2.1. Theoretical Background

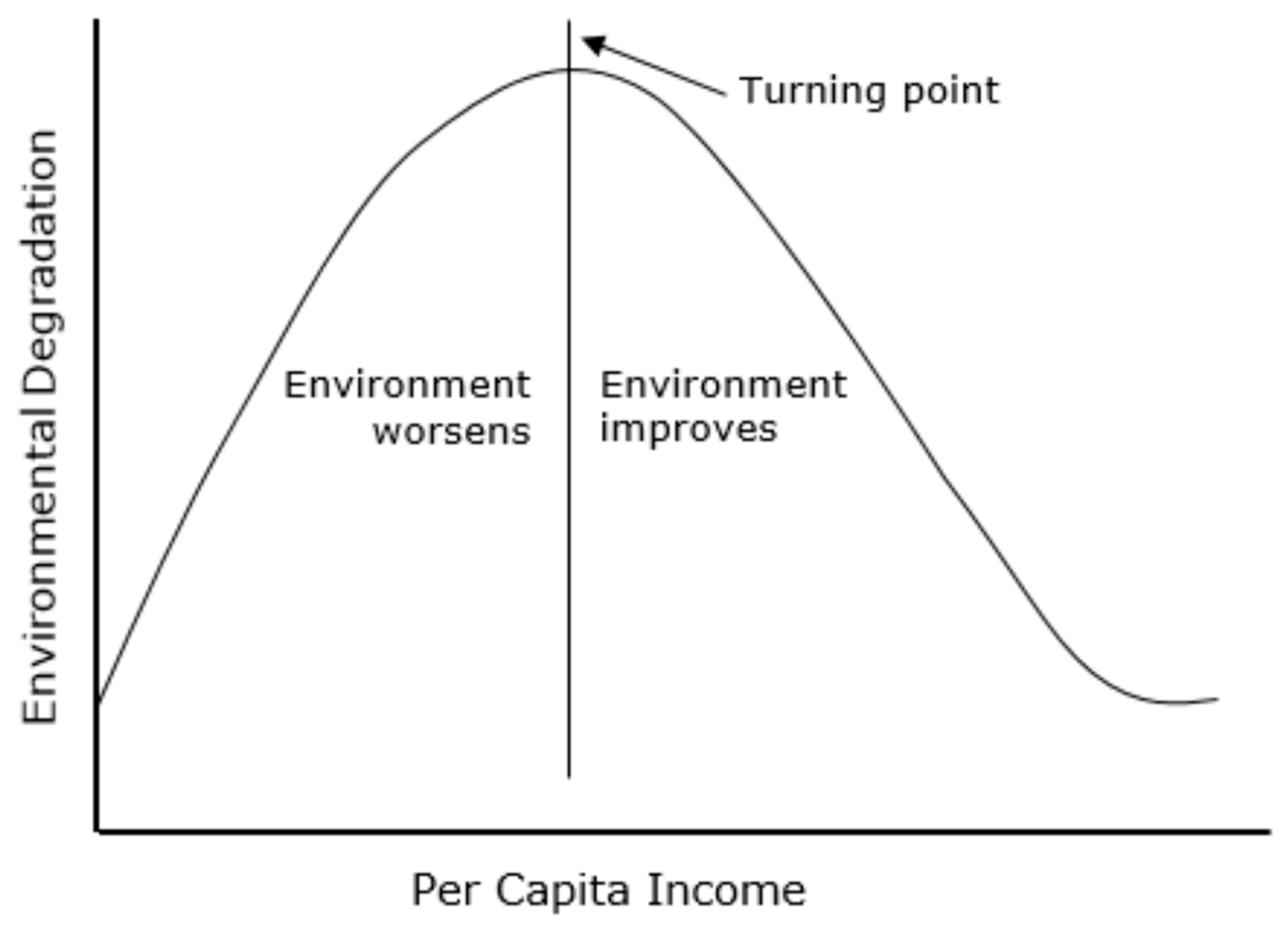

The Kuznets curve hypothesis, which was first discussed by the economist Simon Kuznets in the 1950s, shows that as an economy grows, initial inequality increases and then decreases [

2]. The Kuznets curve indicates that the economic center of the nation will shift to urban regions when the nation experiences industrialization, especially agricultural mechanization [

2]. Therefore, farmers tend to flock into large cities in order to find better-paying jobs. This means that there is a considerable inequality gap between rural and urban areas. Because rural populations plunge while urban populations soar, firm owners earn more profit while laborers in these industries receive an income rise at a slower rate and farmer incomes reduce. However, the inequality then hopefully drops when economic growth reaches the highest point of average income and the well-being of the state, reaching from industrialization to democratization, allows beneficial growth, leading to an increase in GDP per capita. Kuznets shows that inequality would have a trend like an inverted U-shape as it first increases and then decreases along with the increase of GDP per capita. While Kuznets curve diagrams illustrate an inverted U-shape curve, several variables along the axes are usually mixed and matched, such as the Gini coefficient or inequality on the

Y-axis and economic growth, time, or GPD per capita on the

X-axis.

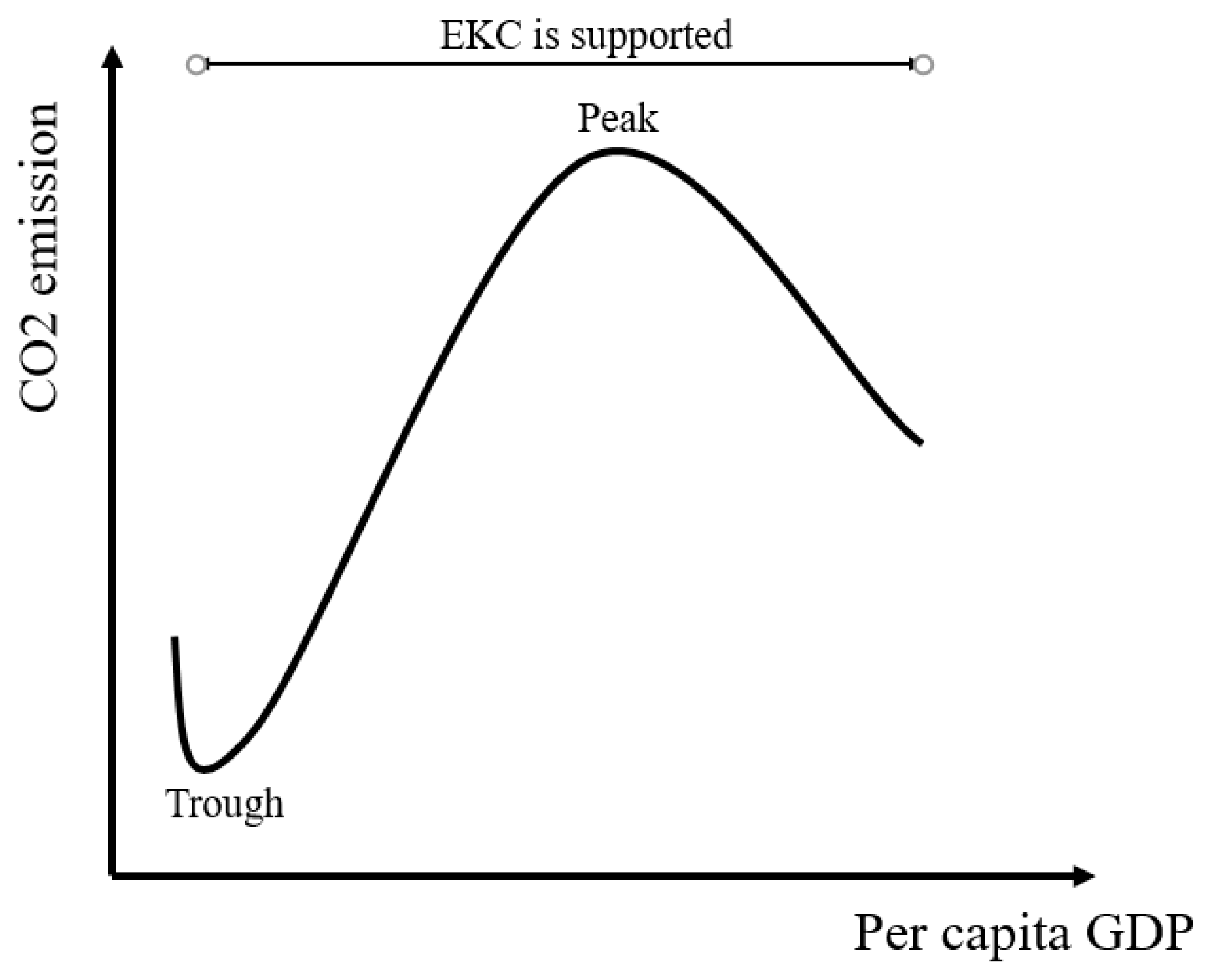

After a few decades, Kruger and Grossman [

3] applied this hypothesis in the environmental sector. It shows that economic development and environmental degradation is in an inverted U-shaped correlation which is known as the Environmental Kuznets Curve (EKC) theory. The EKC theory states that economic development and environmental degradation have a positive relationship. When the country is at an early stage of economic growth, improvement in living standards may be at the expense of the environment. However, when a high level of economic growth and development has been achieved, concerns about the environment emerge (

Figure 1). As a result, the inverted U-shape of the EKC curve is supported by evidence from various empirical studies, including Shafik [

4] and Omotor and Orubu [

5]; it was considered a standard feature in the creation of environmental policy. Onafowora and Owoye’s research [

6] showed that the long-run relationship between economic development and CO

2 release follows an N-shape. Al-Mulali and Oxturk [

7] indicated a U-shaped relationship between GDP and CO

2 emission.

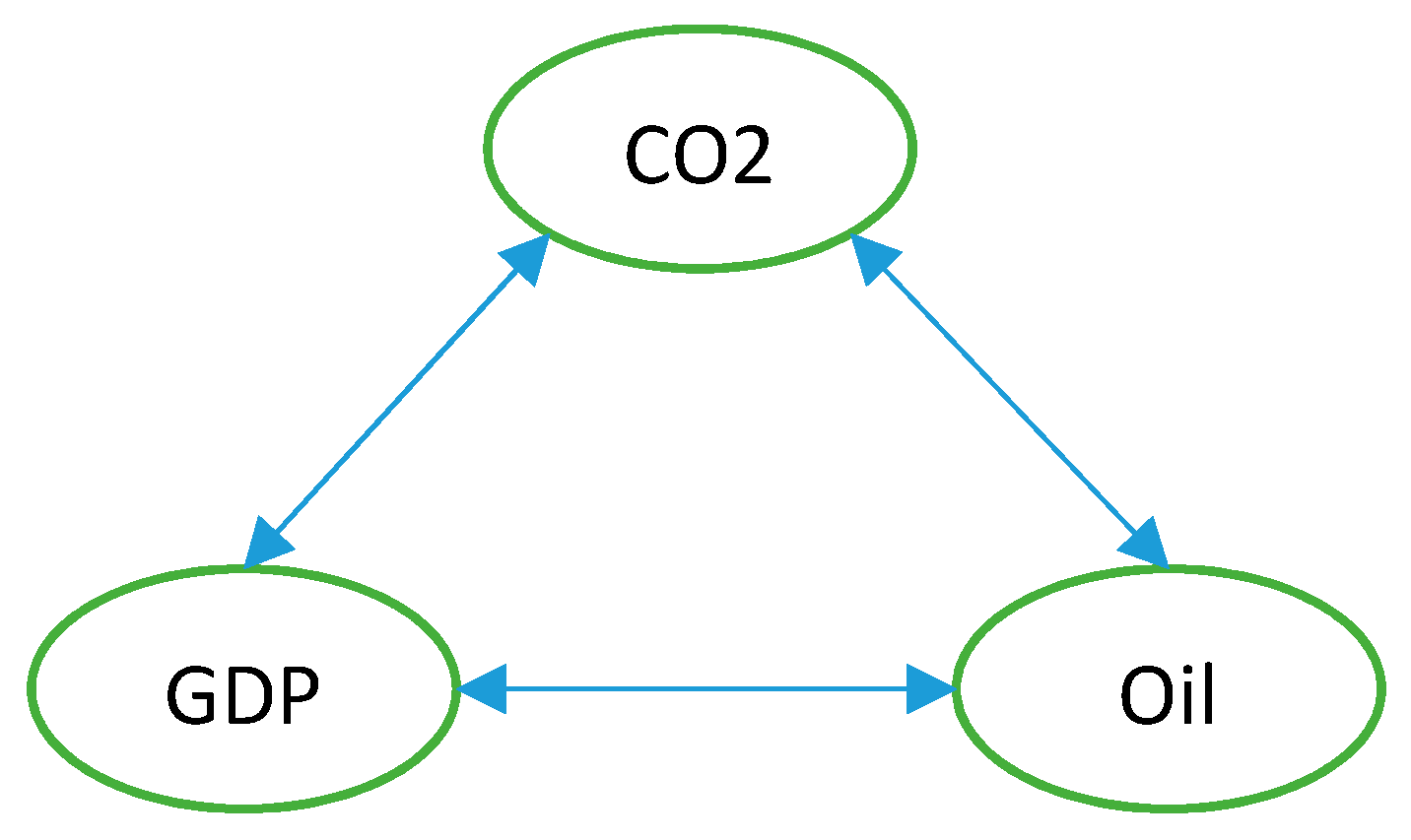

The second theory on the issue is generally known as the pollution heaven hypothesis, which states that polluting industries will be relocated to jurisdictions where environmental regulations are less stringent. There are two main arguments concerning the benefits that FDI brings to the economic development of host countries. First, FDI diminishes environmental degradation through technological innovation. Second, some have argued that FDIs take the environment issue more seriously, which increases CO2 emissions where pollution-intensive industries could be transferred from the rich to the poorer countries due to weak environmental law and regulations in the host countries. Similarly, in relation to economic growth and emission, this relationship is complicated and inconsistent. Findings from previous studies showed that FDI can have a positive or negative impact on the environment.

2.2. Empirical Literature

In general, there are three main schools of thought in relation to the causal relationship between FDI, economic growth, CO2 emissions, and energy consumption. The first stream is related to the empirical studies that mainly tested the validity of the Environmental Kuznets Curve (EKC) hypothesis. The second stream is the examination concentrating on the relationship between energy consumption and CO2 emissions. The final stream is the investigation of the hypothesis that there is a causal relationship between trade liberalization, which is represented by FDI flows, and CO2 emissions.

Utilizing panel cointegration with a pooled sample to test the EKC hypothesis, Lean and Smyth [

8] concluded that, generally, for the whole sample of 5 Association of Southeast Asian Nations (ASEAN) countries, the EKC hypothesis is supported. However, at an individual country level, the relationship between economic growth and CO

2 emissions varies. While the EKC hypothesis is supported in the Philippines, there is no support of EKC for Malaysia and Thailand. For Indonesia, income has a positive one-directional relationship with CO

2 emissions. When panel Granger causality test is utilised, there is no causal relationship from income to CO

2 emissions in both the short and the long run. However, there is a causal relationship between CO

2 emissions and income in the long run.

However, EKC theory is not supported by other studies. Narayan and Narayan [

9] investigated the EKC hypothesis by comparing the long and short run income elasticity of 43 developing countries and found that the EKC was not supported. Their findings for ASEAN-5 is that there is no evidence supporting the EKC for Indonesia, Malaysia, Philippines, and Thailand, while income in the Philippines has a positive impact on its CO

2 emissions. This study shows that there is a long-run relationship between income and CO

2 emissions.

Besides the test of the validity of traditional EKC theory (inverted U-shape), the new stream expanded into testing the existence of an N-shape relationship of income and CO

2 emissions. This stream raised many empirical research questions for researchers such as Churchill et al. [

10], Sarkodie and Strezov [

11], and Zhou et al. [

12]. Churchill et al. [

10] tested N-shape for OECD countries in the period 1870–2014 by using mean group estimators (MG, PMG, AMG, and CCEMG), and found there are two turning points of GDP per capita or the relationship exhibits N-shape for some countries, such as Australia, Canada, and Japan, but some countries do not follow this shape, such as Spain and the UK. Moreover, Sarkodie and Strezov [

11] also tested this N-shape for the top five greenhouse gas emitting developing countries—China, Iran, Indonesia, India, and South Africa—by using panel quantile regression with data from 1982 to 2016. The findings stated there is an N-shape of per capita income and CO

2 emissions for selected countries and this still supports EKC theory [

11].

Niu et al. [

13] utilized panel data to analyze the causal relationships between GDP, energy consumption, and CO

2 emissions for the Asia–Pacific countries, including developing countries such as China, India, Thailand, and Indonesia, and the results are mixed. While there is a long-run nexus between energy consumption, coal, oil, and CO

2 emissions, there is no long-run nexus between natural gas and electricity on CO

2 emissions. Like previous studies, they concluded that the energy consumption is the main cause of CO

2 emissions. Moreover, the individual countries were examined by applying the individually-fixed varying coefficient model between CO

2 emissions and the amount of energy used per capita [

13]. In addition, Granger causality test showed that there is a causality between CO

2 emissions and GDP, and energy consumption and CO

2 emissions in the long run. Nevertheless, for the short-run analysis, it is significant for unidirectional causality between energy consumption and CO

2 emissions.

Hossain M.S. [

14] used panel data of 9 newly-industrialized nations, including Malaysia, the Philippines, and Thailand, to investigate the nexus between CO

2 emissions, energy consumption, and economic growth as well as trade openness and urbanization. The paper found that income and energy consumption significantly impact on CO

2 emissions in the long run for the Philippines and Thailand, whereas it is not significant for the case of Malaysia. Furthermore, the panel Granger causality test shows that there is no causal relationship between income, energy consumption, and CO

2 emissions in the long run [

14]. Nonetheless, in the short run, there was significant causality running from income to CO

2 emissions.

More specifically, Ang [

15] examined the relationship between GDP, CO

2 emissions and energy consumption in the long run for the Malaysia case. The study showed that CO

2 emissions and energy consumption have positive impacts on GDP in the long run. Like [

14], the Granger causality test found evidence of unidirectional causality running from GDP to energy consumption in the long run. Similarly, the causality nexus between CO

2 emissions and growth is weak and, therefore, it is inclusive.

There are a lot of empirical studies about the pollution heaven hypothesis (PHH) [

16,

17,

18,

19,

20,

21,

22,

23,

24,

25,

26,

27]; however, there are also conflicting findings between them. For instance, Sun et al. [

16] used Auto Regressive Distributed Lag model (ARDL) to test this hypothesis for China; they confirmed the validity of PHH, but Zhang and Zhou [

17], who also used it with Chinese data, found contrasting findings—a negative nexus between FDI and CO

2 emissions. In addition, Zhu et al. [

18] researched for 5 countries in Asia from 1981 to 2011 using panel quartile regression; they rejected the validity of PHH in these countries, while Behera and Dash [

19] used data from 17 countries in Asia (including 5 countries from Zhu et al. [

18]) from 1980 to 2012 and found contradictory results—a positive nexus between FDI and CO

2 emissions; this supported the PHH. Furthermore, Tang and Tan [

20], who used time series data in Vietnam from 1976 to 2009, found a negative nexus, while Phuong and Tuyen [

21], also using data from Vietnam from 1986 to 2015, found no evidence on FDI and CO

2 emissions. Moreover, a lot of previous empirical studies had similar conflicts in their findings. For the support side of PHH, Solarin et al. [

22], who used the ARDL model with Ghanaian time series data, Zakarya et al. [

23], who used panel data from 6 BRICS countries (Brazil, Russia, India, China, and South Africa) from 1990–2015, and Zhou et al. [

12], who used data from 285 cities in China with GMM method for Random and Fixed Effect model, found a long-run positive relationship between FDI and CO

2 emissions. For the rejected side, Kirkulak et al. [

24], Acharya [

25], and Jorgenson [

26] found the negative nexus. In an opposite analysis, Atici [

27] used panel data from 1970 to 2006 of ASEAN countries and Japan and found no evidence for this relationship.

In conclusion, previous studies show the complexity of the causal relationship between CO

2 emissions, energy consumption, and economic growth [

8,

9,

10,

11,

12,

13,

14,

15,

16,

17,

18,

19,

20,

21,

22,

23,

24,

25,

26,

27]. The findings on these relationships are not robust. The evidence is inclusive and mixed among the studies. Moreover, the evidence on testing the validity of the EKC is also mixed in previous empirical studies. In addition, previous studies had not put great emphasis on analyzing the complexity of the relationship between FDI and CO

2 emission. All these weaknesses are considered in this study.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}