The Economic Policy Uncertainty and Its Effect on Sustainable Investment: A Panel ARDL Approach

,

,  ,

,  and

and

Abstract

:1. Introduction

2. Data and Methods

2.1. Data

2.2. Research Method

2.2.1. Panel Unit Root Tests and Cointegration Tests

2.2.2. Panel Model ARDL

3. Empirical Analysis

3.1. Descriptive Statistics

3.2. Panel Unit Root Test and Cointegration Test

3.3. Panel ARDL Approach

3.4. PMG Individual Nations Short-Run Results

4. Discussion

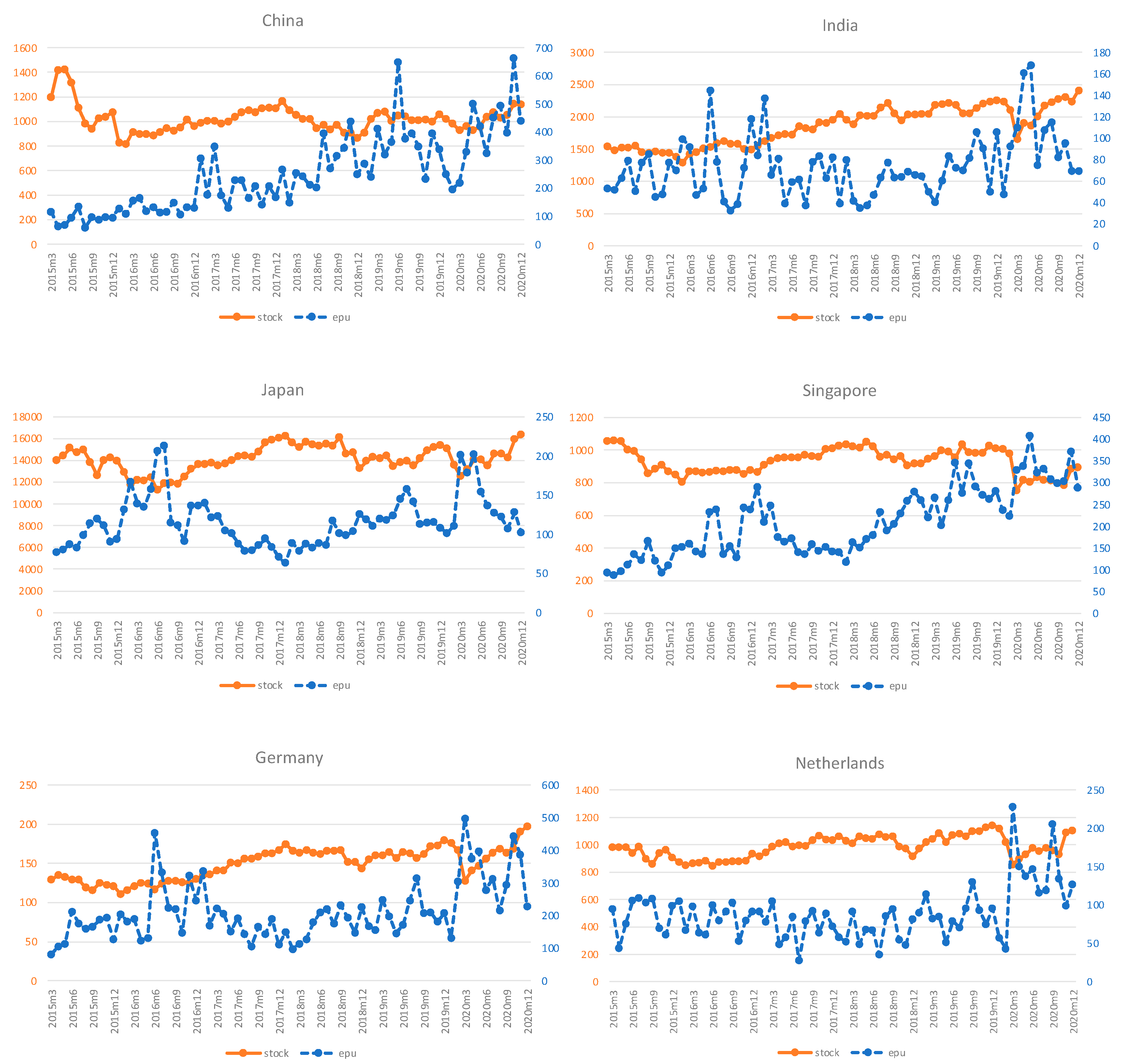

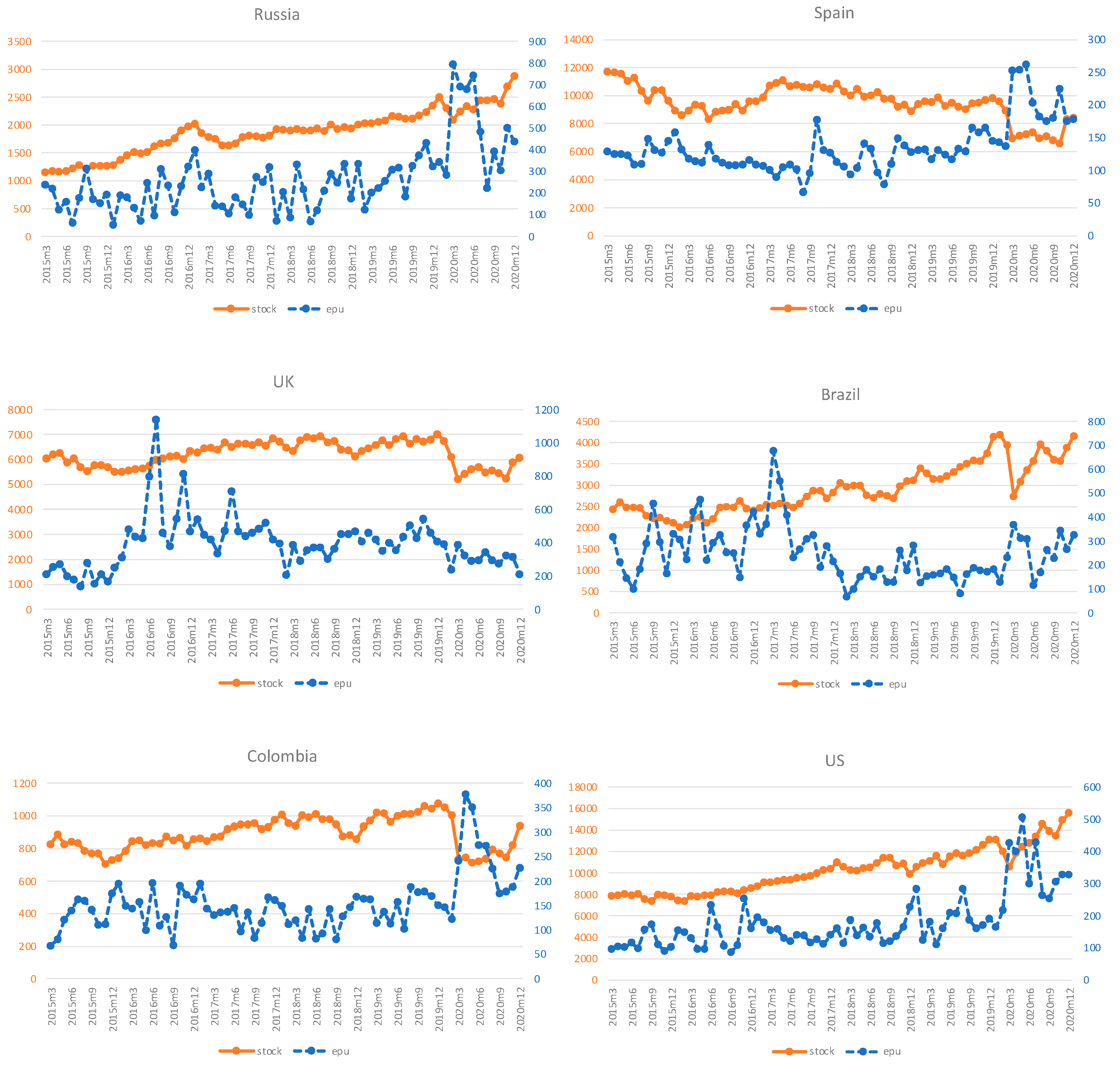

4.1. Correlation between the EPU and Sustainable Stock Market Returns

4.2. Effect of EPU, Gold, Oil, and Bitcoin Prices on Individual Sustainable Stock Market Returns

4.3. Practical Implications

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Abbas, Faisal, Shoaib Ali, Imran Yousaf, and Wing-Keung Wong. 2021. Dynamics of Funding Liquidity and Risk-taking: Evidence from Commercial Banks. Journal of Risk and Financial Management 14: 281. [Google Scholar] [CrossRef]

- Ahmed, Walid M. A. 2021. Stock Market Reactions to Upside and Downside Volatility of Bitcoin: A Quantile Analysis. North American Journal of Economics and Finance 57: 101379. [Google Scholar] [CrossRef]

- Ali, F., Y. Jiang, and A. Sensoy. 2021. Downside risk in Dow Jones Islamic equity indices: Precious metals and portfolio diversification before and after the COVID-19 bear market. Research in International Business and Finance 58: 101502. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, Ioannis Chatziantoniou, and George Filis. 2013. Dynamic Co-Movements of Stock Market Returns, Implied Volatility and Policy Uncertainty. Economics Letters 120: 87–92. [Google Scholar] [CrossRef]

- Arouri, Mohamed, Christophe Estay, Christophe Rault, and David Roubaud. 2016. Economic Policy Uncertainty and Stock Markets: Long-Run Evidence from the US. Finance Research Letters 18: 136–41. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring Economic Policy Uncertainty. The Quarterly Journal of Economics 131: 1593–636. [Google Scholar] [CrossRef]

- Boateng, Ebenezer, Anokye M. Adam, and Peterson Owusu Junior. 2021. Modelling the Heterogeneous Relationship between the Crude Oil Implied Volatility Index and African Stocks in the Coronavirus Pandemic. Resources Policy 74: 102389. [Google Scholar] [CrossRef]

- Broadstock, David C., Kalok Chan, Louis T.W. Cheng, and Xiaowei Wang. 2021. The Role of ESG Performance during Times of Financial Crisis: Evidence from COVID-19 in China. Finance Research Letters 38: 101716. [Google Scholar] [CrossRef]

- Chang, Kuang Liang. 2021. Do Economic Policy Uncertainty Indices Matter in Joint Volatility Cycles between US and Japanese Stock Markets? Finance Research Letters 47: 102579. [Google Scholar] [CrossRef]

- Chang, Tsangyao, Wen Yi Chen, Rangan Gupta, and Duc Khuong Nguyen. 2015. Are Stock Prices Related to the Political Uncertainty Index in OECD Countries? Evidence from the Bootstrap Panel Causality Test. Economic Systems 39: 288–300. [Google Scholar] [CrossRef] [Green Version]

- Cheng, Yushan, Yongchang Hui, Michael McAleer, and Wing Keung Wong. 2021. Spurious Relationships for Nearly Non-stationary Series. Journal of Risk and Financial Management 14: 366. [Google Scholar] [CrossRef]

- Chiah, Mardy, and Angel Zhong. 2020. Trading from Home: The Impact of COVID-19 on Trading Volume around the World. Finance Research Letters 37: 101784. [Google Scholar] [CrossRef]

- Chiang, Thomas C. 2019. Economic Policy Uncertainty, Risk and Stock Returns: Evidence from G7 Stock Markets. Finance Research Letters 29: 41–49. [Google Scholar] [CrossRef]

- Christou, Christina, Juncal Cunado, Rangan Gupta, and Christis Hassapis. 2017. Economic Policy Uncertainty and Stock Market Returns in PacificRim Countries: Evidence Based on a Bayesian Panel VAR Model. Journal of Multinational Financial Management 40: 92–102. [Google Scholar] [CrossRef]

- Dai, Peng Fei, Xiong Xiong, Toan Luu Duc Huynh, and Jiqiang Wang. 2021. The Impact of Economic Policy Uncertainties on the Volatility of European Carbon Market. Journal of Commodity Markets 26: 100208. [Google Scholar] [CrossRef]

- Dakhlaoui, Imen, and Chaker Aloui. 2016. The Interactive Relationship between the US Economic Policy Uncertainty and BRIC Stock Markets. International Economics 146: 141–57. [Google Scholar] [CrossRef]

- Darsono, Susilo Nur Aji Cokro, Wing Keung Wong, Tran Thai Ha Nguyen, Hafsah Fajar Jati, and Diah Setyawati Dewanti Dewanti. 2022. Good Governance and Sustainable Investment: The Effects of Governance Indicators on Stock Market Returns. Advances in Decision Sciences 26: 69–101. [Google Scholar]

- Das, Debojyoti, M. Kannadhasan, and Malay Bhattacharyya. 2019. Do the Emerging Stock Markets React to International Economic Policy Uncertainty, Geopolitical Risk and Financial Stress Alike? North American Journal of Economics and Finance 48: 1–19. [Google Scholar] [CrossRef]

- Escrig-Olmedo, Elena, Juana María Rivera-Lirio, María Jesús Muñoz-Torres, and María Ángeles Fernández-Izquierdo. 2017. Integrating Multiple ESG Investors’ Preferences into Sustainable Investment: A Fuzzy Multicriteria Methodological Approach. Journal of Cleaner Production 162: 1334–45. [Google Scholar] [CrossRef]

- Fang, Libing, Baizhu Chen, Honghai Yu, and Cheng Xiong. 2018. The Effect of Economic Policy Uncertainty on the Long-Run Correlation between Crude Oil and the U.S. Stock Markets. Finance Research Letters 24: 199–220. [Google Scholar] [CrossRef]

- Fasanya, Ismail O., Johnson A. Oliyide, Oluwasegun B. Adekoya, and Taofeek Agbatogun. 2021. How Does Economic Policy Uncertainty Connect with the Dynamic Spillovers between Precious Metals and Bitcoin Markets? Resources Policy 72: 102077. [Google Scholar] [CrossRef]

- Garcia, Alexandre Sanches, Wesley Mendes-Da-Silva, and Renato Orsato. 2017. Sensitive Industries Produce Better ESG Performance: Evidence from Emerging Markets. Journal of Cleaner Production 150: 135–47. [Google Scholar] [CrossRef]

- Guo, Peng, Huiming Zhu, and Wanhai You. 2018. Asymmetric Dependence between Economic Policy Uncertainty and Stock Market Returns in G7 and BRIC: A Quantile Regression Approach. Finance Research Letters 25: 251–58. [Google Scholar] [CrossRef]

- Hashmi, Shabir Mohsin, Muhammad Akram Gilal, and Wing Keung Wong. 2021. Sustainability of Global Economic Policy and Stock Market Returns in Indonesia. Sustainability 13: 5422. [Google Scholar] [CrossRef]

- Hussain Shahzad, Syed Jawad, Elie Bouri, David Roubaud, and Ladislav Kristoufek. 2020. Safe Haven, Hedge and Diversification for G7 Stock Markets: Gold versus Bitcoin. Economic Modelling 87: 212–24. [Google Scholar] [CrossRef]

- Im, Kyung So, M. Hashem Pesaran, and Yongcheol Shin. 2003. Testing for Unit Roots in Heterogeneous Panels. Journal of Econometrics 115: 53–74. [Google Scholar] [CrossRef]

- Jin, Xuejun, Ziqing Chen, and Xiaolan Yang. 2019. Economic Policy Uncertainty and Stock Price Crash Risk. Accounting & Finance 58: 1291–1318. [Google Scholar]

- Kang, Wensheng, Fernando Perez de Gracia, and Ronald A. Ratti. 2017. Oil Price Shocks, Policy Uncertainty, and Stock Returns of Oil and Gas Corporations. Journal of International Money and Finance 70: 344–59. [Google Scholar] [CrossRef]

- Kao, Chihwa. 1999. Spurious Regression and Residual-Based Tests for Cointegration in Panel Data. Journal of Econometrics 90: 1–44. [Google Scholar] [CrossRef]

- Kundu, Srikanta, and Amartya Paul. 2022. Effect of Economic Policy Uncertainty on Stock Market Return and Volatility under Heterogeneous Market Characteristics. International Review of Economics and Finance 80: 597–612. [Google Scholar] [CrossRef]

- Levin, Andrew, Chien-Fu Lin, and Chia-Shang James Chu. 2002. Unit Root Tests in Panel Data: Asymptotic and Ÿnite-Sample Properties. Journal of Econometrics 108: 1–24. [Google Scholar] [CrossRef]

- Liu, Li, and Tao Zhang. 2015. Economic Policy Uncertainty and Stock Market Volatility. Finance Research Letters 15: 99–105. [Google Scholar] [CrossRef] [Green Version]

- Li, Xiaorong, Steven Shuye Wang, and Xue Wang. 2017. Trust and Stock Price Crash Risk: Evidence from China. Journal of Banking & Finance 76: 74–91. [Google Scholar]

- Luo, Yan, and Chenyang Zhang. 2020. Economic Policy Uncertainty and Stock Price Crash Risk. Research in International Business and Finance 51: 1–24. [Google Scholar] [CrossRef]

- Matkovskyy, Roman, Akanksha Jalan, and Michael Dowling. 2020. Effects of Economic Policy Uncertainty Shocks on the Interdependence between Bitcoin and Traditional Financial Markets. Quarterly Review of Economics and Finance 77: 150–55. [Google Scholar] [CrossRef]

- Mensi, W., S. Hammoudeh, I. M. W. Al-Jarrah, A. Sensoy, and S. H. Kang. 2017. Dynamic risk spillovers between gold, oil prices and conventional, sustainability and Islamic equity aggregates and sectors with portfolio implications. Energy Economics 67: 454–75. [Google Scholar] [CrossRef]

- Mokni, Khaled, Ahdi Noomen Ajmi, Elie Bouri, and Xuan Vinh Vo. 2020. Economic Policy Uncertainty and the Bitcoin-US Stock Nexus. Journal of Multinational Financial Management 57–58: 100656. [Google Scholar] [CrossRef]

- Nakai, Miwa, Keiko Yamaguchi, and Kenji Takeuchi. 2016. Can SRI Funds Better Resist Global Financial Crisis? Evidence from Japan. International Review of Financial Analysis 48: 12–20. [Google Scholar] [CrossRef] [Green Version]

- Oliyide, Johnson A., Oluwasegun B. Adekoya, and Muhammad A. Khan. 2021. Economic Policy Uncertainty and the Volatility Connectedness between Oil Shocks and Metal Market: An Extension. International Economics 167: 136–50. [Google Scholar] [CrossRef]

- Pastor, Lubos, and Pietro Veronesi. 2012. Uncertainty about Government Policy and Stock Prices. The Journal of Finance 67: 1219–64. [Google Scholar] [CrossRef]

- Pedroni, Peter. 1999. Critical Values for Cointegration Tests in Heterogeneous Panels with Multiple Regressors. Oxford Bulletin of Economics and Statistics 61: 653–70. [Google Scholar] [CrossRef]

- Pedroni, Peter. 2004. Panel Cointegration: Asymptotic and Finite Sampleproperties of Pooled Timeseries Tests with Anapplication to Theppp Hypothesis. Econometric Theory 20: 597–625. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, M. Hashem, and Ron Smith. 1995. Estimating Long-Run Relationships from Dynamic Heterogeneous Panels. Journal of Econometrics 68: 79–113. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, and Yongcheol Shin. 1999. An Autoregressive Distributed Lag Modelling Approach to Cointegration Analysis. In Econometrics and Economic Theory in the 20th Century: The Ragnar Frish Centennial Symposium. Edited by S. Strom. Cambridge: Cambridge University Press, pp. 371–413. [Google Scholar]

- Pesaran, M. Hashem, Yongcheol Shin, and Ron P. Smith. 1997. Pooled Estimation of Long-Run Relationship in Dynamic Heterogeneous Panels. In Cambridge Working Papers in Economics. Cambridge: Faculty of Economics, University of Cambridge. [Google Scholar]

- Pesaran, M. Hashem, Yongcheol Shin, and Ron P. Smith. 1999. Pooled Mean Group Estimation of Dynamic Heterogeneous Panels. Journal of the American Statistical Association 94: 621–34. [Google Scholar] [CrossRef]

- Pham, Linh, and Canh Phuc Nguyen. 2022. How Do Stock, Oil, and Economic Policy Uncertainty Influence the Green Bond Market? Finance Research Letters 45: 102128. [Google Scholar] [CrossRef]

- Prawoto, N., and B. A. Putra. 2020. The Factors Affecting the Composite Stock Price Index (CSPI) of Indonesia Stock Exchange. Jurnal Ekonomi & Studi Pembangunan 21: 69–83. [Google Scholar]

- Raza, Syed Ali, Isma Zaighum, and Nida Shah. 2018. Economic Policy Uncertainty, Equity Premium and Dependence between Their Quantiles: Evidence from Quantile-on-Quantile Approach. Physica A: Statistical Mechanics and Its Applications 492: 2079–91. [Google Scholar] [CrossRef]

- Robiyanto, R., B. A. Nugroho, A. D. Huruta, B. Frensidy, and S. Suyanto. 2021. Identifying the role of gold on sustainable investment in Indonesia: The dcc-garch approach. Economies 9: 119. [Google Scholar] [CrossRef]

- SSE Initiatives. 2010. Sustainable Stock Exchanges Initiatives. United Nations. Available online: https://sseinitiative.org/about/ (accessed on 15 September 2020).

- Su, Zhi, Tong Fang, and Libo Yin. 2018. Understanding Stock Market Volatility: What Is the Role of US Uncertainty? North American Journal of Economics and Finance 48: 582–90. [Google Scholar] [CrossRef]

- Sum, Vichet. 2013. The ASEAN Stock Market Performance and Economic Policy Uncertainty in the United States. Economic Papers 32: 512–21. [Google Scholar] [CrossRef]

- Tseng, M. L., P. A. Tan, S. Y. Jeng, C. W. R. Lin, Y. T. Negash, and S. N. A. C. Darsono. 2019. Sustainable investment: Interrelated among corporate governance, economic performance and market risks using investor preference approach. Sustainability 11: 2108. [Google Scholar] [CrossRef] [Green Version]

- Vo, Hong, Quoc Dat Trinh, Minh Le, and Thuy Ngan Nguyen. 2021. Does Economic Policy Uncertainty Affect Investment Sensitivity to Peer Stock Prices? Economic Analysis and Policy 72: 685–99. [Google Scholar] [CrossRef]

- Wang, Fengrong, William Mbanyele, and Linda Muchenje. 2022. Economic Policy Uncertainty and Stock Liquidity: The Mitigating Effect of Information Disclosure. Research in International Business and Finance 59: 101553. [Google Scholar] [CrossRef]

- Wong, Wing Keung. 2020. Editorial Statement and Research Ideas for Efficiency and Anomalies in Stock Markets. Economies 8: 10. [Google Scholar] [CrossRef] [Green Version]

- Wu, Tsung Pao, Shu Bing Liu, and Shun Jen Hsueh. 2016. The Causal Relationship between Economic Policy Uncertainty and Stock Market: A Panel Data Analysis. International Economic Journal 30: 109–22. [Google Scholar] [CrossRef]

- Xu, Yongan, Jianqiong Wang, Zhonglu Chen, and Chao Liang. 2021. Economic Policy Uncertainty and Stock Market Returns: New Evidence. The North American Journal of Economics and Finance 58: 101525. [Google Scholar] [CrossRef]

- Yang, Miao, and Zhi Qiang Jiang. 2016. The Dynamic Correlation between Policy Uncertainty and Stock Market Returns in China. Physica A: Statistical Mechanics and Its Applications 461: 92–100. [Google Scholar] [CrossRef]

- Yang, T., F. Zhou, M. Du, Q. Du, and S. Zhou. 2021. Fluctuation in the global oil market, stock market volatility, and economic policy uncertainty: A study of the US and China. Quarterly Review of Economics and Finance. [Google Scholar] [CrossRef]

- Yu, Xiaoling, and Yirong Huang. 2021. The Impact of Economic Policy Uncertainty on Stock Volatility: Evidence from GARCH–MIDAS Approach. Physica A: Statistical Mechanics and its Applications 570: 125794. [Google Scholar] [CrossRef]

- Yuan, Di, Sufang Li, Rong Li, and Feipeng Zhang. 2022a. Economic Policy Uncertainty, Oil and Stock Markets in BRIC: Evidence from Quantiles Analysis. Energy Economics 110: 105972. [Google Scholar] [CrossRef]

- Yuan, Mengyi, Lin Zhang, and Yonghui Lian. 2022b. Economic Policy Uncertainty and Stock Price Crash Risk of Commercial Banks: Evidence from China. Economic Analysis and Policy 74: 587–605. [Google Scholar] [CrossRef]

- Zhao, Wen, and Yu Dong Wang. 2021. On the Time-Varying Correlations between Oil-, Gold-, and Stock Markets: The Heterogeneous Roles of Policy Uncertainty in the US and China. Petroleum Science. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Countries | Index | Mean | Max | Min | Std. Dev. | Skew. | Kurt. |

|---|---|---|---|---|---|---|---|

| China | SSECGI | 1021.13 | 1425.45 | 816.40 | 110.77 | 1.47 | 3.98 |

| India | NIFTY100 ESG | 1852.85 | 2409.95 | 1286.13 | 300.57 | −0.09 | −1.35 |

| Japan | JPXNK400 | 14,134.92 | 16,341.80 | 11,250.20 | 1205.22 | −0.30 | −0.38 |

| Singapore | iEdge SG ESG | 930.79 | 1059.65 | 753.60 | 76.53 | −0.26 | −0.85 |

| Germany | SXWESGU | 149.07 | 197.00 | 111.00 | 20.40 | −0.06 | −0.95 |

| Netherlands | EURONEXT100 | 985.54 | 1144.39 | 846.47 | 79.54 | −0.04 | −1.01 |

| Russia | MRSV | 1865.22 | 2875.55 | 1152.78 | 397.46 | −0.01 | −0.32 |

| Spain | IBEXFG | 9503.16 | 11,690.40 | 6576.10 | 1203.78 | −0.62 | 0.20 |

| UK | FT4GDBUK | 6231.08 | 7024.85 | 5211.55 | 494.37 | −0.31 | −1.11 |

| Brazil | ISE B3 | 2902.70 | 4182.17 | 2011.55 | 570.74 | 0.57 | −0.57 |

| Colombia | COLIR | 889.60 | 1075.67 | 704.79 | 99.50 | −0.07 | −1.05 |

| US | FT4GDBUS | 10,203.73 | 15,556.21 | 7338.26 | 2050.17 | 0.51 | −0.42 |

| Total Obs | 840 | ||||||

| Countries | Mean | Max | Min | Std. Dev. | Skew. | Kurt. |

|---|---|---|---|---|---|---|

| China | 247.46 | 661.83 | 60.21 | 137.45 | 0.88 | 0.50 |

| India | 73.55 | 167.75 | 32.88 | 28.73 | 1.17 | 1.76 |

| Japan | 116.34 | 212.49 | 63.29 | 32.57 | 1.14 | 1.36 |

| Singapore | 210.18 | 406.95 | 86.58 | 78.76 | 0.39 | −0.80 |

| Germany | 211.75 | 498.06 | 80.56 | 88.87 | 1.28 | 1.50 |

| Netherlands | 88.15 | 228.70 | 27.63 | 34.65 | 1.50 | 4.26 |

| Russia | 261.30 | 793.63 | 55.10 | 155.61 | 1.51 | 2.85 |

| Spain | 134.48 | 261.61 | 66.65 | 38.35 | 1.53 | 2.79 |

| UK | 393.69 | 1141.80 | 137.50 | 159.67 | 1.84 | 6.73 |

| Brazil | 247.27 | 676.96 | 68.46 | 113.96 | 1.16 | 2.06 |

| Colombia | 153.29 | 376.84 | 67.82 | 56.57 | 1.64 | 4.39 |

| US | 180.22 | 503.96 | 86.34 | 88.09 | 1.72 | 2.95 |

| Total Obs | 840 | |||||

| Summary | GOLD | OIL | BITCOIN |

|---|---|---|---|

| Mean | 1352.56 | 53.47 | 5483.87 |

| Max | 1969 | 77 | 28933 |

| Min | 1068 | 30 | 229 |

| Std. Dev | 217.25 | 11.03 | 5256.25 |

| Skew | 1.37 | 0.05 | 1.51 |

| Kurt | 1.03 | −0.60 | 4.09 |

| Variable | Levin-Lin-Chiu | Im-Pesaran-Shin | ||

|---|---|---|---|---|

| Level | 1st Difference | Level | 1st Difference | |

| SSMR | −4.034 *** | −32.645 *** | −3.327 | −31.051 *** |

| EPU | −9.457 *** | −9.124 *** | ||

| GOLD | 1.201 | −26.593 *** | 3.277 | −25.469 *** |

| OIL | −3.172 | −43.928 *** | −0.7404 | −40.965 *** |

| BTC | −4.486 *** | −28.3066 *** | −0.9973 | −26.481 *** |

| Kao Test | Pedroni Test | ||||

|---|---|---|---|---|---|

| Statistics | p-Value | Statistics | p-Value | ||

| Modified Dickey-Fuller | 3.138 | 0.0008 | Modified Phillips-Perron | −6.385 | 0.000 |

| Dickey-Fuller | 4.373 | 0.000 | Phillips-Perron | −9.006 | 0.000 |

| Augmented Dicky-Fuller | 5.107 | 0.000 | ADF | −9.286 | 0.000 |

| Unadjusted modified DF | −7.846 | 0.000 | |||

| Unadjusted DF | −4.0002 | 0.000 | |||

| Estimator | MG | PMG | |||

|---|---|---|---|---|---|

| Variable | Coefficient | p-Value | Coefficient | p-Value | |

| Long Run | EPU | −0.052 * (0.0226) | 0.022 | −0.071 ** (0.025) | 0.004 |

| GOLD | 0.256 * (0.119) | 0.031 | 0.503 *** (0.096) | 0.000 | |

| OIL | 0.204 *** (0.029) | 0.000 | 0.254 *** (0.053) | 0.000 | |

| BTC | 0.0323 *** (0.009) | 0.000 | 0.047 *** (0.009) | 0.000 | |

| Short Run | Ect | −0.490 *** (0.032) | 0.000 | −0.174 *** (0.044) | 0.000 |

| EPU | −0.010 (0.009) | 0.242 | −0.019 (0.013) | 0.137 | |

| GOLD | 0.0259 (0.045) | 0.572 | 0.061 (0.069) | 0.378 | |

| OIL | 0.067 *** (0.016) | 0.000 | 0.116 *** (0.020) | 0.000 | |

| BTC | 0.0459 *** (0.005) | 0.000 | 0.048 *** (0.006) | 0.000 | |

| Cons | 2.572 (0.587) | 0.000 | 0.433 (0.110) | 0.000 | |

| Hausman Test | 6.16 (0.8015) |

| Nation | ECT | D(EPU) | D(GOLD) | D(OIL) | D(BTC) | Const |

|---|---|---|---|---|---|---|

| China | −0.093 * (0.053) | 0.0136 (0.0183) | 0.448 *** (0.140) | 0.130 *** (0.042) | 0.05 *** (0.014) | 0.208 (0.143) |

| India | −0.374 *** (0.094) | −0.00003 (0.013) | 0.214 ** (0.104) | 0.0512 (0.04) | 0.06 *** (0.010) | 1.05 *** (0.400) |

| Japan | −0.144 *** (0.051) | −0.0306 (0.034) | −0.185 (0113) | 0.0116 (0.038) | 0.08 *** (0.012) | 0.705 ** (0.280) |

| Singapore | −0.055 (0.046) | −0.066 *** (0.022) | −0.113 (0.115) | 0.193 *** (0.037) | 0.019 * (0.012) | 0.121 (0.113) |

| Germany | −0.494 *** (0.104) | −0.020 (0.013) | −0.013 (0.103) | 0.040 (0.036) | 0.076 *** (0.008) | 0.182 (0.392) |

| Netherlands | −0.118 ** (0.057) | −0.019 * (0.012) | −0.063 (0.106) | 0.089 ** (0.036) | 0.054 *** (0.011) | 0.259 (0.158) |

| Russia | −0.162 *** (0.063) | 0.028 * (0.015) | 0.133 (0.170) | 0.067 (0.055) | 0.038 ** (0.018) | 0.476 ** (0.219) |

| Spain | −0.039 (0.036) | −0.137 *** (0.041) | −0.0213 (0.148) | 0.188 *** (0.049) | 0.036 ** (0.015) | 0.170 (0.166) |

| UK | −0.028 (0.036) | 0.006 (0.016) | −0.171 * (0.095) | 0.171 *** (0.030) | 0.035 *** (0.010) | 0.116 (0.155) |

| Brazil | −0.378 *** (0.093) | 0.008 (0.0198) | 0.437 *** (0.162) | 0.143 ** (0.058) | 0.020 (0.016) | 1.264 *** (0.402) |

| Colombia | −0.112 * (0.064) | −0.016 (0.020) | −0.047 (0.144) | 0.232 *** (0.048) | 0.04 *** (0.015) | 0.239 (0.164) |

| US | −0.087 (0.057) | 0.0026 (0.015) | 0.306 *** (0.103) | 0.070 ** (0.036) | 0.072 *** (0.010) | 0.400 (0.267) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Darsono, S.N.A.C.; Wong, W.-K.; Nguyen, T.T.H.; Wardani, D.T.K. The Economic Policy Uncertainty and Its Effect on Sustainable Investment: A Panel ARDL Approach. J. Risk Financial Manag. 2022, 15, 254. https://doi.org/10.3390/jrfm15060254

Darsono SNAC, Wong W-K, Nguyen TTH, Wardani DTK. The Economic Policy Uncertainty and Its Effect on Sustainable Investment: A Panel ARDL Approach. Journal of Risk and Financial Management. 2022; 15(6):254. https://doi.org/10.3390/jrfm15060254

Chicago/Turabian StyleDarsono, Susilo Nur Aji Cokro, Wing-Keung Wong, Tran Thai Ha Nguyen, and Dyah Titis Kusuma Wardani. 2022. "The Economic Policy Uncertainty and Its Effect on Sustainable Investment: A Panel ARDL Approach" Journal of Risk and Financial Management 15, no. 6: 254. https://doi.org/10.3390/jrfm15060254