4.1. Descriptive Statistics

A total of 450 questionnaires were distributed in Iran and 350 questionnaires in Iraq, of which 365 questionnaires were completed in Iran and 250 questionnaires in Iraq. The questionnaire completion ratio was 0.81% in Iran and 0.71% in Iraq. These questionnaires were filled out by all the partners, managers and auditors working in auditing firms in Iran and the partners of the auditing firm, assistant auditors, individual second rank and individual first rank for Iraq working in companies active in the stock exchanges of Iran and Iraq.

As shown in

Table 2, in terms of gender the number of male respondents to the questionnaire in Iran is more than female respondents; most are between 30 and 39 years old. Most of the group has a bachelor’s degree, and they work in the accounting field with experience of between 1 and 5 years. Also, most of the respondents to the questionnaire in Iraq were men, and most of the respondents were between 40 and 49 years old. Most of the group have postgraduate education and work in accounting with 11 to 15 years of experience.

Table 3 shows the descriptive statistics of business ethics data in Iran and Iraq. According to the table, the average and median of the answers given by all the partners, managers and supervisors of audit institutions in Iran are 4, which is a high choice, and the mode in the received answers is also an increased choice. After that, the frequency, including the number and percentage of each of the responses to the Iranian questionnaire, which 365 people completed, was stated in order. In Iraq, mode and median are often chosen as 4 or 5, which are many and very many options. Therefore, we can point out the importance and role of business ethics in Iraq.

Table 3 shows the descriptive statistics of aggression data in Iran and Iraq. The mean and median of the responses provided by all the partners, managers and supervisors of audit institutions in Iran are 2, which is low, and the mode in the received responses is also low. The mean and median of the answers provided by all the partners, managers and supervisors of audit institutions in Iraq are 2, representing a low option, and the mode in the received answers is also very low.

Table 3 shows the descriptive statistics of effort and reward mismatch in Iran and Iraq. The mean and median of the responses provided by all the partners, managers and supervisors of audit institutions in Iran are 3, which is the medium option, and the mode in the received responses is also the high option. The average and median of the responses provided by all the partners, managers and supervisors of audit institutions in Iraq are 4, which is a large number of choices. The mode in the received responses also has a large number of choices.

Table 3 shows the descriptive statistics of the happiness data of the two countries of Iran and Iraq. The mean and median of the responses provided by all the partners, managers and supervisors of audit institutions in Iran are 4, which is a large number of choices. The mode in the received responses also has a large number of choices. Also, the mean and median of the responses provided by all the partners, managers and supervisors of audit institutions in Iraq are 4, which is a high choice, and the mode in the received answers is also high.

4.2. Inferencing Data

Before examining the research hypotheses, the validity and reliability of the research questionnaire are examined. When enough evidence has been accumulated about the validity and reliability of the questionnaires, the research hypotheses can be evaluated correctly. The results of these cases are shown in

Table 4 as indices of the Cronbach’s alpha coefficient, composite reliability coefficient and average variance extracted. The alpha coefficient ranges from 0 to 1. The alpha coefficient for Iran’s questionnaire is equal to 0.835, and for Iraq’s questionnaire is equal to 0.811, which is in the appropriate range. To evaluate the validity of the construct, the average variance index was extracted, and the Fornell and Larcker criteria were used. The AVE index in

Table 4 states that the average extracted variance of each model dimension has a value greater than 0.5; therefore, the convergent validity of the model is confirmed. According to

Table 4, the AVE value for the model’s variables is higher than 0.5, so it can be said that the cross-validation-communality was used in the convergence validity of the measurement model.

In order to measure the goodness of fit of the current research, two indices were used, the results of which are presented in

Table 5. It can be concluded that the model fit is suitable for the data of Iran and Iraq, and the accumulated data and the obtained results are reliable.

In

Table 6, the results of the equality test of the mean of Iran and Iraq questionnaires are displayed in order to investigate the impact of business ethics on the psychological conditions of auditors.

Table 6 compares Iran and Iraq’s average responses received on business ethics. In comparing the averages, the opposite hypothesis is considered in three ways of inequality, Iran’s largeness of average received responses and Iraq’s largeness of average received responses. In most of the questions, the average answers received by Iraq were higher than Iran. Therefore, business ethics in Iraq has a more prominent role than in Iran. On the contrary, regarding the second question, the average answers received by the two countries are the same. Therefore, the essential and the effective role in the work environment is the same from the point of view of the respondents of Iraq and Iran. Also, in terms of the question, ‘To what extent are you looking for a higher rank and position in your current role?’ the same answer was given by both groups. On the contrary, for the first question the average answers received in Iran were higher than in Iraq. Therefore, compared to Iraqi respondents, Iranian respondents perform their work duties with more caution and care.

Table 6 compares the average responses to aggression questions for Iran and Iraq. This section contains 29 questions. Regarding half of the questions in this section, the average of the two groups is equal. For questions 7 and 15, the average aggression of Iraq is lower than that of Iran. For 12 questions, Iran’s average was lower than Iraq’s.

Table 6 includes the average answers received to the questions about a mismatch between the efforts and rewards of the two countries. This section consists of 16 questions. The average of these two countries is also significantly different from each other. The average mismatch between effort and reward is lower in Iran than in Iraq. Only for two questions, 8 and 15, is the average of the two countries is the same. In addition, regarding questions 9 and 13, Iraq’s average was lower than Iran’s.

Table 6 includes the average answers to the happiness questions of the two countries. This section consists of eight questions. The average of these two countries is different from each other on three out of the eight questions, and they are equal to each other on the other five questions. Regarding questions 2, 3 and 4, the average of Iran regarding happiness is lower than Iraq’s.

Psychological conditions include happiness, aggression and inconsistency between effort and reward. Each of these factors has been obtained through several questions through averaging. Business ethics itself is obtained through 16 questions. The component of happiness was obtained through 8 questions, aggression through 29 questions and inconsistency between effort and reward through 16 questions.

Table 7 shows the components of each part of the questionnaire and the number of questions that make them up.

In addition, in

Table 7, Cronbach’s alpha of each part of the questionnaire is also calculated. Considering that Cronbach’s alpha was calculated between 0.839 and 0.892 for Iran’s questionnaire and between 0.812 and 0.884 for Iraq, the questionnaires of both countries have a suitable internal structure.

In

Table 8, the descriptive statistics of each of the components and then the leading indicators are shown. It is worth mentioning that the number of participants in the Iran questionnaire is 365, and the number of respondents in the Iraq questionnaire is 250. According to the average and minimum obtained from each component, it can be recognized that Iraqi people attach a stronger role to business ethics. The average obtained for Iraqi respondents is 4.086, and for Iranian respondents it is 3.760. In addition, the minimum average for Iraqi interviewees is 2.813, and for Iranian interviewees it is equal to 2.5.

Aggression in two countries can be said to have the same average. However, the discrepancy between effort and reward is greater in Iraq than in Iran, so the average in Iraq is equal to 3.475, and for Iran it is equal to 3.161. Iraqi people are happier than Iranians. The average calculated for Iraq is 3.532, and for Iran it is 3.266. The psychological condition variable, which results from three components of aggression, the dissonance between effort and reward and happiness, is more than in Iraq. The average mental condition for Iraq is 3.005, and for Iran it equals 2.814.

After that, in

Table 9, the correlation between the research components of Iran and Iraq has been obtained. The business ethics component affects all indicators of psychological conditions in Iran. In this regard, business ethics has a negative effect on the components of aggression and inconsistency between effort and reward. On the contrary, the business ethics component positively and significantly affects happiness. In general, business ethics has a negative effect on psychological conditions in Iran at the 99% confidence level.

Similar to what was obtained regarding Iran’s data, the business ethics component affects all three indicators of psychological conditions in Iraq. Business ethics has a negative effect on the components of aggression and inconsistency between reward and effort. On the contrary, the business ethics component positively and significantly affects happiness. In general, business ethics has a negative effect on psychological conditions in Iraq at the 99% confidence level.

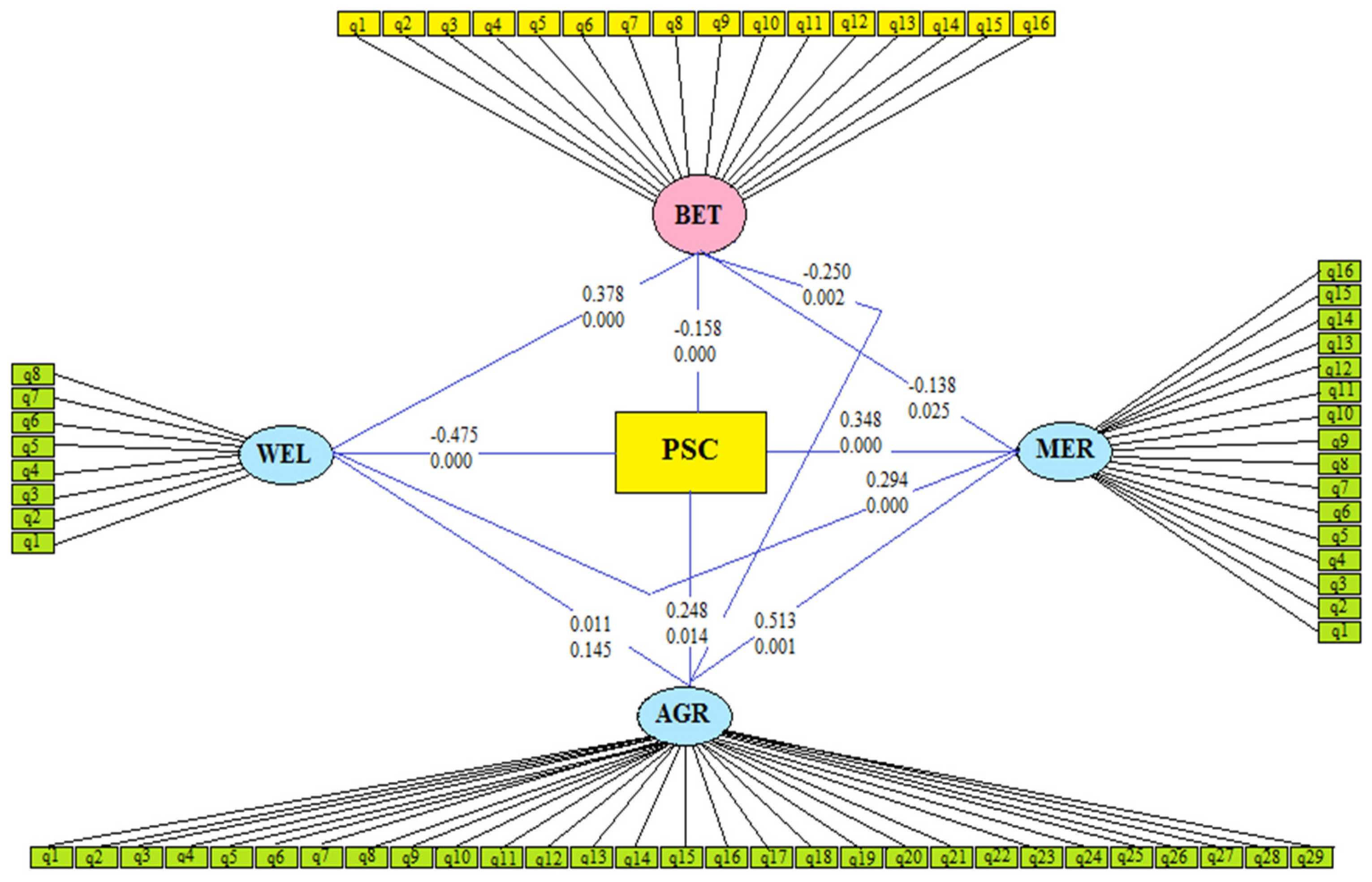

In

Figure 1, the output and the effect of the hidden and obvious variables of the Iranian questionnaire are drawn. According to the output of PLS software, the business ethics component affects all three indicators of psychological conditions in Iran. The coefficient of the happiness variable is equal to −0.475, which is significant at the 99% level. On the other hand, the coefficients of inconsistency variables between effort and reward and aggression variables were calculated as 0.348 and 0.248, respectively, which are significant. In general, business ethics has a negative effect on psychological conditions in Iran at the 99% confidence level. The coefficient of this variable is equal to −0.158.

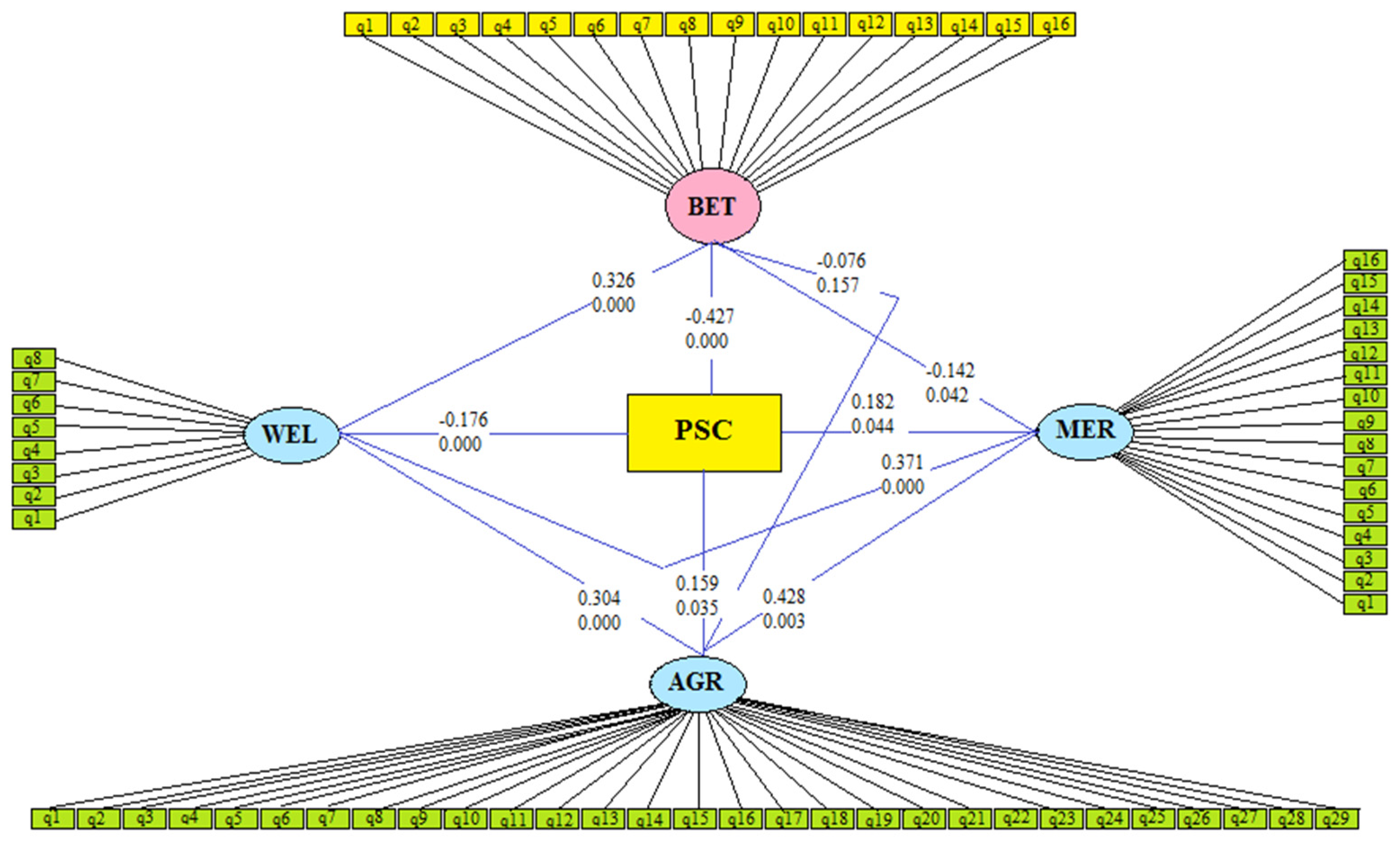

In

Figure 2, the output and the effect of the hidden and obvious variables of the questionnaire are drawn. According to the output of PLS software, the business ethics component affects two indicators of psychological conditions in Iraq and does not affect aggression. The effectiveness coefficient of the happiness variable is equal to −0.176, which is significant at the 99% level. On the other hand, the coefficients of the inconsistency variables between effort and reward and the aggression variable were calculated as 0.182 and 0.159, respectively, which are significant. In general, business ethics has a negative effect on psychological conditions in Iran at the 99% confidence level. The coefficient of this variable is equal to −0.427.

After that, ordinary least squares regression was used to investigate the relationship between business ethics and psychological conditions.

Table 10 shows the results of these regressions for Iranian data. This table contains 4 regressions. In the first model, the dependent variable is the psychological condition (PSC). The variable of business ethics has a negative and significant effect on psychological conditions. With a one percent improvement in the ethics and business variable, mental conditions decrease at the 95 percent confidence level, equivalent to 0.147 percent. The variables of gender and job rank also have a positive and significant effect on psychological conditions at the 99% level. The coefficients of these variables were obtained as 0.179 and 0.471, respectively.

In the second regression, the dependent variable is aggression. Business conditions have a negative effect on aggression. The coefficient of this variable is equal to −0.372, which is significant at the 99% confidence level. In the third regression, the dependent variable is the mismatch between effort and reward. Business conditions have a negative effect on effort-reward mismatch at the 90% confidence level. In the fourth model, the effect of business conditions on happiness has been measured. According to the obtained results, the variable coefficient of business conditions is equal to 0.335, which is significant at the 99% confidence level.

Considering the data of Iraq, in

Table 11 the dependent variable of the first model is the psychological condition (PSC). The variable of business ethics has a negative and significant effect on psychological conditions. Therefore, with a one percent improvement in business ethics in Iraq, psychological conditions will decrease at 99% confidence, equivalent to 0.485 percent. Gender and job experience also increase psychological conditions at the 90% confidence level.

In the second regression, the dependent variable is aggression. Business conditions have a negative effect on aggression. The coefficient of this variable is equal to −0.246, which is significant at the 95% confidence level. In the third regression, the dependent variable is the mismatch between effort and reward. Business conditions have a negative effect on effort-reward mismatch at the 99% confidence level. In the fourth model, the effect of business conditions on happiness was measured. According to the results, the variable coefficient of business conditions equals 0.343, which is significant at the 99% confidence level.

{kind=link}

{kind=link}