The Spillover of Inflation among the G7 Countries

Abstract

:1. Introduction

2. Review of Literature

2.1. Business Cycle and International Co-Movement

2.2. Common Macroeconomic Shocks

2.3. Market-Driven Forces

2.4. Common Monetary Policies and Purchasing Power Parity

3. Methodology

3.1. The Spillover Index Framework of Diebold and Yilmaz

3.2. The Spillover Index Framework of Barunik and Krehlik

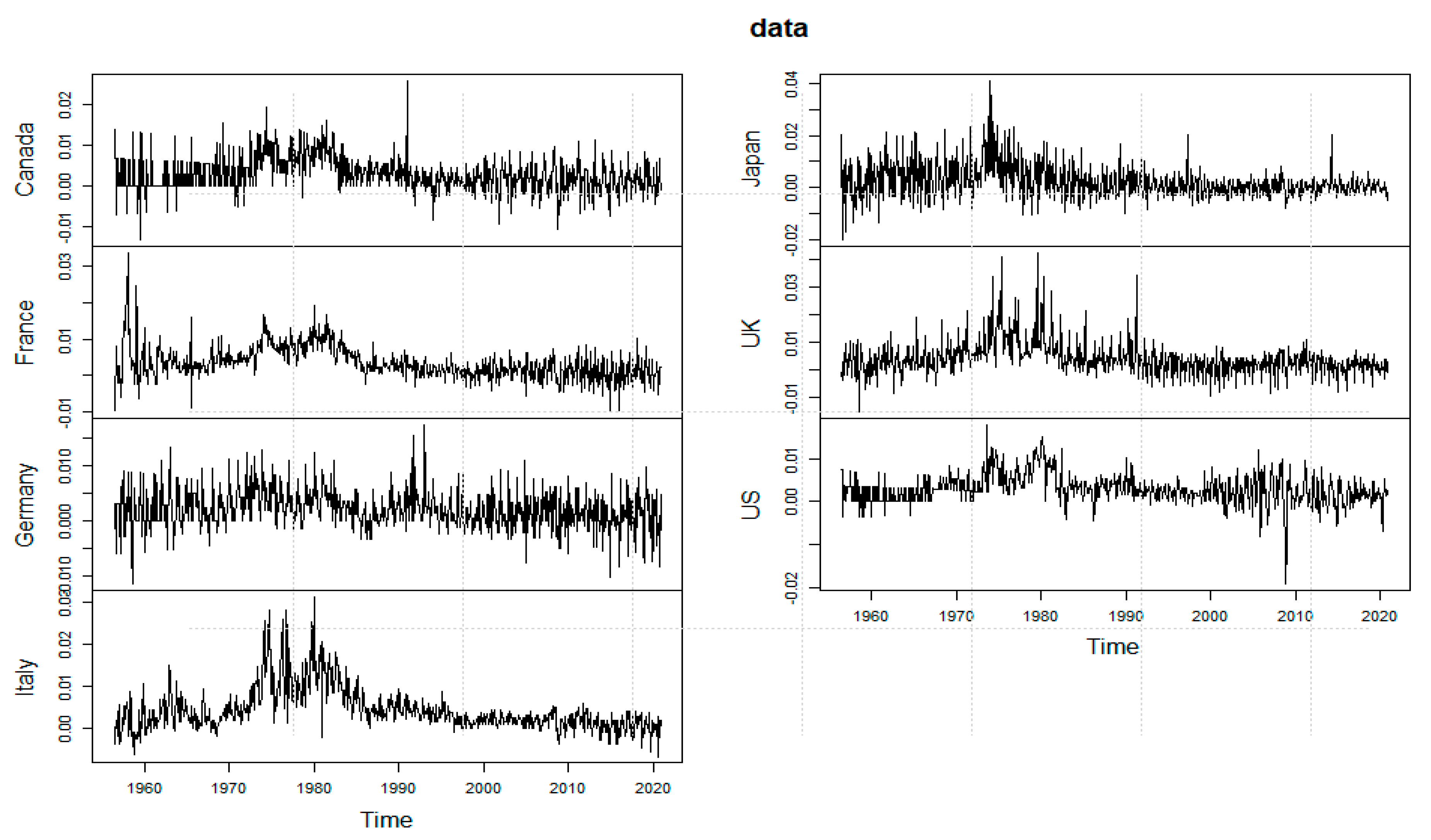

4. Data and Motivation

5. Estimation Findings

5.1. Estimation Results Based on the Spillover Index Methodology of Diebold and Yilmaz

5.2. Estimation Results Based on the Spillover Index Methodology of Barunik and Krehlik

6. Economic Analysis of the Findings

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

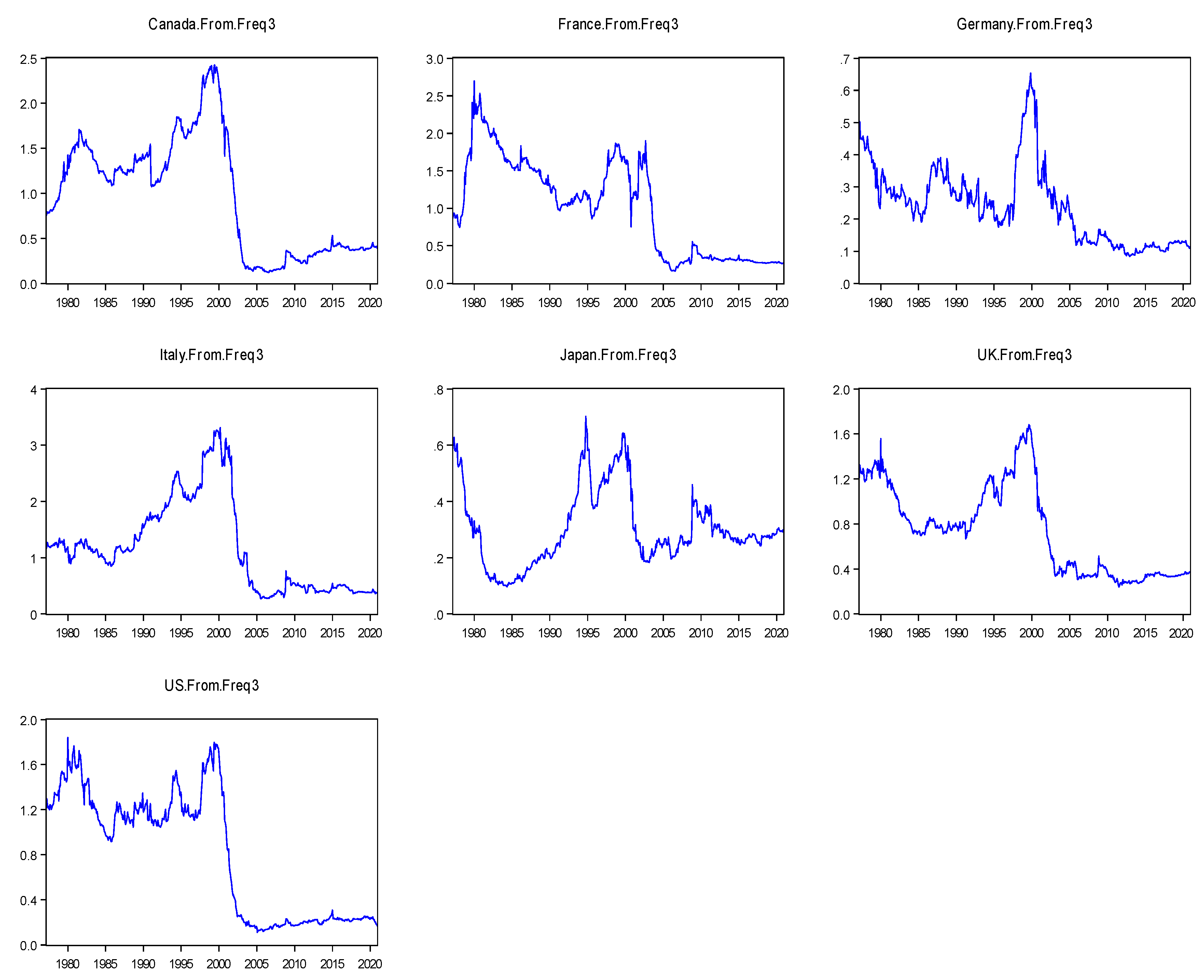

| 1 | The correlations of inflation between Canada and the United States were found to be 0.641 and 0.528 for the period of January 1956 to December 2015 and January 2016 to December 2020, respectively. So, the inflation spillover between Canada and the United States was low during the January 2016 to December 2020 period. |

| 2 | https://www.federalreserve.gov/boarddocs/testimony/2005/20051103/default.htm (accessed on 18 January 2021). |

| 3 |

References

- Aastveit, Knut Are, Hilde Christiane Bjørnland, and Leif Anders Thorsrud. 2016. The world is not enough! Small open economies and regional dependence. The Scandinavian Journal of Economics 118: 168–95. [Google Scholar] [CrossRef] [Green Version]

- Abosedra, Salah, Mahmoud Arayssi, Bernard Ben Sita, and Crispin Mutshinda. 2020. Exploring GDP growth volatility spillovers across countries. Economic Modelling 89: 577–89. [Google Scholar] [CrossRef]

- Alam, Md. Rafayet, and Khandokar Istiak. 2020. Impact of US policy uncertainty on Mexico: Evidence from linear and nonlinear tests. Quarterly Review of Economics and Finance 77: 355–66. [Google Scholar] [CrossRef]

- Antonakakis, Nikolas, and Harald Badinger. 2016. Economic growth, volatility, and cross-country spillovers: New evidence for the G7 countries. Economic Modelling 52: 352–65. [Google Scholar] [CrossRef] [Green Version]

- Arčabić, Vladimir, and Tihana Škrinjarić. 2021. Sharing is caring: Spillovers and synchronization of business cycles in the European Union. Economic Modelling 96: 25–39. [Google Scholar] [CrossRef]

- Aslanidis, Nektarios, Aurelio Bariviera, and Alejandro Perez-Laborda. 2021. Are cryptocurrencies becoming more interconnected? Economics Letters 199: 1–7. [Google Scholar] [CrossRef]

- Barunik, Jozef, and Tomáš Krehlik. 2018. Measuring the frequency dynamics of financial connectedness and systemic risk. Journal of Financial Econometrics 16: 271–96. [Google Scholar] [CrossRef]

- Beck, Günter W., Kristin Hubrich, and Marcellino Massimiliano. 2009. Regional inflation dynamics within and across euro area countries and a comparison with the United States [with discussion]. Economic Policy 24: 141–84. [Google Scholar] [CrossRef]

- Belke, Ansgar, and Thomas Osowski. 2019. Measuring fiscal spillovers in EMU and beyond: A Global VAR approach. Scottish Journal of Political Economy 66: 54–93. [Google Scholar] [CrossRef]

- Bernanke, Ben. 2007. Globalization and Monetary Policy. Remarks by Chairman Ben Shalom. Bernanke at the Fourth Economic Summit. Stanford: Stanford Institute for Economic Policy Research. [Google Scholar]

- Chang, Tsangyao, Wen-Chi Liu, and Chin-Ping Yu. 2010. Revisiting purchasing power parity for G7 countries: Further evidence based on panel SURKSS tests. Applied Economics Letters 17: 1383–87. [Google Scholar] [CrossRef]

- Ciccarelli, Matteo, and Benoit Mojon. 2010. Global inflation. The Review of Economics and Statistics 92: 524–35. [Google Scholar] [CrossRef]

- Clarida, Richard, Jordi Gali, and Mark Gertler. 1998. Monetary policy rules in practice: Some international evidence. European Economic Review 42: 1033–67. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis X., and Kamil Yilmaz. 2012. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting 28: 57–66. [Google Scholar] [CrossRef] [Green Version]

- Gambetti, Luca, and Alberto Musso. 2017. The Macroeconomic Impact of the ECB’s Expanded Asset Purchase Programme (APP). ECB Working Paper No. 2075. Frankfurt: ECB. [Google Scholar]

- Gefang, Deborah. 2008. Investigating nonlinear purchasing power parity during the post-Bretton Woods era—A Bayesian exponential smooth transition VECM approach. In Bayesian Econometrics. Advances in Econometrics. Edited by Siddhartha Chib, William Griffiths, Gary Koop and Dek Terrell. Bingley: Emerald Group Publishing Limited, vol. 23, pp. 471–500. [Google Scholar]

- Henriksen, Espen, Finn Kydland, and Roman Sustek. 2011. The High Cross-Country Correlations of Prices and Interest Rates. Discussion Paper 11/01. Nottingham: University of Nottingham, Centre for Finance, Credit and Macroeconomics (CFCM). [Google Scholar]

- Istiak, Khandokar, and Md. Rafayet Alam. 2019. Oil prices, policy uncertainty and asymmetries in inflation expectations. Journal of Economic Studies 46: 324–34. [Google Scholar] [CrossRef]

- Istiak, Khandokar, and Md. Rafayet Alam. 2020. US economic policy uncertainty spillover on the stock markets of the GCC countries. Journal of Economic Studies 47: 36–50. [Google Scholar] [CrossRef]

- Johnson, David. 2002. The effect of inflation targeting on the behavior of expected inflation: Evidence from an 11 country panel. Journal of Monetary Economics 49: 1521–38. [Google Scholar] [CrossRef]

- Kose, M. Ayhan, Christopher Otrok, and Charles H. Whiteman. 2003. International business cycles: World, region, and country-specific factors. American Economic Review 93: 1216–39. [Google Scholar] [CrossRef] [Green Version]

- Lv, Lei, Zhixin Liu, and Yingying Xu. 2019. Technological progress, globalization and low-inflation: Evidence from the United States. PLoS ONE 14: e0215366. [Google Scholar] [CrossRef]

- Monacelli, Tommaso, and Luca Sala. 2009. The international dimension of inflation: Evidence from disaggregated consumer price data. Journal of Money, Credit and Banking 41: 101–20. [Google Scholar] [CrossRef]

- Mumtaz, Haroon, Saverio Simonelli, and Paolo Surico. 2011. International co-movements, business cycle and inflation: A historical perspective. Review of Economic Dynamics 14: 176–98. [Google Scholar] [CrossRef] [Green Version]

- Neely, Christopher J., and David E. Rapach. 2011. International comovements in inflation rates and country characteristics. Journal of International Money and Finance 30: 1471–90. [Google Scholar] [CrossRef]

- O’Donnell, D. 2015. G7 in Figures. Wiesbaden: Statistisches Bundesamt (Federal Statistical Office). [Google Scholar]

- Osorio, Carolina, and D. Filiz Unsal. 2013. Inflation dynamics in Asia: Causes, changes, and spillovers from China. Journal of Asian Economics 24: 26–40. [Google Scholar] [CrossRef] [Green Version]

- Rogoff, Kenneth. 2003. Globalization and global disinflation. Economic Review 88: 45–80. [Google Scholar]

- Tiwari, Aviral Kumar, Niyati Bhanja, Arif Billah Dar, and Olaolu Richard Olayeni. 2015. Analyzing time-frequency based co-movement in inflation: Evidence from G-7 countries. Computational Economics 45: 91–109. [Google Scholar] [CrossRef]

- Tiwari, Aviral Kumar, Niyati Bhanja, and Arif Billah Dar. 2016. Frequency based co-movement of inflation in selected euro area countries. OECD Journal: Journal of Business Cycle Measurement and Analysis 2015: 1–13. [Google Scholar] [CrossRef]

- Tiwari, Aviral Kumar, Muhammad Shahbaz, Haslifah M. Hasim, and Mohamed M. Elheddad. 2019. Analysing the spillover of inflation in selected Euro-area countries. Journal of Quantitative Economics 17: 551–77. [Google Scholar] [CrossRef]

- Wang, Pengfei, and Yi Wen. 2007. Inflation dynamics: A cross-country investigation. Journal of Monetary Economics 54: 2004–31. [Google Scholar] [CrossRef] [Green Version]

- Yang, Jian, Hui Guo, and Zijun Wang. 2006. International transmission of inflation among G-7 countries: A data-determined VAR analysis. Journal of Banking & Finance 30: 2681–700. [Google Scholar]

- Zhou, Su, Mohsen Bahmani-Oskooee, and Ali M. Kutan. 2008. Purchasing power parity before and after the adoption of the Euro. Review of World Economics 144: 134–50. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Canada | France | Germany | Italy | Japan | UK | US | |

|---|---|---|---|---|---|---|---|

| Minimum | −0.013 | −0.01 | −0.012 | −0.007 | −0.02 | −0.016 | −0.019 |

| Maximum | 0.026 | 0.034 | 0.017 | 0.031 | 0.041 | 0.042 | 0.018 |

| Median | 0.002 | 0.003 | 0.002 | 0.003 | 0.001 | 0.003 | 0.003 |

| Mean | 0.003 | 0.003 | 0.002 | 0.004 | 0.002 | 0.004 | 0.003 |

| Standard Dev. | 0.004 | 0.004 | 0.004 | 0.005 | 0.007 | 0.006 | 0.003 |

| Jarque–Bera value | 108.8 | 783.0 | 67.4 | 827.8 | 657.5 | 2685.8 | 317.1 |

| Observations | 775 | 775 | 775 | 775 | 775 | 775 | 775 |

| Contribution from (→) Contribution to (↓) | Canada | France | Germany | Italy | Japan | UK | US | Contribution from Others |

|---|---|---|---|---|---|---|---|---|

| Canada | 67.51003 | 2.2799 | 2.1497 | 4.172 | 8.631 | 3.3201 | 11.9301 | 32.48 |

| France | 6.44 * | 61.9402 | 4.34 | 1.827 | 13.272 | 4.1601 | 8.0199 | 38.08 |

| Germany | 1.97001 | 6.8299 | 70.399 | 4.102 | 5.537 | 5.9003 | 5.2703 | 29.61 |

| Italy | 7.94003 | 2.0797 | 5.81 | 47.04 | 18.172 | 6.0802 | 12.88 | 52.99 |

| Japan | 2.06997 | 1.9502 | 8.2901 | 5.908 | 70.77 | 6.2097 | 4.83 | 29.26 |

| UK | 4.51003 | 2.4199 | 4.2399 | 3.92 | 16.023 | 57.3902 | 11.5003 | 42.63 |

| US | 5.56997 | 1.3503 | 3.5301 | 3.857 | 7.847 | 3.5301 | 74.298 | 25.69 |

| Contribution to others | 28.49 | 16.94 | 28.35 | 23.8 | 69.51 | 29.19 | 54.39 | ∑(Contribution to others) = ∑(Contribution from others) = 250.74 |

| Contribution to own and others | 96.01004 | 78.8501 | 98.7588 | 70.826 | 140.252 | 86.5907 | 128.7286 | ∑(Contribution to own and others) = 700 |

| Net inflation spillover | −3.9914 | −21.14 | −1.232 | −29.22 | 40.222 | −13.412 | 28.728 | |

| Spillover index (SI) = × 100 = 35.82 | ||||||||

| Canada | France | Germany | Italy | Japan | UK | US | |

|---|---|---|---|---|---|---|---|

| Canada | - | −4.1601 | 0.17969 | −3.76803 | 6.56103 | −1.18993 | 6.3601 * |

| France | 4.1601 | - | −2.4899 | −0.2527 | 11.3218 | 1.7402 | 6.6696 |

| Germany | −0.17969 | 2.4899 | - | −1.708 | −2.7531 | 1.6604 | 1.7402 |

| Italy | 3.76803 | 0.2527 | 1.708 | - | 12.264 | 2.1602 | 9.023 |

| Japan | −6.56103 | −11.3218 | 2.7531 | −12.264 | - | −9.8133 ** | −3.017 |

| UK | 1.18993 | −1.7402 | −1.6604 | −2.1602 | 9.8133 | - | 7.9702 |

| US | −6.36013 | −6.6696 | −1.7402 | −9.023 | 3.017 | −7.9702 | - |

| Panel A: The Spillover for Band 3.14 to 0.79 Roughly Corresponds to 1 to 4 Months (Short Term) | ||||||||

| Canada | France | Germany | Italy | Japan | UK | US | Contribution From | |

| Canada | 52.030 | 1.500 | 1.510 | 1.869 | 1.880 | 2.121 | 4.050 | 12.950 |

| France | 1.400 * | 29.130 | 2.730 | 0.763 | 1.440 | 2.821 | 1.550 | 10.710 |

| Germany | 1.290 | 5.680 | 46.250 | 3.283 | 2.440 | 4.452 | 2.240 | 19.390 |

| Italy | 1.120 | 1.230 | 1.240 | 20.797 | 1.480 | 1.470 | 1.240 | 7.770 |

| Japan | 1.660 | 1.560 | 2.750 | 5.068 | 46.470 | 5.698 | 2.790 | 19.530 |

| UK | 1.860 | 1.920 | 1.290 | 1.498 | 2.760 | 41.552 | 3.160 | 12.460 |

| US | 1.760 | 0.740 | 2.650 | 1.078 | 1.520 | 1.967 | 32.740 | 9.730 |

| Contribution to | 9.100 | 12.600 | 12.180 | 13.580 | 11.480 | 18.550 | 15.050 | ∑(Contribution to/from others) = 92.54 |

| Net spillover | −3.850 | 1.890 | −7.210 | 5.810 | −8.050 | 6.090 | 5.320 | SI = × 100 = 13.22 |

| Panel B: The Spillover for Band 0.79 to 0.31 Roughly Corresponds to 4 to 10 Months (Medium Term) | ||||||||

| Canada | France | Germany | Italy | Japan | UK | US | Contribution From | |

| Canada | 8.040 | 0.740 | 0.460 | 0.413 | 0.270 | 0.119 | 1.700 | 3.710 |

| France | 1.070 | 13.290 | 0.380 | 0.322 | 0.310 | 0.567 | 0.520 | 3.150 |

| Germany | 0.530 | 0.880 | 14.860 | 0.658 | 1.100 | 1.239 | 0.570 | 4.970 |

| Italy | 0.610 | 0.530 | 2.300 | 6.132 | 0.330 | 0.777 | 0.500 | 5.040 |

| Japan | 0.120 | 0.210 | 0.740 | 0.259 | 7.910 | 0.147 | 0.870 | 2.380 |

| UK | 0.640 | 0.070 | 2.030 | 0.539 | 1.000 | 7.567 | 0.410 | 4.690 |

| US | 1.470 | 0.430 | 0.520 | 0.560 | 0.570 | 0.567 | 17.360 | 4.130 |

| Contribution to | 4.480 | 2.870 | 6.440 | 2.730 | 3.570 | 3.430 | 4.550 | ∑(Contribution to/from others) = 28.07 |

| Net Spillover | 0.740 | −0.307 | 1.467 | −2.310 | 1.227 | −1.261 | 0.443 | SI = × 100 = 4.01 |

| Panel C: The Spillover for Band 0.31 to 0.00 Roughly Corresponds to 10 to An Infinite Number of Months (Long Term) | ||||||||

| Canada | France | Germany | Italy | Japan | UK | US | Contribution From | |

| Canada | 7.440 | 0.030 | 0.180 | 1.897 | 6.480 | 1.078 | 6.180 ** | 2.270 |

| France | 3.970 | 19.520 | 1.230 | 0.749 | 11.520 | 0.770 | 5.950 | 3.460 |

| Germany | 0.140 | 0.270 | 9.290 | 0.161 | 2.010 | 0.210 | 2.460 | 0.750 |

| Italy | 6.200 | 0.330 | 2.270 | 20.097 | 16.360 | 3.829 | 11.140 | 5.730 |

| Japan | 0.290 | 0.180 | 4.790 | 0.588 | 16.350 | 0.357 | 1.170 | 1.050 |

| UK | 2.010 | 0.430 | 0.920 | 1.883 | 12.270 | 8.267 | 7.920 | 3.630 |

| US | 2.330 | 0.190 | 0.360 | 2.219 | 5.760 | 0.980 | 24.200 | 1.690 |

| Contribution to | 14.980 | 1.400 | 9.730 | 7.490 | 54.390 | 7.210 | 34.860 | ∑(Contribution to/from others) = 28.07 |

| Net spillover | 12.710 | −2.060 | 8.980 | 1.760 | 53.340 | 3.580 | 33.170 | SI = × 100 = 18.58 |

| Panel A: The Spillover for 1 to 4 Months (Short Term) | |||||||

| Canada | France | Germany | Italy | Japan | UK | US | |

| Canada | - | 0.1001 | 0.2198 | 0.749 | 0.2205 | 0.2611 | 2.2904 * |

| France | −0.1001 | - | −2.9498 | −0.4669 | −0.1204 | 0.9009 | 0.8099 |

| Germany | −0.2198 | 2.9498 | - | 2.0433 | −0.3101 | 3.1619 | −0.4102 |

| Italy | −0.749 | 0.4669 | −2.0433 | - | −3.5882 | −0.028 | 0.1617 |

| Japan | −0.2205 | 0.1204 | 0.3101 | 3.5882 | - | 2.9379 | 1.2705 |

| UK | −0.2611 | −0.9009 | −3.1619 | 0.028 | −2.9379 | - | 1.1928 |

| US | −2.2904 | −0.8099 | 0.4102 | −0.1617 | −1.2705 | −1.1928 | - |

| Panel B: The Spillover for 4 to 10 Months (Medium Term) | |||||||

| Canada | France | Germany | Italy | Japan | UK | US | |

| Canada | - | −0.3304 | −0.07 | −0.1967 | 0.1505 | −0.5208 | 0.2303 |

| France | 0.3304 | - | −0.4998 | −0.2079 | 0.1001 | 0.497 | 0.0903 |

| Germany | 0.07 | 0.4998 | - | −1.6422 | 0.3598 | −0.791 | 0.0497 |

| Italy | 0.1967 | 0.2079 | 1.6422 | - | 0.0707 | 0.238 | −0.0602 |

| Japan | −0.1505 | −0.1001 | −0.3598 | −0.0707 | - | −0.8533 | 0.3003 |

| UK | 0.5208 | −0.497 | 0.791 | −0.238 | 0.8533 | - | −0.1568 |

| US | −0.2303 | −0.0903 | −0.0497 | 0.0602 | −0.3003 | 0.1568 | - |

| Panel C: The Spillover for 10 to An Infinite Number of Months (Long Term) | |||||||

| Canada | France | Germany | Italy | Japan | UK | US | |

| Canada | - | −3.9396 | 0.0399 | −4.3029 | 6.1901 | −0.9317 | 3.85 |

| France | 3.9396 | - | 0.9597 | 0.4193 | 11.34 | 0.3402 | 5.7603 |

| Germany | −0.0399 | −0.9597 | - | −2.1091 | −2.7804 | −0.7098 | 2.1 |

| Italy | 4.3029 | −0.4193 | 2.1091 | - | 15.7717 | 1.946 | 8.9208 |

| Japan | −6.1901 | −11.34 ** | 2.7804 | −15.7717 | - | −11.9133 | −4.5906 |

| UK | 0.9317 | −0.3402 | 0.7098 | −1.946 | 11.9133 | - | 6.9398 |

| US | −3.85 | −5.7603 | −2.1 | −8.9208 | 4.5906 | −6.9398 | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Istiak, K.; Tiwari, A.K.; Husain, H.; Sohag, K. The Spillover of Inflation among the G7 Countries. J. Risk Financial Manag. 2021, 14, 392. https://doi.org/10.3390/jrfm14080392

Istiak K, Tiwari AK, Husain H, Sohag K. The Spillover of Inflation among the G7 Countries. Journal of Risk and Financial Management. 2021; 14(8):392. https://doi.org/10.3390/jrfm14080392

Chicago/Turabian StyleIstiak, Khandokar, Aviral Kumar Tiwari, Humaira Husain, and Kazi Sohag. 2021. "The Spillover of Inflation among the G7 Countries" Journal of Risk and Financial Management 14, no. 8: 392. https://doi.org/10.3390/jrfm14080392