The Impact of FASB Staff Position APB 14-1 on Corporate Financing: A Debt Contracting Perspective

Abstract

:1. Introduction

2. Background

2.1. FASB Staff Position APB 14-1

2.2. Institutional Background of Convertible Debt Financing

2.3. Prior Literature

2.3.1. Economic Consequences of Mandatory GAAP Changes

2.3.2. Debt Contracting and Financial Accounting Information

3. Hypotheses Development

4. Sample Selection and Research Design

4.1. Sample Selection

4.2. Research Design

4.2.1. Response to APB 14-1 and Ability to Bear the Costs of Repurchases

4.2.2. Response to APB 14-1 and Debt Contracting Practices

5. Empirical Results

5.1. Descriptive Statistics

5.2. Multivariate Tests

5.2.1. Firm’s Ability to Carry Out the Repurchases

5.2.2. Debt Contracting Practices and Repurchase of Cash-Settled Convertibles

6. Sensitivity Analysis

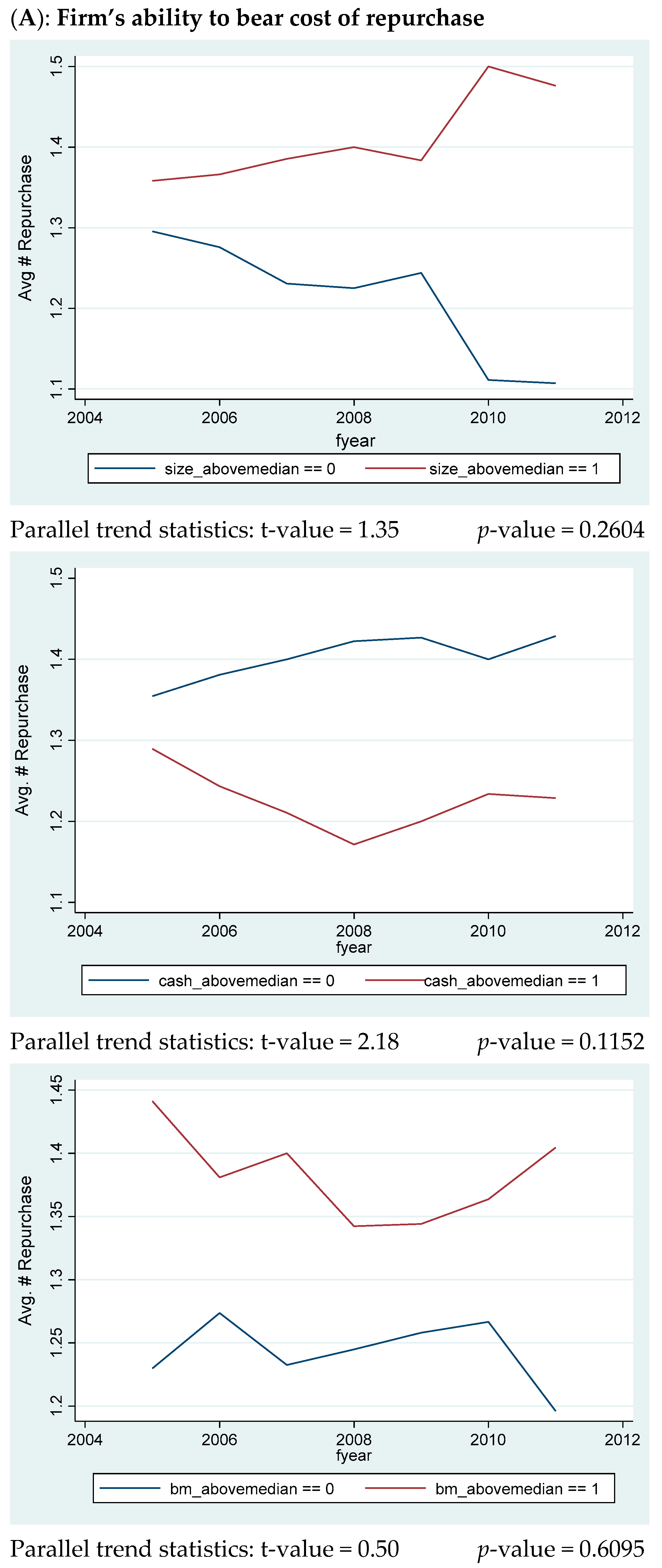

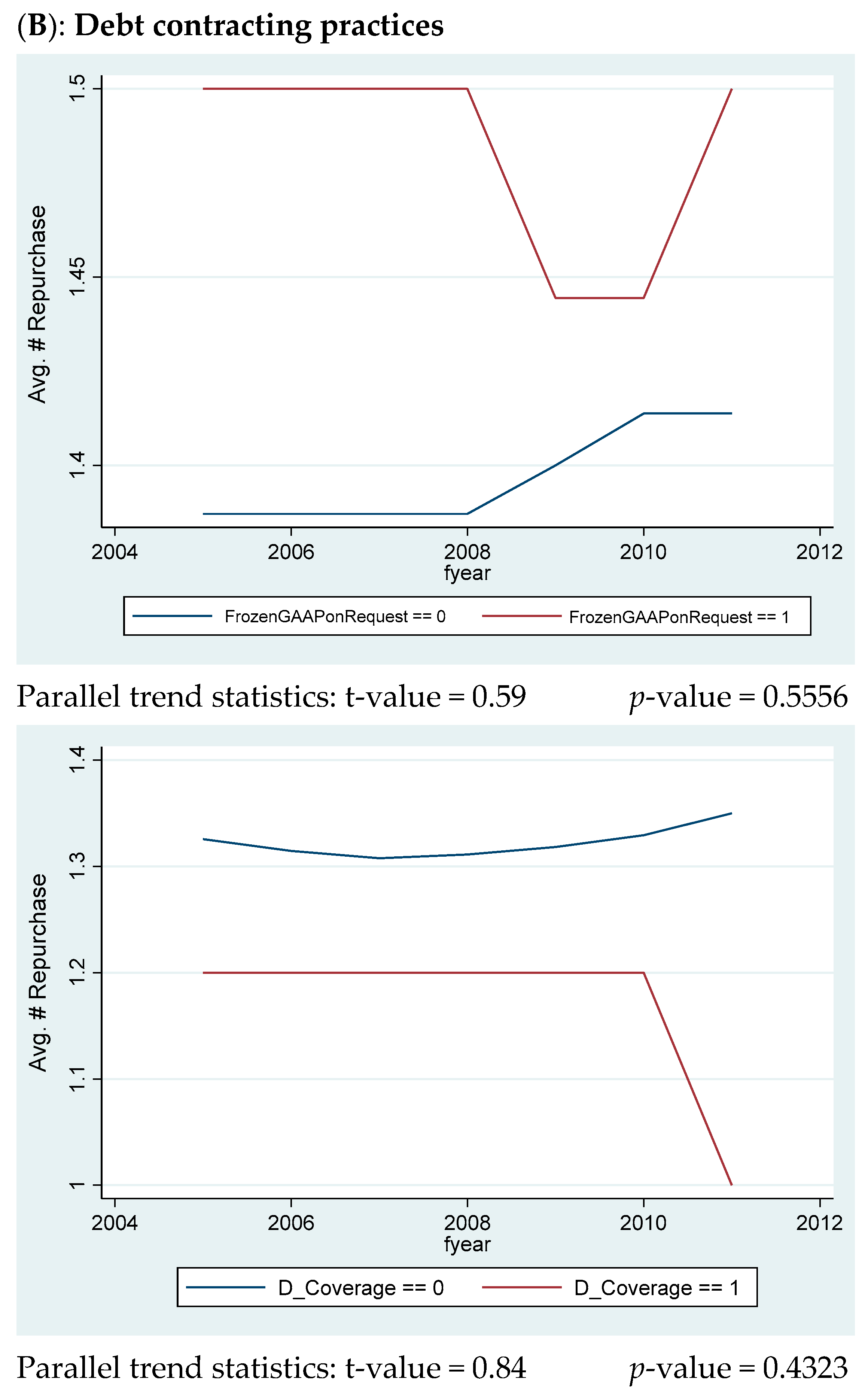

6.1. Parallel Trends Assumption

6.2. Firms’ Investment Efficiency and Repurchase Decision

6.3. Impact of Financial Constraints

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Examples of the Impact of Bifurcation under APB 14-1

| Present value of the principal—$100,000,000 payable in 10 years at the 8% market rate | $46,319,349 |

| Present value of interest—$2,000,000 payable annually in arrears for 10 years | $13,420,163 |

| Total liability component | $59,739,512 |

| Total equity component/debt discount ($100,000,000–$59,739,512) | $40,260,488 |

{kind=link}

{kind=link}

| Pre-APB 14-1: Example 1 (1 January 2007) | Post-APB 14-1: Example 2 (1 January 2009) | Impact of APB 14-1 on the Same Convertible Debt if Issued in 2007 vs. 2009 | ||

| (1) | (2) | ((2)-(1)) | ((2)-(1)) ÷ (1) | |

| Total liability component | $100,000,000 | $59,739,512 | ($40,260,488) | −40.26% |

| Total equity component | $0 | $40,260,488 | $40,260,488 | 100.00% |

| Reported net income | $10,000,000 | $7,220,839 | ($2,779,161) | −27.79% |

| Interest expense for 2009 | $2,000,000 | $4,779,161 | $2,779,161 | 138.96% |

| Total interest expense over 10-year life | $20,000,000 | $40,260,488 | $20,260,488 | 101.30% |

| The basic EPS | 0.5 | 0.361 | (0.139) | −27.80% |

| Adjustment to the numerator | $0 | $0 | $0 | 0.00% |

| Adjustment to the denominator | 90,909 shares | 90,909 shares | 90,909 shares | 0% |

| Diluted EPS | 0.497 | 0.359 | (0.138) | −27.76% |

Appendix B. Variable Definitions

| Variable | Description | |

| APB | = | Indicator variable that equals one if repurchase in 2008 or 2009, and zero otherwise. |

| BM | = | Book value of equity divided by market value of equity at end of year. |

| CAPX | = | Capital expenditure ÷ total assets. |

| Cash | = | Cash on hand ÷ total assets. |

| EarlyRedeem | = | Indicator variable that equals one if issuer has an option to redeem outstanding convertibles prior to maturity date, and zero otherwise. |

| InterestImpact | = | Hypothetical changes in reported interest expense as a result of bifurcation if firms do not repurchase their cash-settled convertibles, scaled by the issuers’ EBIT each year. Under APB 14-1, the equity component of cash-settled convertible will be amortized as debt discount and added to reported interest expense using effective interest method. Please refer to Appendix A for detailed calculations of reported interest expense. Thus, this variable measures the impact of increased interest expense on issuers’ EBIT due to the bifurcation required by APB14-1. |

| InterestCoverage | = | Issuers’ EBIT ÷ issuers’ interest expense. |

| InvEff | = | Average investment efficiency measures over the past eight years (2000–2007), calculated following Biddle et al. (2009). |

| LEV | = | Book value of total liabilities ÷ (book value of total liabilities + market value of equity). |

| LevImpact | = | Hypothetical changes in reported leverage ratio as a result of bifurcation if firms do not repurchase their cash-settled convertibles. Please refer to Appendix A for detailed calculations of debt and equity components under APB 14-1. Thus, this variable measures the impact of bifurcation on leverage ratio. |

| Public | = | Indicator variable that equals one if the issuance is public, and zero otherwise. |

| rankFinConst | = | The tertile ranking of the financial constraint measure calculated using the methodology from Lamont et al. (2001). They regress investments on firm characteristics, including cash flow, Tobin’s Q, leverage, dividends, and cash holdings scaled by the book value of assets, using the sample from Kaplan and Zingales (1997). They then construct a financial constraint index using the coefficients from this regression. This index is calculated as: −1.001909*CashFlow/Assets + 3.139193*LTDebt/Assets − 39.36780*Dividends/Assets − 1.314759*Cash/Assets + 0.2826389*Tobin’s Q. Higher rankings represent more constrained firms. |

| Repurchase | = | Indicator variable that equals one if the issuer of cash-settled convertible debt repurchased any amount of its outstanding convertible debt during our sample period, and zero otherwise. |

| ROA | = | Issuer’s EBIT ÷ average total assets. |

| Size | = | The log of total assets at the end of each fiscal year. |

Appendix C. Examples of Contracting Treatment of GAAP Changes

- Rolling GAAP

- 2.

- Rolling GAAP for voluntary accounting changes

- 3.

- Frozen GAAP

- 4.

- Frozen GAAP on request

| 1 | In August 2020, the FASB issued ASU 2020-06, Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity. This guidance removes the bifurcation requirement in ASC 470-20 for issuers of cash-settled convertible debt. Instead, cash-settled convertible debt should be recognized as debt in its entirety, regardless of the likelihood of cash settlement. The guidance in ASU 2020-06 also requires entities to calculate diluted earnings per share (EPS) for convertible instruments by using the if-converted method. In addition, entities must presume share settlement for purposes of calculating diluted EPS when an instrument may be settled in cash or shares. ASU 2020-06 will become effective for public companies starting on 15 December 2021. |

| 2 | FASB APB 14—Accounting for Convertible Debt and Debt Issued with Stock Purchase Warrants, March 1969. |

| 3 | The FASB amended EITF 90-19 in 2002 to provide accounting guidance related to cash-settled convertible debt instruments. Under amended EITF 90-19, cash-settled convertible debt is accounted for in its entirety as a liability. However, the FASB allows the exclusion of cash-settled convertible debt from the calculation of diluted EPS. As a result, cash-settled convertible debt “has less of a dilutive effect than a convertible debt instrument that requires application of the if-converted method.” (https://dart.deloitte.com/USDART/pdf/9c7ce6b6-3f30-11e6-95db-2337c6a5456e, accessed on 1 February 2021) |

| 4 | FASB Preliminary Views—Financial Instruments with Characteristics of Equity, November 2007. |

| 5 | The sample selection is explained in Section 4.1. |

| 6 | Lewis and Verwijmeren (2011) provide a more detailed discussion of the innovations in convertible security designs. |

| 7 | Issuers can select from the following choices if they select a cash settlement feature in their convertible bond design. First, issuers can pay the full conversion value in cash. Second, issuers can pay the sum of the principal and accrued interest in cash and the conversion spread in either cash or common stock. Third, issuers can choose any combination of cash and common stock at conversion or maturity. The second choice is the most popular among the sample firms in this study. All of the issuers of cash-settled convertible bonds in our sample selected the second method. |

| 8 | APB 14-1 requires that the modified convertible debt instrument “shall continue to be accounted for separately unless the original instrument is required to be derecognized under Issues 06-6 and 96-19 (i.e., the debt instrument does not contain a substantive conversion feature as of its issuance date)”. |

| 9 | The sample period starts in 2005 to avoid any confounding effect of changes in Contingent Convertible (COCO) accounting in 2004. For a detailed discussion of the consequences of such accounting changes, please refer to Marquardt and Wiedman (2007). The sample period ends in 2011 so that we have two balanced subperiods surrounding 2008. |

| 10 | Regulated industries such as utilities and financial industries may issue and repurchase cash-settled convertibles to meet capital requirements rather than benefitting from the financial reporting incentives examined in this study. |

| 11 | We hand-collect the following information from issuers’ public filings. First, we collect the details of the convertible debt offerings, such as method of settlement and call schedule. Second, we collect repurchase-related information (e.g., year of repurchase, source of funding, and gain or loss from repurchase). Third, we obtain the actual discount rate that issuers use to calculate the present value of the debt component of the convertible bonds. Fourth, we collect information about the impact of APB 14-1 on interest expense and leverage ratios that issuers disclosed beginning in fiscal year 2009. All of this information is used in this study’s empirical tests. |

| 12 | Data is available on Amir Sufi’s website (http://faculty.chicagobooth.edu/amir.sufi, accessed on 1 February 2021). |

| 13 | The conversion spread at the end of 2007: $110 × 1,000,000 shares − $100,000,000 = $10,000,000. The additional shares that will be issued at the conversion date: $10,000,000 ÷ $110 = 90,909 shares. |

| 14 | $10,000,000 ÷ (20,000,000 + 90,909) = 0.497. |

| 15 | The debt discount for 2009 is calculated with interest method: 8% × 59,739,512 − 2% × $100,000,000 = $2,779,161. |

| 16 | The conversion spread at the end of 2009: $110 × 1,000,000 shares − $100,000,000 = $10,000,000. The additional shares that will be issued at the conversion date: $10,000,000 ÷ $110 = 90,909 shares. |

| 17 | $7,220,839 ÷ (20,000,000 + 90,909) = 0.359. |

References

- Aboody, David, Mary E. Barth, and Ron Kasznik. 2004. SFAS No. 123 Stock-Based Compensation Expense and Equity Market Values. The Accounting Review 79: 251–75. [Google Scholar] [CrossRef]

- Baber, William R., Patricia M. Fairfield, and James A. Haggard. 1991. The effect of concern about reported income on discretionary spending decisions: The case of research and development. The Accounting Review 66: 818–29. [Google Scholar]

- Barthelme, Christian, Paraskevi V. Kiosse, and Thorsten Sellhorn. 2019. The impact of accounting standards on pension investment decisions. European Accounting Review 28: 1–33. [Google Scholar] [CrossRef]

- Barth, Mary E., William H. Beaver, and Wayne R. Landsman. 1996. Value-relevance of banks’ fair value disclosures under SFAS 107. The Accounting Review 71: 513–37. [Google Scholar]

- Beatty, Anne, K. Ramesh, and Joseph P. Weber. 2002. The importance of excluding accounting changes from the calculation of debt covenant compliance. Journal of Accounting and Economics 33: 205–27. [Google Scholar] [CrossRef]

- Bens, Daniel A., and Steven J. Monahan. 2008. Altering investment decisions to manage financial reporting outcomes: Asset-backed commercial paper conduits and FIN 46. Journal of Accounting Research 46: 1017–55. [Google Scholar] [CrossRef]

- Bens, Daniel A., Venky Nagar, Douglas Skinner, and M. H. Franco Wong. 2003. Employee stock options, EPS dilution, and stock repurchases. Journal of Accounting and Economics 36: 51–90. [Google Scholar] [CrossRef]

- Biddle, Gary C., Gilles Hilary, and Rodrigo S. Verdi. 2009. How Does Financial Reporting Quality Relate to Investment Efficiency? Journal of Accounting and Economics 48: 112–31. [Google Scholar] [CrossRef]

- Campello, Murillo, John R. Graham, and Campbell R. Harvey. 2010. The Real Effects of Financial Constraints: Evidence from a Financial Crisis. Journal of Financial Economics 97: 470–87. [Google Scholar] [CrossRef] [Green Version]

- Chava, Sudheer, and Michael R. Roberts. 2008. How does financing impact investment? The role of debt covenants. The Journal of Finance 63: 2085–121. [Google Scholar] [CrossRef]

- Choudhary, Preeti. 2011. Evidence on differences between recognition and disclosure: A comparison of inputs to estimate fair values of employee stock options. Journal of Accounting and Economics 51: 77–94. [Google Scholar] [CrossRef]

- Choudhary, Preeti, Shivaram Rajgopal, and Mohan Venkatachalam. 2009. Accelerated vesting of stock options in anticipation of SFAS 123R. Journal of Accounting Research 47: 105–46. [Google Scholar] [CrossRef]

- Christensen, Hans B., and Valeri V. Nikolaev. 2017. Contracting on GAAP changes: Large sample evidence. Journal of Accounting Research 55: 1021–50. [Google Scholar] [CrossRef]

- Christensen, Hans B., Valeri V. Nikolaev, and Regina Wittenberg-Moerman. 2016. Accounting information in financial contracting: The incomplete contract theory perspective. Journal of Accounting Research 54: 397–435. [Google Scholar] [CrossRef]

- Cohen, Moshe, Sharon P. Katz, Sunay Mutlu, and Gil Sadka. 2019. Do Debt Covenants Constrain Borrowings Prior to Violation? Evidence from SFAS 160. The Accounting Review 94: 133–56. [Google Scholar] [CrossRef]

- Cunningham, Lauren M., Chan Li, Sarah E. Stein, and Nicole S. Wright. 2019. What’s in a name? Initial evidence of U.S. audit partner identification using difference-in-difference analyses. The Accounting Review 94: 139–63. [Google Scholar] [CrossRef]

- Darrough, Masako N., and Mingcherng Deng. 2019. The role of accounting information in optimal debt contracts with informed lenders. The Accounting Review 94: 165–200. [Google Scholar] [CrossRef]

- Demerjian, Peter R. 2011. Accounting standards and debt covenants: Has the “balance sheet approach” led to a decline in the use of balance sheet covenants? Journal of Accounting and Economics 52: 178–202. [Google Scholar] [CrossRef]

- Devos, Erik, Shofiqur Rahman, and Desmond Tsang. 2017. Debt Covenants and the Speed of Capital Structure Adjustment. Journal of Corporate Finance 45: 1–18. [Google Scholar] [CrossRef]

- Elliott, John, Gordon Richardson, Thomas Dyckman, and Roland Dukes. 1984. The impact of SFAS No. 2 on firm expenditures on research and development: Replications and extensions. Journal of Accounting Research 22: 85–102. [Google Scholar] [CrossRef]

- Glaum, Martin, Tobias Keller, and Donna L. Street. 2018. Discretionary accounting choices: The case of IAS 19 pension accounting. Accounting and Business Research 48: 139–70. [Google Scholar] [CrossRef]

- Graham, John R., and Campbell R. Harvey. 2001. The theory and practice of corporate finance: Evidence from the field. Journal of Financial Economics 60: 187–243. [Google Scholar] [CrossRef]

- Hart, Oliver. 1993. Theories of Optimal Capital Structure: A Managerial Discretion Perspective. In The Deal Decade. Edited by Margaret M. Blair. Washington, DC: The Brookings Institution. [Google Scholar]

- Hodder, Leslie, William Maydew, Mary Lea McNally, and Connie D. Weaver. 2006. Employee stock option fair-value estimates: Do managerial discretion and incentives explain accuracy? Contemporary Accounting Research 23: 933–75. [Google Scholar] [CrossRef]

- Ivashina, Victoria, and David Scharfstein. 2010. Bank lending during the financial crisis of 2008. Journal of Financial Economics 97: 319–38. [Google Scholar] [CrossRef]

- Kaplan, Steven N., and Luigi Zingales. 1997. Do Investment–Cash Flow Sensitivities Provide Useful Measures of Financial Constraints? Quarterly Journal of Economics 112: 159–216. [Google Scholar] [CrossRef] [Green Version]

- Kausar, Asad, Nemit Shroff, and Hal White. 2016. Real effects of audit choice. Journal of Accounting and Economics 62: 157–81. [Google Scholar] [CrossRef]

- Kraft, Pepa. 2015a. Do Rating Agencies Cater?—Evidence from Rating-Based Contracts. Journal of Accounting and Economics 59: 264–83. [Google Scholar] [CrossRef]

- Kraft, Pepa. 2015b. Rating Agency Adjustments to GAAP Financial Statements and Their Effect on Ratings and Credit Spreads. The Accounting Review 90: 641–74. [Google Scholar] [CrossRef]

- Kraft, Pepa, Wayne R. Landsman, and Zilu Shan. 2021. Effect of Mandatory IFRS Adoption on Accounting-Based Prediction Models for CDS Spreads. European Accounting Review 30: 1–28. [Google Scholar] [CrossRef]

- Lamont, Owen, Christopher Polk, and Jesús Saaá-Requejo. 2001. Financial constraints and stock Return. Review of Financial Studies 14: 529–54. [Google Scholar] [CrossRef]

- Leone, Marie. 2008. Convertible Bonds’ Goose Is Cooked. CFO.com. August 22. Available online: http://ww2.cfo.com/accounting-tax/2008/08/convertible-bonds-goose-is-cooked/ (accessed on 1 February 2021).

- Levi, Shai, and Benjamin Segal. 2014. The impact of debt–equity reporting classifications on firms’ decision to issue hybrid securities. European Accounting Review 24: 801–22. [Google Scholar] [CrossRef]

- Lewis, Craig M., and Patrick Verwijmeren. 2011. Convertible security design and contract innovation. Journal of Corporate Finance 17: 809–31. [Google Scholar] [CrossRef]

- Marquardt, Carol, and Christine Wiedman. 2005. Earnings management through transaction structuring: Contingent convertible debt and diluted EPS. Journal of Accounting Research 43: 205–43. [Google Scholar] [CrossRef]

- Marquardt, Carol, and Christine Wiedman. 2007. Economic consequences of regulation of financial reporting: Diluted EPS and contingent convertible securities. Review of Accounting Studies 12: 487–523. [Google Scholar] [CrossRef]

- Myers, Stewart C. 1977. Determinants of Corporate Borrowing. Journal of financial Economics 5: 147–75. [Google Scholar] [CrossRef] [Green Version]

- Nikolaev, Valeri. 2010. Debt covenants and accounting conservatism. Journal of Accounting Research 48: 137–76. [Google Scholar] [CrossRef]

- Nini, Greg, David C. Smith, and Amir Sufi. 2012. Creditor Control Rights, Corporate Governance, and Firm Value. The Review of Financial Studies 25: 1713–61. [Google Scholar] [CrossRef]

- Scott, Thomas W., Christine Wiedman, and Heather A. Wier. 2011. Transaction Structuring and Canadian Convertible Debt. Contemporary Accounting Research 28: 1046–71. [Google Scholar] [CrossRef]

- Teach, Edward. 2014. A Splitting Headache? CFO.com. September 14. Available online: http://ww2.cfo.com/accounting-tax/2007/09/a-splitting-headache/ (accessed on 7 May 2014).

| Panel A: Sample Selection | ||||

| Issuance | Firms | |||

| Number of convertible debt issuances 2005–2011 | 626 | 478 | ||

| Less: firms from financial and utilities industries | −115 | −79 | ||

| Total number of unique observations | 511 | 390 | ||

| Less: firms missing Compustat data | −34 | −30 | ||

| Cash-settled convertible debt | 359 | 279 | ||

| Panel B: Distribution of cash-settled convertible debt issuers by industries | ||||

| Industry | # of Issuances | % of Sample | # of Issuers | % of Sample |

| Business Services | 45 | 12.53 | 32 | 11.47 |

| Chemicals and Allied Products | 52 | 14.48 | 40 | 14.34 |

| Coal | 7 | 1.95 | 5 | 1.79 |

| Communication | 20 | 5.57 | 14 | 5.02 |

| Electronic and Other Electrical Equipment | 39 | 10.86 | 27 | 9.68 |

| Engineering, Accounting, and Management Services | 4 | 1.11 | 3 | 1.08 |

| Fabricated Products | 9 | 2.51 | 8 | 2.87 |

| Food Products | 5 | 1.39 | 5 | 1.79 |

| Food Stores | 2 | 0.56 | 2 | 0.72 |

| Healthcare | 10 | 2.79 | 8 | 2.87 |

| Industrial and Commercial Machinery | 20 | 5.57 | 17 | 6.09 |

| Measuring and Control Equipment | 34 | 9.47 | 27 | 9.68 |

| Metal Mining | 8 | 2.23 | 5 | 1.79 |

| Oil and Gas Extraction | 20 | 5.57 | 15 | 5.38 |

| Primary Metal Industries | 7 | 1.95 | 6 | 2.15 |

| Air Transportation | 8 | 2.23 | 7 | 2.51 |

| Transportation Equipment | 12 | 3.34 | 10 | 3.58 |

| Wholesale Trade-Durable Goods | 11 | 3.06 | 8 | 2.87 |

| All Others | 46 | 12.81 | 40 | 14.34 |

| Total | 359 | 100 | 279 | 100 |

| Cash-Settled Convertible Debt | Sum of Cash- and Equity-Settled Convertible Debt | Proportion of Cash-Settled to Sum of Cash- and Equity-Settled Convertible Debt | ||||

|---|---|---|---|---|---|---|

| Issue Year | Total Proceeds ($billions) | No. of Issuance | Total Proceeds ($billions) | No. of Issuance | Total Proceeds (%) | No. of Issuance (%) |

| 2005 | 14.8 | 48 | 15.74 | 55 | 94.03 | 87.27 |

| 2006 | 45.48 | 76 | 46.59 | 85 | 97.62 | 89.41 |

| 2007 | 40.05 | 88 | 46.56 | 109 | 86.02 | 80.73 |

| 2008 | 13.78 | 39 | 16.37 | 52 | 84.18 | 75.00 |

| 2009 | 16.48 | 40 | 23.94 | 72 | 68.84 | 55.56 |

| 2010 | 12.65 | 34 | 16.67 | 54 | 75.88 | 62.96 |

| 2011 | 10.14 | 34 | 13.35 | 50 | 75.96 | 68.00 |

| Total | 153.38 | 359 | 179.22 | 477 | 85.58 | 75.26 |

| Variable | N | Mean | S.D. | 0.25 | Median | 0.75 | Max | |

|---|---|---|---|---|---|---|---|---|

| Variable of interests | ||||||||

| APB | 2312 | 0.29 | 0.45 | 0 | 0 | 1 | 1 | |

| Repurchase | 2312 | 0.47 | 0.50 | 0 | 0 | 1 | 1 | |

| InterestImpact (%) | 1634 | 0.07 | 0.17 | 0.01 | 0.02 | 0.05 | 1.33 | |

| LevImpact | 2312 | 0.06 | 0.12 | 0.01 | 0.03 | 0.06 | 1.32 | |

| Control variables | ||||||||

| EarlyRedeem | 2312 | 0.49 | 0.50 | 0 | 0 | 1 | 1 | |

| Size | 2312 | 7.52 | 1.43 | 6.66 | 7.44 | 8.33 | 11.05 | |

| BM | 2312 | 0.52 | 0.58 | 0.24 | 0.43 | 0.74 | 3.79 | |

| ROA | 2312 | 0.04 | 0.15 | 0.01 | 0.07 | 0.11 | 0.35 | |

| Cash | 2281 | 0.14 | 0.14 | 0.04 | 0.1 | 0.2 | 0.72 | |

| LEV | 2312 | 0.4 | 0.23 | 0.22 | 0.37 | 0.56 | 0.96 | |

| InterestCoverage | 2215 | 15.32 | 72.67 | 0.69 | 3.48 | 8.52 | 531.22 | |

| CAPX | 2309 | 0.06 | 0.08 | 0.02 | 0.03 | 0.07 | 0.46 | |

| Public | 2312 | 0.31 | 0.46 | 0 | 0 | 1 | 1 | |

| Debt contracting variables | ||||||||

| RollingGAAP | 747 | 0.27 | 0.44 | 0 | 0 | 1 | 1 | |

| RollingGAAP_Voluntary | 747 | 0.04 | 0.19 | 0 | 0 | 0 | 1 | |

| FrozenGAAP | 747 | 0.14 | 0.35 | 0 | 0 | 0 | 1 | |

| FrozenGAAPonRequest | 747 | 0.55 | 0.50 | 0 | 1 | 1 | 1 | |

| D_Coverage | 1395 | 0.11 | 0.3161 | 0 | 0 | 0 | 1 | |

| First-Time Repurchase Year | Cash-Settled | % of Total |

|---|---|---|

| 2005 | 0 | 0 |

| 2006 | 3 | 2% |

| 2007 | 3 | 2% |

| 2008 | 37 | 25% |

| 2009 | 47 | 32% |

| 2010 | 26 | 18% |

| 2011 | 31 | 21% |

| Total | 147 | 100% |

| Panel A: Size Partitions | |||

| Variable | Predicted Sign | Above Median | Below Median |

| (1) | (2) | ||

| APB | + | −0.4699 | 0.6180 *** |

| (−1.59) | (2.62) | ||

| InterestImpactit | + | 0.4560 | 0.0210 |

| (0.67) | (0.06) | ||

| LevImpactit | – | −1.6601 | −2.0725 ** |

| (−0.42) | (−2.05) | ||

| InterestImpact*APB | + | 4.1947 ** | −0.0500 |

| (2.37) | (−0.12) | ||

| LevImpact*APB | – | −1.8115 | 0.0932 |

| (−1.16) | (0.18) | ||

| EarlyRedeemit | + | 0.2328 | 0.4764 ** |

| (0.98) | (2.08) | ||

| Sizeit | + | −0.0602 | −0.2848 * |

| (−0.43) | (−1.66) | ||

| BMit | + | −0.0728 | 0.0229 |

| (−0.52) | (0.19) | ||

| ROAit | + | −0.6901 | 0.8648 |

| (−0.53) | (1.41) | ||

| Cashit | + | 1.8800 * | −0.6818 |

| (1.84) | (−1.12) | ||

| LEVit | + | 1.1767 * | −0.1086 |

| (1.65) | (−0.22) | ||

| InterestCoverageit | – | −0.0023 | −0.0020 |

| (−1.14) | (−1.26) | ||

| CAPXit | + | 0.9737 | −1.3185 |

| (0.42) | (−0.90) | ||

| Publicit | – | −0.3189 | −0.3810 |

| (−1.25) | (−1.30) | ||

| H0: (above − below) = 0 | |||

| IntImpact*APB | χ2 = 5.41, p value = 0.020 | ||

| LevImpact*APB | χ2 = 1.20, p value = 0.273 | ||

| Industry fixed effect | Yes | Yes | |

| Year fixed effect | Yes | Yes | |

| # of obs | 758 | 627 | |

| Pseudo-R2 | 0.168 | 0.153 | |

| Panel B: Operating Cash Flow Partitions | |||

| Variable | Predicted Sign | Above Median | Below Median |

| (1) | (2) | ||

| APB | + | −0.2876 | 0.5928 *** |

| (−1.03) | (2.75) | ||

| InterestImpactit | + | 0.2747 | −0.0147 |

| (0.40) | (−0.04) | ||

| LevImpactit | – | 0.6066 | −1.7754 * |

| (0.24) | (−1.78) | ||

| InterestImpact*APB | + | 2.3280 * | 0.1234 |

| (1.29) | (0.29) | ||

| LevImpact*APB | – | −3.3583 *** | −0.3239 |

| (−2.34) | (−0.68) | ||

| EarlyRedeemit | + | 0.2830 | 0.4197 ** |

| (1.30) | (1.98) | ||

| Sizeit | + | −0.1794 | −0.2130 * |

| (−1.63) | (−1.73) | ||

| BMit | + | −0.1862 | 0.1236 |

| (−0.99) | (1.30) | ||

| ROAit | + | −0.2145 | 0.5438 |

| (−0.19) | (0.90) | ||

| Cashit | + | 0.4580 | −0.6508 |

| (0.51) | (−1.13) | ||

| LEVit | + | 0.9958 | 0.0712 |

| (1.41) | (0.17) | ||

| InterestCoverageit | – | −0.0018 | −0.0038 * |

| (−1.16) | (−1.67) | ||

| CAPXit | + | 0.3399 | −1.3040 |

| (0.15) | (−1.11) | ||

| Publicit | – | −0.2704 | −0.3431 |

| (−1.15) | (−1.39) | ||

| H0: (above − below) = 0 | |||

| IntImpact*APB | χ2 = 1.33, p value = 0.249 | ||

| LevImpact*APB | χ2 = 3.75, p value = 0.052 | ||

| Industry fixed effect | Yes | Yes | |

| Year fixed effect | Yes | Yes | |

| # of obs | 783 | 663 | |

| Pseudo-R2 | 0.158 | 0.132 | |

| Panel C: Book-to-Market Ratio Partitions | |||

| Variable | Predicted Sign | Above Median | Below Median |

| (1) | (2) | ||

| APB | + | −0.4203 | 0.1318 |

| (−1.18) | (0.48) | ||

| InterestImpactit | + | −0.7370 | 0.5366 |

| (−1.28) | (1.44) | ||

| LevImpactit | – | −1.3167 | −0.4121 |

| (−1.38) | (−0.37) | ||

| InterestImpact*APB | + | 1.0726 * | −0.2256 |

| (1.54) | (−0.43) | ||

| LevImpact*APB | – | −0.5815 | −0.3676 |

| (−0.91) | (−0.29) | ||

| EarlyRedeemit | + | 0.0929 | 0.5514 *** |

| (0.44) | (2.64) | ||

| Sizeit | + | −0.1973 * | −0.1439 |

| (−1.83) | (−1.55) | ||

| BMit | + | −0.0736 | 0.4574 ** |

| (−0.46) | (1.97) | ||

| ROAit | + | −0.4425 | 0.6070 |

| (−0.49) | (1.01) | ||

| Cashit | + | −0.3396 | 0.1488 |

| (−0.36) | (0.28) | ||

| LEVit | + | 0.4608 | 1.1621 ** |

| (0.68) | (2.09) | ||

| InterestCoverageit | – | −0.0029 * | −0.0022 |

| (−1.89) | (−1.37) | ||

| CAPXit | + | −1.3691 | −0.4528 |

| (−0.75) | (−0.32) | ||

| Publicit | – | −0.1866 | −0.3693 |

| (−0.86) | (−1.59) | ||

| H0: (above − below) = 0 | |||

| IntImpact*APB | χ2 = 2.05, p value = 0.152 | ||

| LevImpact*APB | χ2 = 0.02, p value = 0.884 | ||

| Industry fixed effect | Yes | Yes | |

| Year fixed effect | Yes | Yes | |

| # of obs | 712 | 727 | |

| Pseudo-R2 | 0.122 | 0.143 | |

| Panel A: GAAP Terms | ||

| Variable | Predicted Sign | FrozenGAAPonRequest |

| APB | + | −0.1621 |

| (−0.28) | ||

| FrozenGAAPonRequest | – | −0.4043 |

| (−0.87) | ||

| FrozenGAAPonRequest*APB | – | −0.4662 ** |

| (−1.97) | ||

| InterestImpactit | + | −0.7281 |

| (−0.30) | ||

| InterestImpact*APB | + | 11.0411 ** |

| (2.13) | ||

| InterestImpact*FrozenGAAPonRequest*APB | – | −11.2136 ** |

| (−2.06) | ||

| InterestImpact*FrozenGAAPonRequest | + | 2.9167 |

| (1.08) | ||

| LevImpactit | – | −0.4690 |

| (−0.05) | ||

| LevImpact*APB | – | −19.4080 ** |

| (−2.26) | ||

| LevImpact*FrozenGAAPonRequest*APB | + | 20.0697 ** |

| (2.32) | ||

| LevImpact*FrozenGAAPonRequest | + | −4.4599 |

| (−0.47) | ||

| EarlyRedeemit | + | 0.7745 ** |

| (2.25) | ||

| Sizeit | + | −0.2394 |

| (−1.50) | ||

| BMit | – | −0.0119 |

| (−0.05) | ||

| ROAit | + | 3.4093 ** |

| (2.01) | ||

| Cashit | + | 1.7894 |

| (1.03) | ||

| LEVit | – | 1.8920 * |

| (1.91) | ||

| InterestCoverageit | + | −0.0003 |

| (−0.04) | ||

| CAPXit | + | 2.3701 |

| (0.84) | ||

| Publicit | – | 0.5959 * |

| (1.77) | ||

| Industry fixed effect | Yes | |

| Year fixed effect | Yes | |

| # of obs | 399 | |

| Pseudo-R2 | 0.258 | |

| Panel B: Interest Coverage Covenant | ||

| Variable | Predicted Sign | Interest Coverage Covenant |

| APB | + | 0.3002 |

| (1.49) | ||

| InterestImpactit | + | 0.6678 |

| (1.05) | ||

| D_Coverage | + | 0.1020 |

| (0.21) | ||

| D_Coverage*APB | + | −0.3165 |

| (−0.46) | ||

| InterestImpact*APB | + | −1.0229 |

| (−0.53) | ||

| InterestImpactt*D_Coverage | + | −0.4207 |

| (−0.94) | ||

| InterestImpact*D_Coverage*APB | + | 6.4554 ** |

| (2.41) | ||

| LevImpactit | – | 1.1106 |

| (0.70) | ||

| LevImpact*APB | – | −0.5670 |

| (−0.77) | ||

| LevImpact*D_Coverage | ? | −2.0633 |

| (−0.14) | ||

| LevImpact*D_Coverage*APB | ? | 3.4016 |

| (0.20) | ||

| EarlyRedeemit | + | 0.5215 ** |

| (2.31) | ||

| Sizeit | + | −0.3223 *** |

| (−3.18) | ||

| BMit | 0.1643 | |

| (0.97) | ||

| ROAit | + | 1.5799 ** |

| (2.44) | ||

| Cashit | + | −0.7643 |

| (−1.29) | ||

| LEVit | – | 0.2877 |

| (0.52) | ||

| InterestCoverageit | + | −0.0017 |

| (−1.56) | ||

| CAPXit | + | −3.6539 ** |

| (−2.12) | ||

| Publicit | – | 0.1331 |

| (0.53) | ||

| Industry fixed effect | Yes | |

| Year fixed effect | Yes | |

| # of obs | 873 | |

| Pseudo-R2 | 0.156 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jin, J.Y.; Kanagaretnam, K.; Li, N. The Impact of FASB Staff Position APB 14-1 on Corporate Financing: A Debt Contracting Perspective. J. Risk Financial Manag. 2023, 16, 213. https://doi.org/10.3390/jrfm16040213

Jin JY, Kanagaretnam K, Li N. The Impact of FASB Staff Position APB 14-1 on Corporate Financing: A Debt Contracting Perspective. Journal of Risk and Financial Management. 2023; 16(4):213. https://doi.org/10.3390/jrfm16040213

Chicago/Turabian StyleJin, Justin Y., Kiridaran Kanagaretnam, and Na Li. 2023. "The Impact of FASB Staff Position APB 14-1 on Corporate Financing: A Debt Contracting Perspective" Journal of Risk and Financial Management 16, no. 4: 213. https://doi.org/10.3390/jrfm16040213