1. Introduction

Electricity is usually traded in a short-term market (spot market) and a long-term market via contracts for future delivery (forward contracts). The electricity market is characterized by being highly volatile when compared to other commodity markets. This high volatility in terms of price and quantity is due to market circumstances (e.g., expectations or strategies of each company and economic dynamics) and physical conditions (e.g., climate, water availability, fuel production, or damage to the power transmission network [

1]).

Electricity trading implies the consideration of three main characteristics: (i) the limitation of storage for large amounts of electricity and long periods, (ii) the technical difficulties or environmental and social restrictions for long-distance transmission, and (iii) the intensive use of capital required for expanding systems at a large scale, which presents long and uncertain payback periods. Under those conditions, multiple uncertainties exist in both the electric power system and market operation. As far as the electric power system is concerned, the need for preserving the stability of the system involves different issues—e.g., economic dispatch, unit commitment, optimal power flow and power system expansion planning—that are subject to various uncertainties, including demand variations, transmission interruptions, generator failure, fuel availability, weather conditions, as explained by [

2,

3], and regulatory modifications, among other causes. Those real-time conditions affect the electricity pricing and imply uncertainties over the financial results for the market agents (sellers and buyers) that can drive to significant financial losses or even bankruptcy [

4]. These uncertainty levels are rising due to the increase of renewable energy sources in electric power systems [

5]. All of these factors explain how reliable and economically viable operations of electric power systems depend on a collection of optimization problems to coordinate electric power systems.

To achieve the best results for electricity generators, reduce their risk levels, and reach their business objectives, they must define the quantity of electricity to be sold through forward contracts and to be traded at a spot price. It should be noted that electricity generators face price and quantity uncertainty, unlike in other types of financial products; Ref. [

6] explains the spot price volatility, because electricity cannot be economically stored and must be produced instantaneously to satisfy the demand. In these circumstances, ref. [

7] considers the implications of load uncertainty that cannot be perfectly hedged applying financial derivatives. Ref. [

8] describes how demand unpredictability is a regular matter for any commodity. Holding inventory is an answer to mitigate quantity risk for those commodities that can be economically stored; this is mentioned by [

9] as a limitation to execute intertemporal arbitrage in electricity markets.

Quantity risk (or volumetric risk) is driven by different conditions, such as the economic cycle, fuel availability, hydrologic inflows, or climate. These conditions also affect price; hence, generated quantity and price tend to be correlated. Due to the limitations regarding electricity storage for extended periods (i.e., months or years), the cost-of-carry valuation is not applicable to value the theoretical forward price. Therefore, market agents set the forward price based on their expectations and the risks they assume, which gives rise to the forward risk premium (FRP).

This FRP has been studied by [

10,

11] for the Pennsylvania–New Jersey–Maryland (PJM) electricity market; Ref. [

12] for the Nord Pool; Ref. [

13] for the Colombian electricity market; Ref. [

14] for the European Electricity Exchange (EEX); and [

15] for the British electricity market [

16]. The incorporation of an FRP immediately leads to a difference between the forward price and the spot price expectations. Regarding the behavior of uncertainty sources, the literature studies typically address the hedging problem in electricity markets by assuming normality either on the variables or on their logarithm. Although this is a common assumption—used by [

7,

8], and [

17], among other authors—to properly select the number of forward contracts to hedge the risk associated with transactions in electricity markets, it presents limitations to deal with problems that involve cases of skewness and kurtosis.

Nevertheless, ref. [

18] indicates that some variables in electricity markets exhibit conditions of skewness and kurtosis and higher-order moments that are not adequately represented only using normal distributions. These authors show that semi-nonparametric (SNP) distributions allow a better fit for hydrologic inflows, spot price, and even demand for electricity data. Ref. [

19] shows that SNP distributions serve to treat historical variables featuring skewness and heavy tails. Ref. [

20] uses SNP modeling to describe the co-movements of price and volume in the stock market of the United States (US), and [

21] also employs the SNP distribution to model returns in the US and United Kingdom (UK) stock markets. Other works that adopt SNP approaches to expand series beyond the traditional normal or lognormal distributions are those by [

22], who measures the productivity of researchers worldwide, and [

23], who estimates the size distribution of US firms.

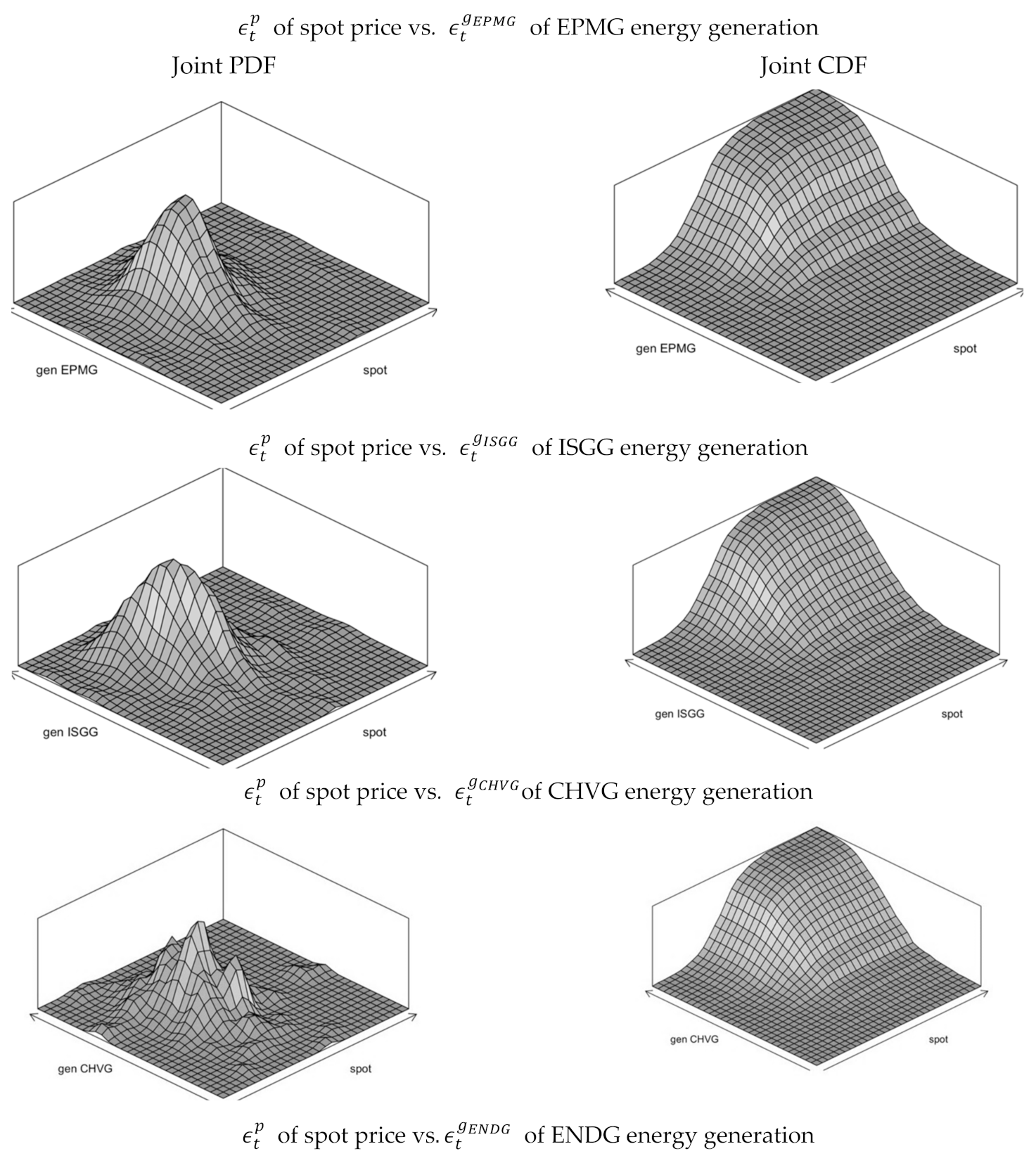

In this study, we go a step further by considering the uncertain components of each electricity generator’s price and energy generation understudy to follow a joint SNP distribution. Ref. [

24] described this type of distribution and explained how it is estimated, and more recently, refs. [

25,

26] applied related densities to forecast financial variables. However, to the best of our knowledge, this is the first attempt to model electricity markets in a multivariate SNP framework. Furthermore, the joint modeling of price and quantity through a SNP distribution allows us to capture not only the correlation between both variables but also the dependence between all moment structures. All of these features pay a fundamental role on the risk positions of electricity generators and their strategies.

As a direct application of the model, we propose a static hedging strategy for electricity generators that participate in a competitive market where hedging is carried out through forward contracts that include a risk premium in their valuation. We consider the spot price and energy generation variables to follow a bivariate SNP distribution in terms of the Gram–Charlier expansion. This distribution allows us to not only model the mean, the variance, and their correlation but also the skewness, the kurtosis, and higher-order moments. We employ Monte Carlo simulation to analyze the effect of three risk indicators (standard deviation, value-at-risk (VaR), and conditional VaR (CVaR) on energy sales. We consider the Colombian electricity market as the case study, where the energy sources are predominant renewables.

The main contribution of the paper to the analysis of electricity markets is the structuring of an energy portfolio that does not impose the assumption of normality in both price and energy generation. The results show that the optimal quantity of energy to be sold through forward contracts is dependent not only on the conditions of spot price and quantity uncertainty but also on the way market agents weigh the assumed risk levels. Particularly, this methodology is used for hydropower generators affected by flow regimen aspects. Furthermore, the number of forward sales is determined by the correlation between price and energy generation and the FRP.

The rest of the paper is structured as follows.

Section 2 introduces the mathematical model and the methodology implemented to jointly model prices and quantity uncertainty.

Section 3 describes the data used in the case study.

Section 4 discusses the results, analyzing the sensitivity of the risk of forward energy contracts not only to the SNP density characteristics but also to the rest of the elements of the forward contracts. Finally,

Section 5 draws the main conclusions.

2. Model and Methodology

Electricity generators tend to hedge their sales of energy, which they may supply through self-generation or spot purchases. Ref. [

7] proposes the hedging strategy of electricity generator

i as an optimization problem with a mean–variance utility function over its net energy sales

. This problem is represented by Equation (1) and depends on the level of risk aversion

. The mean–variance utility function exhibits limitations when the forward price does not match the expected spot price, i.e., when there is an FRP. Ref. [

17] states that when there is a risk premium in electricity markets, the optimization of the mean–variance utility function is subject to the decision makers’ level of risk aversion, as illustrated in Equation (1), where

represents the expected utility of generator

i on the decision variable

.

We consider an electricity generator i that faces uncertainty over its net sales at time ; therefore, it decides to sell long-term electricity contracts beforehand starting from time (). If such a generator participated in an electricity market whose spot price and energy generation derived from a multivariate SNP distribution, our research question is: how many contracts should it trade to hedge its risk?

2.1. Spot Price and Energy Generation

We propose modeling these two variables through multivariate SNP functions. Below, we describe the portfolio multivariate SNP distribution, which generalizes the multivariate normal in terms of Gram–Charlier (Type A) series for every portfolio variable. Let us assume that

is a vector that contains

J variables distributed with zero mean and multivariate SNP distribution. Its joint probability density function (pdf)

is written, as proposed by [

24], as follows:

where

is a multivariate normal pdf with zero mean, covariance matrix

—with general element

and marginal pdfs represented by

—i.e.,

and

,

; and

is a linear combination of the first

terms of the Gram–Charlier series Hermite polynomial, as shown in Equation (3). The terms of these expansions,

is the so-called Hermite polynomials (HP) or order

m—see Equation (5), which is weighted by parameter

capturing the raw moment of order

m for the marginal variable

j.

Hence, the marginal pdf of

is:

Note that the univariate Gram–Charlier density in Equation (4) is an expansion of a normal pdf in terms of orthogonal polynomials—as described in Equation (7) below—and truncated at an arbitrary order

that depends on the degree of accuracy and flexibility required for the SNP approximation. It can be easily proven that the even (odd) moment of order

r of variable

depends linearly on

for all

j ≤

r and

j even (odd). Particularly, mean and variance are

and

, respectively, and the covariance between the variables

and

is defined by the corresponding entry in matrix

, i.e.,

. Furthermore, if

(

), then the

j-th marginal pdf features positive (negative) skewness, when

the marginal pdf of

exhibits leptokurtosis, and the higher-order even parameters account for extreme values. A further discussion on the interpretation of such parameters can be found in the studies by [

18,

21,

23] for the case of electricity markets.

The main advantage of the SNP modeling lies in its ability to capture the full density (skewness, kurtosis, higher order moments, and their dependencies) with a flexible formulation. As a matter of fact, the asymptotic Gram–Charlier expansion captures the true underlying distribution. However, the truncated expansions might present positivity problems that are traditionally tackled through positive transformations—see, e.g., refs. [

20,

27], analyzing positivity surfaces [

28] or implementing controlled optimization [

21]. In this paper we opt for the latter method since constrained/transformed SNP densities may also present convergence problems due to complex nonlinearities among the moment structure—see, e.g., ref. [

29].

The HP of order

m,

is defined in terms of the

m-th derivative of the standard normal pdf,

, and thus, can be calculated by solving Equation (5).

Hence, the first five HPs used to represent the standardized random variable

are:

It is noteworthy that the HPs form an orthonormal basis, since:

Next, we define the joint SNP pdf for spot price and energy generation. Let

be the natural logarithm of the spot price

and

, that of the energy generation by generator

i. We assume that

and

are governed by a bivariate SNP process on the stochastic standardized (i.e., zero mean and unit variance) variables

and

with correlation coefficient

, whose joint pdf is given by:

being a standardized bivariate normal pdf with correlation and and N (0, 1) pdf.

Thus, marginal distributions can be written as follows (see proof in

Appendix A):

where

and

2.2. Forward Price

If an agent purchased a forward contract at time

to receive an amount of electricity at maturity time

at price

it would receive such agreed amount at maturity at the agreed price

. Since such electricity received at time

is valued at the spot price

, its net income will be given by the difference between the spot price and the agreed price stated in the contract, as in Equation (10).

The seller will be paid at the agreed price in exchange for delivering the agreed amount of electricity, which will be valued at the spot price at maturity, as the short forward payout in Equation (11). This relation is used to measure the sensitivity of the risk indicators.

Some authors [

30] argued that traditional cost-based valuation models are not applicable in electricity markets. The assessment of assumed risk levels is reflected in the traded contracts’ price, as demonstrated for those who studied the FRP in electricity markets. Thus, the price of an electricity forward contract agreed at time

and a maturity T will be different from the expected spot price. This difference is known as the forward risk premium (FRP), represented by Equation (12).

The FRP sign indicates who is the agent hedging the risk and paying for it: when the sign of the FRP is positive, the seller is the one paying for the hedging, while when it is negative, the buyer is the one paying for it. According to [

13], a positive FRP value denotes a normal backwardation condition. This FRP may describe the expected spot price or the forward price based on the following relationships:

Due to the nature of forward contracts, convergence must occur at maturity, i.e., a forward price agreed on that matures at

T should be equal to the spot price, as stated by [

31]. Therefore as maturity approaches, the FRP becomes null in electricity markets [

17], as follows:

2.3. Pay-Off Function

Assuming that an electricity generator that has produced an amount of electricity

at time

sells all this electricity at the market spot price

, then its net sales

are given by the product of the spot price and its energy generation:

At time

, the spot price and the energy generation values are unknown, which means that the generator is taking a risk due to variations in price and quantity. To hedge the assumed risk, the generator decides to implement certain strategy

at time

, whose pay-off function is

; its net energy sales will be given by:

where

is the vector of the parameters necessary to specify strategy

implemented by electricity generator

at the initial time

. According to [

9], when the hedging strategy corresponds to the sale of fixed-price (forward) contracts, its pay-off function

will be equal to

This function depends on the amount of electricity sold under the forward contract,

, and the difference between the fixed price of the contract,

, and the spot price,

. Hence, the sales of a generator that hedges its risk through forward sales is given by:

If we also assume that, at time

, the conditional expected value of the energy generation is denoted by

, the previous expression can be written relatively to the expected generation unit, as follows:

where

will be the energy generation with respect to the expected value and, analogously,

and

. The previous equation can also be rewritten by grouping the random variables in the first term

and the deterministic ones in the second term

, as shown below:

For this purpose, the production cost is ignored. However, this mainly applies to hydropower renewables. Thermal plants have fuel costs typically correlating with power prices.

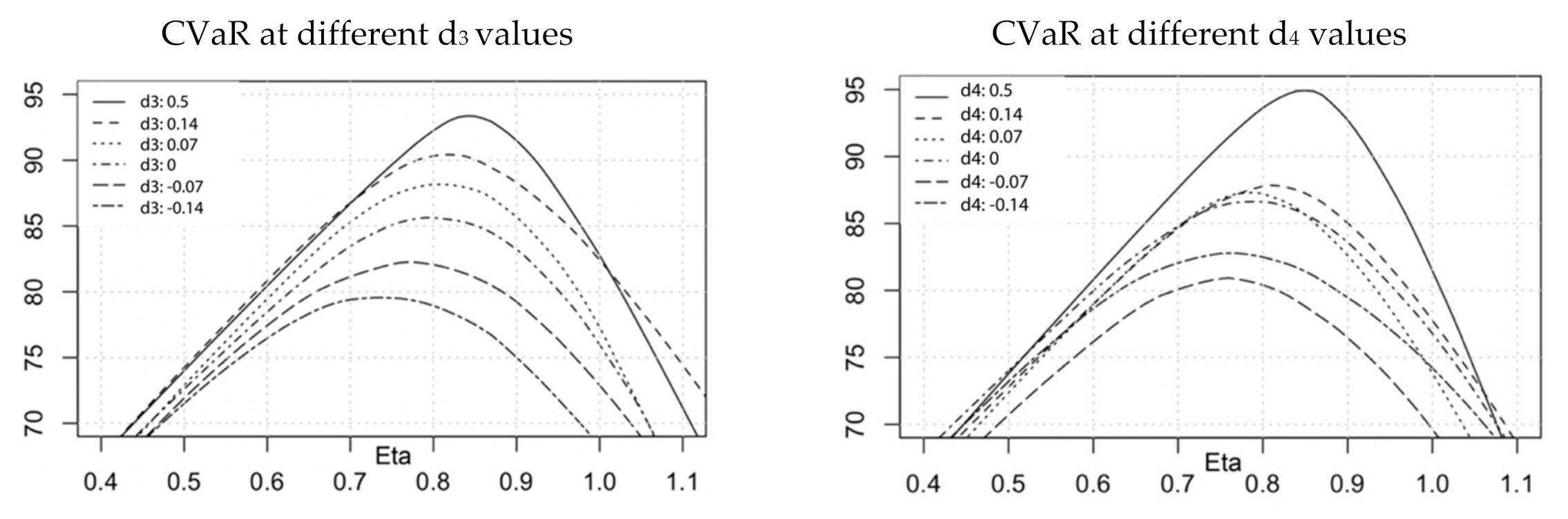

2.4. Risk Indicators

The standard deviation (Std) measures the dispersion of the variable

from its mean.

The VaR captures the lowest income that would be expected at the desired confidence level (e.g.,

), which can be written as:

where

is the probability density function; the CVaR also estimates the lowest profit expected but given that the VaR level has been exceeded. CVaR averages all the net income levels below the VaR; it is computed as in Equation (22).

The optimal hedge portfolio for risk should include searching for conditions that maximize the VaR and the CVaR or minimize the standard deviation for the portfolio sales.

2.5. Methodology

We propose a stepwise procedure in three stages: (i) estimation of the deterministic component parameters, (ii) estimation of the random (bivariate) component parameters, and (iii) sensitivity analysis and simulation of electricity generator’s portfolios under Monte Carlo simulation.

- (i)

Parameter estimation of spot price and energy generation

Regarding the spot price

, we considered an exponential model represented by a stochastic process with a deterministic long-term mean and mean reversion, as described by Equation (23). This structure was developed based on the models proposed by [

32,

33], which have been applied to the case of Colombia by [

17,

34].

Similarly, as for the energy generation of agent

i, we have:

where

and

are deterministic trend specifications. There,

and

are stochastic autoregressive of order 1 AR(1) components, which are assumed to be stationary, i.e.,

and

and

and

being white noises with zero mean, variances

and

, respectively, and correlation coefficient

. The set of equations used to estimate the uncertain components of the spot price can also be written in matrix form, with

, as follows:

where

- (ii)

Bivariate distribution estimation for price and energy generation

The vector

is assumed to follow the bivariate SNP distribution defined by the Equation (8). Ref. [

35] proved that the model can be consistently estimated in two steps: First, (quasi) maximum likelihood (QML) estimation of every mean–variance process independently—Equations (23) and (24)—and under normality; Secondly, joint maximum likelihood (ML) of the rest of the parameters of the bivariate pdf,

for

, which we denote by the vector

, as well as the correlation between both variables, denoted by

. This second step considers the standardized series

, where

and, thus, the loglikelihood for generator

i, given a sample of size T, corresponds to Equation (26),

where

is the SNP distribution in Equation (8), conditioned on the parameter set

.

- (iii)

Monte Carlo simulation of bivariate SNP distribution

Once the model was estimated, we analyzed the sensitivity of the results to the parametric uncertainty and its effects on the electricity market hedging under the SNP distributional assumption for the random component. We performed Monte Carlo simulations, which required the extraction of (correlated) random numbers from the bivariate SNP distribution of spot price and energy generation (

). According to [

36], no truly random number can be generated by a computer code as long as it can only perform sequences of deterministic operations. From uniform pseudo-random samples, numbers from any other kind of density distributions applying a specific transformation can be obtained. This transformation can be performed by taking the inverse cumulative distribution function to a sample of uniformed pseudo-random numbers.

A straightforward method to simulate the SNP distribution series can be obtained by implementing the methodology proposed by [

37], valid for any joint distribution. Intuitively, this methodology involves filtering out the joint distribution through its marginal density functions to obtain uniformly distributed functions with a dependence structure.

Based on Meucci’s methodology, each component of vector

can be standardized, using the cumulative functions

and

, towards a space where each variable contains a uniform probability distribution, as follows:

Therefore, to generate a random number from a joint SNP distribution whose cumulative marginal functions are

and

, it will suffice, for the purposes of this study, to evaluate the quantile function Q(.) of the random numbers that maintain the distribution of

and its correlations.

Figure 1 illustrates the set of proposed transformations. In this work, we need to simulate not only one sample but two correlated samples to recreate the bivariate SNP.

To create a sample for the SNP correlated random variables and , we executed a two steps algorithm: (i) generate two pseudo-random uniform-distributed correlated numbers: and , considering a cumulative distribution , and then (ii) filter each number with its inverse-cumulative distribution, using for and for . These distributions correspond to the fitted marginals for the joint SNP distribution. Once the parameters of the random components were calibrated, we implemented this simulation methodology to perform the sensitivity analyses for the portfolio hedging problem.

3. Data Description

We used the information for the electricity spot price from the Colombian electricity market and the main electricity generators from January 2000 to December 2018. The spot price series corresponds to the average price of the monthly energy locally traded in the Colombian energy market, measured in COP (Colombian peso) per kWh (kilowatt-hour) (COP/kWh). Meanwhile, the generation corresponds to the total energy produced monthly for a generator, and it is measured in GWh (106 kWh).

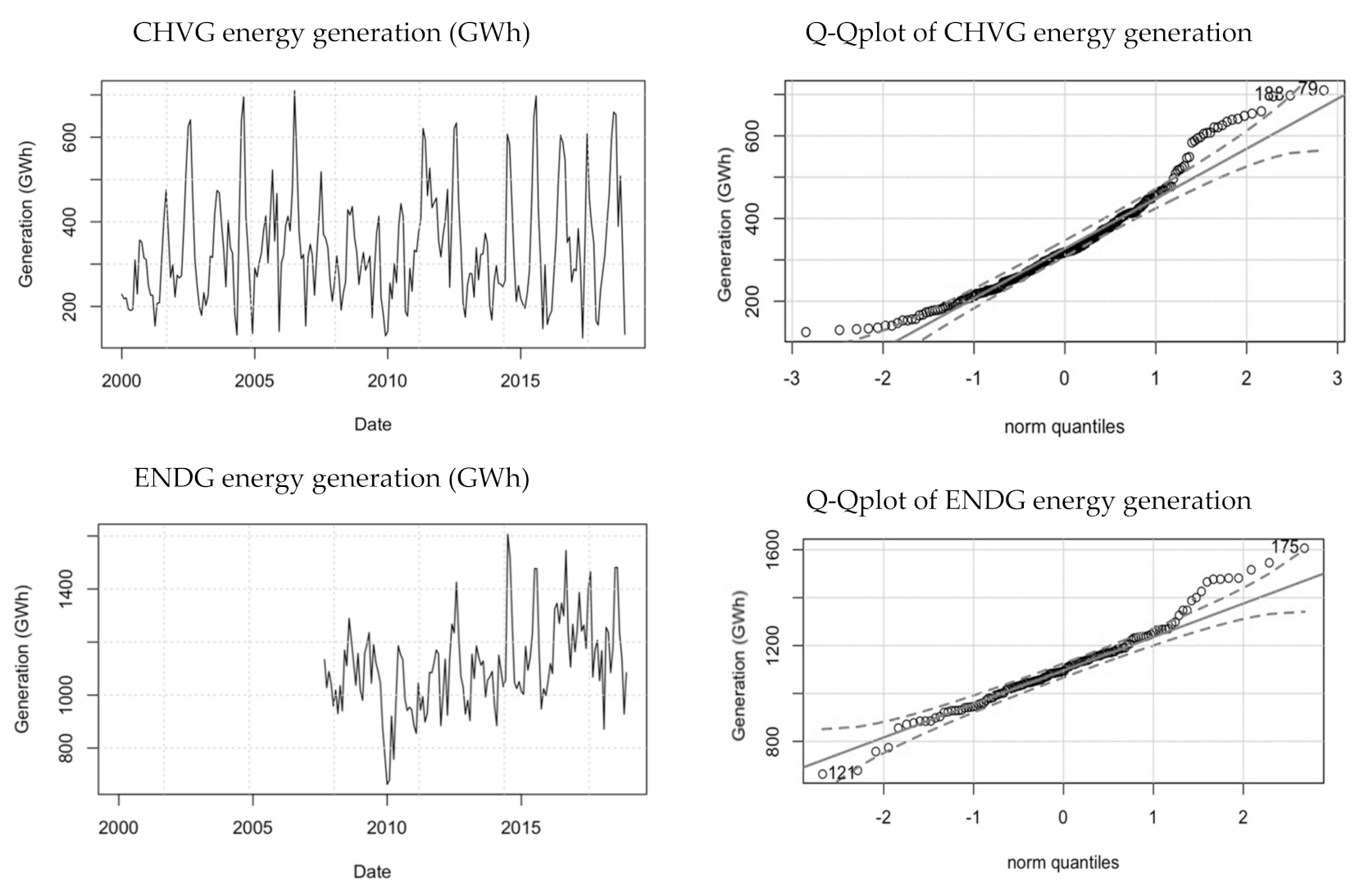

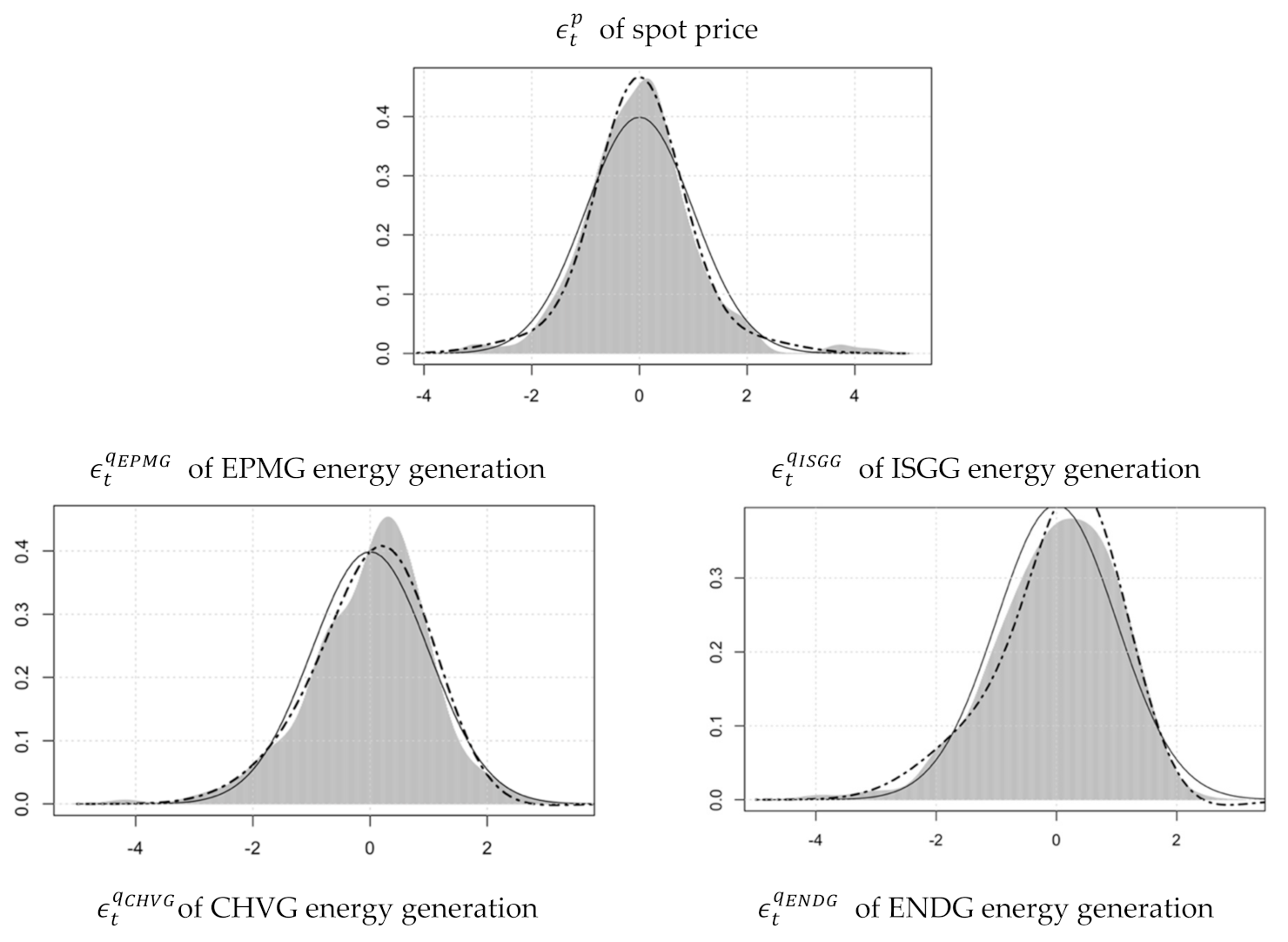

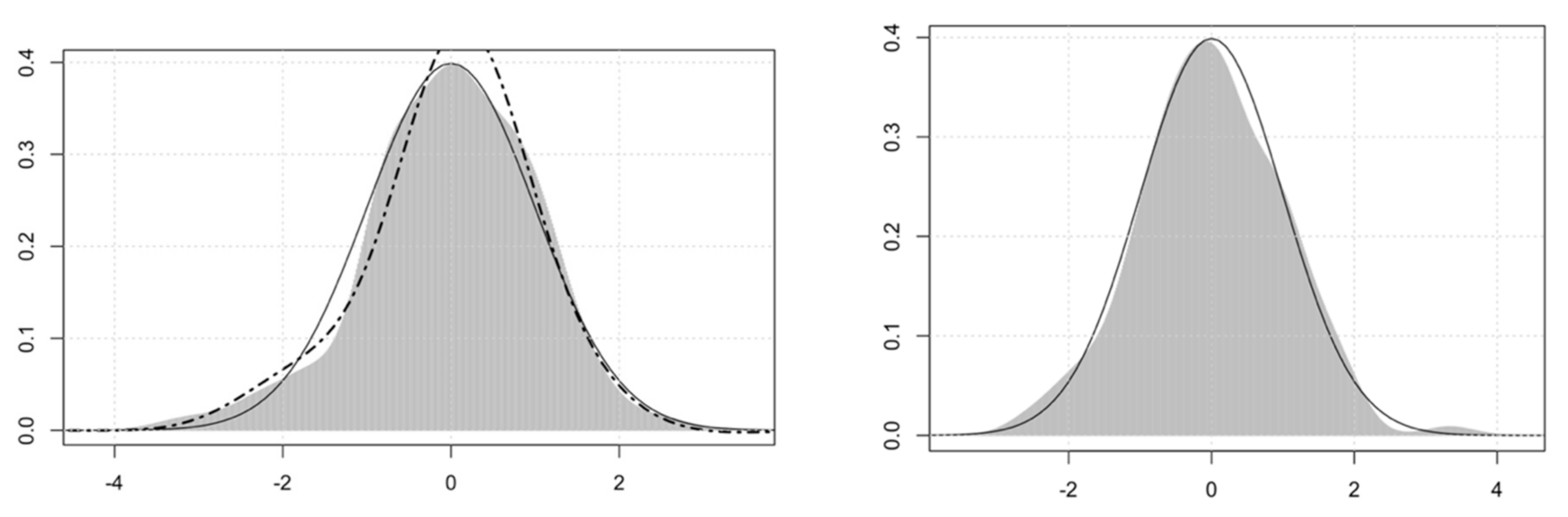

Table 1 shows the descriptive statistics of the series employed in this study. The generators considered were EPM (EPMG), ISAGEN (ISGG), AES Chivor (CHVG), and Enel (ENDG)—which predominantly managed hydraulic resources. The spot price series exhibited the highest value of skewness, while all the energy generation series, except EPMG, showed a positive skewness. Regarding kurtosis, spot price again exhibited the highest value; the kurtosis of CHVG and ENDG was above that of a normal distribution, while that of EPMG and ISGG was below 3. For the sake of comparisons, the series in logarithms and relative to the mean are also displayed.

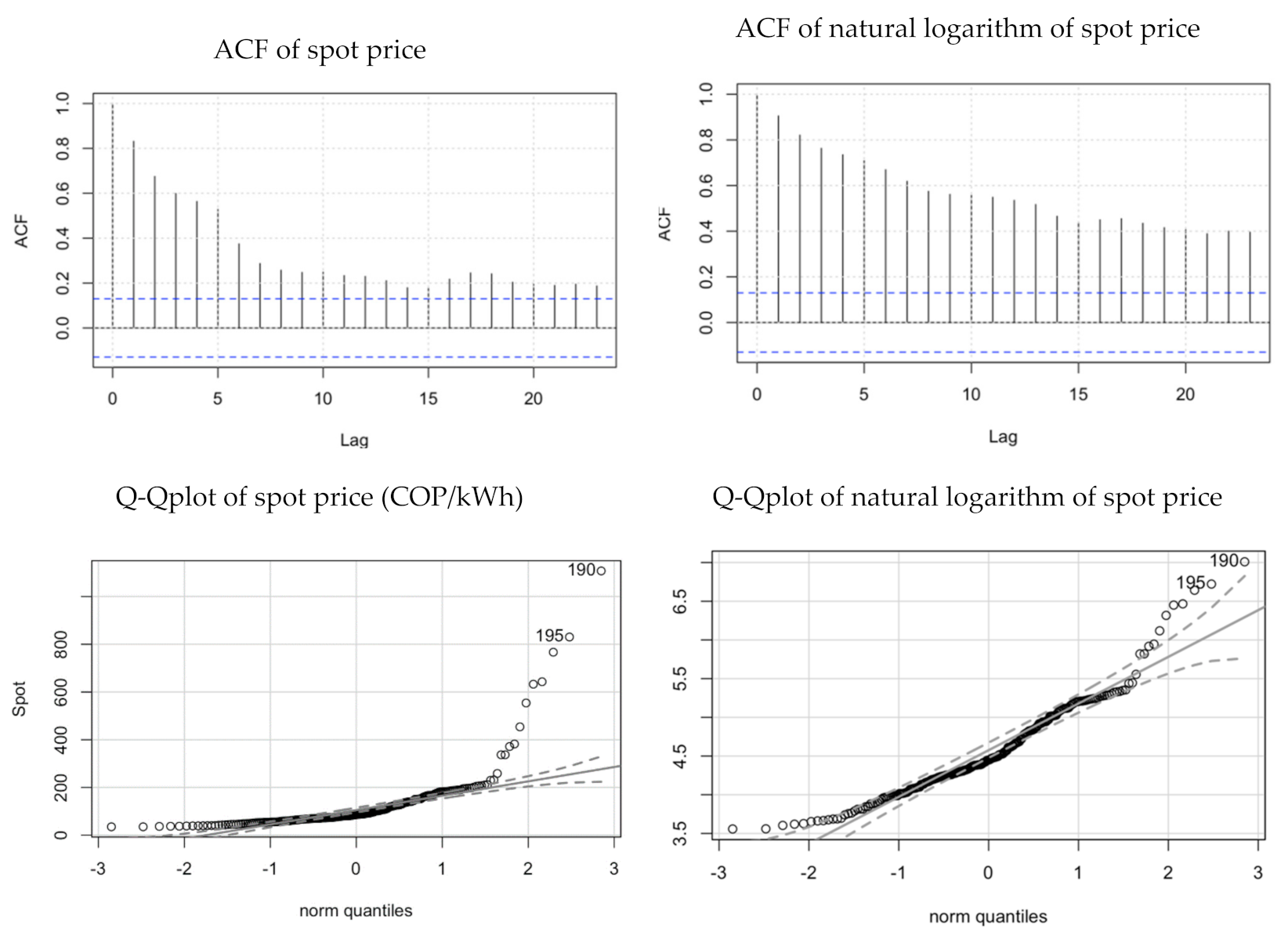

Figure 2 illustrates the spot price series, as well as its autocorrelogram, Q-Qplot, and natural logarithm. There, spot price exhibits a trend and jumps; its highest jump occurs after 2015 due to the occurrence of the El Niño, together with the shortage of natural gas for power generation. The autocorrelograms of spot price and its natural logarithm show the memory condition of this time series. According to the Q-Qplots, which assess the percentiles of the samples, the data do not fit adequately a normal distribution.

ISGG, followed by EPMG and spot price, exhibits the highest level of the first-order autocorrelation, which means that short-term distortions remain for a longer time in these series than in the other ones. Another aspect to highlight is that the skewness changed for the natural logarithm of the series. Regarding dispersion of the series, estimating the percentiles relative to the mean allowed us to observe, for instance, that spot price is between 0.33 times and 2.01 times its mean at a 90% confidence level. After spot price, CHVG is the series with a more extended 90% confidence interval, followed by ISGG, EMPG, and ENDG.

Table 2 shows the autocorrelation levels of the time series.

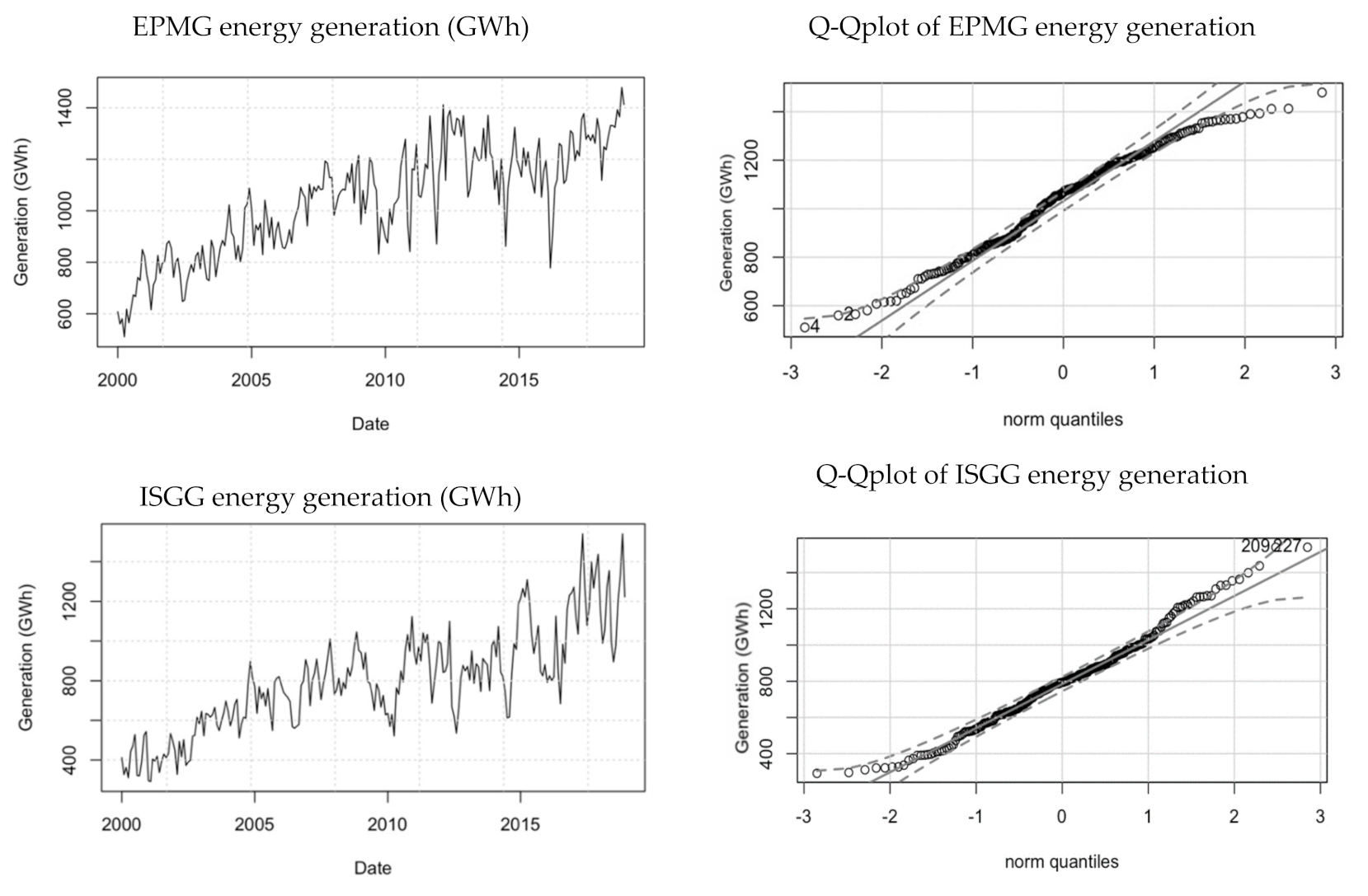

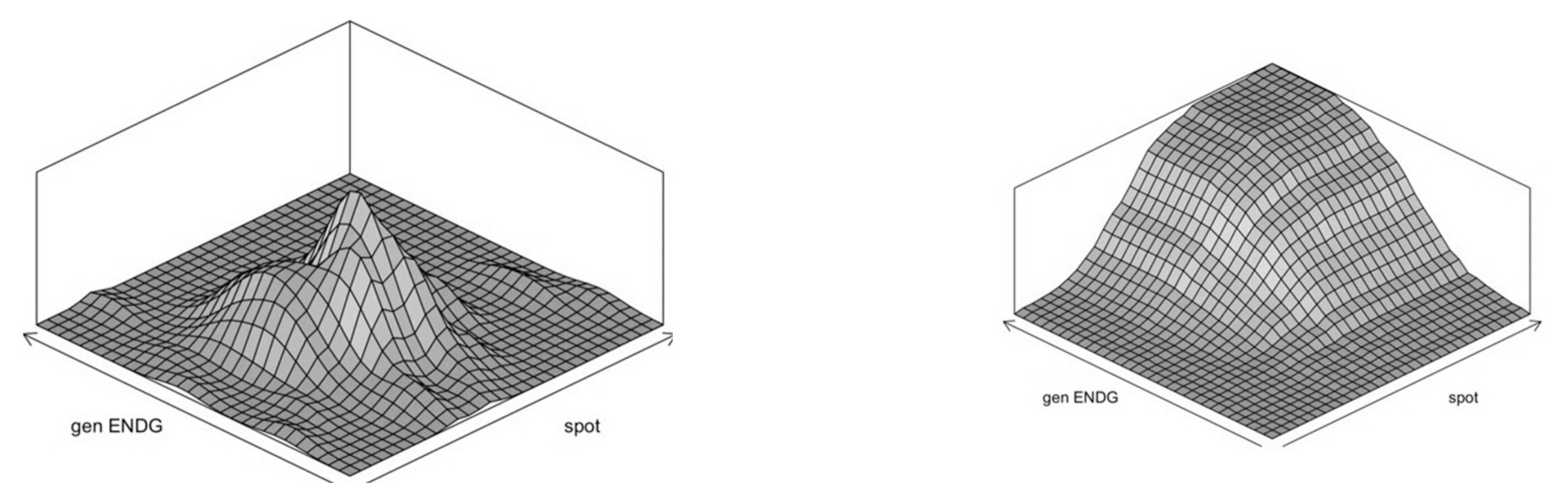

EPMG and ISGG in

Figure 3 show a trend explained by the expansion processes of these electricity generators, which have constructed new power plants in recent years. Furthermore, Q-Qplots show how data do not support the normal assumption, particularly at the extremes of the distribution, which calls for the SNP modeling of the series.

5. Conclusions

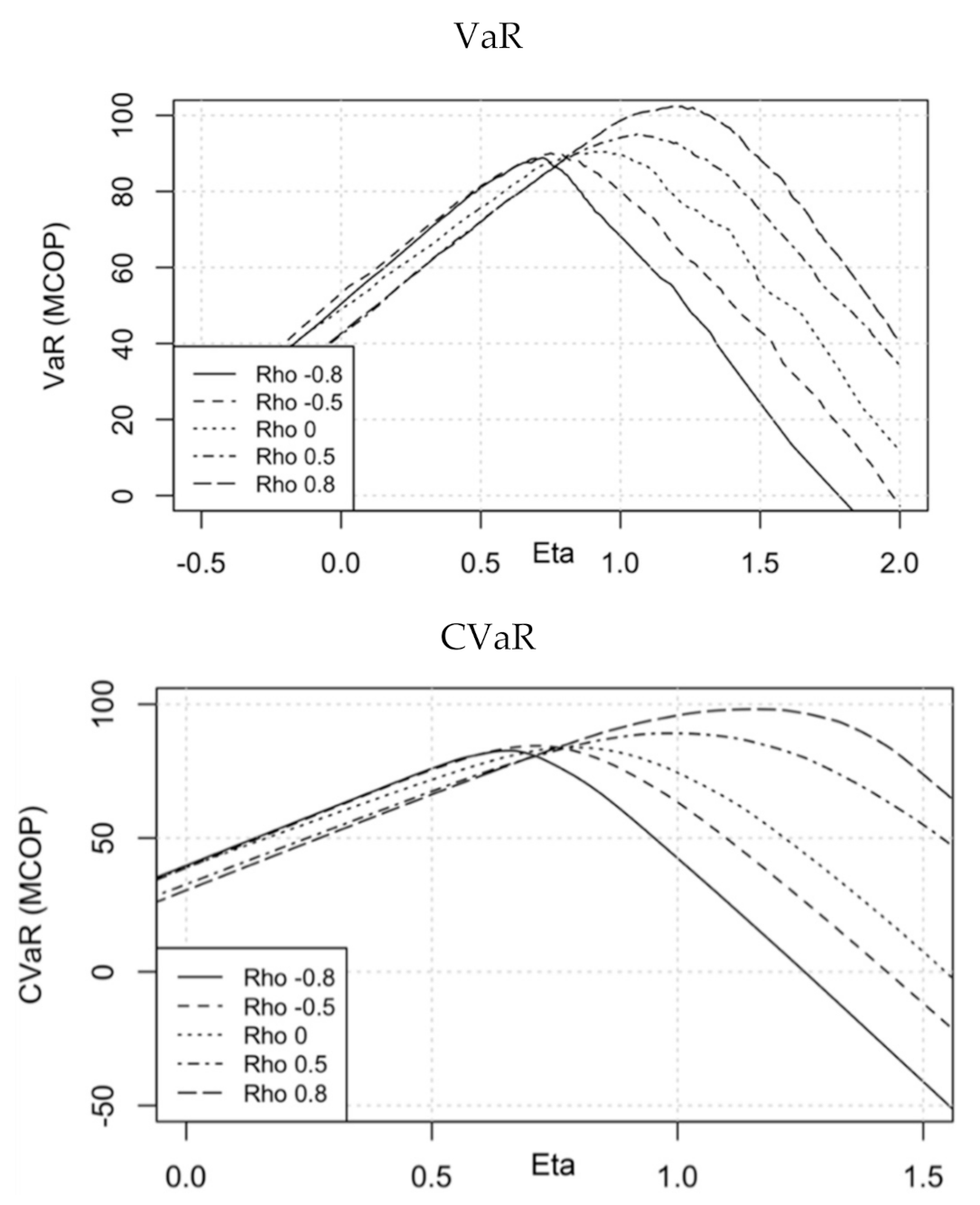

This paper proposes a static hedging strategy for electricity generators that participate in a competitive market where hedging is carried out through forward contracts that include a risk premium in their valuation. We considered the spot price and energy generation variables to follow a bivariate SNP distribution defined in terms of the Gram–Charlier (Type A) expansion. This distribution allowed us to not only model the mean, the variance, and their correlation but also the skewness, the kurtosis, and higher-order moments. Moreover, we used Monte Carlo simulation to analyze the effect of three risk indicators (standard deviation, VaR, and CVaR) on the net profit from energy sales, using information from the Colombian electricity market as the case study. We found that positive correlation between the spot price and energy production tends to increase the hedge ratio; meanwhile, negative correlation tends to reduce it.

This work’s main contribution is the modeling and analysis of the risk faced by electricity generators through flexible SNP multivariate distributions, as well as the structuring of a hedging portfolio that does not impose the assumption of normality on price and energy generation, which is a novelty in this academic field, where, as far as we know, multivariate semi-nonparametric technics have been used before. The performance of the model for implementing forward contracts hedging strategies is assessed though the Monte Carlo simulation of bivariate SNP pdfs and by studying the sensibility of risk measures to the different parameters affecting forward electricity markets.

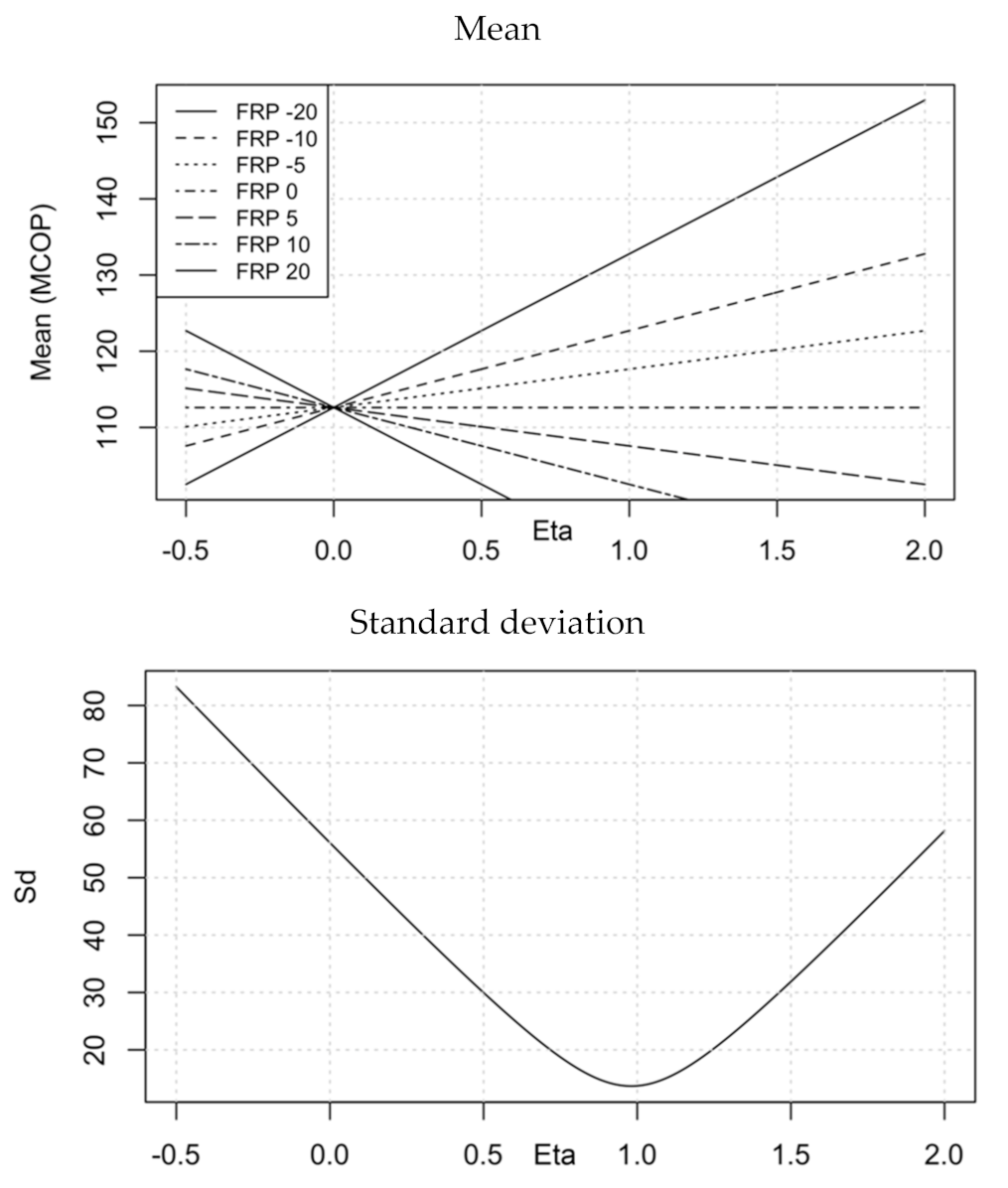

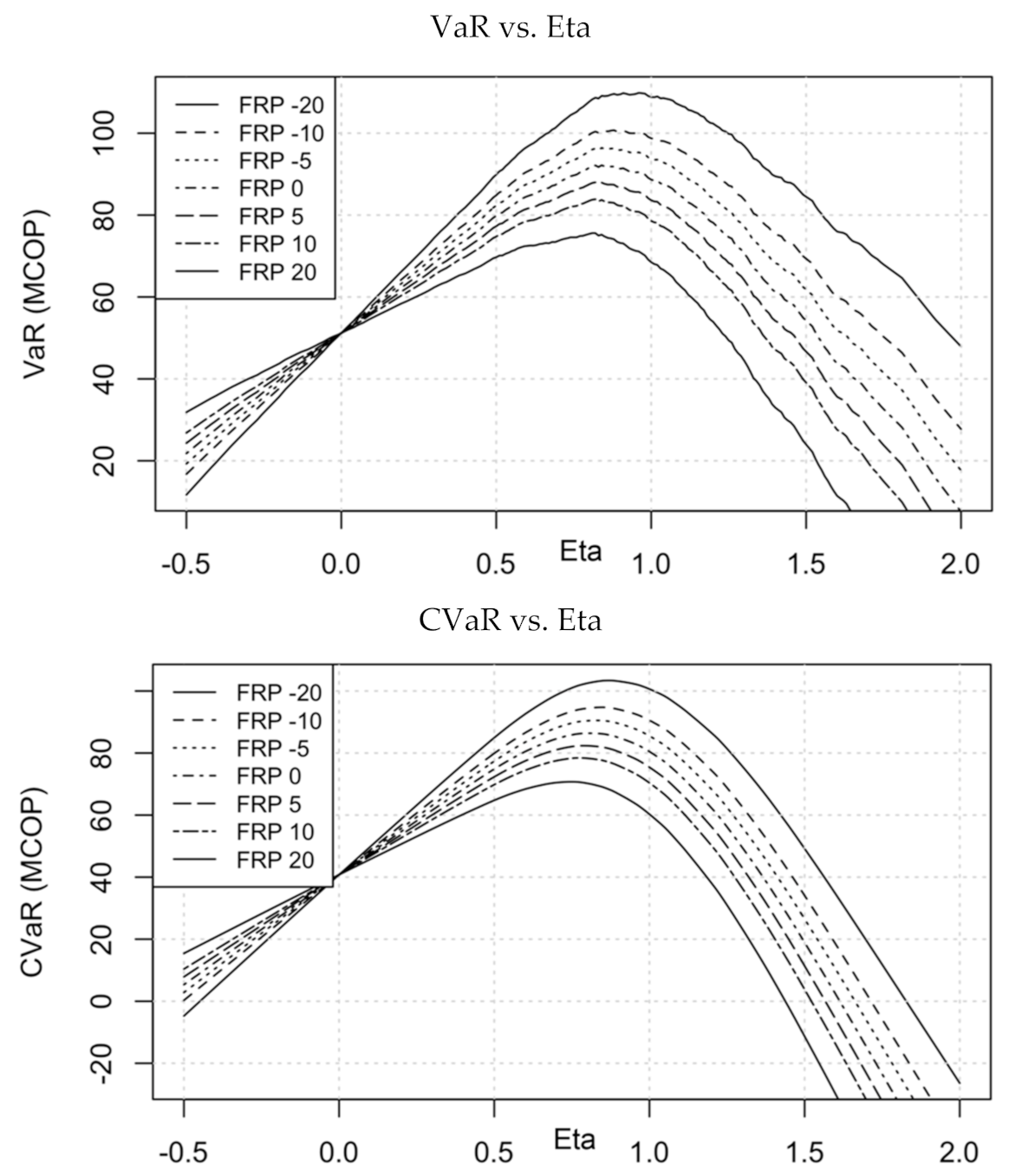

In general, a negative FRP increases an electricity generator’s net profit from its energy sales in the contract market, thus, favoring electricity forward sales. Moreover, the FRP affects the behavior of the mean, VaR, and CVaR indicators regarding the amount of electricity to be sold under forward contracts. This situation does not occur for the standard deviation, whose behavior, instead, is affected by the contracting level, regardless of the FRP value in the market.

The results show that the optimal quantity of energy to be sold through forward contracts is dependent not only on the conditions of spot price and quantity uncertainty but also on the way market agents weigh the assumed risk levels. Therefore, to reduce the risk levels faced by generators, such optimal quantity will depend on the conditions of price and energy generation uncertainty explained by variance, skewness, kurtosis, and higher-order moments. Furthermore, the number of forward sales is determined by the correlation between price and energy generation and the FRP, or an increment on correlation or FRP, tends to reduce the hedge ratio.

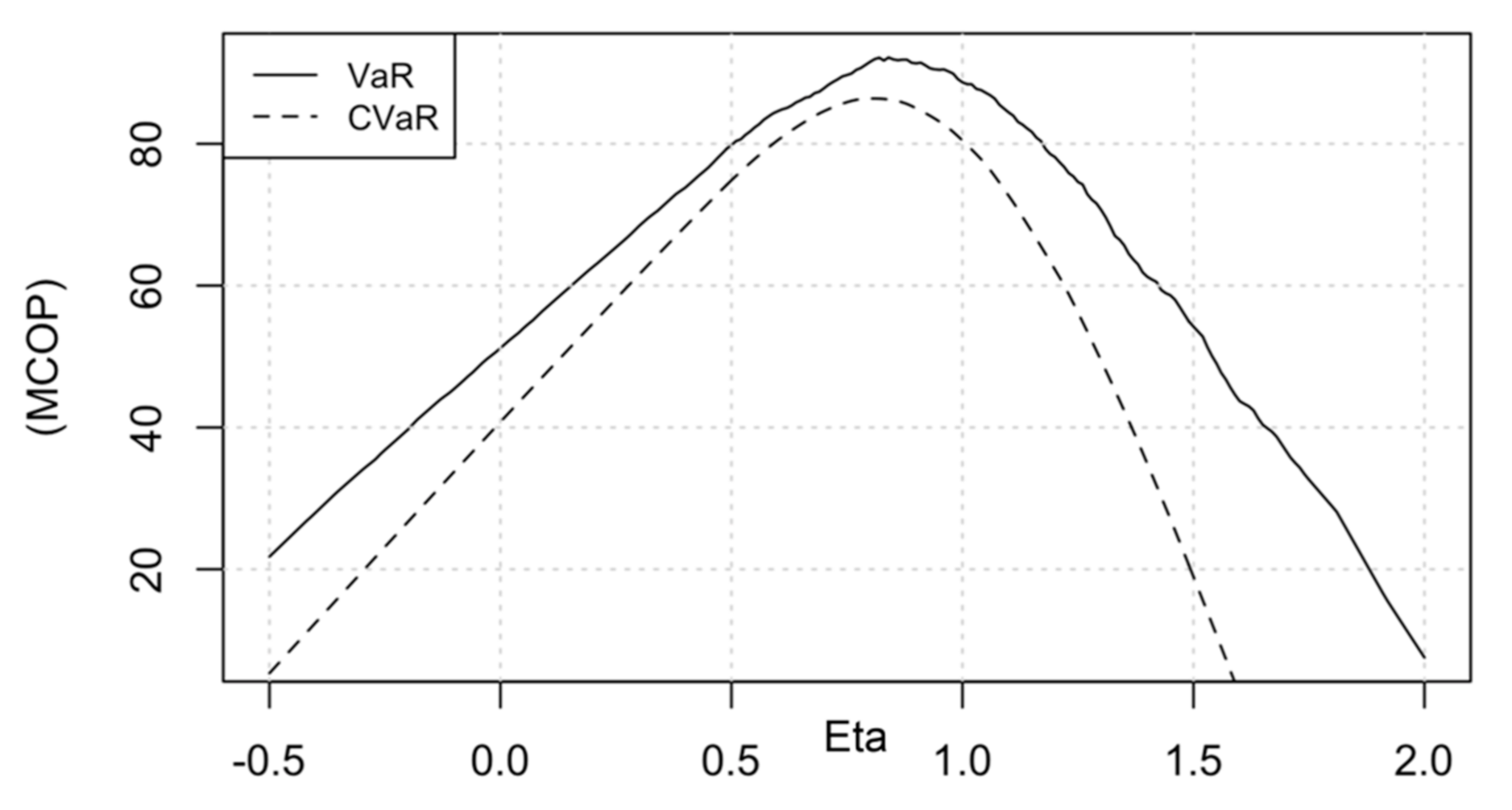

The decision-making criteria also modify the optimal hedge ratio. The VaR-maximization criterion implies a larger hedge ratio than the CVaR-maximization criterion; this criteria selection could have more impact on the optimal decision than the FRP modifications. It suggests that electricity market practitioners must pay significant attention to market conditions and the adequate risk measures that accomplish each business strategy. It is necessary to find coherence among strategy, risk aversion, and risk retention capacity.

All in all, we recommend experts in electricity markets to structure company-specific portfolios based on the market conditions on which the analysis is performed. They should also consider flexible modeling that captures a more significant number of moments than those allowed by a normal distribution for the variables involved and the correlation between the spot price and energy generation. The multivariate SNP distribution can be an appropriate tool for this purpose. As a final remark, although this work is done for a hydropower-dominated market, the convenience of this methodology for other electricity markets should be studied for further works.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}