1. Introduction

The term “lean” originated from the Toyota production system and was introduced by

Krafcik (

1988).

Womack et al. (

2007) catalyzed the lean revolution. According to

Mize et al. (

2000), lean is not just a set of rules commonly seen in factory workshops, but a fundamental change in how people in the organization think and evaluate, thereby changing their behavior.

Shah and Ward (

2003) defined lean as a method to provide the highest value to customers by eliminating waste through process design and human factors. Lean manufacturing aims to eliminate waste in all areas of production, including customer relations, product design, supplier networks, and plant management. Its goal is to combine less human effort, less inventory, less time to develop products, and less space to meet high customer demand while producing top-quality products in the most economical and efficient manner possible (

Mize et al. 2000). Today, lean is a global trend applied to all industries and fields. Lean is no longer confined to the production environment but has expanded to include management and accounting environments.

Indeed, when businesses implement lean strategies, their needs change. They require information about the financial impact of lean improvements, a better way to understand product costs, new ways to measure effectiveness, elimination of waste from accounting processes and systems, and better decision-making focused on customer value (

Maskell et al. 2011). Thus, when businesses shift from mass production to lean production, the accounting system needs to change. Production cannot be sustained without significant changes to the accounting system.

According to

Maskell et al. (

2011), lean accounting has the following characteristics: lean accounting focuses on managing the business around value streams. All cost and financial decisions are made at the value stream level; the lean accounting method is designed to promote continuous, relentless improvement of the value stream; lean accounting eliminates most waste from the control system by integrating control into operational processes. Eliminating the need for wasteful transactions, reports, and meetings leads to the use of simple, understandable reporting and cost methods; and lean accounting applies the principles of lean strategies to accounting processes themselves.

Lean accounting has two main objectives: (1) eliminating waste in production and accounting while freeing up space and simplifying the process as much as possible so that everyone in the business can understand it, not just the accountants. (2) It also strives to fundamentally change the accounting environment to provide relevant information to both customers and employees to support decision-making, allowing all employees to influence positive changes in the business.

Lean accounting aims to create conditions for the necessary changes in the organization to implement lean thinking (

Ofileanu and Topor 2014) and provide a stage for the accounting team to transition from a traditional system to a new high-value advisory role in different areas of the company (

Cunningham et al. 2003). Lean accounting does not require traditional management accounting methods, such as standard costing, variance reporting, complex transaction control systems, and untimely and confusing financial reports, but rather applies a value-based approach (

Rao and Bargerstock 2011). The tools of lean accounting are not entirely new and include value stream; Kaizen, PDCA, box score, value stream costing, target costing, financial reporting in simple language, visual management, and 5S; sales, operations, and financial planning; etc. (

Brosnahan 2008;

Maskell and Baggaley 2006;

Maskell et al. 2011).

Merwe and Thomson (

2007) pointed out three main limitations of lean accounting. First, lean accounting considers absorption standard costing adequate, and all other traditional approaches have the same flaws. The second is that blended cost concept error results in poorer decision support because lean accounting refuses to model operations, whereas operational modeling is essential for decision support because understanding existing causal relationships provides insight into the potential outcomes of decision alternatives. Third, lean accounting strongly implies it has the ability to transform traditional financial accounting just as it desires to transform management accounting. However, the authors’ assessment is that the meaningful support of lean accounting in the field of financial accounting is inventory valuation. From there, the authors conclude that lean accounting needs more technical insight and depth into how it supports operational decision-making, strategic planning, and external reporting. Lean accounting also does not support the decision-making process, and business optimization extends beyond the shop floor.

Since 1996, the Vietnamese government has shown special interest in improving productivity and product quality. The national program “Improving productivity and product quality of Vietnam’s goods by 2020” and the subsequent “National program to support businesses in improving productivity and product quality of goods in the period 2021–2030” are major turning points in promoting the application of various improvement systems, models, and tools to enhance productivity and quality nationwide. These programs have attracted the participation of thousands of businesses from various industries with various scales and have achieved significant achievements. Businesses have become familiar with some management systems and improvement tools, including lean management.

The textile and garment industry is one of the most important economic sectors, with export turnover ranking fourth among economic sectors and contributing 5–7% to Vietnam’s GDP (

VCBS 2022). Vietnam is also among the top five garment exporters in the world. However, with the characteristics of highly fashionable products, it is necessary to regularly change designs, colors, and materials, and in the context of rapidly increasing production costs, inflationary pressure, constantly rising living costs, the fact that the advantage of cheap labor is decreasing, labor productivity is low. More than ever, Vietnamese garment enterprises are forced to improve management, search and apply technology to increase labor productivity, and maintain good competitiveness to ensure stable and sustainable development. Since the characteristics of operation are mainly processing according to orders, products are produced according to customer requirements; with diverse products, the number of products of each small order, and orders changing constantly, Vietnamese garment enterprises are considered one of the types of businesses that are very suitable for lean production. Therefore, since 2006, lean production has been applied to some garment enterprises, first of all in production activities. Some enterprises have successfully applied lean production, such as Nha Be Garment Corporation. After applying lean production, the working time has been significantly reduced, workers do not have to work overtime, the average income increases by 10%, the wages of workers between lines are more uniform, the backlog in working positions is less, and so industrial hygiene is better and it takes less time to clean. In addition, Garment Corporation 10, after applying lean production, saw labor productivity increase by 52%, the defect rate decrease by 8%, working time decrease by 1 h/day, income increase by 10%, and production costs decrease from 5–10%/year (

Le 2015). Thus, the research of lean accounting in textile firms in Vietnam is necessary.

This study is structured as follows.

Section 2 reviews the studies of lean accounting and hypothesis development.

Section 3 describes the data sample collection and methodology employed in the conduct of the research.

Section 4 sets out a discussion of key results while

Section 5 shows some key conclusions and implications of the study practice and recommendations. From the synthesis of previous studies in

Section 2, we built 8 hypotheses with the research model, used Cronbach’s Alpha (CR) test method and exploratory factor analysis (EFA) for independent and dependent variables with Pearson correlation analysis, Multivariate regression analysis, and a residual analysis with SPSS software to perform testing in

Section 3. The results in

Section 4 show that all 8 factors representing 27 observed variables have a favorable influence on the application of lean accounting in Vietnamese garment enterprises. The level of influence of the factors is different and arranged in descending order as follows: leadership, size, cost of implementation, accounting department, education and training, resources, competitiveness, and competitive pressure. With the above results,

Section 5 offers solutions for businesses in general and textile enterprises, in particular to have appropriate and effective strategies to apply lean accounting to ensure business development and sustainability.

2. The Literature Review

Maskell was the first to mention the term lean accounting, stating that “lean accounting aims to provide useful information to those who are making and maintaining lean production” (

Maskell 2000). In 2005, Maskell stated that it was the generic term used for changes required in a company’s accounting, control, measurement, and management processes to support lean manufacturing and lean thinking. It supports a lean culture by fostering investment in people, providing appropriate and actionable information, and empowering continuous improvement at every level of the organization (

Arora and Soral 2017).

Brosnahan (

2008) argues that lean accounting is a new accounting method stemming from the growing interest of organizations in embracing the culture of lean thinking. It is applied in organizations implementing lean thinking (

Ofileanu and Topor 2014;

Pham 2011) to support lean manufacturing and lean thinking (

Maskell and Kennedy 2007).

Nguyen (

2020) argues that lean accounting is the application of lean thinking to all financial and accounting processes and systems of the business.

Achanga et al. (

2006), after studying 10 small and medium enterprises based in the East of England, pointed out four main factors affecting the implementation of lean production, including leadership and management, finance, skills and expertise, and the culture of the organization. Leadership and management commitment are the most important factors in determining the success of a lean project.

Nguyen et al. (

2015), through the study of three lean projects, have divided the important factors determining the successful implementation of lean production in lean manufacturing enterprises in Vietnam. Six aspects of the lean transformation model were presented in the study, including Strategic Initiatives, Process Management, Change Management, Human Resource Management, Situation Management, and External Management. Research has also found that different factors have different effects, but the studies have not evaluated each factor in depth.

Many studies suggest that implementing lean production is not an easy task (

Achanga et al. 2006;

Pirraglia et al. 2009;

Nordin et al. 2010).

Grasso (

2006) divided the barriers to lean accounting into five categories: cultural, organizational, educational, professional, and personal. According to the author, culture is the biggest barrier. For organizational hurdles, a lean transformation of accounting must begin with the integration of accounting into manufacturing operations and have accountants participate in lean production and Kaizen training to avoid the separation of the accounting department from other departments. Educational barriers are accounting training programs that are oriented towards public accounting, financial reporting, and auditing. The lack of lean accounting references is also a factor of educational barriers. The professional hurdles are the professional accounting certifications that contribute to the direction of the educational process focusing on financial accounting and orientation of financial statements. The personal barrier is that accountants can resist change for fear of the unknown. By way of training and self-selection, some accountants may not like risk and change more than others. Accountants have reasons to be apprehensive about a lean switch. They may be afraid of losing influence or stature. As the final hurdle, accounting can have a bias for complexity and detail.

Stenzel (

2007) points out five factors that lead to the implementation of lean accounting failure, namely: people (unwillingness or fear of change, fear of losing jobs, fear of failure of individuals, fear of failure of business, fear of loss of reputation); machinery, materials, and methods (enterprise resource planning systems, independent accounting information systems, mandatory non-financial data are not collected); measures; and environment.

In a quantitative study by

Darabi et al. (

2012), four groups of factors, including cultural, technical, organizational, and economic, are considered barriers to the implementation of lean accounting in factories. Research results have shown that technical factors have the highest obstacles in the implementation of lean accounting in manufacturing companies and the lowest economic factors. Cultural factors include the role of leadership, tactical attitudes, inappropriate reward procedures, resistance of managers, employees, and even customers. The components of the technical barrier in this study include not using lean as a manufacturing strategy, not using general-purpose machinery, not using production systems in a timely manner and without warehouses, and a lack of awareness of lean systems by senior leaders and employees. Meanwhile,

McVay et al. (

2013) only mentioned two barriers. The first is that most people prefer stability and resist change. They are afraid of the unknown, and they are able to cope with what they are used to, even if they know it may not be their best alternative. The second is a lack of knowledge or training on how to make an accounting transition.

Kumar and Kumar (

2014) studied the barriers of lean manufacturing at 47 large and medium-sized manufacturing companies in India. This study looked at companies that are in the process of implementing lean manufacturing or have successfully adopted lean manufacturing systems. The seven main barriers of lean manufacturing deployment include management, resources, knowledge, conflict, employees, finance, and past experience. The results of the study by the average method show the level of resistance of the barriers from low to high as follows: management, knowledge, conflict, finance, employees, resources, and past experience.

Salonitis and Tsinopoulos (

2016) classified barriers into four groups: financial, related to senior management, related to the workforce, and other barriers.

Lodgaard et al. (

2016) studied in-depth case studies at a manufacturing company in Norway for two years on barriers to successful lean implementation. Barriers include management, lean organization, lean tools and practices, and knowledge. Research shows that employees at different levels in a company notice different lean barriers. Top managers attribute limited success to barriers associated with the tool and lean practices. Workers mainly point out the challenges related to management. Middle managers acknowledge there are many barriers but mostly emphasize that roles and responsibilities are not defined and that best practice tools have not been selected.

Nguyen et al. (

2017) focused on identifying critical barriers/difficulties and exploring the source of barriers/difficulties for successful lean implementation at manufacturing companies in Vietnam. The study found seven major barriers to lean implementation success—leaders, employees, workplaces, resources, operational processes, customer relationships, and supplier relationships. Leadership barriers are considered the most important and influential in lean implementation.

From another perspective,

Turesky and Connell (

2010) studied the reasons for the failure to achieve the sustainability of lean manufacturing at a company in northern New England. The authors proposed a four-stage model affecting lean project sustainability: set-up, preparation, implementation, and sustainability. The factors that affect leaning have been considered in stages, and it is assumed that the factors in each stage interact with each other and should not be considered separately. A study of the implementation of lean manufacturing practices in the textile industry found

Shah and Hussain (

2016). The authors used survey methods to collect data from several Pakistani textile companies. Study results show that lean manufacturing practices have a significant relationship with scale. Larger organizations have used more lean manufacturing practices than small and medium-sized organizations. In addition, based on the literature review, ten factors hindering the implementation were identified and included in the questionnaire. Statistics have shown that in noncompliant companies, the four main barriers are employee resistance, lack of communication, company culture, and lack of understanding. On the other hand, companies are transitioning to lean production systems where company culture, employee resistance, lack of communication, and a lack of understanding to implement lean production are key factors. For lean companies, a lack of communication is identified as the main barrier to successful implementation of a lean manufacturing system.

Timm (

2015) investigated factors that influence the adoption of lean accounting in organizations that use lean manufacturing. To add to the understanding of why lean accounting is or is not implemented by lean manufacturers in the United States, the study examined four independent variables—PEOU-I (individual perceived ease of use), PU-I (individual perceived usefulness), PEOU-O (organization perceived ease of use), and PU-O (organization perceived usefulness) and the dependent variable of BI (behavioral intention) management accountants to adopt lean accounting using value-stream costing. The purpose of this study was to examine whether concern about the complexity of value-stream costing or accountants’ perceptions that value-stream costing may not be useful to their organization or to their required job responsibilities may influence their adoption of value-stream costing. In addition, demographic data offered insights into the current state of lean manufacturing and value-stream costing. Therefore, proponents of the use of value-stream costs have foundational information about management accountants’ perceptions of ease of use and usefulness. For both the individual and the organization, value-stream costs have a positive correlation with the intention of implementing value-stream costs. Additionally, PEOU and PU may predict the intention of implementing value-stream costs.

In 2021, Rehman et al. concluded that those factors include a technology gap, fear of unemployment in workers, current status of employees, fear of not knowing, change in reporting structure, skill gap, lack of appropriate communication, fear of people with machines, social disconnect, out-of-scope exposure, fear of managerial change, increasing factors of accountability, unhealthy behavior, the value of unknown technology, unknown ways to use technology, lack of uniformity in technology, technology related to too many paperwork, technology that creates too many jobs, technology abuse, high technology costs, technology that is a threat to personal freedom, technology that is different from what work processes and procedures have been established, the fear that technology will have a negative impact on teamwork and collaboration, bad experience with technology in the past, lack of leadership/support for innovation, level of comfort, the effect of disruption, time to make changes and adjustments, understanding and ability to perform, budget priorities, difficulty/capacity/training time, resistance to learning new technology, stressful/overloaded work, cost, evidence of value, reliability, lack of clear scope, weak motivation to change, lack of money, skepticism in rank, high workforce turnover, little personal empowerment, use of relationships, insufficient knowledge of leanness and inadequate management skills.

Sakataven et al. (

2021) reviewed the literature and found fifteen barriers to lean implementation, and by using the outputs of Interpretive Structural Modelling (ISM) and Impact Matrix Cross-Referencing Multiplication (MICMAC) analyses, the study classified 15 barriers into 10 levels, where “Roles and Responsibilities not defined in Lean Implementation” was at level 1 (the lowest impact level). The most important barriers are “Lack of long-term commitment to change and innovation” and “Personal Attitudes” (level 10). Some levels have many barriers. The study suggests that such classification helps organizations understand the motivating power and dependency of each barrier. This is important because motivation will determine the impact of a successful lean implementation. Barriers should also be addressed along with the consideration of other barriers at the same level.

The relationship between lean governance and green accounting is mentioned by authors

Kuo and Lin (

2020). This study contributes to lean and green management in five ways. First, most of the prior research on green performance has demonstrated how to carry out green operations in a routine job, but few studies have identified the effects of lean management and green operational practices. This paper empirically determines how lean management impacts green operational practices in container terminal operations. Another contribution is that the conceptual framework of this study was formulated based on the literature, and it aims to determine and confirm the effects of lean management, green operational practices, green behavior, and green performance. Third, employees’ green behavior is the key to green performance, and human behavior is also the most difficult factor to control within an organization. The mediating effects of employee green behavior on lean management, green operational practices, and green performance are assessed in this study. Fourth, the relationship between lean management and performance in the context of the manufacturing industry is investigated. Finally, the study results offer useful managerial contributions that can guide terminal operators in establishing an adaptable approach for implementing green practices in container terminals.

Lean accounting or green accounting is a matter of great interest to enterprises in general, in which the successful application of lean accounting in enterprises leads to sustainable development and environmental and social sustainability accounting practice (SAP). In the study of

Oyewo et al. (

2022), the authors also proposed internal management, business strategy, lean accounting quality, and accounting apparatus structure. The results show that the extent to which Nigerian companies have implemented SAP is moderate. The authors find that the level of SAP implementation is significantly associated with market orientation and business strategy but not with the QIT and structure of accounting department. Another study by

Oyewo et al. (

2022) suggests that while the implementation level of SAP by companies is generally moderate, internalities/‘pull factors’ such as market orientation and deliberate strategy formulation significantly determine the sophistication level of SAP. The insignificant effect of the externalities/‘push factors’ (i.e., environmental uncertainty, structure of ownership and control, and intensity of competition) on SAP suggests that external pressure on companies to implement sustainability initiatives is weak.

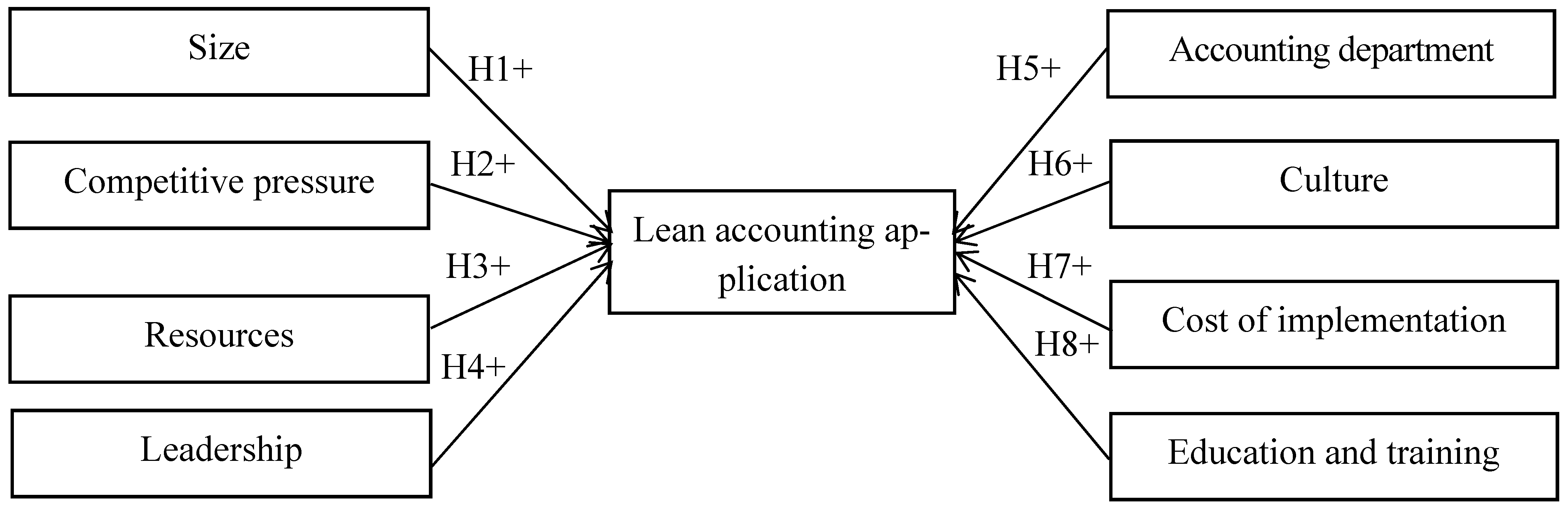

Through the literature review of research works, the study synthesizes factors affecting the application of lean accounting in garment enterprises and builds research models and research hypotheses to survey, analyze, and give results.

4. Results

4.1. Cronbach’s Alpha Test Results of the Scales

The specific results of testing the reliability of Cronbach’s Alpha scales are presented in

Table 1 and

Table 2.

The test results show that all scales have Cronbach’s Alpha coefficient >0.6 and are quite high; the lowest is 0.770, and the highest is 0.941. In addition, the total variable correlation coefficients are >0.3. Therefore, it can be confirmed that the scales of the study are reliable and can be used to analyze the discovery factor in the next step.

4.2. Exploratory Factor Analysis

EFA factor analysis for independent variables. Processing results from SPSS software for independent variables are as follows:

Table 3 shows that KMO = 0.856 > 0.5, so the factor analysis is appropriate. Sig. (Bartlett’s Test) = 0.000 (sig. < 0.05) shows that the observed variables involved in the EFA analysis are correlated.

Table 4 shows that there are 8 factors extracted based on Eigenvalue 1.148 > 1 or 8 factors that summarize the information of 27 observed variables into EFA in the best way. The total variance of these factors extracted is 70.867% > 50%. Thus, the 8 factors cited explained 70.867% of the data variation of 27 observed variables participating in EFA.

The loading factor of the observed variables in the rotation matrix is >0.5 (

Table 5), or these observed variables are all significant contributors to the model.

EFA analysis for the dependent variable. The processing results from the SPSS software for the dependent variable are as follows:

Table 6 shows KMO = 0.937 > 0.5, so the factor analysis is appropriate. Sig. (Bartlett’s Test) = 0.000 (sig. < 0.05) shows that the observed variables involved in the EFA analysis are correlated.

Table 7 shows that there is a factor extracted based on Eigenvalue 6.128 > 1. The extracted variance is 68.094% > 50%.

Table 8 shows that the loading factor of the observed variables in the rotational matrix is >0.5, or these observational variables are all significant contributors to the model.

From the results of exploratory factor analysis of toxic variables and dependent variables, the research has the groups of factors representing the following variables:

Scale Factor—SZ: SZ1, SZ2, SZ3

Competitive Pressure Factor—CP: CP1, CP2, CP3

Resource Factor—RS: RS1, RS2, RS3

Leadership Factor—LD: LD1, LD2, LD3, LD4, LD5

Factor Accounting Department—AD: AD1, AD2, AD3, AD4

Cultural Factors—CT: CT1, CT2, CT3

Implementation Cost Factor—CO: CO1, CO2, CO3

Education and training factors—ET: ET1, ET2, ET3

Factors Applied Lean Accounting—LA: LA1, LA2, LA3, LA4, LA5 LA6, LA7, LA8, LA9

4.3. Correlation Analysis

Pearson correlation analysis was performed to examine the strong linear correlation between the dependent variable (LA) and the independent variables (SZ, CP, RS, LD, AD, CT, CO, and ET) and the early identification of the multicollinearity phenomenon when the independent variables are also strongly correlated with each other.

Regarding the correlation between dependent variables and independent variables, the Pearson correlation analysis table (

Table 9) shows that the correlation coefficients are 1, 0.569, 0.463, 0.554, 0.671, 0.544, 0.480, 0.514, 0.480, or all 8 independent variables in the proposed model are strongly correlated with the dependent variable (

Hoang and Chu 2008).

Regarding the correlation between independent variables,

Table 9 also shows that all sig. between independent variables are less than 0.05 minus sig. between variables CP and ET. However, the Pearson correlation coefficient between independent variables is less than 0.7. Therefore, it is not yet sufficient to conclude between variables that are likely to occur multicollinearity (

Dormann et al. 2013).

4.4. Multivariate Regression Analysis

The processing results from SPSS software are obtained as follows:

Table 10 shows the results of the conformity assessment of the multivariate regression model. R = 0.873 indicates a high degree of correlation. Adjusted R Square correction = 0.754 indicates that the independent variables included in the regression analysis explain 75.4% fluctuations of the dependent variable; the remaining 24.6% is due to variables outside the model and random error. This result also indicates the statistical value of the Durbin–Watson test = 2.19 ≈ 2, which is between 1 and 3, so the result does not violate the first-order self-correlation assumption (

Field 2009).

The ANOVA analysis (

Table 11) indicates the relevance of the regression equation to the data. The test results show that F = 56.856, sig. = 0.000 < 0.05 and prove that R square is non-zero overall. This means that the linear build regression model is suitable.

Correlation coefficient analysis (

Table 12) shows that the value of sig. of all variables is <0.05, or these variables are statistically significant and all affect the dependent variable. All eight theories are accepted. Regression coefficients (B and β) in all 8 independent variables are positive, meaning that all 8 independent variables have a positive effect on the dependent variable.

In addition, VIF variance magnification coefficients of all independent variables in the model were <2, indicating that the data did not violate the multicollinearity assumption or that multicollinearity between independent variables occurred (

Hair et al. 2009).

4.5. Analysis of Residuals

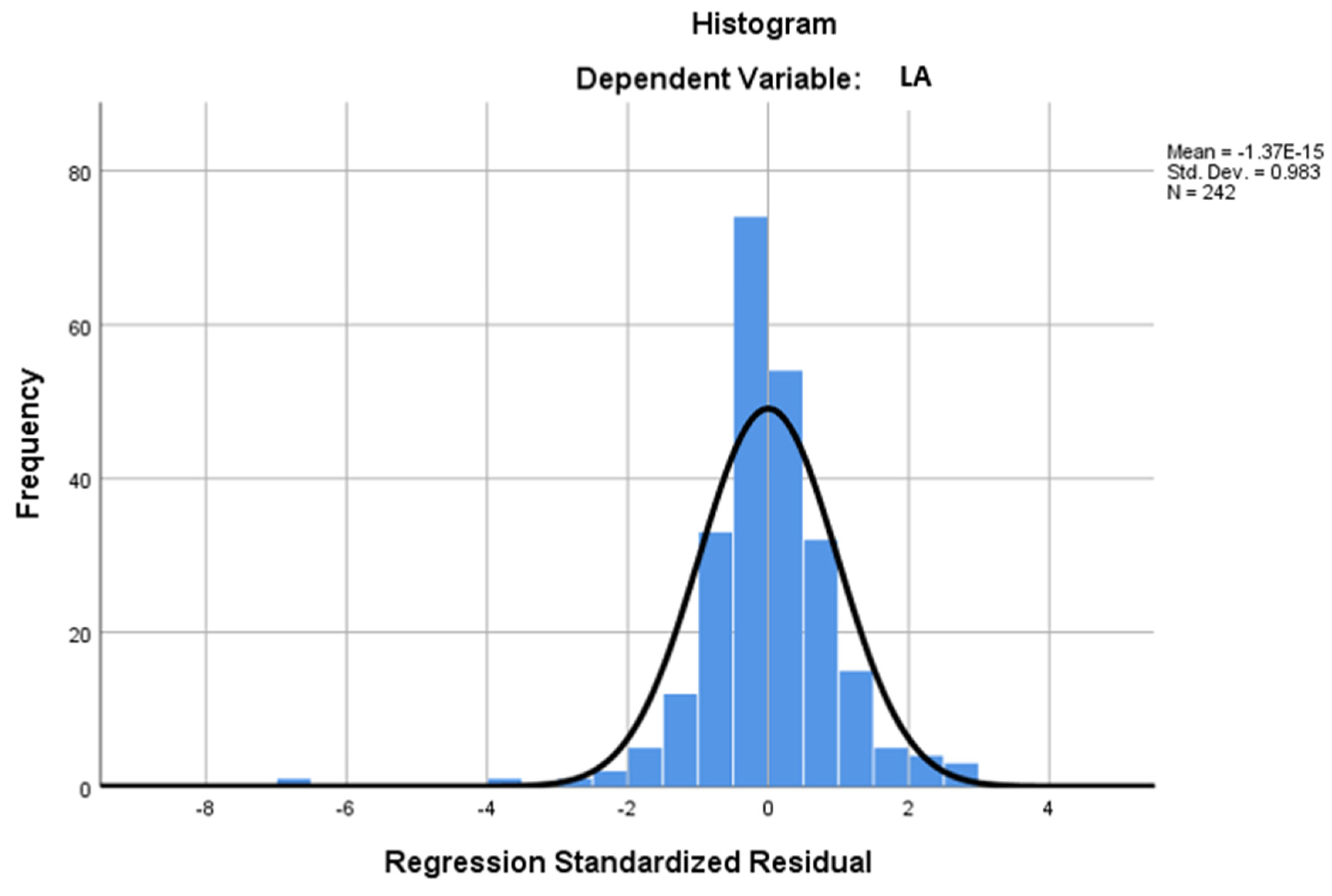

Regarding the test of the standard distribution assumption, looking at

Figure 2, it could be seen that the normalized residue is distributed according to the bell curve, or the shape of the standard distribution. In addition, the mean is 1.37 × 10

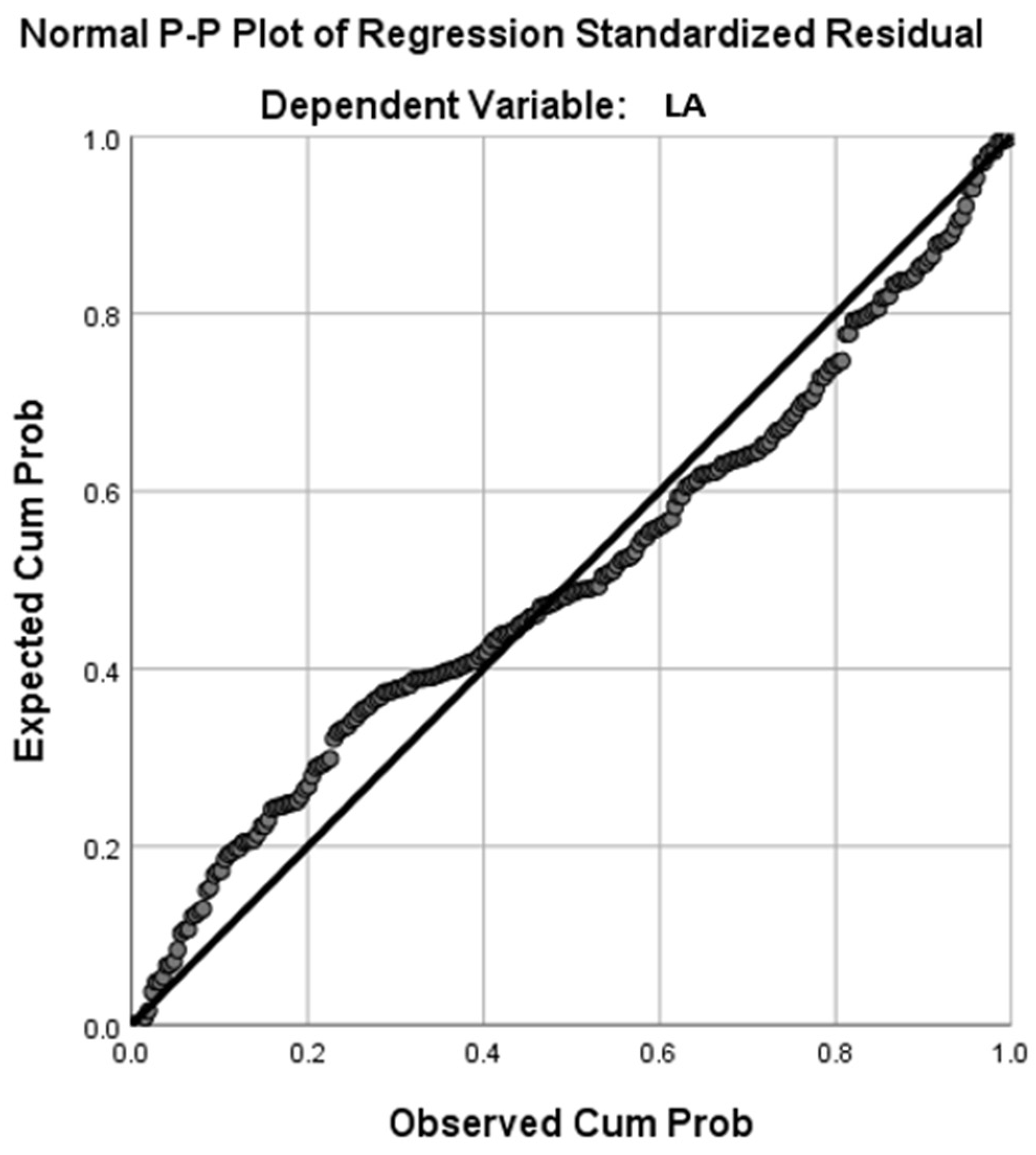

−15 (approximately = 0), and the standard deviation is 0.983 (approximately = 1). In addition, the Normal P-P Plot (

Figure 3) shows that the observed values and expected values are all around the diagonal with no major deviations from the diagonal. This shows that the normalized residue approximates the normal distribution. Thus, it is assumed that the standard distribution of the balance is not violated.

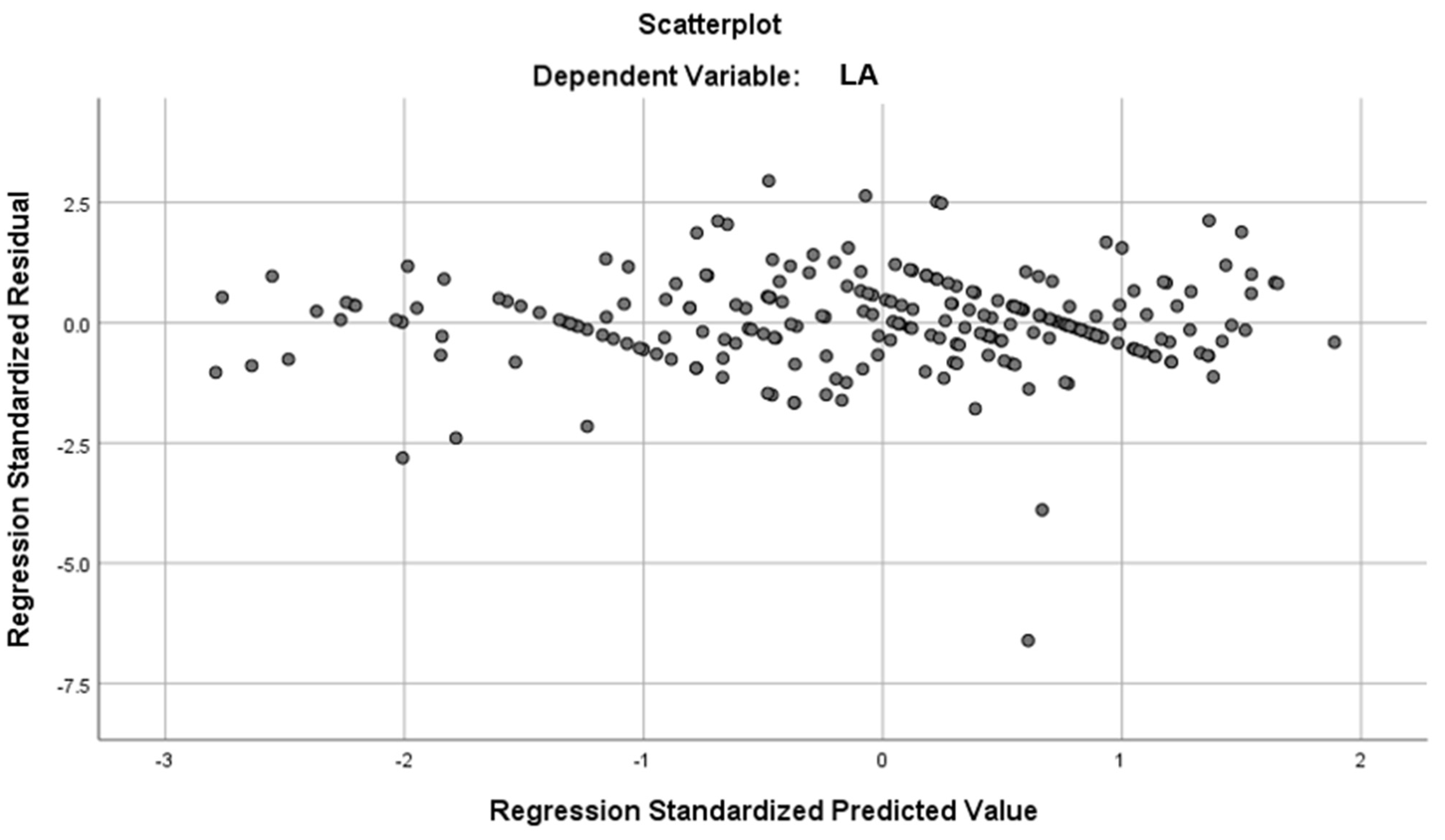

Regarding the test of linear contact and constant variance consumptions, to test these assumptions, the study used the Scatterplot scatter chart. Looking at

Figure 4, it could be seen that the data points are concentrated around the zero point and tend to form a straight line. Thus, the assumptions of linear contact and constant variance of residual are not violated.

6. Conclusions and Recommendations

The research results show that Vietnamese garment enterprises have not applied lean accounting yet, and the level of knowledge of lean accounting is still low. However, a lot of opinions highly appreciate the important role of lean accounting. In order to promote the application of lean accounting in Vietnamese garment enterprises, the study proposes some recommendations and policy implications as follows:

For garment enterprises in Vietnam, enterprises need to have a clear and long-term strategic plan, which is very important for businesses. Because lean accounting is associated with lean practices, the appearance of lean practices has led to the birth of lean accounting. Enterprises often apply food production first and then apply science and technology. Therefore, a clear and long-term strategic plan will be the motivation for enterprises to apply a climate change. In contrast, the application of lean accounting is one of the factors that helps businesses apply lean practices successfully.

In order to create a transformation in accounting, business leaders and accountants must understand the business environment and production processes of enterprises. Understanding will help them overcome barriers of fear, a lacking education system, and the ability to resist cultural change. Enterprises need to have detailed and appropriate training courses and seminars to train leaders and accountants.

When building a lean practice company culture, enterprises need to have a single unified goal of creating value for customers, always have a spirit of cooperation, strive for continuous improvement, and ensure that employees are empowered to decide in a suitable scope. Enterprises are not top-down management but bottom-up management because senior management must unleash the creativity of the workforce.

A communication system also needs to be established. Effective communication allows the faster dissemination of the concepts, benefits, and tools of lean accounting among employees in the enterprise.

Adequate resources for the application of lean accounting should be considered by enterprises. Costs and resources can be specifically planned to bring about appropriate change.

Business leaders talk to accountants about the benefits of new technology and advise and motivate them to minimize fears about the unknown, losing jobs, losing power, and an inability to accept new changes.

For agencies and organizations outside the garment enterprises, while the Ministry of Finance is the highest state management agency in accounting, the Accounting and Auditing Association is the professional organization with the most important role in accounting activities. Therefore, these two units need to be pioneers in the awareness of lean accounting. The Ministry of Finance and the Association of Accountants and Auditors need to coordinate to orient, develop theoretical frameworks, and encourage scholars to study on lean accounting. These units need to organize training courses and seminars, and release materials on lean accounting to improve understanding of information and communication.

The Vietnam Textile and Garment Association holds great importance in the operational orientation of garment enterprises. Therefore, the Association also needs to have a full awareness of the role of lean accounting, as well as research on lean accounting associated with the characteristics of the garment industry to have the right orientations for enterprises.

Educational and training institutions are extremely important in providing accounting knowledge and skills. Therefore, these establishments need to update new accounting knowledge in general as well as lean accounting in particular to keep up with the development of accounting in the world and meet the labor needs of society. Educational and training institutions also need to coordinate with garment enterprises to organize training courses on lean accounting associated with the characteristics of the garment industry for the accounting of these enterprises and provide necessary advice for the application of lean accounting at garment enterprises.

Regarding the limitations of the study, the study was conducted on the basis of the answer sheet of 140 garment enterprises, so the research sample may not be large. No stratified random sampling has been performed to ensure that surveyed enterprises represent Vietnamese garment enterprises in the overall survey. The fact that each garment company answers a survey can help the research results not depend too much on one enterprise, but it can also be skewed if the respondent lacks an understanding of the questionnaire, does not understand the question correctly, and does not provide the correct or leaves it incomplete. We go to study the factors affecting the application of lean accounting, but we have not studied the reasons that the business has not applied lean accounting. This is the limitation of our study: that we have not learned more about why it has not been applied or what the difficulties in applying lean accounting are.

As a suggestion for the future research, from the results and limitations of the study, the next research direction can be implemented, including increasing the number of surveyed enterprises, ensuring the survey for each enterprise has 3 to 5 votes, and choosing randomly stratified samples to increase the reliability of the research results. More independent variables should also be researched to be able to more fully identify the factors affecting the application of lean accounting in Vietnamese garment enterprises. We also need to study the factors affecting the application of lean accounting in enterprises in other fields so that it can be confirmed whether the factors affecting the application of lean accounting depend on the characteristics of the business sector.

{kind=link}

{kind=link}

{kind=link}

{kind=link}