The Impact of ICT on the Profitability of Indian Banks: The Moderating Role of NPA

, , and

, , and

Abstract

:1. Introduction (1200)

2. Review of Literature and Hypotheses Development

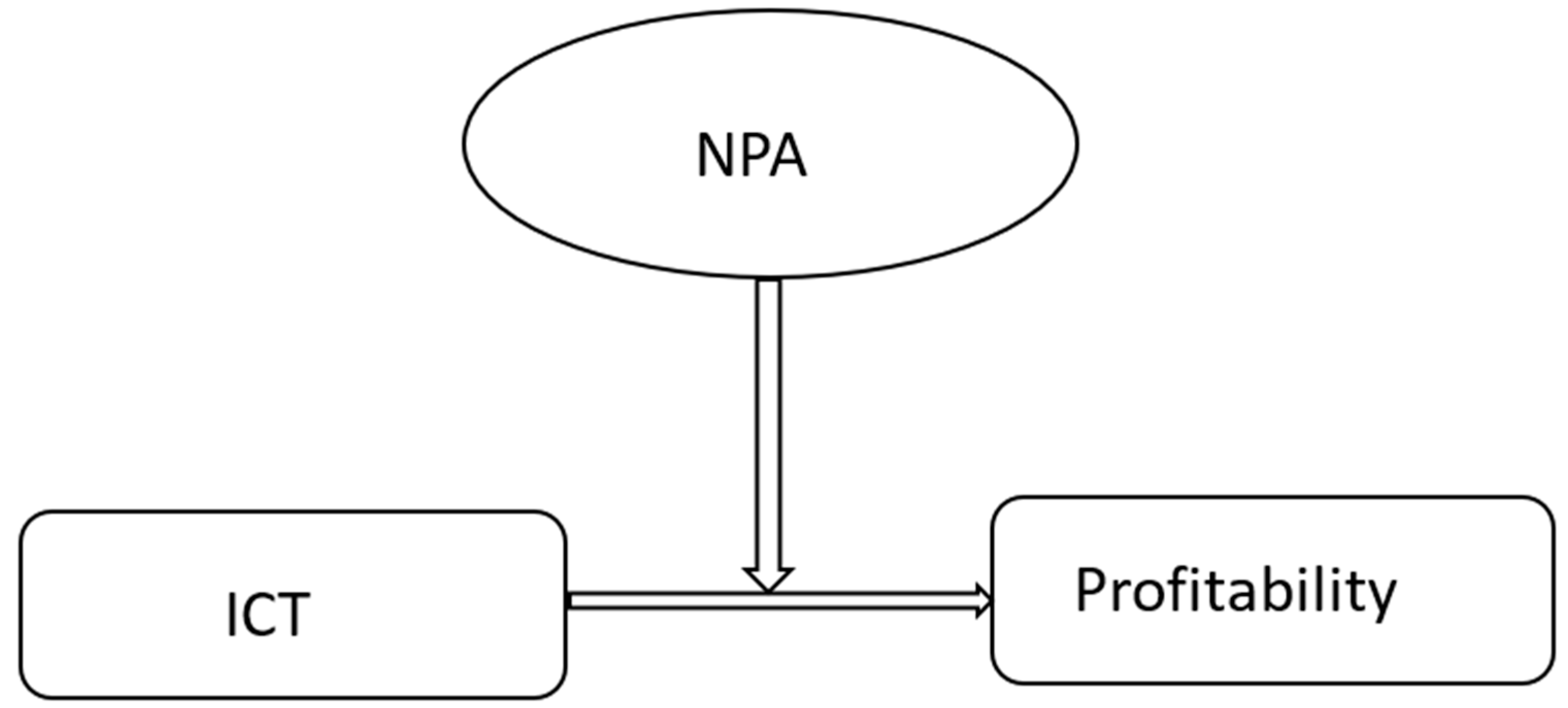

Conceptual Model

3. Sample Data and Methodology

3.1. Sample Data

3.2. Methodology

4. Results

4.1. Descriptive Analysis and Correlation Matrix Table

4.2. Regression Analysis

Results of Model

4.3. Robustness Check

5. Discussion

ICT and Its Relevance for Banks Post-COVID

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| S. No. | Reference | Country | Findings |

|---|---|---|---|

| 1 | JH Coun et al. (2022). | Dutch | ICT improves profitability |

| 2 | Entele (2021) | World | ICT improves profitability |

| 3 | Adane et al. (2021) | Ethiopian | ICT improves profitability |

| 4 | Wang et al. (2021) | China | ICT improves profitability |

| 5 | Zhu et al. (2021) | China | ICT improves profitability |

| 6 | Del Gaudio et al. (2021) | European Union | ICT improves profitability |

| 7 | Scott et al. (2017) | European and American banks | ICT improves profitability |

| 8 | Barpanda and Athira (2022) | India | ICT does not affect profitability |

| 9 | Adeabah et al. (2021) | Worldwide | ICT impacts profitability |

| 10 | Sanga and Aziakpono (2022) | Africa | ICT improves profitability |

References

- Adane, Mahilet Demissie, Teramaje Wale, and Eshetie Woretaw Meried. 2021. Determinants of automated teller machine deployment in commercial banks of Ethiopia. Heliyon 7: e07712. [Google Scholar] [CrossRef]

- Adeabah, David, Simplice Asongu, and Charles Andoh. 2021. Remittances, ICT and pension income coverage: The international evidence. Technological Forecasting and Social Change 173: 121148. [Google Scholar] [CrossRef]

- Albuquerque, Rui, Yrjo Koskinen, Shuai Yang, and Chendi Zhang. 2020. The resiliency of environmental and social stocks: An analysis of the exogenous COVID-19 market crash. The Review of Corporate Finance Studies 9: 593–621. [Google Scholar] [CrossRef]

- Al-Busaidi, Kamla Ali, and Saeed Al-Muharrami. 2021. Beyond profitability: ICT investments and financial institutions performance measures in developing economies. Journal of Enterprise Information Management 34: 900–21. [Google Scholar] [CrossRef]

- Almaqtari, Faozi A., Eissa A. Al-Homaidi, Mosab I. Tabash, and Najib H. Farhan. 2019. The determinants of profitability of Indian commercial banks: A panel data approach. International Journal of Finance and Economics 24: 168–85. [Google Scholar] [CrossRef]

- Balasubramaniam, C. S. 2012. Non-performing assets and profitability of commercial banks in India: Assessment and emerging issues. Abhinav, National Monthly Refereed Journal of Research in Commerce & Management 1: 41–52. [Google Scholar]

- Baltagi, Badi Hani. 2008. Econometric Analysis of Panel Data. Chichester: John Wiley & Sons, vol. 4. [Google Scholar]

- Bansal, Pooja, Sunil Kumar, Aparna Mehra, and Rachita Gulati. 2022. Developing two dynamic Malmquist-Luenberger productivity indices: An illustrated application for assessing productivity performance of Indian banks. Omega 107: 102538. [Google Scholar] [CrossRef]

- Barpanda, Saswat, and S. Athira. 2022. Cause of Attrition in an Information Technology-Enabled Services Company: A Triangulation Approach. International Journal of Human Capital and Information Technology Professionals (IJHCITP) 13: 1–22. [Google Scholar] [CrossRef]

- Ben Naceur, Sami, and Mohamed Goaied. 2008. The determinants of commercial bank interest margin and profitability: Evidence from Tunisia. Frontiers in Finance and Economics 5: 106–30. [Google Scholar] [CrossRef]

- Cazachevici, Alina, Tomas Havranek, and Roman Horvath. 2020. Remittances and economic growth: A meta-analysis. World Development 134: 105021. [Google Scholar] [CrossRef]

- Chhaidar, Ahlem, Mouna Abdelhedi, and Ines Abdelkafi. 2022. The effect of financial technology investment level on european banks’ profitability. Journal of the Knowledge Economy, 1–23. [Google Scholar] [CrossRef]

- Cicchiello, Antonella Francesca, Matteo Cotugno, Stefano Monferra, and Salvatore Perdichizzi. 2021. exploring the impact of ict diffusion in the european banking industry: Evidence in the pre- and Post-COVID-19. Journal of Financial Management, Markets and Institutions 9: 2150010. [Google Scholar] [CrossRef]

- Das, Santosh Kumar, and Khushboo Uppal. 2021. NPAs and profitability in Indian banks: An empirical analysis. Future Business Journal 7: 1–9. [Google Scholar] [CrossRef]

- Del Gaudio, Belinda L., Claudio Porzio, Gabriele Sampagnaro, and Vincenzo Verdoliva. 2021. How do mobile, internet and ICT diffusion affect the banking industry? An empirical analysis. European Management Journal 39: 327–32. [Google Scholar] [CrossRef]

- Doran, Nicoleta Mihaela, Roxana Maria Bădîrcea, and Alina Georgiana Manta. 2022. Digitization and Financial Performance of Banking Sectors Facing COVID-19 Challenges in Central and Eastern European Countries. Electronics 11: 3483. [Google Scholar] [CrossRef]

- Edwards, G., C. Duran, F. Sacchi, B. Ackermann, and L. Conversano. 2018. Déjà vu All over Again: Money Laundering and Sanctions Woes to Continue to Haunt Europe’s Banks. S&P Global Ratings 16 October 2018. Available online: www.allnews.ch/.../ratingsdirect_dejavualloveragainmoneylaunderingandsancti... (accessed on 28 April 2019).

- Entele, Birku Reta. 2021. Impact of institutions and ICT services in avoiding resource curse: Lessons from the successful economies. Heliyon 7: e05961. [Google Scholar] [CrossRef] [PubMed]

- Gaur, Dolly, and Dipti Ranjan Mohapatra. 2021. Non-performing assets and profitability: Case of Indian banking sector. Vision 25: 180–91. [Google Scholar] [CrossRef]

- Gautam, R. S., S. Rastogi, A. Rawal, V. M. Bhimavarapu, J. Kanoujiya, and S. Rastogi. 2022. Financial Technology and Its Impact on Digital Literacy in India: Using Poverty as a Moderating Variable. Journal of Risk and Financial Management 15: 311. [Google Scholar] [CrossRef]

- Horobet, Alexandra, Magdalena Radulescu, Lucian Belascu, and Sandra Maria Dita. 2021. Determinants of Bank Profitability in CEE Countries: Evidence from GMM Panel Data Estimates. Journal of Risk and Financial Management 14: 307. [Google Scholar] [CrossRef]

- Indriasari, Elisa, Harjanto Prabowo, Ford Lumban Gaol, and Betty Purwandari. 2022. Intelligent Digital Banking Technology and Architecture: A Systematic Literature Review. International Journal of Interactive Mobile Technologies 16: 98–117. [Google Scholar] [CrossRef]

- Jaeger, J. 2018. ING Reaches $900M Settlement with Dutch Authorities. Compliance Week. September 4. Available online: www.complianceweek.com/ing-reaches-900m-sttlement-with.../2156.article (accessed on 28 April 2018).

- Jardak, Maha Khemakhem, and Salah Ben Hamad. 2022. The effect of digital transformation on firm performance: Evidence from Swedish listed companies. The Journal of Risk Finance 23: 329–48. [Google Scholar] [CrossRef]

- Jayaraman, T. K., and Keshmeer Makun. 2022. Impact of COVID-19 pandemic on remittance inflow-economic growth-nexus in India: Lessons from an asymmetric analysis. Remittances Review 7: 91–116. [Google Scholar]

- JH Coun, Martine, Pascale Peters, Robert J. Blomme, and Jaap Schaveling. 2022. ‘To empower or not to empower, that’s the question’. Using an empowerment process approach to explain employees’ workplace proactivity. The International Journal of Human Resource Management 33: 2829–55. [Google Scholar] [CrossRef]

- Joseph, Ashly Lynn, and M. Prakash. 2014. A study on analysing the trend of NPA level in private sector banks and public sector banks. International Journal of Scientific and Research Publications 4: 1–9. [Google Scholar]

- Kanoujiya, Jagjeevan, Venkata Mrudula Bhimavarapu, and Shailesh Rastogi. 2021. Banks in India: A balancing act between profitability, regulation and NPA. Vision, 09722629211034417. [Google Scholar] [CrossRef]

- Kanoujiya, J., and S. Rastogi. 2022. Impact of market competitiveness and risk management of NPAs of Indian banks on its efficiency. International Journal of Monetary Economics and Finance 15: 173–93. [Google Scholar] [CrossRef]

- Kiran, K. Prasanth, and T. Mary Jones. 2016. Effect of Non Performing Assets on the profitability of banks–A selective study. International Journal of Business and General Management 5: 53–60. [Google Scholar]

- Kosach, I. A., A. V. Zhavoronok, M. F. Fedyshyn, and A. S. Abramova. 2019. Role of commission receipts in formation of the revenue of the commercial bank. Financial and Credit Activity Problems of Theory and Practice 4: 22–30. [Google Scholar] [CrossRef]

- Köster, Hannes, and Matthias Pelster. 2017. Financial penalties and bank performance. Journal of Banking & Finance 79: 57–73. [Google Scholar]

- Mahdi, Mahruzal, and Muammar Khaddafi. 2020. The Influence of Gross Profit Margin, Operating Profit Margin and Net Profit Margin on the Stock Price of Consumer Good Industry in the Indonesia Stock Exchange on 2012–2014. International Journal of Business, Economics, and Social Development 1: 153–63. [Google Scholar] [CrossRef]

- Manu, K. S., and Rakhi Maheshwari. 2018. Relationship between Non-Preforming Assets (NPA) and Profitability of Development Banks: The Case of India. Asian Journal of Research in Banking and Finance 8: 99–111. [Google Scholar] [CrossRef]

- Najaf, Khakan, Md Imtiaz Mostafiz, and Rabia Najaf. 2021. Fintech firms and banks sustainability: Why cybersecurity risk matters? International Journal of Financial Engineering 8: 2150019. [Google Scholar] [CrossRef]

- Nariswari, Talitha Nathaniela, and Nugi Mohammad Nugraha. 2020. Profit growth: Impact of net profit margin, gross profit margin and total assests turnover. International Journal of Finance & Banking Studies (2147-4486) 9: 87–96. [Google Scholar]

- Narula, Sonia, and Monika Singla. 2014. Empirical study on non-performing assets of bank. International Journal of Advance Research in Computer Science and Management Studies 2: 194–99. [Google Scholar]

- Phan, Dinh Hoang Bach, Paresh Kumar Narayan, R. Eki Rahman, and Akhis R. Hutabarat. 2020. Do financial technology firms influence bank performance? Pacific-Basin Finance Journal 62: 101210. [Google Scholar] [CrossRef]

- Potapova, Ekaterina A., Maxim O. Iskoskov, and Natalia V. Mukhanova. 2022. The Impact of Digitalization on Performance Indicators of Russian Commercial Banks in 2021. Journal of Risk and Financial Management 15: 452. [Google Scholar] [CrossRef]

- Ramlall, Indranarain. 2023. Digitization, Ageing Population and Bank Profitability: Evidence in Light of Two Global Crises. Journal of International Commerce, Economics and Policy, 23500072. [Google Scholar] [CrossRef]

- RBI (Reserve Bank of India) Official Site. 2023. Available online: https://www.rbi.org.in/ (accessed on 27 March 2023).

- Saedun, Nora Shafinaz, and Ibrahim Mohamed. 2017. Measuring employee value of IT staff in banking sector through value profit chain variables. Paper presented at the 2017 6th International Conference on Electrical Engineering and Informatics (ICEEI), Langkawi, Malaysia, November 25–27; pp. 1–6. [Google Scholar]

- Saksonova, Svetlana. 2014. The role of net interest margin in improving banks’ asset structure and assessing the stability and efficiency of their operations. Procedia-Social and Behavioral Sciences 150: 132–41. [Google Scholar] [CrossRef]

- Saleh, Yasser. 2021. ICT, social media and COVID-19: Evidence from informal home-based business community in Kuwait City. Journal of Enterprising Communities: People and Places in the Global Economy 15: 395–413. [Google Scholar] [CrossRef]

- Sanga, Bahati, and Meshach Aziakpono. 2022. The impact of technological innovations on financial deepening: Implications for SME financing in Africa. African Development Review 34: 429–42. [Google Scholar] [CrossRef]

- Sanya, Sarah, and Simon Wolfe. 2011. Can banks in emerging economies benefit from revenue diversification? Journal of Financial Services Research 40: 79–101. [Google Scholar] [CrossRef]

- Sarkar, Sukanta. 2012. The role of information and communication technology (ICT) in higher education for the 21st century. Science 1: 30–41. [Google Scholar]

- Scott, Susan V., John Van Reenen, and Markos Zachariadis. 2017. The long-term effect of digital innovation on bank performance: An empirical study of SWIFT adoption in financial services. Research Policy 46: 984–1004. [Google Scholar] [CrossRef]

- Shinkevich, Alexey I., Svetlana S. Kudryavtseva, and Vera P. Samarina. 2023. Ecosystems as an Innovative Tool for the Development of the Financial Sector in the Digital Economy. Journal of Risk and Financial Management 16: 72. [Google Scholar] [CrossRef]

- Uddin, Md Hamid, Sabur Mollah, and Md Hakim Ali. 2020. Does cyber tech spending matter for bank stability? International Review of Financial Analysis 72: 101587. [Google Scholar] [CrossRef]

- Von Solms, Johan, Josef Langerman, and Carl Marnewick. 2021. Digital transformation in treasury, risk and finance: COVID-19 to accelerate establishment of smart analytical centres in these departments. Journal of Risk Management in Financial Institutions 14: 381–94. [Google Scholar]

- Wagner, Wolf. 2007. The liquidity of bank assets and banking stability. Journal of Banking & Finance 31: 121–39. [Google Scholar]

- Wang, Yang, Sui Xiuping, and Qi Zhang. 2021. Can fintech improve the efficiency of commercial banks?—An analysis based on big data. Research in International Business and Finance 55: 101338. [Google Scholar] [CrossRef]

- Wen, Chunhui, Jinhai Yang, Liu Gan, and Yang Pan. 2021. Big data driven Internet of Things for credit evaluation and early warning in finance. Future Generation Computer Systems 124: 295–307. [Google Scholar] [CrossRef]

- Yan, Yuanyun, Bang Nam Jeon, and Ji Wu. 2023. The impact of the COVID-19 pandemic on bank systemic risk: Some cross-country evidence. China Finance Review International. [Google Scholar] [CrossRef]

- Yeoh, Peter. 2020. Banks’ vulnerabilities to money laundering activities. Journal of Money Laundering Control 23: 122–35. [Google Scholar] [CrossRef]

- Yüksel, Serhat, Shahriyar Mukhtarov, Elvin Mammadov, and Mustafa Özsarı. 2018. Determinants of profitability in the banking sector: An analysis of post-Soviet countries. Economies 6: 41. [Google Scholar] [CrossRef]

- Zhou, Kaiguo, and Michael CS Wong. 2008. The determinants of net interest margins of commercial banks in mainland China. Emerging Markets Finance and Trade 44: 41–53. [Google Scholar] [CrossRef]

- Zhu, Facang, Qianqian Li, Shichun Yang, and Tomas Balezentis. 2021. How ICT and R&D affect productivity? Firm level evidence for China. Economic Research-Ekonomska Istraživanja 34: 3468–86. [Google Scholar]

| SN | Variable | Type | Code | Definition | Citations |

|---|---|---|---|---|---|

| 1 | Net Interest Margin | DV | NIM | The percentage of net interest earned compared to interest outflow of a bank. | Nariswari and Nugraha (2020), Mahdi and Khaddafi (2020) |

| 2 | Information and Communication Technology | IV | ICT | The term for integrating telecommunication and computer medium mediates hardware and software. It is the expenditure on ICT by banks (in INR). The natural log value is taken. | Sarkar (2012), Adeabah et al. (2021) |

| 3 | Non-performing assets | IV | NPA | It is an advance bank given for which interest or principal payments are overdue for 90 days or more. | Joseph and Prakash (2014), Kiran and Jones (2016) |

| 4 | Sales | CV | Ln_salescr | An indicator of revenue brought in by banks (in INR). | Sanya and Wolfe (2011), Kosach et al. (2019) |

| 5 | Assets | CV | Ln_assetscr | The investments in various asset classes by investing team of banks (in INR). | Wagner (2007), Narula and Singla (2014) |

| Correlation Matrix | ||||||

|---|---|---|---|---|---|---|

| lnICT | lnICT_lnNPA | Ln_sales | ln_asset | Mean | SD | |

| lnICT | 1 | 4.540 | 1.66 | |||

| lnICT_lnNPA | 0.3524 * | 1 | - | - | ||

| Ln_sales | 0.9963 * | 0.2920 * | 1 | 8.74 | 1.61 | |

| ln_asset | 0.8393 * | 0.2700 * | 0.8420 * | 1 | 11.75 | 1.40 |

| DV: NIM | ||||||

|---|---|---|---|---|---|---|

| Model 1 | Model 2 | Model 3 | ||||

| Variable Name | Coefficient | SE | Coefficient | SE | Coefficient | SE |

| Constant | −234.60 * | 129.24 | 6.236 ** | 3.287 | 2.417 *** | 0.3492 |

| lnICT | −56.58 * | 30.705 | - | - | - | - |

| DICT2 | - | - | 5.39 × 10−7 | 6.31 × 10−7 | - | - |

| lnNPA | - | - | - | - | - | - |

| lnICT_lnNPA | - | - | - | - | −0.126 *** | 0.022 |

| ln_sales | 56.96 * | 30.744 | 0.0477 * | 0.2510 | 0.2954 *** | 0.0409 |

| Ln_assets | −0.341 *** | 0.083 | −0.3627 | 0.176 | −0.1669 *** | 0.0517 |

| Part B (Model Estimates) | ||||||

| R-Square | 0.0008 * | 0.0428 * | 0.1231 | |||

| BP-Test | 0.00 (1.00) | 8.53 (0.0017) * | 5.58 (0.0091) * | |||

| Hausman Test | 10.78 (0.0130) * | 1.91 (0.3852) | 13.26 (0.0210) * | |||

| No observations (n) | 300 | 300 | 300 | |||

| DV: NIM | |||

|---|---|---|---|

| Model 1 | Model 2 | Model 3 | |

| Durbin Chi-square | 13.657 (0.0002) * | 5.409 (0.0200) * | 4.697 (0.0302) * |

| Wu Hausman Test | 14.069 (0.0002) * | 5.416 (0.0206) * | 4.692 (0.0311) * |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Thakur, S.; Rastogi, S.; Parashar, N.; Tejasmayee, P.; Kappal, J.M. The Impact of ICT on the Profitability of Indian Banks: The Moderating Role of NPA. J. Risk Financial Manag. 2023, 16, 211. https://doi.org/10.3390/jrfm16040211

Thakur S, Rastogi S, Parashar N, Tejasmayee P, Kappal JM. The Impact of ICT on the Profitability of Indian Banks: The Moderating Role of NPA. Journal of Risk and Financial Management. 2023; 16(4):211. https://doi.org/10.3390/jrfm16040211

Chicago/Turabian StyleThakur, Swapnilsingh, Shailesh Rastogi, Neha Parashar, Pracheta Tejasmayee, and Jyoti Mehndiratta Kappal. 2023. "The Impact of ICT on the Profitability of Indian Banks: The Moderating Role of NPA" Journal of Risk and Financial Management 16, no. 4: 211. https://doi.org/10.3390/jrfm16040211