Can Green Hydrogen Production Be Economically Viable under Current Market Conditions

Abstract

:1. Introduction

- Today, industry prevails in total hydrogen consumption. The main consumers are plants for the production of ammonia, methanol, and steel. Almost all hydrogen is produced using fossil fuels, so there is great potential for reducing emissions using clean and ecologically acceptable (green) hydrogen.

- The competitiveness of electric vehicles with hydrogen fuel cells in traffic is conditioned by the costs of fuel cells and hydrogen fueling stations, while the priority for trucks and buses is to reduce the price of supplied hydrogen. Shipping and aviation have limited opportunities to use low-carbon fuels, so new hydrogen-based fuels (synthesized hydrocarbon fuels) are an opportunity to use green hydrogen also in aviation.

- In urban areas, hydrogen can be injected directly into existing natural gas pipelines, with the greatest potential in family households and commercial buildings, especially in dense urban areas, while long-term options could include the use of pure hydrogen in hydrogen gas burners or fuel cells.

- In electric energy production, hydrogen is one of the leading options for storing of temporal excesses of electric energy. Hydrogen can be used in gas turbines to increase the flexibility and robustness of the power systems, and hydrogen produced ammonia could be used in coal-fired power plants to reduce emissions.

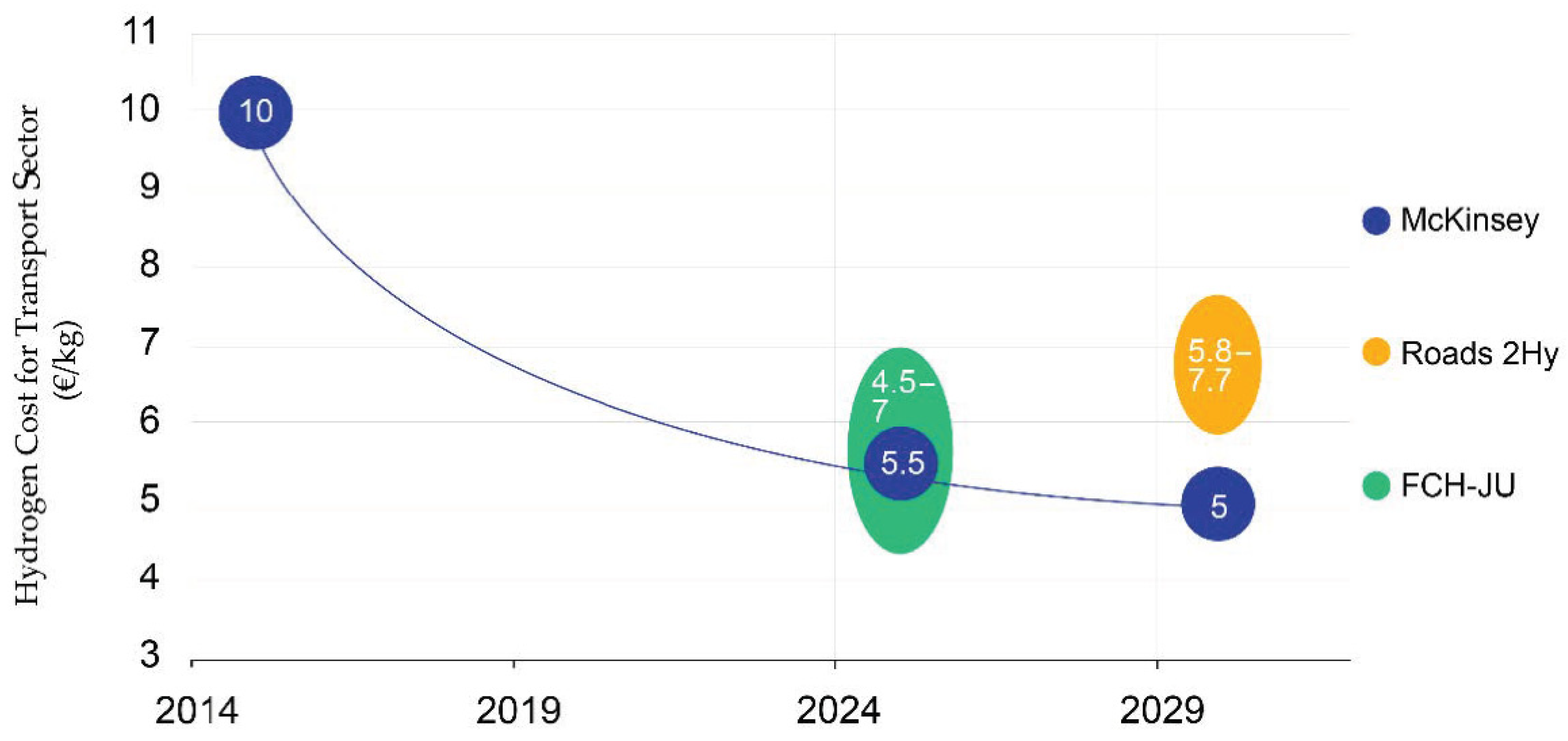

2. Overview of Hydrogen Prices

3. Hydrogen Production in Hydro Power Plant

3.1. Case-Study Hydro Power Plant

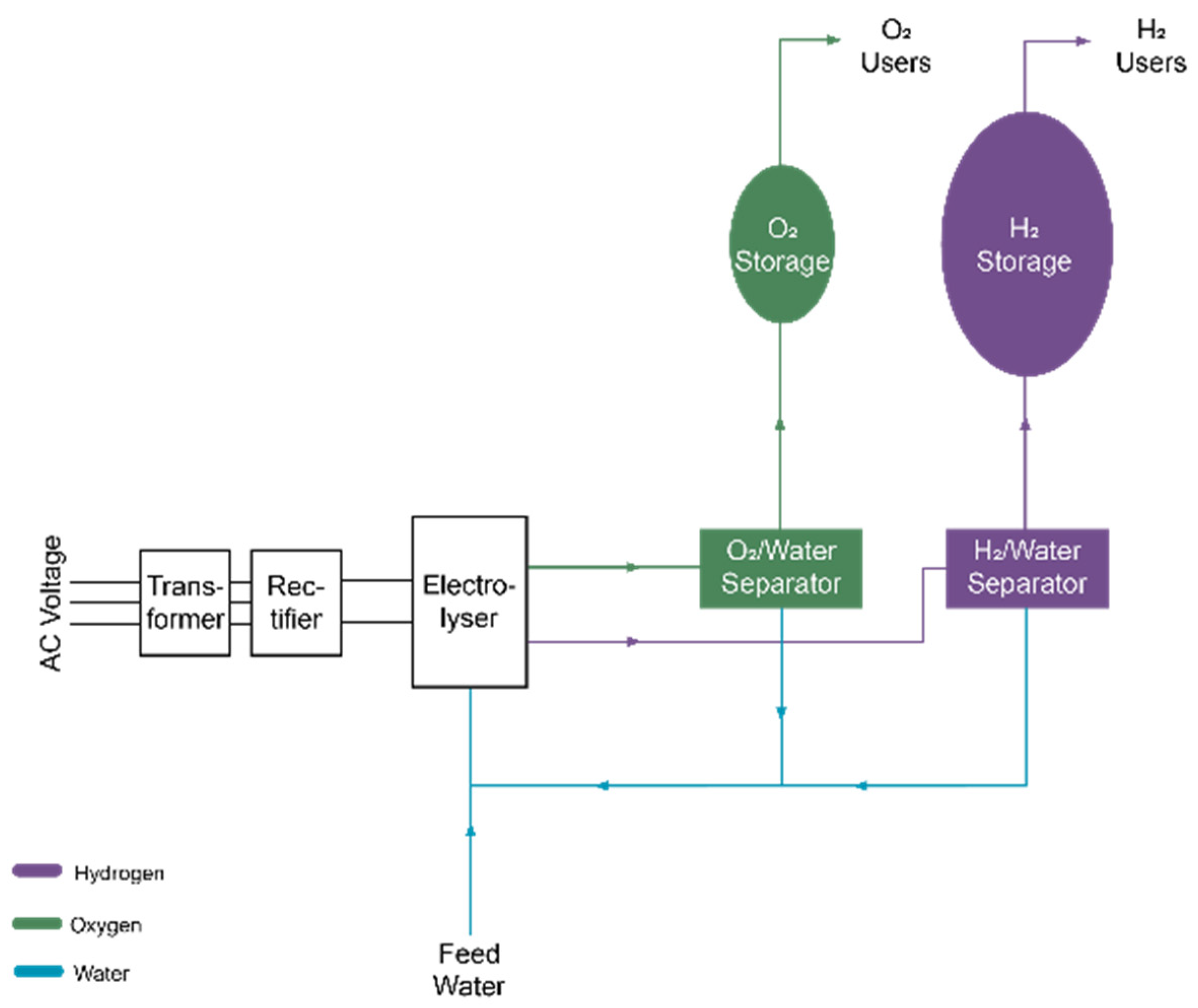

3.2. Equipment for Hydrogen Production

- Specific density: 0.08988 kg/Nm3;

- Lower heating value (LHV): 119.96 MJ/kg (i.e., 33.32 kWh/kg or 3.00 kWh/Nm3).

4. Economic Viability of Hydrogen Production in HPP

4.1. Hydrogen Production Cost in Case-Study HPP

- PC1—cost related to CapEx and OpEx of P2G system equipment and maintenance.

- PC2—cost of electric energy for operation of P2G system and hydrogen generation.

= (2,200,000 € + 15 × 110,000 €)/2,833,860 kg =

= 1.36 €/kg,

= 2,833,860 kg,

4.2. Production of Hydrogen Instead of Electricity

5. Competitiveness of Green Hydrogen within Different Sectors

5.1. Use of Green Hydrogen in Industry as a Feedstock

5.2. Use of Green Hydrogen for Heat Generation

5.3. Use of Green Hydrogen for Transport and Mobility

- Elimination of air pollution (CO, NOx, PM10 particles, etc.) in urban areas;

- Reduction of overall CO2 emissions to the atmosphere (if green hydrogen is produced from excess of green electricity).

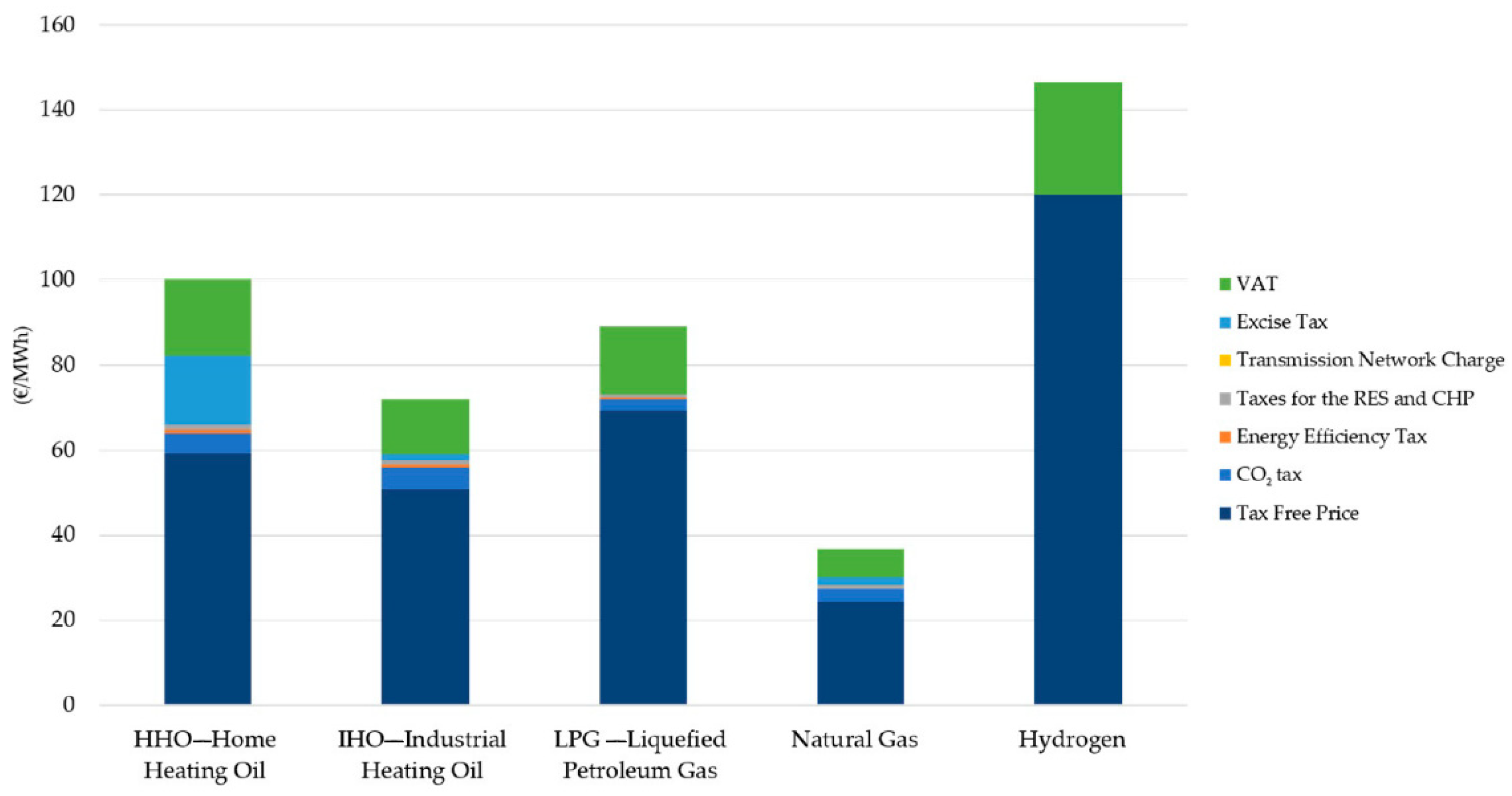

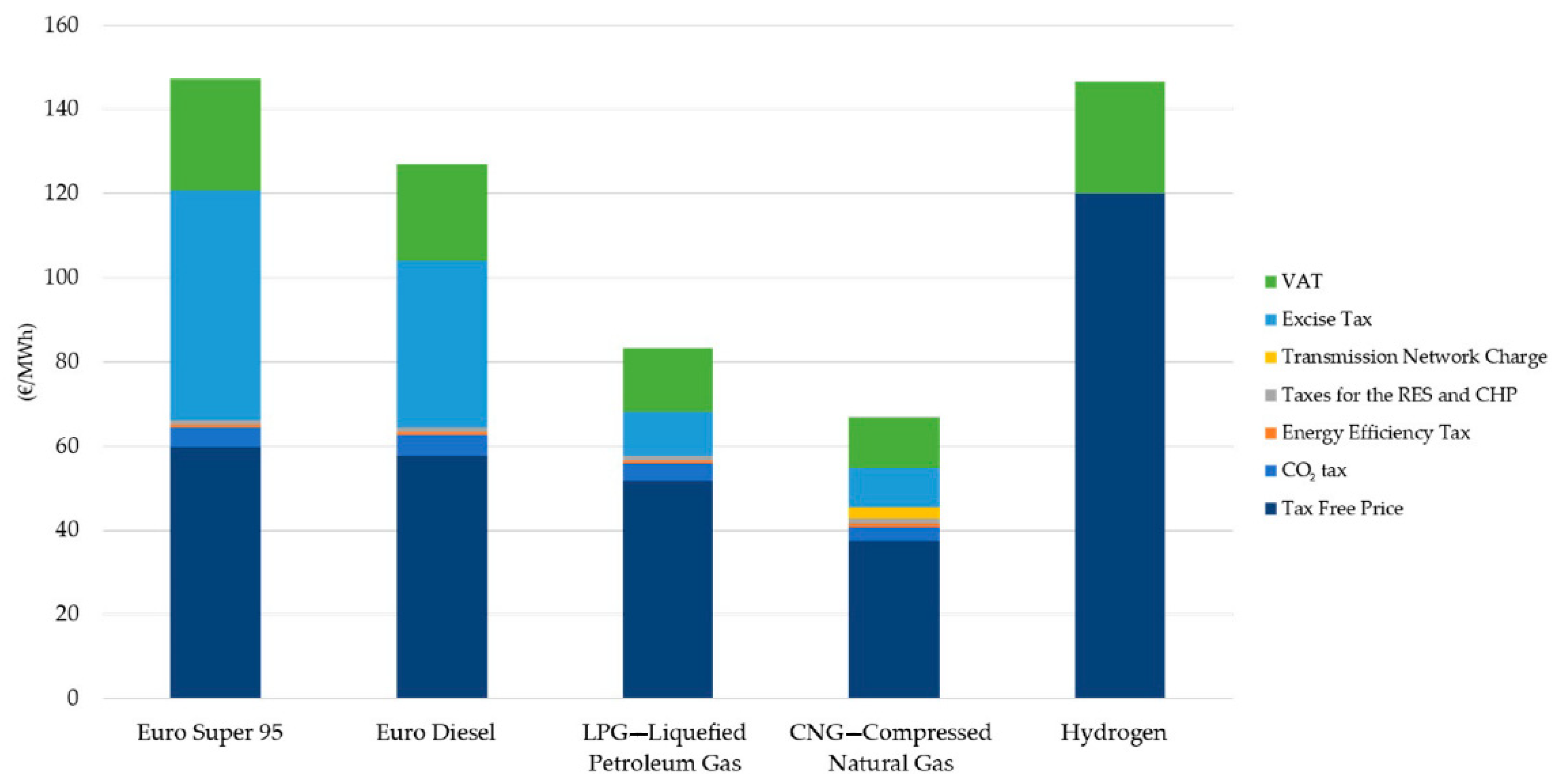

- Fuel price (raw fuel price without taxes),

- Environmental taxes;

- VAT.

- If raw fuel prices (without taxes) are compared in €/MWh, the price of green hydrogen is the highest and cannot compete with hydrocarbon fuels;

- If end fuel processes (with all taxes added) are compared in €/MWh, then green hydrogen price is comparable to gasoline and somewhat higher than diesel;

- Current high taxes of hydrocarbon fuels make green hydrogen a competitive option for transport at current conditions.

- Applications with limited number of vehicles are engaged;

- Applications with large vehicles, so that the cost of the fuel cell propulsion system represents a lower part of total vehicle costs than in the case of e.g., passenger cars;

- Daily travel distance of each vehicle should be substantial and should significantly exceed the capacity of the electric battery, so battery propulsion is not the optimum option;

- Vehicles operate over a limited geographical region, so all vehicles can be refueled at just one or few (e.g., 2–3) refueling stations;

- Longer stop time (as usually required for battery recharge) is not acceptable, vehicles must operate almost continuously, so quick refueling is mandatory.

6. Ancillary Services

- The service is activated automatically by the remote command given by the electric grid operator;

- The service has to start within 30 s after the command and it has to reach the demanded power within 15 min after the command has been given;

- Service providers are payed by the grid operator. They are paid for their readiness by a flat rate of 183,000.00 €/MW/year;

- Additionally, service providers are paid for actually supplied electric energy during the activated SC, at the price, which equals current stock exchange price, increased by certain factor.

- (a)

- In the case of no involvement in SC (Figure 5a), the HPP earns 950 €/h from the electric energy system and 50 €/h from the P2G, which consumes 1 MW of electricity that could otherwise be sold on the market for 50 €/h. Instead, P2G generates an income of 120 €/h due to produced and sold hydrogen. P2G also generates fixed costs of 29.30 €/h of CapEx and OpEx. All of these result in an additional profit of 40.70 €/h compared to the standalone HPP operation without P2G.

- (b)

- In the case of involvement in SC and inactive SC (Figure 5b), the situation is similar to case a), which means that 1 MW of electric power is used for hydrogen generation and no extra power is supplied to the grid. Nevertheless, there is an additional income of 20.89 €/h due to the SC readiness flat rate (183,000.00 €/MW/year). This results in an extra profit of 61.59 €/h compared to standalone HPP.

- (c)

- In the case of involvement in SC and active SC (Figure 5c), HPP supplies 19 MW + 1 MW of electric power to the grid. The price of regular power is 50 €/MWh, while the price of extra power is higher, for this illustrative example, it is assumed to be 90 €/MWh. Consequently, the HPP earns 1040 €/h from the electric energy system. There is no income from hydrogen, since hydrogen production is stopped. The income of 20.89 €/h due to SC readiness and the fixed P2G costs of 29.30 €/h also remain. This leads to a P2G loss of 8.41 €/h and HPP extra profit of 40 €/h, which results in an extra profit of the system of 31.59 €/h.

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Dincer, I. Green methods for hydrogen production. Int. J. Hydrogen Energy 2012, 37, 1954–1971. [Google Scholar] [CrossRef]

- International Energy Agency. The Future of Hydrogen, Seizing Today’s Opportunities; International Energy Agency: Paris, France, 2019. [Google Scholar]

- Fraile, D.; Lanoix, J.C.; Maio, P.; Rangel, A.; Torres, A. Overview of the Market Segmentation for Hydrogen Across Potential Customer Groups, Based on Key Application Areas. European Commission, 2015. Available online: http://www.certifhy.eu/images/D1_2_Overview_of_the_market_segmentation_Final_22_June_low-res.pdf (accessed on 9 November 2020).

- Basile, A.; Linguori, S.; Iulianelli, A. Membrane reactors for energy applications and basic chemical production. In Membrane Reactors for Energy Applications and Basic Chemical Production; Di Paola, L., Piemonte, V., Basile, A., Hai, F., Eds.; Elsevier: Amsterdam, The Netherlands, 2015; pp. 31–59. ISBN 978-1-78242-223-5. [Google Scholar]

- Mazza, A.; Bompard, E.; Chicco, G. Applications of power to gas technologies in emerging electrical systems. Renew. Sustain. Energy Rev. 2018, 92, 794–806. [Google Scholar] [CrossRef]

- Jovan, D.J.; Jovan, V.; Dolanc, G. Technoeconomic Assessment of Introducing P2g System into One of Slovenia’s HPP; Jozef Stefan Institute: Ljubljana, Slovenia, 2020. (In Slovene) [Google Scholar]

- Hyways. Available online: http://www.hyways.de/ (accessed on 29 June 2020).

- McKinsey & Company. A Portfolio of Power-Trains for Europe: A Fact Based Analysis; EESI: Washington, DC, USA; Available online: https://www.eesi.org/files/europe_vehicles.pdf (accessed on 29 June 2020).

- Hinicio. Hydrogen Europe. Available online: https://hydrogeneurope.eu/member/hinicio (accessed on 29 June 2020).

- European Commision. Energy Prices and Costs in Europe; SWD (2019) 1 Final; the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions: Brussels, Belgium, 9 January 2019; Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=COM:2019:1:FIN&from=EN (accessed on 9 November 2020).

- McKinsey & Company. Urban Buses: Alternative Powertrains in Europe. Available online: https://www.fch.europa.eu/sites/default/files/20121029%20Urban%20buses%2C%20alternative%20powertrains%20for%20Europe%20-%20Final%20report_0_0.pdf (accessed on 29 June 2020).

- Ansaldo Energia. Available online: https://www.ansaldoenergia.com/PublishingImages/Idrogeno/Ansaldo-Energia-H2.pdf (accessed on 16 July 2020).

- European Commission. Energy Roadmap 2050; Publications Office of the European Union: Luxembourg, 2012. [Google Scholar]

- Lewandowska-Bernat, A.; Desideri, U. Opportunities of power-to-gas technology in different energy systems architectures. Appl. Energy 2018, 228, 57–67. [Google Scholar] [CrossRef]

- Schiebahn, S.; Grube, T.; Robinius, M.; Tietze, V.; Kumar, B.; Stolten, D. Power to gas: Technological overview, systems analysis and economic assessment for a case study in Germany. Int. J. Hydrogen Energy 2015, 40, 4285–4294. [Google Scholar] [CrossRef]

- Van Leeuwen, C.; Mulder, M. Power-to-gas in electricity markets dominated by renewables. Appl. Energy 2018, 232, 258–272. [Google Scholar] [CrossRef]

- Fischer, D.; Kaufmann, F.; Selinger-Lutz, O.; Voglstätter, C. Power-to-gas in a smart city context—Influence of network restrictions and possible solutions using on-site storage and model predictive controls. Int. J. Hydrogen Energy 2018, 43, 9483–9494. [Google Scholar] [CrossRef]

- Chen, Z.; Zhang, Y.; Ji, T.; Cai, Z.; Li, L.; Xu, Z. Coordinated optimal dispatch and market equilibrium of integrated electric power and natural gas networks with P2G embedded. J. Mod. Power Syst. Clean Energy 2018, 6, 495–508. [Google Scholar] [CrossRef] [Green Version]

- NEL Hydrogen. Containerized Atmospheric Alkaline Electrolyser. Available online: https://nelhydrogen.com/product/atmospheric-alkaline-electrolyser-a-series/ (accessed on 14 October 2020).

- Thema, M.; Bauer, F.; Sterner, M. Power-to-gas: Electrolysis and methanation status review. Renew. Sustain. Energy Rev. 2019, 112, 775–787. [Google Scholar] [CrossRef]

- Gondal, I.A. Hydrogen integration in power-to-gas networks. Int. J. Hydrogen Energy 2019, 44, 1803–1815. [Google Scholar] [CrossRef]

- Schiro, F.; Stoppato, A.; Benato, A. Modelling and analyzing the impact of hydrogen enriched natural gas on domestic gas boilers in a decarbonization perspective. Carbon Resour. Convers. 2020, 3, 122–129. [Google Scholar] [CrossRef]

- Quarton, C.J.; Samsatli, S. Power-to-gas for injection into the gas grid: What can we learn from real-life projects, economic assessments and systems modelling? Renew. Sustain. Energy Rev. 2018, 98, 302–316. [Google Scholar] [CrossRef]

- Trinomics, B.V. Study on Energy Prices, Costs and Subsidies and Their Impact on Industry and Households—Final Report; European Commission—DG Energy: Rotterdam, The Netherlands, 2018. [Google Scholar]

- Thomas, D.; Mertens, D.; Meeus, M.; Van der Laak, W.; Francois, I. Power-to-Gas Roadmap for Flanders—Final Report; WaterstofNet vzw: Groningen, The Netherlands, 2016. [Google Scholar]

- Kaushal, A.; Van Hertem, D.; Hertem, D. An overview of ancillary services and HVDC systems in European context. Energies 2019, 12, 3481. [Google Scholar] [CrossRef] [Green Version]

- Schmidt, O.; Melchior, S.; Hawkes, A.; Staffell, I. Projecting the future levelized cost of electricity storage technologies. Joule 2019, 3, 81–100. [Google Scholar] [CrossRef] [Green Version]

- Bundesministerium für Wirtschaft und Energie. Die Nationale Wasserstoffstrategie; Bundesministerium für Wirtschaft und Energie: Berlin, Germany, 2020. (In German) [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Technical Parameters | Values |

|---|---|

| Nominal power | 1 MW |

| Net production rate | up to 300 Nm3 H2/h |

| Production capacity dynamic range | 15–100% of flow range |

| Power consumption at stack | 3.8–4.4 kWh/Nm3 of H2 |

| Delivery pressure | from 30 bar to 200 bar |

| Main P2G System Implementation Costs | Estimated Cost |

|---|---|

| Project documentation | 100,000 € |

| Electrolyzer | 1,600,000 € |

| High pressure storage | 200,000 € |

| BoP 1 components | 120,000 € |

| Electric connection to HPP | 100,000 € |

| Construction and assembly works | 80,000 € |

| Total costs | 2,200,000 € |

| Electricity Costs | PC1 | PC2 | PC (Total) |

|---|---|---|---|

| 35 €/MWh | 1.36 €/kg | 1.75 €/kg | 3.11 €/kg |

| 50 €/MWh | 1.36 €/kg | 2.50 €/kg | 3.86 €/kg |

| 120 €/MWh | 1.36 €/kg | 6.00 €/kg | 7.36 €/kg |

| Selling Price of Hydrogen (€/kg) | Income (€/MWh) | P2G Equipment Costs (€/MWh) | Electricity Costs (€/MWh) | Extra Profit (€/MWh) |

|---|---|---|---|---|

| 3.86 | 77.20 | 27.20 | 50.00 | 0.00 |

| 4.00 | 80.00 | 27.20 | 50.00 | 2.80 |

| 5.00 | 100.00 | 27.20 | 50.00 | 22.80 |

| 6.00 | 120.00 | 27.20 | 50.00 | 42.80 |

| 7.00 | 140.00 | 27.20 | 50.00 | 62.80 |

| 8.00 | 160.00 | 27.20 | 50.00 | 82.80 |

| Variable | Variable Description | Assumed Value |

|---|---|---|

| PowerH2 | Electric power used for hydrogen generation | 1 MW |

| PriceH2 | Selling price of hydrogen | 6 €/kg |

| ConsH2 | P2G consumption of electricity per unit of mass of generated hydrogen | 50 kWh/kg (0.05 MWh/kg) |

| PowerEE | Electric power of extra electric energy supplied during active SC | 1 MW |

| PriceEE | Selling price of extra electric energy supplied during active SC | 90 €/MWh |

| Parameters | Not involved in SC 100% H2 Prod. | SC Active 10% of the time

| SC active 50% of the time

| SC Active 90% of the time

|

| P2G CapEx (investing in equipment) | 2,200,000.00 | |||

| P2G OpEx (% CapEx per year) | 5.00 | |||

| P2G OpEx (per year) | 110,000.00 | |||

| P2G electricity consumption (MWh/kg H2) | 0.05 | |||

| Electricity selling price (€/MWh) | 50.00 | |||

| Electricity selling price during SC (€/MWh) | -- | 90.00 | ||

| Hydrogen, selling price (€/kg) | 6.00 | |||

| Average hydrogen production power (MW) | 1.00 | 0.90 | 0.50 | 0.10 |

| Average SC power (MW) | 0.00 | 0.10 | 0.50 | 0.90 |

| Power reserved for SC (MW) | 1.00 | 1.00 | 1.00 | 1.00 |

| SC readiness flat rate (€/MW/year) | 0.00 | 183,000.00 | ||

| Observation period (years) | 15.00 | |||

| Interim results | ||||

| Amount of hydrogen produced (kg) | 2,628,000.00 | 2,365,200.00 | 1,314,000.00 | 262,800.00 |

| Hydrogen production energy (MWh) | 131,400.00 | 118,260.00 | 65,700.00 | 13,140.00 |

| SC energy (MWh) | 0.00 | 13,140.00 | 65,700.00 | 118,260.00 |

| Costs (€) | ||||

| P2G CapEx | 2,200,000.00 | 2,200,000.00 | 2,200,000.00 | 2,200,000.00 |

| P2G OpEx | 1,650,000.00 | 1,650,000.00 | 1,650,000.00 | 1,650,000.00 |

| Electricity to produce hydrogen | 6,570,000.00 | 5,913,000.00 | 3,285,000.00 | 657,000.00 |

| Costs (total) | 10,420,000.00 | 9,763,000.00 | 7,135,000.00 | 4,507,000.00 |

| Revenue (€) | ||||

| Sales of hydrogen | 15,768,000.00 | 14,191,200.00 | 7,884,000.00 | 1,576,800.00 |

| SC electricity | 0.00 | 525,600.00 | 2,628,000.00 | 4,730,400.00 |

| SC readiness | 0.00 | 2,745,000.00 | 2,745,000.00 | 2,745,000.00 |

| Revenue (total) | 15,768,000.00 | 17,461,800.00 | 13,257,000.00 | 9,052,200.00 |

| Profit = Costs—Revenue | 5,348,000.00 | 7,698,800.00 | 6,122,000.00 | 4,545,200.00 |

| Variable | Variable Description | Assumed Value |

|---|---|---|

| n | Observation period (years) | 15 |

| t | Year index | 1, 2, 3, …, 15 |

| CCapEx,t | Costs of capital expenditures in year t | 2,200,000 € in year 1, 0 € in following years |

| COpEx,t | Costs of operation expenditures in year t | 110,000 €/year |

| CElec,t | Costs of electricity in year t | 472,310 €/year |

| mt | Mass of produced hydrogen in year t | 188,924 kg/year |

| d | Assumed discounting factor | 5% |

| Electricity Costs | PCLevelized |

|---|---|

| 35 €/MWh | 3.40 €/kg |

| 50 €/MWh | 4.15 €/kg |

| 120 €/MWh | 7.65 €/kg |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jovan, D.J.; Dolanc, G. Can Green Hydrogen Production Be Economically Viable under Current Market Conditions. Energies 2020, 13, 6599. https://doi.org/10.3390/en13246599

Jovan DJ, Dolanc G. Can Green Hydrogen Production Be Economically Viable under Current Market Conditions. Energies. 2020; 13(24):6599. https://doi.org/10.3390/en13246599

Chicago/Turabian StyleJovan, David Jure, and Gregor Dolanc. 2020. "Can Green Hydrogen Production Be Economically Viable under Current Market Conditions" Energies 13, no. 24: 6599. https://doi.org/10.3390/en13246599