Business Models for Demand Response: Exploring the Economic Limits for Small- and Medium-Sized Prosumers

Abstract

:1. Introduction

1.1. Background

1.2. State of the Art on Business Model Concepts and Enabling Technologies

1.3. Scope and Structure of the Paper

- Explicit DR, also called Aggregator BM: This BM considers an aggregator that is active on the balancing market as a Balancing Service Provider (BSP) and communicates flexibility requests to the prosumers via the DELTA solution. The aggregator is assumed to be an independent one, but compensation mechanisms among the BRPs involved are neglected.

- Implicit DR, also called FLESCO BM: The FLESCO as a service provider is responsible for shifting loads for a prosumer in order to minimise costs in a given time-of-use (ToU) pricing scheme. In a ToU scheme, the price varies a few times during the day as well as a during the year.

- Which target segments could be profitable for the BMs?

- What are the key aspects for identifying a profitable target segment?

- What is the critical size of these target customers?

- Which market conditions need to be met to make the BMs profitable?

- Which internal conditions at the service provider need to be met to make the BM work?

- What is the contribution of technology advances?

2. Methodology

- Market data from organised electricity markets, where flexibility can be traded: This includes wholesale day-ahead (DA) and also balancing markets.

- Cost elements: As this is an explorative business modelling approach, there are no suitable cost data available as a reference. Hence, well-founded bottom-up assumptions for the selected BMs have been formulated and validated within the DELTA consortium. This was achieved especially in close cooperation with the technical developers and pilot site managers of the project. As a result, the latest experiences gathered during the installation and deployment of the pilot sites have been fed into these assumptions.

- Other assumptions such as target segment characteristics.

2.1. Aggregator BM

- Share of shiftable loads: The total consumption in each time frame is multiplied by the share of shiftable loads that is available for DR. This shiftable load is generally only available at maximum 50% of the time, as the loads need to be recovered at another time.

- Besides the load shifting potential, a certain share of shedable loads has also been considered. This means that the shiftable loads need to be recovered at a later time of the day, whereas shedable loads do not need to be recovered at all. Shedable loads are generally considered to be available 100% of the time as they do not need to be recovered.

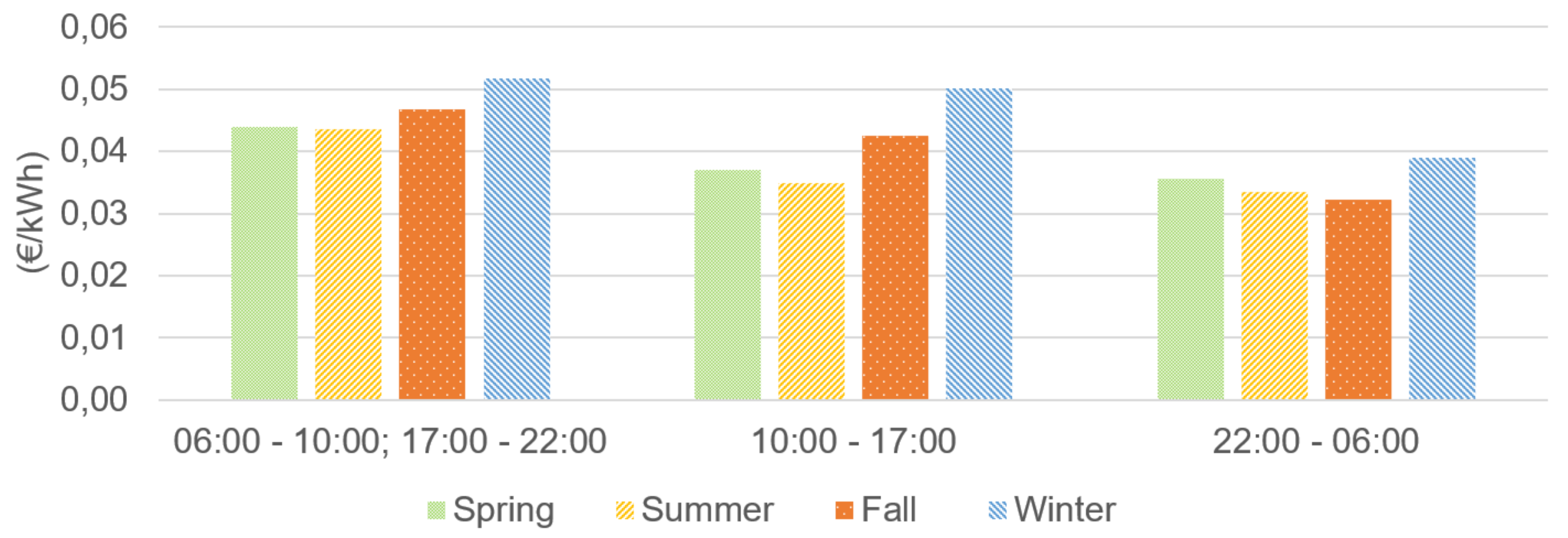

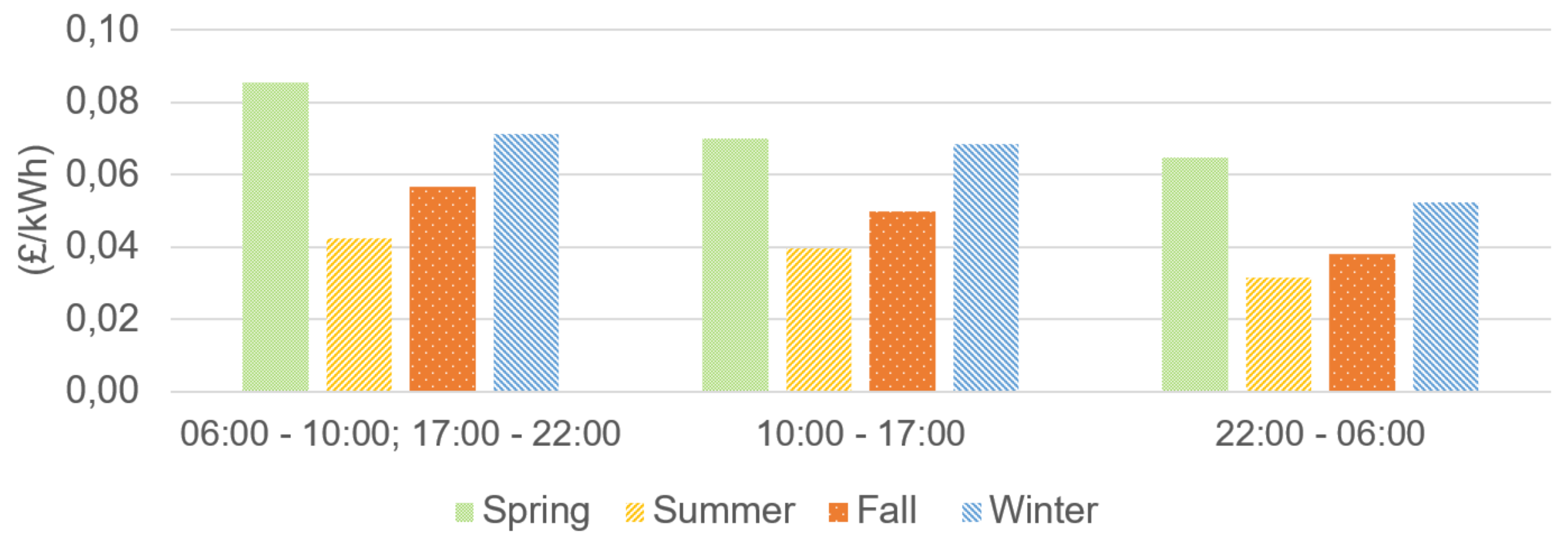

- As the balancing market consists of a two-step auction, the probability of being successful in these auctions needs to be estimated. If the capacity auction has been successful, the aggregator participates in the energy auction. The energy auction is only started if there is a request for flexibility during the specific time slice. The probability for having such a request is shown in Table A3. The probabilities of being successful are estimated with 80% for the capacity auction and 50% for the energy auction.

2.2. FLESCO BM

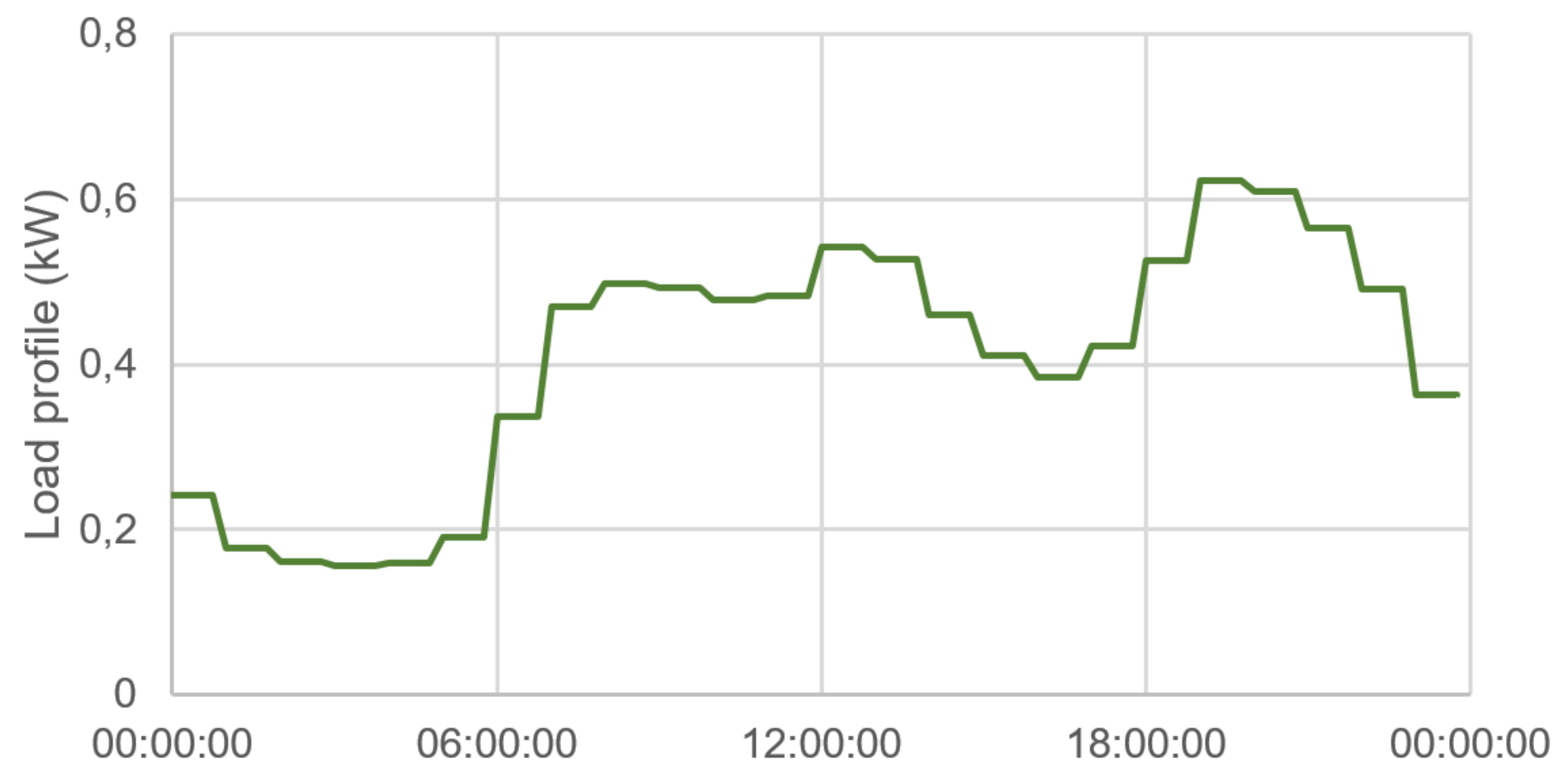

2.3. Target Segments and Cost Data

3. Results

3.1. Aggregator BM

3.2. FLESCO BM

4. Discussion and Conclusions

4.1. Discussion on Calculation Results

4.2. Overall Conclusions on the Viability of the DELTA BMs

4.3. Limitations of the Analysis

4.4. Outlook

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Market Data

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Capacity Price (€/mWh) | Energy Price (€/mWh) | |||||||

|---|---|---|---|---|---|---|---|---|

| Time Slice | Spring | Summer | Fall | Winter | Spring | Summer | Fall | Winter |

| 1 | 0.01 | 0.02 | 0.68 | 0.34 | 44.27 | 52.96 | 66.35 | 69.22 |

| 2 | 0.15 | 0.39 | 1.87 | 0.93 | 52.73 | 92.86 | 81.99 | 75.43 |

| 3 | 0.28 | 1.04 | 4.39 | 2.64 | 62.51 | 72.72 | 88.77 | 92.82 |

| 4 | 0.03 | 0.26 | 1.22 | 1.43 | 54.17 | 52.73 | 86.59 | 80.03 |

| 5 | 0.85 | 1.47 | 5.41 | 3.50 | 70.60 | 69.70 | 88.74 | 85.81 |

| 6 | 0.33 | 1.75 | 2.45 | 0.68 | 65.83 | 83.14 | 94.95 | 76.80 |

| Capacity Price (£/MWh) | |||

|---|---|---|---|

| Spring | Summer | Fall | Winter |

| 7.09 | 6.24 | 8.70 | 9.50 |

| Time Slice | Spring | Summer | Fall | Winter |

|---|---|---|---|---|

| 1 | 76% | 93% | 91% | 90% |

| 2 | 68% | 92% | 93% | 90% |

| 3 | 71% | 89% | 89% | 77% |

| 4 | 73% | 90% | 94% | 81% |

| 5 | 81% | 93% | 91% | 77% |

| 6 | 71% | 90% | 92% | 82% |

| Household “Optima” | Business “Klassik” | |||

|---|---|---|---|---|

| Electricity Unit Price | 0.0988 | €/kWh | 0.06 | €/kWh |

| Electricity Standing Charge | 19.0800 | €/year | 15 | €/year |

| Household “Standard Variable” | Business “British Gas Light” | |||

|---|---|---|---|---|

| Electricity Unit Price | 0.19 | £/kWh | 0.17 | £/kWh |

| Electricity Standing Charge | 87.6 | £/year | 120.45 | £/year |

| Electricity Unit Price Adapted (50%) | 0.095 | £/kWh | 0.085 | £/kWh |

| Electricity Standing Charge Adapted (50%) | 43.8 | £/year | 60.225 | £/year |

| Customer Size | <8000 | 8000–40,000 | >40,000 | kWh/a |

|---|---|---|---|---|

| Surcharge on spot market price | 0.0048 | 0.0019 | 0.0014 | €/kWh |

| Basic supplier fee | 3.0 | 4.8 | 6.0 | €/month |

Appendix B. Target Segments and Cost Data

- Pilot site managers, who have conducted the installation works at the DELTA pilot site premises.

- Technology developers, who have developed key technical components of the DELTA solution (such as the FEID).

- An aggregator, who is experienced with the operational work in existing DR schemes, including customer targeting and cost calculation of individual projects.

| Assumption | Value | Source | |

|---|---|---|---|

| Administrative Staff Costs | 50 | €/h | derived from [47,48] |

| Electrician Staff Costs | 70 | €/h | derived from [48,49] |

| FEID Price | 100 | per FEID | extrapolated from FEID prototyping costs |

Appendix B.1. Households

| Consumer Type | Household | Quantity Required per 5-Year Period * | |||

|---|---|---|---|---|---|

| CA | FA | SFH | |||

| Annual Electricity Consumption (kWh) | 2000 | 3500 | 5000 | ||

| Category | Cost item | (€) | (€) | (€) | |

| Investment | FEID | 20 | 20 | 20 | 1 FEID |

| Other Hardware | - | - | - | no other hardware expected | |

| Establish communication | - | - | - | not for household customers | |

| Installation | 28 | 42 | 56 | E: 2/3/4 h | |

| Contracting | Commercial feasibility | 20 | 20 | 20 | A: 2 h; no on-site visit |

| Technical feasibility | - | - | - | not for household customers | |

| Contract conclusion | 5 | 5 | 5 | A: 0.5 h | |

| Operation/Maintenance | on-site trouble shooting | 0 | 0 | 0 | not for household customers |

| remote maintenance | 7 | 7 | 7 | E: 0,5 h | |

| TOTAL customer fixed costs | 80 | 94 | 108 | * A = Administrative staff; E = Electrician | |

Appendix B.2. Residential Building Blocks (Excl. Households)

| Consumer Type | Residential Building (Excl. Households) | Quantity Required per 5-Year Period * | |||

|---|---|---|---|---|---|

| S | M | L | |||

| Annual Electricity Consumption (kWh) | 10,000 | 50,000 | 200,000 | ||

| Category | Cost item | (€) | (€) | (€) | |

| Investment | FEID | 20 | 20 | 20 | 1 FEID |

| Other Hardware | - | - | - | BEMS available | |

| Establish communication | - | - | - | BEMS available | |

| Installation | 56 | 56 | 112 | E: 4/4/8 h | |

| Contracting | Commercial feasibility | 50 | 70 | 100 | A: 5/7/10 h |

| Technical feasibility | 70 | 98 | 140 | E: 5/7/10 h | |

| Contract conclusion | 30 | 30 | 30 | A: 3/3/3 h | |

| Operation/Maintenance | on-site trouble shooting | 28 | 56 | 112 | E: 2/4/8 h |

| remote maintenance | 28 | 42 | 70 | E: 2/3/5 h | |

| TOTAL customer fixed costs | 282 | 372 | 584 | * A = Administrative staff; E = Electrician | |

| Number of households in building | 10 | 50 | 200 | ||

| Annual Building consumption per household (kWh) | 1000 | 1000 | 1000 | ||

Appendix B.3. Residential Building Blocks (Incl. Households)

| Consumer Type | Residential Building (Incl. Households) | Quantity Required per 5-Year Period * | |||

|---|---|---|---|---|---|

| S | M | L | |||

| Annual Electricity Consumption (kWh) | 40,000 | 200,000 | 800,000 | ||

| Category | Cost Item | (€) | (€) | (€) | |

| Investment | FEID | 20 | 60 | 200 | 1/3/10 FEIDs |

| Other Hardware | - | - | - | ||

| Establish communication | - | - | - | ||

| Installation | 196 | 756 | 2912 | E: 14/54/208 h | |

| Contracting | Commercial feasibility | 150 | 470 | 1100 | A: 15/47/110 |

| Technical feasibility | 70 | 98 | 140 | E: 5/7/10 h | |

| Contract conclusion | 55 | 155 | 530 | A: 5.5/15.5/53 h | |

| Operation/Maintenance | on-site trouble shooting | 28 | 56 | 112 | E: 2/4/8 h |

| remote maintenance | 84 | 252 | 630 | E: 6/18/45 | |

| TOTAL customer fixed costs | 603 | 1847 | 5624 | * A = Administrative staff; E = Electrician | |

| Number of households in building | 10 | 50 | 200 | ||

| Annual general building cons. per household (kWh) | 1000 | 1000 | 1000 | ||

| Annual Consumption per household (kWh) | 3000 | 3000 | 3000 | ||

Appendix B.4. Office Buildings

| Consumer Type | Office Building | Quantity Required per 5-Year Period * | |||

|---|---|---|---|---|---|

| S | M | L | |||

| Annual Electricity Consumption (kWh) | 240,000 | 1,200,000 | 3,200,000 | ||

| Category | Cost item | (€) | (€) | (€) | |

| Investment | FEID | 20 | 20 | 20 | 1 FEID |

| Other Hardware | - | - | - | BEMS available | |

| Establish communication | - | - | - | BEMS available | |

| Installation | 126 | 168 | 210 | E: 9/12/15 h | |

| Contracting | Commercial feasibility | 70 | 140 | 280 | A: 5/10/20 h |

| Technical feasibility | 70 | 140 | 280 | E: 5/10/20 h | |

| Contract conclusion | 30 | 60 | 80 | A: 3/6/8 h | |

| Operation/Maintenance | on-site trouble shooting | 28 | 56 | 112 | E: 2/4/8 h |

| remote maintenance | 56 | 112 | 224 | E: 4/8/16 h | |

| TOTAL customer fixed costs | 400 | 696 | 1206 | * A = Administrative staff; E = Electrician | |

| Office space (m2) | 3000 | 15,000 | 40,000 | ||

| Consumption in kWh per m2 and year | 80 | 80 | 80 | derived from [52,53] | |

Appendix B.5. Retail Buildings

| Consumer Type | Retail Building | Quantity Required per 5-Year Period * | |||

|---|---|---|---|---|---|

| NFS | SM | SC | |||

| Annual Electricity Consumption [kWh] | 72,000 | 198,000 | 12,000,000 | ||

| Category | Cost Item | (€) | (€) | (€) | |

| Investment | FEID | 20 | 20 | 60 | 1/1/3 FEIDs |

| Other Hardware | - | - | - | BEMS available | |

| Establish communication | - | - | - | BEMS available | |

| Installation | 84 | 84 | 560 | E: 6/6/40 h | |

| Contracting | Commercial feasibility | 50 | 50 | 250 | A: 5/5/25 h |

| Technical feasibility | 70 | 70 | 350 | E: 5/5/25 h | |

| Contract conclusion | 30 | 30 | 150 | A: 3/3/15 h | |

| Operation/Maintenance | on-site trouble shooting | 28 | 28 | 280 | E: 2/2/20 h |

| remote maintenance | 28 | 28 | 280 | E: 2/2/20 h | |

| TOTAL customer fixed costs | 310 | 310 | 1930 | * A = Administrative staff; E = Electrician | |

| Retail space [m2] | 600 | 600 | 80,000 | ||

| Consumption per m2 and year | 120 | 330 | 150 | derived from [54] | |

Appendix B.6. Electric Vehicle Charging Stations

| Consumer Type | EV Charging Station | Quantity Required per 5-Year Period * | |||

|---|---|---|---|---|---|

| Single | Residen. | Business | |||

| Annual Electricity Consumption [kWh] | 3000 | 60,000 | 150,000 | ||

| Category | Cost Item | (€) | (€) | (€) | |

| Investment | FEID | - | - | - | controllable charging point available, no FEID required |

| Other Hardware | - | - | - | ||

| Establish communication | - | - | - | ||

| Installation | - | - | - | ||

| Contracting | Commercial feasibility | 10 | 40 | 40 | A: 1/4/4 |

| Technical feasibility | 14 | 56 | 56 | E: 1/4/4 | |

| Contract conclusion | 10 | 20 | 20 | A: 1/2/2 h | |

| Operation/Maintenance | on-site trouble shooting | 0 | 0 | 56 | E: 0/0/4 h |

| remote maintenance | 14 | 28 | 84 | E: 1/2/6 h | |

| TOTAL customer fixed costs | 48 | 144 | 256 | * A = Administrative staff; E = Electrician | |

| Number of BEVs | 1 | 20 | 50 | ||

| Consumption [kWh] per year and BEV | 3000 | 3000 | 3000 | ||

| Kilometres per year and BEV | 15,000 | 15,000 | 15,000 | ||

| Consumption [kWh] per 100 km | 20 | 20 | 20 | ||

Appendix B.7. Overhead Costs

| Number of Customers | 1000 | 10,000 | 10,0000 | |

|---|---|---|---|---|

| Cost Item | (EUR) | (EUR) | (EUR) | Assumption |

| IT infrastructure | 3000 | 6000 | 12,000 | 250/500/1000 EUR server costs per month |

| licenses | 2400 | 24,000 | 240,000 | 0.2 EUR per customer per month |

| Staff costs | 480,000 | 600,000 | 900,000 | 8/10/15 employees, average 60,000 EUR/person/year |

| Office rent | 25,200 | 29,400 | 63,000 | office size: 60, 70, 150 m2; average 35 EUR/m2/month |

| TOTAL overhead | 510,600 | 659,400 | 1,215,000 |

References

- European Commission. Incorporing Demand Side Flexibility, in Particular Demand Response, in Electricity Markets; European Commission: Brussels, Belgium, 2013. [Google Scholar]

- Ribó-Pérez, D.; Larrosa-López, L.; Pecondón-Tricas, D.; Alcázar-Ortega, M. A Critical Review of Demand Response Products as Resource for Ancillary Services: International Experience and Policy Recommendations. Energies 2021, 14, 846. [Google Scholar] [CrossRef]

- Directive 2012/27/EU of the European Parliament and of the Council of 25 October 2012 on Energy Efficiency, Amending Directives 2009/125/EC and 2010/30/EU and Repealing Directives 2004/8/EC and 2006/32; European Parliament: Brussels, Belgium, 2012.

- Zancanella, P.; Bertoldi, P.; Boza-Kiss, B. Why Is Demand Response Not Implemented in the EU? Status of Demand Response and Recommendations to Allow Demand Response to Be Fully Integrated in Energy Markets. In Proceedings of the ECEEE 2017 Summer Study on Energy Efficiency, Consumption, Efficiency and Limits, Toulon/Hyères, France, 29 May–3 June 2017. [Google Scholar]

- Willems, B.; Zhou, J. The Clean Energy Package and Demand Response: Setting Correct Incentives. Energies 2020, 13, 5672. [Google Scholar] [CrossRef]

- Federal Energy Regulatory Commission (FERC). FERC Order No. 2222: Fact Sheet 2020; Federal Energy Regulatory Commission (FERC): Washington, DC, USA, 2020. [Google Scholar]

- Behi, B.; Baniasadi, A.; Arefi, A.; Gorjy, A.; Jennings, P.; Pivrikas, A. Cost–Benefit Analysis of a Virtual Power Plant Including Solar PV, Flow Battery, Heat Pump, and Demand Management: A Western Australian Case Study. Energies 2020, 13, 2614. [Google Scholar] [CrossRef]

- Li, W.; Xu, P.; Lu, X.; Wang, H.; Pang, Z. Electricity demand response in China: Status, feasible market schemes and pilots. Energy 2016, 114, 981–994. [Google Scholar] [CrossRef]

- Parrish, B.; Heptonstall, P.; Gross, R.; Sovacool, B.K. A systematic review of motivations, enablers and barriers for consumer engagement with residential demand response. Energy Policy 2020, 138, 111221. [Google Scholar] [CrossRef]

- Pallonetto, F.; De Rosa, M.; D’Ettorre, F.; Finn, D.P. On the assessment and control optimisation of demand response programs in residential buildings. Renew. Sustain. Energy Rev. 2020, 127, 109861. [Google Scholar] [CrossRef]

- Tzovaras, D. About DELTA. Available online: https://www.delta-h2020.eu/ (accessed on 21 September 2021).

- Paterakis, N.; Erdinç, O.; Catalão, J.P.S. An overview of Demand Response: Key-elements and international experience. Renew. Sustain. Energy Rev. 2017, 69, 871–891. [Google Scholar] [CrossRef]

- Kwac, J.; Rajagopal, R. Data-Driven Targeting of Customers for Demand Response. IEEE Trans. Smart Grid 2016, 7, 2199–2207. [Google Scholar] [CrossRef]

- Qi, N.; Cheng, L.; Xu, H.; Wu, K.; Li, X.; Wang, Y.; Liu, R. Smart meter data-driven evaluation of operational demand response potential of residential air conditioning loads. Appl. Energy 2020, 279, 115708. [Google Scholar] [CrossRef]

- Antonopoulos, I.; Robu, V.; Couraud, B.; Flynn, D. Data-driven modelling of energy demand response behaviour based on a large-scale residential trial. Energy AI 2021, 4, 100071. [Google Scholar] [CrossRef]

- Hamwi, M.; Lizarralde, I.; Legardeur, J. Demand response business model canvas: A tool for flexibility creation in the electricity markets. J. Clean. Prod. 2021, 282, 124539. [Google Scholar] [CrossRef]

- Osterwalder, A.; Pigneur, Y. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers; Wiley: Hoboken, NJ, USA, 2010; ISBN 978-0-470-90103-8. [Google Scholar]

- SEDC. Mapping Demand Response in Europe Today; Smart Energy Demand Coalition: Brussels, Belgium, 2014. [Google Scholar]

- Villar, J.; Bessa, R.; Matos, M. Flexibility products and markets: Literature review. Electr. Power Syst. Res. 2018, 154, 329–340. [Google Scholar] [CrossRef]

- Behrangrad, M. A review of demand side management business models in the electricity market. Renew. Sustain. Energy Rev. 2015, 47, 270–283. [Google Scholar] [CrossRef]

- Van der Veen, A.; Van der Laan, M.; De Heer, H.; Klaassen, E.; Van den Reek, W. Flexibility Value Chain; USEF Foundation: Arnhem, The Netherlands, 2018. [Google Scholar]

- ENTSO-E. Market Design for Demand Side Response-Policy Paper; European Network of Transmission System Operators for Electricity: Brussels, Belgium, 2015. [Google Scholar]

- Lu, X.; Li, K.; Xu, H.; Wang, F.; Zhou, Z.; Zhang, Y. Fundamentals and business model for resource aggregator of demand response in electricity markets. Energy 2020, 204, 117885. [Google Scholar] [CrossRef]

- Ponds, K.T.; Arefi, A.; Sayigh, A.; Ledwich, G. Aggregator of Demand Response for Renewable Integration and Customer Engagement: Strengths, Weaknesses, Opportunities, and Threats. Energies 2018, 11, 2391. [Google Scholar] [CrossRef] [Green Version]

- De Heer, H.; Van der Laan, M. USEF: Workstream on Aggregator Implementation Models; USEF Foundation: Arnhem, The Netherlands, 2017. [Google Scholar]

- Yu, M.; Hong, S.H.; Kim, J.B. Incentive-based demand response approach for aggregated demand side participation. In Proceedings of the 2016 IEEE International Conference on Smart Grid Communications (SmartGridComm), Sydney, Australia, 6–9 November 2016; IEEE: Sydney, Australia, 2016; pp. 51–56. [Google Scholar]

- USEF. USEF: The Framework Explained 2015; USEF Foundation: Arnhem, The Netherlands, 2015. [Google Scholar]

- Joint Research Center Energy Service Companies (ESCOs). Available online: https://e3p.jrc.ec.europa.eu/communities/energy-service-companies (accessed on 21 September 2021).

- Leutgöb, K.; Amann, C.; Tzovaras, D.; Ioannidis, D. New Business Models Enabling Higher Flexibility on Energy Markets. In Proceedings of the ECEEE 2019 Summer Study on Energy Efficiency: Is Efficient Sufficient? Toulon/Hyères, France, 3–8 June 2019. [Google Scholar]

- Ma, Z.; Billanes, J.; Jørgensen, B. Aggregation Potentials for Buildings—Business Models of Demand Response and Virtual Power Plants. Energies 2017, 10, 1646. [Google Scholar] [CrossRef] [Green Version]

- Energati NOVICE Project Proposes New Energy Efficiency Business Model. Available online: https://www.engerati.com/energy-retail/novice-project-proposes-new-energy-efficiency-business-model/ (accessed on 21 September 2021).

- Specht, J.M.; Madlener, R. Energy Supplier 2.0: A conceptual business model for energy suppliers aggregating flexible distributed assets and policy issues raised. Energy Policy 2019, 135, 110911. [Google Scholar] [CrossRef]

- Iria, J.; Soares, F.; Matos, M. Optimal bidding strategy for an aggregator of prosumers in energy and secondary reserve markets. Appl. Energy 2019, 238, 1361–1372. [Google Scholar] [CrossRef]

- Iria, J.P.; Soares, F.J.; Matos, M.A. Trading Small Prosumers Flexibility in the Energy and Tertiary Reserve Markets. IEEE Trans. Smart Grid 2019, 10, 2371–2382. [Google Scholar] [CrossRef]

- Zepter, J.M.; Lüth, A.; Crespo del Granado, P.; Egging, R. Prosumer integration in wholesale electricity markets: Synergies of peer-to-peer trade and residential storage. Energy Build. 2019, 184, 163–176. [Google Scholar] [CrossRef]

- Bertoldi, P.; Zancanella, P.; Boza-Kiss, B. Demand Response Status in EU Member States; Joint Research Center: Ispra, Italy, 2016. [Google Scholar]

- ENTSO-E Prices of Activated Balancing Energy. Available online: https://www.entsoe.eu/network_codes/eb/ (accessed on 14 June 2021).

- National Grid FFR Market Information and Tender Reports. Available online: https://www.nationalgrideso.com/industry-information/balancing-services/frequency-response-services/firm-frequency-response-ffr?market-information (accessed on 5 August 2021).

- National Grid. Firm Frequency Response-Frequently Asked Questions v1.3; National Grid: Warwick, UK, 2017. [Google Scholar]

- ENTSO-E Day-Ahead Prices. Available online: https://transparency.entsoe.eu/ (accessed on 14 June 2021).

- Nord Pool AS Market Data. Available online: https://www.nordpoolgroup.com/Market-data1/#/n2ex/table (accessed on 16 July 2021).

- VITO; Viegand & Maagøe; Armines; Bonn University. Wuppertal Institut Ecodesign Preparatory Study on Smart Appliances (Lot 33)–Task 7 Report Policy and Scenario Analysis; Flemish Institute for Technological Research NV: Boeretang, Belgium, 2018. [Google Scholar]

- The Mobility House Vehicle-to-Grid. Available online: https://www.mobilityhouse.com/int_en/vehicle-to-grid (accessed on 20 October 2021).

- Austrian Power Grid Balancing Statistics 2020. Available online: https://www.apg.at/ (accessed on 16 July 2021).

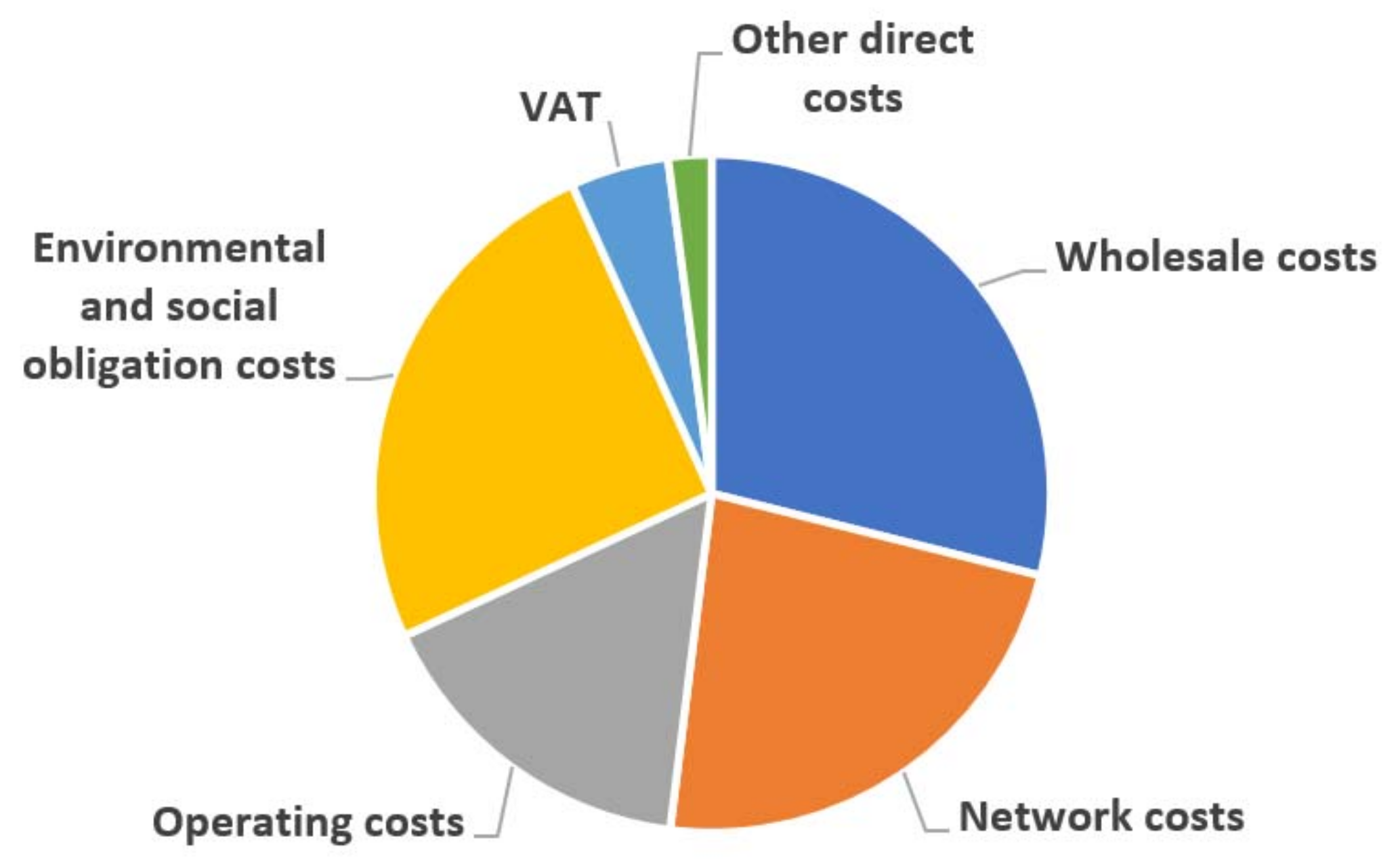

- OFGEM Your Bill Breakdown. Available online: https://www.ofgem.gov.uk/energy-advice-households/costs-your-energy-bill (accessed on 5 August 2021).

- Angebote Strom, Spotty Smart Energy Partner GmbH. Available online: https://www.spottyenergie.at (accessed on 16 July 2021).

- karriere.at Gehaltsvergleich Büroangestellte/r. Available online: https://www.karriere.at/gehalt/b%C3%BCroangestellter (accessed on 20 July 2021).

- Eurostat Wages and Labour Costs. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Wages_and_labour_costs (accessed on 20 July 2021).

- AK Wien Preisvergleich Handwerker in Wien. Available online: https://wien.arbeiterkammer.at/beratung/konsumentenschutz/einkaufundrecht/preisvergleich_handwerker_wien.html (accessed on 20 July 2021).

- BDEW Standardlastprofile Strom. Available online: https://www.bdew.de/energie/standardlastprofile-strom/ (accessed on 20 July 2021).

- Lampersberger, P. DeLight Monitoring-Demo Light Impact-Monitoring and Metrological Investigation of Energy-Efficient Buildings. Available online: https://nachhaltigwirtschaften.at/en/sdz/projects/delight-monitoring.php (accessed on 20 July 2021).

- D’Agostino, D.; Cuniberti, B.; Bertoldi, P. Energy consumption and efficiency technology measures in European non-residential buildings. Energy Build. 2017, 153, 72–86. [Google Scholar] [CrossRef]

- Benke, G.; Leutgöb, K. Energieverbrauch Im Dienstleistungssektor-Kennwerte Und Hochrechnung; E7 Energy Innovation & Engineering: Wien, Austria, 2012. [Google Scholar]

- Statista Stromverbrauch je Quadratmeter Verkaufsfläche im Deutschsprachigen Einzelhandel in den Jahren 2013 und 2015. Available online: https://de.statista.com/statistik/daten/studie/372110/umfrage/stromverbrauch-je-quadratmeter-verkaufsflaeche-im-deutschsprachigen-einzelhandel/ (accessed on 2 August 2021).

- Preßmair, G.; Lampersberger, P. Anschlussleistung Für Wohnhausanlagen Mit E-Ladeinfrastruktur. In Proceedings of the Symposium Energieinnovation, Graz, Austria, 13 February 2020. [Google Scholar]

| Category | Item | Symbol | Comment * |

|---|---|---|---|

| Consumption pattern | Building type | e.g., household, office etc. | |

| Total consumption | cons | kWh/year | |

| Share of shiftable loads | share of total consumption | ||

| Load shifting available | 50% share of shiftable loads | ||

| Share of shedable loads | share of total consumption | ||

| Load shedding available | 100% share of shedable loads | ||

| Market Prices | Market | aFRR+ or FFR | |

| Probability of Success | in capacity auction | share of time slots | |

| in energy auction | share of time slots | ||

| Pricing Model | Remuneration for customer | rem | share of revenue per customer |

| Bau Flat Pricing Scheme | Energy price | Pv | €/kWh |

| Basic fee | Pb | €/year | |

| Cost Structure | Customer fixed costs | Ccustomer | €/year |

| Aggregator fixed costs | Cagg | €/year | |

| Customer Scaling | number of customers | n | number |

| Calculation Step | Item | Symbol | Formula | Unit * |

|---|---|---|---|---|

| Revenue Per Customer | Revenue Balancing Capacity | Rcap | € | |

| Revenue Balancing Energy | Ren | € | ||

| Revenue | R | Rcap + Ren | € | |

| Contribution Margin 1 | Customer Remuneration | Srem | R ∗ rem | € |

| Customer Savings Due to Shedding | Sshed | € | ||

| Customer Savings Total | Stot | Srem + Sshed | € | |

| Customer Savings Relative | Srel | Stot/(pb + pv ∗ cons) | share | |

| Contribution Margin 1 | CM1 | R—Srem | € | |

| Contribution Margin 2 | Customer Fixed Costs | Ccustomer | € | |

| Contribution Margin 2 | CM2 | CM1—Ccustomer | € | |

| Operational Profit | Overall Contribution Margin | CMtot | CM2 ∗ n | € |

| Aggregator Fixed Costs | Cflesco | € | ||

| Operational Profit | OP | CMtot—Cagg | € |

| Category | Item | Symbol | Comment * | |

|---|---|---|---|---|

| Consumption Pattern | Building Type | e.g., household, office etc. | ||

| Total Consumption | cons | kWh/year | ||

| Share of Shiftable Loads | share of total consumption | |||

| Share of Shedable Loads | share of total consumption | |||

| Spring | High/Mid/Low | share of total consumption | ||

| Summer | High/Mid/Low | |||

| Fall | High/Mid/Low | |||

| Winter | High/Mid/Low | |||

| Spot Market Prices | Spring | High/Mid/Low | €/kWh | |

| Summer | High/Mid/Low | |||

| Fall | High/Mid/Low | |||

| Winter | High/Mid/Low | |||

| ToU pricing scheme | Surcharge on Spot Price | €/kWh | ||

| Basic Fee | €/year | |||

| BaU flat pricing scheme | Energy Price | pv | €/kWh | |

| Basic Fee | pb | €/year | ||

| FLESCO pricing model | Remuneration for customer | rem | share of revenue per customer | |

| Cost structure | Customer fixed costs | Ccustomer | €/year | |

| FLESCO fixed costs | Cagg | €/year | ||

| Customer scaling | number of customers | n | number | |

| Calculation Step | Item | Symbol | Formula | Unit * |

|---|---|---|---|---|

| Revenue per customer | Energy costs ToU optimised | Eopt | € | |

| Energy costs BaU flat | Eflat | pb + pv ∗ cons | € | |

| Revenue | R | Eflat—Eopt | € | |

| Contribution margin 1 | Customer remuneration | Srem | R ∗ rem | € |

| Customer savings relative | Srel | Srem/Eflat | share | |

| Contribution margin 1 | CM1 | R—Srem | € | |

| Contribution margin 2 | Customer fixed costs | Ccustomer | € | |

| Contribution margin 2 | CM2 | CM1—Ccustomer | € | |

| Operational profit | Overall contribution margin | CMtot | CM2 ∗ n | € |

| FLESCO fixed costs | Cflesco | € | ||

| Operational profit | OP | CMtot—Cflesco | € |

| Target Segment | Customer Size | Annual Consumption (kWh) | Annual Customer Fixed Costs (€) |

|---|---|---|---|

| Household | Couple apartment (CA) | 2000 | 80 |

| Family apartment (FA) | 3500 | 94 | |

| Single-family house (SFH) | 5000 | 108 | |

| Residential Building (excl. households) | Small (S) | 10,000 | 282 |

| Medium (M) | 50,000 | 372 | |

| Large (L) | 200,000 | 584 | |

| Residential building (incl. households) | Small (S) | 40,000 | 603 |

| Medium (M) | 200,000 | 1847 | |

| Large (L) | 800,000 | 5624 | |

| Office Building | Small (S) | 240,000 | 400 |

| Medium (M) | 1,200,000 | 696 | |

| Large (L) | 3,200,000 | 1206 | |

| Retail Building | Non-food shop (NFS) | 72,000 | 310 |

| Supermarket (SM) | 198,000 | 310 | |

| Shopping centre (SC) | 12,000,000 | 1930 | |

| Electric Vehicle Charging Station | Individual BEV | 3000 | 48 |

| Residential garage | 60,000 | 144 | |

| Business fleet | 150,000 | 256 |

| Segment | Building Type | Household | Res-excl | Res-incl | Unit | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Building Size | CA | FA | SFH | S | M | L | S | M | L | ||

| Scaling | Number of Customers | 10,000 | 10,000 | 10,000 | 500 | 500 | 500 | 500 | 500 | 500 | |

| Revenue per customer | Revenue Balancing Capacity | 0.50 | 0.88 | 1.25 | 2.31 | 11.55 | 46.19 | 9.81 | 49.06 | 196.24 | € |

| Revenue Balancing Energy | 10.18 | 17.82 | 25.45 | 50.67 | 253.37 | 1013.50 | 203.39 | 1016.97 | 4067.87 | € | |

| Revenue | 10.68 | 18.69 | 26.70 | 52.98 | 264.92 | 1 059.68 | 213.21 | 1066.03 | 4264.10 | € | |

| Contribution margin 1 | Customer Remuneration | 5.34 | 9.35 | 13.35 | 26.49 | 132.46 | 529.84 | 106.60 | 533.01 | 2132.05 | € |

| Customer Savings Due to Shedding | 5.30 | 9.27 | 13.24 | 16.70 | 83.52 | 334.08 | 64.96 | 324.81 | 1299.25 | € | |

| Customer Savings Total | 10.64 | 18.62 | 26.60 | 43.20 | 215.98 | 863.93 | 171.57 | 857.83 | 3431.30 | € | |

| Customer Savings Relative | 5% | 5% | 5% | 7% | 7% | 7% | 7% | 7% | 7% | share | |

| Contribution Margin 1 | 5 | 9 | 13 | 26 | 132 | 530 | 107 | 533 | 2132 | € | |

| Contribution margin 2 | Customer Fixed Costs | 80 | 94 | 108 | 282 | 372 | 584 | 603 | 1847 | 5624 | € |

| Contribution Margin 2 | −75 | −85 | −95 | −256 | −240 | −54 | −496 | −1314 | −3492 | € | |

| Operational profit | Overall Contribution Margin | −746,593 | −846,538 | −946,483 | −127,754 | −119,770 | −27,079 | −248,199 | −656,994 | −1,745,975 | € |

| Aggregator Fixed Costs | 659,400 | 659,400 | 659,400 | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | € | |

| Operational Profit | −1,405,993 | −1505,938 | −1,605,883 | −638,354 | −630,370 | −537,679 | −758,799 | −1,167,594 | −2,256,575 | € | |

| Segment | Building Type | Office | Shop | BEV | Unit | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Building Size | S | M | L | NFS | SM | SC | Single | Residen. | Business | ||

| Scaling | Number of Customers | 500 | 500 | 500 | 1000 | 500 | 5 | 10,000 | 500 | 500 | |

| Revenue Per Customer | Revenue Balancing Capacity | 59.51 | 297,56 | 793.51 | 17.86 | 49.11 | 2,976,30 | 1.56 | 31.29 | 78.23 | € |

| Revenue Balancing Energy | 1224.89 | 6124.43 | 16,331.80 | 364,68 | 1002,88 | 6078,068 | 28.11 | 562.19 | 1405.66 | € | |

| Revenue | 1284.40 | 6421.99 | 17,125.31 | 382,54 | 1051,99 | 6375,697 | 29.67 | 593.49 | 1483.89 | € | |

| Contribution Margin 1 | Customer Remuneration | 642.20 | 3211.00 | 8562.66 | 191,27 | 526.00 | 3187,849 | 14.84 | 296.74 | 741.94 | € |

| Customer Savings Due to Shedding | 451.05 | 2255.27 | 6014.04 | 129,09 | 354.99 | 2151,466 | 0.00 | 0.00 | 0.00 | € | |

| Customer Savings Total | 1093.25 | 5466.26 | 14,576.70 | 320,36 | 880.99 | 533,9315 | 14.84 | 296.74 | 741.94 | € | |

| Customer Savings Relative | 8% | 8% | 8% | 7% | 7% | 7% | 6% | 7% | 11% | share | |

| Contribution Margin 1 | 642 | 3211 | 8563 | 191 | 526 | 31 878 | 15 | 297 | 742 | € | |

| Contribution Margin 2 | Customer Fixed Costs | 400 | 696 | 1206 | 310 | 310 | 1 930 | 48 | 144 | 256 | € |

| Contribution Margin 2 | 242 | 2515 | 7357 | −119 | 216 | 29 948 | −33 | 153 | 486 | € | |

| Operational Profit | Overall Contribution Margin | 121,100 | 1,257,498 | 3,678,328 | −118,729 | 107,998 | 149,742 | −331,628 | 76,372 | 242,972 | € |

| Aggregator Fixed Costs | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | 659,400 | 510,600 | 510,600 | € | |

| Operational Profit | −389,500 | 746,898 | 3,167,728 | −629,329 | −402,602 | −360,858 | −991,028 | −434,228 | −267,628 | € | |

| Segment | Building Type | Household | Res-excl | Res-incl | Office | Shop | BEV | Unit |

|---|---|---|---|---|---|---|---|---|

| Building Size | SFH | L | L | L | SC | 50 | ||

| Scaling | Number of Customers | 10,000 | 500 | 500 | 500 | 5 | 500 | |

| Revenue Per Customer | Revenue Balancing Capacity | 6.40 | 252.96 | 1021.10 | 4046.52 | 15,144.37 | 344.25 | £ |

| Revenue Balancing Energy | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0,00 | £ | |

| Revenue | 6.40 | 252.96 | 1021.10 | 4046.52 | 15,144.37 | 344.25 | £ | |

| Contribution Margin 1 | Customer Remuneration | 3.20 | 126.48 | 510.55 | 2023.26 | 7572.19 | 172.13 | £ |

| Customer Savings Due to Shedding | 12.73 | 528.97 | 2057.15 | 8519.90 | 30,479.11 | 0.00 | £ | |

| Customer Savings Total | 15.94 | 655.44 | 2567.70 | 10,543.15 | 38,051.29 | 172.13 | £ | |

| Customer Savings Relative | 3% | 3% | 3% | 4% | 4% | 2% | share | |

| Contribution Margin 1 | 3 | 126 | 511 | 2023 | 7572 | 172 | £ | |

| Contribution Margin 2 | Customer Fixed Costs | 93 | 502 | 4837 | 1037 | 1660 | 310 | £ |

| Contribution Margin 2 | −90 | −376 | −4326 | 986 | 5912 | −137 | £ | |

| Operational Profit | Overall Contribution Margin | −896,794 | −187,881 | −2,163,044 | 493.049 | 29,562 | −68,737 | £ |

| Aggregator Fixed Costs | 567,084 | 439,116 | 1,044,900 | 439.116 | 439,116 | 439,116 | £ |

| Segment | Building Type | Household | Res-excl | Res-incl | Unit | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Building Size | CA | FA | SFH | S | M | L | S | M | L | ||

| Scaling | Number of Customers | 10,000 | 10,000 | 10,000 | 500 | 500 | 500 | 500 | 500 | 500 | |

| Revenue per customer | aFRR+ Revenue | 10.34 | 18.09 | 25.84 | 45.08 | 225.39 | 901.57 | 178.08 | 890.41 | 3561.63 | € |

| DA Revenue | 3.63 | 6.35 | 9.08 | 16.09 | 80.45 | 321.78 | 70.55 | 352.74 | 1410.96 | € | |

| Revenue | 13.97 | 24.44 | 34.91 | 61.17 | 305.84 | 1223.35 | 248.63 | 124,315 | 4972.59 | € | |

| Contribution margin 1 | Customer Remuneration | 6.98 | 12.22 | 17.46 | 30.58 | 152.92 | 611.67 | 124.31 | 621.57 | 2486.29 | € |

| Customer Savings Due to Shedding | 5.30 | 9.27 | 13.24 | 16.70 | 83.52 | 334.08 | 64.96 | 324.81 | 1299.25 | € | |

| Customer Savings Total | 12.28 | 21.49 | 30.70 | 47.29 | 236.44 | 945.76 | 189.28 | 946.39 | 3785.54 | € | |

| Customer Savings Relative | 6% | 6% | 6% | 8% | 8% | 8% | 8% | 8% | 8% | share | |

| Contribution Margin 1 | 7 | 12 | 17 | 31 | 153 | 612 | 124 | 622 | 2486 | € | |

| Contribution margin 2 | Customer Fixed Costs | 80 | 94 | 108 | 282 | 372 | 584 | 603 | 1847 | 5624 | € |

| Contribution Margin 2 | −73 | −82 | −91 | −251 | −219 | 28 | −479 | −1225 | −3138 | € | |

| Operational profit | Overall Contribution Margin | −730,171 | −817,800 | −905,428 | −125,708 | −109,541 | 13,837 | −239,343 | −612,713 | −1,568,853 | € |

| Aggregator Fixed Costs | 659,400 | 659,400 | 659,400 | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | € | |

| Operational Profit | −1,389,571 | −1,477,200 | −1,564,828 | −636,308 | −620,141 | −496,763 | −749,943 | −1,123,313 | −2,079,453 | € | |

| Segment | Building Type | Household | Res-excl | Res-incl | Unit | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Building Size | CA | FA | SFH | S | M | L | S | M | L | ||

| Scaling | Number of Customers | 10,000 | 10,000 | 10,000 | 500 | 500 | 500 | 500 | 500 | 500 | |

| Revenue Per Customer | Energy Costs Optimised | 96.07 | 165.86 | 235.66 | 429.97 | 2106.87 | 8409.48 | 1720.13 | 8576.64 | 34,288.56 | € |

| Energy Costs Bau | 216.68 | 364.88 | 513.08 | 615.00 | 3015.00 | 12,015.00 | 2415.00 | 12,015.00 | 48,015.00 | € | |

| Revenue | 120.61 | 199.02 | 277.42 | 185.03 | 908.13 | 3605.52 | 694.87 | 3438.36 | 13,726.44 | € | |

| Contribution Margin 1 | Customer Remuneration | 60.31 | 99.51 | 138.71 | 92.51 | 454.07 | 1802.76 | 347.44 | 1719.18 | 6863.22 | € |

| Customer Savings Relative | 28% | 27% | 27% | 15% | 15% | 15% | 14% | 14% | 14% | share | |

| Contribution Margin 1 | 60 | 100 | 139 | 93 | 454 | 1803 | 347 | 1719 | 6863 | € | |

| Contribution Margin 2 | Customer Fixed Costs | 80 | 94 | 108 | 282 | 372 | 584 | 603 | 1847 | 5624 | € |

| Contribution Margin 2 | −20 | 6 | 31 | −189 | 82 | 1219 | −256 | −128 | 1239 | € | |

| Operational Profit | Overall Contribution Margin | −196,927 | 55.078 | 307,083 | −94,743 | 41,033 | 609,381 | −127,782 | −63.910 | 619,609 | € |

| FLESCO Fixed Costs | 659,400 | 659.400 | 659,400 | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | € | |

| Operational Profit | −856,327 | −604.322 | −352,317 | −605,343 | −469,567 | 98,781 | −638,382 | −574,510 | 109,009 | € | |

| Segment | Building Type | Office | Shop | BEV | Unit | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Building Size | S | M | L | NFS | SM | SC | Single | Residen. | Business | ||

| Scaling | Number of Customers | 500 | 500 | 500 | 500 | 500 | 5 | 10,000 | 500 | 500 | |

| Revenue Per Customer | Energy Costs Optimised | 10,323.41 | 51,593.04 | 137,571.45 | 3085.65 | 8475.04 | 513,281.09 | 90.78 | 1613.02 | 4024.04 | € |

| Energy Costs Bau | 14,415.00 | 72,015.00 | 192,015.00 | 4335.00 | 11895.00 | 720,015.00 | 234.86 | 4334.66 | 6567.00 | € | |

| Revenue | 4091.59 | 20,421.96 | 54,443.55 | 1249.35 | 3419.96 | 206,733.91 | 144.08 | 2721.64 | 2542.96 | € | |

| Contribution Margin 1 | Customer Remuneration | 2045.80 | 10,210.98 | 27,221.78 | 624.67 | 1709,98 | 103,366.95 | 72.04 | 1360.82 | 1271.48 | € |

| Customer Savings Relative | 14% | 14% | 14% | 14% | 14% | 14% | 31% | 31% | 19% | share | |

| Contribution Margin 1 | 2046 | 10,211 | 27,222 | 625 | 1710 | 103,367 | 72 | 1361 | 1271 | € | |

| Contribution Margin 2 | Customer Fixed Costs | 400 | 696 | 1206 | 310 | 310 | 1930 | 48 | 144 | 256 | € |

| Contribution Margin 2 | 1646 | 9515 | 260,16 | 315 | 1400 | 101,437 | 24 | 1217 | 1015 | € | |

| Operational Profit | Overall Contribution Margin | 822,898 | 4,757,489 | 13,007,888 | 157,337 | 699,990 | 507,185 | 240,413 | 608,411 | 507,741 | € |

| FLESCO Fixed Costs | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | 510,600 | 659,400 | 510,600 | 510,600 | € | |

| Operational Profit | 312,298 | 4,246,889 | 12,497,288 | −353,263 | 189 390 | −3415 | −418,987 | 97,811 | −2859 | € | |

| Segment | Building Type | Household | Res-excl | Res-incl | Office | Shop | BEV | Unit |

|---|---|---|---|---|---|---|---|---|

| Building Size | SFH | L | L | L | SC | Business | ||

| Scaling | Number of Customers | 10,000 | 500 | 500 | 500 | 5 | 500 | |

| Revenue Per Customer | Energy Costs Optimised | 311.93 | 11,265.89 | 46,632.31 | 183,726.70 | 694,647.09 | 5400.09 | £ |

| Energy Costs Bau | 518.80 | 17,060.23 | 68,060.23 | 272,060.23 | 1,020,060.23 | 9342.23 | £ | |

| Revenue | 206.87 | 5794.34 | 21,427.92 | 88,333.52 | 325,413.13 | 3942.14 | £ | |

| Contribution Margin 1 | Customer Remuneration | 103.43 | 2897.17 | 10,713.96 | 44,166.76 | 162,706.57 | 1971.07 | £ |

| Customer Savings Relative | 20% | 17% | 16% | 16% | 16% | 21% | share | |

| Contribution Margin 1 | 103 | 2897 | 10,714 | 44,167 | 162,707 | 1971 | £ | |

| Contribution Margin 2 | Customer Fixed Costs | 93 | 502 | 4837 | 1037 | 1660 | 310 | £ |

| Contribution Margin 2 | 11 | 2395 | 5877 | 43,130 | 161,047 | 1661 | £ | |

| Operational Profit | Overall Contribution Margin | 105,547 | 119,7465 | 293,8660 | 2156,4801 | 805,234 | 830,734 | £ |

| FLESCO Fixed Costs | 567,084 | 439,116 | 439,116 | 439,116 | 439,116 | 439,116 | £ | |

| Operational Profit | −461,537 | 758,349 | 249,9544 | 2112,5685 | 366,118 | 391,618 | £ |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pressmair, G.; Amann, C.; Leutgöb, K. Business Models for Demand Response: Exploring the Economic Limits for Small- and Medium-Sized Prosumers. Energies 2021, 14, 7085. https://doi.org/10.3390/en14217085

Pressmair G, Amann C, Leutgöb K. Business Models for Demand Response: Exploring the Economic Limits for Small- and Medium-Sized Prosumers. Energies. 2021; 14(21):7085. https://doi.org/10.3390/en14217085

Chicago/Turabian StylePressmair, Guntram, Christof Amann, and Klemens Leutgöb. 2021. "Business Models for Demand Response: Exploring the Economic Limits for Small- and Medium-Sized Prosumers" Energies 14, no. 21: 7085. https://doi.org/10.3390/en14217085