The Exposure of French and South Korean Firm Stock Returns to Exchange Rates and the COVID-19 Pandemic

Abstract

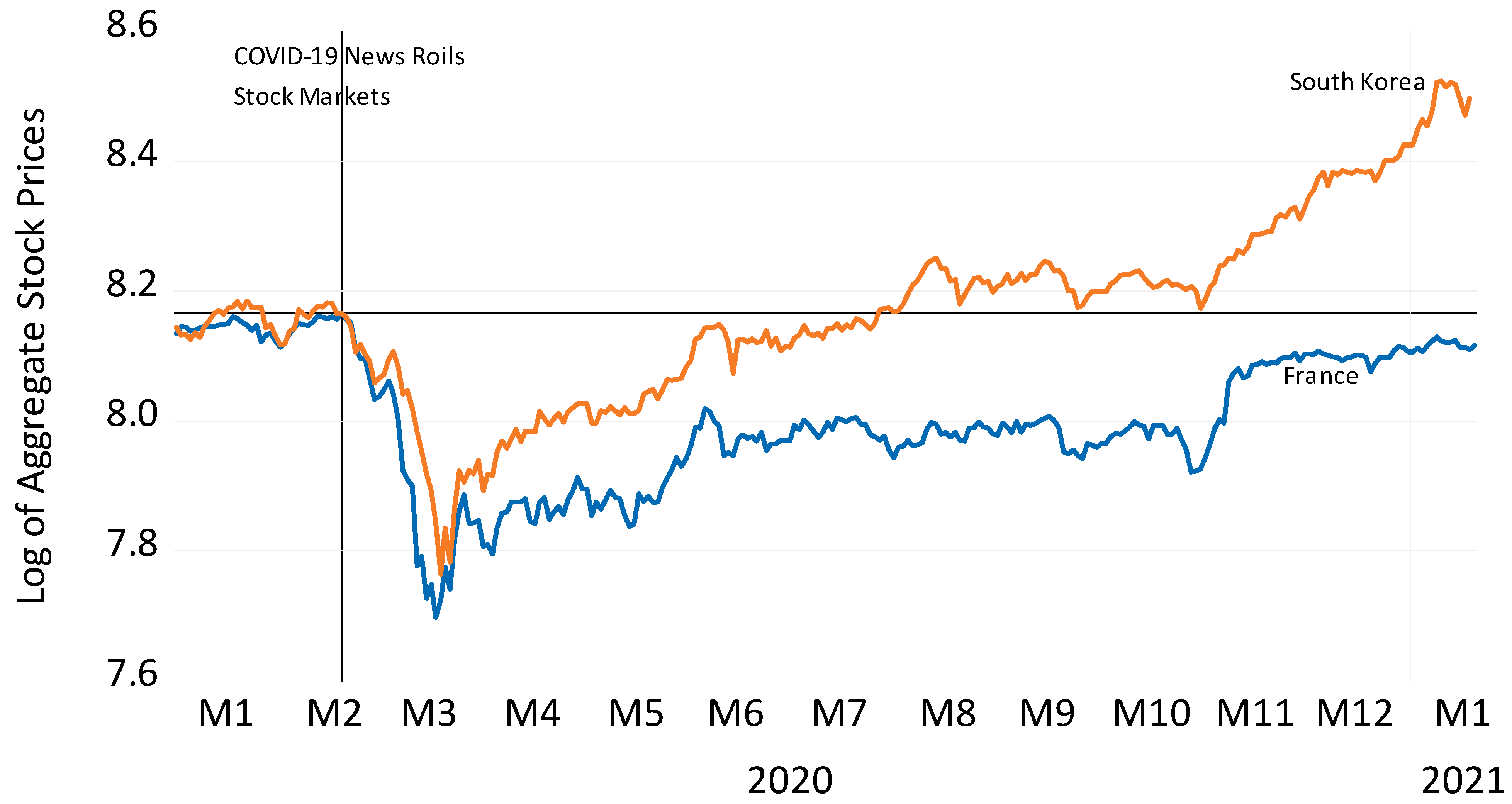

:1. Introduction

2. Materials and Methods

3. Results for Firms’ Exchange Rate Exposures

4. Results for Firms’ Exposures to the Pandemic

5. Discussion and Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Altavilla, Carlo, Luca Brugnolini, Refet S. Gürkaynak, Roberto Motto, and Giuseppe Ragusa. 2019. Measuring Euro. Area Monetary Policy. Journal of Monetary Economics 108: 162–79. [Google Scholar] [CrossRef]

- Aslam, Faheem, Wahbeeah Mohti, and Paulo Ferreira. 2020. Evidence of Intraday Multifractality in European. Stock Markets during the Recent Coronavirus (COVID-19) Outbreak. International Journal of Financial Studies 8: 31. [Google Scholar] [CrossRef]

- Baak, SaangJoon. 2014. Do Chinese and Korean Products Compete in the Japanese Market? An Investigation of Machinery Exports. Journal of the Japanese and International Economies 34: 256–71. [Google Scholar] [CrossRef]

- Baek, Jungho. 2013. Does the Exchange Rate Matter to Bilateral Trade between Korea and Japan? Evidence from Commodity Trade Data. Economic Modeling 30: 856–62. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring Economic Policy Uncertainty. Quarterly Journal of Economics 131: 1593–636. [Google Scholar] [CrossRef]

- Bénassy-Quéré, Agnès, Pierre-Olivier Gourinchas, Philippe Martin, and Guillaume Plantin. 2014. The Euro in the ‘Currency War’. Les notes du conseil d’analyse économique, no. 11. Paris: Conseil d’Analyse Economique. [Google Scholar]

- Berman, Nicolas, Philippe Martin, and Thierry Mayer. 2012. How Do Different Exporters React to Exchange Rate Changes? Quarterly Journal of Economics 127: 437–92. [Google Scholar] [CrossRef]

- Black, Fischer. 1987. Business Cycles and Equilibrium. New York: Basil Blackwell. [Google Scholar]

- Bouri, Elie, Oguzhan Cepni, David Gabauer, and Rangan Gupta. 2021. Return Connectedness across Asset Classes around the COVID-19 Outbreak. International Review of Financial Analysis 73: 101646. [Google Scholar] [CrossRef]

- Boz, Emine, Camila Casas, Georgios Georgiadis, Gita Gopinath, Helena Le Mezo, Arnaud Mehl, and Tra Nguyen. 2020. Patterns in Invoicing Currency in Global Trade. IMF Working Paper No. 20/126. Washington, DC: International Monetary Fund. [Google Scholar]

- Brown, Stephen J., and Jerold B. Warner. 1980. Measuring Security Price Performance. Journal of Financial Economics 8: 205–58. [Google Scholar] [CrossRef]

- Brown, Stephen J., and Jerold B. Warner. 1985. Using Daily Stock Returns: The Case of Event Studies. Journal of Financial Economics 14: 3–31. [Google Scholar] [CrossRef]

- Caldara, Dario, and Matteo Iacoviello. 2018. Measuring Geopolitical Risk. International Finance Discussion Paper No. 1222. Washington, DC: Federal Reserve Board. [Google Scholar]

- Chen, Nai-Fu, Richard Roll, and Stephen A. Ross. 1986. Economic Forces and the Stock Market. The Journal of Business 59: 383–403. [Google Scholar] [CrossRef]

- Conseil National de Productivité. 2019. Productivité et Compétitivité: Où En Est la France Dans la Zone Euro? Paris: Conseil National de Productivité. [Google Scholar]

- Dingel, Jonathan I., and Brent Neiman. 2020. How Many Jobs Can Be Done at Home? NBER Working Paper No. 26948. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Dominguez, Kathryn M. E., and Linda L. Tesar. 2006. Exchange Rate Exposure. Journal of International Economics 68: 188–218. [Google Scholar] [CrossRef]

- Gharib, Cheima, Salma Mefteh-Wali, and Sami Ben Jabeur. 2021. The Bubble Contagion Effect of COVID-19 Outbreak: Evidence from Crude Oil and Gold Markets. Financial Research Letters 38: 101703. [Google Scholar] [CrossRef]

- Goldstein, S. 2021. Here are the European Stocks with Pricing Power to Benefit When Pandemic Ends, according to Citigroup. Barrons, January 20. [Google Scholar]

- Héricourt, Jérôme, Philippe Martin, and Gianluca Orefice. 2014. Les Exportateurs Français Face aux Variations de L’euro. La Lettre du CEPII 340. Paris: Centre D’Etudes Prospectives et D’Information Internationales. [Google Scholar]

- Ilzetzki, Ethan, Carmen M. Reinhart, and Kenneth S. Rogoff. 2020. Will the Secular Decline in Exchange Rate and Inflation Volatility Survive COVID-19? NBER Working Paper No. 28108. Cambridge: National Bureau of Economic Research. [Google Scholar]

- IMF. 2013. Switzerland Selected Issues Paper. IMF Country Report, No. 13-129. Washington, DC: International Monetary Fund. [Google Scholar]

- IMF. 2020. France: Staff Report for the 2020 Article IV Consultation. Washington, DC: International Monetary Fund. [Google Scholar]

- Ito, Takatoshi, Satoshi Koibuchi, Kiyotaka Sato, and Junko Shimizu. 2016. Exchange Rate Exposure and Risk Management: The Case of Japanese Exporting Firms. Journal of the Japanese and International Economies 41: 17–29. [Google Scholar] [CrossRef] [Green Version]

- Kim, Soon Sung, Jaiho Chung, Joon Ho Hwang, and Ju Hyun Pyun. 2020. The Effectiveness of Foreign Debt in Hedging Exchange Rate Exposure: Multinational Enterprises vs. Exporting Firms. Pacific-Basin Finance Journal 64: 101455. [Google Scholar] [CrossRef]

- Kim, Kyungsoo. 2009. Global Financial Crisis and the Korean Economy. Paper presented at Federal Reserve Bank of San Francisco Conference “Asia and the Global Financial Crisis”, Santa Barbara, CA, USA, 19 October; Available online: www.frbsf.org (accessed on 23 February 2021).

- Okorie, David Iheke, and Boqiang Lin. 2021. Adaptive Market Hypothesis: The Story of the Stock Markets and COVID-19 Pandemic. The North American Journal of Economics and Finance 57: 101397. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., and Shuping Shi. 2018. Financial Bubble Implosion and Reverse Regression. Econometric Theory 34: 705–53. [Google Scholar] [CrossRef] [Green Version]

- Rogoff, Kenneth. 2020. The Calm before the Exchange-Rate Storm? Project Syndicate Weblog, November 10. [Google Scholar]

- Shahzad, Syed Jawad Hussain, Elie Bouri, Ladislav Kristoufek, and Tareq Saeed. 2021. Impact of the COVID-19 Outbreak on the US Equity Sectors: Evidence from quantile return spillovers. Financial Innovation 7: 1–23. [Google Scholar] [CrossRef]

- Sharif, Arshian, Chaker Aloui, and Larisa Yarovaya. 2020. Covid-19 Pandemic, Oil Prices, Stock Market, Geopolitical Risk and Policy Uncertainty Nexus in the U.S. economy: Fresh Evidence from the Wavelet Based Approach. International Review of Financial Analysis 70: 101496. [Google Scholar] [CrossRef]

- Thorbecke, Willem, and Atsuyuki Kato. 2018. Exchange Rates and the Swiss Economy. Journal of Policy Modeling 40: 1182–99. [Google Scholar] [CrossRef]

- Thorbecke, Willem. 2019a. How Oil Prices Affect East and Southeast Asian Economies: Evidence from Financial Markets and Implications for Energy Security. Energy Policy 128: 628–38. [Google Scholar] [CrossRef]

- Thorbecke, Willem. 2019b. Why Japan Lost Its Comparative Advantage in Producing Electronic Parts and Components. Journal of the Japanese and International Economies 54: 101050. [Google Scholar] [CrossRef] [Green Version]

- Yoshitomi, Masaru. 2003. Post-Crisis Development Paradigms in Asia. Tokyo: ADBI Publishing. [Google Scholar]

| 1 | These data are obtained from the Federal Reserve Bank of St. Louis Fred website and cover the period from 19 February 2020 and 11 March 2021. They are available at: https://fred.stlouisfed.org/ (accessed on 16 March 2021). |

| 2 | These data are available at: https://atlas.cid.harvard.edu/rankings/ (accessed on 17 March 2021). |

| 3 | These data come from www.statista.com (accessed on 17 March 2021). |

| 4 | These data are available here: https://www.ecb.europa.eu/pub/economic-research/resbull/2020/html/ecb.rb200722~528ea64f0d.et.html#:~:text=This%20section%20briefly%20introduces%20the%20new%20resource,%20the,policy%20announcements%20for%20a%20wide%20range%20of%20assets (accessed on 17 March 2021). |

| 5 | In cases when stock return data are unavailable on 22 January 2001, the data are employed beginning on the first date they are available. |

| 6 | In cases where the adjusted R-squared is less than 0.1, Equation (1) is not used to forecast returns. Not only are the forecasts worse in these cases, but also firms with low R-squared coefficients are often firms with very volatile returns. Including them in the sample could cloud inference. |

| 7 | An F-test permits rejection at the 1% level of the null hypothesis that the six coefficients on the monetary policy variables jointly equal zero. |

| 8 | The Financial Times rated Samsung as the 38th strongest brand in the world, one behind Hermès (see https://www.ft.com/content/3a3419f4-78b1-11e9-be7d-6d846537acab (accessed on 1 March 2021)). |

| 9 | I am indebted to Dr. Sebastien Lechevalier for this point. |

{kind=link}

{kind=link}

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|

| Firm or Portfolio (Market Capitalization in Millions of Euros) | Sector | Exposure to Euro/Dollar Exchange Rate | S.E. | Exposure to French Stock Market | S.E. | Exposure to World Stock Market | S.E. |

| AGGREGATE FRENCH STOCK MARKET | NA | −0.32 *** | 0.02 | NA | NA | 1.10 *** | 0.03 |

| AIRBUS (72,510) | Aerospace | −0.48 *** | 0.05 | 1.22 *** | 0.05 | 0 | 0.06 |

| STMICROELECTRONICS (37,940) | Semiconductors | −0.34 *** | 0.05 | 1.22 *** | 0.04 | 0.23 *** | 0.06 |

| CELLECTIS (1170) | Biotechnology | −0.34 *** | 0.11 | 0.48 *** | 0.08 | 0.24 ** | 0.11 |

| DEVOTEAM (830) | Computer Services | −0.33 *** | 0.07 | 0.67 *** | 0.06 | 0.30 *** | 0.08 |

| AB SCIENCE (756) | Biotechnology | −0.29 ** | 0.12 | 0.51 *** | 0.1 | 0.41 *** | 0.15 |

| SOITEC (3490) | Semiconductors | −0.25 *** | 0.09 | 1.01 *** | 0.07 | 0.56 *** | 0.1 |

| DASSAULT SYSTEMES (60,660) | Software | −0.25 *** | 0.04 | 0.88 *** | 0.04 | 0.12 ** | 0.05 |

| MAISONS DU MONDE (709) | Household Furnishings | −0.24 | 0.18 | 0.80 *** | 0.12 | 0.16 | 0.12 |

| ABIVAX (463) | Biotechnology | −0.22 | 0.21 | 0.54 *** | 0.17 | 0.03 | 0.23 |

| FOCUS HOME INTERACTIVE (322) | Electronic Entertainment | −0.20 | 0.12 | 0.34 *** | 0.09 | 0.25 ** | 0.12 |

| PUBLICIS GROUPE (10,620) | Media | −0.19 *** | 0.04 | 0.96 *** | 0.04 | 0.03 | 0.06 |

| TELEPERFORMANCE (16,679) | Industrial Support Services | −0.18 *** | 0.04 | 0.77 *** | 0.04 | 0.20 *** | 0.06 |

| SOLOCAL GROUP (394) | Media, Publishing | −0.17 | 0.14 | 0.82 *** | 0.11 | 0.23 | 0.25 |

| SOPRA STERIA GROUP (2920) | Computer Services | −0.17 *** | 0.06 | 0.77 *** | 0.05 | 0.12 ** | 0.05 |

| SODEXO (10,920) | Restaurants and Bars | −0.16 *** | 0.05 | 0.82 *** | 0.04 | 0.04 | 0.05 |

| EUTELSAT COMMUNICATIONS (2230) | Telecommunications Equipment | −0.16 *** | 0.04 | 0.49 *** | 0.04 | 0.06 | 0.05 |

| SOLUTIONS 30 SE (1060) | Computer Services | −0.16 ** | 0.08 | 0.21 *** | 0.07 | 0.28 *** | 0.09 |

| MGI DIGITAL Technology (304) | Electronic Equipment: Gauges and Meters | −0.16 *** | 0.06 | 0.13 ** | 0.05 | 0.32 *** | 0.08 |

| ESKER (1400) | Software | −0.16 ** | 0.08 | 0.32 *** | 0.07 | 0.44 *** | 0.1 |

| SII (432) | Computer Services | −0.16 *** | 0.05 | 0.23 *** | 0.04 | 0.19 ** | 0.08 |

| NANOBIOTIX (627) | Biotechnology | −0.16 | 0.14 | 0.58 *** | 0.11 | 0.51 *** | 0.13 |

| INNATE PHARMA (370) | Biotechnology | −0.15 | 0.11 | 0.77 *** | 0.09 | 0.28 ** | 0.12 |

| VETOQUINOL (1110) | Pharmaceuticals | −0.15 ** | 0.06 | 0.09 * | 0.05 | 0.24 *** | 0.09 |

| CLARANOVA (272) | Software | −0.15 | 0.13 | 0.55 *** | 0.09 | 0.39 ** | 0.16 |

| CARMAT (407) | Medical Equipment | −0.14 | 0.12 | 0.49 *** | 0.1 | 0.35 * | 0.18 |

| ALD (4890) | Computer Services | −0.13 | 0.25 | 1.00 *** | 0.11 | 0 | 0.21 |

| ID LOGISTICS GROUP (1310) | Delivery Services | −0.13 ** | 0.06 | 0.30 *** | 0.06 | 0.11 | 0.08 |

| BUREAU VERITAS (10,180) | Industrial Support Services | −0.13 ** | 0.05 | 0.54 *** | 0.03 | 0.27 *** | 0.05 |

| SUEZ (10,820) | Water | −0.13 ** | 0.05 | 0.80 *** | 0.04 | 0.01 | 0.06 |

| SES IMAGOTAG (694) | Electronic Equipment: Gauges and Meters | −0.13 * | 0.07 | 0.25 *** | 0.06 | 0.26 *** | 0.09 |

| CAPGEMINI (24,290) | Computer Services | −0.13 ** | 0.05 | 1.28 *** | 0.05 | 0.06 | 0.06 |

| EUROFINS SCIEN. (18,690) | Medical Services | −0.13 * | 0.07 | 0.48 *** | 0.05 | 0.30 *** | 0.07 |

| TECHNICOLOR (63) | Entertainment, Media | −0.12 | 0.1 | 1.04 *** | 0.08 | 0.28** | 0.11 |

| SARTORIUS STEDIM BIOTECH (36,360) | Medical Supplies | −0.12 ** | 0.05 | 0.27 *** | 0.05 | 0.15 ** | 0.06 |

| UBISOFT ENTERTAINMENT CAT A (10,198) | Electronic Entertainment | −0.11 | 0.08 | 0.91 *** | 0.08 | 0.20 * | 0.1 |

| ALTEN (3140) | Computer Services | −0.11 * | 0.06 | 0.99 *** | 0.06 | 0.11 | 0.08 |

| IPSOS (1290) | Media | −0.11 * | 0.05 | 0.53 *** | 0.05 | 0.24 *** | 0.07 |

| SAMSE (546) | Home Improvement Retailers | −0.11 ** | 0.04 | 0.02 | 0.04 | 0.19 *** | 0.06 |

| AKWEL (615) | Auto Parts | −0.10 | 0.08 | 0.22 *** | 0.08 | 0.19 * | 0.1 |

| SANOFI (123,030) | Pharmaceuticals | −0.10 *** | 0.03 | 0.99 *** | 0.03 | −0.27 *** | 0.04 |

| M6-METROPOLE TV (1900) | Radio Tv Broadcast | −0.10 ** | 0.04 | 0.73 *** | 0.04 | 0.18 *** | 0.06 |

| LA PERLA FASHION (399) | Clothing Accessories | −0.10 | 0.2 | −0.04 | 0.08 | −0.03 | 0.12 |

| BIOMERIEUX (15,090) | Medical Equipment | −0.09 ** | 0.04 | 0.34 *** | 0.06 | 0.15 ** | 0.07 |

| SAFRAN (50,920) | Industrial Goods and Services | −0.09 ** | 0.04 | 0.95 *** | 0.05 | 0.13 * | 0.07 |

| GAUMONT (374) | Entertainment, Media | −0.09 ** | 0.04 | 0.06 * | 0.03 | 0.10 ** | 0.05 |

| THALES (19,950) | Defense | −0.09 | 0.03 | 0.76 *** | 0.04 | 0 | 0.04 |

| BIC (2157) | Drug and Grocery Stores | −0.09 | 0.04 | 0.42 *** | 0.03 | 0.05 | 0.05 |

| IPSEN (6290) | Pharmaceuticals | −0.08 | 0.06 | 0.55 *** | 0.07 | 0.06 | 0.1 |

| BIGBEN INTERACTIVE (426) | Electronic Entertainment | −0.08 | 0.08 | 0.61 *** | 0.07 | 0.03 | 0.09 |

| CGG (658) | Oil Equipment and Services | −0.08 | 0.08 | 0.87 *** | 0.07 | 0.69 *** | 0.09 |

| NRJ GROUP (509) | Radio Tv Broadcast | −0.08 | 0.05 | 0.44 *** | 0.05 | 0.10 * | 0.06 |

| IGE + XAO (247) | Software | −0.08 * | 0.04 | 0.12 *** | 0.04 | 0.10 ** | 0.05 |

| MERCIALYS REIT (684) | Real Estate | −0.08 | 0.05 | 0.50 *** | 0.06 | 0.21 ** | 0.08 |

| NEOEN (4690) | Electricity | −0.08 | 0.19 | 0.42 ** | 0.16 | 0.06 | 0.19 |

| CHRISTIAN DIOR (80,330) | Clothing Accessories | −0.08 ** | 0.03 | 1.05 *** | 0.03 | 0.17 *** | 0.04 |

| ESSILORLUXOTTICA (58,540) | Medical Supplies | −0.08 * | 0.04 | 0.67 *** | 0.04 | −0.12 ** | 0.05 |

| CARBIOS (446) | Chemicals | −0.08 | 0.14 | 0.18 | 0.12 | 0.64 ** | 0.25 |

| ILIAD (10,950) | Telecommunications Services | −0.07 | 0.05 | 0.57 *** | 0.05 | 0.12 * | 0.07 |

| BOIRON (646) | Pharmaceuticals | −0.07 | 0.05 | 0.14 *** | 0.04 | 0.14 ** | 0.06 |

| ALTAREA (2390) | Real Estate | −0.07 | 0.06 | 0.18 *** | 0.05 | −0.03 | 0.07 |

| WORLDLINE (20,880) | Industrial Support Services | −0.07 | 0.08 | 0.80 *** | 0.11 | 0.14 | 0.14 |

| LAGARDERE GROUPE (2482) | Publishing | −0.07 | 0.05 | 0.94 *** | 0.04 | 0.10 * | 0.06 |

| BONDUELLE (652) | Food Producers | −0.07 | 0.04 | 0.23 *** | 0.04 | 0.17 *** | 0.05 |

| STEF (1010) | Trucking | −0.07 | 0.05 | 0.09 ** | 0.03 | 0.11 | 0.07 |

| OENEO (752) | Industrial Goods and Services | −0.07 | 0.07 | 0.27 ** | 0.05 | 0.26 *** | 0.08 |

| SOMFY (5480) | Electrical and Electronic Equipment | −0.07 | 0.04 | 0.13 *** | 0.03 | 0.14 *** | 0.05 |

| ESI GROUP (259) | Software | −0.06 | 0.05 | 0.29 *** | 0.08 | 0.03 | 0.09 |

| INFOTEL (289) | Computer Services | −0.06 | 0.05 | 0.25 *** | 0.03 | 0.14 ** | 0.06 |

| TEAM (49,672) | Aerospace | −0.06 | 0.12 | −0.08 | 0.07 | 0.09 | 0.09 |

| DASSAULT AVIATION (7450) | Aerospace | −0.06 | 0.05 | 0.26 *** | 0.04 | 0.16 *** | 0.06 |

| LECTRA (1010) | Software | −0.06 | 0.06 | 0.21 *** | 0.05 | 0.26 *** | 0.07 |

| BOLLORE (10,650) | Transportation Services | −0.06 | 0.05 | 0.48 *** | 0.04 | 0.13 *** | 0.06 |

| GL EVENTS (281) | Media | −0.06 | 0.06 | 0.33 *** | 0.06 | 0.29 *** | 0.1 |

| LVMH (271,260) | Clothing Accessories | −0.06 * | 0.03 | 1.15 *** | 0.03 | 0.05 | 0.05 |

| EDENRED (11,720) | Industrial Support Services | −0.05 | 0.09 | 0.81 *** | 0.05 | 0.14 ** | 0.07 |

| DELTA PLUS GROUP (618) | Clothing Accessories | −0.05 | 0.06 | 0.07 | 0.05 | 0.22 *** | 0.08 |

| GTT (273) | Oil Equipment and Services | −0.05 | 0.12 | 0.70 *** | 0.09 | 0.06 | 0.15 |

| WAVESTONE (664) | Computer Services | −0.05 | 0.05 | 0.13 *** | 0.04 | 0.33 *** | 0.06 |

| QUADIENT (702) | Electronic Office Equipment | −0.05 | 0.05 | 0.53 *** | 0.04 | 0.07 | 0.06 |

| MICHELIN (4140) | Tires | −0.04 | 0.04 | 0.93 *** | 0.03 | 0.27 *** | 0.06 |

| RAMSAY GEN SANTE (1960) | Health Care | −0.04 | 0.05 | 0.15 *** | 0.04 | 0.22 *** | 0.08 |

| KERING (69,450) | Apparel Retailers | −0.04 | 0.04 | 1.10 *** | 0.03 | −0.05 | −0.02 |

| ATOS (268) | Computer Services | −0.04 | 0.05 | 1.13 *** | 0.05 | 0.01 | 0.06 |

| KORIAN (3210) | Health Care | −0.04 | 0.04 | 0.41 *** | 0.05 | 0.04 | 0.07 |

| XPO LOGISTICS EUROPE (2750) | Transportation Services | −0.04 | 0.07 | 0.27 *** | 0.05 | 0.12 * | 0.07 |

| FIDUCIAL REAL ESTATE (389) | Real Estate | −0.04 | 0.04 | 0.02 | 0.03 | 0.04 | 0.05 |

| LUMIBIRD (381) | Medical Equipment | −0.04 | 0.08 | 0.32 *** | 0.08 | 0.22 ** | 0.09 |

| VIRBAC (1810) | Pharmaceuticals | −0.04 | 0.04 | 0.29 *** | 0.04 | 0.14 *** | 0.05 |

| COVIVIO HOTELS (2080) | Real Estate | −0.04 | 0.07 | 0.15 *** | 0.05 | 0.21 *** | 0.07 |

| HERMES INTL (96,660) | Clothing Accessories | −0.04 | 0.04 | 0.65 *** | 0.05 | 0.09 | 0.07 |

| BAINS MER MONACO (1520) | Casinos Gambling | −0.04 | 0.07 | 0 | 0.06 | 0.23 ** | 0.09 |

| DANONE (36,710) | Food Producers | −0.04 | 0.03 | 0.72 *** | 0.03 | −0.09 ** | 0.04 |

| AIR FRANCE-KLM (2110) | Travel and Leisure | −0.04 | 0.06 | 1.16 *** | 0.06 | 0.18 ** | 0.07 |

| VALNEVA (1220) | Biotechnology | −0.03 | 0.08 | 0.43 *** | 0.08 | 0.22 * | 0.11 |

| SHOWROOMPRIVE (419) | Apparel Retailers | −0.03 | 0.24 | 0.43 ** | 0.16 | 0.54 *** | 0.18 |

| ADP (10,190) | Transportation Services | −0.03 | 0.05 | 0.84 *** | 0.08 | 0.12 | 0.1 |

| SECHE ENVIRONNEMENT (380) | Waste and Disposal Services | −0.03 | 0.06 | 0.22 *** | 0.05 | 0.37 *** | 0.06 |

| LISI (1,210) | Aerospace | −0.03 | 0.05 | 0.45 *** | 0.05 | 0.17 ** | 0.08 |

| AXWAY SOFTWARE (537) | Software | −0.03 | 0.08 | 0.30 *** | 0.06 | 0.09 | 0.08 |

| SWORD GROUP (329) | Computer Services | −0.03 | 0.06 | 0.29 *** | 0.06 | 0.32 *** | 0.1 |

| LDLC.COM (37) | Computer Digital Services | −0.03 | 0.09 | 0.26 *** | 0.07 | 0.14 | 0.11 |

| MERSEN (EX LCL) (591) | Electrical and Electronic Equipment | −0.02 | 0.05 | 0.75 *** | 0.05 | 0.24 *** | 0.06 |

| EXEL INDUSTRIES (449) | Agricultural Machinery | −0.02 | 0.04 | 0.11 *** | 0.03 | 0.14 *** | 0.04 |

| INTERPARFUMS (1798) | Personal Goods | −0.02 | 0.04 | 0.38 *** | 0.04 | 0.10 * | 0.06 |

| GERARD PERRIER (268) | Electronic Components | −0.02 | 0.05 | 0.02 | 0.04 | 0.24 *** | 0.07 |

| NEURONES (601) | Computer Services | −0.02 | 0.04 | 0.29 *** | 0.04 | −0.02 | 0.06 |

| TOTAL GABON (617) | Oil | −0.02 | 0.06 | 0.21 *** | 0.04 | 0.26 *** | 0.07 |

| HOFFMANN GREEN CEMENT TECHNOLOGIES (465) | Cement | −0.02 | 0.43 | 0.26 | 0.17 | 0.37 ** | 0.16 |

| VALEO (7960) | Auto Parts | −0.02 | 0.06 | 1.06 *** | 0.06 | 0.30 *** | 0.08 |

| REMY COINTREAU (7970) | Distillers and Vintners | −0.02 | 0.04 | 0.52 *** | 0.04 | 0.16 ** | 0.07 |

| BENETEAU (1020) | Recreational Vehicles and Boats | −0.02 | 0.05 | 0.59 *** | 0.04 | 0.35 *** | 0.06 |

| ODET (FINC DE L’) (5032) | Transportation Services | −0.02 | 0.04 | 0.29 *** | 0.04 | 0.13 ** | 0.05 |

| L’OREAL (163,760) | Cosmetics | −0.02 | 0.03 | 0.98 *** | 0.03 | −0.19 *** | 0.04 |

| TRIGANO (2960) | Recreational Products | −0.01 | 0.07 | 0.57 *** | 0.06 | 0.42 *** | 0.07 |

| THERMADOR GROUPE (710) | Industrial Suppliers | −0.01 | 0.04 | 0.09 *** | 0.03 | 0.24 *** | 0.05 |

| RUBIS (4060) | Specialty Retailers | −0.01 | 0.04 | 0.39 *** | 0.03 | 0.17 *** | 0.05 |

| BEL (2410) | Food Producers | −0.01 | 0.07 | 0.08 * | 0.04 | 0.06 | 0.07 |

| FNAC DARTY (1290) | Specialty Retailers | −0.01 | 0.11 | 0.66 *** | 0.08 | 0.36 *** | 0.12 |

| MALTERIES F-BELGES (382) | Brewers | −0.01 | 0.06 | 0.02 | 0.09 | 0.08 | 0.1 |

| LEGRAND (20,790) | Electrical and Electronic Equipment | −0.01 | 0.04 | 0.95 *** | 0.04 | 0.03 | 0.06 |

| ARGAN (722) | Real Estate | −0.01 | 0.06 | 0.26 *** | 0.06 | 0.05 | 0.08 |

| TOTAL (92,295) | International Oil and Gas | −0.01 | 0.03 | 0.97 *** | 0.03 | 0 | 0.03 |

| BASTIDE(CONFORT MED.) (394) | Health Care | 0 | 0.06 | 0.22 *** | 0.05 | 0.25 *** | 0.06 |

| CREDIT AGRICOLE BRIE PICARDIE (1134) | Banks | 0 | 0.06 | 0.24 *** | 0.05 | 0.16 ** | 0.07 |

| ELIOR GROUP (989) | Consumer Services | 0 | 0.12 | 1.04 *** | 0.17 | 0.09 | 0.21 |

| GUERBET (427) | Pharmaceuticals | 0 | 0.06 | 0.26 *** | 0.05 | 0.06 | 0.07 |

| AUBAY (497) | Computer Services | 0 | 0.07 | 0.51 *** | 0.07 | 0.1 | 0.08 |

| TF1 (TV.FSE.1) (1500) | Media | 0 | 0.04 | 0.99 *** | 0.04 | 0.12 ** | 0.05 |

| TFF GROUP (611) | General Industrials | 0 | 0.04 | 0.10 | 0.03 | 0.12 ** | 0.06 |

| RENAULT (2342) | Automobiles | 0 | 0.05 | 1.14 *** | 0.04 | 0.46 *** | 0.06 |

| JCDECAUX (3690) | Media | 0 | 0.05 | 0.79 *** | 0.07 | 0.18 * | 0.09 |

| SELECTIRENTE (364) | Real Estate | 0 | 0.04 | −0.01 | 0.02 | 0.14 *** | 0.04 |

| MANUTAN INTL (577) | Industrial Suppliers | 0 | 0.05 | 0.18 *** | 0.04 | 0.1 | 0.07 |

| CREDIT AGR.ILE DE FRANCE (34,840) | Banks | 0 | 0.04 | 0.18 *** | 0.04 | 0.01 | 0.06 |

| VIVENDI (30,560) | Media | 0 | 0.05 | 1.28 *** | 0.08 | −0.29 *** | 0.09 |

| PERNOD-RICARD (42,932) | Distillers and Vintners | 0.01 | 0.04 | 0.61 *** | 0.04 | 0.05 | 0.08 |

| CRCAM NORD CCI (372) | Bank | 0.01 | 0.05 | 0.17 *** | 0.04 | 0.14 * | 0.08 |

| COLAS (4780) | Construction | 0.01 | 0.04 | 0.24 *** | 0.03 | 0.21 *** | 0.04 |

| ORPEA (7450) | Health Care | 0.01 | 0.04 | 0.54 *** | 0.04 | 0.10 * | 0.05 |

| VOLTALIA (2310) | Electricity | 0.01 | 0.1 | 0.07 | 0.06 | 0.27 *** | 0.09 |

| L AIR LQE.SC.ANYME. POUR L ETUDE ET L EPXTN (4780) | Chemicals | 0.01 | 0.02 | 0.91 *** | 0.02 | −0.02 | 0.04 |

| GROUPE CRIT (698) | Industrial Support Services | 0.01 | 0.07 | 0.30 *** | 0.07 | 0.29 *** | 0.1 |

| ORANGE (31,570) | Telecommunications Services | 0.01 | 0.05 | 1.26 *** | 0.05 | −0.35 *** | 0.05 |

| COVIVIO (6449) | Real Estate | 0.01 | 0.05 | 0.44 *** | 0.07 | 0.34 *** | 0.08 |

| IMMOBILIERE DASSAULT (397) | Real Estate | 0.01 | 0.04 | 0.02 | 0.03 | 0.09 | 0.06 |

| LDC (1700) | Food Producers | 0.01 | 0.03 | 0.09 *** | 0.03 | 0.06 | 0.04 |

| NEXITY (2130) | Real Estate | 0.02 | 0.06 | 0.72 *** | 0.04 | 0.37 *** | 0.07 |

| CREDIT FONCIER DE MONACO (NA) | Banks | 0.02 | 0.06 | 0.1 | 0.06 | 0.01 | 0.08 |

| BOUYGUES (12,760) | Construction | 0.02 | 0.03 | 1.15 *** | 0.04 | 0.02 | 0.05 |

| SAVENCIA (853) | Food Producers | 0.02 | 0.05 | 0.12 *** | 0.04 | 0.12 *** | 0.04 |

| UNIBEL (1510) | Food Producers | 0.02 | 0.06 | 0.02 | 0.04 | 0.02 | 0.06 |

| DERICHEBOURG (934) | Waste and Disposal Services | 0.02 | 0.09 | 1.08 *** | 0.08 | 0.35 *** | 0.1 |

| ACCOR (8080) | Hotels and Motels | 0.02 | 0.04 | 1.07 *** | 0.04 | 0.12 ** | 0.05 |

| VERALLIA (3660) | Industrial Goods and Services | 0.02 | 0.55 | 0.31 | 0.19 | 0.51 | 0.32 |

| LNA SANTE (470) | Health Care | 0.02 | 0.04 | 0.30 *** | 0.04 | 0.15 *** | 0.05 |

| GENSIGHT BIOLOGICS (299) | Health Care | 0.02 | 0.28 | 0.37 ** | 0.18 | 0.86 *** | 0.27 |

| GROUPE GUILLIN (463) | General Industrials | 0.02 | 0.05 | 0.13 *** | 0.04 | 0.08 | 0.06 |

| CEGEREAL REIT (509) | Real Estate | 0.02 | 0.04 | 0.18 *** | 0.04 | 0 | 0.06 |

| ROBERTET (2240) | Chemicals | 0.03 | 0.05 | 0.15 *** | 0.03 | 0.04 | 0.05 |

| KAUFMAN ET BROAD (841) | Home Constructions | 0.03 | 0.05 | 0.25 *** | 0.05 | 0.34 *** | 0.1 |

| X-FAB SILICON FOUNDRIES (929) | Semiconductor | 0.03 | 0.27 | 0.73 *** | 0.18 | 0.69 *** | 0.22 |

| ARKEMA (6790) | Chemicals | 0.03 | 0.06 | 1.05 *** | 0.05 | 0.25 *** | 0.07 |

| ICADE REIT (4442) | Real Estate | 0.03 | 0.04 | 0.39 *** | 0.06 | 0.30 *** | 0.06 |

| FONCIERE INEA (317) | Real Estate | 0.03 | 0.05 | 0.12 ** | 0.06 | −0.02 | 0.08 |

| CEGEDIM (337) | Computer Services | 0.04 | 0.05 | 0.24 ** | 0.05 | 0.11 * | 0.07 |

| CARREFOUR (11,900) | Food Retailers and Wholesalers | 0.04 | 0.04 | 1.05 *** | 0.04 | −0.16 *** | 0.04 |

| TESSI (424) | Computer Services | 0.04 | 0.05 | 0.11 *** | 0.04 | 0.17 *** | 0.05 |

| FREY (728) | Real Estate | 0.04 | 0.03 | 0.02 | 0.02 | 0 | 0.03 |

| COMPAGNIE DES ALPES (466) | Travel and Leisure | 0.04 | 0.04 | 0.23 *** | 0.04 | 0.06 | 0.06 |

| SOCIETE FONC.LYONNAISE (464) | Banks | 0.04 | 0.03 | 0.10 *** | 0.03 | 0.11 ** | 0.05 |

| PHARMAGEST INTERACTIVE (1710) | Software | 0.04 | 0.05 | 0.29 *** | 0.05 | −0.05 | 0.07 |

| EDF (32,490) | Electricity | 0.05 | 0.04 | 0.95 *** | 0.04 | −0.02 | 0.06 |

| H&K (2267) | Defense | 0.05 | 0.26 | 0.16 | 0.15 | −0.17 | 0.21 |

| ELECTRICITE STRASBOURG (864) | Electricity | 0.05 | 0.04 | 0.17 *** | 0.04 | 0.14 ** | 0.05 |

| HEXAOM (253) | Home Construction | 0.05 | 0.06 | 0.20 *** | 0.04 | 0.25 *** | 0.06 |

| JACQUET METALS (351) | Industrial Metals | 0.05 | 0.07 | 0.51 *** | 0.06 | 0.24 ** | 0.09 |

| MANITOU (1080) | Construction and Handling Machinery | 0.05 | 0.07 | 0.56 *** | 0.05 | 0.27 *** | 0.08 |

| REXEL (4760) | Electrical and Electronic Equipment | 0.05 | 0.06 | 1.07 *** | 0.07 | 0.15 * | 0.09 |

| CHARGEURS (511) | Textile Products | 0.06 | 0.06 | 0.38 *** | 0.05 | 0.21 ** | 0.08 |

| SERMA GROUP (308) | Industrial Support Services | 0.06 | 0.14 | −0.05 | 0.09 | 0.04 | 0.13 |

| KLEPIERRE REIT (5193) | Real Estate | 0.07 | 0.04 | 0.62 *** | 0.08 | 0.29 *** | 0.09 |

| LAURENT PERRIER (446) | Distillers and Vintners | 0.07 | 0.05 | 0.17 *** | 0.04 | 0.09 | 0.07 |

| IMERYS (3470) | Industrial Metals and Mines | 0.08 * | 0.04 | 0.65 *** | 0.04 | 0.30 *** | 0.06 |

| VOYAGEURS DU MONDE (281) | Travel and Tourism | 0.08 | 0.05 | 0.16 *** | 0.05 | 0.07 | 0.06 |

| SYNERGIE (770) | Industrial Support Services | 0.08 | 0.07 | 0.36 *** | 0.05 | 0.14 | 0.1 |

| GECINA (9140) | Real Estate | 0.08 * | 0.04 | 0.45 *** | 0.05 | 0.37 *** | 0.06 |

| RALLYE (346) | Retailers | 0.09 * | 0.05 | 0.79 *** | 0.05 | 0.13 * | 0.07 |

| ALBIOMA (1340) | Electricity | 0.09 * | 0.05 | 0.36 *** | 0.04 | 0.32 *** | 0.05 |

| VILMORIN & CIE (1210) | Food Producers | 0.09 ** | 0.04 | 0.17 *** | 0.03 | 0.25 *** | 0.05 |

| NATIXIS (144) | Banks | 0.09 | 0.07 | 1.08 *** | 0.08 | 0.31 *** | 0.1 |

| VALLOUREC (289) | Iron and Steel | 0.09 | 0.07 | 0.76 *** | 0.05 | 0.51 *** | 0.07 |

| FAURECIA (6040) | Auto Parts | 0.09 | 0.06 | 1.01 *** | 0.05 | 0.35 *** | 0.07 |

| MAUREL ET PROM (353) | Crude Oil Producers | 0.09 | 0.06 | 0.42 *** | 0.05 | 0.50 *** | 0.06 |

| BASSAC (767) | Real Estate | 0.1 | 0.09 | 0.48 *** | 0.07 | 0.12 | 0.09 |

| INVENTIVA (555) | Health Care | 0.1 | 0.41 | 0.72 *** | 0.26 | 0.29 | 0.29 |

| CASINO GUICHARD-P (2621) | Drugs/Grocery Stores | 0.10 ** | 0.04 | 0.76 *** | 0.03 | −0.03 | 0.04 |

| VICAT (1710) | Cements | 0.11 ** | 0.04 | 0.47 *** | 0.04 | 0.20 *** | 0.05 |

| GETLINK (7510) | Railroads | 0.12 * | 0.06 | 0.83 *** | 0.06 | 0.14 | 0.09 |

| PLASTIC OMNIUM (4920) | Auto Parts | 0.12 * | 0.07 | 0.69 *** | 0.05 | 0.16 ** | 0.07 |

| VINCI (48,951) | Construction | 0.12 *** | 0.04 | 0.91 *** | 0.05 | 0.15 *** | 0.05 |

| SCHNEIDER ELECTRIC (69,830) | Electrical and Electronic Equipment | 0.12 *** | 0.04 | 1.09 *** | 0.04 | 0.14 ** | 0.06 |

| VEOLIA ENVIRON (12,660) | Electronic Recycling | 0.13 *** | 0.04 | 0.90 *** | 0.04 | −0.01 | 0.06 |

| NEXANS (1050) | Electrical and Electronic Equipment | 0.13 ** | 0.06 | 0.92 *** | 0.05 | 0.34 *** | 0.06 |

| GALIMMO (461) | Real Estate | 0.16 | 0.15 | −0.05 | 0.15 | 0.1 | 0.2 |

| BURELLE (1580) | Auto Parts | 0.17 ** | 0.06 | 0.31 *** | 0.05 | 0.14 * | 0.07 |

| ALSTOM (16,210) | Electrical and Electronic Equipment | 0.18 ** | 0.08 | 1.19 *** | 0.07 | 0.05 | 0.09 |

| SOCIETE GENERALE (14,850) | Banks | 0.20 *** | 0.07 | 1.56 *** | 0.05 | 0.06 | 0.1 |

| EIFFAGE (8150) | Construction | 0.21 *** | 0.05 | 0.76 *** | 0.05 | 0.22 *** | 0.05 |

| BNP PARIBAS (54,890) | Banks | 0.21 *** | 0.05 | 1.48 *** | 0.05 | −0.07 | 0.1 |

| CREDIT AGRICOLE (29,560) | Banks | 0.25 *** | 0.06 | 1.43 *** | 0.05 | 0 | 0.09 |

| CARMILA (1650) | Real Estate | 0.27 | 0.25 | 0.21 | 0.13 | 0.26 | 0.19 |

| ELIS (2930) | Industrial Suppliers, Industrial Support Services’ | 0.29 ** | 0.14 | 1.18 *** | 0.18 | −0.07 | 0.2 |

| ERAMET (618) | Nonferrous Metals | 0.31 *** | 0.07 | 0.65 *** | 0.07 | 0.73 * | 0.1 |

| ALTAREIT (854) | Real Estate | 0.36 * | 0.21 | 0.09 | 0.09 | −0.04 | 0.16 |

| NOVACYT (596) | Medical Equipment | 0.48 * | 0.24 | −0.07 | 0.28 | 0.23 | 0.48 |

| SMCP (312) | Clothing Accessories | 0.56 | 0.38 | 1.57 *** | 0.19 | −0.41 | 0.29 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|

| Firm or Portfolio (Market Capitalization in Trillions of Korean Won) | Sector | Exposure to Won/Dollar Exchange Rate | S.E. | Exposure to Korean Stock Market | S.E. | Exposure to World Stock Market | S.E. |

| AGGREGATE KOREAN STOCK MARKET | NA | −0.25 *** | 0.03 | NA | NA | 0.64 *** | 0.02 |

| CELLTRION HEALTHCARE (21.89) | Biotechnology | 0.43 | 0.34 | 1.24 *** | 0.15 | −0.26 ** | 0.11 |

| PEARLABYSS (4.76) | Electronic Entertainment | 0.32 | 0.23 | 0.68 *** | 0.09 | 0.07 | 0.09 |

| NETMARBLE (11.85) | Electronic Entertainment | 0.29 | 0.26 | 0.81 *** | 0.11 | −0.01 | 0.09 |

| HYUNDAI MOTOR (27.18) | Automobiles | 0.28 *** | 0.06 | 1.14 *** | 0.03 | −0.10 *** | 0.03 |

| ORION (0.78) | Food Producers | 0.26 | 0.22 | 0.71 *** | 0.09 | −0.06 | 0.08 |

| KIA MOTORS (35.02) | Automobiles | 0.23 *** | 0.07 | 1.08 *** | 0.03 | −0.07 | 0.04 |

| LG ELECTRONICS (30.29) | Consumer Electronics | 0.21 *** | 0.05 | 1.04 *** | 0.02 | 0.02 | 0.04 |

| HYUNDAI MOBIS (31.51) | Auto Parts | 0.18 *** | 0.06 | 0.98 *** | 0.03 | −0.10 ** | 0.04 |

| LG DISPLAY (8.56) | Electronic Components | 0.16 ** | 0.06 | 1.11 *** | 0.04 | 0.06 | 0.05 |

| ECOPRO BM (3.93) | Electronic and Electrical Equipment | 0.14 | 0.47 | 1.12 *** | 0.14 | 0.14 | 0.12 |

| SAMSUNG ELTO.MECHANICS (20.99) | Electronic Components | 0.13 ** | 0.06 | 1.09 *** | 0.02 | 0.04 | 0.05 |

| LG INNOTEK (5.03) | Electronic Components | 0.13 | 0.12 | 1.08 *** | 0.08 | −0.02 | 0.06 |

| SAMSUNG BIOLOGICS (52.87) | Biologics | 0.12 | 0.24 | 1.01 *** | 0.11 | −0.10 | 0.12 |

| SAMSUNG ELECTRONICS (554.28) | Technology Hardware | 0.10 *** | 0.05 | 1.17 *** | 0.02 | −0.10 *** | 0.02 |

| SAMSUNG FIRE & MAR.IN. (8.57) | Insurance | 0.07 | 0.04 | 0.82 *** | 0.02 | −0.04 | 0.03 |

| SAMSUNG LIFE INSURANCE (14.34) | Insurance | 0.06 | 0.08 | 0.70 *** | 0.05 | 0.02 | 0.04 |

| HYUNDAI GLOVIS (7.82) | Trucking | 0.05 | 0.09 | 0.86 *** | 0.04 | 0 | 0.04 |

| NCSOFT (22.55) | Electronic Entertainment | 0.04 | 0.07 | 0.85 *** | 0.03 | 0.03 | 0.06 |

| NH INVESTMENT & SECS. (3.47) | Investment Banking and Brokerage | 0.04 | 0.1 | 1.44 *** | 0.03 | −0.02 | 0.04 |

| HANON SYSTEMS (9.80) | Auto Parts | 0.03 | 0.06 | 0.80 *** | 0.03 | 0 | 0.04 |

| COWAY (5.28) | Household Equipment Producers | 0.03 | 0.06 | 0.70 *** | 0.04 | −0.07 | 0.04 |

| LG (12.91) | Diversified Industrials | 0.03 | 0.05 | 1.06 *** | 0.03 | 0.05 | 0.04 |

| KAKAO (43.35) | Consumer Digital Services | 0.03 | 0.08 | 0.90 *** | 0.04 | 0.03 | 0.05 |

| KB FINANCIAL GROUP (18.76) | Banks | 0.02 | 0.1 | 1.08 *** | 0.03 | 0.03 | 0.05 |

| SAMSUNG SDI (55.11) | Technology Hardware | 0.01 | 0.05 | 1.02 *** | 0.03 | −0.01 | 0.04 |

| DOUZONBIZON (3.44) | Software and Computer Services | 0.01 | 0.09 | 0.74 *** | 0.05 | 0.06 | 0.07 |

| S-1 (3.093) | Security Services | 0.01 | 0.06 | 0.59 *** | 0.03 | −0.02 | 0.03 |

| SHINHAN FINL.GROUP (17.0) | Banks | 0 | 0.07 | 1.03 *** | 0.02 | −0.01 | 0.04 |

| CELLTRION (42.6) | Healthcare | 0 | 0.1 | 0.77 *** | 0.05 | −0.07 | 0.06 |

| WOORI FINANCIAL GROUP (7.0 | Banks | −0.01 | 0.1 | 0.89 *** | 0.06 | 0.01 | 0.06 |

| CELLTRION PHARM (5.79) | Pharmaceuticals | −0.01 | 0.13 | 0.74 *** | 0.07 | 0.05 | 0.07 |

| KT & G (10.8) | Tobacco | −0.02 | 0.05 | 0.37 *** | 0.02 | −0.04 | 0.02 |

| SAMSUNG SDS (15.5) | Computer Services | −0.03 | 0.13 | 0.88 *** | 0.07 | 0.09 | 0.06 |

| GREEN CROSS (4.37) | Pharmaceuticals | −0.04 | 0.05 | 0.42 *** | 0.05 | 0.01 | 0.05 |

| LG CHEM (64.7) | Chemicals | −0.04 | 0.06 | 1.10 *** | 0.03 | 0.04 | 0.04 |

| POSCO (21.0) | Iron and Steel | −0.05 | 0.06 | 0.90 *** | 0.02 | 0.11 *** | 0.03 |

| HANKOOK TIRE & TECHNOLOGY (6.5) | Tires | −0.06 | 0.11 | 0.82 *** | 0.07 | 0 | 0.05 |

| SK HYNIX (99.4) | Semiconductor | −0.06 | 0.09 | 1.39 *** | 0.05 | 0 | 0.07 |

| LG HHLD. & HLTH.CARE (27.7) | Drug-Grocery Stores | −0.06 | 0.06 | 0.60 *** | 0.03 | 0 | 0.04 |

| SKC (4.8) | Chemicals | −0.06 | 0.09 | 1.05 *** | 0.04 | 0.22 *** | 0.05 |

| GS HOLDINGS (3.9) | Diversified Industrials | −0.06 | 0.09 | 0.98 *** | 0.03 | 0.08 ** | 0.03 |

| KANGWON LAND (5.3) | Travel and Leisure | −0.06 | 0.06 | 0.68 *** | 0.03 | 0.04 | 0.03 |

| S-OIL (10.1) | Oil Refining and Marketing | −0.06 | 0.07 | 0.77 *** | 0.04 | 0.10 ** | 0.04 |

| MACQUARIE KOREA INFR.FD. (5.1) | Investment Banking | −0.07 * | 0.04 | 0.16 *** | 0.02 | 0.02 | 0.02 |

| AMOREPACIFIC (16.4) | Cosmetics | −0.07 | 0.07 | 0.53 *** | 0.04 | 0.01 | 0.04 |

| INDUSTRIAL BANK OF KOREA (6.2) | Banks | −0.07 | 0.08 | 0.99 *** | 0.03 | 0.11 *** | 0.04 |

| CJ ENM (3.1) | Retailers | −0.08 | 0.07 | 0.76 *** | 0.03 | 0.03 | 0.04 |

| DB INSURANCE (2.9) | Insurance | −0.08 | 0.13 | 1.07 *** | 0.05 | 0.02 | 0.05 |

| DONGSUH (4.2) | Food Producers | −0.08 | 0.06 | 0.25 *** | 0.02 | 0.01 | 0.03 |

| CJ LOGISTICS (3.9) | Transportation Services | −0.08 | 0.07 | 0.60 *** | 0.04 | −0.03 | 0.04 |

| NAVER (63.5) | Consumer Digital Services | −0.08 | 0.06 | 0.88 *** | 0.04 | −0.04 | 0.04 |

| SAMSUNG SECURITIES (3.4) | Investment Banking | −0.09 | 0.07 | 1.25 *** | 0.03 | 0.04 | 0.04 |

| LOTTE (6.3) | Food Producers | −0.1 | 0.09 | 0.49 *** | 0.03 | 0.07 * | 0.04 |

| LOTTE CHEMICAL (10.4) | Chemicals | −0.1 | 0.08 | 1.15 *** | 0.04 | 0.11 | 0.05 |

| KOREA ELECTRIC POWER (13.8) | Electricity | −0.11 | 0.08 | 0.64 *** | 0.03 | 0 | 0.04 |

| MIRAE ASSET DAEWOO (7.8) | Investment Banking | −0.11 * | 0.06 | 1.46 *** | 0.03 | 0.04 | 0.04 |

| SK HOLDINGS (19.8) | Software and Computer Services | −0.11 | 0.11 | 0.82 *** | 0.09 | 0.10 | 0.07 |

| YUHAN (4.5) | Pharmaceuticals | −0.11 * | 0.06 | 0.40 *** | 0.03 | 0 | 0.04 |

| HOTEL SHILLA (3.3) | Retailers | −0.12 | 0.08 | 0.82 *** | 0.03 | 0.11 *** | 0.04 |

| SAMSUNG C&T (23.4) | Construction | −0.12 | 0.11 | 1.15 *** | 0.06 | 0.01 | 0.06 |

| SEEGENE (4.0) | Biotechnology | −0.13 | 0.17 | 0.40 *** | 0.11 | 0.04 | 0.25 |

| SSANGYONG CEMENT INDL. (3.5) | Cement | −0.13 | 0.08 | 0.86 *** | 0.04 | 0.05 | 0.05 |

| E-MART (5.0) | Retailers | −0.13 | 0.1 | 0.54 *** | 0.04 | −0.02 | 0.05 |

| POSCO CHEMICAL (13.0) | Chemicals | −0.14 * | 0.07 | 0.51 *** | 0.04 | 0.05 | 0.04 |

| SK MATERIALS (3.4) | Basic Materials | −0.14 | 0.1 | 1.00 *** | 0.04 | 0.08 | 0.05 |

| HYUNDAI HEAVY INDUSTRIES (7.4) | Marine Transport | −0.15 ** | 0.07 | 1.12 *** | 0.03 | 0.15 *** | 0.03 |

| CJ CHEILJEDANG (7.1) | Food Producers | −0.15 | 0.1 | 0.58 *** | 0.08 | 0.06 | 0.09 |

| HANA FINANCIAL GROUP (10.9) | Banks | −0.15 | 0.12 | 1.06 *** | 0.04 | 0.06 | 0.08 |

| KOREAN AIR LINES (9.8) | Airlines | −0.16 | 0.1 | 1.07 *** | 0.04 | 0.04 | 0.04 |

| KUMHO PETRO CHEMICAL (7.8) | Chemicals | −0.17 | 0.1 | 0.99 *** | 0.05 | 0.17 ** | 0.07 |

| GS ENGR. & CON. (3.2) | Construction | −0.18 ** | 0.07 | 1.18 *** | 0.04 | 0.05 | 0.04 |

| HYUNDAI STEEL (5.3) | Iron and Steel | −0.19 *** | 0.06 | 1.07 *** | 0.03 | 0.23 *** | 0.04 |

| SK INNOVATION (26.6) | Oil Refining and Marketing | −0.19 ** | 0.07 | 1.24 *** | 0.05 | 0.11 *** | 0.04 |

| HLB (3.6) | Consumer Products and Services | −0.19 | 0.12 | 0.51 *** | 0.07 | 0.20 ** | 0.08 |

| KOREA INVESTMENT HDG. (4.0) | Investment Banking | −0.20 ** | 0.09 | 1.24 *** | 0.05 | 0.09 * | 0.05 |

| HANWHA SOLUTIONS (9.4) | Chemicals | −0.22 ** | 0.1 | 1.28 *** | 0.03 | 0.11 ** | 0.05 |

| HMM (5.7) | Marine Transportation | −0.22 ** | 0.09 | 0.95 *** | 0.04 | −0.04 | 0.06 |

| HANMI SCIENCE (4.5) | Pharmaceuticals | −0.23 ** | 0.06 | 0.65 *** | 0.04 | 0.03 | 0.05 |

| SAMSUNG HEAVY INDS. (24.9) | Marine Transport | −0.24 *** | 0.08 | 1.08 *** | 0.03 | 0.18 *** | 0.05 |

| KOREA ZINC (8.1) | Precious Metals and Mines | −0.25 *** | 0.08 | 0.89 *** | 0.03 | 0.12 *** | 0.04 |

| AMOREPACIFIC GROUP (6.6) | Cosmetics | −0.28 *** | 0.11 | 0.62 *** | 0.03 | 0.07 | 0.05 |

| DOOSAN HVY.IN&C. (4.2) | Industrial Machinery | −0.30 *** | 0.09 | 1.04 *** | 0.04 | 0.14 *** | 0.05 |

| ALTEOGEN (3.8) | Biotechnology | −0.35 | 0.26 | 0.85 *** | 0.15 | 0.37 *** | 0.14 |

| HYUNDAI ENGR & CON. (4.6) | Construction | −0.36 *** | 0.11 | 1.14 *** | 0.04 | −0.02 | 0.04 |

| SHIN POONG PHARM. (4.2) | Pharmaceuticals | −0.36 *** | 0.08 | 0.50 *** | 0.05 | 0.09 | 0.08 |

| CS WIND (3.3) | Energy | −0.37 ** | 0.18 | 0.83 *** | 0.11 | 0.30 *** | 0.12 |

| HYUNDAI HEAVY INDUSTRIES HOLDINGS (4.1) | Commercial Vehicle Parts | −0.37 | 0.25 | 0.93 *** | 0.08 | 0.05 | 0.07 |

| GENEXINE (2.5) | Biotechnology | −0.41 *** | 0.12 | 0.81 *** | 0.08 | 0.09 | 0.1 |

| HANMI PHARM (4.1) | Pharmaceuticals | −0.46 *** | 0.12 | 0.54 *** | 0.06 | −0.05 | 0.06 |

| HANJIN KAL (3.9) | Travel and Leisure | −0.58 *** | 0.21 | 0.65 *** | 0.15 | −0.11 | 0.25 |

| SK CHEMICALS (4.8) | Chemicals | −0.79 ** | 0.38 | 0.32 * | 0.17 | 0.05 | 0.19 |

| DOOSAN FUEL CELL (4.2) | Construction | −1.11 | 0.63 | 0.92 *** | 0.29 | 0.27 | 0.29 |

| (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|

| Firm or Portfolio (Market Capitalization in Millions of Euros) | Sector | ∆ Log of Stock Price between 19 February 2020 and 20 January 2021 Driven by All Factors | ∆ Log of Stock Price between 19 February 2020 and 20 January 2021 Driven by Macro Factors | ∆ Log of Stock Price between 19 February 2020 and 20 January 2021 Driven by Other Factors |

| AGGREGATE FRENCH STOCK MARKET | NA | −0.05 | 0.08 | −0.13 |

| AIRBUS (72,510) | Aerospace | −0.36 | −0.06 | −0.30 |

| STMICROELECTRONICS (37,940) | Semiconductors | 0.14 | −0.13 | 0.27 |

| DEVOTEAM (830) | Computer Services | 0.14 | −0.03 | 0.16 |

| SOITEC (3490) | Semiconductors | 0.72 | −0.09 | 0.81 |

| DASSAULT SYSTEMES (60,660) | Software | 0.03 | 0.01 | 0.02 |

| MAISONS DU MONDE (709) | Household Furnishings | 0.25 | −0.16 | 0.40 |

| PUBLICIS GROUPE (10,620) | Media | 0.05 | −0.07 | 0.13 |

| TELEPERFORMANCE (16,679) | Industrial Support Services | 0.17 | 0.04 | 0.13 |

| SOLOCAL GROUP (394) | Media, Publishing | −1.39 | −0.38 | −1.02 |

| SOPRA STERIA GROUP (2920) | Computer Services | −0.025 | 0.01 | 0.01 |

| SODEXO (10,920) | Restaurants and Bars | −0.25 | −0.02 | −0.22 |

| EUTELSAT COMMUNICATIONS (2230) | Telecommunications Equipment | −0.30 | −0.03 | −0.27 |

| INNATE PHARMA (370) | Biotechnology | −0.59 | −0.04 | −0.55 |

| ALD (4890) | Computer Services | −0.01 | −0.05 | 0.04 |

| BUREAU VERITAS (10,180) | Industrial Support Services | −0.10 | 0.05 | −0.15 |

| SUEZ (10,820) | Water | 0.11 | −0.10 | 0.21 |

| CAPGEMINI (24,290) | Computer Services | 0.08 | −0.12 | 0.20 |

| EUROFINS SCIEN (18,690) | Medical Services | 0.49 | 0.11 | 0.38 |

| TECHNICOLOR (63) | Entertainment, Media | −1.53 | −0.41 | −1.11 |

| UBISOFT ENTERTAINMENT CAT A (10,198) | Electronic Entertainment | 0.12 | 0.04 | 0.08 |

| ALTEN (3140) | Computer Services | −0.14 | 0 | −0.14 |

| IPSOS (1290) | Media | −0.11 | 0 | −0.11 |

| SANOFI (123,030) | Pharmaceuticals | −0.13 | −0.08 | −0.05 |

| M6-METROPOLE TV (1900) | Radio Tv Broadcast | −0.09 | −0.08 | −0.01 |

| BIOMERIEUX (15,090) | Medical Equipment | 0.22 | 0.06 | 0.16 |

| SAFRAN (50,920) | Industrial Goods and Services | −0.24 | 0.01 | −0.25 |

| THALES (19,950) | Defense | −0.20 | −0.02 | −0.18 |

| BIC (2157) | Drug and Grocery Stores | −0.22 | −0.02 | −0.20 |

| IPSEN (6290) | Pharmaceuticals | 0.08 | 0.05 | 0.02 |

| CGG (658) | Oil Equipment and Services | −1.15 | −0.18 | −0.97 |

| NRJ GROUP (509) | Radio Tv Broadcast | 0.07 | −0.11 | 0.18 |

| MERCIALYS REIT (684) | Real Estate | −0.46 | −0.01 | −0.45 |

| NEOEN (4690) | Electricity | 0.61 | 0.36 | 0.25 |

| CHRISTIAN DIOR (80,330) | Clothing Accessories | −0.01 | 0.05 | −0.06 |

| ESSILORLUXOTTICA (58,540) | Medical Supplies | −0.14 | 0.04 | −0.17 |

| ILIAD (10,950) | Telecommunications Services | 0.15 | 0.06 | 0.09 |

| WORLDLINE (20,880) | Industrial Support Services | −0.05 | 0.17 | −0.22 |

| LAGARDERE GROUPE (2482) | Publishing | 0.03 | −0.12 | 0.16 |

| BOLLORE (10,650) | Transportation Services | −0.06 | 0.07 | −0.13 |

| LVMH (271,260) | Clothing Accessories | 0.19 | 0.01 | 0.18 |

| EDENRED (11,720) | Industrial Support Services | −0.07 | 0.05 | −0.12 |

| GTT (273) | Oil Equipment and Services | −0.13 | 0.05 | 0.18 |

| QUADIENT (702) | Electronic Office Equipment | −0.32 | −0.03 | −0.30 |

| MICHELIN (4140) | Tires | 0.01 | 0.01 | 0 |

| KERING (69,450) | Apparel Retailers | −0.05 | −0.02 | −0.04 |

| ATOS (268) | Computer Services | −0.16 | −0.08 | −0.08 |

| KORIAN (3210) | Health Care | −0.30 | 0 | −0.30 |

| HERMES INTL (96,660) | Clothing Accessories | 0.20 | 0.10 | 0.10 |

| DANONE (36,710) | Food Producers | −0.26 | −0.03 | −0.23 |

| AIR FRANCE-KLM (2110) | Travel and Leisure | −0.69 | −0.09 | −0.59 |

| ADP (10,190) | Transportation Services | −0.57 | 0.07 | −0.63 |

| LISI (1210) | Aerospace | −0.35 | 0.07 | −0.42 |

| SWORD GROUP (329) | Computer Services | −0.02 | 0.09 | −0.11 |

| MERSEN (EX LCL) (591) | Electrical and Electronic Equipment | −0.11 | −0.06 | −0.05 |

| VALEO (7960) | Auto Parts | 0.15 | −0.01 | 0.16 |

| REMY COINTREAU (7970) | Distillers and Vintners | 0.33 | 0.03 | 0.30 |

| BENETEAU (1020) | Recreational Vehicles and Boats | 0.07 | −0.01 | 0.08 |

| L’OREAL (163,760) | Cosmetics | 0.08 | −0.03 | 0.10 |

| TRIGANO (2960) | Recreational Products | 0.59 | 0.08 | 0.51 |

| RUBIS (4060) | Specialty Retailers | −0.32 | 0.09 | −0.41 |

| FNAC DARTY (1290) | Specialty Retailers | 0.12 | 0.04 | 0.08 |

| LEGRAND (20,790) | Electrical and Electronic Equipment | 0.04 | 0.02 | 0.02 |

| TOTAL (92,295) | International Oil and Gas | −0.19 | −0.02 | −0.18 |

| ELIOR GROUP (989) | Consumer Services | −0.85 | −0.06 | −0.79 |

| TF1 (TV.FSE.1) (1500) | Media | −0.07 | −0.16 | 0.09 |

| RENAULT (2342) | Automobiles | 0.09 | −0.06 | 0.15 |

| JCDECAUX (3690) | Media | −0.34 | −0.01 | −0.33 |

| VIVENDI (30,560) | Media | 0.05 | −0.17 | 0.22 |

| PERNOD-RICARD (42,932) | Distillers and Vintners | −0.09 | 0.06 | −0.16 |

| COLAS (4780) | Construction | −0.09 | 0.04 | −0.12 |

| ORPEA (7450) | Health Care | −0.09 | 0.11 | −0.20 |

| L AIR LQE.SC.ANYME. POUR L ETUDE ET L EPXTN (4780) | Chemicals | −0.07 | 0.01 | −0.08 |

| ORANGE (31,570) | Telecommunications Services | −0.33 | −0.20 | −0.14 |

| COVIVIO (6449) | Real Estate | −0.45 | 0.10 | −0.55 |

| NEXITY (2130) | Real Estate | −0.19 | 0.06 | −0.25 |

| BOUYGUES (12,760) | Construction | −0.12 | −0.08 | −0.04 |

| DERICHEBOURG (934) | Waste and Disposal Services | 0.57 | −0.17 | 0.73 |

| ACCOR (8080) | Hotels and Motels | −0.26 | −0.04 | −0.22 |

| LNA SANTE (470) | Health Care | −0.01 | 0.11 | −0.12 |

| X-FAB SILICON FOUNDRIES (929) | Semiconductor | 0.34 | −0.16 | 0.50 |

| ARKEMA (6790) | Chemicals | 0.13 | 0.03 | 0.11 |

| ICADE REIT (4442) | Real Estate | −0.55 | 0.07 | −0.62 |

| CARREFOUR (11,900) | Food Retailers and Wholesalers | −0.08 | −0.15 | 0.07 |

| EDF (32,490) | Electricity | −0.11 | −0.14 | 0.03 |

| JACQUET METALS (351) | Industrial Metals | 0.06 | 0 | 0.05 |

| MANITOU (1080) | Construction and Handling Machinery | 0.41 | −0.01 | 0.42 |

| REXEL (4760) | Electrical and Electronic Equipment | 0.04 | −0.06 | 0.11 |

| KLEPIERRE REIT (5193) | Real Estate | −0.55 | 0.05 | −0.60 |

| IMERYS (3470) | Industrial Metals and Mines | 0.06 | 0.01 | 0.04 |

| GECINA (9140) | Real Estate | −0.42 | 0.07 | −0.55 |

| RALLYE (346) | Retailers | −0.42 | 0.07 | −0.49 |

| ALBIOMA (1340) | Electricity | 0.36 | 0.14 | 0.22 |

| NATIXIS (144) | Banks | −0.31 | −0.03 | −0.29 |

| VALLOUREC (289) | Iron and Steel | −1.27 | −0.03 | −1.24 |

| FAURECIA (6040) | Auto Parts | 0 | −0.01 | 0.01 |

| MAUREL ET PROM (353) | Crude Oil Producers | −0.34 | 0.06 | −0.39 |

| CASINO GUICHARD-P (2621) | Drugs/Grocery Stores | −0.30 | −0.09 | −0.21 |

| VICAT (1710) | Cements | −0.06 | 0.03 | −0.08 |

| GETLINK (7510) | Railroads | −0.20 | −0.06 | −0.14 |

| PLASTIC OMNIUM (4920) | Auto Parts | 0.29 | 0.09 | 0.20 |

| VINCI (48,951) | Construction | −0.25 | 0.03 | −0.27 |

| SCHNEIDER ELECTRIC (69,830) | Electrical and Electronic Equipment | 0.24 | 0.01 | 0.23 |

| VEOLIA ENVIRON (12,660) | Electronic Recycling | −0.21 | −0.08 | −0.13 |

| NEXANS (1050) | Electrical and Electronic Equipment | 0.29 | 0 | 0.29 |

| ALSTOM (16,210) | Electrical and Electronic Equipment | 0.10 | −0.10 | 0.20 |

| SOCIETE GENERALE (14,850) | Banks | −0.62 | −0.11 | −0.51 |

| EIFFAGE (8150) | Construction | −0.32 | 0.11 | −0.43 |

| BNP PARIBAS (54,890) | Banks | −0.19 | 0.08 | −0.11 |

| CREDIT AGRICOLE (29,560) | Banks | −0.27 | −0.09 | −0.18 |

| ELIS (2930) | Industrial Suppliers, Industrial Support Services’ | −0.32 | 0.06 | −0.38 |

| ERAMET (618) | Nonferrous Metals | 0.23 | 0.04 | 0.19 |

| SMCP (312) | Clothing Accessories | −0.47 | −0.55 | 0.08 |

| (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|

| Firm or Portfolio (Market Capitalization in Trillions of Korean Won) | Sector | ∆ Log of Stock Price between 19 February 2020 and 20 January 2021 Driven by All Factors | ∆ Log of Stock Price between 19 February 2020 and 20 January 2021 Driven by Macro Factors | ∆ Log of Stock Price between 19 February 2020 and 20 January 2021 Driven by Other Factors |

| AGGREGATE KOREAN STOCK MARKET | NA | 0.33 | 0.16 | 0.17 |

| CELLTRION HEALTHCARE (21.89) | Biotechnology | 0.76 | 0.60 | 0.16 |

| NETMARBLE (11.85) | Electronic Entertainment | 0.25 | 0.20 | 0.05 |

| HYUNDAI MOTOR (27.18) | Automobiles | 0.69 | 0.38 | 0.30 |

| KIA MOTORS (35.02) | Automobiles | 0.70 | 0.35 | 0.35 |

| LG ELECTRONICS (30.29) | Consumer Electronics | 0.77 | 0.31 | 0.45 |

| HYUNDAI MOBIS (31.51) | Auto Parts | 0.38 | 0.43 | −0.04 |

| LG DISPLAY (8.56) | Electronic Components | 0.29 | 0.25 | 0.05 |

| ECOPRO BM (3.93) | Electronic and Electrical Equipment | 0.80 | 0.69 | 0.11 |

| SAMSUNG ELTO.MECHANICS (20.99) | Electronic Components | 0.35 | 0.34 | 0.01 |

| LG INNOTEK (5.03) | Electronic Components | 0.23 | 0.38 | −0.15 |

| SAMSUNG BIOLOGICS (52.87) | Biologics | 0.46 | 0.69 | −0.24 |

| SAMSUNG ELECTRONICS (554.28) | Technology Hardware | 0.37 | 0.42 | −0.06 |

| SAMSUNG FIRE & MAR.IN. (8.57) | Insurance | −0.11 | 0.31 | −0.42 |

| SAMSUNG LIFE INSURANCE (14.34) | Insurance | 0.19 | 0.13 | 0.06 |

| HYUNDAI GLOVIS (7.82) | Trucking | 0.29 | 0.29 | 0 |

| NCSOFT (22.55) | Electronic Entertainment | 0.33 | 0.34 | −0.01 |

| NH INVESTMENT & SECS. (3.47) | Investment Banking and Brokerage | 0.05 | 0.38 | −0.33 |

| HANON SYSTEMS (9.80) | Auto Parts | 0.48 | 0.39 | 0.09 |

| COWAY (5.28) | Household Equipment Producers | 0 | 0.36 | −0.35 |

| LG (12.91) | Diversified Industrials | 0.29 | 0.39 | −0.10 |

| KAKAO (43.35) | Consumer Digital Services | 0.84 | 0.28 | 0.56 |

| KB FINANCIAL GROUP (18.76) | Banks | 0.08 | 0.32 | −0.24 |

| SAMSUNG SDI (55.11) | Technology Hardware | 0.79 | 0.35 | 0.43 |

| DOUZONBIZON (3.44) | Software and Computer Services | 0.11 | 0.23 | −0.22 |

| S-1 (3.093) | Security Services | 0.01 | 0.25 | −0.24 |

| SHINHAN FINL.GROUP (17.0) | Banks | −0.10 | 0.32 | −0.42 |

| WOORI FINANCIAL GROUP (7.0 | Banks | −0.02 | 0.20 | −0.21 |

| SAMSUNG SDS (15.5) | Computer Services | 0.01 | 0.24 | −0.23 |

| LG CHEM (64.7) | Chemicals | 0.90 | 0.49 | 0.42 |

| POSCO (21.0) | Iron and Steel | 0.23 | 0.30 | −0.07 |

| HANKOOK TIRE & TECHNOLOGY (6.5) | Tires | 0.38 | 0.15 | 0.23 |

| SK HYNIX (99.4) | Semiconductor | 0.23 | 0.34 | −0.11 |

| LG HHLD & HLTH.CARE (27.7) | Drug-Grocery Stores | 0.10 | 0.38 | −0.29 |

| SKC (4.8) | Chemicals | 0.68 | 0.40 | −0.28 |

| GS HOLDINGS (3.9) | Diversified Industrials | −0.16 | 0.32 | −0.48 |

| KANGWON LAND (5.3) | Travel and Leisure | −0.07 | 0.23 | −0.29 |

| S-OIL (10.1) | Oil Refining and Marketing | −0.04 | 0.32 | −0.37 |

| INDUSTRIAL BANK OF KOREA (6.2) | Banks | −0.16 | 0.33 | −0.48 |

| CJ ENM (3.1) | Retailers | 0.10 | 0.29 | −0.19 |

| DB INSURANCE (2.9) | Insurance | 0 | 0.47 | −047 |

| NAVER (63.5) | Consumer Digital Services | 0.49 | 0.47 | 0.01 |

| SAMSUNG SECURITIES (3.4) | Investment Banking | 0.16 | 0.34 | −0.18 |

| LOTTE CHEMICAL (10.4) | Chemicals | 0.35 | 0.47 | −0.12 |

| KOREA ELECTRIC POWER (13.8) | Electricity | −0.04 | 0.20 | −0.23 |

| MIRAE ASSET DAEWOO (7.8) | Investment Banking | 0.37 | 0.40 | −0.03 |

| SK HOLDINGS (19.8) | Software and Computer Services | 0.32 | 0.37 | −0.05 |

| HOTEL SHILLA (3.3) | Retailers | −0.11 | 0.37 | −0.48 |

| SAMSUNG C&T (23.4) | Construction | 0.20 | 0.36 | −0.16 |

| SSANGYONG CEMENT INDL. (3.5) | Cement | 0.35 | 0.31 | 0.04 |

| SK MATERIALS (3.4) | Basic Materials | 0.71 | 0.47 | 0.23 |

| HYUNDAI HEAVY INDUSTRIES (7.4) | Marine Transport | −0.04 | 0.41 | −0.45 |

| CJ CHEILJEDANG (7.1) | Food Producers | 047 | 0.16 | 0.31 |

| HANA FINANCIAL GROUP (10.9) | Banks | 0.15 | 0.33 | −0.18 |

| KOREAN AIR LINES (9.8) | Airlines | 0.43 | 0.36 | 0.07 |

| KUMHO PETRO CHEMICAL (7.8) | Chemicals | 0.90 | 0.42 | 0.48 |

| GS ENGR. & CON. (3.2) | Construction | 0.45 | 0.44 | 0 |

| HYUNDAI STEEL (5.3) | Iron and Steel | 0.47 | 0.43 | 0.05 |

| SK INNOVATION (26.6) | Oil Refining and Marketing | 0.69 | 0.39 | 0.30 |

| KOREA INVESTMENT HDG. (4.0) | Investment Banking | 0.25 | 0.49 | −0.25 |

| HANWHA SOLUTIONS (9.4) | Chemicals | 1.10 | 0.42 | 0.68 |

| HMM (5.7) | Marine Transportation | 1.39 | 0.42 | 0.68 |

| SAMSUNG HEAVY INDS. (24.9) | Marine Transport | 0.04 | 0.34 | −0.30 |

| KOREA ZINC (8.1) | Precious Metals and Mines | −0.10 | 0.37 | −0.46 |

| AMOREPACIFIC GROUP (6.6) | Cosmetics | −0.14 | 0.37 | −0.52 |

| DOOSAN HVY.IN&C. (4.2) | Industrial Machinery | 0.94 | 0.39 | 0.55 |

| ALTEOGEN (3.8) | Biotechnology | 0.011 | 0.04 | 0.04 |

| HYUNDAI ENGR & CON. (4.6) | Construction | 0.17 | 0.30 | −0.14 |

| CS WIND (3.3) | Energy | 1.59 | 0.36 | 1.24 |

| HYUNDAI HEAVY INDUSTRIES HOLDINGS (4.1) | Commercial Vehicle Parts | −0.09 | 0.18 | −0.27 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Thorbecke, W. The Exposure of French and South Korean Firm Stock Returns to Exchange Rates and the COVID-19 Pandemic. J. Risk Financial Manag. 2021, 14, 154. https://doi.org/10.3390/jrfm14040154

Thorbecke W. The Exposure of French and South Korean Firm Stock Returns to Exchange Rates and the COVID-19 Pandemic. Journal of Risk and Financial Management. 2021; 14(4):154. https://doi.org/10.3390/jrfm14040154

Chicago/Turabian StyleThorbecke, Willem. 2021. "The Exposure of French and South Korean Firm Stock Returns to Exchange Rates and the COVID-19 Pandemic" Journal of Risk and Financial Management 14, no. 4: 154. https://doi.org/10.3390/jrfm14040154