1. Introduction

Despite agricultural commodities representing only a fraction of most countries’ gross domestic product (GDP), problems pertaining to agriculture significantly influence economies and their respective societies. As a primary industry, agriculture produces grains, fibers and biological assets, deemed as key inputs to several industries, for example those involving intensive agricultural projects whether confined or not, food and clothes production, the cosmetics sector and pharmaceuticals. These industries transform raw materials to produce finished goods that assist in building wealth for either shareholders in particular or economies in general. However, it is evident that natural resources may be depleted with the result that companies might encounter significant risk and loss (

ACCA et al. 2012;

Dasgupta 2008;

Costanza et al. 2014).

Consequently, it is essential to properly manage the depletion and consumption of these resources by taking global actions to protect the wealth of humanity. At the company level, requirements must be followed related to the environment and reports of how these are satisfied must be included as part of their disclosures on corporate social responsibility. Such practices increase the value relevance of information and, as noted by

Ogilvy (

2015), the measurement of biological assets (bearer plants, livestock, the harvest and produce) is required by all accounting bodies.

In most countries, agricultural enterprises are primarily regulated under International Accounting Standards (IAS) number 41 Agriculture, as “

Agricultural activity is the management by an entity of the biological transformation and harvest of biological assets for sale or for conversion into agricultural produce or into additional biological assets” (

IFRS 2021a, IAS 41, para. 5).

Biological assets (BA) include livestock, crops, and fruits. Changes in the physical characteristics of living animals or plants directly increase or decrease the economic benefits to the business (

Deloitte 2000). “

This Standard is applied to agricultural produce, which is the harvested produce of the entity’s biological assets, at the point of harvest. Thereafter, IAS 2 Inventories or another applicable Standard is applied. Accordingly, this Standard does not deal with the processing of agricultural produce after harvest; for example, the processing of grapes into wine by a vintner who has grown the grapes. While such processing may be a logical and natural extension of agricultural activity, and the events taking place may bear some similarity to biological transformation, such processing is not included within the definition of agricultural activity in this Standard” (

IFRS 2021a, IAS 41, para. 3).

The relative importance of agriculture in the global economy has traditionally received little recognition, and therefore accounting in this field did not begin to attract attention from scholars in the accounting field until the issuance of IAS 41 by the IASB (

Fisher and Marsh 2013;

Herbohn and Herbohn 2006).

With the introduction of IAS 41 in 2001, accounting for agricultural activities became more flexible with the opportunity to switch from the cost to the fair value (FV) approach. In this context, agricultural enterprises have been given the choice of using the principle of acquisition cost minus accumulated depreciation and loss due to impairment (cost model), or the revaluation model (in which the fair value of can be reliably measured) to track variations in asset values. The resultant change in asset value influences the firm value (

Ogilvy 2015). Since then, accounting scholars have discussed the pros and cons of FV accounting over historical costs (

Bozzolan et al. 2016).

Alternatively,

Filho et al. (

2013) found that the adoption of fair value had a positive impact on the equity of the companies they analyzed, which in turn benefited all stakeholders. Thus, important perspectives can be noticed in terms of the decision maker’s power in valuing biological assets, such as the application of the present value by measuring the discounted cash flow. The existence of specific parameters for determining discount rates, which are guided by recognized accounting standards may decrease the need for managerial judgment, and reduce the likelihood of errors and manipulation problems as well as enhancing comparability (

Eckel et al. 2003).

This major switch from the traditional acquisition cost model to the FV model (

Lefter and Roman 2007) caused an important debate on accounting within agriculture (

Argilés et al. 2011). Subjectivity is a manifest challenge of FV due to the difficulty of computing FV, particularly if the market is not efficient and there is an absence or unavailability of Level 1 inputs for assets and liabilities (

Pandya et al. 2021).

Within the content of IAS 41, accounting rules allow management discretion in selecting accounting practices, and this change has prompted research interest. For example, studies by

Cormier et al. (

2009) in France and

Hellman (

2011) in Sweden provided some signs regarding the implementation of discretionary power when applying the International Financial Reporting Standards (IFRS). Such discretion was evidenced in the use of the FV model in the absence of observable data, and results in managers being held responsible for using the present value method, which can make them more or less prudent in their forecasts (

Silva et al. 2015).

Moreover, during the consultation on the IASB 2011 agenda, numerous respondents expressed concern about the cost complications and practical difficulty of measuring BA at FV, especially in the absence of an active market (

Bozzolan et al. 2016).

Furthermore, confusion may occur due to the increased focus on the value relevance of accounting information at the expense of either cost reduction or discretionality, and the increased faithful representation of information secured by using the cost model. The best accounting practices might be governed by certain firm characteristics, whereas the suitable measurement and the pertinent disclosures of agricultural activities may vary across such characteristics (

Gonçalves and Lopes 2015).

The relative importance of agriculture in the global economy has traditionally received little recognition, and therefore accounting in this field did not begin to attract attention from scholars in the accounting field until the issuance of IAS 41 by the International Accounting Standards board (IASB) (

Fisher and Marsh 2013;

Herbohn and Herbohn 2006).

The use of fair value to measure biological assets permits managerial judgment that may precipitate arbitrary decisions, particularly when using discounted cash flows and/or where an active market is absent, thereby affecting the amount of relevant information presented (

Silva et al. 2015). However,

Silva et al. (

2015) were unable to find sufficient evidence of the level of discretionary differences; consequently, it is deemed valuable to inspect the accounting practices associated with measurement and disclosure within agricultural activities companies, and to do so using firm characteristics as variables. Additionally, as agricultural commodities represent a major portion of many developing countries’ GDP including Jordan, there is merit in this study. Particularly, recent support and guidance are directed toward this sector in Jordan. Furthermore, the study findings provide key inputs to the agricultural sector in Jordan and other countries, enabling better management of resources at both the company and global levels. Jordan can be considered a good example to represent developing countries due to its early adoption of IAS.

Moreover, the measurement and disclosure practices pertaining to agricultural activities in Jordan need to be clarified and explored to facilitate the missions of responsible bodies in Jordan regarding the directions and financial or logistic supports. Exploring the accounting practices of agricultural firms based on general firm characteristics simplifies the direction of either guidance or financial and logistic supports according to these characteristics. These general characteristics are directly related to the companies, not to the board and management who ruled these companies. The general characteristics have a more constant nature compared to other characteristics associated with corporate board characteristics. A constant nature is more desirable for directing support and guidance.

To sum up, the current study does not aim to examine the pros and cons of FV versus historical cost, but rather focuses on exploring accounting practices related to measurement and disclosures in Jordanian companies that engage in agricultural activities based on their characteristics, and the extent to which companies adhere to the disclosure requirements mandated in IAS 41. Research in this area is worthwhile as it should be of value to standards setters in enhancing their understanding of measurement and disclosure practices with agricultural companies in a developing country.

3. Methodology

3.1. Data and Sample

As the Jordanian Companies Control Department allows companies to declare more than one purpose, the study population consisted of all reporting entities operating in Jordan that embraced one or more agricultural activity within its purposes. Reporting requirements in Jordan mandate that all companies enjoying limited liabilities such as corporations and limited private companies prepare and publish their financial reports according to full IFRS and submit these reports to the Companies Control Department (

SDC 2006). Companies that do not enjoy limited liabilities, such as general partnerships and limited partnerships, are only required by the Companies Law to prepare and publish their financial reports according to full IFRS and submit these reports to the Companies Control Department if their capital or turnover exceeds 100,000 JD (

SDC 2006). Therefore, the population consisted of reporting entities with capital exceeding 100,000 JD and declaring agricultural activity within its purposes.

The Articles number based on the legal form that required this in the Jordanian companies’ law are listed as the following:

General partnership: Article 24 B.

Limited partnership: Article 48.

Limited liabilities: Article 62.

Limited private company: Article 75 bis.

Listed corporation: Articles 184–185 bis.

Although the regulator obliges all companies with limited liabilities to prepare and publish their financial reports according to full IFRS regardless of either capital or turnover amount, this study used the 100,000 JD as a minimum amount for the capital of companies included in its population. This was performed to eliminate micro or small entities since they usually encounter obstacles in adopting international standards when compared to medium and large entities. Additionally, their elimination was believed to enhance the consistency of sample, and to avoid size outliers. Equally important is the fact that the reporting entities followed the requirements of the Jordan Securities Commission regarding the disclosure instructions that were issued in 2004 and amended in 2019 (

JSC 2019). Article 14 of disclosure instructions issued by the Jordan Securities Commission requires companies to prepare their financial information based on full IFRS in terms of presentation, measurement, and recognition (

JSC 2019). The disclosures are directed by the Jordan Securities Commission.

After filtering the registered companies in the Companies Control Department based on the above criteria, the population of companies totaled 276 companies (that also replied to questionnaire), all of which were targeted for gathering secondary data via the disclosure index. However, 17 companies were excluded based on IAS 41 paragraphs 1, 5, 10, 12, and 30, that specified the companies that must be excluded from the adoption of IAS 41. Accordingly, the total number of population is 259 companies that were entirely targeted.

3.2. The Method

Given the dimensions of this study, a multimethod approach (see

Tashakkori and Teddlie 2003) was used involving two quantitative instruments, these being a questionnaire survey and a disclosure index.

The structured questionnaire survey with financial managers was implemented to obtain information that could not be directly gathered from the financial reports of companies. In detail, the questionnaire survey (

Appendix A) comprised fourteen questions about topics not featured in financial reports. These questions were divided into two main categories.

The first category contained five questions relating to inclusion and exclusion that were developed based on IAS 41 paragraphs 1, 5, 10, 12, and 30. If the answer to any of these questions was YES (except for Question number two where the answer should be NO), the company was excluded from the data set as this would mean that its agricultural transactions would be exempted from the requirements of IAS 41.

The second category contained nine questions associated with classification matters, which determined the number of items (in the disclosure index) that each company could disclose. For instance, Question 6 helped in classifying the company based on measurement, dividing companies into two categories, which eventually helped in specifying the number of items within the index that each company could disclose according to the adopted measurement method. These questions were developed based on the paragraphs within IAS 41 and distributed to the financial managers of the targeted companies.

During the second half of 2022, the questionnaires were distributed and collected by the author in person or via email, or by filling the responses from financial managers by telephone. The contact information about companies were available at Jordanian companies control department as well as on the website of some companies. The questionnaires were distributed to 334 companies (all reporting firms engaged in agricultural activities), only 83% (276 questionnaires from 276 companies) were returned. However, 17 companies were excluded for the aforementioned reason. Thus, the final number of targeted companies was 259. The high response rate is due to that the questionnaire was designed to obtain factual responses related to adoption of IAS 41 rather than seeking opinions or perceptions. In addition, the number of question was not many (only 14 questions).

As shown in

Appendix A, the index also includes the company number and was used to obtain data from financial reports. This comprised two main parts: the first pertaining to company characteristics, and the second associated with disclosure requirements (based on IAS 41 paragraphs). The amendments made to the indexes used in previous studies are shown in

Appendix B together with the justifications for those changes. The number of paragraphs that were used in developing the disclosure index is provided for each items as illustrated in

Appendix A and

Appendix B.

In order to link the responses secured by these two techniques, the questionnaire for each company was cross-coded according to the published information before distribution, and the eventual questionnaire data were subsequently attached to the corresponding published data for each company. The respondents were informed of this process.

The questions regarding classification in the questionnaire were linked to specific items within the disclosure index (e.g., Question 9 about government grants linked with items 35–37 on the same topic) in order to specify the number of items that can be disclosed by the pertinent company, this number being used to compute the item index for each company. Both instruments were used to test the relationships between the variables accurately.

Table 1 presents the rationale for each question in the questionnaire (developed based on IAS 41 paragraphs).

The disclosure index measured the level of disclosure as the dependent variable, as has commonly been used in previous studies (

Lopes and Rodrigues 2007;

Oliveira et al. 2006;

Akhtaruddin 2005;

Owusu-Ansah 1998;

Inchausti 1997). In terms of BA,

Scherch et al. (

2013) and

Silva et al. (

2012) used a disclosure index developed for the Brazilian context according to the disclosure requirements of IAS 41. That particular index is comprised of three main categories namely: mandatory disclosures; non-mandatory but recommended disclosures; and non-mandatory disclosures that are not recommended. The first and the second classifications cover all disclosure items required by the IAS 41, whereas the third category represents voluntary information which is only relevant to companies that measure their BA based on FV. However,

Lopes and Rodrigues (

2007) note that the disclosure index is unweighted and in their study, was adjusted for non-applicable items. Additionally, the use of an adjusted index regarding the disclosure level disregards the influence of the measurement method of BA on number of items in the index that each company can disclose.

Moreover, the index used in previous studies does not reflect the current update to IAS 41 made in 2014, nor other annual amendments.

To overcome this issue and the one pertaining to missing data, companies were classified according to their measurement methods as indicated in the questionnaire. As shown in

Table 1, the questions regarding classification in the questionnaire are linked to specific items within the disclosure index (e.g., Question 9 about government grant in the questionnaire is linked with items 35–37 about government grant in the disclosure index) in order to specify the number of items that can be disclosed by the pertinent company as this number is used to compute each company’s item index.

The disclosure index consisted of three questions and 37 items. The items concerning the disclosure practices were divided into two categories, namely mandatory and voluntary. Unlike in the previous disclosure index where voluntary items were only associated with the FV method, in this disclosure index some voluntary items were related to both the FV and cost methods.

Furthermore, the disclosure index in the current study contained amendments to the index used in previous research by for example,

Scherch et al. (

2013), and

Silva et al. (

2012), to reflect the current update made on IAS 41 and to suit the particularity of the context in terms of the regulation and nature of companies. The amendments made to the previous disclosure index are illustrated in

Appendix B. Therefore, this study mainly referred to the IAS 41 to develop and update the disclosure indices used by previous studies.

The details of the three questions related to company characteristics as well as the 37 disclosure items are shown in

Table 2.

The entire disclosure level was computed by aggregating the score of all disclosed items, giving a score of 1 to an item if it was disclosed, and a score of 0 if it was not disclosed. Accordingly, the total score of the disclosure index is:

where

di equals 1 if the item is disclosed or 0 if the items is not disclosed;

n is the number of items that a firm can disclose. The questions in the questionnaire pertaining to classifications are used to determine the (

n) for each company, thereby enhancing the adequacy of results. Measurement practices is measured according to measurement method, where it equals 1 if the company measure its BA based on FV and 0 if it is based on the cost method.

4. Empirical Results

After applying the eligibility criteria related to IAS 41 paragraphs 1, 5, 10, 12, and 30, that specified the companies that must be excluded from the adoption of IAS 41, a total of 17 companies were excluded, as the BA of 15 companies were bearer plants. These bearer plants are used in the production or supply of agricultural produce, produced for more than one period, or likely to be sold as agricultural produce. Five companies out of the 17 did not control their BA.

Given that some companies reported more than discarding issue related to questions from 1 to 5. The eventual population was 259 companies. That was entirely targeted in this study for collecting data via index.

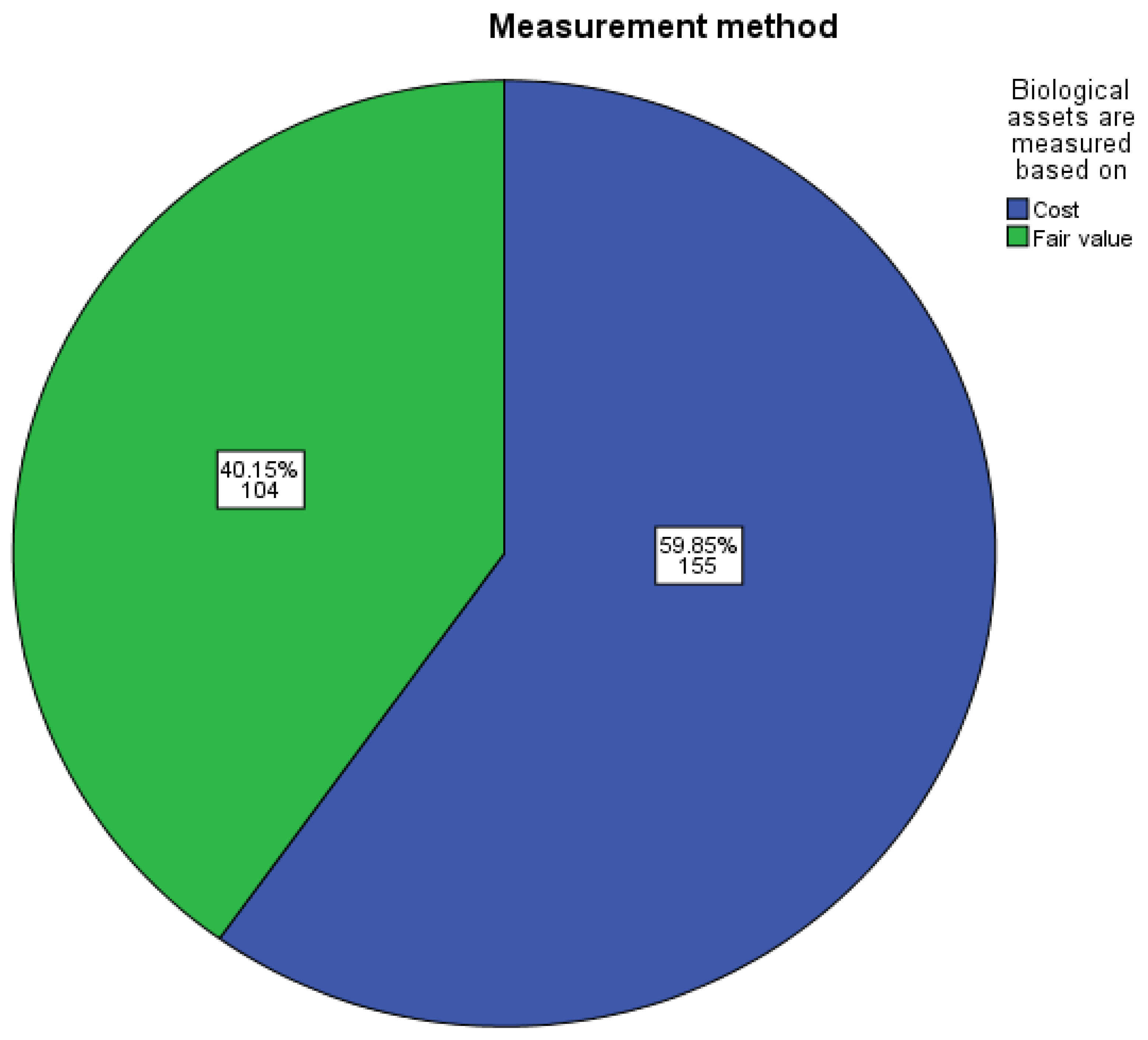

Figure 2 shows the number and percentage of companies according to their measurement method. Approximately 60% (155 companies) used the cost method to account their BA, while the rest (104 companies) relied upon the FV method.

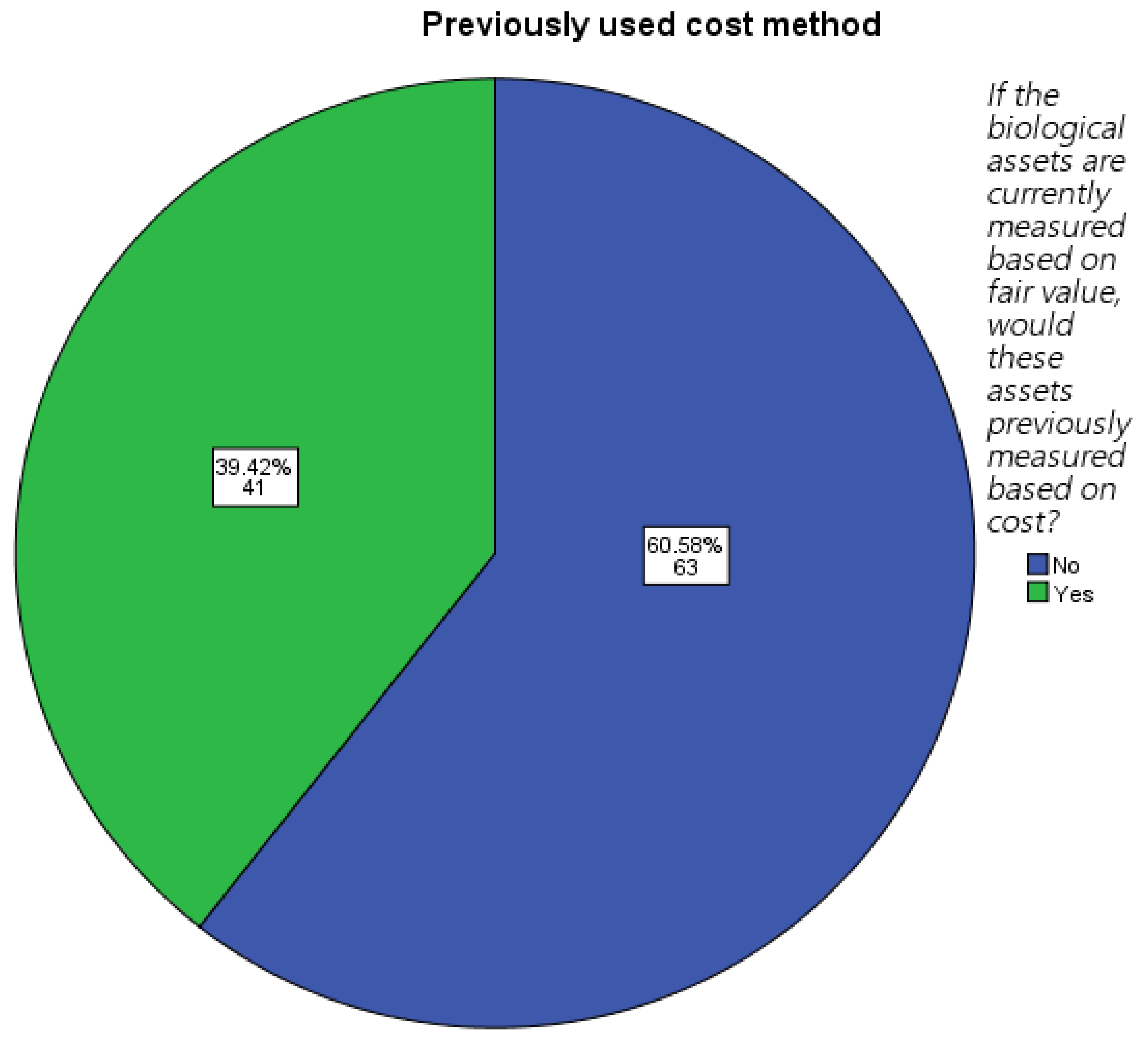

Only 39.4% (41) of companies that used FV (104 companies) for measuring their BA had previously used the cost method. The remaining 63 companies had adopted the FV approach since their commencement date of operations as illustrated in

Figure 3.

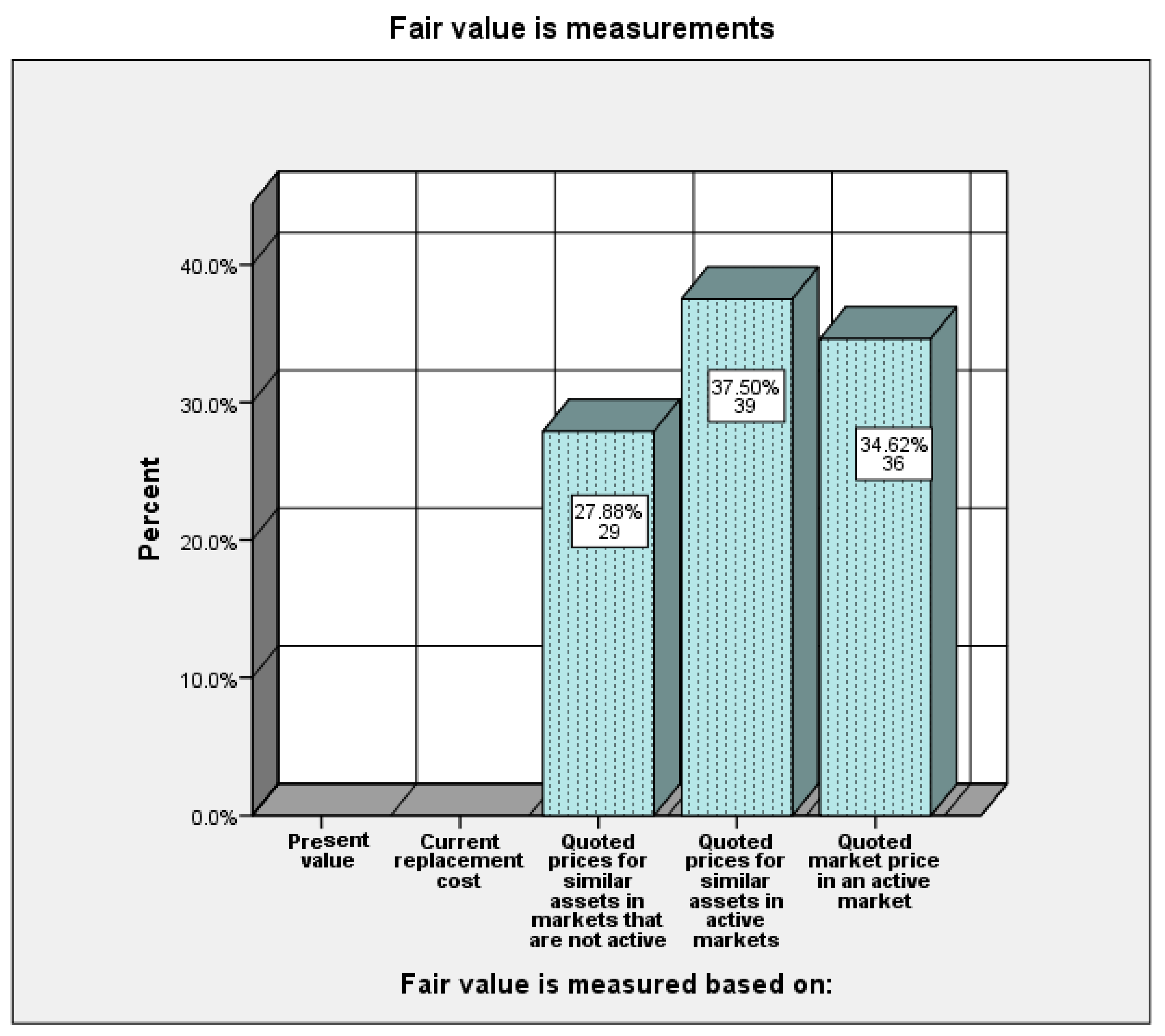

When companies were classified as using FV as their method for measuring their BA, it was seen (

Figure 4) that the present value and replacement cost methods were not used in computing the FV. While almost 35% (36 companies) used quoted prices for their BA in the active market, the remainder used the quoted prices for similar assets in either an active or non-active market because of the diversity of BA possessed by them. Quoted prices for similar assets in an active market was the most used method whilst quoted prices for similar assets in a non-active market was the least used method.

Table 3 present the cross-tabulated frequencies between the level of international activities and audit for the Big Four. The vast majority of the sampled companies (77.2%) did not audit their financial reports using one of the Big Four accounting firms. Approximately 31% of companies have a good or high level of international activities, while the rest have either a poor level or no international activities at all (30.1% and 38.6%, respectively). Importantly, it is obvious that the number of companies whose financial reports were audited by one of the Big Four increases with the level of international activities. As demonstrated, only three companies of the 100 that had no international activities used a Big Four auditor, whereas the pattern reverses in terms of companies that report a high level of international activities, with 20 out of 31 companies reporting using a Big Four firm.

Table 4 shows some descriptive statistics regarding the intensity of BA and total assets. The mean scores indicate that the percent of BA to total assets is approximately 33% (993238.88/2974073.33). However, by reviewing the data set, the percentages of BA to total assets are seen to vary across size clusters, legal form and sector type.

The descriptive analysis presented in

Table 5 reveals the overall disclosure level and mandatory disclosure level to be relatively low within Jordanian companies, these being 34.17% and 39.47%, respectively. One reason might be that some companies do not enjoy limited liabilities (limited partnership and partnership) and are therefore not mandated to provide that information, whereas those with limited liabilities (limited private company, corporation, and limited liabilities companies) are obligated to do so by the Jordanian Securities Commission rules. Overall, the voluntary disclosure level was very low because Jordan does not have any institutional body requiring such disclosure. As aforementioned, 40.15% of companies use the FV measure.

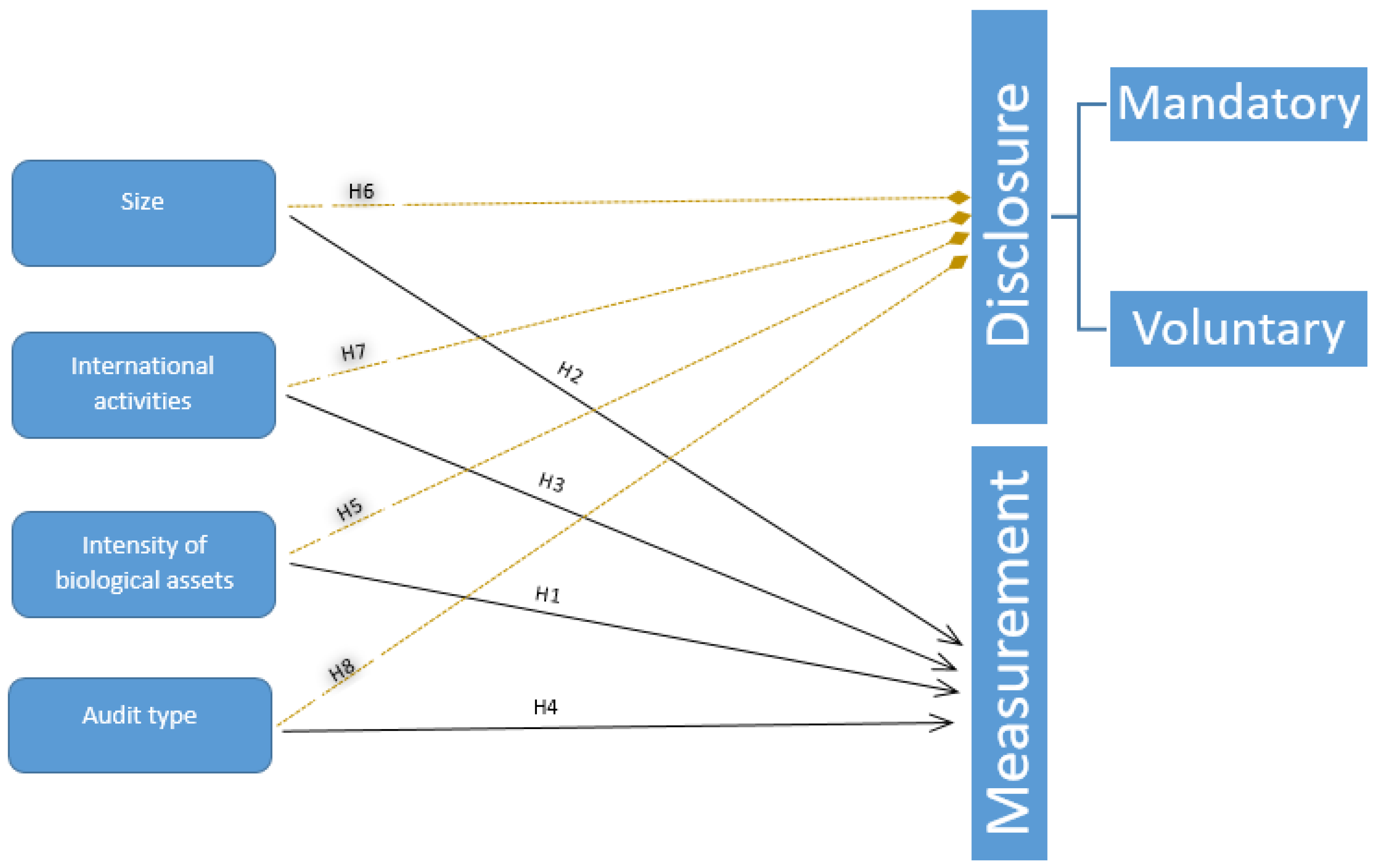

Multiple regression is not appropriate when the outcome variable is categorical. Therefore, logistic regression is used to test the impact of firms’ characteristics on measurement practices (H1 to H4) as the dependent variable is categorical, where the predictor can be categorical or continuous.

Testing the impact of firms’ characteristics on disclosure level (H5 to H8) is performed by multiple regression as the independent variable is ratio. Given that two separate models were estimated for testing this impact, one for the companies that use FV to measure their BA and another for the companies that use the cost method.

With reference to

Tabachnick and Fidell (

1996), the problem of multicollinearity between the variables arises for correlation coefficients more than 90%. For other researchers such as

Gujarati (

1995), the correlations must not exceed 80% in order to avoid the multicollinearity problem. As illustrated in

Table 6, the maximum correlation coefficient was 0.570, between audit for the Big Four and firm size, which indicates that the multicollinearity issue is not presented in the current study. The VIF and the tolerance are also tested and explained throughout regression analysis to ensure the absence of the multicollinearity problem.

The regression results of model (1) are shown in

Table 7 and

Table 8, and explained below.

Logistic regression was executed to assess the impact of firms’ characteristics on measurement practice. The model consisted of four independent variables (level of international activities, intensity of Bay, firm size, and audit for the Big Four). As shown in

Table 7, this model was statistically significant (Omnibus test) χ

2 (4, N = 259) = 133.188,

p < 0.001, demonstrating that the model is able to distinct firms that measured their BA based on FV from those measured based on the cost method. The model explained between 47.1% (Cox and Snell R square) and 62.3% (Nagelkerke R squared) of the variance in measurement methods.

Regarding the Hosmer–Lemeshow Goodness of Fit,

Table 7 showed that the significance value was more than 0.05, which supports this model, where the chi-square value was 11.354, with a significance level of 0.182.

As exhibited in

Table 8, only two of the independent variables made a unique statistically significant contribution to the model (level of international activities, and intensity of BA). The strongest predictor of reporting a FV was the level of international activities with an odds ratio of 5.256. This indicated that firms with a higher level of international activities were 5.256-fold more likely to measure their BA based on FV.

The regression results of model (2) are shown in

Table 9 and

Table 10 and explained below.

Based on the R square score presented in

Table 9, the model (which includes intensity of BA, size, international activities, and audit for the Big Four) explains 33.7% of the variance in overall disclosure level. ANOVA findings indicate that the model was statistically significant: F (4, 254) = 32.257,

p < 0.01.

Table 10 demonstrates that the Sig. values were less than 0.05 for both the international activities and audit for the Big Four variables, thereby indicating that these two variables make a significant contribution to the prediction of overall disclosure level, as they positively influence (due to beta signs) overall disclosure. On the contrary, the intensity of BA and size variables have Sig. values exceeding 0.05, demonstrating no significant impact on overall disclosure level made by either the intensity of BA or size variables.

The highest standardized coefficient of beta score was 0.463, which was for the audit for the Big Four variable. Therefore, audit for the Big Four makes the strongest contribution to explaining the overall disclosure level, thus implying that maximizing the scores of the audit for the Big Four variable by one standard deviation will result in increasing the overall disclosure level by 0.463 standard deviation units. The international activities variable also makes a statistically significant contribution (beta = 0.131).

The VIF values for all variables are less than 10, and the tolerance values exceed 0.10, indicating an absence of multicollinearity.

As illustrated in

Table 11, the null hypothesis of homoscedasticity or constant variance is accepted because the

p-value was more than 0.05 for the Breusch–Pagan/Cook–Weisberg test. This implied that there is no evidence of heteroscedasticity problem.

As mentioned above, two separate models were estimated to test the influence of firms’ characteristics on disclosure level, one for the companies that use FV and another for the companies that use cost.

The main reason for estimating these two separate models is that the results of the Chow test, F (5, 249) = 15.32,

p < 0.01, as illustrated in

Table 12, indicated that the behavior in terms of the impact on disclosure level, was differed between companies that measured its BA based on FV and those measured BA based on the cost method. Therefore, the conclusion regarding the effect of companies’ characteristics on disclosure level based on IAS 41 can be drawn from the results of model (2a) (for companies’ measured BA based on FV) and model (2b) (for companies’ measured’ BA based on the cost method) instead of relying upon the results of model (2) (for companies’ measured BA by any measurement method).

The regression results of models (2a) and (2b) are shown in

Table 13 and

Table 14 and explained below.

Based on the R square score presented in

Table 13 for model (2a) (for firms measured BA based on FV), this explains 42.4% of the variance in overall disclosure level. ANOVA findings indicate that the model (2a) was statistically significant: F (4, 99) = 18.211,

p < 0.01.

The R square score of model (2b) (for firms measured BA based on the cost method), which also includes intensity of BA, size, international activities, and audit for the Big Four, explains 52.7% of the variance in overall disclosure level. ANOVA findings indicate that model (2b) was statistically significant: F (4, 150) = 41.860, p < 0.01.

Model (2a) in

Table 14 reveals that the Sig. values were less than 0.05 for audit for the Big Four and the level of international activities variables, thereby showing that these variables make a significant contribution to the prediction of overall disclosure level for companies measuring their BA based on FV, as they positively influence (due to beta signs) overall disclosure. The highest standardized coefficient of beta score in model (2a) was 0.563, which was for audit for the Big Four. This implies that maximizing the scores of the audit for the Big Four variable by one standard deviation will result in increasing the overall disclosure level by 0.563 standard deviation units. On the contrary, the intensity of BA and size variables have Sig. values exceeding 0.05, demonstrating no significant impact of these variables on overall disclosure level.

Model (2b) in

Table 14 demonstrates that the Sig. values were less than 0.05 for all variables except firm size, thereby indicating that these variables make a significant contribution to the prediction of overall disclosure level for the companies that measured their BA based on the cost method, as they positively influence (due to beta signs) overall disclosure.

The highest standardized coefficient of beta score in model (2b) was 0.410, which was for audit for the Big Four. Therefore, the latter variable makes the strongest contribution to explaining the overall disclosure level for the companies that measured their BA based on the cost method, thus implying that maximizing the scores of the audit for the Big Four variable by one standard deviation will result in increasing the overall disclosure level by 0.410 standard deviation units. This is followed by the level of international activities and then the intensity of BA, which also make a statistically significant contribution to predict the overall disclosure level.

Although the results regarding the variables affecting overall disclosure level for the companies that measured their BA by any measurement method model (2) were similar to those that measured their BA based on the FV model (2a), the results differed from those that measured their BA based on the cost method model (2b). Regarding the rank of variables that contribute in explaining the overall disclosure level, the audit for the Big Four variable has the strongest contribution to explaining the overall disclosure level for the two models (2a) and (2b), followed by the level of international activities variable. The intensity of the BA variable contributes significantly only in predicting the overall disclosure for companies that measure their BA based on the cost method model (2b), given that its influence was less than both the audit for the Big Four and level of international activities variables as demonstrated by the standardized coefficient of beta score.

5. Discussion

This study aimed to examine the impact of firms’ characteristics on measurement and disclosure practices pertaining to biological assets based on the requirement prescribed by IAS 41 in the context of Jordanian companies that have agricultural activities. This study is mainly distinct from previous studies as it used the developed disclosure index to reflect the most updated amendments made in IAS 41 by the IASB, especially those conducted after 2014 as aforementioned. Further, this study investigated the measurement and disclosure practices related to agricultural activities and primarily to BA rather than other non-financial assets as most studies did. Furthermore, the adjusted index in the current study overcame the issue regarding the influence of the measurement method of BA on the number of items that the company can disclosed as already explained.

The findings of this study reveal that the intensity of BA has positive impact on measurement practices as indicated by the results of H1 that was accepted. The findings were alligned with those of other studies (e.g.,

Rahman and Hossain 2020;

Christensen and Nikolaev 2013;

Hlaing and Pourjalali 2012) that found an influence coming from non-financial asset intensity on the adoption of FV. This can be traced back to the fact that the companies would be encouraged to use the FV to measure their BA that represent a significant amount of total assets, as FV provides all stakeholders with more relevant information about the market value of BA compared to the cost method. Particularly, BA is subject to change in value at a rate higher than other assets due to their nature.

However, the intensity of BA has no impact on the level of disclosure for companies that measure its BA based on the FV model (2a) that resulted in rejecting H5 based on model (2a). This finding contradicts those of other researchers (e.g.,

Scherch et al. 2013;

Gonçalves and Lopes 2015). This can be justified based on the fact that the adoption of FV may impose further cost. Or reduce the relevance, as

Filho et al. (

2013) observed that most Brazilian companies operating in the agriculture-food sector that measure their biological assets using the fair value approach, do not disclose the method adopted when computing the fair value. This also justified by the results of model (2b), that indicated a positive impact on the level of disclosure for firms measuring their BA based on the cost method, which implied accepting the H5 based on the results of model (2b). To sum up the disclosure level was influenced by firms’ characteristics that used the cost method for measuring BA due to the simple calculation of BA cost in comparison to the complexity related to measuring BA based on FV that may imply further cost pertaining to measure FV reliably and reduce the relevance (

Filho et al. 2013).

Moreover, to the best of the researcher’s knowledge, there has been limited attention toward the influence of intensity of BA on FV adoption since the amendment made to IAS 41 in 2014 regarding measurement requirements. Previous studies (e.g.,

Rahman and Hossain 2020;

Christensen and Nikolaev 2013;

Hlaing and Pourjalali 2012) tested the impact of non-financial asset intensity, whereas the current study has examined the impact of BA intensity. Therefore, various findings could be raised.

H2 and H6 relating to the positive impact of firm size on measurement practice and disclosure level were rejected. The results with respect to the influence on disclosure level were not in agreement with those achieved by other scholars such as

Haddad et al. (

2020) and

Gonçalves and Lopes (

2015). This can be traced back to the fact that the target group includes listed and non-listed entities whose disclosure practices vary according to company law and Jordanian Securities Commission requirements. This may also be the reason for the difference in findings between the current and previous studies in terms of the influence on measurement practices. The trend of small businesses in terms of their use of FV is not constant because they are cautious about the high costs associated with the approach, but they do appreciate that its use may help to decrease information asymmetry (

Daniel et al. 2010). However, large firms report higher agency costs (

Jensen and Meckling 1976), and

“have both the available resources and necessary incentives to comply with accounting standards” (

Cairns et al. 2011, p. 7). The findings were not consistent with those of

Quagli and Avallone (

2010) and

Rahman and Hossain (

2020), who tested the influnce of firm size on the revaluation decision. Moreover, most earlier studies tested the impact of firm size on the revaluation decision or using FV for non-finnancial assets rather than to measure BA as has been performed in the current study.

With respect to the level of international activities, H3 and H7 were accepted, confirming the positive impact of the level of international activities on measurement practices model (1) as well as on the level of disclosure models (2a) and (2b). Additionally, here, the results concurred with those of

Daniel et al. (

2010) and

Taplin et al. (

2014) concerning measurment practices. Likewise, the results were aligned with those of

Daske et al. (

2013). The reason for these outcomes is their association with the idea that companies are assisted in their efforts to convey their international position to stakeholders (

Oliveira et al. 2006).

With regard to audit for the Big Four, H4 was rejected, thereby confirming the absence of impact of audit for the Big Four on measurement practices. This can be justified based on the existence of several challenges as highlighted by

Nordlund et al. (

2022),

Alqatamin and Ezeani (

2020), and

Oyewo et al. (

2020) relating to the risk of management bias, the difficulties faced by auditors in investigating the estimates of measured fair value, and increasing audit fees.

On the other hand, the findings of the current study show that audit for the Big Four positively impacts the overall disclosure level and makes the strongest contribution to explaining the overall disclosure level for all models (2a) and (2b), agreeing with previous researchers (e.g.,

Glaum et al. 2013;

Hodgdon et al. 2009). The quality of the audit work and the value relevance of accounting information are positively related to the size of the audit firm (

DeAngelo 1981;

Abdollahi et al. 2020). This is in addition to minimizing the agency cost by having the financial report audited by independent auditors (

Jensen and Meckling 1976), leading to reduced information asymmetry.

6. Conclusions

The aim of this study is to describe the accounting practices of the agricultural activities of Jordanian firms based on those firms’ characteristics, and was conducted in light of IAS 41 in terms of financial disclosure and measurement.

The findings revealed that both intensity of BA and level of international activities have a positive impact on measurement practices, where the contribution of the level of international activities variable better explained measurement practices compared to the intensity of BA variable. Audit for the Big Four was the strongest variable that positively influenced the overall disclosure level prescribed by IAS 41, followed by the level of international activities. The intensity of the BA variable affects only the overall disclosure level for companies that measure their BA based on the cost method model (2b). Firm size was found to have no influence on either measurement practices or disclosure level.

The results of this article may have theoretical and practical implications. This study provided new insights into the influence of firms’ characteristics on measurement and disclosure practices for companies that include agricultural activities—particularly in the context of developing countries, such as Jordan. This contributed to the body of literature concerning either accounting standards related to agricultural activities in general or biological assets in particular.

The current study contributed to the literature of financial reporting by examining the influence of firms’ characteristics on measurement and disclosure practices, where the previous studies essentially tested the impact of agricultural firms on disclosure level with evident absence of measurement practice. However, other previous studies investigated the impact on either measurement or disclosure that was related to non-financial assets rather than BA.

In terms of methodological contribution, the problems pertaining to the disclosure indices used in previous studies regarding disregarding the influence of the measurement method of BA on the number of items in the index that each company can disclose was overcome. This was overcome by using the question in the questionnaire pertaining to measurement of BA based on FV or cost in order to determine the number of items that each company can disclose, thereby enhancing the adequacy of results, given that two separate models were estimated to test the influence of firms’ characteristics on disclosure level, one for the companies that use FV and another for the companies that use cost, which also enriches the findings and enhances accuracy.

Moreover, the index used in previous studies does not reflect the current update to IAS 41 made in 2014, nor other annual amendments. The index of current studies relied mainly upon IAS 41 and reflected the most updated items.

The items concerning the disclosure practices were divided into two categories, namely mandatory and voluntary. Unlike in the previous disclosure index, where voluntary items were only associated with the FV method, some voluntary items were related to both the FV and cost methods in this disclosure index.

Furthermore, the disclosure index in the current study contained amendments to the index used in previous research by, for example,

Scherch et al. (

2013) and

Silva et al. (

2012), to reflect the current update made on IAS 41 and to suit the particularity of the context in terms of the regulation and nature of companies. The amendments made to the previous disclosure index are illustrated in

Appendix B. Therefore, this study mainly referred to IAS 41 to develop and update the disclosure indices used by previous studies.

Equally important, numerous practical implications can be directed toward management, standards setters and other stakeholders especially in developing countries. This study helps standards setters and regulators to understand the determinants of measurement and disclosure practices based on companies’ characteristics within the context of Jordan, which in turn facilitates amending and directing financial regulation according to these determinants. This eventually promotes the accounting practices related to agricultural activities. To enhance this, establishment of an institutional structure is necessary to simplify and support the valuation of BA measured based on fair value. This would enhance comparability, reduce implicit costs as well as avoid the additional audit fees, eliminate or at least mitigate arbitrary discretionality and the difficulty of computing fair values, reduce agency cost as well as information asymmetry, and increase firms’ ability to access the international market.

Investigating the measurement and disclosure practices based on firms’ characteristics assists in determining the companies (based on tested characteristics) that need more support to overcome the problem pertaining to the low level of disclosure or undesirable measurement practices. In particular, proper measurement practice and a high level of disclosure enhance the relevance of accounting information that increase the value relevance and reduce the information asymmetry and eventually decrease agency cost.

Furthermore, the findings pointed out that the measurement practice was influenced by international activities and the intensity of BA variable, while disclosure practice was mainly influenced by international activities and audit for the Big Four of firms. This implied that the auditors who do not belong to a Big Four firm must rely on audit procedures and plans conducted by the Big Four companies. This might result in enhancing the ability of firms (that are audited by non-Big Four firms) to increase the disclosure level to provide more relevant information to stakeholders. The results of this study also provided indicators to both standards setters and responsible bodies for the purpose of inspecting the reasons behind the low level of disclosure for firms with a lower level of international activities and lower intensity of BA, in addition to their use of the cost model instead of FV to measure BA.

Future research might be needed in terms of testing the impact of other structured characteristics of companies such as legal form or listing status and sector, on mandatory and voluntary disclosure. Conducting comparative studies in the context of developing countries to examine the influence of the aforementioned determinants, owing to the availability of data, the latter investigation might only include the listed companies from several countries, in order to widen the generalizability of finding. In addition, discovering the reasons behind the low level of disclosure and using the cost model for valuing BA is deemed a worthwhile mission.

{kind=link}

{kind=link}

{kind=link}

{kind=link}