The Risk Contagion between Chinese and Mature Stock Markets: Evidence from a Markov-Switching Mixed-Clayton Copula Model

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Marginal Distribution Modeling

3.2. Markov-Switching Mixed-Clayton Copula Function

3.3. Markov-Switching Mixed-Clayton Copula Function

3.4. Parameter Estimation Method

3.5. VaR and CoVaR

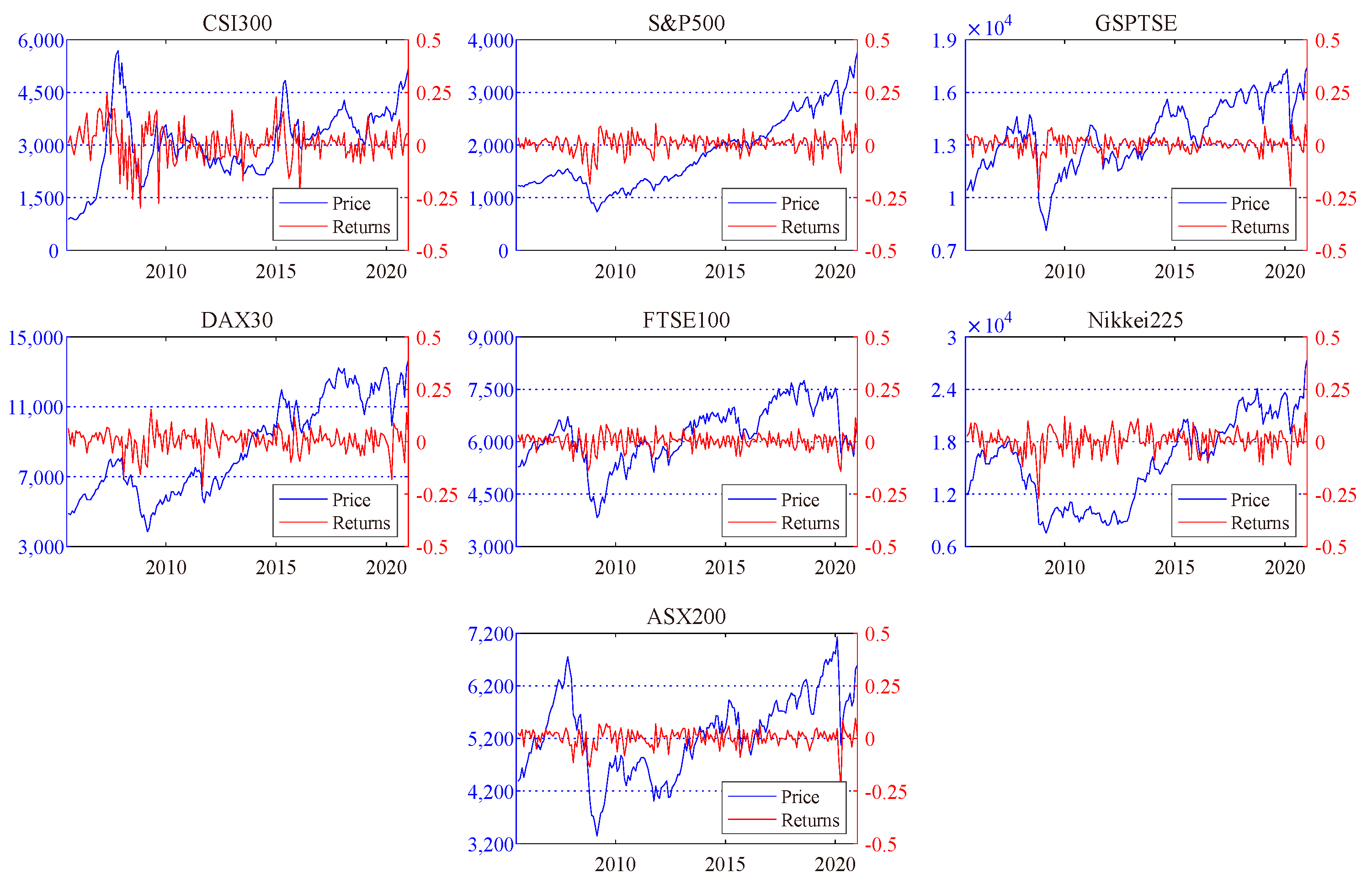

4. Data and Descriptive Statistics

5. Empirical Results

5.1. Marginal Distribution Estimation

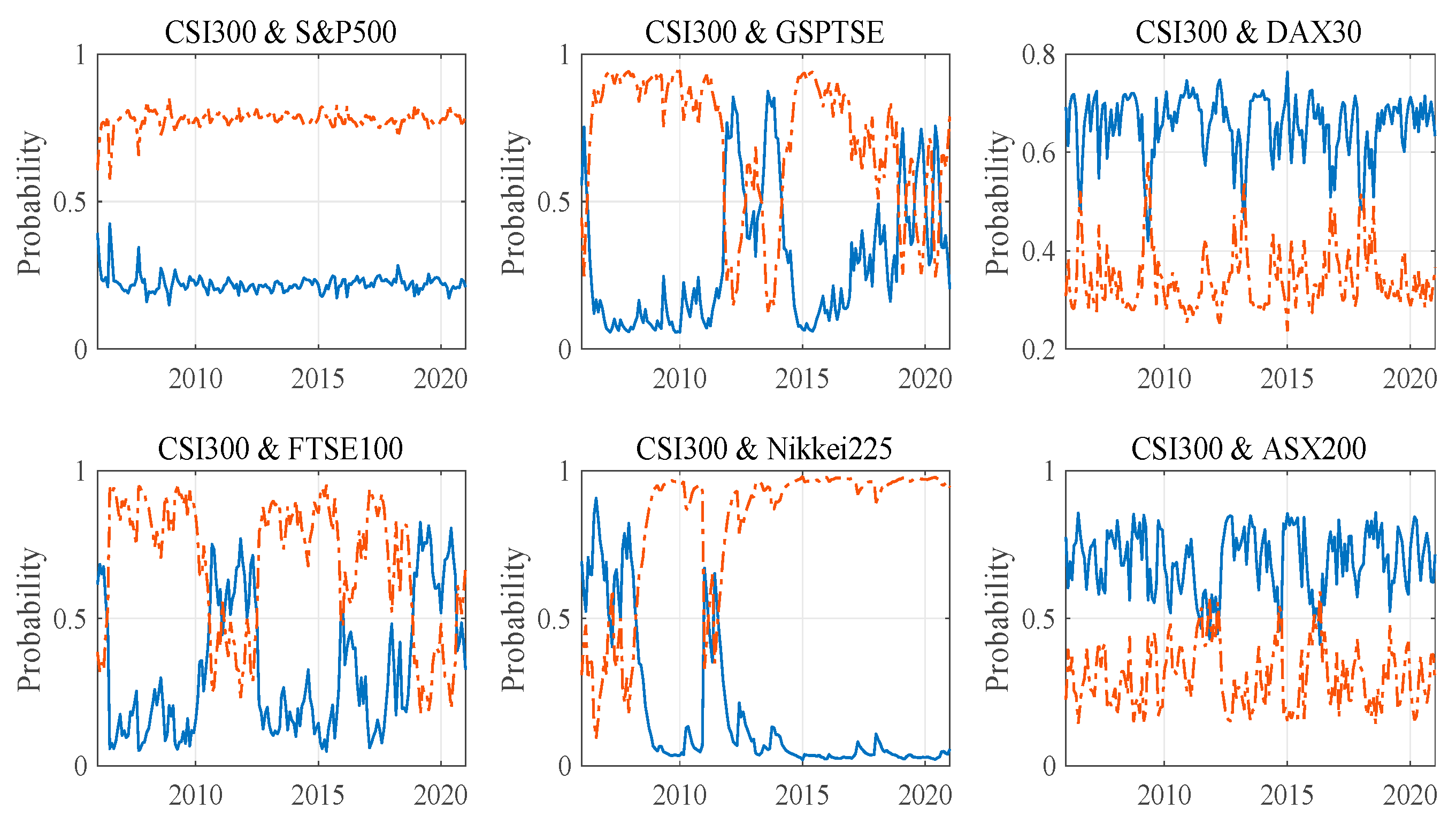

5.2. Dynamic and Asymmetric Dependence Measured by MS-M-Clayton Copula

5.3. Comparative Analysis

5.3.1. Static Dependence Measured by Invariant Copula Models

5.3.2. Dynamic Dependence Measured by Time-Varying Parameter Copula

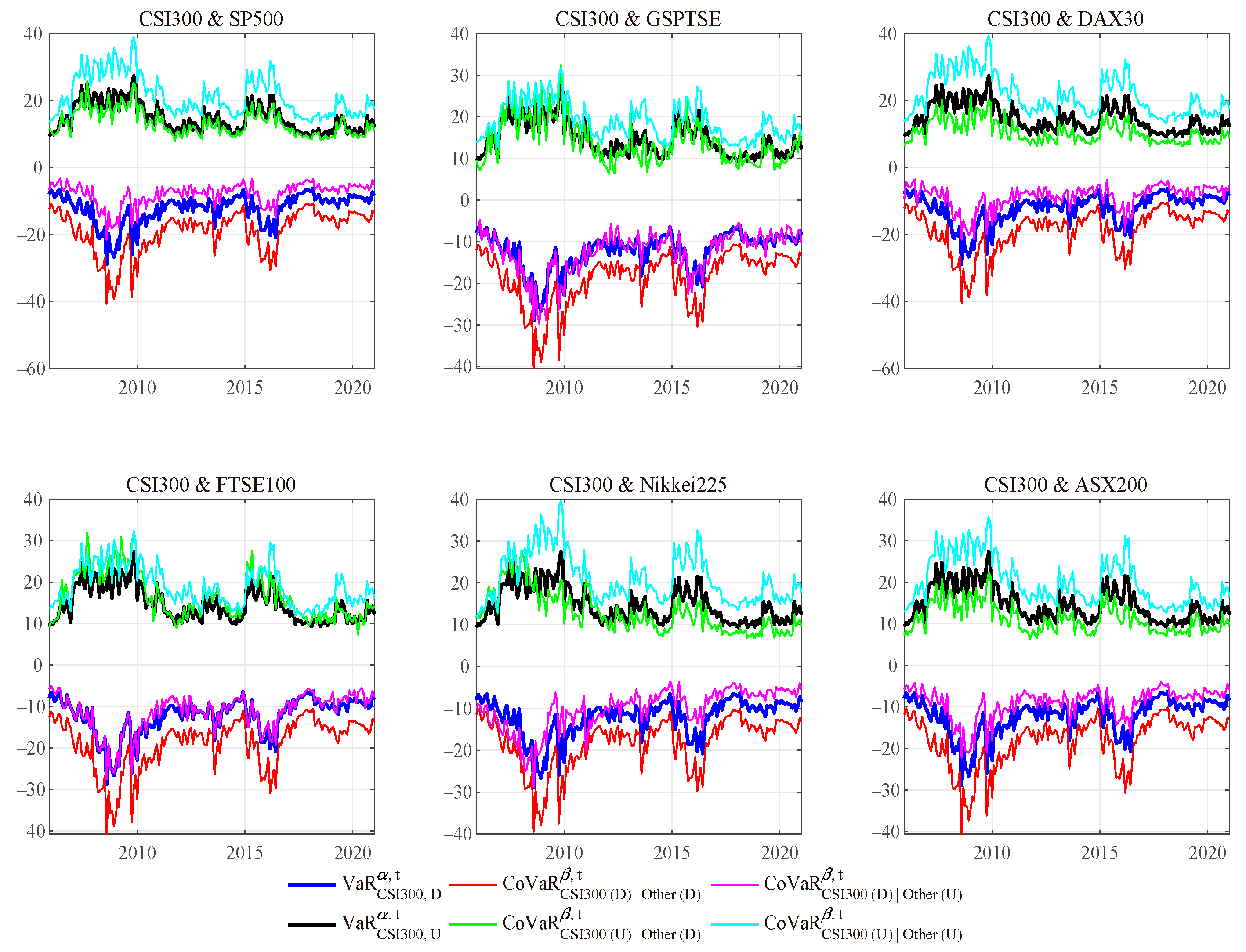

5.4. Asymmetric Risk Spillover Measurement by VaR, CoVaR and Nomalized CoVaR

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| CSI300 | S&P500 | GSPTSE | DAX30 | FTSE100 | Nikkei225 | ASX200 | |

|---|---|---|---|---|---|---|---|

| ADF | −11.633 *** | −12.099 *** | −11.859 *** | −12.234 *** | −13.419 *** | −11.760 *** | −12.253 *** |

| PP | −12.293 *** | −12.145 *** | −11.920 *** | −12.181 *** | −13.418 *** | −11.763 *** | −12.248 *** |

| KPSS | 0.104 | 0.179 | 0.033 | 0.045 | 0.059 | 0.135 | 0.048 |

| Q (5) | 21.335 *** | 6.294 | 7.096 | 7.109 | 3.385 | 4.423 | 3.236 |

| Q (10) | 25.902 *** | 15.362 | 14.193 | 15.727 | 9.440 | 8.564 | 6.966 |

| Q2(5) | 28.419 *** | 48.390 *** | 16.423 *** | 5.253 | 17.739 *** | 5.174 | 11.914 ** |

| Q2(10) | 58.267 *** | 52.676 *** | 18.408 ** | 12.539 | 39.787 *** | 10.733 | 14.600 |

| ARCH (1) | 0.704 | 26.472 *** | 15.538 *** | 2.126 | 15.553 *** | 3.634 * | 11.383 *** |

| ARCH (5) | 14.973 *** | 40.282 *** | 17.452 *** | 4.533 | 17.119 *** | 7.610 | 11.441 ** |

| Parameters | CSI300 | S&P500 | GSPTSE | DAX30 | FTSE100 | Nikkei225 | ASX200 | |

|---|---|---|---|---|---|---|---|---|

| Panel A. | 1.348 ** (0.668) | 1.092 *** (0.240) | 0.282 *** (0.100) | 0.589 (0.398) | 0.447 (0.280) | 0.659 (0.494) | 0.760 *** (0.286) | |

| AR-GARCH model | 0.092 * (0.071) | |||||||

| 0.189 *** (0.062) | ||||||||

| 4.201 (4.241) | 1.137 (0.937) | 0.642 *** (0.211) | 1.106 (1.058) | 4.700 (3.963) | 11.320 *** (2.144) | |||

| 0.153 (0.116) | 0.248 *** (0.102) | 0.535 *** (0.103) | 0.132 ** (0.062) | 0.128 ** (0.053) | 0.356 *** (0.130) | |||

| 0.797 *** (0.135) | 0.723 *** (0.105) | 0.342 *** (0.097) | 0.809 *** (0.102) | 0.730 *** (0.149) | ||||

| GED. | 1.193 *** (0.135) | 1.286 *** (0.213) | 1.652 *** (0.262) | 1.494 *** (0.242) | ||||

| Panel B. | Log-L | −627.552 | −510.743 | −343.105 | −578.161 | −511.389 | −579.028 | −517.528 |

| Diagnostic tests | AIC | 6.973 | 5.546 | 3.732 | 6.228 | 5.553 | 6.314 | 5.608 |

| Q (5) | 3.820 | 1.698 | 3.799 | 7.109 | 0.712 | 0.474 | 1.594 | |

| Q (10) | 6.385 | 6.374 | 7.398 | 15.727 | 4.119 | 3.896 | 5.102 | |

| Q2 (5) | 2.549 | 3.639 | 3.505 | 5.971 | 5.056 | 2.588 | 1.393 | |

| Q2 (10) | 9.202 | 9.977 | 9.374 | 12.817 | 15.250 | 7.690 | 9.668 | |

| ARCH (1) | 0.278 | 1.998 | 2.009 | 2.124 | 2.289 | 0.796 | 0.590 | |

| ARCH (5) | 2.491 | 3.607 | 3.678 | 4.533 | 4.583 | 3.340 | 1.273 |

| Hypotheses | CSI300-S&P500 | CSI300-GSPTSE | CSI300-DAX30 | CSI300-FTSE100 | CSI300-Nikkei225 | CSI300-ASX200 |

|---|---|---|---|---|---|---|

| ; . | 1.000 *** (0.000) | 1.000 *** (0.000) | 1.000 *** (0.000) | 1.000 *** (0.000) | 0.945 *** (0.000) | 0.550 *** (0.000) |

| ; . | 1.000 *** (0.000) | 0.824 *** (0.000) | 1.000 *** (0.000) | 0.577 *** (0.000) | 0.896 *** (0.000) | 0.445 *** (0.000) |

| Hypotheses | CSI300-S&P500 | CSI300-GSPTSE | CSI300-DAX30 | CSI300-FTSE100 | CSI300-Nikkei225 | CSI300-ASX200 |

|---|---|---|---|---|---|---|

| ; . | 0.615 *** (0.000) | 0.797 *** (0.000) | 0.440 *** (0.000) | 0.830 *** (0.000) | 0.247 *** (0.000) | 0.412 *** (0.000) |

| ; . | 0.989 *** (0.000) | 0.346 *** (0.000) | 0.253 (0.217) | 0.703 *** (0.000) | 0.484 *** (0.000) | 0.473 *** (0.000) |

References

- Vogl, M. Chaos Measure Dynamics and a Multifactor Model for Financial Markets. Available at SSRN 4251673. 2022. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4251673 (accessed on 20 October 2022).

- Vogl, M. Quantitative modelling frontiers: A literature review on the evolution in financial and risk modelling after the financial crisis (2008–2019). SN Bus. Econ. 2022, 2, 183. [Google Scholar] [CrossRef] [PubMed]

- Liu, Y.; Wei, Y.; Wang, Q.; Liu, Y. International stock market risk contagion during the COVID-19 pandemic. Financ. Res. Lett. 2022, 45, 102145. [Google Scholar] [CrossRef] [PubMed]

- Marfatia, H.A. A fresh look at integration of risks in the international stock markets: A wavelet approach. Rev. Financ. Econ. 2017, 34, 33–49. [Google Scholar] [CrossRef]

- Marfatia, H.A. Investors’ risk perceptions in the US and global stock market integration. Res. Int. Bus. Financ. 2020, 52, 101169. [Google Scholar] [CrossRef]

- Bhatti, M.I.; Nguyen, C.C. Diversification evidence from international equity markets using extreme values and stochastic copulas. J. Int. Financ. Mark. Inst. Money 2012, 22, 622–646. [Google Scholar] [CrossRef]

- An, S. Dynamic Multiscale Information Spillover among Crude Oil Time Series. Entropy 2022, 24, 1248. [Google Scholar] [CrossRef]

- Lai, Y.H.; Tseng, J.C. The role of Chinese stock market in global stock markets: A safe haven or a hedge? Int. Rev. Econ. Financ. 2010, 19, 211–218. [Google Scholar] [CrossRef]

- Zhong, Y.; Liu, J.P. Correlations and volatility spillovers between China and Southeast Asian stock markets. Quart. Rev. Econ. Financ. 2021, 81, 57–69. [Google Scholar] [CrossRef]

- Kole, E.; Koedijk, K.; Verbeek, M. Selecting copulas for risk management. J. Bank Financ. 2007, 31, 2405–2423. [Google Scholar] [CrossRef] [Green Version]

- Luo, C.Q.; Xie, C.; Yu, C.; Xu, Y. Measuring financial market risk contagion using dynamic MRS-Copula models: The case of Chinese and other international stock markets. Econ. Model. 2015, 51, 657–671. [Google Scholar]

- Di Persio, L.; Vettori, S. Markov Switching Model Analysis of Implied Volatility for Market Indexes with Applications to S&P 500 and DAX. J. Math. 2014, 2014, 1–17. [Google Scholar]

- Fermanian, J.-D. Recent Developments in Copula Models. Econometrics 2017, 5, 34. [Google Scholar] [CrossRef] [Green Version]

- Ji, Q.; Liu, B.-Y.; Cunado, J.; Gupta, R. Risk spillover between the US and the remaining G7 stock markets using time-varying copulas with Markov switching: Evidence from over a century of data. N. Am. J. Econ. Financ. 2020, 51, 100846. [Google Scholar] [CrossRef] [Green Version]

- Di Persio, L.; Frigo, M. Gibbs sampling approach to regime switching analysis of financial time series. J. Comput. Appl. Math. 2016, 300, 43–55. [Google Scholar] [CrossRef]

- Segnon, M.; Trede, M. Forecasting market risk of portfolios: Copula-Markov switching multifractal approach. Eur. J. Financ. 2017, 24, 1123–1143. [Google Scholar] [CrossRef] [Green Version]

- Rajwani, S.; Kumar, D. Measuring dependence between the USA and the Asian economies: A time-varying Copula approach. Glob. Bus. Rev. 2019, 20, 962–980. [Google Scholar] [CrossRef]

- Wang, K.; Chen, Y.-H.; Huang, S.-W. The dynamic dependence between the Chinese market and other international stock markets: A time-varying copula approach. Int. Rev. Econ. Financ. 2011, 20, 654–664. [Google Scholar] [CrossRef]

- Jiang, C.X.; Li, Y.Q.; Xu, Q.F.; Liu, Y. Measuring risk spillovers from multiple developed stock markets to China: A vine-copula-GARCH-MIDAS model. Int. Rev. Econ. Financ. 2021, 75, 386–398. [Google Scholar] [CrossRef]

- Liu, X.-D.; Pan, F.; Cai, W.-L.; Peng, R. Correlation and risk measurement modeling: A Markov-switching mixed Clayton copula approach. Reliab. Eng. Syst. Saf. 2020, 197, 106808. [Google Scholar] [CrossRef]

- Abakah, E.J.A.; Tiwari, A.K.; Alagidede, I.P.; Gil-Alana, L.A. Re-examination of risk-return dynamics in international equity markets and the role of policy uncertainty, geopolitical risk and VIX: Evidence using Markov-switching copulas. Financ. Res. Lett. 2022, 47, 102535. [Google Scholar] [CrossRef]

- Reinhart, C.M.; Calvo, S. Capital Flows to Latin America: Is There Evidence of Contagion Effects; Peterson Institute for International Economics: Washington, DC, USA, 1996. [Google Scholar]

- Forbes, K.; Rigobon, R. No contagion, only interdependence: Measuring stock market comovements. J. Financ. 2010, 57, 2223–2261. [Google Scholar] [CrossRef]

- Mihai, N.; Maria, M.P. Time-varying dependence in European equity markets: A contagion and investor sentiment driven analysis. Econ. Model. 2020, 86, 133–147. [Google Scholar]

- Ajaya, K.P.; Pradiptarathi, P.; Swagatika, N.; Parad, A. Information bias and its spillover effect on return volatility: A study on stock markets in the Asia-Pacific region. Pac.-Basin Financ. J. 2021, 69, 101653. [Google Scholar]

- Fan, H.C.; Gou, Q.; Peng, Y.C. Spillover effects of capital controls on capital flows and financial risk contagion. J. Int. Money Financ. 2020, 105, 102189. [Google Scholar] [CrossRef]

- Alberto, B.; David, L.T.; Danilo, L.; Marsiglio, S. Financial contagion and economic development: An epidemiological approach. J. Econ. Behav. Organ. 2019, 162, 211–228. [Google Scholar]

- Cheng, H.; Glascock, J.L. Stock market linkages before and after the Asian financial crisis: Evidence from three greater china economic area stock markets and the us. Rev. Pac. Basin Financ. 2006, 9, 297–315. [Google Scholar] [CrossRef]

- Li, H. International linkages of the Chinese stock exchanges: A multivariate GARCH analysis. Appl. Financ. Econ. 2007, 17, 285–297. [Google Scholar] [CrossRef]

- Chatziantoniou, I.; Gabauer, D.; Marfatia, H.A. Dynamic connectedness and spillovers across sectors: Evidence from the Indian stock market. Scott. J. Political Econ. 2021, 69, 283–300. [Google Scholar] [CrossRef]

- Sklar, A. Fonctions de repartition à n dimensions et leurs marges. Publ. De L’institut De Stat. De L’université De Paris 1959, 8, 229–231. [Google Scholar]

- Chang, K.L. Does REIT index hedge inflation risk? new evidence from the tail quantile dependences of the Markov-switching GRG copula. N. Am. J. Econ. Financ. 2017, 39, 56–67. [Google Scholar] [CrossRef]

- Huang, J.J.; Lee, K.J.; Liang, H.M.; Lin, W.F. Estimating value at risk of portfolio by conditional copula-GARCH method. Insur. Math. Econ. 2009, 45, 315–324. [Google Scholar] [CrossRef]

- Hussain, S.I.; Li, S. The dependence structure between Chinese and other major stock markets using extreme values and copulas. Int. Rev. Econ. Financ. 2018, 56, 421–437. [Google Scholar] [CrossRef]

- Luo, C.Q.; Liu, L.; Wang, D. Multiscale financial risk contagion between international stock markets: Evidence from EMD-Copula-CoVaR analysis. N. Am. J. Econ. Financ. 2021, 58, 101512. [Google Scholar] [CrossRef]

- Patton, A.J. Modelling asymmetric exchange rate dependence. Int. Econ. Rev. 2006, 47, 527–556. [Google Scholar] [CrossRef] [Green Version]

- Zhang, X.; Zhang, T.; Lee, C.C. The path of financial risk spillover in the stock market based on the R-vine-Copula model. Physics A 2022, 600, 127470. [Google Scholar] [CrossRef]

- Andrieu, C.; Thoms, J. A tutorial on adaptive MCMC. Stat. Comput. 2008, 18, 343–373. [Google Scholar] [CrossRef]

- Huang, C.W.; Hsu, C.P.; Chiou, W.J.P. Can Time-Varying Copulas Improve the Mean-Variance Portfolio; Springer: New York, NY, USA, 2014. [Google Scholar]

- Wang, Y.C.; Wu, J.L.; Lai, Y.H. A revisit to the dependence structure between the stock and foreign exchange markets: A dependence-switching copula approach. J. Bank. Financ. 2013, 37, 1706–1719. [Google Scholar] [CrossRef]

- Ji, Q.; Bouri, E.; Roubaud, D.; Shahzad, S.J.H. Risk spillover between energy and agricultural commodity markets: A dependence-switching CoVaR-copula model. Energy Econ. 2018, 75, 14–27. [Google Scholar] [CrossRef]

- Reboredo, J.C.; Ugolini, A. Systemic risk in European sovereign debt markets: A CoVaR-copula approach. J. Int. Money Financ. 2015, 51, 214–244. [Google Scholar] [CrossRef]

- Reboredo, J.C.; Ugolini, A. Downside/upside price spillovers between precious metals: A vine copula approach. N. Am. J. Econ. Financ. 2015, 34, 84–102. [Google Scholar] [CrossRef]

- Xiao, Y. The risk spillovers from the Chinese stock market to major East Asian stock markets: A MSGARCH-EVT-copula approach. Int. Rev. Econ. Financ. 2020, 65, 173–186. [Google Scholar] [CrossRef]

- Sun, X.; Liu, C.; Wang, J.; Li, J. Assessing the extreme risk spillovers of international commodities on maritime markets: A GARCH-Copula-CoVaR approach. Int. Rev. Financ. Anal. 2020, 68, 101453. [Google Scholar] [CrossRef]

- Bai, X.; Lam, J.S.L. A copula-GARCH approach for analyzing dynamic conditional dependence structure between liquefied petroleum gas freight rate, product price arbitrage and crude oil price. Energy Econ. 2019, 78, 412–427. [Google Scholar] [CrossRef]

- Nguyen, Q.N.; Bedoui, R.; Majdoub, N.; Guesmi, K.; Chevallier, J. Hedging and safe-haven characteristics of gold against currencies: An investigation based on multivariate dynamic copula theory. Resour. Policy 2020, 68, 101766. [Google Scholar] [CrossRef]

- Liu, X.D.; Pan, F.; Yuan, L.; Chen, Y. The dependence structure between crude oil futures prices and Chinese agricultural commodity futures prices: Measurement based on Markov-switching GRG copula. Energy 2019, 182, 999–1012. [Google Scholar] [CrossRef]

- Joe, H. Multivariate Models and Dependence Concepts; Chapman & Hall: London, UK, 1997. [Google Scholar]

- Dempster, A.P. Maximum likelihood from incomplete data via the EM algorithm. J. R. Stat. Soc. 1977, 39, 1–38. [Google Scholar]

- Li, M.; Lu, Y. Genetic Algorithm Based Maximum Likelihood DOA Estimation. In Proceedings of the 2002 International Radar Conference, Edinburgh, UK, 15–17 October 2002; pp. 502–506, IET Digital Library. [Google Scholar]

- Gray, S.F. Modeling the conditional distribution of interest rates as a regime-switching process. J. Financ. Econ. 1996, 42, 27–62. [Google Scholar] [CrossRef]

- Li, X.F.; Wei, Y. The dependence and risk spillover between crude oil market and China stock market: New evidence from a variational mode decomposition-based copula method. Energy Econ. 2018, 74, 565–581. [Google Scholar] [CrossRef]

- Huang, Q.; Wang, X.; Zhang, S. The effects of exchange rate fluctuations on the stock market and the affecting mechanisms: Evidence from BRICS countries. N. Am. J. Econ. Financ. 2021, 56, 101340. [Google Scholar] [CrossRef]

| CSI300 | S&P500 | GSPTSE | DAX30 | FTSE100 | Nikkei225 | ASX200 | |

|---|---|---|---|---|---|---|---|

| Mean | 0.0096 | 0.0062 | 0.0030 | 0.0059 | 0.0013 | 0.0046 | 0.0023 |

| Max. | 0.2463 | 0.1194 | 0.0997 | 0.1550 | 0.1155 | 0.1401 | 0.0949 |

| Min. | −0.2991 | −0.1856 | −0.2168 | −0.2131 | −0.1413 | −0.2722 | −0.2380 |

| Std. | 0.0858 | 0.0436 | 0.0404 | 0.0543 | 0.0402 | 0.0570 | 0.0428 |

| Skew. | −0.524 | −0.888 | −1.649 | −0.809 | −0.668 | −0.896 | −1.470 |

| Kurt. | 4.691 | 5.245 | 9.930 | 5.010 | 4.236 | 5.347 | 7.963 |

| J-B. | 30.685 a | 63.540 a | 456.478 a | 51.620 a | 25.654 a | 67.595 a | 257.900 a |

| Pearson. | 1.000 | 0.402 a | 0.403 a | 0.374 a | 0.307 a | 0.361 a | 0.380 a |

| CSI300-S&P500 | CSI300-GSPTSE | CSI300-DAX30 | CSI300-FTSE100 | CSI300-Nikkei225 | CSI300-ASX200 | |

|---|---|---|---|---|---|---|

| 0.682 a | 2.194 a | 0.889 a | 0.892 a | 0.488 a | 0.969 a | |

| 2.68 × 10−7 a | 8.67 × 10−8 a | 1.69 × 10−7 a | 3.24 × 10−8 a | 49.415 a | 5.23 × 10−7 a | |

| 0.674 a | 0.513 a | 2.587 a | 7.08 × 10−9 a | 0.506 a | 4.705 a | |

| 3.0967 a | 5.58 × 10−8 a | 1.18 × 10−7 a | 9.049 a | 5.946 a | 2.45 × 10−7 a | |

| 0.924 a | 0.594 a | 0.571 a | 0.923 a | 0.947 a | 0.443 a | |

| Log-L | −13.473 | −8.808 | −10.369 | −10.453 | −10.075 | −9.776 |

| Copula | CSI300-S&P500 | CSI300-GSPTSE | CSI300-DAX30 | CSI300-FTSE100 | CSI300-Nikkei225 | CSI300-ASX200 |

|---|---|---|---|---|---|---|

| 3.176 | 0.262 a | 0.652 a | 1.622 | 0.527 a | 0.243 a | |

| 1.82 × 10−10 a | 9.12 × 10−8 a | 25.801 a | 4.11 × 10−9 a | 54.908 a | 2.68 × 10−8 a | |

| 0.601 c | 5.594 a | 0.998 a | 3.278 a | 2.66 × 10−9 a | 0.141 | |

| 3.043 | 8.28 × 10−8 a | 3.95 × 10−9 a | 1.70 × 10−9 a | 3.62 × 10−9 a | 1.770 | |

| 0.584 a | 1.637 a | 0.275 | 0.653 a | 0.461 a | 1.627 | |

| 1.95 × 10−10 a | 3.23 × 10−8 a | 1.11 × 10−10 a | 3.28 × 10−9 a | 3.24 × 10−10 a | 0.094 | |

| 0.616 a | 1.39 × 10−7 a | 20.078 a | 1.93 × 10−10 a | 0.776 a | 5.363 a | |

| 3.077 | 8.03 × 10−9 a | 5.89 × 10−10 a | 6.832 a | 6.844 a | 1.37 × 10−8 a | |

| 0.656 b | 0.984 a | 0.978 a | 0.827 a | 0.676 a | 1.000 a | |

| 0.999 a | 0.676 a | 0.415 c | 0.817 a | 0.971 a | 0.932 c | |

| 0.517 | 0.943 a | 0.846 a | 0.941 a | 0.943 a | 0.881 a | |

| 0.864 a | 0.974 a | 0.710 a | 0.971 a | 0.993 a | 0.727 a | |

| Log-L | −13.626 | −11.276 | −12.487 | −12.369 | −11.522 | −11.777 |

| State 1 | State 2 | |||||||

|---|---|---|---|---|---|---|---|---|

| CSI300-S&P500 | 0.264 | 0.000 | 0.103 | 0.137 | 0.152 | 0.000 | 0.162 | 0.001 |

| CSI300-GSPTSE | 0.035 | 0.000 | 0.435 | 0.000 | 0.221 | 0.000 | 0.000 | 0.000 |

| CSI300-DAX30 | 0.169 | 0.011 | 0.244 | 0.000 | 0.017 | 0.000 | 0.200 | 0.000 |

| CSI300-FTSE100 | 0.270 | 0.000 | 0.334 | 0.000 | 0.141 | 0.000 | 0.000 | 0.083 |

| CSI300-Nikkei225 | 0.091 | 0.160 | 0.000 | 0.000 | 0.108 | 0.000 | 0.199 | 0.013 |

| CSI300-ASX200 | 0.029 | 0.000 | 0.004 | 0.000 | 0.304 | 0.000 | 0.410 | 0.000 |

| Copula | CSI300-SP500 | CSI300-GSPTSE | CSI300-DAX30 | CSI300-FTSE100 | CSI300-Nikkei225 | CSI300-ASX200 |

|---|---|---|---|---|---|---|

| Gaussian | ||||||

| 0.372 a | 0.348 a | 0.361 a | 0.266 a | 0.314 a | 0.349 a | |

| Log-L | −12.496 | −10.781 | −11.660 | −6.077 | −8.637 | −10.853 |

| Student’s t | ||||||

| 0.372 a | 0.347 a | 0.375 a | 0.285 a | 0.314 a | 0.356 a | |

| 99.899 a | 99.983 a | 7.966 a | 7.527 a | 99.320 a | 8.910 a | |

| Log-L | −12.474 | −10.596 | −12.438 | −7.069 | −8.634 | −11.710 |

| Gumbel | ||||||

| 1.223 a | 1.183 a | 1.260 a | 1.141 a | 1.183 a | 1.228 a | |

| Log-L | −6.541 | −4.251 | −8.307 | −2.477 | −4.729 | −6.603 |

| 180° rotated Gumbel | ||||||

| 1.326 a | 1.281 a | 1.329 a | 1.259 a | 1.256 a | 1.316 a | |

| Log-L | −15.498 | −11.794 | −14.612 | −10.533 | −10.484 | −14.249 |

| Clayton | ||||||

| 0.630 a | 0.543 a | 0.594 a | 0.523 b | 0.505 a | 0.593 a | |

| Log-L | −16.645 | −13.235 | −14.419 | −12.023 | −12.126 | −14.634 |

| 180° rotated Clayton | ||||||

| 0.307 c | 0.263 | 0.355 c | 0.130 | 0.237 | 0.310 c | |

| Log-L | −4.233 | −3.046 | −5.244 | −0.671 | −2.478 | −4.320 |

| SJC | ||||||

| 2.83 × 10−7 | 4.77 × 10−7 | 5.57 × 10−8 | 1.85 × 10−7 | 4.21 × 10−7 | 4.96 × 10−7 | |

| 0.380 | 0.404 | 0.366 a | 0.346 | 0.320 | 0.354 | |

| Log-L | −16.508 | −11.868 | −14.474 | −12.044 | −11.464 | −14.735 |

| Copula | CSI300-S&P500 | CSI300-GSPTSE | CSI300-DAX30 | CSI300-FTSE100 | CSI300-Nikkei225 | CSI300-ASX200 |

|---|---|---|---|---|---|---|

| TVP-Gaussian | ||||||

| 0.255 a | 1.162 a | 0.091 a | 0.711 a | 0.321 a | 1.601 a | |

| 0.270 a | 0.258 a | −0.169 a | 0.023 a | −0.049 a | −0.739 a | |

| 1.227 a | −1.423 a | 2.042 a | −0.635 a | 1.117 a | −1.762 a | |

| Log-L | −13.283 | −10.836 | −13.771 | −6.078 | −8.661 | −11.657 |

| TVP-180° Rotated Gumbel | ||||||

| 2.435 a | 1.144 a | 2.800 a | 1.557 a | 0.993 a | −0.429 a | |

| −0.815 a | −0.311 a | −0.768 a | −0.557 a | −0.324 a | 0.683 a | |

| −2.851 a | −0.766 a | −5.030 a | −1.291 a | −0.263 a | 0.340 a | |

| Log-L | −18.779 | −11.955 | −17.436 | −10.738 | −10.512 | −14.862 |

| TVP-Gumbel | ||||||

| 2.338 a | 2.903 a | 3.366 a | 3.106 a | −0.654 a | −0.608 a | |

| −0.916 a | −0.744 a | −1.018 a | −1.363 a | 0.942 a | 0.620 a | |

| −2.541 a | −6.164 a | −6.821 a | −4.265 a | −0.110 a | 1.100 a | |

| Log-L | −9.867 | −9.881 | −15.758 | −7.732 | −5.015 | −8.784 |

| TVP-SJC | ||||||

| −14.830 a | −14.363 a | −15.343 a | −15.242 a | −14.593 a | −14.490 a | |

| −0.012 a | −0.002 b | −8.391 × 10−4 c | −0.002 a | −0.002 a | −5.799 × 10−4 b | |

| −0.003 a | 7.327 × 10−5 | 4.025 × 10−6 | −1.465 × 10−6 | −1.469 × 10−5 | −1.642 × 10−4 | |

| 2.792 a | 0.459 a | 5.150 a | 4.447 a | −0.181 a | −2.235 a | |

| −5.960 a | −2.988 a | −18.110 a | −15.809 a | −1.477 a | 1.071 a | |

| −4.505 a | −1.209 a | −4.230 a | −4.203 a | −0.858 a | 3.771 a | |

| Log-L | −19.595 | −12.379 | −17.450 | −12.804 | −11.371 | −14.976 |

| CSI300-S&P500 | CSI300-GSPTSE | CSI300-DAX30 | CSI300-FTSE100 | CSI300-Nikkei225 | CSI300-ASX200 | |

|---|---|---|---|---|---|---|

| −12.258 (4.483) | ||||||

| 14.720 (4.227) | ||||||

| −19.060 (6.337) | −18.840 (6.335) | −18.791 (6.271) | −19.021 (6.228) | −18.275 (6.143) | −18.369 (6.126) | |

| −7.773 (3.309) | −12.474 (5.122) | −8.736 (3.646) | −11.459 (4.664) | −10.170 (4.875) | −9.026 (3.706) | |

| 13.260 (3.827) | 14.060 (5.324) | 10.639 (3.344) | 16.491 (5.574) | 12.942 (5.057) | 11.247 (3.468) | |

| 21.470 (6.056) | 19.090 (4.497) | 21.704 (6.116) | 18.901 (4.802) | 21.119 (5.988) | 20.147 (5.650) | |

| Null Hypotheses | CSI300-S&P500 | CSI300-GSPTSE | CSI300-DAX30 | CSI300-FTSE100 | CSI300-Nikkei225 | CSI300-ASX200 |

|---|---|---|---|---|---|---|

| 0.593 a (0.000) | 0.577 a (0.000) | 0.577 a (0.000) | 0.582 a (0.000) | 0.550 a (0.000) | 0.550 a (0.000) | |

| 0.582 a (0.000) | 0.077 (0.637) | 0.456 a (0.000) | 0.159 b (0.017) | 0.330 a (0.000) | 0.445 a (0.000) | |

| 0.181 a (0.004) | 0.220 a (0.000) | 0.478 a (0.000) | 0.132 (0.077) | 0.324 b (0.047) | 0.412 a (0.000) | |

| 0.533 a (0.000) | 0.456 a (0.000) | 0.544 a (0.000) | 0.418 a (0.000) | 0.517 a (0.000) | 0.473 a (0.000) |

| CSI300-SP500 | CSI300-GSPTSE | CSI300-DAX30 | CSI300-FTSE100 | CSI300-Nikkei225 | CSI300-ASX200 | |

|---|---|---|---|---|---|---|

| 1.571 (0.082) | 1.551 (0.082) | 1.548 (0.079) | 1.569 (0.080) | 1.504 (0.069) | 1.513 (0.080) | |

| 0.625 (0.056) | 1.014 (0.161) | 0.707 (0.101) | 0.926 (0.094) | 0.828 (0.264) | 0.729 (0.054) | |

| 0.903 (0.056) | 0.943 (0.162) | 0.721 (0.063) | 1.110 (0.113) | 0.871 (0.185) | 0.762 (0.051) | |

| 1.461 (0.055) | 1.317 (0.110) | 1.478 (0.059) | 1.299 (0.118) | 1.441 (0.111) | 1.372 (0.061) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Niu, H.; Xu, K.; Xiong, M. The Risk Contagion between Chinese and Mature Stock Markets: Evidence from a Markov-Switching Mixed-Clayton Copula Model. Entropy 2023, 25, 619. https://doi.org/10.3390/e25040619

Niu H, Xu K, Xiong M. The Risk Contagion between Chinese and Mature Stock Markets: Evidence from a Markov-Switching Mixed-Clayton Copula Model. Entropy. 2023; 25(4):619. https://doi.org/10.3390/e25040619

Chicago/Turabian StyleNiu, Hongli, Kunliang Xu, and Mengyuan Xiong. 2023. "The Risk Contagion between Chinese and Mature Stock Markets: Evidence from a Markov-Switching Mixed-Clayton Copula Model" Entropy 25, no. 4: 619. https://doi.org/10.3390/e25040619