1. Introduction

One of the main issues for any industry is to fulfill its energy needs in the smartest way possible. However, the management of an energy portfolio should simultaneously: reduce the cost, manage the risk associated and satisfy the demand, increasing the management complexity. These aspects are often a concern in the literature given the many opportunities, the different methods and tools that can be used.

In addition, the energy sector is characterized by many risks, opportunities, given the technology and renewable energy developments, which allow the energy portfolio manager to take advantage of. Hence, one of today’s challenge is to use the energy resources available efficiently and towards to improvement of performance indicators as: cost, risk and renewable energy.

In the electricity sector we have three key players: the private investors, the managers commercializing energy and the planners. They all interact in the markets but face different problems and uncertainties, changing its behavior based on its preferences over tools or mechanisms of the markets [

1]. The investors invest in technology mixes that favor them and maximize their profit, while planners seek social welfare maximization. The managers commercialize energy and their biggest concern is to maximize return and minimize risk. The latter includes both the buyers and sellers of energy [

2]. Although the managers’ side is nowadays key in electricity markets, their risk management problems are less developed than the planners’ [

1]. These players resort to electricity markets to contract their energy needs, with few available tools that can use and take advantage of, to develop a long-term and short-term plan.

Electricity markets worldwide normally offer two types of market structure to trade energy: spot (or day-ahead or pool) market and forward market. The spot market is the energy traded in the real time and day-ahead market and the most popular structure is a centralized pool-base auction where the buyers and sellers submit bids [

3]. The corresponding problem, with a different approach, was considered for the electricity balance market with the use of a historical data set and the best-known solutions have been improved [

4]. However, drawback spot market is its price volatility, being the highest when compared to any other commodities’ spot markets [

5]. Although, the forward markets is seen as the way, to overcome the lumpy prices in the spot market, where with forward contracts, consumers and suppliers commit on the trading of a specific amount of electricity, at a specific future time against a fixed price [

6]. There are several European electricity markets where the players can interact. As example, there is the Iberian electricity market, which is operated by OMIE, which is the nominated electricity market operator, responsible for managing the Iberian Peninsula’s day-ahead and intraday electricity markets [

7].

These electricity markets are nowadays flooded by numerous sources of uncertainty that arise since the sector itself and historically, are particularly unpredictable. Hence, to plan over it, is necessary to predict which future conditions the market may face, such as: how will the fossil fuel prices evolve, what will be the demand profile, will the electricity generation still so hardly depend on fossil fuels. The literature over the last two decades has primarily focused on the uncertainties that come from such factors as fuel prices, demand growth and CO2 prices. However, other factors, such as renewable resources availability, technology development, social opposition and emissions limits, also play an important role [

2].

In some cases, a linear programming formulation can be proposed to characterize, not only, the distribution network characteristics, but also, consider the market compensation processes for flexible charging and distributed energy resources, leading to reserve and reactive power compensation [

8].

Given all the opportunities and threads present in the energy sector, it is important for any consumer to best take advantage in the procurement of its energy needs. To do so, a proper portfolio optimization would be essential. However, regarding electricity markets, literature has paid little attention to the buyer’s perspective and so, the goal of this article is to make a contribution in this direction. To do so, a portfolio optimization for a large consumer is conducted, with the aim of simultaneously reducing the expected cost and minimizing the risk associated. A mixed integer linear formulation is proposed to support the decision-maker, while the trade-off between several optimal alternatives are provided, leading to energy portfolio characterization. The problem addressed is an energy portfolio optimization for a large consumer, using a multi-objective approach to minimize the total expected cost and risk associated.

The study has the following structure: in

Section 1, an introduction is made, where the background and general motivation are set, the characterization of the electricity markets is provided, as well as the objectives and article structure. In

Section 2 explores the literature review focus in methods and trend of energy transition from a circular economy perspective. In

Section 3 is defined the methodology to be used: steps of the analysis and problem characterization. The mathematical formulation is presented in

Section 4, followed by the explanation of how the data were collected and how was it was fitted, in

Section 5. In

Section 6 is shown the results and its analysis from three case studies. Finally, general conclusions and further work are considered on

Section 7.

3. Methodology and Problem Statement

3.1. Methodology

The methodology undertaken in this work follows several steps and explores several methodologies. The first step identifies, in the literature review, the gap that remains to be fulfilled, considering the energy portfolio optimization of large consumer, from buyers’ perspective. Followed by the stakeholder’s identification and its roll characterization, mainly electricity suppliers’ options and large consumer needs. The Iberian Market is explored, as large consumer stakeholder. Three electricity suppliers’ options are considered: day-ahead market, forward contract and self-generation.

The forward contract will be set in a specific time and its output will be divided in 4 blocks of energy, each with a specific price. The self-generation energy implies a long-term investment, providing a constant energy throughout every hour of the planning horizon. A long-term investment aversion from the decision-maker must be considered. Its energy is divided in 4 blocks, each with a different price as well. The day-ahead market trading stands as the factor that brings uncertainty into the decision-making.

Data collecting and screening for further analysis and data characterization is performed. 48 weeks is considered as a final sample. However, this step is of high importance to grab the sector characteristics and feed the model with accurate information. Based on that, a deeper analysis over seasonality patterns identification is undertaken, such as: yearly, weekly and daily. Data categorization is undertaken according to their average spot price, in three categories: valley, shoulder and peak hours. Some parameters are estimated, and some information is omitted due confidentiality reasons.

The aim of this work is to explore the energy portfolio optimization considering simultaneously the cost and the risk, which trigger to a multi-objective approach. The trade-off between the two objectives is explored through the weighed-sum approach and its results characterized using the Pareto Font representation. An economic indicator, as costs is used as one of the objective functions, while a risk measure, as CVaR is explored to mitigate the risk.

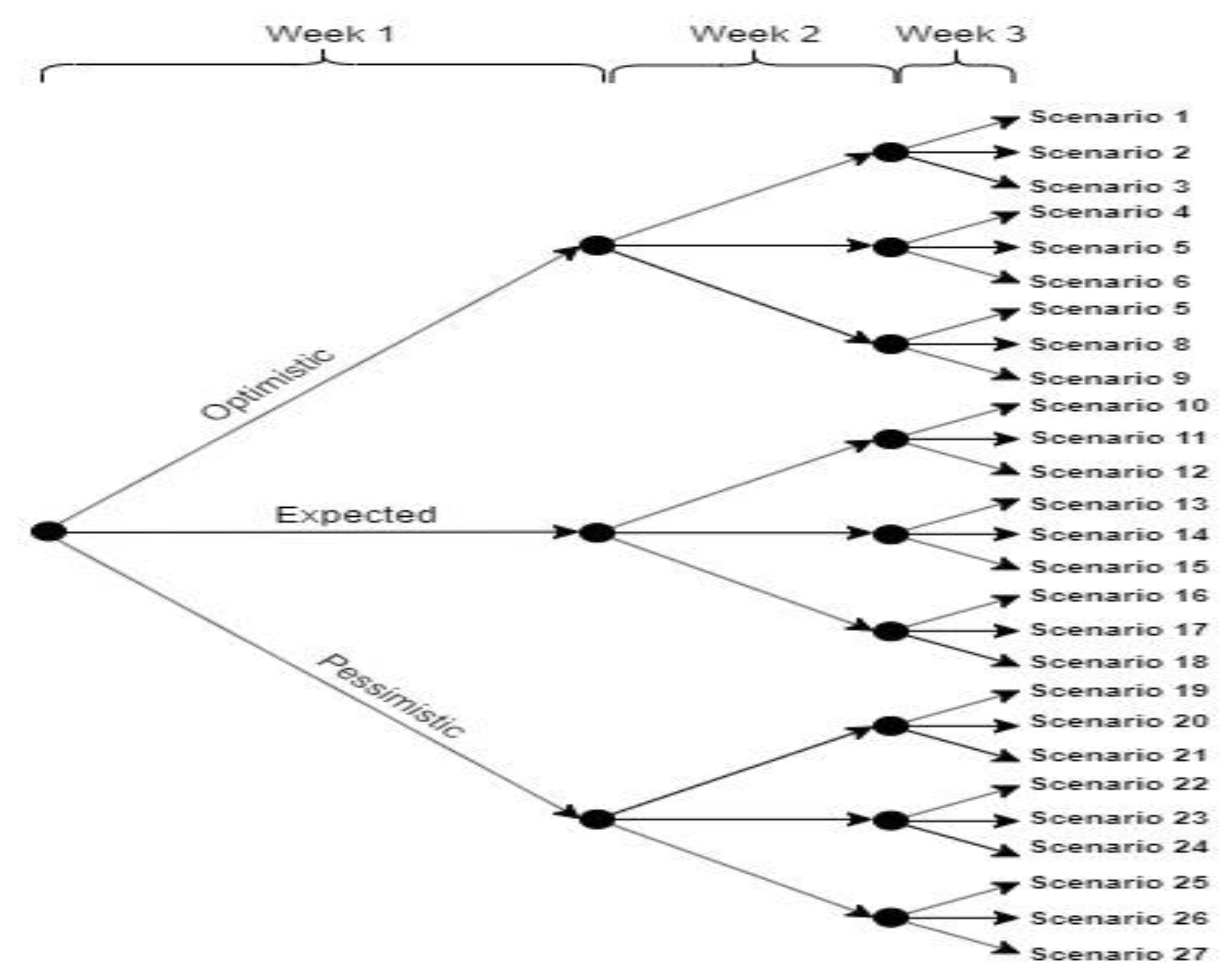

Another relevant aspect is the electricity market variability/uncertainty. Its behavior is characterized through a Scenario Tree approach [

49], as defined in

Figure 1. The scenario tree has 3 branches leaving each node and 3 nodes, resulting in 3

3 = 27 scenarios. Each branch denotes one week, with a total planning horizon of 3 weeks. On each node decisions regarding weekly forward contracts and spot market trading are done and exclusively on the first node, the decisions regarding 3-week Contract and self-generation production are taken.

3.2. Problem Statement

A portfolio optimization for a large consumer is conducted, from a buyer´s perspective, mitigating expected cost and risk. The mixed integer linear programming formulation is extended from [

40,

48] and Iberian electricity market is used as large consumer.

Three different electricity supply options are considered: forward contracts, self-generation facilities and pool market trading. In the forward contracts a specific quantity of energy is purchase in advance, for a specific price, to be delivered in a specific time. The pool market trades in the day-ahead market. While the self-generation the decision-maker must embrace an investment to pursue this option.

Hence, given sources price, scenarios and its probability, demand to be satisfied, the aversion to long term investment from the decision-maker and the confidence level for the CVaR calculation.

The model determines: procurement of electricity on each of the electricity options, the optimized scheduled and the non-dominate solution, allowing the trade-off between the expected cost and the CVaR, for several risk postures.

It is subject to: expected cost and CVaR minimization.

4. Mathematical Formulation

This work is extended from [

48], with the aim of support the large consumer, from a buyer perspective, in the electricity portfolio optimization. A mixed integer linear program (MILP) based on [

48] is proposed to simultaneously minimize the cost and risk.

4.1. Forward Contract

| Notation: |

| Index |

| s | = Week |

| d | = Day |

| t | = Hour |

| w | = Scenario |

| c | = Contract |

| b | = Block |

| g | = Self-generation facility |

| k | = Stage |

| Sets: |

| Ns | = {s: set of weeks in the planning horizon} |

| Nd | = {d: set of days in the planning horizon} |

| Nt | = {t: set of hours in a day} |

| Nw | = {w: set of scenarios} |

| Nc | = {c: set of contracts available} |

| Nb | = {b: set of blocks available in each forward contract} |

| Ng | = {g: set of generation facilities} |

| Nk | = {k: set of stages} |

| CDs | = {c: set of forward contracts available in week s} |

| CTt | = {c: set of forward contracts available at hour t} |

| Data Parameters: |

| H | = Number of hours in the planning horizon |

| = Maximum amount of energy available for contract c in block b (MWh) |

| = Minimum amount of energy to be consumed from contract c in block b (MWh) |

| = Price of energy unit of contract c for block b (€/MWh) |

| = Minimum energy to be generated from self-generation facility g in block b (MWh) |

| = Maximum energy to be generated from self-generation facility g in block b (MWh) |

| = Levelized cost of energy unit from self-generation facility g (€/MWh) |

| = Demand of energy for day d at t (MWh) |

| = Probability of scenario w |

| A | = Non-anticipativity matrix. |

| = Stage at which a decision for forward contract c is made |

| Parameters defined by the Decision-maker: |

| = Risk aversion factor |

| = Aversion factor to long-term generation investment |

| = Confidence level |

| Binary Variables: |

| = 1 if forward contract c is selected in scenario w, 0 otherwise |

| = 1 if self-generation investment g is selected, 0 otherwise |

| Variables: |

| = Amount of energy contracted from contract c and block b for scenario w (MWh) |

| = Amount of energy self-generated from g in block b (MWh) |

| = Amount of energy purchased from the pool for week s, day d and hour t in scenario w (MWh) |

| = Forward costs contracting (€) |

| = Total levelized cost of self-generation for the whole planning horizon (€) |

| = Purchases cost for the pool (€) |

| CVaR | = Conditional value-at-risk |

| = Value at risk |

| = Auxiliary variable for CVaR |

| OF | = Objective function |

The forward contracts use weekly intervals and deliver the same quantity of energy each hour over the contract horizon and can be set on single or multiple week’s bases. The energy available in each contract,

c, for a block,

b, must verify its capacity, Equation (1).

The quantify the amount of energy contracted in contract c, for block b, in scenario w. The binary variable is equal to 1, if contract c is assigned in scenario w, 0 otherwise. The parameters and define the maximum and minimum amounts of electricity, respectively.

Its cost is quantified in variable

in Equation (2). The parameter

defines the price for the block

b, in contract

c, which is available in week s,

and, at hour t

.

In forward contracts, the dependency between different scenarios regarding contract decisions is guaranteed through non-anticipativity constraints. Scenarios that are equal until a certain decision stage, should have the same decisions made until that stage, which is guaranteed by Equation (3). As done in [

34], using a matrix of 0 s and 1 s where A(w, k) is equal to 1 scenario w and w+1 are equal up to stage k, 0 otherwise. Hence, the matrix’s size is (N

w − 1) × (N

k − 1), which in our case is a 26 × 3 matrix. Using A we can formulate the constraint as done in (3). The

defines the stage at which a decision on contract, c is undertaken.

4.2. Self-Generation Facilities

Self-generation facilities are a source of electricity, which must satisfy the minimum and maximum self-generation capacities, as in Equation (4).

The quantifies the amount of energy self-generated in the facility g. The binary variable takes the value 1, if the self-generated facility g is installed, 0 otherwise. The defines, respectively, the maximum and the minimum energy self-generated,

The cost of the self-generation facilities is given by Equation (5), with the H as the planning horizon and,

the price per energy unit.

4.3. Day-Ahead Spot Market and Energy Balance

In the day-ahead spot market is assumed that the costumer is a price-taker and, by that, its trades don´t impact in the market-clearing price. There is no real need to constrain the trade in the spot market. However, is necessary to guarantee the consumer only interacts as a buyer and guarantee that the self-generated electricity is not sold (partial self-generation are not allowed). Must be guranted that the energy procured from the day-ahead market,

, must be positive by Equation (6).

The cost is defined by Equation (7), the parameter,

, quantify the price, per energy unit.

The energy balance constraint, Equation (8), ensures the energy available per hour, from the three different sources: self-generated, forward contracted and the spot market, must satisfy the demand

.

4.4. Conditional Value-at-Risk Definition

The mitigation of risk cost variability is performed using the conditional value-at-risk as in Equation (9). The Equation (9) denotes the expected cost of the (1-α) × 100% scenarios with greatest cost. The variables

ζ and

ηw characterize the Value-at-Risk and conditional value-at-risk, respectively, used in Equations (10) and (11). The variable π

w, defines the scenarios probability. The formulation followed is based on [

48].

4.5. Objective Function

The objective function (OF) is defined though the weighted sum approach. The aim is to minimize the cost and risk of the portfolio, as in Equation (12). The weights used in the trade-off are defined through the value of the risk aversion factor β. This factor defines the decision-maker’s propensity towards risk. If β became equal to 0, the OF only considers the cost, representing 100% of OF, but if β takes the value 5, the weight associated to the cost term of the OF is 1/6 and the remaining related to the CVaR term, as 5/6.

The decision-maker aversion to long-term investment is characterized by the parameter, λ. This parameter aims to countering or favoring the production of self-generated energy based on the willingness to contract technology with high fixed costs and long-life span.

The objective function is defined in Equation (12), which minimizes the costs and risk, based on β values.

5. Data Collection and Parameter Estimation

The electricity data explored in the work is from Iberian Operator database [

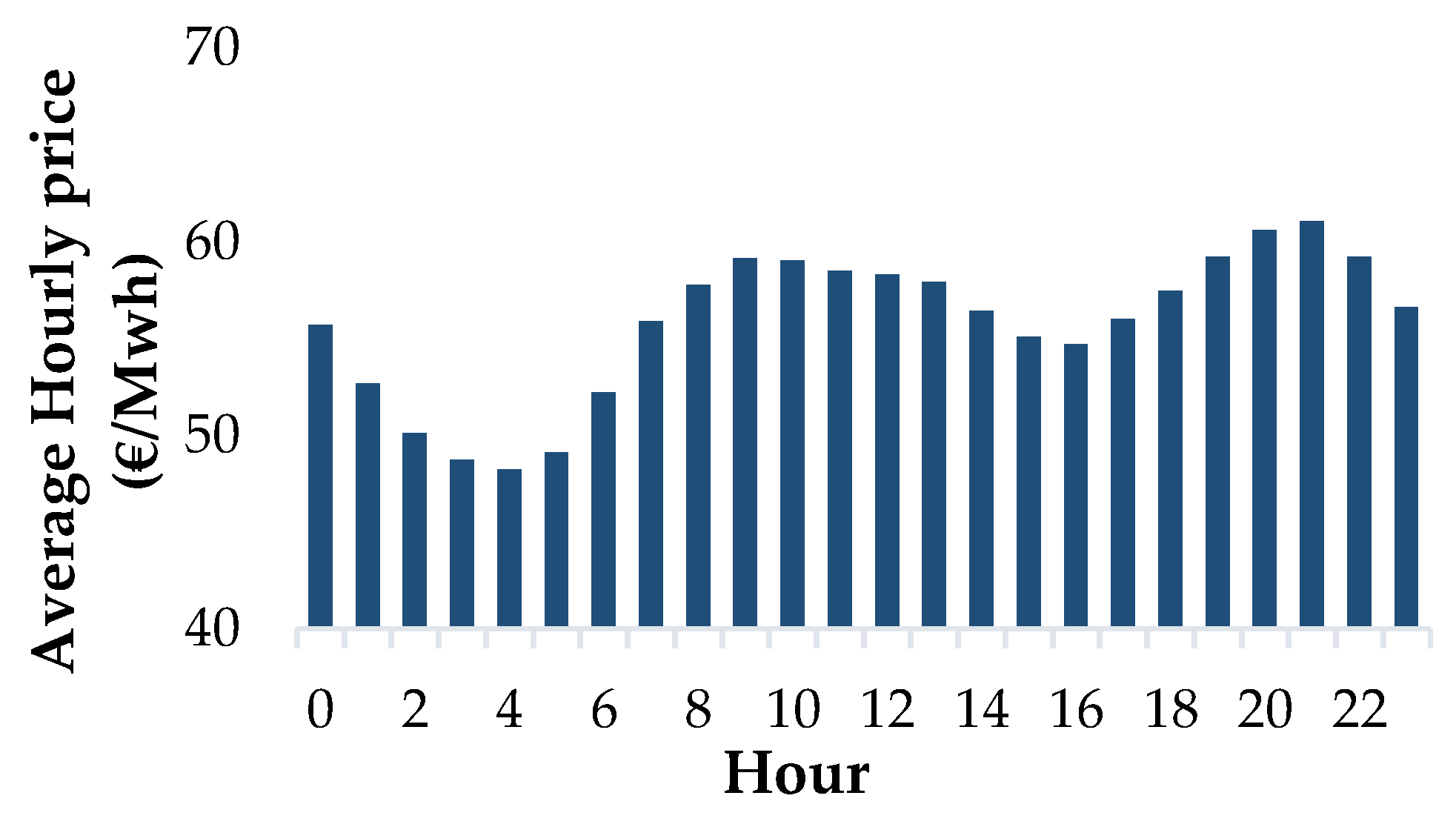

7], over one year (September 2018 to August 2019). The year considered is representative of the Iberian electricity market. However, data screening was performed and 48 weeks is considered as a final sample. The seasonality and daily market variability are shown in

Figure 2 and

Figure 3.

Along the day, the spot market prices follow a high variability, triggering a very high data volume. To overcome this drawback, the hourly price values for the planning horizon over the 24 h in the 48 weeks, are averaged, as shown in

Figure 2. The variability pattern in 24 h, denotes amplitude of 12.97 €, with its maximum of 61.02 € at 10 p.m. and a minimum of 48.23 € at 5 a.m. Considering this pattern, the data are categorized according to their average spot price, in three categories: valley, shoulder and peak hours. Those categories are associated to low, medium and high price, respectively. The valley hours define the hours with an average market value lower than 54 €, the peak define the hours with an average market value higher than 58 € and the shoulder define the hours with values in between. For 24 h, the following sets are defined:

Valley = {1, 2, 3, 4, 5, 6, 16}

Shoulder = {0, 7, 14, 15, 17, 18, 23}

Peak == {8, 9, 10, 11, 12, 13, 19, 20, 21, 22}

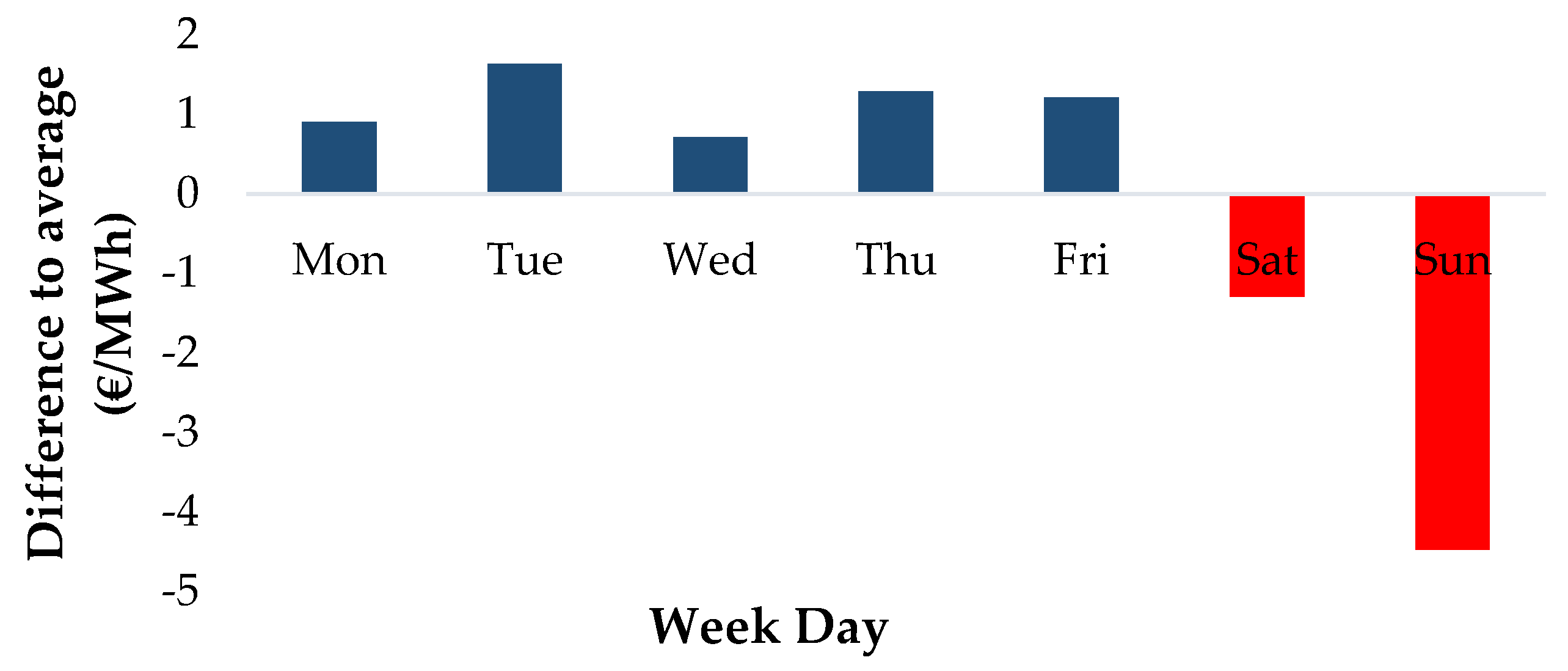

Other relevant data are to define the price for each day of the week, denoted from now on as, weekly day price. The weekly day price pattern results from the difference between the average price of each day of the week over the 48 weeks and the year average, shown in

Figure 3. The weekly day pattern has its highest value on Tuesday and the lowest on Saturday and Sunday. This pattern is directly related with the electricity spot market prices variability.

5.1. Scenario Generation

In the scenario generation, a representative period of three weeks data are used to characterize the scenario: optimistic, pessimistic and expected week, as shown in

Table 1.

The weeks with the highest and lowest average price are chosen as pessimistic and optimistic scenario, respectively. The expected week takes the median of the average value.

In scenario tree,

Figure 1, three branches leave each node, optimistic, expected and pessimistic, leading to 27 scenarios, for the three weeks. The probabilities for each scenario are based on the probability assigned to each branch over the 3 weeks. The scenarios’ probability characterization used the 48 weeks data, to consider yearly seasonality. Using the three weeks average values as a benchmark, the remaining weeks of the data set were divided in 3 sets, based on their average value. Each week is assigned to the set (characterized pessimist, average optimist), which as the closest value to the benchmark. The probabilities of each week shown in

Table 2, is the ration between the numbers of weeks in each set by the total set of 48 weeks. Finally, each scenario probability is obtained using the conditional probability and assuming independence between the events (multiplying the probabilities associated to the three branches leading to that scenario).

5.2. Forward Contract Data

The forward contract explores two different contracts: weekly and 3-week. Beyond that, a map of contract is also considered,

Table 3. The contracts will either set on the 24 h of the weeks they are settled on, denoted as base contracts or on one of the 3 sets of hours of the day, defined above: valley, shoulder and peak, denoted from now one as time-of-day contracts. Therefore 16 contracts are considered, as shown in

Table 3.

Each contract is characterized in 4 blocks based on electricity prices and its electricity availability (maximum and minimum). Each block has 20 MWh available, which adds up to 80 MWh of electricity available per hour in each contract. If a contract is signed, it must have a minimum output of 20 MWh per hour.

The prices of the blocks are assigned to represent the behavior of a price-maker, similar methodology was followed by [

50].

The prices assigned to the block 2 contract, is used as a baseline. Its values were defined considering the average price of each of these times in the spot market (e.g., the valley contracts have the lowest price per energy unit and peak contracts the highest). The prices in blocks 3 and 4 are increased by 5% and 10%, respectively, using the baseline. The baseline price was decreased by 2% to characterize the block 1. The price of the base contracts set is obtained through the prices of the valley, shoulder and peak contracts and the fraction of the day they represent. The resulting prices are shown in

Table 4.

The price of the second block for the 3-week contracts is determined by decreasing the values of the corresponding weekly contract in 2%. The price for the other blocks is calculated following the same methodology as the one used in the weekly contracts.

5.3. Self-Generation Facility

The self-generation case explores the implementation of a single renewable electricity source, with a levelized electricity price to characterize the fixed and variable costs. The levelized electricity price assumes the price per energy unit produced throughout the entire expected lifetime of the equipment. This way, it is possible to put the long-term investment into perspective, enabling a comparison with the electricity spot market prices, which allows an analysis of trade-off of the two.

Data were taken from study conducted by Fraunhofer Institute for Solar Energy Systems [

51]. The installation of a PV technology is assumed. The levelized price is 35.5 €/MWh. This will be the price for the first block of energy. The following blocks’ prices are obtained by subsequently increasing in 10% the value of the original block, shown in

Table 5. This method represents other costs that arise as the investment grows, e.g., cost of space for the PV panels. Each block has 15 MWh of energy available and there is a minimum of 15 MWh, if this source is chosen.

7. Conclusions

This work proposes a mixed integer linear formulation for the energy portfolio optimization problem for large consumer in a buyer perspective. A multi-objective approach is explored to deploy several options to the decision-maker based on its risk pattern. A weighted sum formulation is presented for the expected cost and risk minimization. The binary variables define the procurement decisions and the continuous variables define the electricity procured, cost of each electricity supplier options, as well as the value of the CVaR.

The Iberian electricity market is considered as a case study. The data analysis and screening are developed and are highlighted and used in the cases studies for price seasonality, weekly and daily bases. The electricity supply options explored for the portfolio characterization are pool market, forward contract and self-generation.

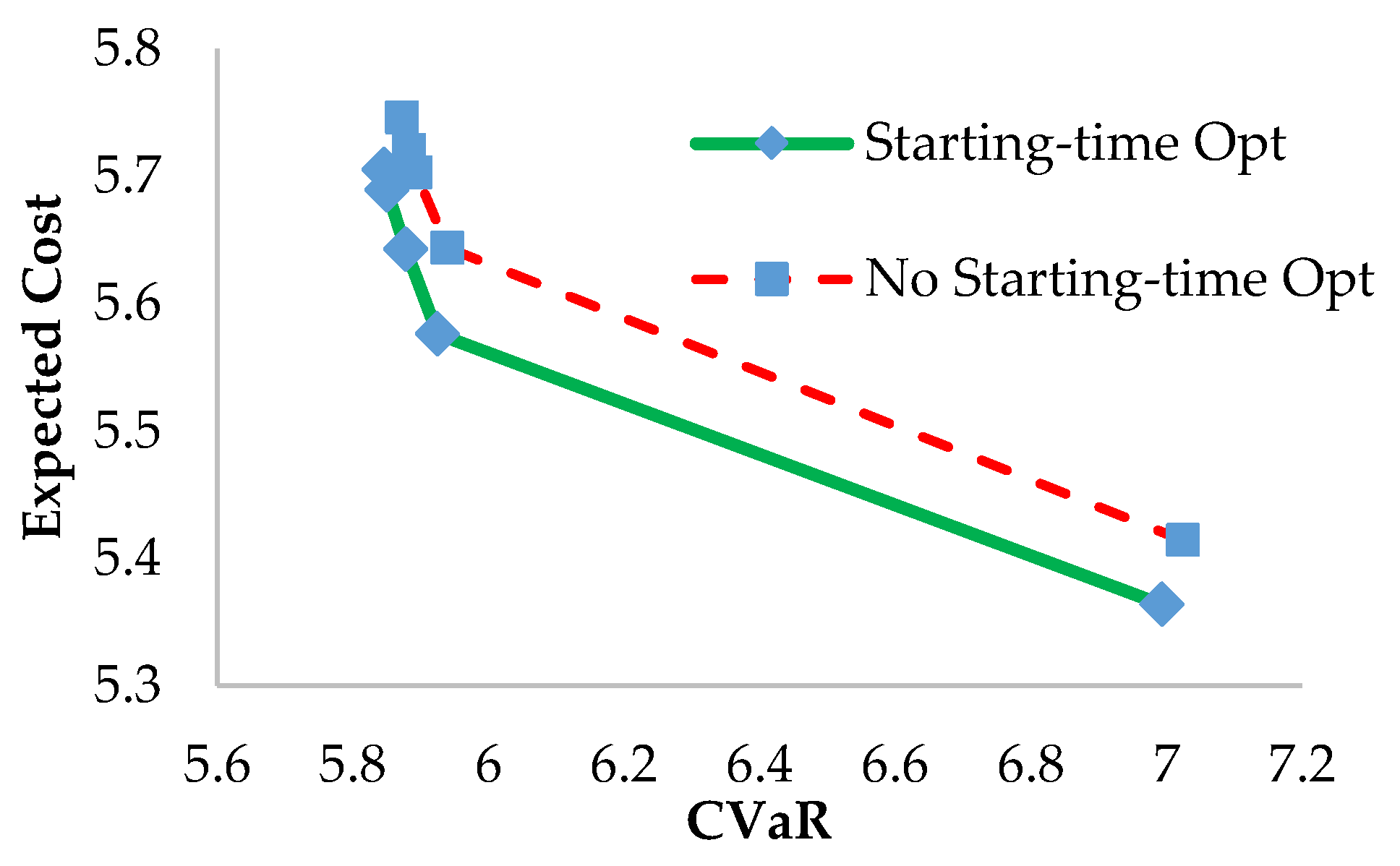

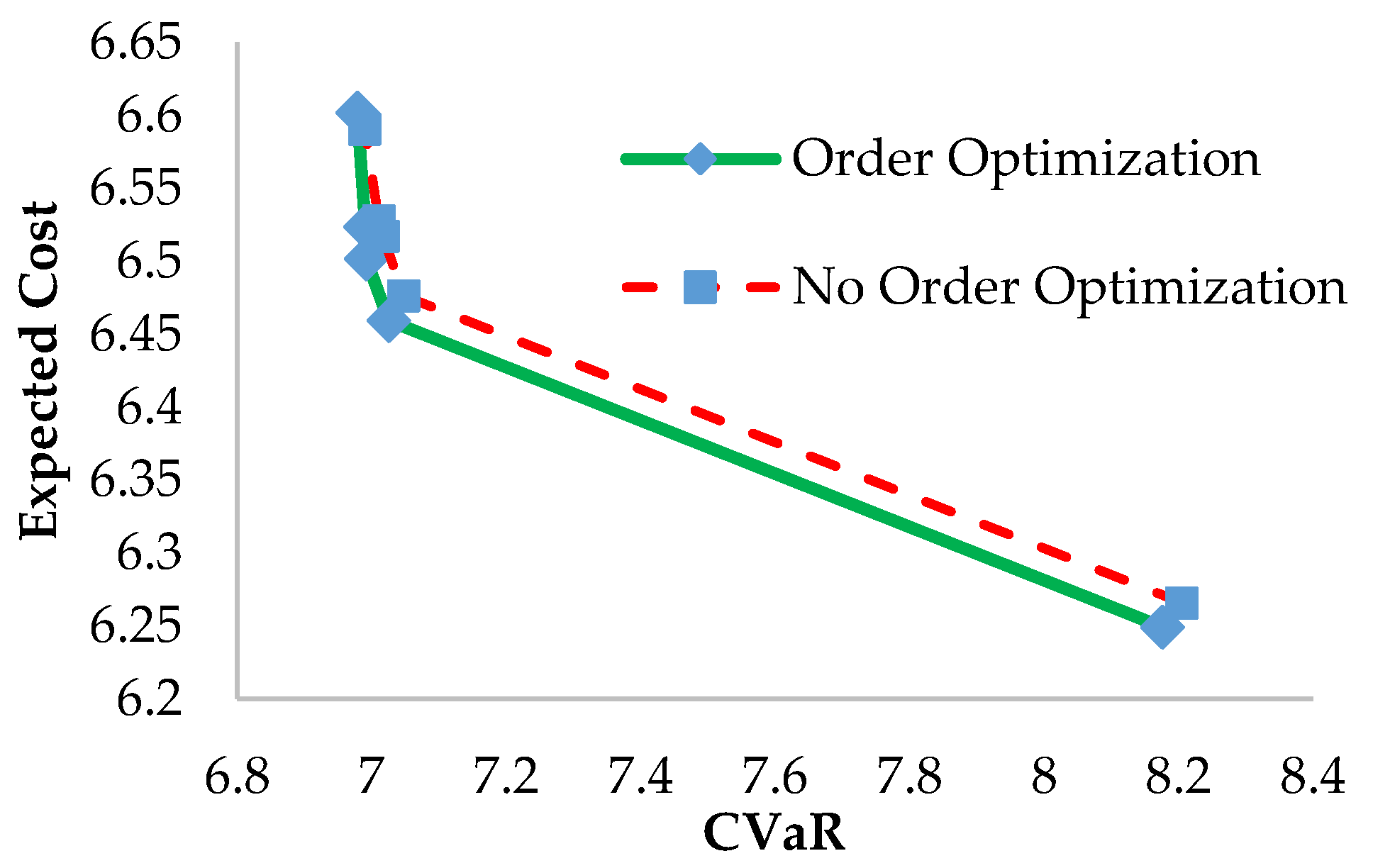

The portfolio characterization and the decision-maker behavior towards to risk is developed exploring three cases. Case a) uses constant demand profile; case b) explores manufacturing aspect, considering a cyclic daily demand and a comparison between nominal operating starting time and its optimization is developed, while case c) explores the weekly day price seasonality. In all cases different values of the risk aversion factor are explored.

Some practical guidelines may be drawn from the results. From case a) the pool market procurement reveals more suitable for decision-maker with pattern taker to risk, while risk averted decision-maker prefer forward contracts and self-generated energy. These different postures lead to a higher CVaR and lower expected cost for the risk taker decision-maker and lower CVaR and higher expected cost for the risk averted decision-maker.

The seasonality effect is explored in cases b) and c). The results from case b), which consider the hour seasonality, avoid the high price hours and favor the low-price hours. In case c) the week seasonality is considered and the tendency is favoring low price days rather than high price. The advantage from using the hour price seasonality (case b) shows better results in terms of objective than case c). As a guideline for the decision-maker, the demand allocation considering the hours of the day, reveled more effective in price reduction than solely paying attention to the day of the week.

Three aspects should be considered as further work. The self-generated energy should be explored not only from the buyers, but also the seller perspective. The use of converting temporarily the electricity in some other form, taking advantage from the low price, so as to be used in the short term. In addition, data analytics approaches, to deal with more detailed information and real-time optimization.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}