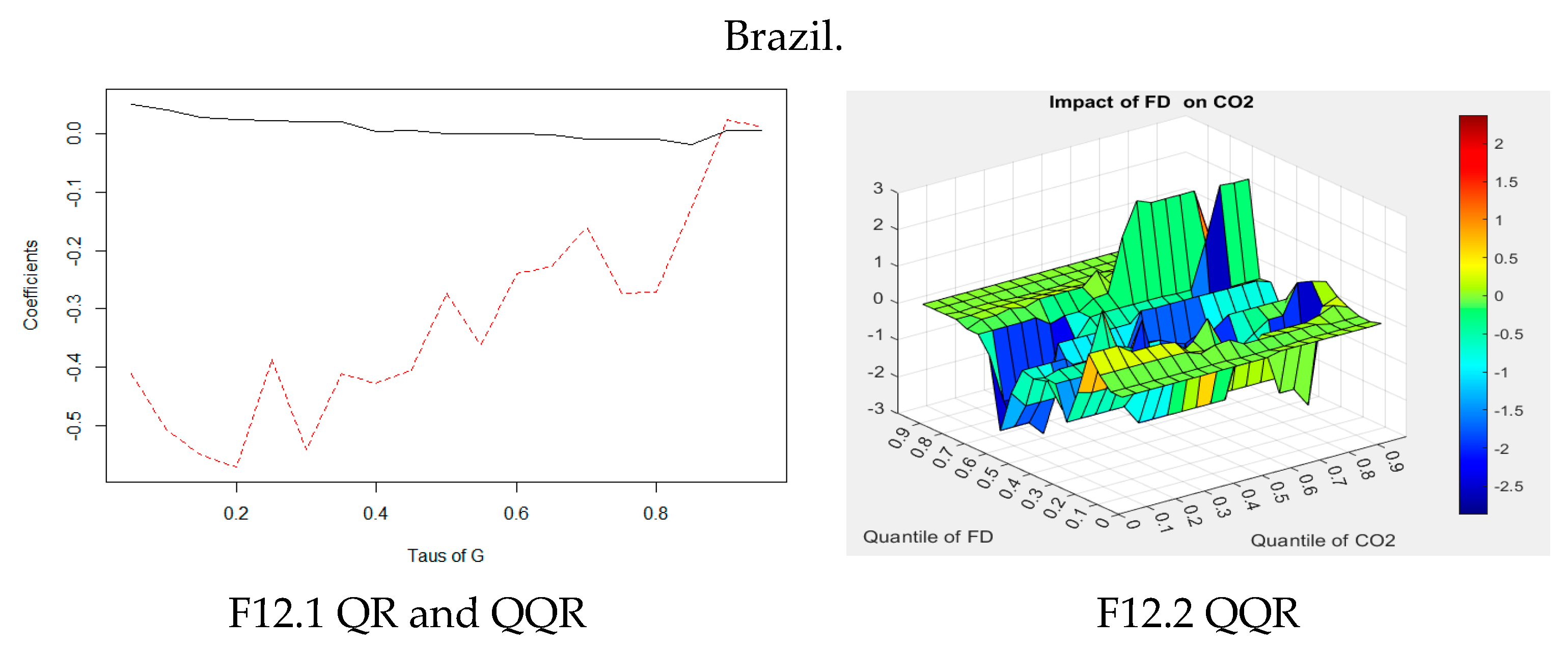

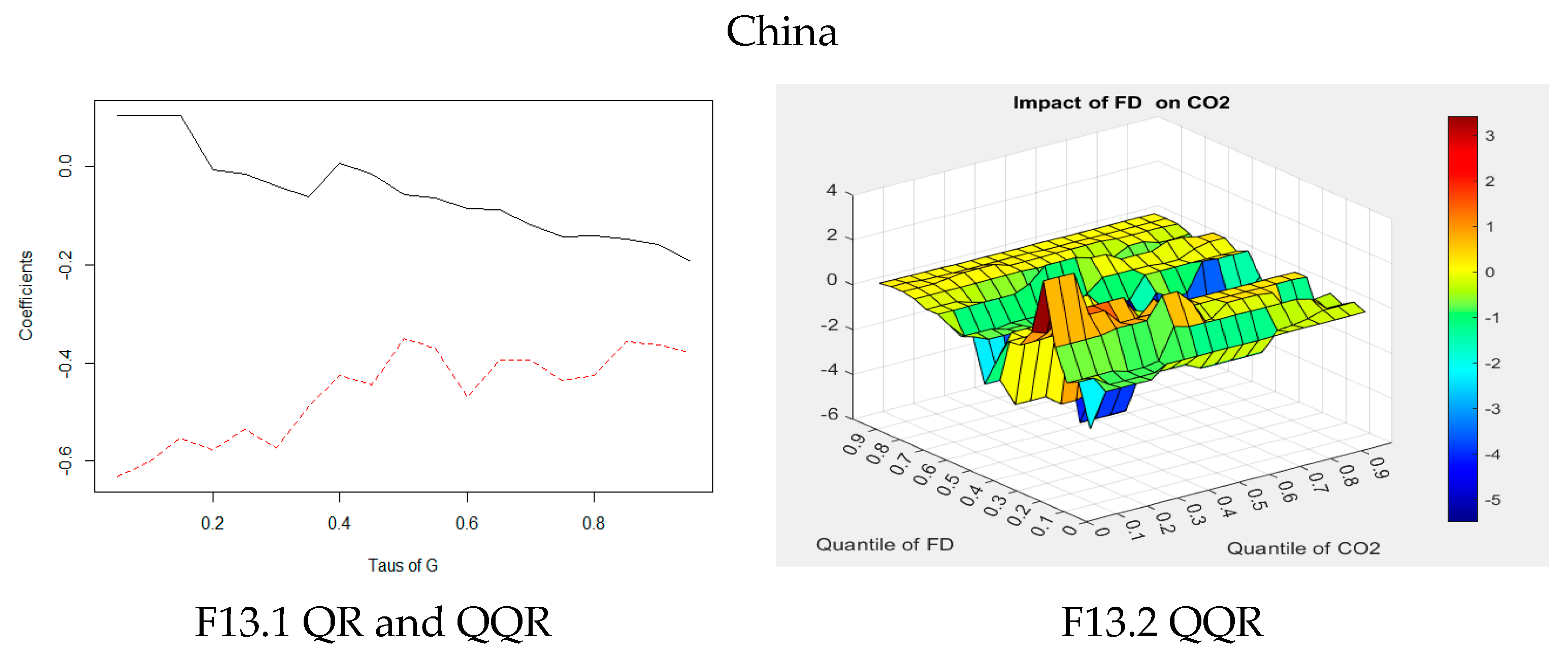

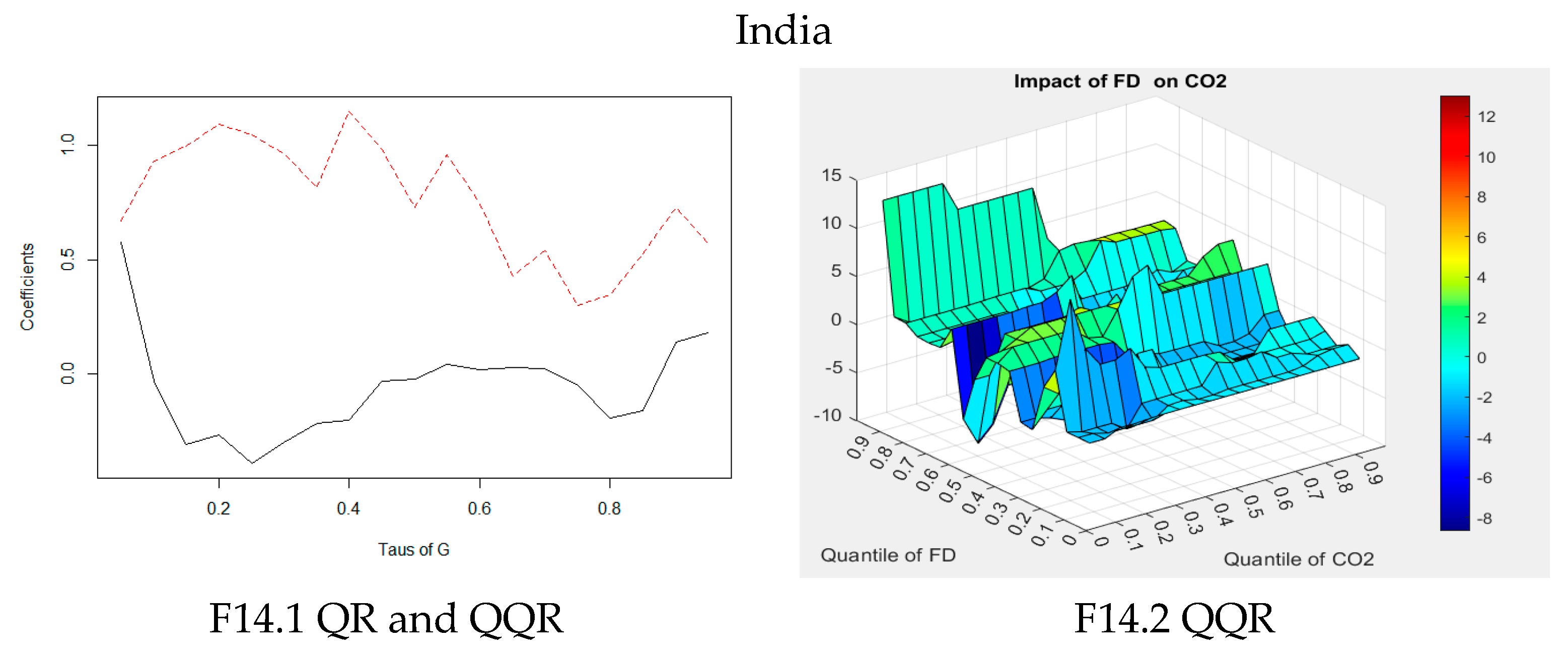

Two important findings were made: first, there is a smooth structure break between CO2 emissions and financial development in China and South Africa in the long-term under the EKC hypothesis. Second, in the short-term, from the QR at 0.6 quantile, Brazil’s CO2 emissions have a positive impact on financial development. On a closer look at the quantile-on-quantile, Brazil’s CO2 emissions in the 0.58–0.62 quantile were seen to have a strong positive impact on the financial development of the 0.68–0.72 quantile, while the financial development in the 0.63–0.67 quantile had a negative impact on CO2 emissions in the 0.83–1 quantile, suggesting that Brazil’s environment is gradually improving in the short-term. India’s financial development in the 0.93–1 quantile had the strongest impact on CO2 emissions in the low quantile (0–0.27), suggesting that India’s environmental emissions of CO2 improved with financial development. It was found that the Chinese and South African governments’ policies were efficient in reducing CO2 emissions and improving financial development because the policies of the two countries produced structural and transformational change between CO2 emissions and financial development under economic growth in the long-term.

The conclusion is that financial development has a significant impact on CO2 emissions, and this connection should be considered when formulating low-carbon policies. While ensuring the effective completion of low-carbon targets, the possible impact of CO2 emission restrictions on the financial stability and stable economic growth of all countries should not be ignored.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}