Multi-Criteria Analysis of Startup Investment Alternatives Using the Hierarchy Method

Department of Mathematics and Computer Sciences, Faculty of Science and Technology, Jan Dlugosz University in Czestochowa, al. Armii Krajowej 13/15, 42-200 Czestochowa, Poland

*

Author to whom correspondence should be addressed.

Entropy 2023, 25(5), 723; https://doi.org/10.3390/e25050723

Submission received: 24 February 2023

/

Revised: 7 April 2023

/

Accepted: 24 April 2023

/

Published: 27 April 2023

(This article belongs to the Special Issue Recent Trends and Developments in Econophysics)

Abstract

:In this paper, we discuss the use of multi-criteria analysis for investment alternatives as a rational, transparent, and systematic approach that reveals the decision-making process during a study of influences and relationships in complex organizational systems. It is shown that this approach considers not only quantitative but also qualitative influences, statistical and individual properties of the object, and expert objective evaluation. We define the criteria for evaluating startup investment prerogatives, which are organized in thematic clusters (types of potential). To compare the investment alternatives, Saaty’s hierarchy method is used. As an example, the analysis of three startups is carried out based on the phase mechanism and Saaty’s analytic hierarchy process to identify investment appeal of startups according to their specific features. As a result, it is possible to diversify the risks of an investor through the allocation of resources between several projects, in accordance with the received vector of global priorities.

1. Introduction

The positive tendencies towards economic development require updated business entities according to the current market conditions and the emergence of new structural units, all of which form a competitive economic system. The active development of any economy is not possible without the constant emergence of new economic enterprises. This process stimulates the formation of the market environment with healthy competition and ensures scientific and reproducible functioning. Currently, we observe the positive tendency towards building potential for realizing business ideas through the creation of startups, whose business concepts have been dictated by the needs of the modern society and industries. A startup is a strategic economic unit with innovative concepts with the potential to enter the market. First, we outline the essential features of startups:

- (1)

- the innovation of an idea;

- (2)

- the necessity of capital investment;

- (3)

- reproducibility (possibility to sell the inventive solution multiple times);

- (4)

- business expansion;

- (5)

- the existence of a detailed and structured business plan;

- (6)

- generally, a startup is a project in initial stages of implementation;

- (7)

- the possibility of significant growth of the project;

- (8)

- often, startups propose new technologies;

- (9)

- uniqueness;

- (10)

- the potential team of professionals;

- (11)

- the riskiness of the investments;

- (12)

- the concentration of management decisions by the startup founders;

- (13)

- the flexibility as well as quick and efficient adaptation to changes in the environment;

- (14)

- the possibility to individualize the products, according to the demands of consumers;

- (15)

- the dependence on credit resources;

- (16)

- the close relations between the founder and the employees, etc.

Currently, one of the biggest problems is finding investors for startups, the qualified and objective evaluation of the concepts in terms of costs and benefits for future investment, and the successful presentation of the project to investors. Often, this work is entrusted to consulting agencies that professionally evaluate innovative ideas. For the investor, it is important to have a final estimation containing not only a list of factors justifying the appropriateness of investments in the suggested startups but also the method used for comparing several investment alternatives. For an objective and comprehensive assessment of a startup, a large number of criteria should be taken into account; however, this complicates the evaluation process and prolongs its execution. To assess investment alternatives, many methods, mechanisms, techniques, and tools enable the investigation of investments from different points of view. Research has been concentrated in several directions: the economic basis of startups, the mechanisms of their initiation, and the behaviors of investors. The most substantiated and successful in practice are mathematical models that predict the best investment alternatives. Based on the startup founder’s viewpoint, a comprehensive analysis of investment alternatives should involve the requirements from the idea to launch, from the gathering and successful use of information to the potential of the startup’s innovation in a functioning market. This step-by-step mechanism for building a business was precisely outlined in [1].

The behaviors of investors (especially, business “angels”) towards newly created enterprises in the early stages of their development, the ways of evaluating those enterprises, and the interactions of investors and entrepreneurs were described in [2,3]. The basics of practical venture capital management and the details of the cooperation of venture capitalists and entrepreneurs were presented in [4]. Practical advice and the confirmation of the importance of a correct, accurate assessment of the business opportunities of startups were given in [5]. An analysis of venture capital from the viewpoint of current and future investing in an uncertain environment and the high level of competition confirms complexity of the investment choice [6].

An important step towards identifying the most attractive startup for investment involves not only formulating the list of criteria but also establishing their importance (weights). Today, many consulting companies use expert assignment methods to identify the weights of the criteria, but sometimes, the methods are too subjective and dependent on the composition of the expert team, the expert engagement, and lobbying interests. In this area, special attention is paid to the decision-making theory and the Saaty hierarchy method. The multi-criteria decision-making analysis, known as the analytic hierarchy process, was elaborated by Saaty [7,8,9,10,11,12,13]. This approach has been applied to many areas, such as economics, management, engineering, mathematics, information systems, cybernetics, mechanics, design, chemistry, health service, etc. The literature on this subject is considerable, including the following books [14,15,16,17,18,19] and review articles [20,21,22,23,24,25,26,27,28,29,30,31,32,33], where additional references can be found.

The choice and the comparison of the criteria are important parts of decision-making. As the criteria and their weights can significantly influence decision-making, several approaches to solve this problem have been elaborated. In the analytic hierarchy process (AHP), several prioritization methods have been used for deriving weights, such as the eigenvalue (EV) method [8,10,34,35], the logarithmic least squares (LLS) method [36,37], the weighted least squares (WLS) method [38,39], the fuzzy preference programming (FPP) method [40,41,42,43], and the cosine maximization method (CMM) developed in [44]. A good description of several of the most-used methods was given by Srdjevic [45]. The main feature of the step-wise weight assessment ratio analysis (SWARA) [46,47] is the possibility to estimate the opinions of experts and interested groups according to the significance ratio of the criteria in the process of their weight determination. In the best–worst method (BMW) [48,49,50], two vectors of pair-wise comparison were used to determine the weights of the criteria. The full consistency method (FUCOM) [51,52,53] is based on the pairwise comparison of the criteria and the satisfaction of the mathematical transitivity conditions. The level based weight assessment (LBWA) model [54,55] is suitable for use in complex multi-criteria models with a large number of criteria, and it allows for the additional corrections of the values of the weight coefficients, depending on the preferences of the decision-makers.

The main purpose of this article is to provide a comparison of several startups from the investor viewpoint. In this paper, we discuss the use of a multi-criteria analysis for investment alternatives as a rational, transparent, and systematic approach that reveals the decision-making process during the study of influences and relationships in complex organizational systems. The proposed methods can be useful for consulting agencies, investors, and also for startups founders, who can then assess their competitive position against offers from other competitors in the selected economic branch or industrial sector. The procedure of the startup assessment, especially during the initial stages of implementation (development, operation, execution phases, etc.) is often subjective and challenging, as it requires the determination and account of many indexes as well as extended expert consultation, the formation of criteria, and so on. We propose new criteria and a new criteria composition for evaluating the investment appeal of startups. As an example, we consider three alternative investments in startups: the production of LED traffic lights, the manufacture of information–reference electronic terminals, and the manufacture of rotor-reactive turbo-rotational heaters of liquids. The analysis of the three startups is carried out based on the phase mechanisms and Saaty’s analytic hierarchy process to identify the investment appeal of the startups accounting for their specific features. The consistency index, the consistency ratio, and the global priority vector are calculated. As a result, it is possible to diversify the risks of an investor through the allocation of resources among several projects, in accordance with the calculated vector of global priorities.

2. Criteria Composition for Evaluating Investment Attractiveness of Startups

Based upon the review of the literature, the study of the practice of founding and launching startups, successful experiences of investing in startup enterprises, and the results of our previous research, we suggest the following criteria composition, which are consolidated into 12 blocks (Table 1). Similar grouping of sub-criteria into blocks was considered, for example, in [41]. We used several of the block-criteria discussed in [56,57,58,59], and then we supplemented and extended these according to our own criteria.

This criteria could be adjusted according to the economic branch or industrial sector, according to the special features of the business plans presented to the investor. The criteria allow us to analyze the characteristics of startups in a variety of ways, and grouping the proposed criteria could enable potential investors to predetermine the priority groups of the criteria and use the proposed “sketch” of the influential factors to focus attention on the current trends. This criteria-composition model aims to draw the attention of the researcher (investor, consultant) not only on the “classical” list of basic investment indicators (such as payback period and the value of investments) but also to the governmental support of the industry, the innovation and autonomy of startups, time, and resources, as well as the social, scientific, technical, informational, and environmental characteristics.

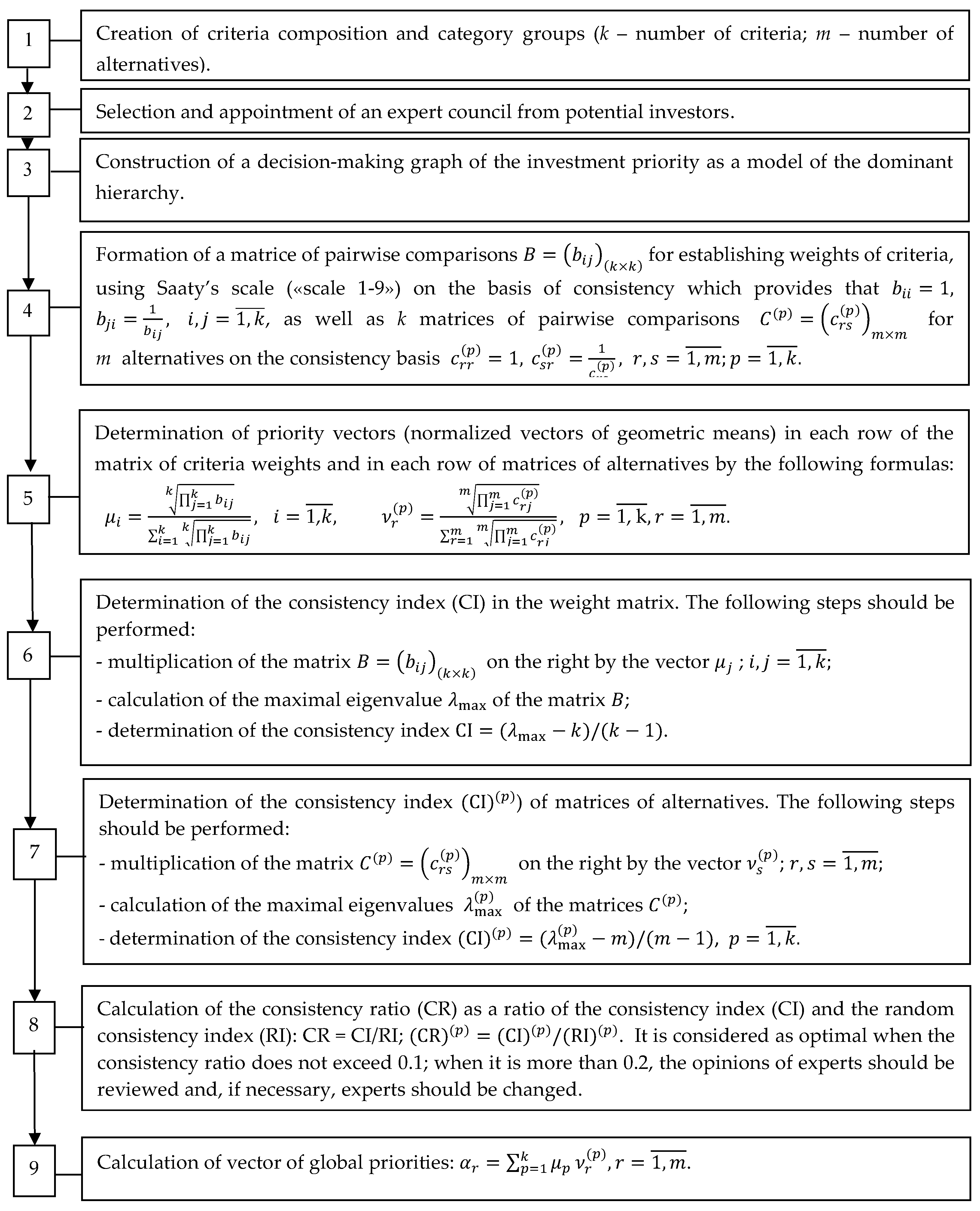

Figure 1 presents the structure of the Saaty method as the operational algorithm, indicating the priority of investments in startups.

3. Implementation of the Saaty Method for Identified Criteria Composition

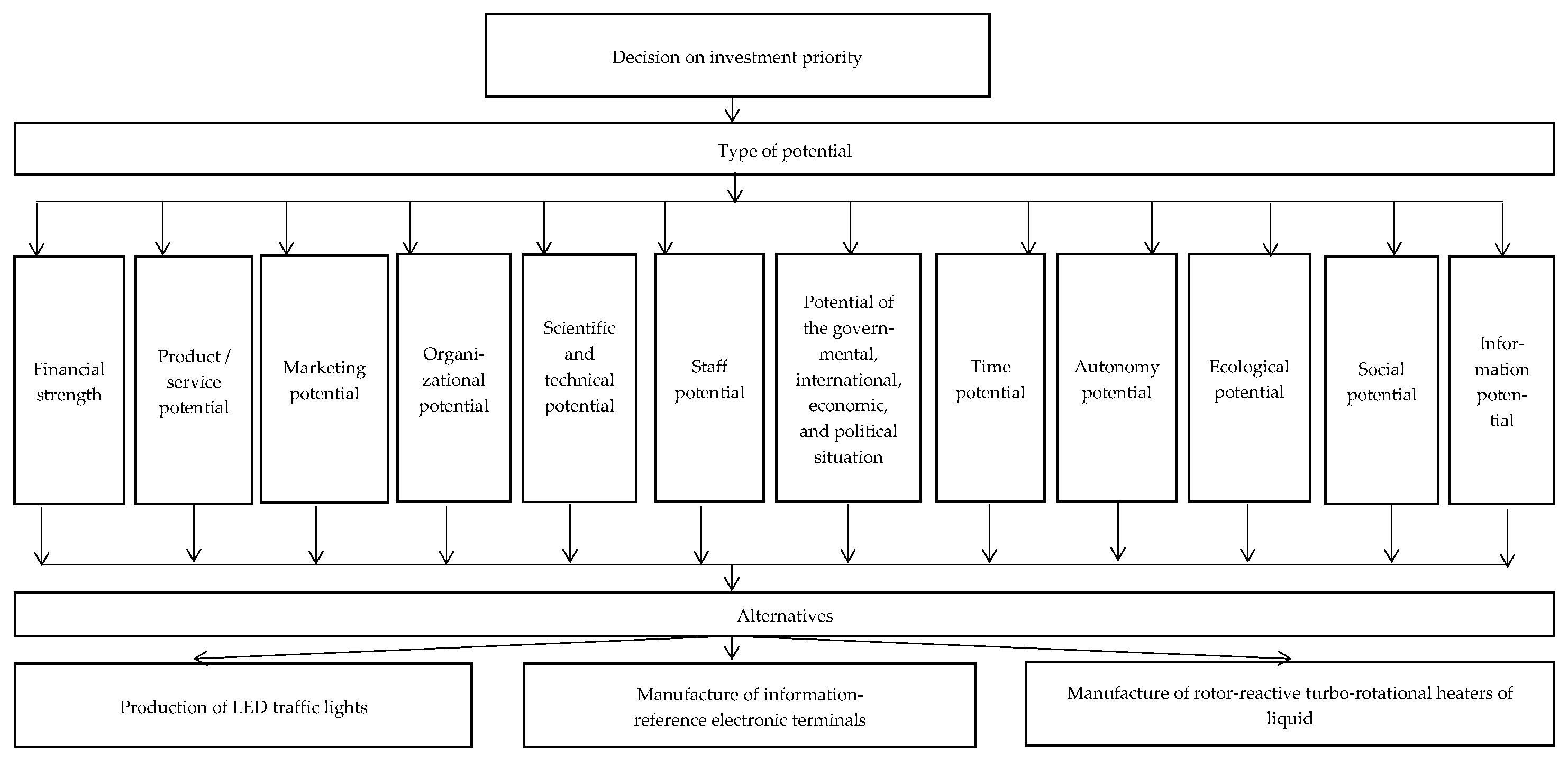

To illustrate practically the Saaty method, we analyze three investment alternatives of startups: the production of LED traffic lights, the manufacture of information–reference electronic terminals, and the manufacture of rotor-reactive turbo-rotational heaters of liquids. The structure of the method is first presented as the dominant hierarchy model in an oriented graph (Figure 2).

After considering the business plans of three investment alternatives and establishing the criteria for assessing the prerogatives of investing in the compared startups, we identified the investment priorities. First, we determined the weights of the criteria according to the sequence of the algorithm; this was the fourth step of the hierarchical procedure, as shown in Figure 1. Table 2 presents the results of the criteria comparison for evaluating the startups using Saaty’s scale (“scale 1–9”) [60,61]. Therefore, we obtained the matrix of pairwise comparisons for establishing the weights of the criteria. The numbers 1–12 in the top row and the first column correspond to the name of the criteria in Table 1. The priority vector () is calculated as the normalized geometric means in accordance with step 5 (see Figure 1). The column RM presents the results of the multiplication of the paired comparison matrix on the right by the vector . The column DV is obtained by dividing the component of the vector in the column RM by the corresponding component of the vector . The approximation of the maximal eigenvalue is calculated as the arithmetic mean of the components of the vector in the column DV and equals . The consistency index . According to [7], for , the random consistency index ; therefore, the consistency ratio is and does not exceed 0.1.

A similar analysis was performed for the 12 matrices with 3 alternatives. The results for the group of criteria “Financial strength” are shown in Table 3. In this case, we obtain . The consistency index . The random consistency index for [7]. The consistency ratio and does not exceed 0.1. Taking into account the 12 criteria groups, the final results are shown in Table 4. The conducted research allows us to assert that the startup for manufacturing information–reference electronic terminals is most attractive for investment, as its global priority of 0.3855 is the highest among the analyzed investment proposals. At the same time, the values of the global priorities for the startups producing LED traffic lights and manufacturing rotor-reactive turbo-rotational heaters of liquids are equal to 0.2547 and 0.3599, respectively.

4. Concluding Remarks

New criteria and new criteria composition for the comparison of investment alternatives were proposed. Considering the sub-criteria could aid establishing weights of groups of criteria. The criteria and alternatives are mutually independent. A multi-criteria approach based on the analytic hierarchy method was used providing a gradual, clear, and logically structured assessment of the parameters of the given alternatives to ensure a successful solution. The proposed approach also has some limitations. For a large number of criteria and alternatives, Saaty’s scale 1–9 could not be enough. The decision-making process could also be time consuming for a large number of criteria and alternatives. For example, in the case of 32 sub-criteria, there appears a large matrix of pairwise comparisons, and for in the literature there is no value of the random index (RI) and only an approximate estimation of the consistency ratio (CR) can be obtained. Therefore, we grouped the 32 new sub-criteria proposed in this study into 12 blocks (potentials). Despite these limitations, the AHP approach is one of the most popular and objective methods for multi-criteria decision-making. The proposed use of the Saaty method for optimal decision-making has a number of advantages, as well. It does not require the unification of the units of measurement for different criteria. It ensures the accuracy of the evaluation by increasing the possibility of intra-matching within the selected criteria. In addition, the presence of a numeric scale allows the relations between the factors to be clearly identified. Finally, this method is adaptable, enabling the criteria composition to be modified by adding or eliminating factors. We compared the maximal eigenvalues obtained as the arithmetic mean of the vector in column DV and the value of obtained using the available mathematical package. With a precision of four digits, the results were the same. It should be emphasized that the consistency ratio (CR) of the pairwise comparison of the 12 groups of criteria, as well as all the 12 consistency ratios , did not exceed 0.1; therefore, the evaluation was consistent.

In the future, we are planning to extend our research to compare our results with results obtained by other techniques, in particular, using the Bellman–Zadeh fuzzy set approach.

Author Contributions

Conceptualization, T.K. and Y.P.; methodology, T.K.; validation, Y.P.; formal analysis, T.K.; investigation, T.K. and Y.P.; writing—original draft preparation, T.K. and Y.P; writing—review and editing, T.K. and Y.P.; supervision, Y.P. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

The authors would like to thank the reviewers for the helpful comments that allowed us to improve the final version of the paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Blank, S.; Dorf, B. The Startup Owner’s Manual: The Step-by-Step Guide for Building a Great Company; K&S Ranch Press: Pescadero, CA, USA, 2012. [Google Scholar]

- Benjamin, G.A.; Margulis, J.B. The Angel Investor’s Handbook: How to Profit from Early-Stage Investing; Bloomberg Press: Princeton, NJ, USA, 2001. [Google Scholar]

- Belton, V.; Stewart, T. Multiple Criteria Decision Analysis: An Integrated Approach; Springer: New York, NY, USA, 2002. [Google Scholar]

- Campbell, K. Smarter Ventures: A Survivor’s Guide to Venture Capital through the New Cycle; Prentice Hall: Harlow, UK, 2003. [Google Scholar]

- Kessler, A. Eat People: Furthermore, Other Unapologetic Rules for Game-Changing Entrepreneurs; Penguin Group: New York, NY, USA, 2011. [Google Scholar]

- Li, Y. Duration analysis of venture capital staging: A real options perspective. J. Bus. Ventur. 2008, 23, 497–512. [Google Scholar] [CrossRef]

- Saaty, T.L. The Analytical Hierarchy Process: Planning, Priority Setting, Resource Allocation; McGraw-Hill: New York, NY, USA, 1980. [Google Scholar]

- Saaty, T.L. Multicriteria Decision Making: The Analytical Hierarchy Process; RWS Publications: Pittsburgh, PA, USA, 1988. [Google Scholar]

- Saaty, T.L. Decision Making with Dependence and Feedback: The Analytical Network Process, 2nd ed.; RWS Publications: Pittsburgh, PA, USA, 2001. [Google Scholar]

- Saaty, T.L. Fundamentals of Decision Making and Priority Theory with the Analytical Hierarchy Process, 2nd ed.; RWS Publications: Pittsburgh, PA, USA, 2006. [Google Scholar]

- Saaty, T.L.; Vargas, L.G. Decision Making with the Analytical Network Process: Economic, Political, Social and Technological Applications with Benefits, Opportunities, Costs and Risks; Springer: New York, NY, USA, 2006. [Google Scholar]

- Saaty, T.L. Decision Making for Leaders: The Analytical Hierarchy Process for Decisions in a Complex World, 3rd ed.; RWS Publications: Pittsburgh, PA, USA, 2012. [Google Scholar]

- Saaty, T.L.; Vargas, L.G. Models, Methods, Concepts & Applications of the Analytical Hierarchy Process, 2nd ed.; Springer: New York, NY, USA, 2012. [Google Scholar]

- Brunelli, M. Introduction to the Analytical Hierarchy Process; Springer: Cham, Switzerland, 2015. [Google Scholar]

- Roy, U.; Majumder, M. Vulnerability of Watersheds to Climate Change Assessed by Neural Network and Analytical Hierarchy Process; Springer: Singapore, 2016. [Google Scholar]

- De Felice, F.; Saaty, T.L.; Petrillo, A. (Eds.) Applications and Theory of Analytical Hierarchy Process—Decision Making for Strategic Decisions; IntechOpen: London, UK, 2016. [Google Scholar]

- Ozsahin, D.U.; Hüseyin Gökçekuş, H.; Uzun, B.; LaMoreaux, J. (Eds.) Application of Multi-Criteria Decision Analysis in Environmental and Civil Engineering; Springer: Cham, Switzerland, 2021. [Google Scholar]

- Thakkar, J.J. Multi-Criteria Decision Making; Springer: Singapore, 2021. [Google Scholar]

- Kulakowski, K. Understanding the Analytical Hierarchy Process; Chapman and Hall/CRC: Boca Raton, FL, USA, 2022. [Google Scholar]

- Pohekar, S.D.; Ramachandran, M. Application of multi-criteria decision making to sustainable energy planning—A review. Renew. Sustain. Energy Rev. 2004, 8, 365–381. [Google Scholar] [CrossRef]

- Vaidya, O.S.; Kumar, S. Analytical hierarchy process: An overview of applications. Eur. J. Oper. Res. 2006, 169, 1–29. [Google Scholar] [CrossRef]

- Ho, W. Integrated analytical hierarchy process and its applications—A literature review. Eur. J. Oper. Res. 2008, 186, 211–228. [Google Scholar] [CrossRef]

- Liberatore, M.J.; Nydick, R.L. The analytical hierarchy process in medical and health care decision making: A literature review. Eur. J. Oper. Res. 2008, 189, 294–307. [Google Scholar] [CrossRef]

- Ishizaka, A.; Labib, A. Review of the main developments in the Analytical Hierarchy Process. Expert Syst. Appl. 2011, 38, 14336–14345. [Google Scholar]

- Subramanian, N.; Ramanathan, R. A review of applications of Analytical Hierarchy Process in operations management. Int. J. Prod. Econ. 2012, 138, 215–241. [Google Scholar] [CrossRef]

- Schmidt, K.; Aumann, I.; Hollander, I.; Damm, K.; von der Schulenburg, J.M.G. Applying the Analytical Hierarchy Process in healthcare research: A systematic literature review and evaluation of reporting. BMC Med. Inform. Decis. Mak. 2015, 15, 112. [Google Scholar] [CrossRef]

- Russo, R.F.S.M.; Camanho, R. Criteria in AHP: A systematic review of literature. Procedia Comput. Sci. 2015, 55, 1123–1132. [Google Scholar] [CrossRef]

- Nisel, S.; Özdemir, M. AHP/ANP in sports: A comprehensive literature review. Int. J. Anal. Hierarchy Process 2016, 8, 405–429. [Google Scholar]

- Emrouznejad, A.; Marra, M. The state of the art development of AHP (1979–2017): A literature review with a social network analysis. Int. J. Prod. Res. 2017, 55, 6653–6675. [Google Scholar] [CrossRef]

- Rajput, V.; Kumar, D.; Sharma, A.; Singh, S.; Rambhagat. A literature review on AHP (Analytical Hierarchy Process). J. Adv. Res. Appl. Sci. 2018, 5, 349–355. [Google Scholar]

- Darko, A.; Chan, A.P.C.; Ameyaw, E.E.; Owusu, E.K.; Pärn, E.; Edwards, D.J. Review of application of analytical hierarchy process (AHP) in construction. Int. J. Constr. Manag. 2019, 19, 436–452. [Google Scholar]

- Goyal, P.; Kumar, D.; Kumar, V. Application of multi-criteria decision analysis in the area of sustainability: A literature review. Int. J. Anal. Hierarchy Process 2020, 12, 512–545. [Google Scholar]

- Madzík, P.; Falát, L. State-of-the-art on analytical hierarchy process in the last 40 years: Literature review based on Latent Dirichlet Allocation topic modelling. PLoS ONE 2022, 17, e0268777. [Google Scholar] [CrossRef]

- Saaty, T.L.; Hu, G. Ranking by eigenvector versus other methods in the Analytical Hierarchy Process. Appl. Math. Lett. 1998, 11, 121–125. [Google Scholar] [CrossRef]

- Saaty, T.L. Decision-making with the AHP: Why is the principal eigenvector necessary. Eur. J. Oper. Res. 2003, 145, 85–91. [Google Scholar] [CrossRef]

- Crawford, G.B. The geometric mean procedure for estimating the scale of a judgment matrix. Math. Model. 1987, 9, 327–334. [Google Scholar] [CrossRef]

- Csató, L. A characterization of the Logarithmic Least Squares Method. Eur. J. Oper. Res. 2019, 276, 212–216. [Google Scholar] [CrossRef]

- Wang, L.; Xu, L.; Feng, S.; Meng, M.Q.-H.; Wang, K. Multi–Gaussian fitting for pulse waveform using Weighted Least Squares and multi-criteria decision making method. Comput. Biol. Med. 2013, 43, 1661–1672. [Google Scholar] [CrossRef]

- Wu, S.; Fu, Y.; Lai, K.K.; Leung, W.K.J. A Weighted Least-Square Dissimilarity Approach for multiple criteria ABC inventory classification. Asia-Pac. J. Oper. Res. 2018, 35, 1850025. [Google Scholar] [CrossRef]

- Mikhailov, L. Fuzzy programming method for deriving priorities in the Analytical Hierarchy Process. J. Oper. Res. Soc. 2000, 51, 341–349. [Google Scholar] [CrossRef]

- Wang, J.; Fan, K.; Wang, W. Integration of fuzzy AHP and FPP with TOPSIS methodology for aeroengine health assessment. Expert Syst. Appl. 2010, 37, 8516–8526. [Google Scholar] [CrossRef]

- Almulhim, T.; Mikhailov, L.; Xu, D.-L. A fuzzy group prioritization method for deriving weights and its software implementation. Int. J. Artif. Intell. Interact. Multimed. 2013, 2, 7–14. [Google Scholar] [CrossRef]

- Fallahpour, A.; Wong, K.Y.; Rajoo, S.; Olugu, E.U.; Nilashi, M.; Turskis, Z. A fuzzy decision support system for sustainable construction project selection: An integrated FPP-FIS model. J. Civ. Eng. Manag. 2020, 26, 247–258. [Google Scholar] [CrossRef]

- Kou, G.; Lin, C. A cosine maximization method for the priority vector derivation in AHP. Eur. J. Oper. Res. 2014, 235, 225–235. [Google Scholar] [CrossRef]

- Srdjevic, B. Combining different prioritization methods in the analytical hierarchy process synthesis. Comput. Oper. Res. 2005, 32, 1897–1919. [Google Scholar] [CrossRef]

- Keršulienė, V.; Zavadskas, E.K.; Turskis, Z. Selection of rational dispute resolution method by applying new stepwise weight assessment ratio analysis (SWARA). J. Bus. Econ. Manag. 2010, 11, 243–258. [Google Scholar] [CrossRef]

- Stanujkic, D.; Karabasevic, D.; Zavadskas, E.K. A framework for the selection of a packaging design based on the SWARA method. Eng. Econ. 2015, 26, 181–187. [Google Scholar] [CrossRef]

- Rezaei, J. Best-worst multi-criteria decision-making method. Omega 2015, 53, 49–57. [Google Scholar] [CrossRef]

- Rezaei, J. Best-worst multi-criteria decision-making method: Some properties and a linear model. Omega 2016, 64, 126–130. [Google Scholar] [CrossRef]

- Pamučar, D.; Ecer, F.; Cirovic, G.; Arlasheedi, M.A. Application of improved best worst method (BWM) in real-world problems. Mathematics 2020, 8, 1342. [Google Scholar] [CrossRef]

- Pamučar, D.; Stević, Ž.; Sremac, S. A new model for determining weight coefficients of criteria in MCDM models: Full Consistency Method (FUCOM). Symmetry 2018, 10, 393. [Google Scholar] [CrossRef]

- Fazlollahtabar, H.; Smailbašić, A.; Stević, Ž. FUCOM method in group decision-making: Selection of forklift in a warehouse. Decis. Mak. Appl. Manag. Eng. 2019, 2, 49–65. [Google Scholar] [CrossRef]

- Stević, Ž.; Brković, N. A novel integrated FUCOM-MARCOS model for evaluation of human resources in a transport company. Logistics 2020, 4, 4. [Google Scholar] [CrossRef]

- Žižović, M.; Pamučar, D. New model for determining criteria weights: Level Based Weight Assessment (LBWA) model. Decis. Mak. Appl. Manag. Eng. 2019, 2, 126–137. [Google Scholar] [CrossRef]

- Božanić, D.; Ranđelović, A.; Radovanović, M.; Tešić, D. A hybrid LBWA - IR-MAIRCA multi-criteria decision-making model for determination of constructive elements of weapons. Facta Univ. Ser. Mech. Eng. 2020, 18, 399–418. [Google Scholar] [CrossRef]

- Greblikaitė, J.; Daugėlienė, R. Cluster analysis of expression of entrepreneurship characteristics in the EU innovative projects for SME’s and KTU regional science park. Eur. Integr. Stud. 2009, 3, 184–189. [Google Scholar]

- Yüksel, I. Developing a multi-criteria decision making model for PESTEL analysis. Int. J. Bus. Manag. 2012, 7, 52–66. [Google Scholar] [CrossRef]

- Leyva Vázquez, M.; Hechavarría Hernández, J.; Batista Hernández, N.; Alarcón Salvatierra, J.A.; Gómez Baryolo, O. A framework for PEST analysis based on fuzzy decision maps. Rev. Espac. 2018, 39. Available online: https://www.revistaespacios.com/a18v39n16/18391603.html (accessed on 10 January 2018).

- Greblikaitė, J.; Astrovienė, J.; Montvydaitė, D. Value-added agricultural bio-business development in European countries. Manag. Theory Stud. Rural Bus. Infrastruct. Dev. 2020, 42, 235–247. [Google Scholar] [CrossRef]

- Saaty, R.W. The analytical hierarchy process – what it is and how it is used. Math. Model. 1987, 9, 161–176. [Google Scholar] [CrossRef]

- Saaty, T.L. Decision making with the analytical hierarchy process. Int. J. Serv. Sci. 2008, 1, 83–98. [Google Scholar]

Figure 1.

Saaty’s analytic hierarchy process for the identification of the investment appeal of startups based on their specific features.

Figure 1.

Saaty’s analytic hierarchy process for the identification of the investment appeal of startups based on their specific features.

Figure 2.

The dominant hierarchical representation of the problem of choosing investment alternatives in startups.

Figure 2.

The dominant hierarchical representation of the problem of choosing investment alternatives in startups.

{kind=link}

{kind=link}

Table 1.

Criteria composition for evaluating investment appeal of a startup.

| No | Type of Potential | Criteria |

|---|---|---|

| 1. | Financial strength | 1. Value of investment 2. Payback period (PBP) 3. Expected profitability 4. Risk level 5. Full or partial investor control of the startup 6. Possibility of reverse repurchase (RRP) 7. Possibility of tranche-funding, depending on the stage of the project |

| 2. | Product/service potential | 8. Availability of samples or models of the product |

| 3. | Marketing potential | 9. Startup position in the market 10. Forecasted level of demand for the product/service 11. Level of competition in the economic branch or industrial sector 12. Evaluation of startup competitiveness 13. Significant target audience 14. Availability of marketing strategy 15. Requirements to attract and interact with customers within the startup initial stage |

| 4. | Organizational potential | 16. Availability of organizational plan |

| 5. | Scientific and technical potential | 17. Innovation of idea 18. Innovation of technology 19. Availability of project plan for technical realization 20. Availability of intellectual property rights |

| 6. | Staff potential | 21. Availability of potential specialists 22. Uniqueness of specialists |

| 7. | Potential of the governmental, international, economic, and political situation | 23. The level of development of economic branch or sector in which the startup will operate 24. The level of governmental support of industry branch |

| 8. | Time potential | 25. Period of project completion 26. Stage of project development 27. Duration of product introductory period/start of retail service |

| 9. | Autonomy potential | 28. Dependence of the startup on other economic branches or industrial sectors 29. Dependence of the startup on other similar projects |

| 10. | Ecological potential | 30. Level of negative impact on the environment |

| 11. | Social potential | 31. Accessibility of project’s social utility |

| 12. | Information potential | 32. Availability, reliability, and quality of information in economic branch or industrial sector in which the startup will operate |

Table 2.

The matrix of pairwise comparisons to determine the validity of 12 groups of criteria.

| Groups of Criteria | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | RM | DV | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 1 | 3 | 3 | 4 | 2 | 1 | 2 | 2 | 4 | 5 | 4 | 3 | 0.1893 | 2.3312 | 12.31 |

| 2 | 1/3 | 1 | 1/2 | 1 | 1/2 | 1/2 | 1 | 1/2 | 3 | 3 | 3 | 4 | 0.0800 | 1.1099 | 13.87 |

| 3 | 1/3 | 2 | 1 | 2 | 1 | 1/2 | 1 | 1 | 2 | 2 | 2 | 2 | 0.0911 | 1.1345 | 12.45 |

| 4 | 1/4 | 1 | 1/2 | 1 | 1/2 | 1/5 | 1 | 1/2 | 1 | 1 | 1 | 1 | 0.0490 | 0.6099 | 12.45 |

| 5 | 1/2 | 2 | 1 | 2 | 1 | 1 | 2 | 1 | 2 | 2 | 2 | 2 | 0.1058 | 1.2968 | 12.26 |

| 6 | 1 | 2 | 2 | 5 | 1 | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 0.1282 | 1.6571 | 12.93 |

| 7 | 1/2 | 1 | 1 | 1 | 1/2 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 0.0666 | 0.8525 | 12.80 |

| 8 | 1/2 | 2 | 1 | 2 | 1 | 1/2 | 1 | 1 | 2 | 2 | 2 | 2 | 0.0942 | 1.1661 | 12.38 |

| 9 | 1/4 | 1/3 | 1/2 | 1 | 1/2 | 1/2 | 1 | 1/2 | 1 | 1 | 1 | 1 | 0.0483 | 0.5950 | 12.32 |

| 10 | 1/5 | 1/3 | 1/2 | 1 | 1/2 | 1/2 | 1 | 1/2 | 1 | 1 | 1/2 | 1/2 | 0.0422 | 0.5329 | 12.63 |

| 11 | 1/4 | 1/3 | 1/2 | 1 | 1/2 | 1 | 1 | 1/2 | 1 | 2 | 1 | 1/2 | 0.0511 | 0.6742 | 13.19 |

| 12 | 1/3 | 1/4 | 1/2 | 1 | 1/2 | 1/2 | 1 | 1/2 | 1 | 2 | 2 | 1 | 0.0542 | 0.6975 | 12.87 |

Table 3.

The matrix of pairwise comparisons for the group of criteria “Financial strength”.

| Startup | Production of LED Traffic Lights | Manufacture of Information–Reference Electronic Terminals | Manufacture of Rotor-Reactive Turbo-Rotational Heaters of Liquids | Priority Vector (The Normalized Vector of Geometric Means) | RM | DV |

|---|---|---|---|---|---|---|

| Production of LED traffic lights | 1 | 1/3 | 1 | 0.20984 | 0.63337 | 3.01835 |

| Manufacture of information–reference electronic terminals | 3 | 1 | 2 | 0.54994 | 1.65990 | 3.01833 |

| Manufacture of rotor-reactive turbo-rotational heaters of liquids | 1 | 1/2 | 1 | 0.24021 | 0.72503 | 3.01832 |

Table 4.

The optimal choice of startups according to the investment alternatives, based on the groups of criteria.

Table 4.

The optimal choice of startups according to the investment alternatives, based on the groups of criteria.

| Investing Alternatives in Startups | Production of LED Traffic Lights | Manufacture of Information–Reference Electronic Terminals | Manufacture of Rotor-Reactive Turbo-Rotational Heaters of Liquids | |

|---|---|---|---|---|

| No | Groups of Criteria | Priority Vectors | ||

| 1. | Financial strength | 0.2098 | 0.5499 | 0.2402 |

| 2. | Product/service potential | 0.2000 | 0.4000 | 0.4000 |

| 3. | Marketing potential | 0.2000 | 0.4000 | 0.4000 |

| 4. | Organizational potential | 0.2500 | 0.5000 | 0.2500 |

| 5. | Scientific and technical potential | 0.1634 | 0.5396 | 0.2970 |

| 6. | Staff potential | 0.1958 | 0.3108 | 0.4934 |

| 7. | Potential of governmental, international, | |||

| economic, and political situation | 0.2500 | 0.2500 | 0.5000 | |

| 8. | Time potential | 0.5936 | 0.1571 | 0.2493 |

| 9. | Autonomy potential | 0.1634 | 0.2970 | 0.5396 |

| 10. | Ecological potential | 0.2500 | 0.5000 | 0.2500 |

| 11. | Social potential | 0.3333 | 0.3333 | 0.3333 |

| 12. | Information potential | 0.3325 | 0.1396 | 0.5278 |

| 13. | Vector of global priorities | 0.2547 | 0.3855 | 0.3599 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kyrylych, T.; Povstenko, Y. Multi-Criteria Analysis of Startup Investment Alternatives Using the Hierarchy Method. Entropy 2023, 25, 723. https://doi.org/10.3390/e25050723

AMA Style

Kyrylych T, Povstenko Y. Multi-Criteria Analysis of Startup Investment Alternatives Using the Hierarchy Method. Entropy. 2023; 25(5):723. https://doi.org/10.3390/e25050723

Chicago/Turabian StyleKyrylych, Tamara, and Yuriy Povstenko. 2023. "Multi-Criteria Analysis of Startup Investment Alternatives Using the Hierarchy Method" Entropy 25, no. 5: 723. https://doi.org/10.3390/e25050723

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.