1. Introduction

The trade-off between risk and return is a fundamental concept in finance. The return on a risk-free asset is a crucial variable in financial equilibrium models, yet its selection and value have been a source of controversy. In the US equity market,

Mehra and Prescott (

1985) and

Weil (

1989) link the problem of a higher equity premium than predicted by theory to the puzzle of why the risk-free rate should be so low. Traditionally, the return on a treasury bill has been used as a proxy for the risk-free rate, but there has been ongoing debate regarding the appropriate tenor of the T-bill. As a result, researchers have utilized treasury securities with various maturities in order to enhance asset pricing models. For instance,

Mehra and Prescott (

1985) utilise a one-year rate, and

Albuquerque et al. (

2016) examine the applicability of 1-, 5-, and 20-year rates.

Barberis et al. (

2015) develop the assumption that a risk-free rate is constant over long periods, whereas

Fama and French (

1993) use a 1-month T-bill rate, which changes each month.

He et al. (

2022) examine gold, T-bills, Interbank Offered Rates (IBOR), and Overnight Index Swaps (OIS) to identify proxies for risk-free assets.

In this paper, we assume that the risk-free rate is constantly changing but question the nature of the asset used to derive this short-term rate. The return on Treasury bills is traditionally used as a risk-free rate in asset pricing models (

Carhart 1997;

Fama and French 1993,

2015,

2018,

2020). Treasury bills are presumed to constitute risk-free investments, since their issuing governments are viewed as ‘default-free’ entities that offer guaranteed investments. If governments default or the possibility of default arises, then their obligations do not remain guaranteed. Even for the United States,

Nippani and Smith (

2010) reveal that Treasury securities are not default-free, as they witnessed observed nonzero Credit Default Swap premia during the financial crisis. The same is doubly true of Treasury securities of less creditworthy states such as Mexico, Greece, Spain, and Italy. In the foundational market model of the Capital Asset Pricing Model (CAPM), the risk-free rate provides the foundation for estimating the cost of equity and the expected returns of risky assets or securities. If Treasury bills do not remain risk-free investments, then the application of the return on Treasury bills may not be the appropriate proxy for the risk-free rate. Given this, it is important to consider alternative assets to determine if they may be more appropriate proxies for the risk-free rate.

Using a correct proxy for the risk-free rate has remained an ongoing topic of debate among academicians and practitioners (

He et al. 2022). In contrast to the return on debt issued by governments, gold has a long history of serving as a financial security and has been used as a form of currency in various countries. Gold has received significant attention in financial markets due to its remarkable performance during the global financial crisis of 2008, and researchers have labeled it a safe-haven asset since it acts as a stabilizing force for financial systems in developed markets (

Baur and Lucey 2010;

Baur and McDermott 2010;

Long et al. 2021). The safe-haven, currency hedging, and diversification benefits of gold during the global financial crisis in 2008 have been reassessed and reaffirmed in other studies (e.g.,

Hoang et al. 2015;

O’Connor et al. 2015). The prior literature also shows a close relationship between the gold return and the return on Treasury bills.

Barro and Misra (

2016) examine the returns on gold and US Treasury bills from 1836 to 2011 and reveal that the real price change in gold is close to the real return on Treasury bills. Additionally, it has been observed that gold prices react swiftly to changes in federal fund rates (

Kontonikas et al. 2013).

Although gold is widely recognized as a safe-haven and hedging instrument, as supported by existing research (

Bekiros et al. 2017;

Faria and McAdam 2012;

Gil-Alana et al. 2015;

He et al. 2018;

Nguyen et al. 2019;

Wu and Chiu 2017;

Cui et al. 2023), there has been a paucity of literature examining the use of gold as a zero-beta asset in asset pricing models. Previous studies by

He et al. (

2018,

2022) have explored gold, T-bills, Interbank Offered Rates (IBOR), and Overnight Index Swaps (OIS) to identify suitable proxies for risk-free assets. They have found that gold can serve as a proxy for risk-free assets in the United Kingdom and China, while for T-bills in Japan and IBOR in China. However, these studies fail to provide evidence for an appropriate proxy for the US market when applying a single-factor CAPM on a sample of S&P 500 stocks.

Therefore, this paper extends the existing empirical research by thoroughly investigating the applicability of gold as a zero-beta asset in traditional asset pricing models, utilizing a wide range of test assets in the US equity market. In the spirit of

Black et al. (

1972, hereafter BJS) and

He et al. (

2018), we use the returns on gold as the return on a zero-beta asset. Several studies have found gold to have a zero beta with respect to the market, as evidenced by

Jaffe (

1989),

Chua et al. (

1990),

McCown and Zimmerman (

2006),

Baur and McDermott (

2010),

Blose (

2010),

Reboredo (

2013),

He et al. (

2018).

Research by

Wang et al. (

2011) and

Ntim et al. (

2015) indicates weak-form efficiency in the US gold market, which is a desirable feature for assets to satisfy Arrow–Debreu conditions. This finding suggests that gold returns may be a better candidate to satisfy these conditions compared with the returns on Treasury bills, as noted by

Constantinides and Duffie (

1996). Before using gold in asset pricing models in the US equity market, we examine the criteria of the BJS’s zero-beta rate, specifically that gold shows zero beta, minimum variance, and efficiency. To this end, we perform variance-ratio tests to assess the efficiency of the gold market. Furthermore, we plot the minimum variance Frontier by using gold returns and different sets of test portfolios to test the criteria of the zero-beta rate.

Our study contributes to the existing literature in several significant ways. Firstly, we employ gold as a zero-beta asset in traditional asset pricing models on a wide range of test assets in the US equity market. We demonstrate that using gold in this way is preferable to the traditional use of the yield on a 1-month T-bill as a risk-free rate, which has significant theoretical limitations in terms of its suitability as a risk-free return. Secondly, we show that the return on gold lacks the shortcomings associated with T-bills and is therefore preferable on theoretical grounds. Furthermore, we find that asset pricing models which use gold as a zero-beta asset have better time-series and cross-sectional performance than traditional models using the T-bill risk-free rate. Thirdly, we investigate the extended

Carhart (

1997) and

Fama and French (

1993,

2015,

2017) models, ranging from three factors to six factors. To the best of our knowledge, no other paper has compared these six extended factor models together in a single study. We also conduct our analyses using both time-series and cross-sectional data. It is worth noting that our study is limited to using gold returns as a proxy for the zero-beta rate, rather than considering a portfolio of risky securities as proposed by

Black et al. (

1972) in their original zero-beta model. Our study assumes that using a zero-beta rate based on gold has advantages over a portfolio of risky assets due to gold’s traditional and historical safe-haven abilities. A portfolio of risky assets still faces a risk of losing its value in different time periods, whereas gold has maintained its reputation of retaining its value over centuries.

In the field of asset pricing, gold has been traditionally used in the

Merton (

1973) ICAPM framework to examine gold factor exposures in industry equity portfolio returns (

Chan and Faff 2002;

Davidson et al. 2003). However, we advance upon these by examining the employment of the gold return as a replacement for the risk-free rate, hitherto unexplored in the asset pricing literature. Furthermore, we provide a comprehensive comparison of the traditional

Fama and French (

1993,

2015,

2017) and

Carhart (

1997) models with those that employ gold as a zero-beta asset on an extensive range of test assets. For robustness and ease of comparison with

Fama and French (

2015), we assess the performance of these asset pricing models with and without small stocks and demonstrate improved pricing of small stocks.

Ang et al. (

2006) use a volatility factor to improve the performance of the

Fama and French (

1993) three-factor model on portfolios sorted by cash-flow volatility, and in a similar vein, we examine gold as a zero-beta asset to price portfolios sorted by variance. BJS relax the CAPM assumption that investors can borrow and lend freely and to an unlimited extent at the risk-free rate, as well as examine the CAPM with limited borrowing, permitting investors to lend but not borrow at the zero-beta rate. Similarly, we restrict investors from investing but not borrowing at the gold return rate.

Our results show that, in time series, models that employ gold as a zero-beta asset exhibit higher R-squared values, lower Sharpe ratios of alphas, and fewer significant pricing errors. We find that such models are better able to price portfolios of small stocks, where traditional models struggle. In cross-section, we find fewer cross-sectional pricing errors and economically plausible values of the market risk premium appearing for test assets where traditional models generate implausible negative prices of market risk. We show that the CAPM, the

Fama and French (

1993) three-factor model, the

Carhart (

1997) four-factor model, and the

Fama and French (

2015) five-factor model all exhibit improved asset pricing performance when using gold as a zero-beta asset. Furthermore, we find that there is information in the return on gold beyond that captured by the

Carhart (

1997) factors, as a gold return factor constructed to be orthogonal to these remains significant in cross-section when added to the

Carhart (

1997) model. This suggests that the use of gold as a zero-beta asset in asset pricing models captures additional variance not encompassed by the traditional factors. Overall, our study highlights the advantages of using gold as a zero-beta asset in equity asset pricing models and provides evidence for its superior performance over the traditional use of the yield on a 1-month T-bill as a risk-free rate.

The structure of this paper is as follows:

Section 1 introduces the problems associated with the risk-free rate in empirical asset pricing and highlights the efficiency, hedging, and zero-beta characteristics of gold.

Section 2 presents the theoretical framework of the zero-beta CAPM, explains the development of the extended versions of the traditional CAPM model, and discusses the relationships between interest rates, Treasury bills, gold, and stock prices.

Section 3 describes the data used, and

Section 4 briefly covers the methodology of the asset pricing tests.

Section 5 presents the empirical findings, and

Section 6 concludes.

5. Empirical Results

Descriptive Statistics: In the below, we compare the relative performance of the CAPM, the three-, four-, five-, and six-factor models with the G-CAPM, the G-three-, G-four-, G-five-, and G-six-factor models in pricing US equities. We begin the empirical analysis by assessing the summary statistics for the independent variables in the time-series regressions.

In

Table 1, we report the summary statistics and pairwise correlations for the return on gold, Treasury bills, the excess market return, the difference between the return on gold and the return on Treasury bills (

), SMB, HML, RMW, CMA, and MOM. In

Table 1, the return on Treasury bills shows a significantly positive mean return, whereas the average gold return is insignificantly positive and is lower than that of Treasury bills. However, the standard deviation and kurtosis of the gold return are much higher than that of Treasury bills due to its higher volatility. The higher kurtosis for gold shows the ability of gold to react swiftly in the wake of market uncertainty. On the other hand, the gold return has a much lower skewness than Treasury bills. In Panel B, the correlation matrix shows a near-zero correlation between the excess gold return and the excess market return. Furthermore, the correlation of gold with the Fama–French and Carhart (momentum) factors is very close to zero. Panel C reports the results of the regression:

for the 420 months from January 1981 to December 2015. In line with previous studies (

Jaffe 1989;

Chua et al. 1990;

McCown and Zimmerman 2006), we find that the return on gold has a market beta which is almost exactly equal to zero for this period, and hence verify that it is a suitable zero-beta asset.

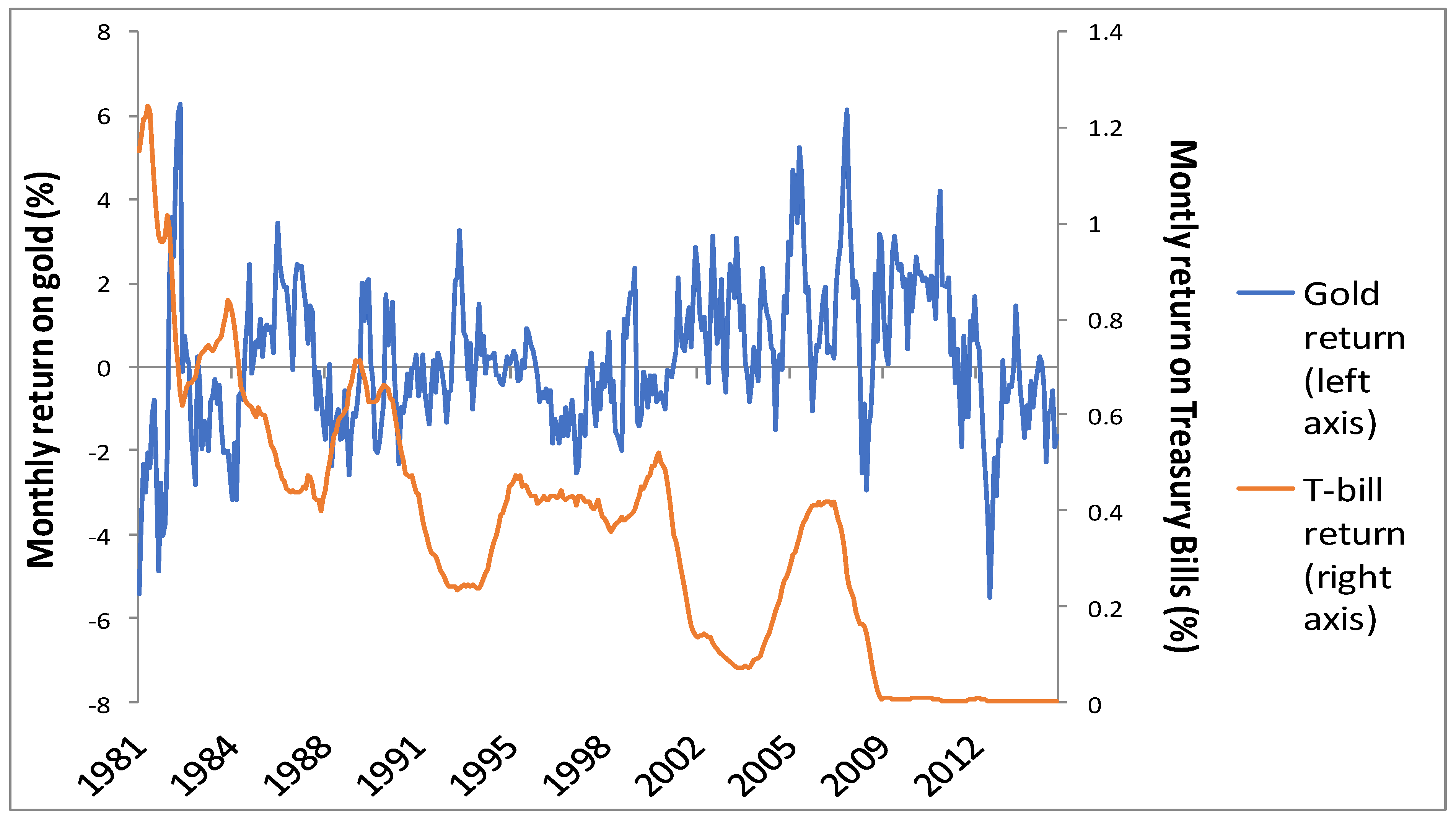

In

Figure 1, we use 6-month moving averages of the 1-month returns on gold and Treasury bills to illustrate their trends in different time periods. The returns on gold and Treasury bills have always tended to move in opposite directions, widening during periods of financial crisis, e.g., the stock market crash of 1987, the Mexican peso crisis in 1994, the dot-com bubble in 1993, and the global financial crisis of 2008. This flight-to-safety feature of gold makes it a safe-haven asset during times of market turmoil and crisis, as argued by

Baur and Lucey (

2010),

Baur and McDermott (

2010),

Kontonikas et al. (

2013), and

O’Connor et al. (

2015).

Market Efficiency Tests: Firstly, we use

Lo and MacKinlay (

1988) parametric variance-ratio tests and

Wright (

2000) nonparametric variance-ratio tests to examine the efficiency of gold price series. Results are shown in

Table 2, where q shows a number of days, and M1 and M2 show results of the parametric

Lo and MacKinlay (

1988) test. M1 tests the

RWS hypothesis and M2 tests the

MDS hypothesis. R1, R2, and S1 are the ranks and signs of the nonparametric test of

Wright (

2000). R1 and R2 show ranks and test the random walks (RWS), and S1 is the sign that tests the martingale sequence difference hypothesis (MDS).

Lo and MacKinlay’s (

1988) parametric and

Wright’s (

2000) nonparametric tests do not reject the null hypotheses of random walks

(RWS) and martingale difference sequence (

MDS) and confirm the weak-form efficiency of the gold price series.

We further perform the multiple variance-ratio tests of

Whang and Kim (

2003) using three different time periods (1981–2015, 1990–2015, and 2000–2015) by using six different subsamples. The sampling periods are chosen by using the rule cited in

Whang and Kim (

2003).

3 It allows us to deeply investigate market efficiency, as this procedure allows multiple subsampling to test weak-form efficiency. Results are reported in

Table 3 and show that the efficiency of the gold market greatly increased from 2000 onwards. These results are consistent with results of

Wang et al. (

2011), who found that gold markets achieved greater efficiency after 2000 in the US gold market. This efficiency improves from 1990 onwards and becomes even stronger from 2000 onwards.

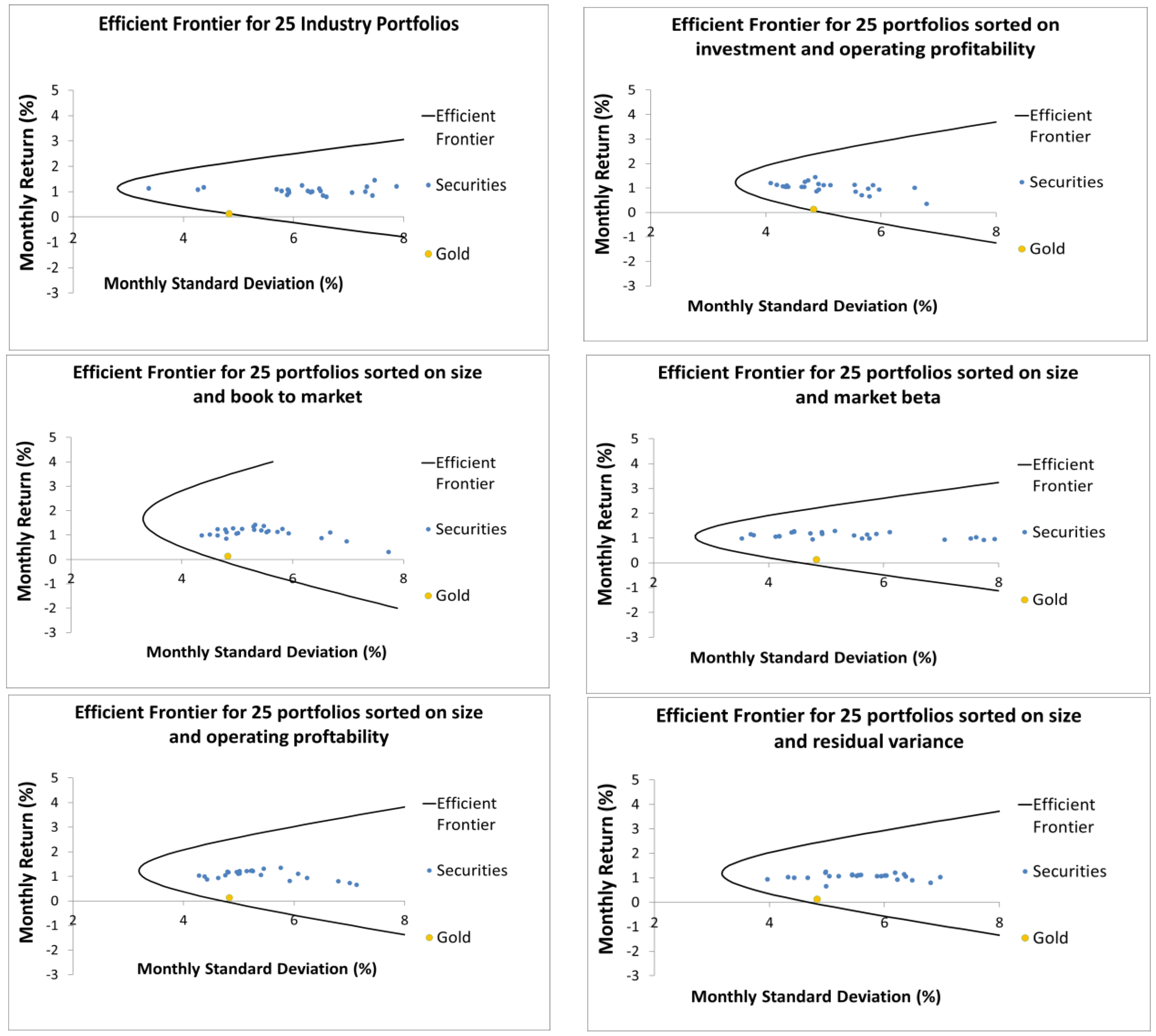

Minimum Variance Efficient Frontier: Gold must be located on minimum variance frontier to satisfy the conditions of

Black et al. (

1972). Contrary to Treasury bill yield, gold exhibits higher volatility, and this study underlines this limitation and does not attempt to use gold as a risk-free asset.

4 Instead, it explores the applicability of gold as a zero-beta asset in a comparative vein of

Black et al. (

1972). Hence, this study is unique and distinct from

Black et al. (

1972). However, we still consider the restriction that gold must be located on the efficient frontier to be qualified as a potential zero-beta asset that may replace a risk-free rate or zero-beta portfolio in empirical asset pricing models.

Our study employs the methods of

Clarke et al. (

2006) and

Kan and Smith (

2008) to estimate the minimum variance frontier, and our results are presented graphically in

Figure 2. The figure illustrates the position of gold on the minimum variance efficient frontier when plotted against various factors, including the 25 industries, the 25 investment and operating profitability, the 25 size and book-to-market, the 25 size and market beta, the 25 size and operating profitability, and the 25 size and residual variance portfolios. Our analysis shows that gold is located close to the minimum variance frontier when plotted against the 25 size and book-to-market, the 25 size and market beta, the 25 size and operating profitability, and the 25 size and residual variance portfolios. However, when plotted against the 25 industries and the 25 investment and operating profitability portfolios, gold is located directly on the minimum variance frontier. These findings suggest that the potential use of gold return as a zero-beta rate warrants further examination to enhance the pricing of industries, investment, and profitability portfolios.

Tests of Factor Models: We begin our analysis by using the returns on the 49 industry portfolios as test assets, since significant industry portfolio exposures to a gold return factor have already been found in the ICAPM framework (

Chan and Faff 2002;

Davidson et al. 2003).

Table 4 and

Table 5 report the time-series regression alphas, t-statistics, and R-squared values for the CAPM, three-factor, four-factor, and five-factor models, together with their gold analogues, while

Table 6 reports GRS test statistics, the mean-adjusted R-squared, and mean absolute alpha. These results show that first-stage pricing errors are reduced, and R-squared values are substantially improved when gold is used as a zero-beta asset, compared with the conventional models.

We find that gold zero-beta models outperform traditional models, having lower GRS test scores and higher mean-adjusted R-squared values. Wald statistics of the GRS test show that gold is a better proxy of the zero-beta rate than the yield on 1-month T-bills when we apply CAPM and the traditional multifactor models on industry portfolios. Though the single-factor CAPM and G-CAPM, both pass the GRS test at the 5% level, we observe that the gold zero-beta models have a lower number of significant pricing errors compared with the traditional models. For instance, while the single-factor G-CAPM produces four significant pricing errors, the traditional CAPM produces seven. For each model in turn, we obtain fewer significant pricing errors and higher times-series R-squared values by using the gold return in place of the T-bill yield.

Table 7 shows the second-stage

Fama and MacBeth (

1973) regression results for the 49 industry portfolios. We obtain a positive market risk premium for the G-CAPM with an insignificant cross-sectional alpha, whereas the traditional CAPM produces an implausible negative market risk premium with a significant cross-sectional alpha, showing that the single-factor CAPM improves with gold as a zero-beta asset. While we obtain insignificantly positive market risk premia for both the traditional four-factor model and its gold analogue, we find that the gold model performs better, since it has an insignificant second-stage alpha, whereas that for the conventional model is significant. While the traditional five-factor model performs better than the traditional four-factor model since it has an insignificant alpha with a positive market risk premium, its gold analogue is still superior since it has a higher R-squared. We note that the average cross-sectional R-squared is higher for the single-, three-, four-, and five-factor models when we use gold as a zero-beta asset with industry portfolios.

In unreported results from robustness checks, we also estimate models with Generalized Method of Moments (GMM), adopting the

Cochrane (

2009) methodology and with Generalized Least Squares (GLS) by using the

Kan et al. (

2013) procedure. These results are qualitatively similar in terms of demonstrating the advantages of the gold zero-beta asset model and are available from authors on request. Having compared the performance of industry portfolios as test assets, we now move to compare the performance of test portfolios sorted by size and book-to-market ratio.

Table 8 shows the time-series alphas, t-statistics, and R-squared values for the CAPM, three-factor, four-factor, five-factor, and six-factor models and their gold analogues. The comparison of the traditional and the gold zero-beta models shows that pricing errors are reduced, and R-squared values are improved when the gold return is used as a zero-beta asset. Like BJS, we find that gold zero-beta models produce significantly negative alphas for small, low book-to-market portfolios and positive alphas for high book-to-market portfolios.

Table 9 presents a summary of GRS test results for traditional CAPM and gold zero-beta models. We estimate models with (denoted 5 × 5) and without microcaps (denoted 4 × 5) to assess whether our zero-beta models enable us to price smaller stocks, which have been reported as challenging and difficult to price by traditional models (

Fama and French 2012). We show results in four pairs of columns, contrasting results from traditional and gold zero-beta models, with and without microcaps. Compared with traditional CAPM models, we obtain higher R-squared and lower Sharpe ratio of alphas with zero-beta models. In particular, for the six-factor model, we find improved performance with the gold zero-beta model, obtaining only four significant pricing errors compared with eight with the traditional model.

Table 10 reports the second-stage cross-sectional results for traditional and gold zero-beta models for portfolios sorted by size and book-to-market. In the cross-sectional analysis, a gold zero-beta six-factor model outperforms, as it produces much lower cross-sectional alphas while having only a marginally smaller R-squared.

Fama and French (

2012,

2015) find that the four-factor model does a better job in explaining average returns in the US market than other models. We therefore compare the performance of traditional and zero-beta G-four-factor models on different sets of test portfolios.

Table 11, Panel A presents a summary of GRS test results for the traditional and gold zero-beta four-factor models for test assets of 25 portfolios, sorted, respectively, by size and momentum, size and investment, and size and operating profitability. Panel B presents results on sets of 25 portfolios, sorted, respectively, by size and accruals, size and variance, size and residual variance, and size and market beta. Panel C presents results on three sets of 32 portfolios sorted simultaneously by size, book-to-market, and operating profitability, by size, book-to-market, and investment, and by size, operating profitability, and investment, respectively, while Panel D presents results for test assets of 35 portfolios sorted by size and net share issues. We do not report the alpha coefficients, t-statistics, and R-squared values for space reasons but only report the summary statistics, namely the GRS test score, mean-adjusted R-squared, Sharpe ratio of alphas, and number of significant alpha coefficients across all test portfolios. The performance of the zero-beta G-four-factor models remains superior across all test portfolios, since we obtain higher mean-adjusted R-squared values and a lower Sharpe ratio of alphas with gold zero-beta models. Furthermore, the zero-beta G-four-factor models produce fewer significant pricing errors on all test portfolios. However, the traditional and gold zero-beta four-factor model succeeds in passing the GRS test only on the size and book-to-market portfolios, whereas the zero-beta four-factor model produces just two pricing errors compared with five with the traditional four-factor model. As expected, performance is considerably improved when microcaps are omitted for both traditional and zero-beta models.

Table 12 assesses the ability of traditional and zero-beta four-factor models to explain the cross-section of returns on the portfolios explored above. The traditional four-factor model does a reasonable job, as we cannot reject the null hypothesis that second-stage pricing errors are significantly different from zero. In general, for the traditional four-factor model, we obtain an insignificantly positive estimate of the market risk premium and an insignificant cross-sectional alpha. The exceptions are for the 25 size and residual variance portfolios and the 32 size, book-to-market, and investment portfolios, where we find alphas for the traditional model are significant, and the market risk premia are negative, contrary to theory. However, in these instances, we find that the corresponding gold zero-beta model succeeds, having insignificant alphas and a positive estimate of the market risk premium, in line with the theory.

Satisfyingly, we obtained a positive estimate of the market risk premium with the gold zero-beta four-factor model on all test portfolios. The estimate of the market risk premium is significant on the 25 size and momentum and 32 size, book-to-market, and investment portfolios. However, when we exclude microcap portfolios, we obtain insignificantly positive cross-sectional market coefficients. These results are similar and comparable to the traditional four-factor model. We infer from this that employing gold as a zero-beta asset helps to price smaller stocks.

Kothari et al. (

1995) find that the conclusions made using CAPM tests are sensitive to the time period employed. We therefore perform a subperiod analysis and find that zero-beta models perform better during periods of market uncertainty. The results are not reported, but they are available from the authors on request.

As a robustness test, we derive the orthogonalized gold residual factor,

, as above, and include it as a fifth factor in the traditional four-factor model for portfolios sorted by size and momentum in order to test whether the return on gold contains additional explanatory power beyond the four-factor model.

Table 13 demonstrates that this residual factor

is significant in cross-section and therefore adds significant information beyond the four-factor model in explaining portfolio returns.

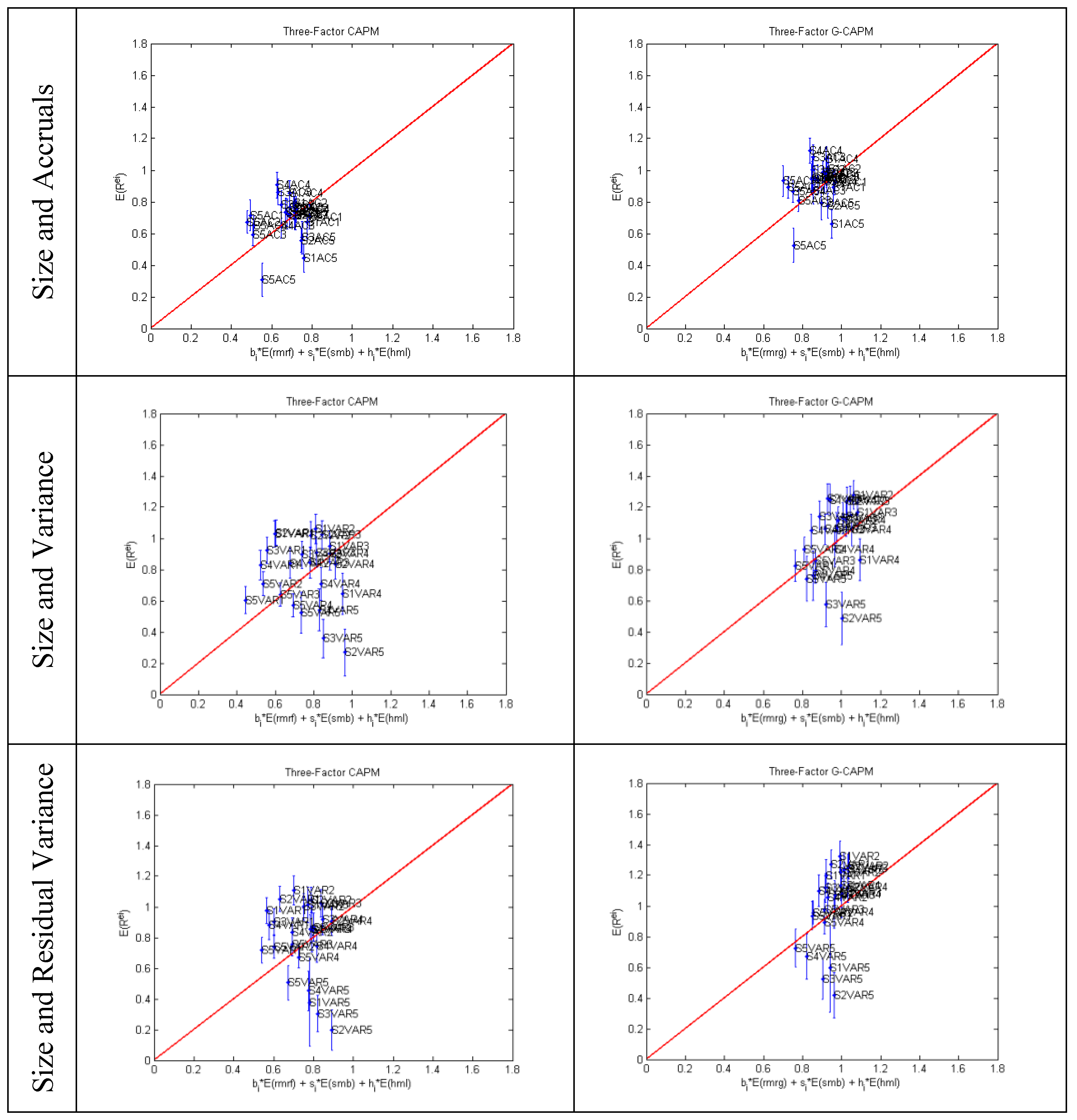

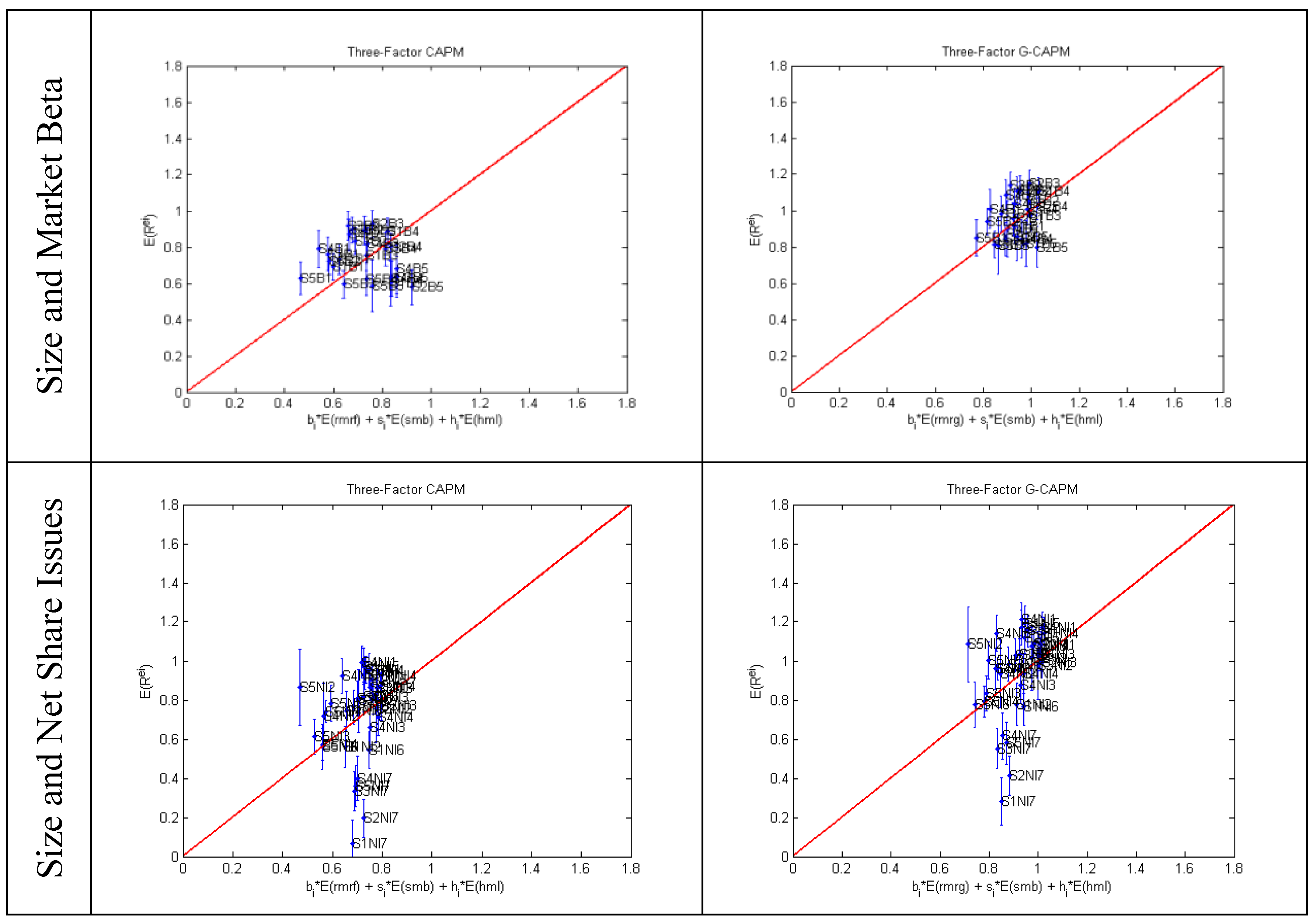

After assessing the performance of the gold zero-beta four-factor model, we assess the performance of the three-factor gold zero-beta model against the traditional three-factor model on test assets of the 25 portfolios sorted, respectively, by size and accruals, by size and variance, by size and residual variance, and by size and market beta, as well as 35 portfolios sorted by size and net share issues. The results of the GRS test in

Table 14 show that the gold zero-beta three-factor model produces a lower Sharpe ratio of alphas

SR(a) and higher adjusted R-squared values on all test portfolios compared with the traditional three-factor model. The zero-beta three-factor model passes the GRS test at the 5% level on the size and market beta portfolios, whereas the traditional three-factor model fails the GRS test on these assets, with and without microcaps. Furthermore, the zero-beta G-three-factor model produces fewer significant pricing errors on all test portfolios, particularly on portfolios sorted by size and net share issues, whereas it only produces six significant time-series alphas, compared with fifteen with the traditional three-factor model.

Table 15 shows that the gold zero-beta three-factor model performs better in explaining cross-sectional returns than the traditional three-factor model on test portfolios which are not sorted by the Fama–French factors. For the traditional model, we obtain significant cross-sectional alphas for portfolios sorted by size and variance, by size and residual variance, and by size and net share issues at the 5% level. By contrast, the gold zero-beta three-factor model on these test assets yields insignificant cross-sectional alphas. Furthermore, the traditional three-factor model produces an implausibly negative estimate of the market risk premium, whereas the gold zero-beta three-factor model produces an insignificant but economically plausible and positive estimate for all test portfolios, except for those sorted by size and accruals. When we exclude microcaps, we obtain similar and comparable estimates for the traditional and gold zero-beta three-factor models, showing that gold as a zero-beta factor improves the pricing of microcaps in particular. The actual and predicted returns estimated from traditional and zero-beta three-factor models are graphically shown in

Figure 3.

We also examine the applicability of gold as a zero-beta asset on the

Fama and French (

2015) five-factor model. The results are shown in

Table 16 in four pairs of columns for comparison, as before. Panel A shows results for test assets of 25 portfolios, sorted by size and momentum, by size and investment, and by size and operating profitability. We find relatively lower Sharpe ratios of alphas

SR(a) with the gold zero-beta five-factor model and higher mean-adjusted R-squared values compared with the traditional five-factor model, showing that the gold zero-beta model performs notably better. For instance, for the G-five factor model, we obtain an R-squared of 0.90 on the 25 size and momentum portfolios, as compared with 0.84 for the traditional five-factor model; for the G-five-factor model, we obtain an R-squared of 0.96 on portfolios sorted by size and investment and size and operating profitability, as compared with 0.92 for the traditional five-factor model. In Panel B, the traditional five-factor model produces ten significant alphas for the 32 portfolios sorted by size, book-to-market, and operating profitability, whereas the G-five-factor model produces only seven significant alphas. It also yields a lower Sharpe ratio

SR(a) of alphas than the traditional five-factor model. The G-five-factor similarly outperforms the 35 portfolios sorted by size and net share issues.

Table 17 reports the second-stage results for the above regressions and assesses the ability of the traditional and G-five-factor models to explain returns in cross-section. For the traditional five-factor model, we reject the null hypothesis that pricing errors are insignificantly different from zero for the 25 size and investment portfolios at the 5% significance level. In panel B, we likewise reject this null hypothesis for the 32 size, book-to-market, and investment portfolios. We also obtain an implausibly negative estimate of the market risk premium for the traditional five-factor model on the 25 size and momentum, 25 size and investment, and 32 size, book-to-market, and investment portfolios.

The G-five-factor model performs much better: the only portfolio where we can reject the null hypothesis of zero pricing errors at the 5% level is for the 25 size and momentum portfolios. Additionally, we obtain an insignificantly positive estimate of the market risk premium on the 25 size and investment portfolios and a significantly positive estimate for the 25 size and momentum portfolios and for the 32 size, book-to-market, and investment portfolios. In summary, we find that the G-five-factor model does a better job in the portfolios where the traditional five-factor model struggles to explain the cross-section of returns.

6. Conclusions and Areas for Future Research

Our findings indicate that the gold zero-beta models can play a significant role in enhancing the empirical performance of asset pricing models. This study attempts to improve the estimation of expected returns for a wide range of portfolios of US stocks over a 35-year time sample by utilizing gold as a zero-beta asset. We used the price of a fixed weight of gold in lieu of a 1-month T-bill. By using gold returns as a substitute zero-beta rate, we transform all asset prices into units of a fixed weight of gold, as we quote stock prices in terms of ounces of gold rather than quoting in units of Treasury bills. This approach allows for the development of an alternative and parallel technique for estimating stock returns with asset pricing models. Wald statistics of the GRS tests show that gold is a better proxy of the zero-beta rate than the yield on 1-month T-bills when we apply CAPM and the traditional multifactor models on the US industry portfolios and the 25 test portfolios sorted by size and market beta. Overall, empirical findings indicate that asset pricing models employing gold as a zero-beta asset in place of the conventional T-bill risk-free rate have superior time-series and cross-sectional performance.

Our primary findings pertain to the three-factor, four-factor, and five-factor models. For all these, we find that when we use gold as a zero-beta factor in place of the T-bill yield as a risk-free rate, we obtain higher mean-adjusted R-squared values and lower Sharpe ratios of alphas in time series. This indicates that gold as a zero-beta asset improves the time-series performance of traditional empirical factor models. In the second-stage, cross-sectional results, we find that the use of gold as a zero-beta factor brings improvements in two areas. Firstly, our findings suggest that gold as a zero-beta asset can be used to enhance the pricing of smaller stocks, as gold zero-beta models generate economically plausible prices of market risk on test assets, including microcaps, when traditional models with T-bill rates as risk-free assets tend to fail to do so, resulting in negative estimates of the price of market risk. Secondly, we find that using gold as a zero-beta asset reduces the magnitude of pricing errors where traditional models exhibit significant cross-sectional pricing of the intercept.

We also identify the specific test assets on which the gold zero-beta models clearly outperform traditional models. Firstly, the G-four- and five-factor models demonstrate superior performance for portfolios sorted by industry, size, and momentum, as well as for portfolios simultaneously sorted by size, book-to-market, and investment. Secondly, the G-three-factor model performs better for portfolios sorted by size and variance, size and residual variance, and size and market beta. The inclusion of gold as a zero-beta factor in security analysis may provide an alternative estimate for determining whether securities are undervalued or overvalued, and thus may aid investors in making more informed investment decisions. The findings of this research can be valuable for policymakers in making central bank rate-setting decisions and for regulatory bodies in framing appropriate regulations during abrupt market conditions. The use of gold as a zero-beta factor in asset pricing models has the potential to act as a ‘whistleblower’ for regulatory authorities, helping to implement effective policies during periods of financial and economic crises. Subperiod analyses provided improved estimates of market risk; however, these results are not presented in this paper but can be made available upon request from the authors.

In terms of security analysis, utilizing gold as a zero-beta asset may provide an alternative estimate for assessing whether securities are undervalued or overvalued. This can assist investors in making rational investment decisions. Furthermore, utilizing gold as an alternative to the Treasury bill rate may help overcome the empirical weaknesses of factor models during periods of market volatility and uncertainty, as it obtains better estimates of the actual market returns in small and large datasets. The precise estimation of returns made possible through the use of gold zero-beta models can enable investors to assess whether securities are appropriately priced when making investment decisions. Additionally, as mentioned earlier, gold zero-beta models may work as a whistle-blower for regulatory authorities as it can help them to determine the fair return on Treasury bills.

Our paper suggests several potential avenues for future research. Firstly, it is conjectured that gold zero-beta models may be particularly useful during financial crises and pandemics when the risk-free rate, as measured by T-bills, tends to be artificially depressed below the natural risk-free rate as a policy measure. As such, these models may be doubly useful to investors and regulatory authorities during such periods. We strongly argue that gold as a zero-beta asset can be equally useful during periods of pandemics and market volatility, as gold prices swiftly react and adjust prices in response to uncertain market conditions. Secondly, the validity of gold zero-beta models needs to be assessed on markets other than the US to avoid accusations of data snooping, which may arise if only one market is investigated. Thirdly, as recent research suggests that forecasting models can predict future gold prices (

Wang et al. 2011;

Mihaylov et al. 2015), the findings of this paper open prospects for future research in predicting market booms and crashes. Finally, other statistical modeling techniques, such as neural networks (e.g.,

Guresen et al. 2011;

Khashei and Bijari 2014) and gene expression programming, as well as more conventional econometric modeling methods such as GMM and novel models such as ILCC (

Liang et al. 2022), Bidirectional Long Short-Term Memory Network (BiLSTM), Attention Mechanism, Convolutional Neural Network (CNN) (

Lin et al. 2022a), and the VMD-AR-IBiLSTM-ELMAN model with asymmetric features and nonlinear integration approach (

Lin et al. 2022b) could be applied to assess whether different results are obtained.

It is important to acknowledge the limitations of this study. The use of gold returns as a proxy for the zero-beta rate, rather than a portfolio of risky securities, restricts the generalizability of the results to other assets. However, the study assumes that gold has unique properties that make it a suitable proxy for the zero-beta rate, including its reputation as a safe-haven asset. Despite this, the study cannot claim that gold is a completely risk-free asset, and further research is needed to determine the effectiveness of using gold as a proxy for the risk-free rate across different markets and asset classes. Moreover, the study is limited to the US equity market and may not be generalizable to other regions or markets. Additionally, the study only considers a limited number of test assets and may not account for the full range of asset classes available to investors. Finally, the study’s findings may be sensitive to the time period and sample used, and future research should consider these factors when applying the results.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}