Analyzing Trade in Continuous Intra-Day Electricity Market: An Agent-Based Modeling Approach

, , and

, , and

Abstract

:1. Introduction

2. Related Works

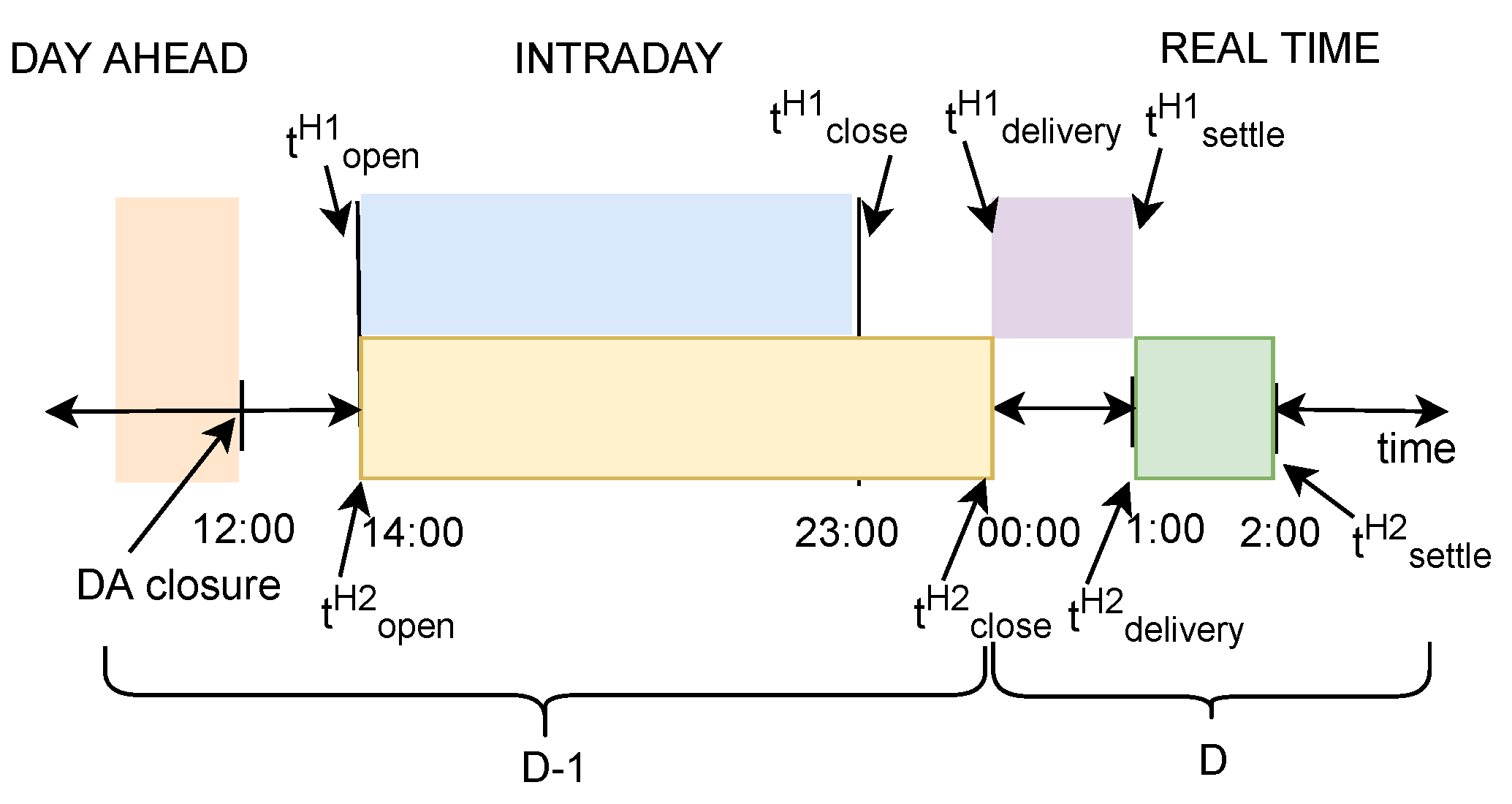

3. Principles of Continuous Intra-Day Markets

3.1. Market Set-Up

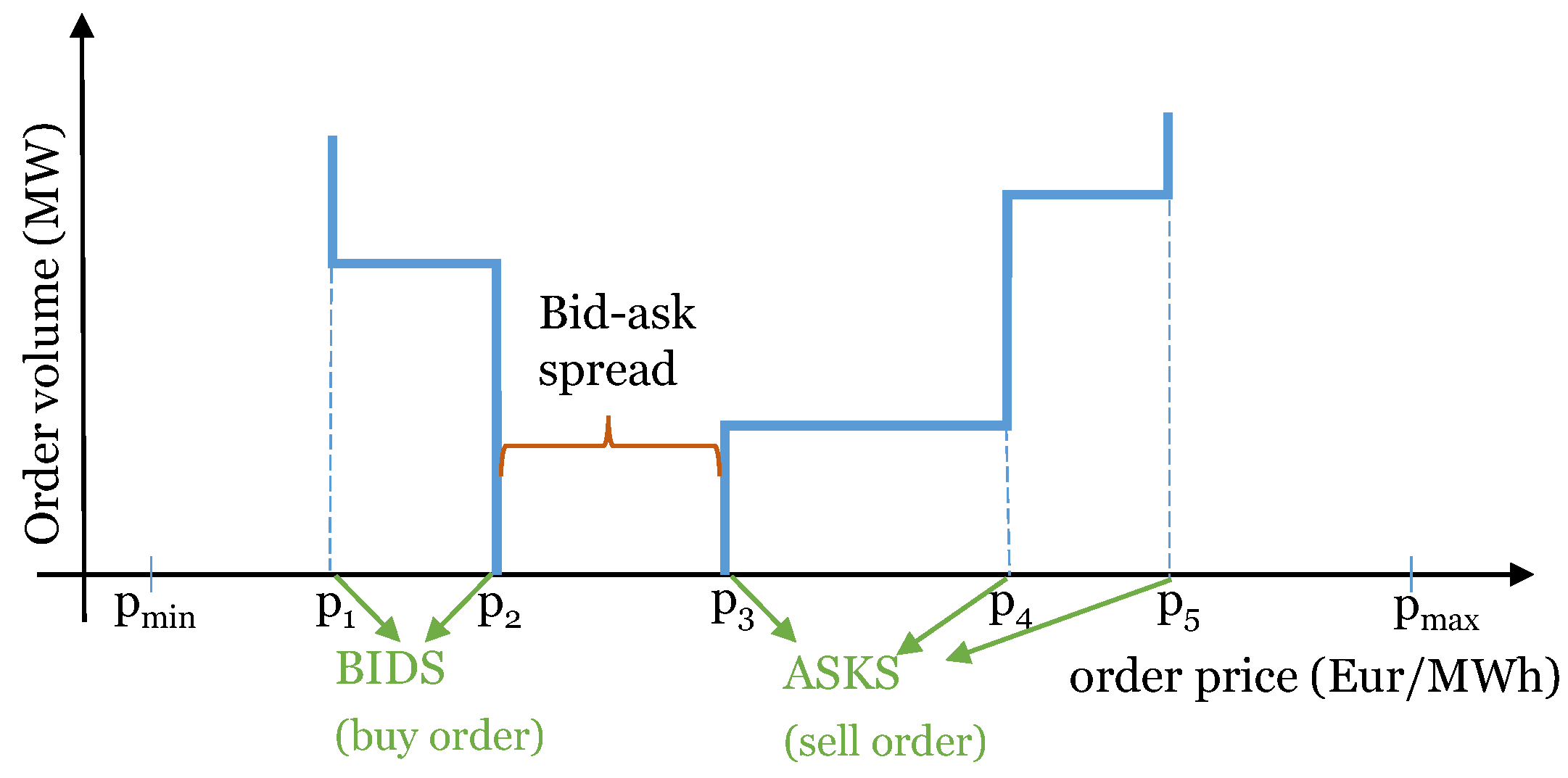

3.2. Market Mechanism

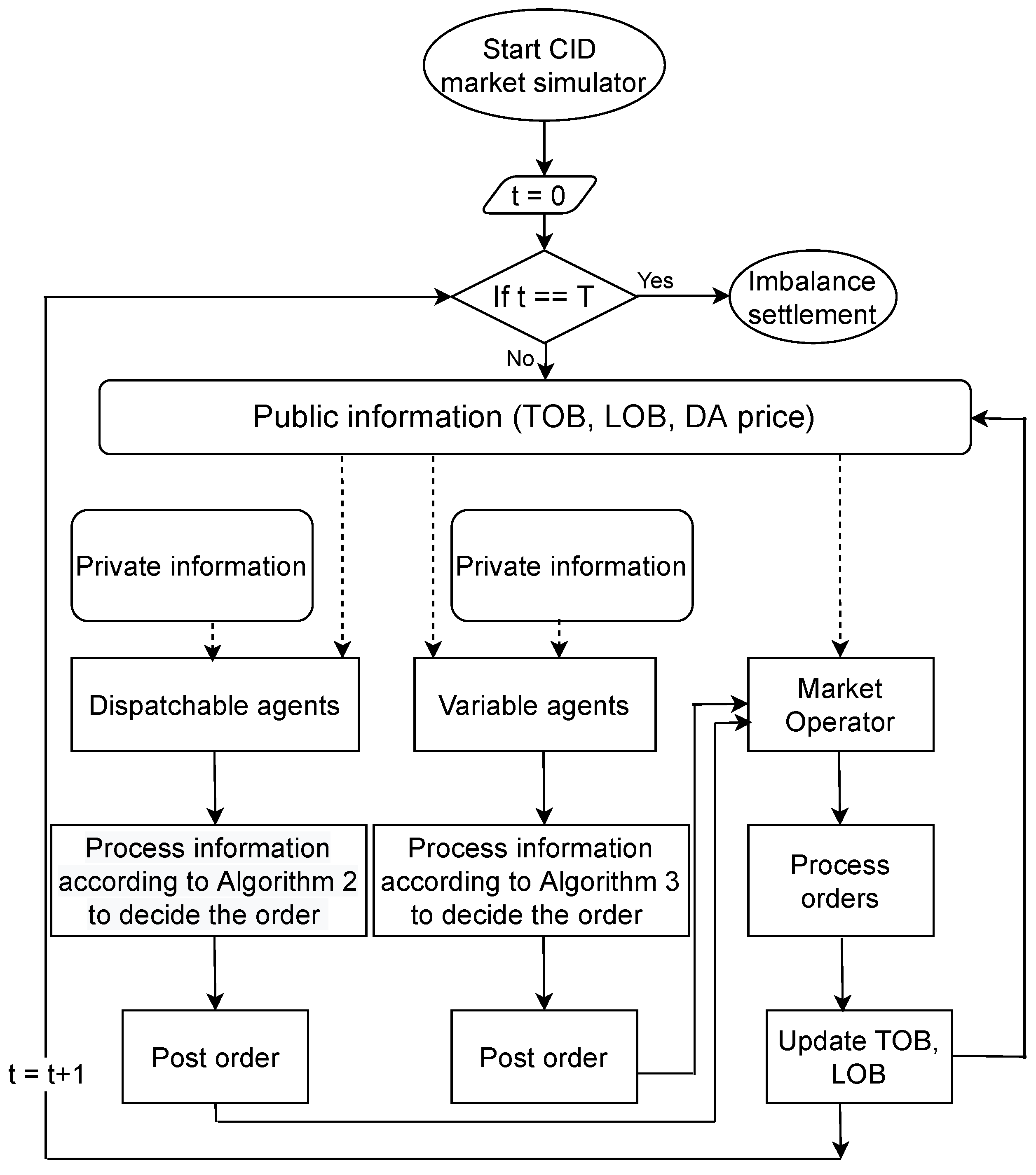

4. Continuous Market Clearing

4.1. Continuous Market Operation

| Algorithm 1 Run the market |

|

4.2. Order Processing

4.3. Updating Agents’ Beliefs

4.4. Transaction Confirmation

5. Trading Agents

5.1. Generic Agent

5.1.1. Private Information

5.1.2. Potential Functionalities

(1) Strategy

(2) Outage

(3) Imbalance Price forecaster

(4) Confirm a Transaction Locally

5.2. Dispatchable Agent

5.2.1. Private Information

5.2.2. Potential Functionalities

(1) Strategy

| Algorithm 2 Steps to decide the orders to be placed |

5.3. Variable Agent

5.3.1. Private Information

5.3.2. Potential Functionalities

(1) Forecasting functionality

- Cosinusoidal forecast:

- Sinusoidal forecast:

- Constant offset forecast:where denotes the amplitude/offset of the error and is a constant that can adjust the frequency of the error. Thus, the private information of a variable agent i writes aswhere is the private information available to the agent i at time t according to Equation (1) and is the forecast of production/consumption of the variable agent.

(2) Strategy

| Algorithm 3 Variable agent strategy |

6. Pricing Strategies

6.1. Generic Strategy

6.2. Naive Strategy

6.3. Modified Trader AA Strategy

- The competitive equilibrium price estimate is computed at each step as the mean value of K past transactions according to:

- The aggressiveness a is updated aswhere is a proxy of the degree of aggressiveness that would form a price equal to the best bid price , if the agent is a buyer and the last event is a bid, or equal to the best ask price, , if the agent is a seller and the last event is an ask. In case the last event is a transaction, the price reference is the transaction price . The learning process of the aggressiveness takes place in a step-wise manner that depends on the step-size parameter .

- The target price parameter is only updated when a transaction takes place, while the magnitude of the update depends on the market volatility through function . The updated parameters are given by

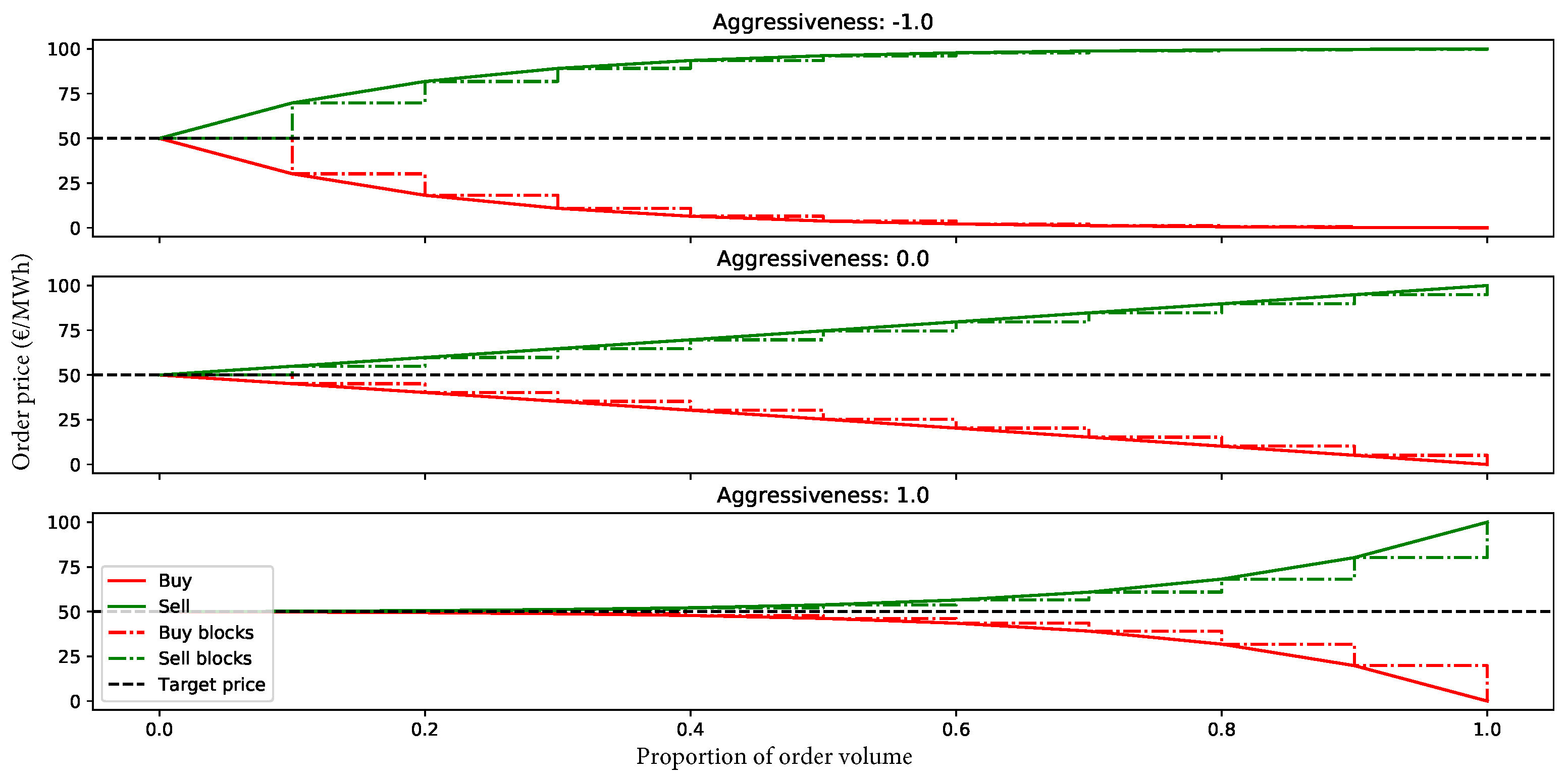

- The target price at each step t is computed as a function of the aggressiveness level a, the estimated equilibrium price and the limit prices to buy/sell (, ). Compactly, it writes:where defines the shape of the exponential.

7. Imbalance Settlement

7.1. Impact on System Regulation

8. Test Case, Results and Discussion

8.1. Test Case Set-Up

8.1.1. Trading Agents Configuration

8.1.2. Market Operator Configuration

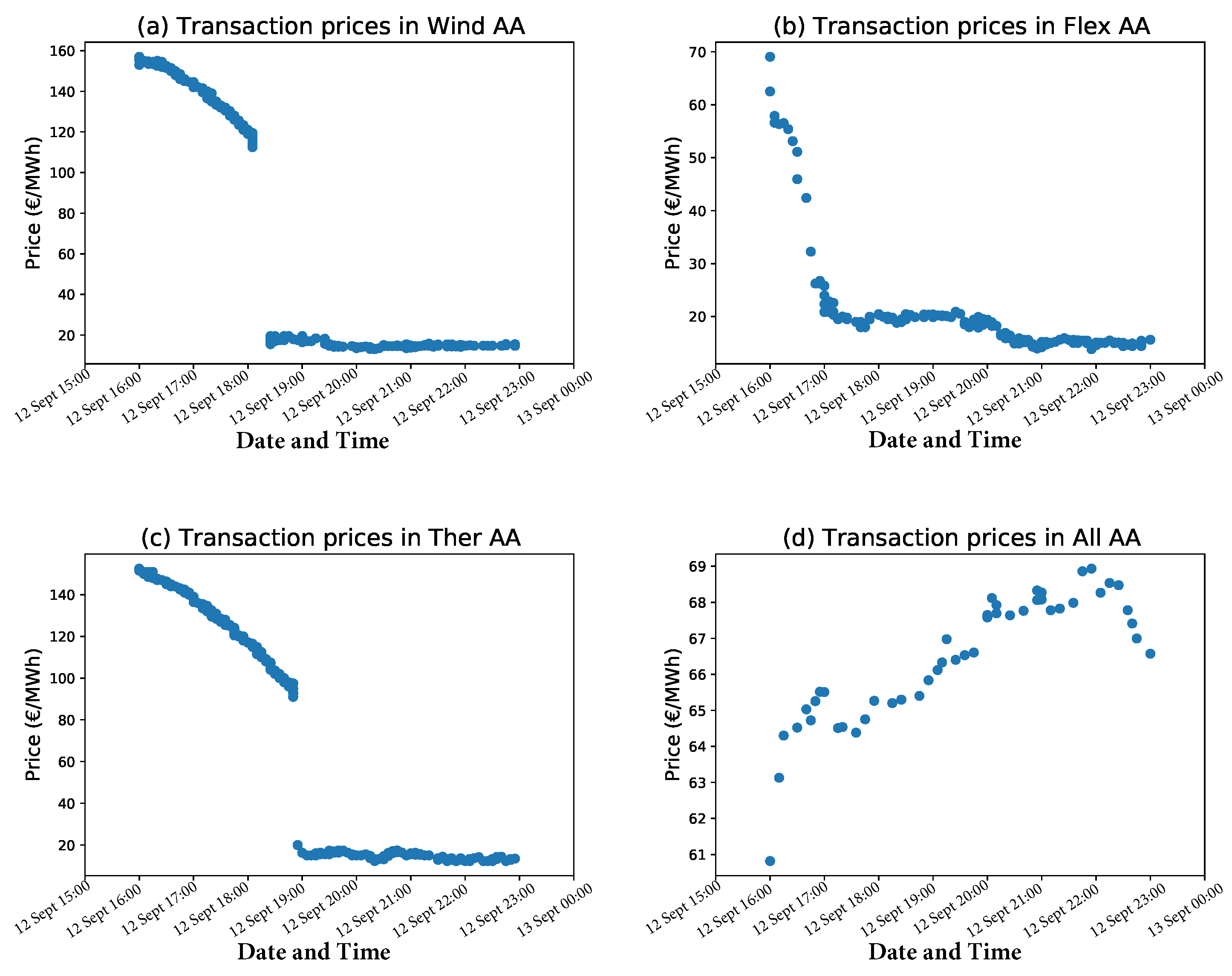

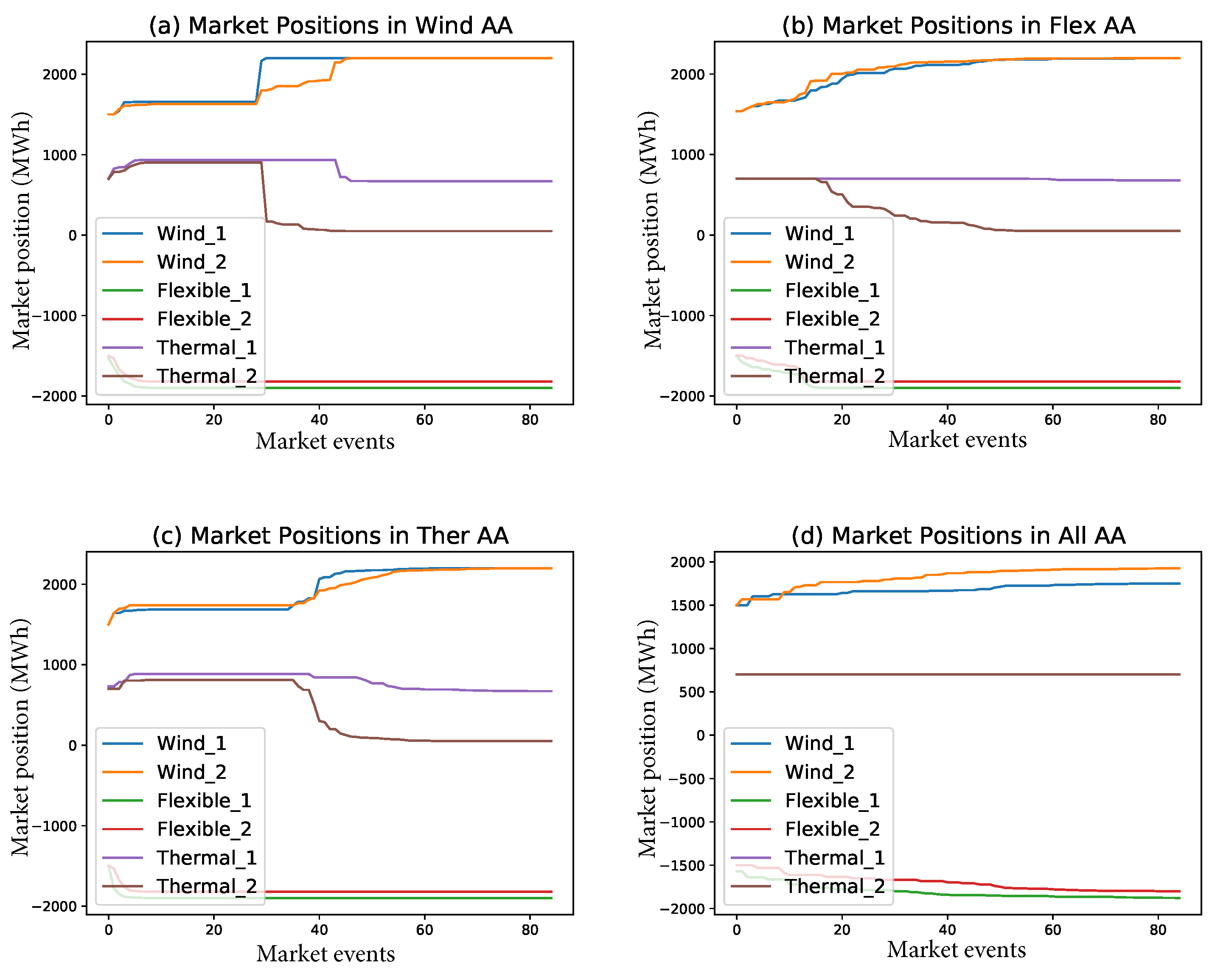

8.2. Evaluating the Effect of Different Pricing Strategies

8.3. Comparing the Response to Capacity Outages

- Case I: all the agents follow the naive strategy;

- Case II: only the agent that suffers the outage follows an MTAA strategy while all the other agents are naive;

- Case III: all agents adopt the MTAA strategy except the one that suffers the outage;

- Case IV: all agents follow the MTAA strategy.

8.4. Evaluating the Effect of the Imbalance Price Information Asymmetry

8.4.1. Effect of Information Asymmetry on the Wind Agent

8.4.2. Effect of Information Asymmetry on the Flexible Agent

8.5. Discussion

9. Conclusions

- The proposed ABM provides a formalized tool to study the behavior of agents (market players) under different CID market settings;

- The MTAA strategy presented in this work outperforms the benchmark (i.e., a naive strategy) in terms of revenue and coping after outages;

- Information asymmetry among agents regarding the imbalance prices influences the transaction prices in the CID market, favoring those agents with more information.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Nomenclature

| Abbreviations | |

| Adaptive aggressiveness | |

| Agent-based model | |

| Continuous double auction | |

| Continuous intra-day | |

| Day ahead | |

| First-come–first-serve | |

| Intra-day | |

| Imbalance settlement period | |

| Limit order book | |

| Market operator | |

| Modified trader adaptive aggressiveness | |

| Renewable energy sources | |

| Top of the order book | |

| Wind power producer | |

| Cross-border intra-day | |

| Indices | |

| i | Agent that participates in the CID market |

| t | Time |

| j | Order number |

| Parameters | |

| Gate opening time for intra-day trade for hourly product | |

| Gate closing time for intra-day trade for hourly product | |

| Start time of the physical delivery for hourly product | |

| End time of the physical delivery for hourly product | |

| CID trading horizon for a specific CID product | |

| Discretization step for the trading horizon | |

| N | Total number of agents participating in the CID market |

| Day-ahead price | |

| Position of an agent i after DA market clearing | |

| Effective capacity of agent i at time | |

| n | Number of orders placed by an agent in CID market |

| Factor to represent the deviation of the forecast with respect tothe real | |

| imbalance price | |

| Real positive imbalance price | |

| Real negative imbalance price | |

| Up-regulation price | |

| Down-regulation price | |

| Minimum stable load of a dispatchable agent i | |

| A step factor to update limit prices | |

| Initial limit of an agent to buy | |

| Initial limit of an agent to sell | |

| Amplitude/offset of the forecast error | |

| Parameter to define the shape of forecast of agent i at time t | |

| Frequency of arrival of new forecasts | |

| The actual production/consumption of a variable agent | |

| R | Parameter indicating the size and sign of regulation volume to counteract |

| the system imbalance | |

| k | Probability of having a positive imbalance |

| f | Imbalance influence factor |

| Variables | |

| Binary Variables | |

| Y | Binary variable that indicates if the system was up- or down-regulating |

| Order side of an order posted by agent i at time t | |

| Positive Variables | |

| The volume that a dispatchable agent i can buy at t | |

| The volume that a dispatchable agent i can sell at t | |

| Effective capacity of an agent i at time t | |

| Volume of an order posted by agent i at time t | |

| Remainder volume from order i at time t | |

| Matched volume from order i at time t | |

| Best bid volume at time t | |

| Best ask volume at time t | |

| Volumes matched in a transaction | |

| Continuous Variables | |

| Cumulative revenues collected by an agent i at each time-step t of the | |

| trading process | |

| Price of an order posted by agent i at time t | |

| Best buy price at time t | |

| Best ask price at time t | |

| Volume weighted-average price in the bid side at t | |

| Volume weighted-average price in the ask side at t | |

| Price at which orders are matched | |

| The net volume of energy traded by agent i until time-step t | |

| Imbalance of an agent i at time t | |

| Recent prediction of negative imbalance price by agent i at time t | |

| Recent prediction of positive imbalance price by agent i at time t | |

| Final imbalance of an agent i | |

| Maximum price that an agent i is willing to pay to buy at time t | |

| Minimum price at which an agent i can sell at time t | |

| The market position at the closing time of the CID market | |

| The recent forecast of uncertain production/consumption at t | |

| Error component that relates the forecasted and actual production/ | |

| consumption of variable agents | |

| Best bid price of the previous step | |

| Best ask price of the previous step | |

| Best bid volume of the previous step | |

| Best ask volume of the previous step | |

| Single imbalance pricing settlement amount | |

| Dual imbalance pricing amount under up-regulation | |

| Dual imbalance pricing amount under down-regulation | |

| The cumulative imbalance caused by agents trading in the CID market | |

| Compilation of Variables | |

| Order book that contains outstanding bids and asks at time t | |

| Order posted by an agent i at time t | |

| Top of the order book at time t | |

| Sets | |

| I | Set of agents participating in the CID market |

| T | Set of time-steps available for trading in CID market |

| Set of candidate prices in naive strategy | |

| A private ledger by agent i to track its outstanding orders in the CID | |

| market at time-step t | |

| Set of private information available to agent i at time t | |

| Set of private information available to a dispatchable agent i at time t | |

| Outage Parameters | |

| Probability of outage | |

| Outage percentage | |

| Naive Strategy Parameters and Variables | |

| Size of price range considered in naive strategy | |

| m | The number of evenly spaced parts of price range in naive strategy |

| Minimum price value at which a naive agent can buy | |

| Maximum price value for a naive agent to buy | |

| Minimum price value at which a naive agent can sell | |

| Maximum price value for a naive agent to sell | |

| Set containing the candidate prices for ask orders | |

| Set containing the candidate prices for bid orders | |

| Price step | |

| MTAA Strategy Parameters and Variables | |

| User-defined minimum price value for MTAA strategy | |

| User-defined maximum price in the MTAA strategy | |

| Price of an ask order determined by MTAA strategy for agent i at time t | |

| Price of a bid order determined by MTAA strategy for agent i at time t | |

| Aggressiveness of agent i | |

| Target price for an agent i | |

| Parameter that relates r with | |

| Competitive equilibrium price | |

| Step-size parameter to update aggressiveness | |

| Market volatility | |

| Set of price values of ask orders as a function of proportion of order volume | |

| Set of price values of bid orders as a function of proportion of order volume | |

| Operators | |

| Maximum operator | |

| Minimum operator | |

Appendix A. Algorithms

| Algorithm A1 Order processing |

|

| Algorithm A2 Match |

|

| Algorithm A3 Update LOB |

|

| Algorithm A4 Update posted order |

|

References

- ENTSOE. Power Facts Europe 2019. Available online: https://eepublicdownloads.blob.core.windows.net/public-cdn-container/clean-documents/Publications/ENTSO-E%20general%20publications/ENTSO-E_PowerFacts_2019.pdf (accessed on 8 March 2021).

- Neuhoff, K.; Ritter, N.; Salah-Abou-El-Enien, A.; Vassilopoulos, P. Intraday Markets for Power: Discretizing the Continuous Trading? 2016. Available online: https://ssrn.com/abstract=2723902 (accessed on 25 June 2021).

- Ciferri, D.; D’Errico, M.C.; Polinori, P. Integration and convergence in European electricity markets. Econ. Politica 2020, 37, 463–492. [Google Scholar] [CrossRef] [Green Version]

- Pogosjan, D.; Winberg, J. Förändringar av Marknadsdesign och deras påverkan på balanshållningen i det Svenska Kraftsystemet: En kartläggning och analys av de Balansansvarigas arbetsgång. 2013. Available online: https://www.svk.se/siteassets/5.jobba-har/dokument-exjobb/forandringar-av-marknadsdesign-och-deras-paverkan-balanshallningen.pdf?_t_id=qWowEhUA1rBRRNtzXdqH-w==&_t_uuid=-UEFAhWSR7eX49e5YldH_Q&_t_q=sf6-gas&_t_tags=language:sv,siteid:40c776fe-7e5c-4838-841c-63d91e5a03c9,andquerymatch&_t_hit.id=SVK_WebUI_Models_Media_OfficeDocument/_ffc3ccaf-a4bd-441d-a665-a05a3e9b59d8&_t_hit.pos=259 (accessed on 15 February 2021).

- Dobschinski, J.; De Pascalis, E.; Wessel, A.; von Bremen, L.; Lange, B.; Rohrig, K.; Saint-Drenan, Y.M.; Fraunhofer, I.W.E.S.; ForWind, O.; Germany, E. The potential of advanced shortest-term forecasts and dynamic prediction intervals for reducing the wind power induced reserve requirements. In Proceedings of the Scientific Proceedings of the European Wind Power Conference, Warsaw, Poland, 20–23 April 2010; pp. 177–182. [Google Scholar]

- Holttinen, H. Handling of wind power forecast errors in the nordic power market. In Proceedings of the Probabilistic Methods Applied to Power Systems, Stockholm, Sweden, 11–15 June 2006. [Google Scholar]

- Le, H.L.; Ilea, V.; Bovo, C. Integrated European intra-day electricity market: Rules, modeling and analysis. Appl. Energy 2019, 238, 258–273. [Google Scholar] [CrossRef]

- Schittekatte, T.; Reif, V.; Meeus, L. The EU Electricity Network Codes (2019 ed.). Available online: https://fsrglobalforum.eu/wp-content/uploads/2019/03/FSR_2019_EU_Electricity_Network_Codes.pdf (accessed on 21 February 2021).

- Nordic TSOs. Short-Term Markets. Available online: https://www.svk.se/siteassets/press-och-nyheter/nyheter/tsos-discussion-paper-for-consultation.pdf (accessed on 4 December 2020).

- Coulter, K. 5 Trends Reshaping Today’s Global Power Market. Available online: https://www.renewableenergyworld.com/2020/01/14/5-trends-reshaping-todays-global-power-market/#gref (accessed on 12 March 2021).

- Nord Pool. Bots Disguised as Electricity Traders Are Placing Orders. Available online: https://careers.nordpoolgroup.com/blog/posts/25998-bots-disguised-as-electricity-traders-are-placing-orders (accessed on 5 April 2021).

- NordPool. Nord Pool Key Statistic July 2019. Available online: https://www.nordpoolgroup.com/message-center-container/newsroom/\exchange-message-list/2019/q3/nord-pool-key-statistics—july-2019/ (accessed on 10 December 2020).

- Shinde, P.; Amelin, M. A literature review of intraday electricity markets and prices. In Proceedings of the 2019 IEEE Milan PowerTech, Milan, Italy, 23–27 June 2019; pp. 1–6. [Google Scholar]

- Skajaa, A.; Edlund, K.; Morales, J.M. Intraday trading of wind energy. IEEE Trans. Power Syst. 2015, 30, 3181–3189. [Google Scholar] [CrossRef] [Green Version]

- Boukas, I.; Ernst, D.; Théate, T.; Bolland, A.; Huynen, A.; Buchwald, M.; Wynants, C.; Cornélusse, B. A deep reinforcement learning framework for continuous intraday market bidding. arXiv 2020, arXiv:2004.05940. [Google Scholar]

- Richard Scharff and Mikael Amelin. Trading behaviour on the continuous intraday market elbas. Energy Policy 2016, 88, 544–557. [Google Scholar] [CrossRef]

- Alexander von Selasinsky. The Integration of Renewable Energy Sources in Continuos Intraday Markets for Electricity. Ph.D. Thesis, TU Dresden, Dresden, Germany, 2016.

- Vytelingum, P. The Structure and Behaviour of the Continuous Double Auction. Ph.D. Thesis, University of Southampton, Southampton, UK, 2006. [Google Scholar]

- Veselka, T.; Boyd, G.; Conzelmann, G.; Koritarov, V.; Macal, C.; North, M.; Schoepfle, B.; Thimmapuram, P. Simulating the Behavior of Electricity Markets with an Agent-Based Methodology: The Electric Market Complex Adaptive Systems (emcas) Model; Center for Energy, Environmental, and Economic Systems Analysis (CEEESA): Vancouver, Canada, 2002; Available online: https://ceeesa.es.anl.gov/pubs/43943.pdf (accessed on 25 June 2021).

- Charles, M.; Thimmapuram, P.; Koritarov, V.; Conzelmann, G.; Veselka, T.; North, M.; Mahalik, M.; Botterud, A.; Cirillo, R. Agent-based modeling of electric power markets. In Proceedings of the IEEE Winter Simulation Conference, Savannah, GA, USA, 7–10 December 2014. [Google Scholar]

- Grozev, G.; Batten, D.; Anderson, M.; Lewis, G.; Mo, J.; Katzfey, J. Nemsim: Agent-based simulator for australia’s national electricity market. In Proceedings of the SimTecT 2005 Conference Proceedings, Sydney, Australia, 9–12 May 2005. [Google Scholar]

- Audouin, R.; Hermon, F.; Entriken, R. Extending a spot market multi-agent simulator to model investment decisions. In Proceedings of the 2006 IEEE PES Power Systems Conference and Exposition, Atlanta, GA, USA, 29 October–1 November 2006. [Google Scholar]

- Harp, S.A.; Brignone, S.; Wollenberg, B.F.; Samad, T. Sepia. a simulator for electric power industry agents. IEEE Control Syst. Mag. 2000, 20, 53–69. [Google Scholar]

- Sun, J.; Tesfatsion, L. An agent-based computational laboratory for wholesale power market design. In Proceedings of the 2007 IEEE Power Engineering Society General Meeting, Tampa, FL, USA, 24–28 June 2007; pp. 1–6. [Google Scholar]

- Praça, I.; Ramos, C.; Vale, Z.; Cordeiro, M. Mascem: A multiagent system that simulates competitive electricity markets. IEEE Intell. Syst. 2003, 18, 4–60. [Google Scholar] [CrossRef]

- Zhou, Z.; Chan, W.K.V.; Chow, J.H. Agent-based simulation of electricity markets: a survey of tools. Artif. Intell. Rev. 2007, 28, 305–342. [Google Scholar] [CrossRef]

- Aliabadi, D.E.; Kaya, M.; Şahin, G. An agent-based simulation of power generation company behavior in electricity markets under different market-clearing mechanisms. Energy Policy 2017, 100. [Google Scholar] [CrossRef]

- Lopes, F.; Coelho, H. Electricity Markets with Increasing Levels of Renewable Generation: Structure, Operation, Agent-Based Simulation, and Emerging Designs; Springer: Berlin/Heidelberg, Germany, 2018; Volume 144. [Google Scholar]

- Vermeulen, B.; Pyka, A. Agent-based Modeling for Decision Making in Economics under Uncertainty. Econ. Open-Access Open-Assess. E-J. 2016, 10, 1–33. [Google Scholar] [CrossRef] [Green Version]

- Aliabadi, D.E.; Kaya, M.; Sahin, G. Competition, risk and learning in electricity markets: An agent-based simulation study. Appl. Energy 2017, 195, 1000–1011. [Google Scholar]

- Poplavskaya, K.; Lago, J.; de Vries, L. Effect of market design on strategic bidding behavior: Model-based analysis of European electricity balancing markets. Appl. Energy 2020, 270. [Google Scholar] [CrossRef]

- Shinde, P.; Amelin, M. Agent-Based Models in Electricity Markets: A Literature Review. In Proceedings of the 2019 IEEE Chengdu, China Innovative Smart Grid Technologies—Asia (ISGT Asia), Chengdu, China, 21–24 May 2019; pp. 1–6. [Google Scholar]

- Faia, R.; Pinto, T.; Vale, Z.; Corchado, J.M. Portfolio optimization of electricity markets participation using forecasting error in risk formulation. Int. J. Electr. Power Energy Syst. 2018, 106739. [Google Scholar] [CrossRef]

- Canelas, E.; Pinto-Varela, T.; Sawik, B. PortfolioElectricity Portfolio Optimization for Large Consumers: Iberian Electricity Market Case Study. Energies 2018, 13, 106739. [Google Scholar]

- Vytelingum, P.; Cliff, D.; Jennings, N.R. Strategic bidding in continuous double auctions. Artif. Intell. 2008, 172, 1700–1729. [Google Scholar] [CrossRef] [Green Version]

- Luca, M.D.; Cliff, D. Human-agent auction interactions: Adaptive-aggressive agents dominate. IJCAI Int. Jt. Conf. Artif. Intell. 2011, 178–185. [Google Scholar] [CrossRef]

- NordPool. Market Opening and Closing Times. Available online: https://www.nordpoolgroup.com/trading/intraday-trading/order-types/ (accessed on 10 December 2020).

- EPEXSPOT. Epexspot Operational Rules. Available online: https://www.epexspot.com/document/40170/EPEX%20SPOT%20Market%20Rules (accessed on 6 June 2020).

- Cliff, D. BSE: A minimal simulation of a limit-order-book stock exchange. In Proceedings of the 30th European Modeling and Simulation Symposium, EMSS 2018, Budapest, Hungary, 17–19 September 2018; pp. 194–203. [Google Scholar]

- Repository. Intraday Market Simulator. Available online: https://gitlab.uliege.be/Ioannis.Boukas/intraday-market-simulator (accessed on 15 March 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| (MWh) | 2500 | 2400 | 2500 | 2400 | 1000 | 1000 | |

| (MWh) | 1500 | 1400 | −1500 | −1500 | 700 | 700 | |

| (MWh) | 1600 | 1800 | −1800 | −1900 | |||

| (MWh) | 1700 | 1600 | −2400 | −2300 | |||

| (EUR/MWh) | 10 | 10 | 30 | 30 | 80 | 80 | |

| (EUR/MWh) | 150 | 150 | 150 | 150 | 15 | 20 | |

| (EUR/MWh) | 20 | 40 | 100 | 100 | 50 | 50 | |

| (-) | 4 | 4 | 4 | 4 | |||

| (-) | 0.5 | ||||||

| (-) | 20 | ||||||

| Scenario | ||||

|---|---|---|---|---|

| Agent | Wind AA | Consumer AA | Thermal AA | All AA |

| 79.20 | 64.48 | 84.41 | 68.16 | |

| 70.51 | 61.76 | 89.67 | 61.09 | |

| −106.76 | −61.26 | −105.50 | −71.75 | |

| −94.39 | −55.26 | −92.81 | −69.15 | |

| 54.03 | 20.86 | 35.96 | 26.80 | |

| 36.40 | 8.41 | 27.26 | 23.84 | |

| (%) Time | Case I | Case II | Case III | Case IV | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bef. | Af. | (%) | Bef. | Af. | (%) | Bef. | Af. | (%) | Bef. | Af. | (%) | |

| 25% | 65 | 70 | 7.69 | 58 | 62 | 6.89 | 69 | 86 | 24.63 | 77 | 77.8 | 1.04 |

| 50% | 40 | 47 | 17.5 | 25 | 35 | 40 | 68 | 90 | 32.35 | 74.5 | 75 | 0.67 |

| 75% | 20 | 25 | 25 | 20 | 85 | 325 | 65 | 85 | 30.76 | 76.5 | 77.5 | 1.30 |

| (%) Time | Case I | Case II | Case III | Case IV | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bef. | Af. | (%) | Bef. | Af. | (%) | Bef. | Af. | (%) | Bef. | Af. | (%) | |

| 25% | 65 | 165 | 153.8 | 57.5 | 70 | 21.7 | 15 | 165 | 1000 | 76.8 | 77.5 | 0.91 |

| 50% | 45 | 165 | 266.6 | 18 | 80 | 344.4 | 15 | 165 | 1000 | 65 | 67 | 3.07 |

| 75% | 20 | 165 | 725 | 17 | 87 | 411.7 | 15 | 165 | 1000 | 40 | 47 | 17.5 |

| Parameter | Units | Wind1 | |||||

|---|---|---|---|---|---|---|---|

| EUR/MWh | 0.0 | 50.0 | 100.0 | 150.0 | 200.0 | 250.0 | |

| EUR/MWh | 80.5 | 80.5 | 84.0 | 80.0 | 80.0 | 82.0 | |

| EUR/MWh | 73.0 | 73.0 | 15.0 | 14.0 | 13.0 | 12.0 | |

| % | −9.32 | −9.32 | −82.14 | −82.50 | −83.75 | −85.37 | |

| Parameter | Units | Flex1 | ||||

|---|---|---|---|---|---|---|

| EUR/MWh | 0.0 | 50.0 | 150.0 | 250.0 | 300.0 | |

| EUR/MWh | 80.0 | 91.0 | 73.0 | 63.0 | 66.0 | |

| EUR/MWh | 77.0 | 80.0 | 80.1 | 69.2 | 80.0 | |

| % | −3.75 | −1.23 | 9.72 | 9.84 | 21.21 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shinde, P.; Boukas, I.; Radu, D.; Manuel de Villena, M.; Amelin, M. Analyzing Trade in Continuous Intra-Day Electricity Market: An Agent-Based Modeling Approach. Energies 2021, 14, 3860. https://doi.org/10.3390/en14133860

Shinde P, Boukas I, Radu D, Manuel de Villena M, Amelin M. Analyzing Trade in Continuous Intra-Day Electricity Market: An Agent-Based Modeling Approach. Energies. 2021; 14(13):3860. https://doi.org/10.3390/en14133860

Chicago/Turabian StyleShinde, Priyanka, Ioannis Boukas, David Radu, Miguel Manuel de Villena, and Mikael Amelin. 2021. "Analyzing Trade in Continuous Intra-Day Electricity Market: An Agent-Based Modeling Approach" Energies 14, no. 13: 3860. https://doi.org/10.3390/en14133860