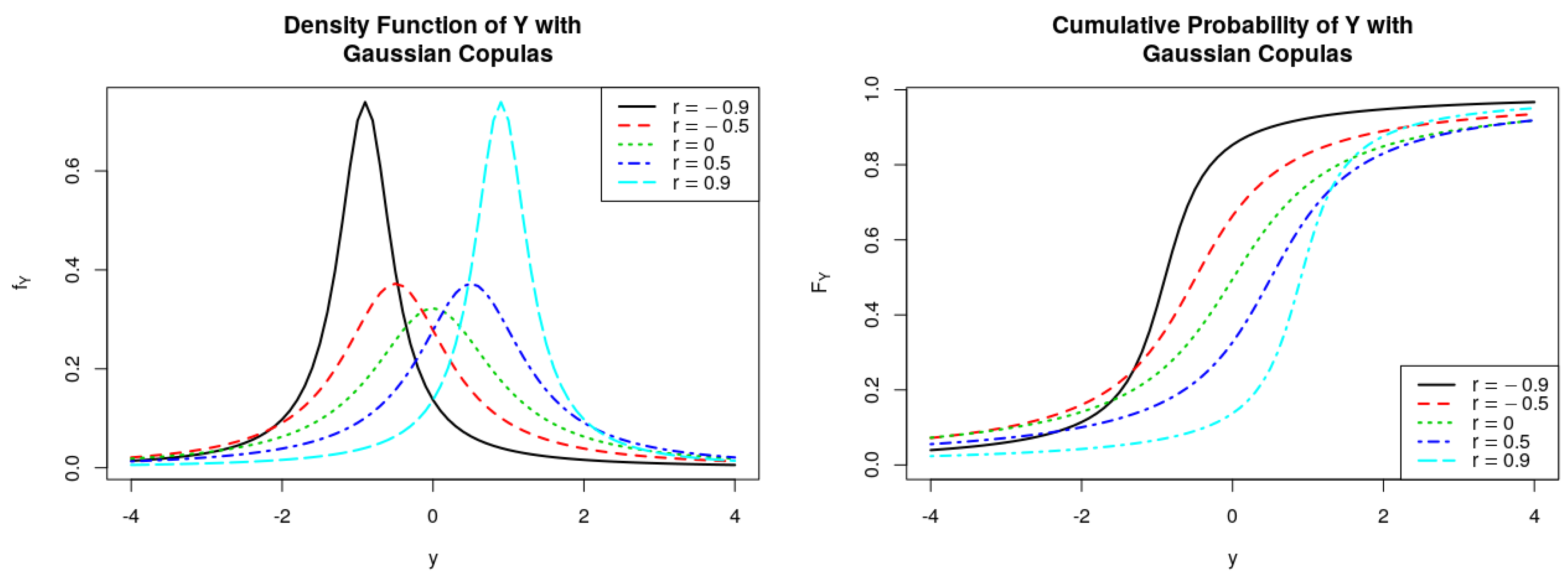

Figure 1.

PDFs and CDFs of the ratio , where follows Gaussian Copulas.

Figure 1.

PDFs and CDFs of the ratio , where follows Gaussian Copulas.

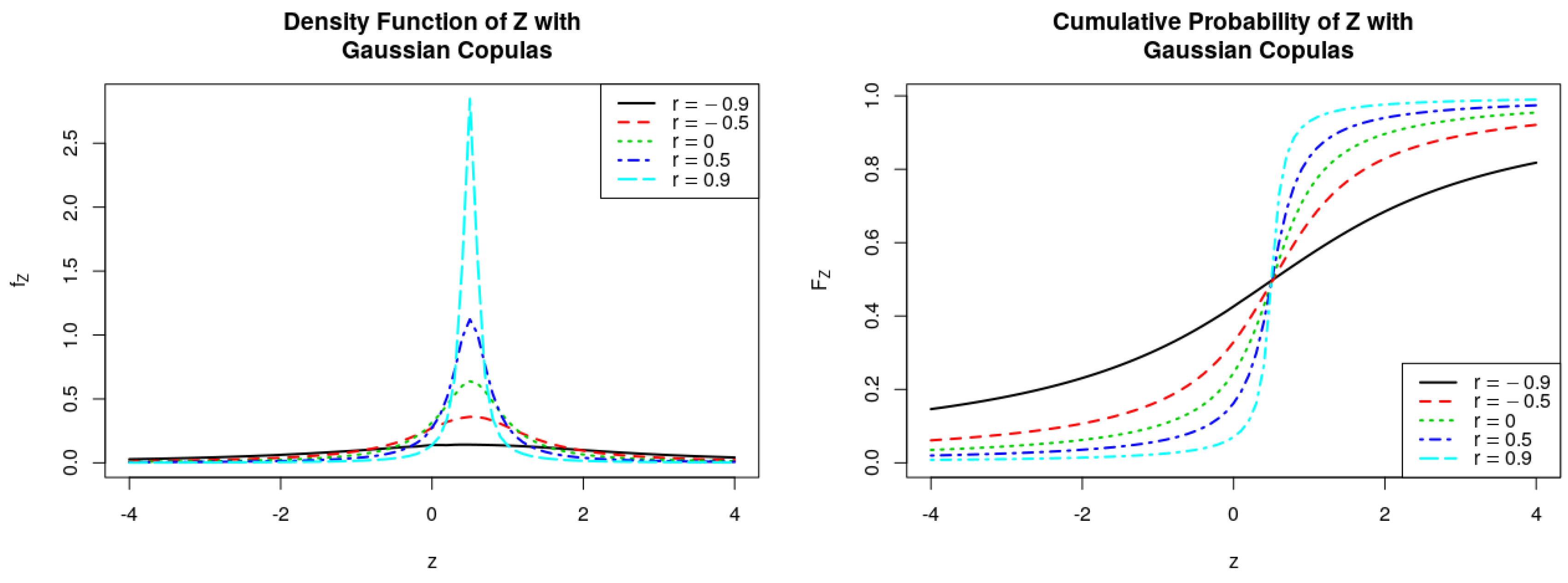

Figure 2.

PDFs and CDFs of the ratio , where follows Gaussian Copulas.

Figure 2.

PDFs and CDFs of the ratio , where follows Gaussian Copulas.

Figure 3.

PDFs and CDFs of the ratio , where follows Student-t Copulas, .

Figure 3.

PDFs and CDFs of the ratio , where follows Student-t Copulas, .

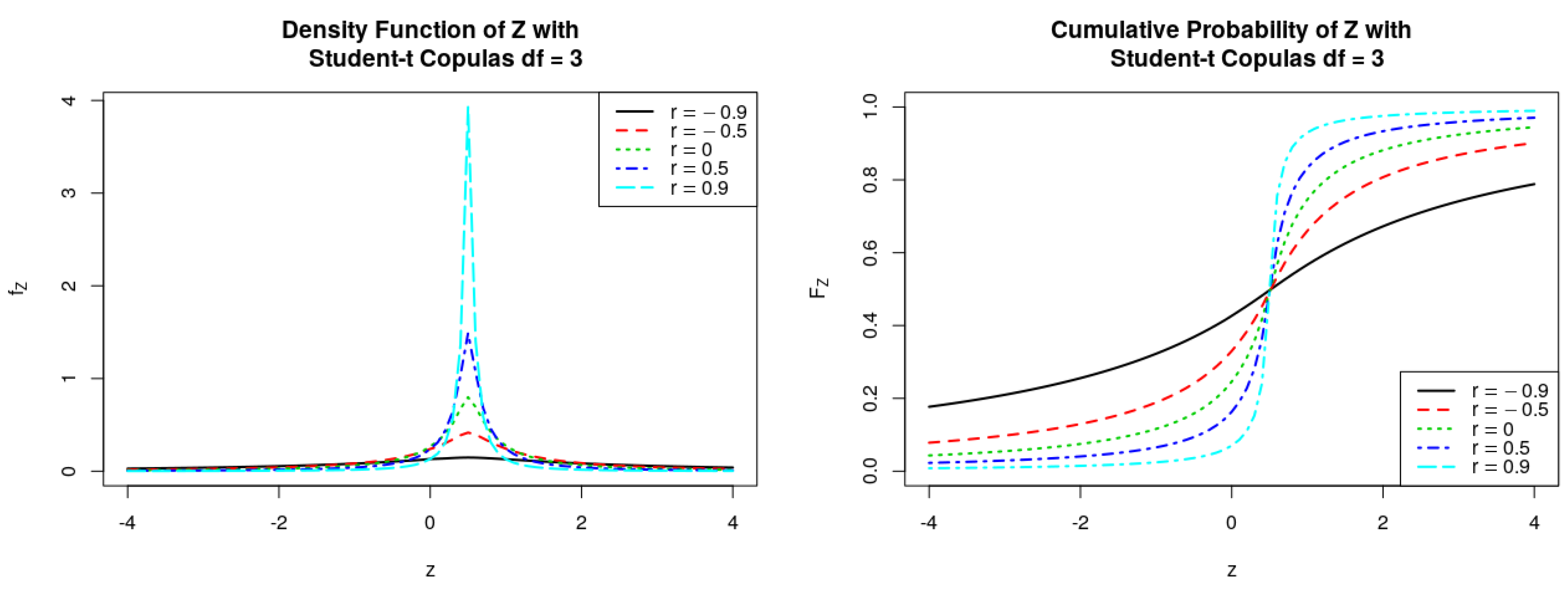

Figure 4.

PDFs and CDFs of the ratio , where follows Student-t Copulas, .

Figure 4.

PDFs and CDFs of the ratio , where follows Student-t Copulas, .

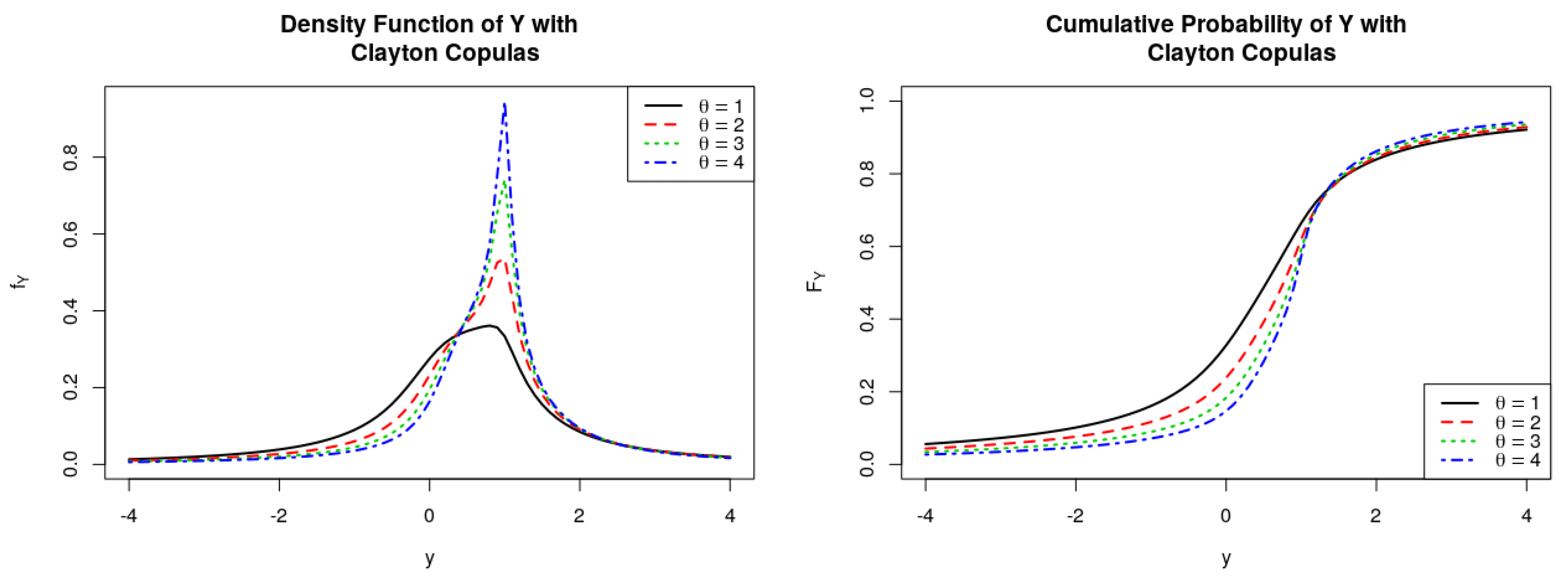

Figure 5.

PDFs and CDFs of the ratio , where follows Clayton Copulas.

Figure 5.

PDFs and CDFs of the ratio , where follows Clayton Copulas.

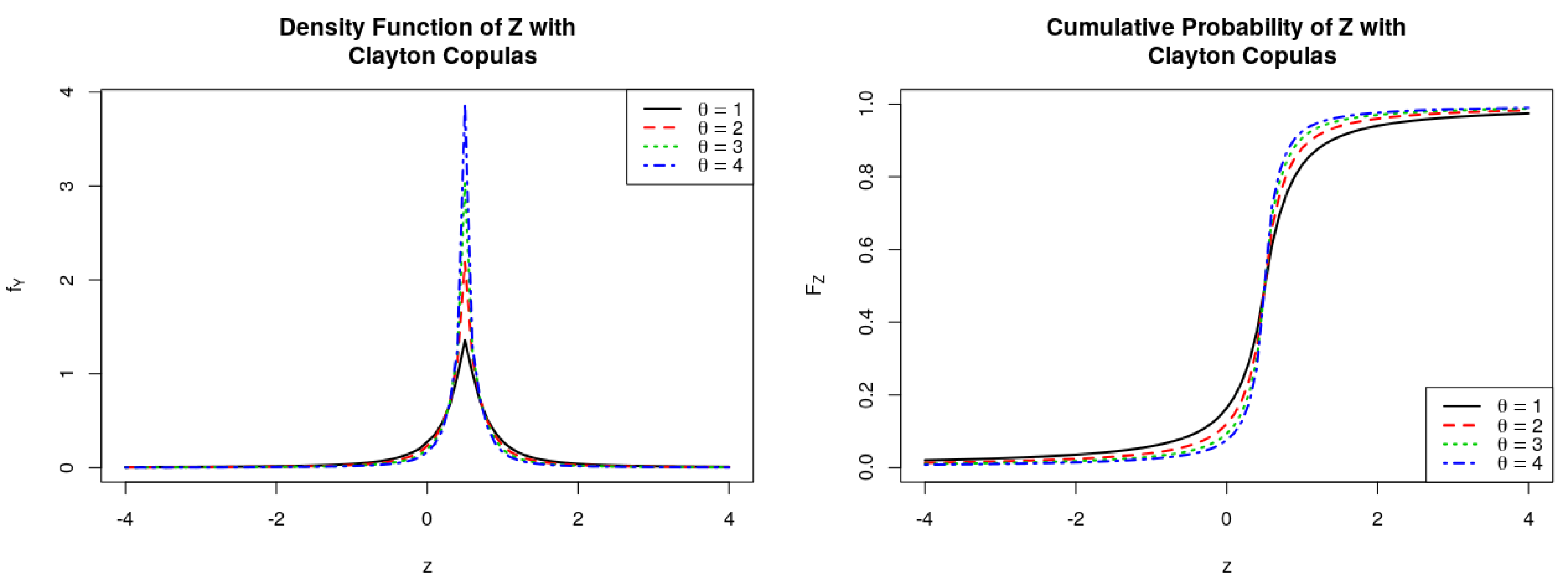

Figure 6.

PDFs and CDFs of the ratio , where follows Clayton Copulas.

Figure 6.

PDFs and CDFs of the ratio , where follows Clayton Copulas.

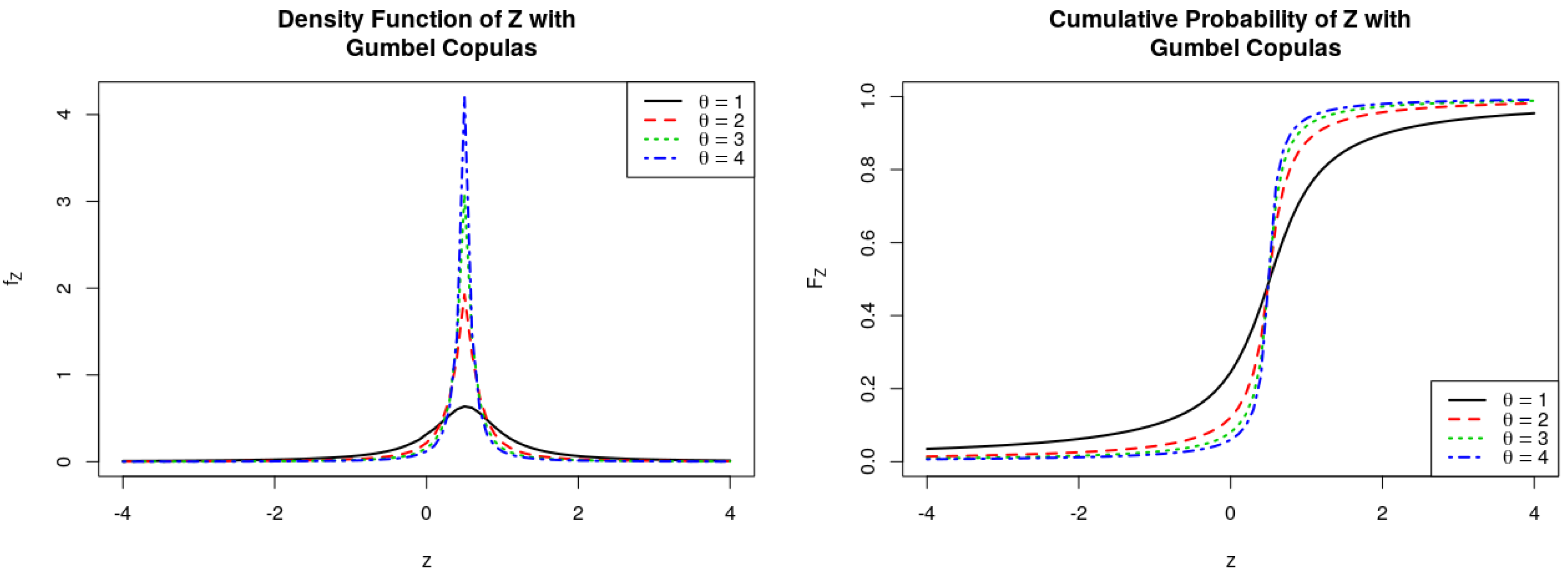

Figure 7.

PDFs and CDFs of the ratio , where follows Gumbel Copulas.

Figure 7.

PDFs and CDFs of the ratio , where follows Gumbel Copulas.

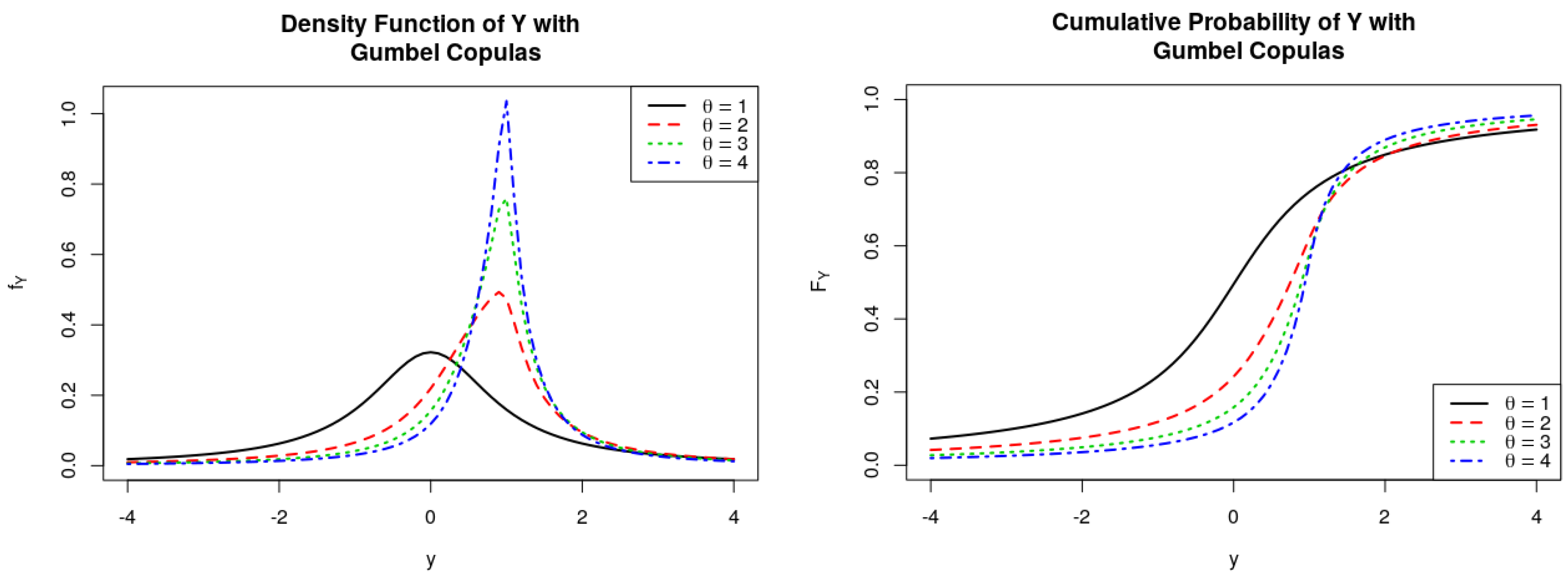

Figure 8.

PDFs and CDFs of the ratio , where follows Gumbel Copulas.

Figure 8.

PDFs and CDFs of the ratio , where follows Gumbel Copulas.

Figure 9.

PDF and CDF of quotient of the ratio , where follows Frank Copulas.

Figure 9.

PDF and CDF of quotient of the ratio , where follows Frank Copulas.

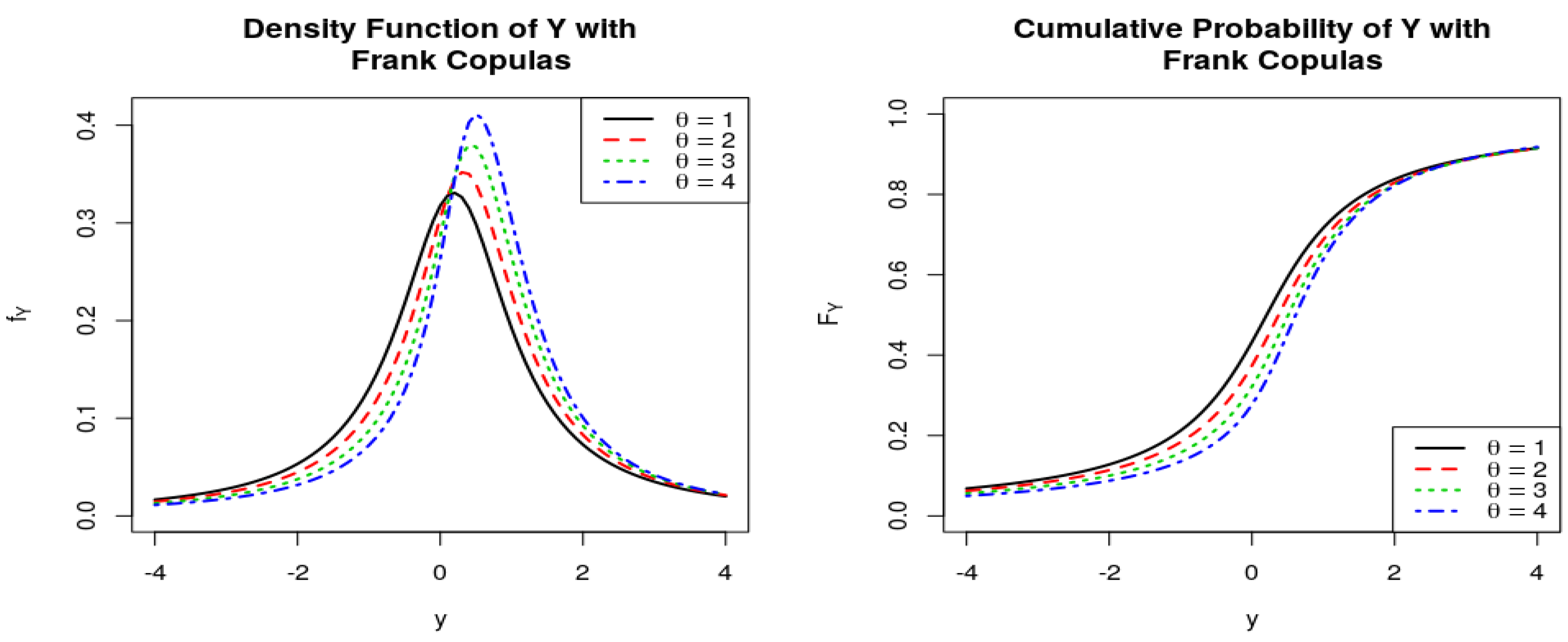

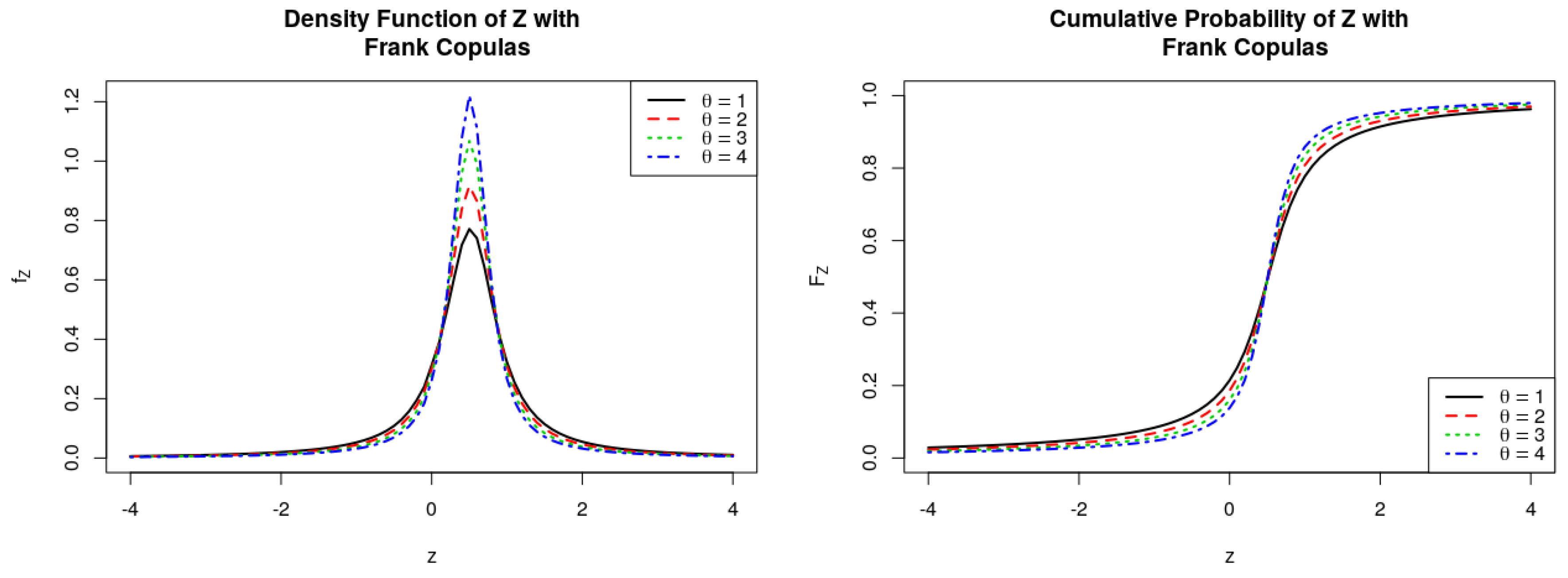

Figure 10.

PDF and CDF of the ratio , where follows Frank Copulas.

Figure 10.

PDF and CDF of the ratio , where follows Frank Copulas.

Figure 11.

PDFs and CDFs of the ratio , where follows Joe Copulas.

Figure 11.

PDFs and CDFs of the ratio , where follows Joe Copulas.

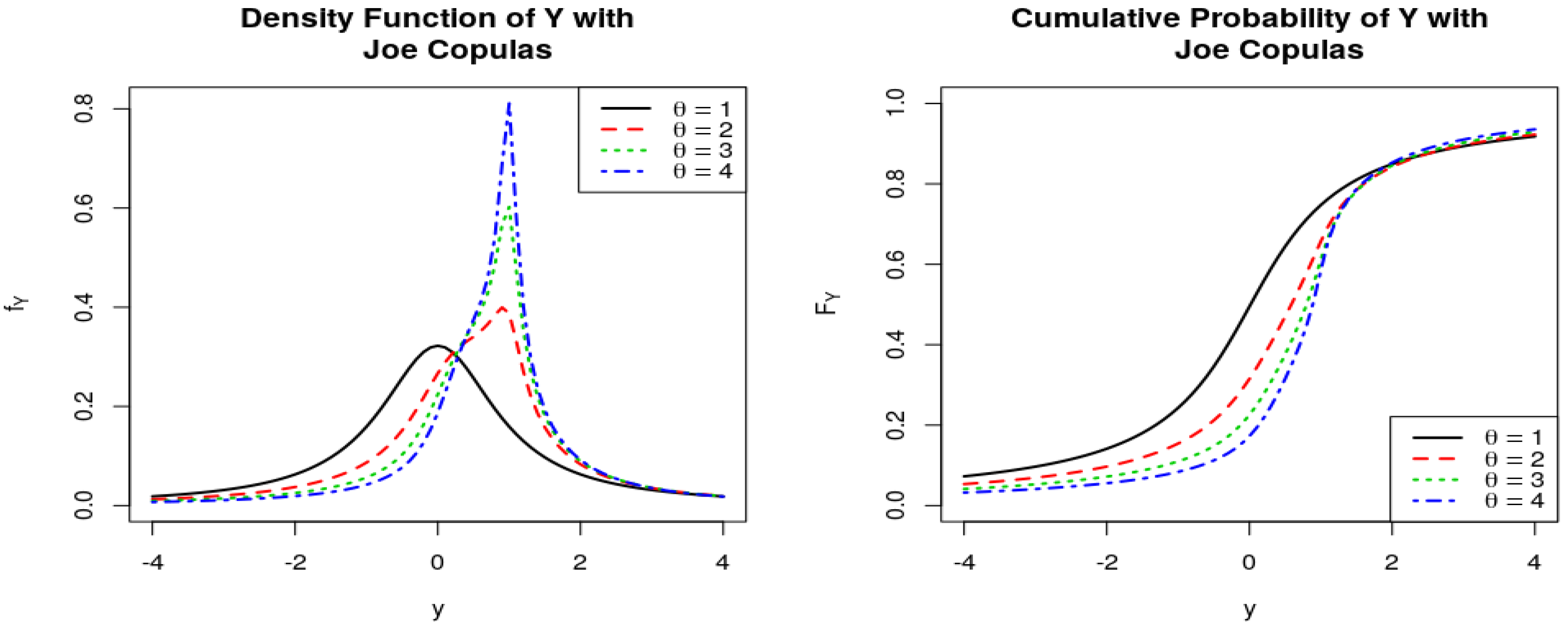

Figure 12.

PDFs and CDFs of the ratio , where follows Joe Copulas.

Figure 12.

PDFs and CDFs of the ratio , where follows Joe Copulas.

Figure 13.

PDFs and CDFs of the ratio , where modeled with six Copulas having the same .

Figure 13.

PDFs and CDFs of the ratio , where modeled with six Copulas having the same .

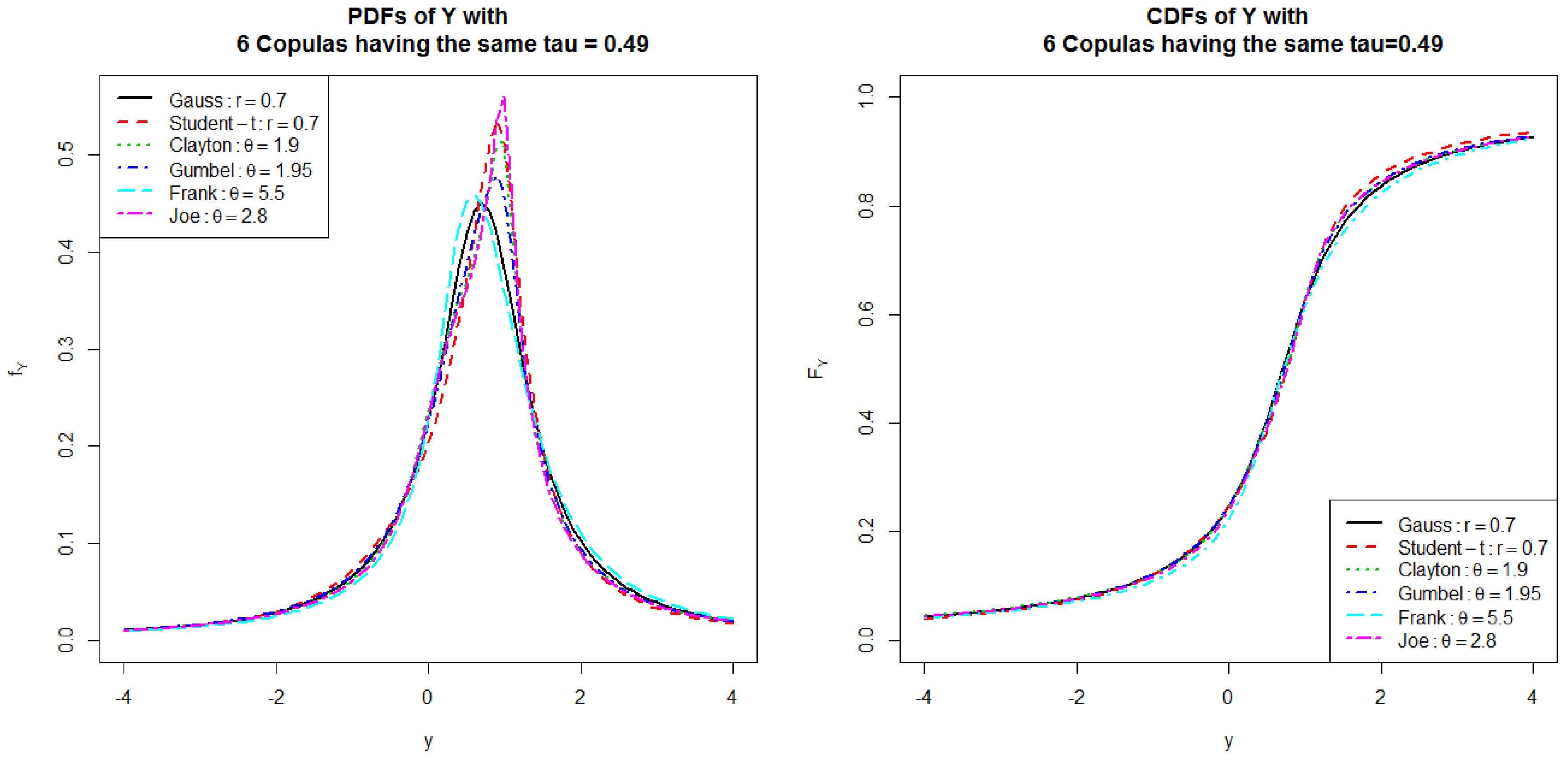

Figure 14.

PDF and CDF of the ratio , where modeled with six Copulas having the same .

Figure 14.

PDF and CDF of the ratio , where modeled with six Copulas having the same .

Table 1.

Some percentiles of , where follows Gaussian Copulas.

Table 1.

Some percentiles of , where follows Gaussian Copulas.

| r | | | | Median | | |

|---|

| | −3.65 | −1.34 | −0.9 | −0.46 | 1.85 |

| | −5.97 | −1.37 | −0.5 | 0.37 | 4.97 |

| 0 | 0 | −6.31 | −1.00 | 0.0 | 1.00 | 6.31 |

| 0.5 | 0.33 | −4.97 | −0.37 | 0.5 | 1.37 | 5.97 |

| 0.9 | 0.71 | −1.85 | 0.46 | 0.9 | 1.34 | 3.65 |

Table 2.

Some percentiles of , where follows Gaussian Copulas.

Table 2.

Some percentiles of , where follows Gaussian Copulas.

| r | | | | Median | | |

|---|

| | −13.27 | −1.68 | 0.5 | 2.68 | 14.26 |

| | −4.97 | −0.37 | 0.5 | 1.37 | 5.97 |

| 0 | 0 | −2.66 | 0.00 | 0.5 | 1.00 | 3.65 |

| 0.5 | 0.33 | −1.33 | 0.21 | 0.5 | 0.79 | 2.32 |

| 0.9 | 0.71 | −0.23 | 0.39 | 0.5 | 0.61 | 1.22 |

Table 3.

Some percentiles of , where follows Student-t Copulas, .

Table 3.

Some percentiles of , where follows Student-t Copulas, .

| r | | | | Median | | |

|---|

| | −3.42 | −1.26 | −0.92 | −0.50 | 1.82 |

| | −5.18 | −1.28 | −0.56 | 0.40 | 4.42 |

| 0 | 0 | −5.40 | −1.00 | 0.00 | 1.00 | 5.41 |

| 0.5 | 0.33 | −4.42 | −0.40 | 0.56 | 1.28 | 5.18 |

| 0.9 | 0.71 | −1.81 | 0.50 | 0.92 | 1.26 | 3.42 |

Table 4.

Some percentiles of , where follows Student-t Copulas, .

Table 4.

Some percentiles of , where follows Student-t Copulas, .

| r | | | | Median | | |

|---|

| | −18.20 | −2.05 | 0.5 | 3.05 | 19.21 |

| | −6.62 | −0.45 | 0.5 | 1.45 | 7.61 |

| 0 | 0 | −3.35 | 0.00 | 0.5 | 1.00 | 4.35 |

| 0.5 | 0.33 | −1.54 | 0.24 | 0.5 | 0.76 | 2.54 |

| 0.9 | 0.71 | −0.24 | 0.40 | 0.5 | 0.60 | 1.24 |

Table 5.

Some percentiles of , where follows Clayton Copulas.

Table 5.

Some percentiles of , where follows Clayton Copulas.

| | | | Median | | |

|---|

| 1 | 0.33 | −4.97 | −0.36 | 0.53 | 1.31 | 5.83 |

| 2 | 0.5 | −3.83 | 0.03 | 0.76 | 1.34 | 5.24 |

| 3 | 0.60 | −2.87 | 0.25 | 0.86 | 1.34 | 4.71 |

| 4 | 0.67 | −2.12 | 0.39 | 0.91 | 1.32 | 4.25 |

Table 6.

Some percentiles of , where follows Clayton Copulas.

Table 6.

Some percentiles of , where follows Clayton Copulas.

| | | | Median | | |

|---|

| 1 | 0.33 | −1.31 | 0.22 | 0.5 | 0.78 | 2.31 |

| 2 | 0.5 | −0.73 | 0.30 | 0.5 | 0.70 | 1.73 |

| 3 | 0.60 | −0.42 | 0.35 | 0.5 | 0.65 | 1.42 |

| 4 | 0.67 | −0.24 | 0.37 | 0.5 | 0.63 | 1.24 |

Table 7.

Some percentiles of , where follows Gumbel Copulas.

Table 7.

Some percentiles of , where follows Gumbel Copulas.

| | | | Median | | |

|---|

| 1 | 0 | −6.31 | −1.00 | 0.00 | 1.00 | 6.32 |

| 2 | 0.5 | −3.70 | 0.00 | 0.74 | 1.36 | 5.01 |

| 3 | 0.67 | −2.26 | 0.38 | 0.89 | 1.32 | 3.95 |

| 4 | 0.75 | −1.45 | 0.56 | 0.94 | 1.27 | 3.30 |

Table 8.

Some percentiles of , where follows Gumbel Copulas.

Table 8.

Some percentiles of , where follows Gumbel Copulas.

| | | | Median | | |

|---|

| 1 | 0 | −2.66 | 0.00 | 0.5 | 1.00 | 3.66 |

| 2 | 0.5 | −0.82 | 0.30 | 0.5 | 0.70 | 1.82 |

| 3 | 0.67 | −0.34 | 0.37 | 0.5 | 0.63 | 1.34 |

| 4 | 0.75 | −0.12 | 0.41 | 0.5 | 0.59 | 1.12 |

Table 9.

Some percentiles of , where follows Frank Copulas.

Table 9.

Some percentiles of , where follows Frank Copulas.

| | | | Median | | |

|---|

| 1 | 0.11 | −6.03 | −0.79 | 0.19 | 1.18 | 6.42 |

| 2 | 0.21 | −5.59 | −0.56 | 0.36 | 1.31 | 6.37 |

| 3 | 0.31 | −5.05 | −0.33 | 0.50 | 1.40 | 6.19 |

| 4 | 0.39 | −4.46 | −0.14 | 0.60 | 1.46 | 5.90 |

Table 10.

Some percentiles of , where follows Frank Copulas.

Table 10.

Some percentiles of , where follows Frank Copulas.

| | | | Median | | |

|---|

| 1 | 0.11 | −2.09 | 0.09 | 0.5 | 0.91 | 3.09 |

| 2 | 0.21 | −1.62 | 0.16 | 0.5 | 0.84 | 2.62 |

| 3 | 0.31 | −1.25 | 0.21 | 0.5 | 0.79 | 2.25 |

| 4 | 0.39 | −0.96 | 0.25 | 0.5 | 0.75 | 1.96 |

Table 11.

Some percentiles of , where follows Joe Copulas.

Table 11.

Some percentiles of , where follows Joe Copulas.

| | | | Median | | |

|---|

| 1 | 0 | −6.31 | −1.00 | 0.00 | 1.00 | 6.32 |

| 2 | 0.36 | −4.82 | −0.32 | 0.57 | 1.30 | 5.67 |

| 3 | 0.52 | −3.66 | 0.07 | 0.79 | 1.33 | 5.13 |

| 4 | 0.61 | −2.71 | 0.29 | 0.88 | 1.33 | 4.62 |

Table 12.

Some percentiles of , where follows Joe Copulas.

Table 12.

Some percentiles of , where follows Joe Copulas.

| | | | Median | | |

|---|

| 1 | 0 | −2.66 | 0.00 | 0.5 | 1.00 | 3.66 |

| 2 | 0.36 | −1.25 | 0.23 | 0.5 | 0.77 | 2.25 |

| 3 | 0.52 | −0.66 | 0.31 | 0.5 | 0.69 | 1.66 |

| 4 | 0.61 | −0.37 | 0.35 | 0.5 | 0.65 | 1.37 |

Table 13.

Some percentiles of , where modelled with six copulas having the same Kendall coefficient .

Table 13.

Some percentiles of , where modelled with six copulas having the same Kendall coefficient .

| Copulas | Parameters | | | | Median | | |

|---|

| Gaussian | 0.7 | 0.49 | −3.81 | −0.01 | 0.70 | 1.41 | 5.21 |

| Student-t | 0.7, | 0.49 | −3.52 | −0.02 | 0.76 | 1.31 | 4.63 |

| Clayton | 1.90 | 0.49 | −3.93 | 0.00 | 0.74 | 1.34 | 5.30 |

| Gumbel | 1.95 | 0.49 | −3.80 | −0.03 | 0.72 | 1.36 | 5.07 |

| Frank | 5.5 | 0.49 | −3.60 | 0.08 | 0.72 | 1.49 | 5.41 |

| Joe | 2.8 | 0.49 | −3.88 | 0.01 | 0.76 | 1.33 | 5.24 |

Table 14.

Some percentiles of , where modelled with six copulas having the same Kendall coefficient .

Table 14.

Some percentiles of , where modelled with six copulas having the same Kendall coefficient .

| Copulas | Parameters | | | | Median | | |

|---|

| Gaussian | 0.7 | 0.49 | | 0.29 | 0.5 | 0.71 | 1.83 |

| Student-t | 0.7, | 0.49 | | 0.31 | 0.5 | 0.69 | 1.92 |

| Clayton | 1.90 | 0.49 | | 0.30 | 0.5 | 0.70 | 1.77 |

| Gumbel | 1.95 | 0.49 | | 0.30 | 0.5 | 0.70 | 1.86 |

| Frank | 5.5 | 0.49 | | 0.29 | 0.5 | 0.71 | 1.65 |

| Joe | 2.8 | 0.49 | | 0.30 | 0.5 | 0.70 | 1.74 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}