The Impact of M&As on Shareholders’ Wealth: Evidence from Greece

Abstract

:1. Introduction

2. Literature Review

3. Research Design

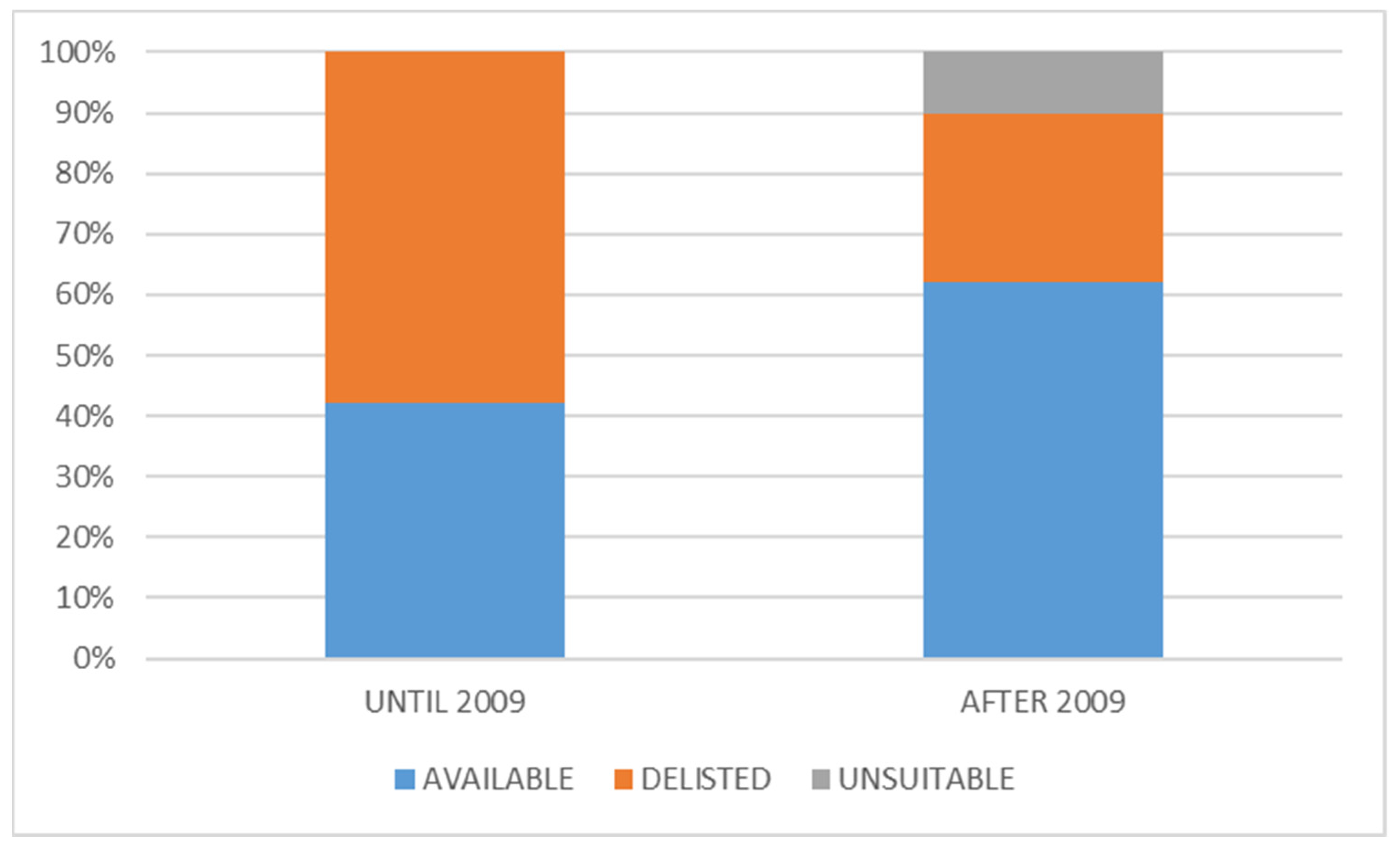

3.1. Data Sampling

3.2. Selection of Statistical Model

4. Empirical Data Analysis and Discussion

4.1. Normal Distribution Tests

4.2. Descriptive Statistics

4.3. Findings on Abnormal Returns

4.3.1. Daily Abnormal Returns

4.3.2. Cumulative Abnormal Returns

4.4. Discussion

The Effect of the Recent Crisis on Value Creation of Greek Bidders

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

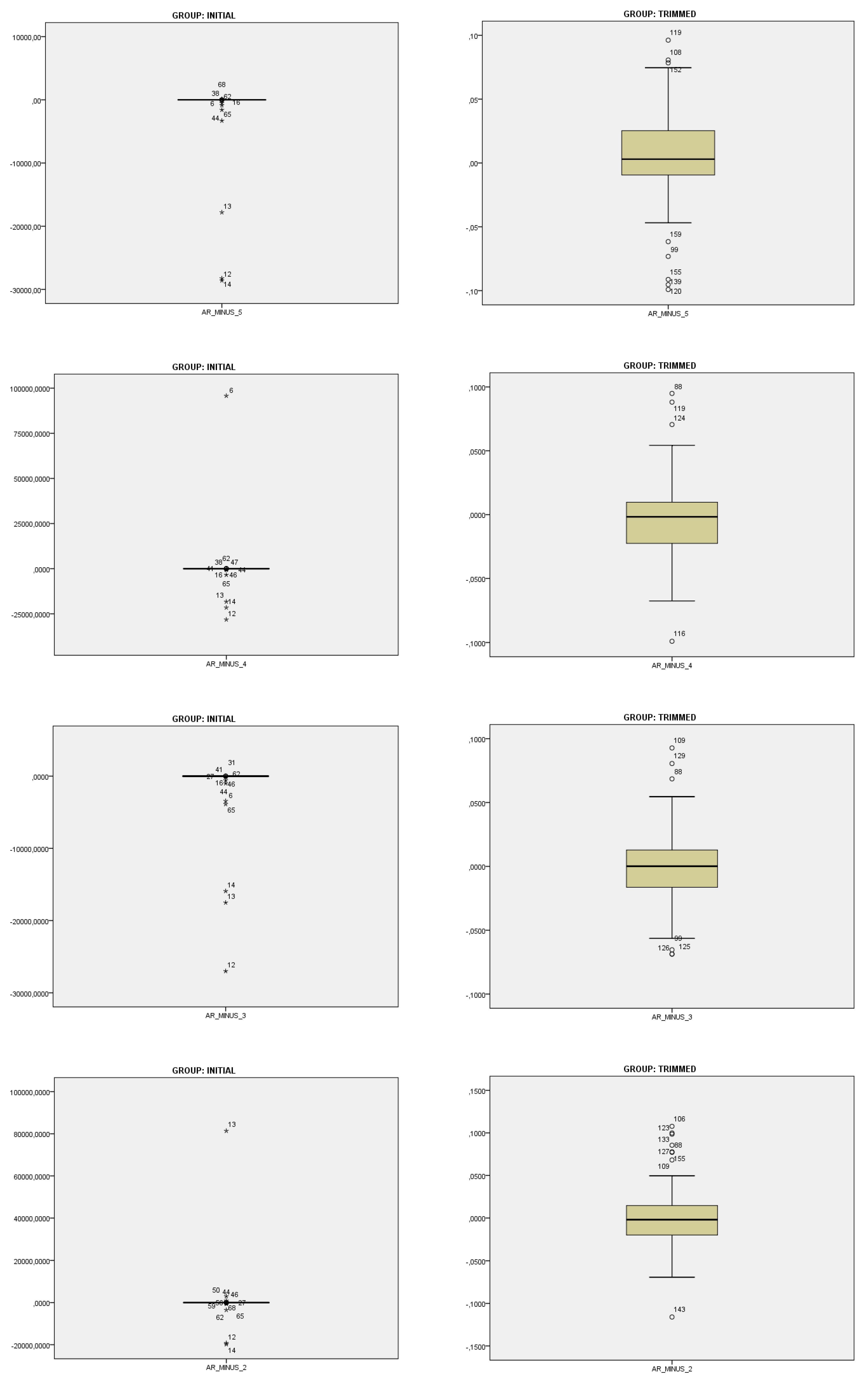

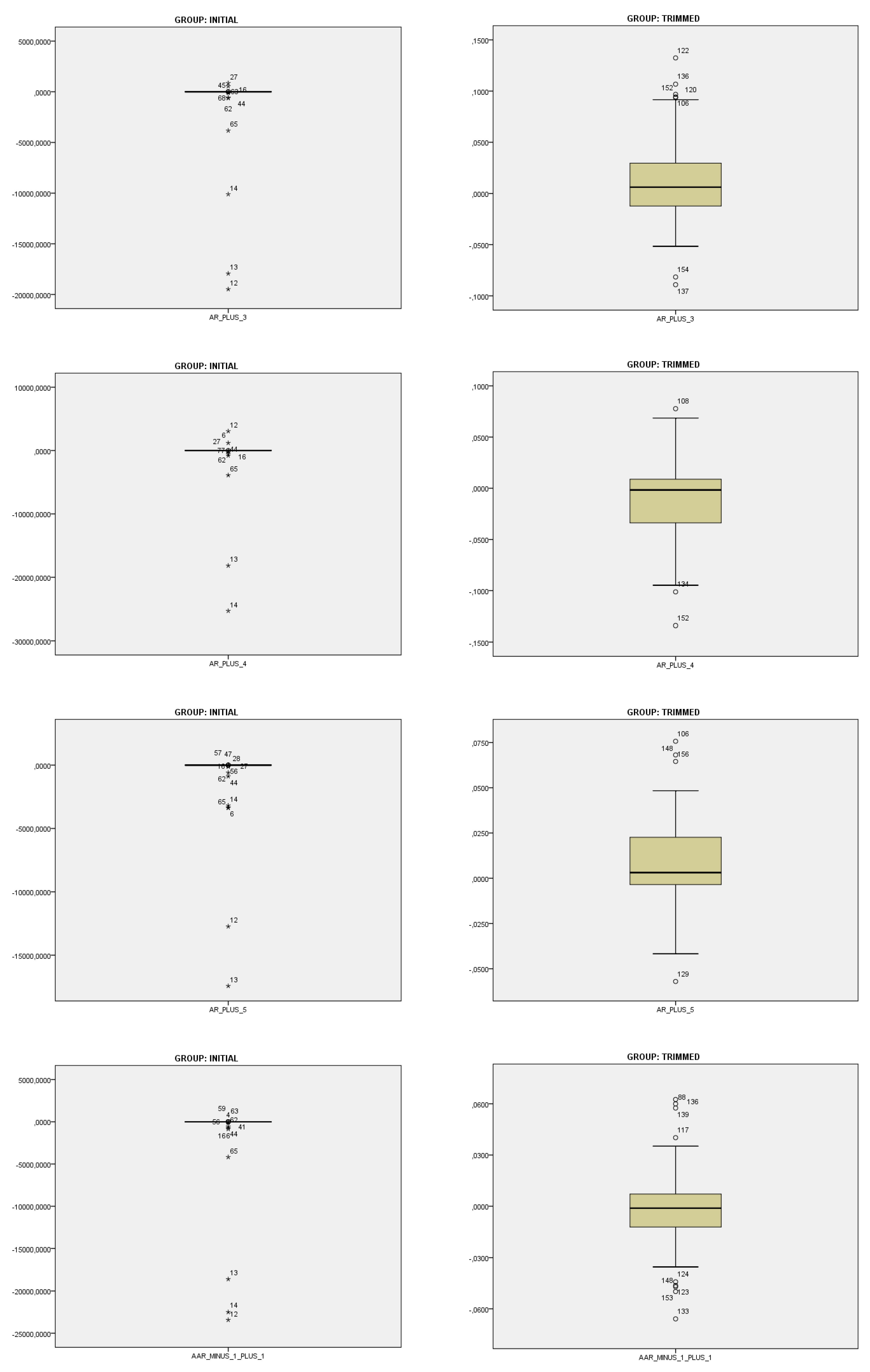

Appendix A. Boxplots of Initial and Trimmed Data

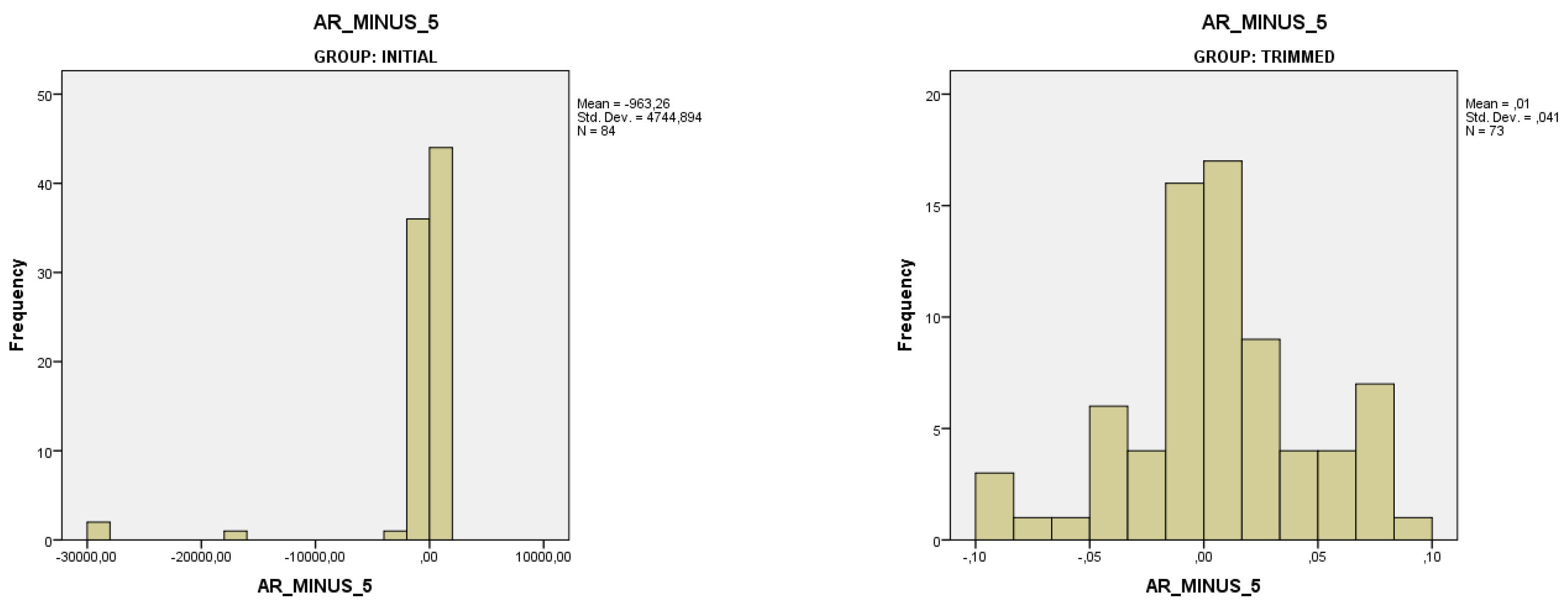

Appendix B. Histograms of Initial and Trimmed Data

References

- Agrawal, Anup, Jeffrey F. Jaffe, and Gershon N. Mandelker. 1992. The post-merger performance of acquiring firms: A re-examination of an anomaly. Journal of Finance 47: 1605–21. [Google Scholar] [CrossRef]

- Antoniou, Antonios, Philippe Arbour, and Huainan Zhao. 2006. The Effects of the Cross-Correlation of Stock Returns on Post Merger Stock Performance. EFMA Basel Meetings Paper. Basel: EFMA Basel. [Google Scholar] [CrossRef]

- Arasa, Oirere David. 2020. Effect of Mergers and Acquisition on Shareholders Wealth of Listed Firms at Nairobi Securities Exchange, Kenya. Journal of Economics and Finance 11: 24–32. [Google Scholar]

- Asquith, Paul. 1983. Merger bids, uncertainty, and stockholder returns. Journal of Financial Economics 11: 51–83. [Google Scholar] [CrossRef]

- AT Kearney, Inc. 1999. Corporate Marriage: Blight or Bliss? A Monograph on Post-Merger Integration. Chicago: A.T. Kearney. [Google Scholar]

- Bradley, Michael, Anand Desai, and E. Han Kim. 1988. Synergistic gains from corporate acquisitions and their division between the stockholders of target and acquiring firms. Journal of Financial Economics 21: 3–40. [Google Scholar] [CrossRef] [Green Version]

- Brealey, Richard A., Stewart C. Myers, and Alan J. Marcus. 2001. Fundamentals of Corporate Finance, 3rd ed. New York: McGraw-Hill. [Google Scholar]

- Brown, Stephen J., and Jerold B. Warner. 1980. Measuring security price performance. Journal of Financial Economics 8: 205–58. [Google Scholar] [CrossRef]

- Brown, Stephen J., and Jerold B. Warner. 1985. Using daily stock returns: The case of event studies. Journal of Financial Economics 14: 3–31. [Google Scholar] [CrossRef]

- Chakrabarti, Rajesh, Swasti Gupta-Mukherjee, and Narayanan Jayaraman. 2005. Mars-Venus Marriages: Culture and Cross-Border M&A. SSRN Electronic Journal 40: 216–36. [Google Scholar] [CrossRef]

- Chang, Saeyoung. 2002. Takeovers of Privately Held Targets, Methods of Payment, and Bidder Returns. Journal of Finance 53: 773–84. [Google Scholar] [CrossRef]

- Dodd, Peter. 1980. Merger proposals management discretion and stockholder wealth. Journal of Financial Economics 8: 105–38. [Google Scholar] [CrossRef]

- Dodd, Peter, and Richard Ruback. 1977. Tender offers and stockholder returns: An empirical analysis. Journal of Financial Economics 5: 351–73. [Google Scholar] [CrossRef]

- Eckbo, B. Espen. 1983. Horizontal mergers, collusion, and stockholder wealth. Journal of Financial Economics 11: 241–73. [Google Scholar] [CrossRef]

- Fama, Eugene F., Lawrence Fisher, Michael C. Jensen, and Richard Roll. 1969. The adjustment of stock prices to new information. International Economic Review 10: 1–21. [Google Scholar] [CrossRef]

- Franks, Julian R., and Robert S. Harris. 1989. Shareholder wealth effects of corporate takeovers: The UK experience 1955–85. Journal of Financial Economics 23: 195–224. [Google Scholar] [CrossRef]

- Goergen, Marc, and Luc Renneboog. 2004. Shareholder Wealth Effects of European Domestic and Cross-Border Takeover Bids. European Financial Management 10: 9–45. [Google Scholar] [CrossRef]

- Heaton, James B. 2002. Managerial Optimism and Corporate Finance. Financial Management 31: 33–45. [Google Scholar] [CrossRef]

- Higson, Chris, and Jamie Elliott. 1998. Post-takeover returns: The UK evidence. Journal of Empirical Finance 5: 27–46. [Google Scholar] [CrossRef]

- Malatesta, Paul H. 1983. The wealth effect of merger activity and the objective function of merging firms. Journal of Financial Economics 11: 155–82. [Google Scholar] [CrossRef]

- Martynova, M., and L. Renneboog. 2006. Mergers and Acquisitions in Europe. ECGI Working Paper N.114/2006. Available online: https://core.ac.uk/reader/6651890 (accessed on 4 March 2023).

- Monga, Suman. 2021. Impact of Mergers and Acquisitions Announcement on Shareholders’ Wealth: Evidence from Indian Corporate Sector. Turkish Online Journal of Qualitative Inquiry 12: 10. [Google Scholar]

- Petmezas, D. 2009. What Drives Acquisitions? Journal of Multinational Financial Management 19: 54–74. [Google Scholar] [CrossRef] [Green Version]

- Protopapas, G. P., N. G. Travlos, and N. V. Tsagarakis. 2003. Mergers and Acquisitions in Greece: Stock price Reaction of Acquiring and Target Firms. Piraeus: SPOUDAI, vol. 53, pp. 80–104. [Google Scholar]

- Rani, Neelam, Surendra S. Yadav, and P. K. Jain. 2013. Impact of Corporate Governance Score on Abnormal Returns of Mergers and Acquisitions. Procedia Economics and Finance 5: 637–46. [Google Scholar] [CrossRef] [Green Version]

- Shohaieb, D., M. Elmarzouky, and K. Albitar. 2022. Corporate governance and diversity management: Evidence from a disclosure perspective. International Journal of Accounting & Information Management, ahead-of-print. [Google Scholar]

- Sudarsanam, Sudi, Peter Holl, and Ayo Salami. 1996. Shareholder wealth gains in mergers: Effect of synergy and ownership structure. Journal of Business Finance and Accounting 23: 673–98. [Google Scholar] [CrossRef]

- Tampakoudis, Ioannis, and Evgenia Anagnostopoulou. 2020. The effect of mergers and acquisitions on environmental, social and governance performance and market value: Evidence from EU acquirers. Business Strategy and the Environment 29: 1865–75. [Google Scholar] [CrossRef]

- Tampakoudis, Ioannis, Michail Nerantzidis, Gabriel Eweje, and Stergios Leventis. 2022. The impact of gender diversity on shareholder wealth: Evidence from European bank M&A. Journal of Financial Stability 60: 101020. [Google Scholar]

- Teti, Emanuele, and Stefano Tului. 2020. Do mergers and acquisitions create shareholder value in the infrastructure and utility sectors? Analysis of market perceptions. Utilities Policy 64: 101053. [Google Scholar] [CrossRef]

- Varmaz, Armin, and Jonas Laibner. 2016. Announced versus canceled bank mergers and acquisitions—Evidence from the European banking industry. The Journal of Risk Finance 17: 510–44. [Google Scholar] [CrossRef]

- Wasilewski, Mirosław, Serhiy Zabolotnyy, and Dmytro Osiichuk. 2021. Characteristics and shareholder wealth effects of mergers and acquisitions involving European renewable energy companies. Energies 14: 7126. [Google Scholar] [CrossRef]

- Weber, Roberto A., and Colin F. Camerer. 2003. Cultural Conflict and Merger Failure: An Experimental Approach. Management Science 49: 400–15. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Notations | Name of the Variables |

|---|---|

| AR_MINUS_5 | the average abnormal return 5 days before the event |

| AR_MINUS_4 | the average abnormal return 4 days before the event |

| AR_MINUS_3 | the average abnormal return 3 days before the event |

| AR_MINUS_2 | the average abnormal return 2 days before the event |

| AR_MINUS_1 | the average abnormal return 1 day before the event |

| AR_0 | the average abnormal return 5 on the day of the event |

| AR_PLUS_1 | the average abnormal return 1 day after the event |

| AR_PLUS_2 | the average abnormal return 2 days after the event |

| AR_PLUS_3 | the average abnormal return 3 days after the event |

| AR_PLUS_4 | the average abnormal return 4 days after the event |

| AR_PLUS_5 | the average abnormal return 5 days after the event |

| CAR_MINUS_1_PLUS_1 | the cumulative average abnormal return 3 days around the event |

| CAR_MINUS_5_PLUS_5 | the cumulative abnormal return 11 days around the event |

| Kolmogorov–Smirnov | Shapiro–Wilk | |||||

|---|---|---|---|---|---|---|

| Statistics | df | Sig. | Statistics | df | Sig. | |

| AR_MINUS_5 | 0.487 | 84 | 0.000 | 0.206 | 84 | 0.000 |

| AR_MINUS_4 | 0.498 | 84 | 0.000 | 0.193 | 84 | 0.000 |

| AR_MINUS_3 | 0.490 | 84 | 0.000 | 0.222 | 84 | 0.000 |

| AR_MINUS_2 | 0.485 | 84 | 0.000 | 0.172 | 84 | 0.000 |

| AR_MINUS_1 | 0.490 | 84 | 0.000 | 0.206 | 84 | 0.000 |

| AR_0 | 0.496 | 84 | 0.000 | 0.246 | 84 | 0.000 |

| AR_PLUS_1 | 0.482 | 84 | 0.000 | 0.250 | 84 | 0.000 |

| AR_PLUS_2 | 0.500 | 84 | 0.000 | 0.154 | 84 | 0.000 |

| AR_PLUS_3 | 0.495 | 84 | 0.000 | 0.220 | 84 | 0.000 |

| AR_PLUS_4 | 0.488 | 84 | 0.000 | 0.195 | 84 | 0.000 |

| AR_PLUS_5 | 0.480 | 84 | 0.000 | 0.215 | 84 | 0.000 |

| CAR_MINUS_1_PLUS_1 | 0.489 | 84 | 0.000 | 0.211 | 84 | 0.000 |

| CAR_MINUS_5_PLUS_5 | 0.494 | 84 | 0.000 | 0.226 | 84 | 0.000 |

| Kolmogorov-Smirnov | Shapiro-Wilk | |||||

| Statistics | df | Sig. | Statistics | df | Sig. | |

| AR_MINUS_5 | 0.136 | 73 | 0.002 | 0.963 | 73 | 0.031 |

| AR_MINUS_4 | 0.117 | 74 | 0.014 | 0.953 | 74 | 0.007 |

| AR_MINUS_3 | 0.107 | 73 | 0.039 | 0.966 | 73 | 0.046 |

| AR_MINUS_2 | 0.138 | 72 | 0.002 | 0.930 | 72 | 0.001 |

| AR_MINUS_1 | 0.121 | 72 | 0.011 | 0.959 | 72 | 0.019 |

| AR_0 | 0.112 | 72 | 0.025 | 0.962 | 72 | 0.029 |

| AR_PLUS_1 | 0.116 | 70 | 0.021 | 0.950 | 70 | 0.007 |

| AR_PLUS_2 | 0.087 | 73 | 0.200 | 0.974 | 73 | 0.135 |

| AR_PLUS_3 | 0.111 | 73 | 0.026 | 0.961 | 73 | 0.022 |

| AR_PLUS_4 | 0.135 | 74 | 0.002 | 0.943 | 74 | 0.002 |

| AR_PLUS_5 | 0.163 | 68 | 0.000 | 0.947 | 68 | 0.006 |

| CAR_MINUS_1_PLUS_1 | 0.119 | 74 | 0.011 | 0.946 | 74 | 0.003 |

| CAR_MINUS_5_PLUS_5 | 0.097 | 74 | 0.083 | 0.969 | 74 | 0.065 |

| N | Mean | Median | Std. Deviation | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|

| PANEL A: INITIAL | ||||||

| AR_MINUS_5 | 84 | −963.262 | 0.001 | 4744.894 | −5.327 | 27.983 |

| AR_MINUS_4 | 84 | 274.422 | −0.007 | 11,387.225 | 6.939 | 61.632 |

| AR_MINUS_3 | 84 | −827.320 | −0.003 | 3895.957 | −5.429 | 30.552 |

| AR_MINUS_2 | 84 | 496.160 | −0.002 | 9433.135 | 7.545 | 67.428 |

| AR_MINUS_1 | 84 | −882.057 | −0.007 | 4322.376 | −5.195 | 26.350 |

| AR_0 | 84 | −842.689 | −0.005 | 3616.690 | −4.590 | 20.539 |

| AR_PLUS_1 | 84 | −812.086 | −0.001 | 4542.388 | −5.014 | 27.042 |

| AR_PLUS_2 | 84 | 581.702 | −0.003 | 9808.163 | 7.852 | 71.000 |

| AR_PLUS_3 | 84 | −610.407 | 0.004 | 3081.988 | −5.390 | 29.196 |

| AR_PLUS_4 | 84 | −531.415 | −0.003 | 3425.308 | −6.349 | 41.485 |

| AR_PLUS_5 | 84 | −497.492 | 0.000 | 2402.937 | −6.001 | 37.627 |

| AAR_MINUS_1_PLUS_1 | 84 | −845.611 | −0.003 | 4048.298 | −5.072 | 24.837 |

| AAR_MINUS_5_PLUS_5 | 84 | −419.495 | −0.001 | 3121.921 | −5.301 | 33.097 |

| CAR_MINUS_1_PLUS_1 | 84 | −2536.832 | −0.009 | 12,144.895 | −5.072 | 24.837 |

| CAR_MINUS_5_PLUS_5 | 84 | −4614.445 | −0.013 | 34,341.133 | −5.301 | 33.097 |

| PANEL B: TRIMMED | ||||||

| AR_MINUS_5 | 73 | 0.006 | 0.003 | 0.041 | −0.243 | 0.521 |

| AR_MINUS_4 | 74 | −0.005 | −0.002 | 0.033 | 0.371 | 1.856 |

| AR_MINUS_3 | 73 | 0.000 | 0.000 | 0.033 | 0.250 | 0.572 |

| AR_MINUS_2 | 72 | 0.001 | −0.002 | 0.039 | 0.525 | 1.769 |

| AR_MINUS_1 | 72 | −0.010 | −0.005 | 0.032 | −0.127 | 1.297 |

| AR_0 | 72 | −0.004 | −0.001 | 0.037 | −0.253 | 0.837 |

| AR_PLUS_1 | 70 | 0.005 | 0.002 | 0.034 | 0.312 | 1.333 |

| AR_PLUS_2 | 73 | −0.005 | −0.002 | 0.039 | −0.212 | 0.682 |

| AR_PLUS_3 | 73 | 0.012 | 0.006 | 0.042 | 0.532 | 0.767 |

| AR_PLUS_4 | 74 | −0.011 | −0.002 | 0.037 | −0.649 | 1.608 |

| AR_PLUS_5 | 68 | 0.009 | 0.003 | 0.025 | 0.393 | 0.788 |

| AAR_MINUS_1_PLUS_1 | 74 | −0.001 | −0.001 | 0.023 | 0.175 | 1.717 |

| AAR_MINUS_5_PLUS_5 | 74 | 0.000 | −0.001 | 0.012 | 0.129 | 1.767 |

| CAR_MINUS_1_PLUS_1 | 74 | −0.003 | −0.003 | 0.069 | 0.175 | 1.717 |

| CAR_MINUS_5_PLUS_5 | 74 | 0.001 | −0.011 | 0.132 | 0.129 | 1.767 |

| t | df | Sig. (2 Tailed) | Mean Difference | 95% Confidence Interval of the Difference | ||

|---|---|---|---|---|---|---|

| Lower | Upper | |||||

| PANEL A: INITIAL | ||||||

| AR_MINUS_5 | −1.861 | 83 | 0.066 | −963.262 | −1992.968 | 66.443 |

| AR_MINUS_4 | 0.221 | 83 | 0.826 | 274.422 | −2196.758 | 2745.601 |

| AR_MINUS_3 | −1.946 | 83 | 0.055 | −827.320 | −1672.795 | 18.154 |

| AR_MINUS_2 | 0.482 | 83 | 0.631 | 496.160 | −1550.956 | 2543.276 |

| AR_MINUS_1 | −1.870 | 83 | 0.065 | −882.057 | −1820.070 | 55.956 |

| AR_0 | −2.135 | 83 | 0.036 | −842.689 | −1627.559 | −57.819 |

| AR_PLUS_1 | −1.639 | 83 | 0.105 | −812.086 | −1797.845 | 173.672 |

| AR_PLUS_2 | 0.544 | 83 | 0.588 | 581.702 | −1546.800 | 2710.204 |

| AR_PLUS_3 | −1.815 | 83 | 0.073 | −610.407 | −1279.239 | 58.426 |

| AR_PLUS_4 | −1.422 | 83 | 0.159 | −531.415 | −1274.753 | 211.922 |

| AR_PLUS_5 | −1.898 | 83 | 0.061 | −497.492 | −1018.961 | 23.977 |

| PANEL B: TRIMMED | ||||||

| AR_MINUS_5 | 1.194 | 72 | 0.236 | 0.006 | −0.004 | 0.015 |

| AR_MINUS_4 | −1.389 | 73 | 0.169 | −0.005 | −0.013 | 0.002 |

| AR_MINUS_3 | −0.022 | 72 | 0.983 | 0.000 | −0.008 | 0.008 |

| AR_MINUS_2 | 0.194 | 71 | 0.847 | 0.001 | −0.008 | 0.010 |

| AR_MINUS_1 | −2.701 | 71 | 0.009 | −0.010 | −0.018 | −0.003 |

| AR_0 | −0.964 | 71 | 0.338 | −0.004 | −0.013 | 0.004 |

| AR_PLUS_1 | 1.357 | 69 | 0.179 | 0.005 | −0.003 | 0.013 |

| AR_PLUS_2 | −1.111 | 72 | 0.270 | −0.005 | −0.014 | 0.004 |

| AR_PLUS_3 | 2.468 | 72 | 0.016 | 0.012 | 0.002 | 0.022 |

| AR_PLUS_4 | −2.476 | 73 | 0.016 | −0.011 | −0.019 | −0.002 |

| AR_PLUS_5 | 2.841 | 67 | 0.006 | 0.009 | 0.003 | 0.015 |

| t | df | Sig. (2 Tailed) | Mean Difference | 95% Confidence Interval of the Difference | ||

|---|---|---|---|---|---|---|

| Lower | Upper | |||||

| PANEL A: INITIAL | ||||||

| CAR_MINUS_1_PLUS_1 | −1.914 | 83 | 0.059 | −2536.832 | −5172.436 | 98.771 |

| CAR_MINUS_5_PLUS_5 | −1.232 | 83 | 0.222 | −4614.445 | −12,066.928 | 2838.037 |

| PANEL B: TRIMMED | ||||||

| CAR_MINUS_1_PLUS_1 | −0.419 | 73 | 0.676 | −0.003 | −0.019 | 0.013 |

| CAR_MINUS_5_PLUS_5 | 0.091 | 73 | 0.928 | 0.001 | −0.029 | 0.032 |

| INITIAL | TRIMMED | |||||

|---|---|---|---|---|---|---|

| N | Median | W-Sig. | N | Median | W-Sig. | |

| AR_MINUS_5 | 84 | 0.001 | 0.925 | 73 | 0.003 | 0.149 |

| AR_MINUS_4 | 84 | −0.007 | 0.004 | 74 | −0.002 | 0.070 |

| AR_MINUS_3 | 84 | −0.003 | 0.035 | 73 | 0.000 | 0.832 |

| AR_MINUS_2 | 84 | −0.002 | 0.409 | 72 | −0.002 | 0.559 |

| AR_MINUS_1 | 84 | −0.007 | 0.000 | 72 | −0.005 | 0.005 |

| AR_0 | 84 | −0.005 | 0.035 | 72 | −0.001 | 0.394 |

| AR_PLUS_1 | 84 | −0.001 | 0.844 | 70 | 0.002 | 0.245 |

| AR_PLUS_2 | 84 | −0.003 | 0.102 | 73 | −0.002 | 0.351 |

| AR_PLUS_3 | 84 | 0.004 | 0.230 | 73 | 0.006 | 0.029 |

| AR_PLUS_4 | 84 | −0.003 | 0.021 | 74 | −0.002 | 0.055 |

| AR_PLUS_5 | 84 | 0.000 | 0.779 | 68 | 0.003 | 0.013 |

| CAR_MINUS_1_PLUS_1 | 84 | −0.009 | 0.023 | 74 | −0.003 | 0.548 |

| CAR_MINUS_5_PLUS_5 | 84 | −0.013 | 0.593 | 74 | −0.011 | 0.848 |

| Counts | Percentages | χ2 Test | ||||

|---|---|---|---|---|---|---|

| Negative | Positive | Negative | Positive | Statistics | Sig. | |

| AR_MINUS_5_DUMMY | 49 | 35 | 58% | 42% | 2.333 | 0.127 |

| AR_MINUS_4_DUMMY | 51 | 33 | 61% | 39% | 3.857 | 0.050 |

| AR_MINUS_3_DUMMY | 47 | 37 | 56% | 44% | 1.190 | 0.275 |

| AR_MINUS_2_DUMMY | 47 | 37 | 56% | 44% | 1.190 | 0.275 |

| AR_MINUS_1_DUMMY | 56 | 28 | 67% | 33% | 9.333 | 0.002 |

| AR_0_DUMMY | 48 | 36 | 57% | 43% | 1.714 | 0.190 |

| AR_PLUS_1_DUMMY | 44 | 40 | 52% | 48% | 0.190 | 0,663 |

| AR_PLUS_2_DUMMY | 46 | 38 | 55% | 45% | 0.762 | 0.383 |

| AR_PLUS_3_DUMMY | 35 | 49 | 42% | 58% | 2.333 | 0.127 |

| AR_PLUS_4_DUMMY | 48 | 36 | 57% | 43% | 1.714 | 0.190 |

| AR_PLUS_5_DUMMY | 42 | 42 | 50% | 50% | 0.000 | 1.000 |

| CAR_MINUS_1_PLUS_1_DUMMY | 49 | 35 | 58% | 42% | 2.333 | 0.127 |

| CAR_MINUS_5_PLUS_5_DUMMY | 46 | 38 | 55% | 45% | 0.762 | 0.383 |

| t | df | Sig. (2 Tailed) | Mean Difference | 95% Confidence Interval of the Difference | ||

|---|---|---|---|---|---|---|

| Lower | Upper | |||||

| PANEL A: BEFORE CRISIS | ||||||

| AR_MINUS_5 | 0.010 | 30 | 0.992 | 0.000 | −0.012 | 0.012 |

| AR_MINUS_4 | −1.107 | 31 | 0.277 | −0.007 | −0.019 | 0.005 |

| AR_MINUS_3 | −0.056 | 31 | 0.956 | 0.000 | −0.013 | 0.012 |

| AR_MINUS_2 | 0.107 | 31 | 0.915 | 0.001 | −0.013 | 0.014 |

| AR_MINUS_1 | −0.437 | 31 | 0.665 | −0.003 | −0.015 | 0.010 |

| AR_0 | 0.117 | 31 | 0.908 | 0.001 | −0.013 | 0.014 |

| AR_PLUS_1 | 1.800 | 30 | 0.082 | 0.012 | −0.002 | 0.025 |

| AR_PLUS_2 | −0.466 | 31 | 0.645 | −0.003 | −0.014 | 0.009 |

| AR_PLUS_3 | 1.394 | 31 | 0.173 | 0.009 | −0.004 | 0.021 |

| AR_PLUS_4 | −1.076 | 31 | 0.290 | −0.007 | −0.021 | 0.006 |

| AR_PLUS_5 | 1.666 | 30 | 0.106 | 0.008 | −0.002 | 0.017 |

| CAR_MINUS_1_PLUS_1 | 1.499 | 31 | 0.144 | 0.013 | −0.005 | 0.031 |

| CAR_MINUS_5_PLUS_5 | 1.097 | 31 | 0.281 | 0.023 | −0.020 | 0.065 |

| PANEL B: AFTER CRISIS | ||||||

| AR_MINUS_5 | 1.391 | 41 | 0.172 | 0.010 | −0.004 | 0.024 |

| AR_MINUS_4 | −0.863 | 41 | 0.393 | −0.004 | −0.015 | 0.006 |

| AR_MINUS_3 | 0.023 | 40 | 0.982 | 0.000 | −0.010 | 0.010 |

| AR_MINUS_2 | 0.160 | 39 | 0.873 | 0.001 | −0.012 | 0.014 |

| AR_MINUS_1 | −3.599 | 39 | 0.001 | −0.016 | −0.025 | −0.007 |

| AR_0 | −1.423 | 39 | 0.163 | −0.008 | −0.020 | 0.003 |

| AR_PLUS_1 | 0.077 | 38 | 0.939 | 0.000 | −0.010 | 0.010 |

| AR_PLUS_2 | −1.012 | 40 | 0.318 | −0.007 | −0.021 | 0.007 |

| AR_PLUS_3 | 2.025 | 40 | 0.050 | 0.015 | 0.000 | 0.029 |

| AR_PLUS_4 | −2.353 | 41 | 0.023 | −0.013 | −0.025 | −0.002 |

| AR_PLUS_5 | 2.309 | 36 | 0.027 | 0.009 | 0.001 | 0.018 |

| CAR_MINUS_1_PLUS_1 | −1.323 | 41 | 0.193 | −0.016 | −0.040 | 0.008 |

| CAR_MINUS_5_PLUS_5 | −0.691 | 41 | 0.494 | −0.015 | −0.059 | 0.029 |

| Before Crisis | After Crisis | |||||

|---|---|---|---|---|---|---|

| N | Median | W-Sig. | N | Median | W-Sig. | |

| AR_MINUS_5 | 31 | 0.000 | 0.814 | 42 | 0.008 | 0.063 |

| AR_MINUS_4 | 32 | −0.007 | 0.064 | 42 | 0.001 | 0.427 |

| AR_MINUS_3 | 32 | −0.001 | 0.837 | 41 | 0.001 | 0.964 |

| AR_MINUS_2 | 32 | −0.002 | 0.614 | 40 | −0.001 | 0.657 |

| AR_MINUS_1 | 32 | −0.004 | 0.411 | 40 | −0.009 | 0.002 |

| AR_0 | 32 | −0.001 | 0.911 | 40 | 0.000 | 0.313 |

| AR_PLUS_1 | 31 | 0.008 | 0.092 | 39 | −0.001 | 0.900 |

| AR_PLUS_2 | 32 | −0.001 | 0.708 | 41 | −0.002 | 0.361 |

| AR_PLUS_3 | 32 | 0.008 | 0.286 | 41 | 0.006 | 0.045 |

| AR_PLUS_4 | 32 | 0.000 | 0.411 | 42 | −0.004 | 0.071 |

| AR_PLUS_5 | 31 | 0.000 | 0.248 | 37 | 0.004 | 0.020 |

| AAR_MINUS_1_PLUS_1 | 32 | 0.003 | 0.210 | 42 | −0.004 | 0.086 |

| AAR_MINUS_5_PLUS_5 | 32 | 0.000 | 0.588 | 42 | −0.001 | 0.413 |

| CAR_MINUS_1_PLUS_1 | 32 | 0.010 | 0.210 | 42 | −0.011 | 0.086 |

| CAR_MINUS_5_PLUS_5 | 32 | 0.002 | 0.588 | 42 | −0.014 | 0.413 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Giannopoulos, G.; Lianou, A.; Elmarzouky, M. The Impact of M&As on Shareholders’ Wealth: Evidence from Greece. J. Risk Financial Manag. 2023, 16, 199. https://doi.org/10.3390/jrfm16030199

Giannopoulos G, Lianou A, Elmarzouky M. The Impact of M&As on Shareholders’ Wealth: Evidence from Greece. Journal of Risk and Financial Management. 2023; 16(3):199. https://doi.org/10.3390/jrfm16030199

Chicago/Turabian StyleGiannopoulos, George, Alexandra Lianou, and Mahmoud Elmarzouky. 2023. "The Impact of M&As on Shareholders’ Wealth: Evidence from Greece" Journal of Risk and Financial Management 16, no. 3: 199. https://doi.org/10.3390/jrfm16030199