Multi-Party Evolutionary Game Analysis of Accounts Receivable Financing under the Application of Central Bank Digital Currency

Abstract

:1. Introduction

2. Literature Review

2.1. Supply Chain Finance

2.2. Central Bank Digital Currency

2.3. Contribution to the Literature

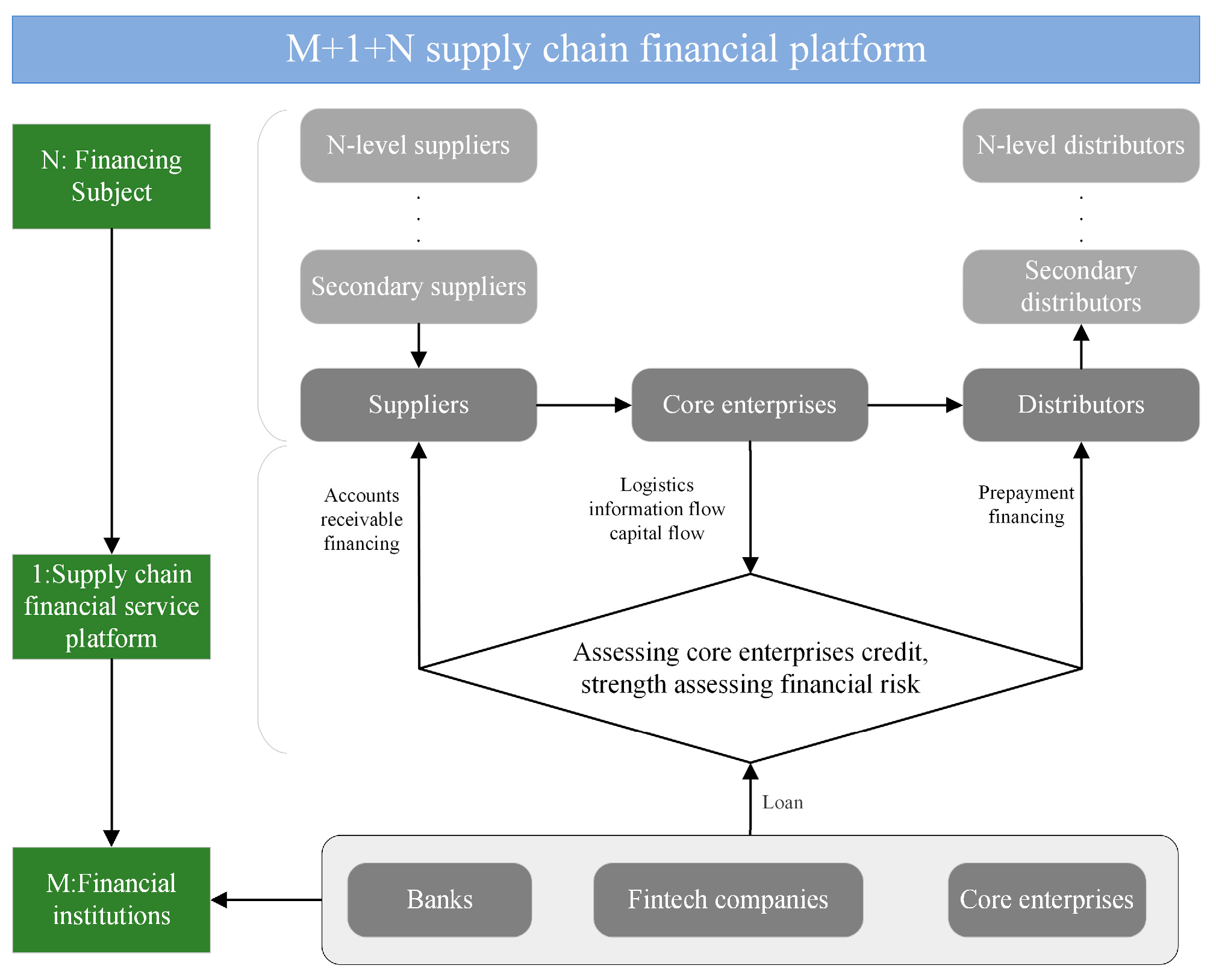

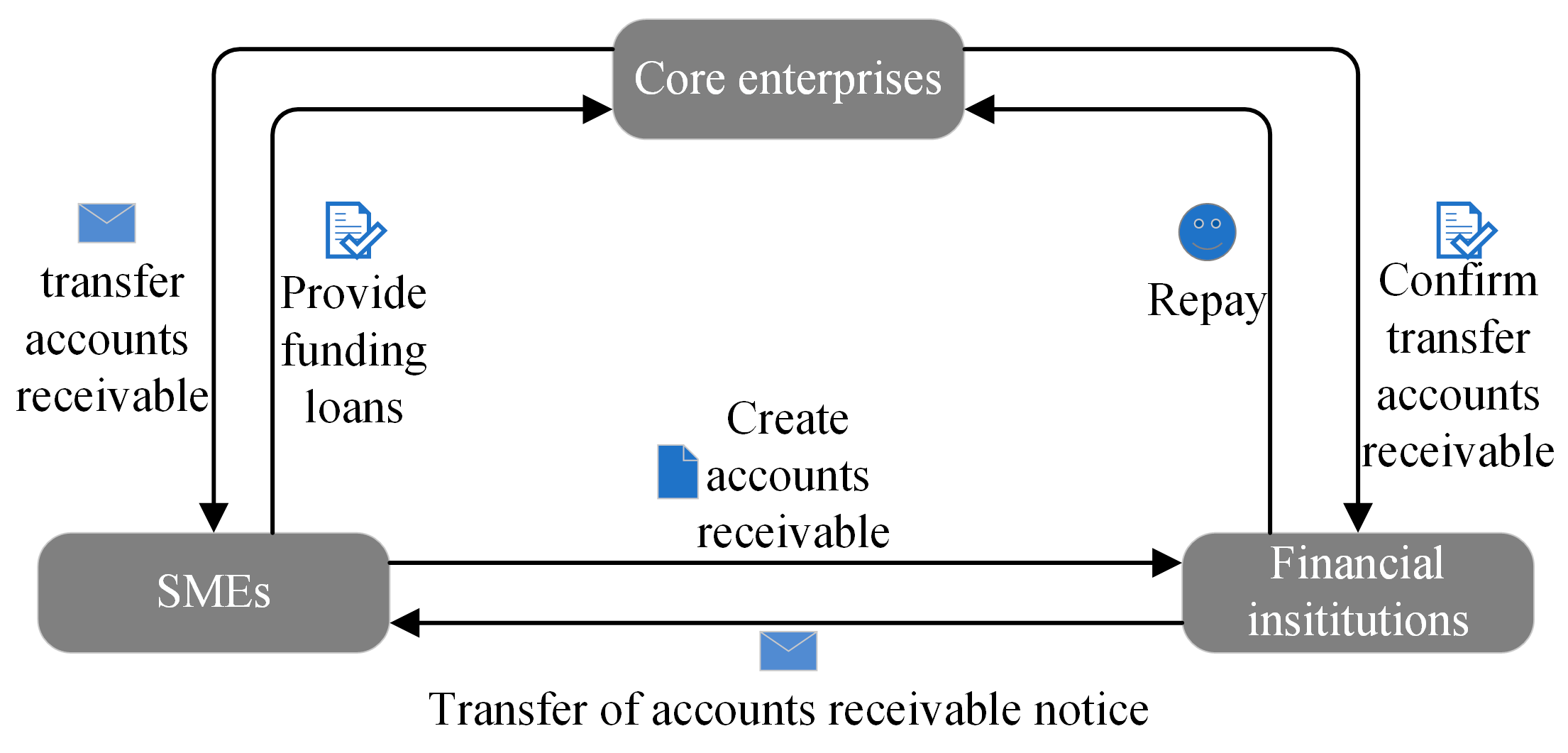

3. Accounts Receivable Financing Issues

3.1. Accounts Receivable Financing

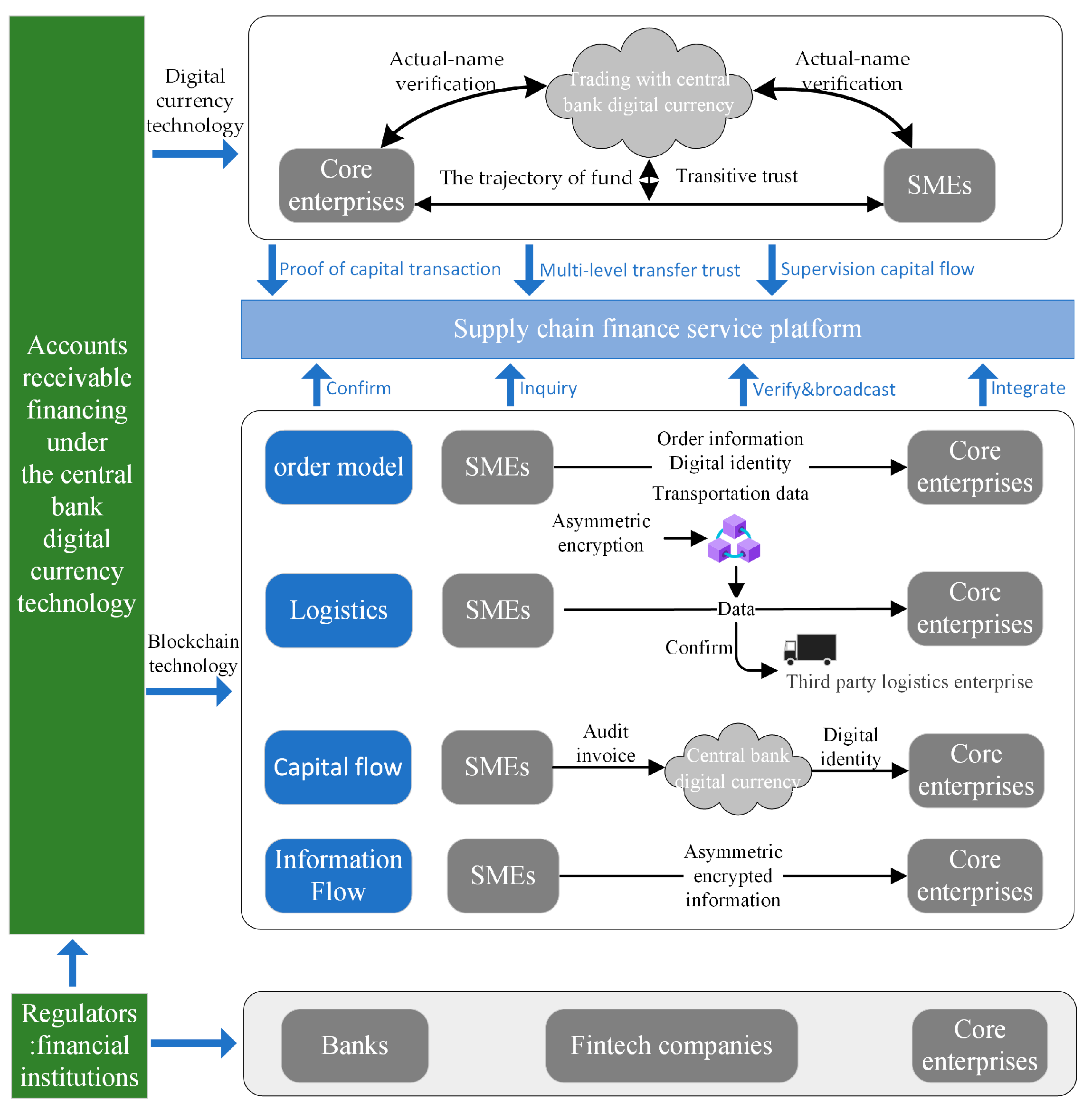

3.2. Accounts Receivable Financing Using Central Bank Digital Currency Technology

3.2.1. Digital Currency Technology

3.2.2. Blockchain Technology

3.2.3. Simplified Accounts Receivable Financing and Comments

- Digital currency technology provides cheaper transaction costs, safer payments, and improved payment efficiency in the accounts receivable financing process. Compared to traditional paper currency, it is enabled to show the flow of loan and record the date, location, and recipient of the loan, making it much easier for financial institutions to comprehend and monitor, whether for forwarding supervision or backward monitoring.

- Blockchain technology is used by the central bank digital currency technology system to reduce credit costs for financial institutions, avoid traditional supply chain finance, and improve the ability to share logistics, information flow, and capital flow in accounts receivable financing among various supply chain financial platform topics. Additionally, built on smart contracts, information invariance, and traceability, it prevents fraudulent collaborative lending and boosts financial security.

- The service platform’s dispersed and trading information of variable quality for accounts receivable financing prevents the development of information barriers. Furthermore, core enterprises’ credit does not transfer well. Central bank digital currency technology enables the multi-level transmission of core enterprise credit through capital circulation, enhances the penetration of core enterprise credit throughout the entire supply chain, and facilitates credit access for SMEs at all levels.

4. Descriptions of the Parameters and Model Presumptions

4.1. Descriptions of the Parameters

4.2. Model Presumptions

4.3. Evolutionary Game Analysis

4.3.1. Financial Institutions and SMEs’ Strategic Stability Analyses

4.3.2. Equilibrium Point Stability Analysis

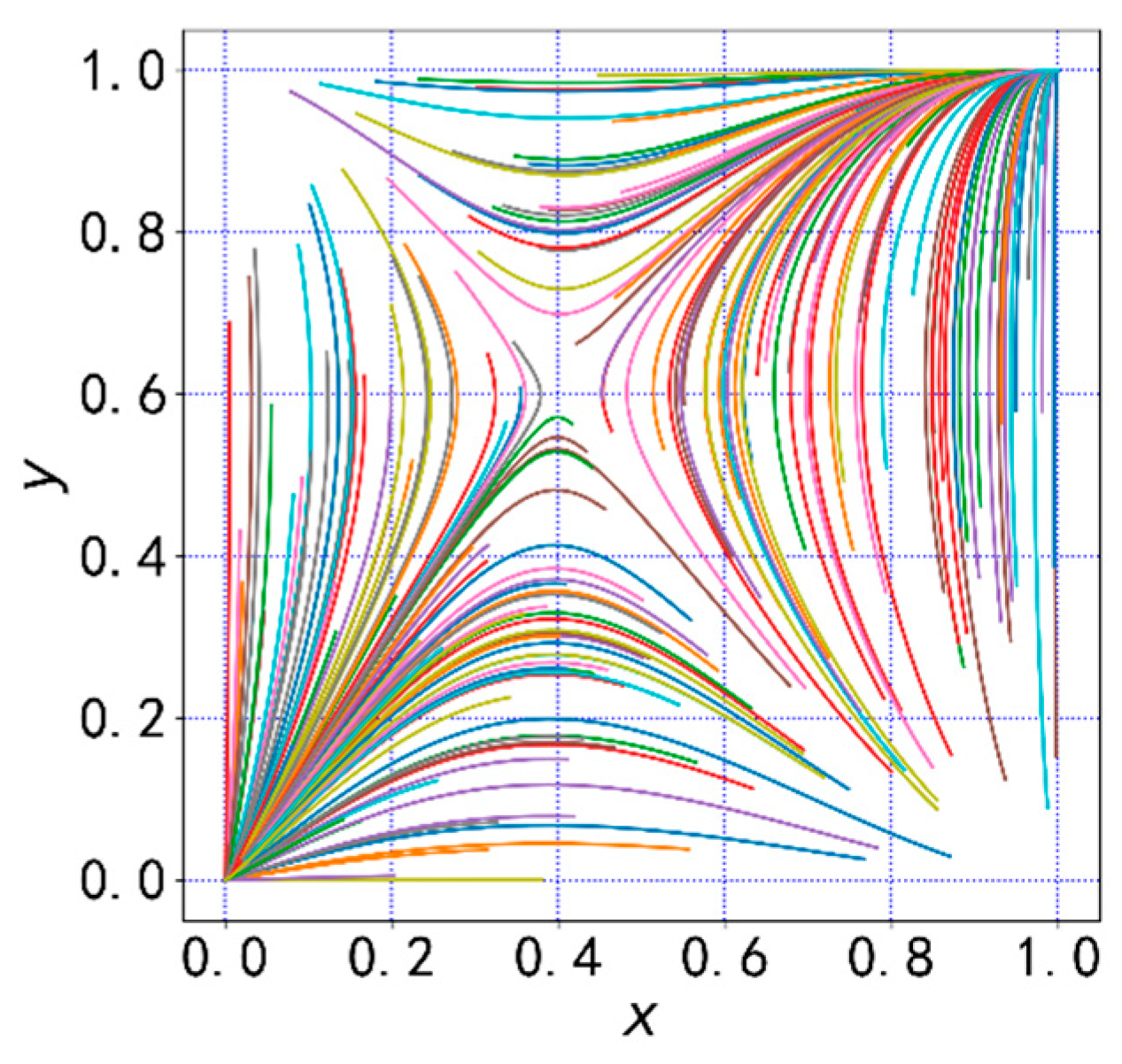

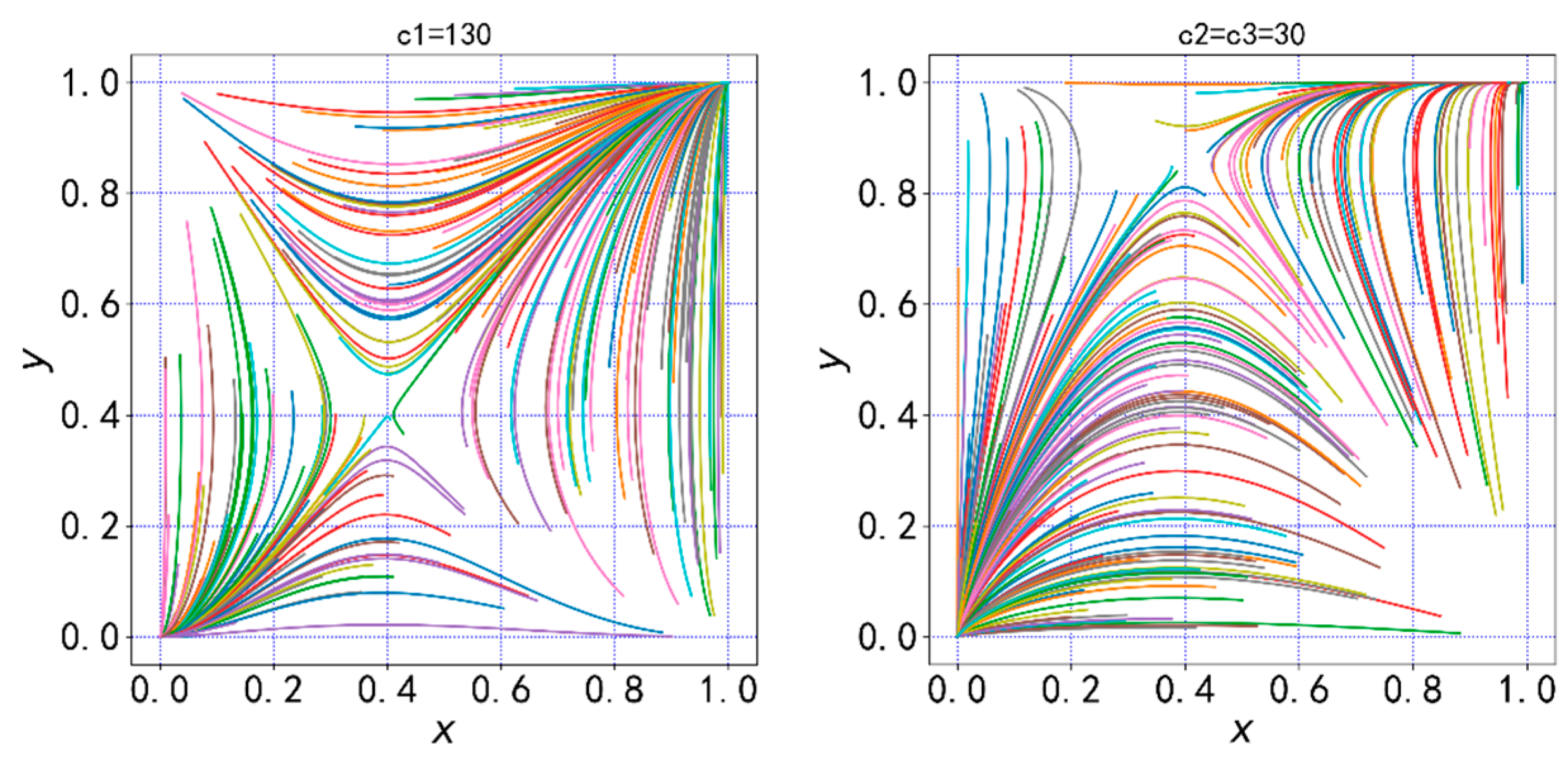

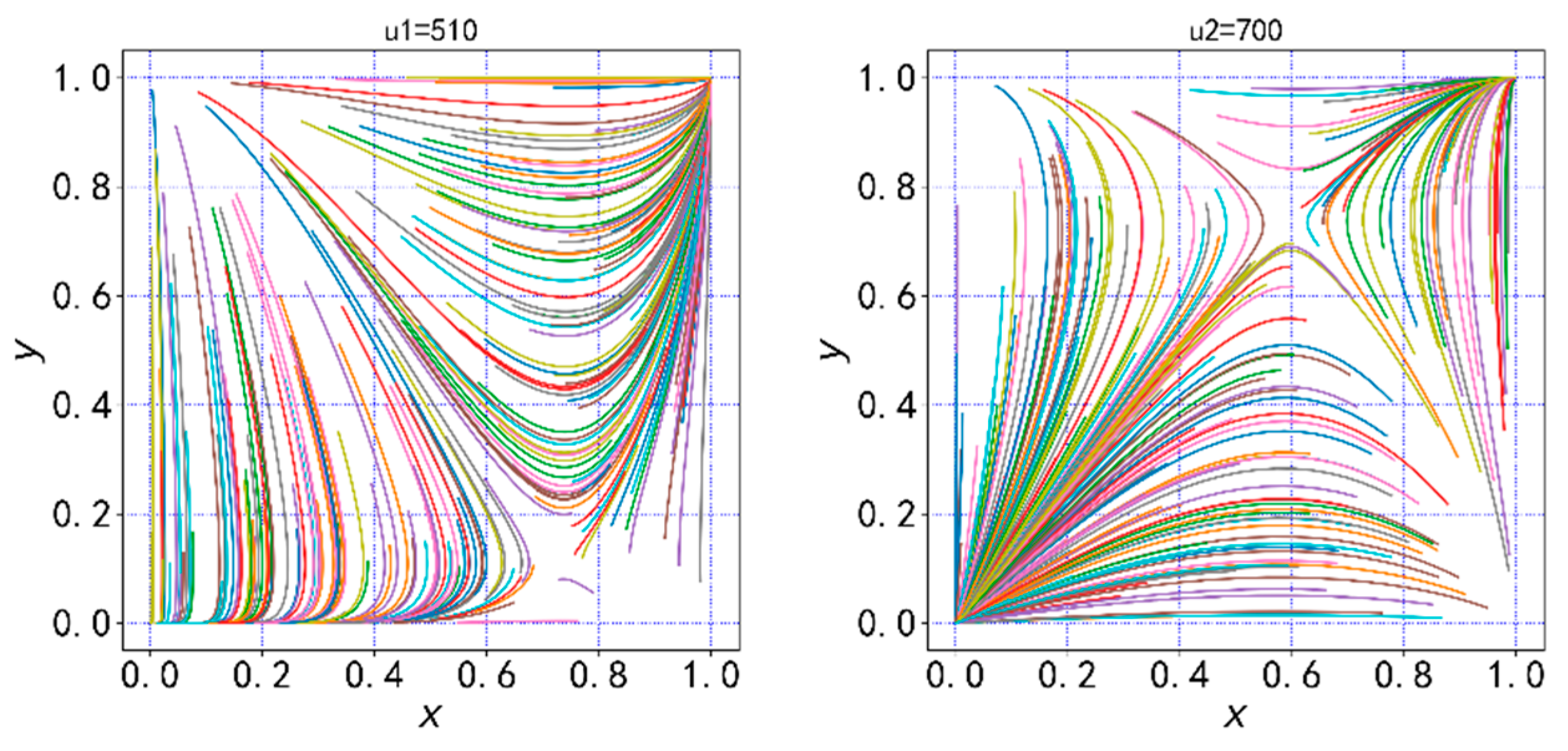

5. Discussion

5.1. Parameters Analysis

5.2. Simulation Analysis

6. Conclusions

- (1)

- Central bank digital currency technology can decrease the costs of credit collection for financial institutions, increase the convenience of financing transactions, and remove credit barriers in the traditional accounts receivable financing process. It can also strengthen the authenticity and sharing of logistics, capital flow, and information flow, promote the transmission of core enterprise credit, and assist SMEs at multiple levels in obtaining a loan.

- (2)

- The costs of supervising capital flow may be seen in central bank digital currency technology costs. Central bank digital currency technology’s high costs are a significant barrier to its adoption and promotion. However, as technology advances and the concept of central bank digital currency is gradually adopted, it will become more mature and less expensive, making it possible for more financial institutions and enterprises to adopt it.

- (3)

- Central bank digital currency technology has a specific technical threshold and necessitates a high level of enterprise digitization, so initial acceptance will typically be limited. As a result, it needs more industry promotion and popularization. In addition, because the supervision of the flow of funds must be safe, it is best to support the enactment of laws to prevent the leakage of information by SMEs.

- (4)

- Financial institutions are crucial in providing incentives for repayment and punishing for non-repayment. In order to protect the interests of financial institutions, they can act as a deterrent to SMEs while guiding them to adhere to contracts and make payments on time. Financial institutions can also entice SMEs to participate by offering incentives that will result in a situation where everyone wins.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Akram, U.; Fülöp, M.T.; Tiron-Tudor, A.; Topor, D.I.; Căpușneanu, S. Impact of Digitalization on Customers’ Well-Being in the Pandemic Period: Challenges and Opportunities for the Retail Industry. Int. J. Environ. Res. Public Health 2021, 18, 7533. [Google Scholar] [CrossRef]

- Gelsomino, L.M.; Mangiaracina, R.; Perego, A.; Tumino, A. Supply Chain Finance: A Literature Review. Int. J. Phys. Distrib. Logist. Manag. 2016, 13. [Google Scholar] [CrossRef]

- Sun, R.; He, D.; Su, H. Evolutionary Game Analysis of Blockchain Technology Preventing Supply Chain Financial Risks. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 2824–2842. [Google Scholar] [CrossRef]

- Liu, Z.; Qian, Q.; Hu, B.; Shang, W.-L.; Li, L.; Zhao, Y.; Zhao, Z.; Han, C. Government Regulation to Promote Coordinated Emission Reduction among Enterprises in the Green Supply Chain Based on Evolutionary Game Analysis. Resour. Conserv. Recycl. 2022, 182, 106290. [Google Scholar] [CrossRef]

- Zhou, J.; Deng, L.; Gibson, P. SMEs’ Changing Perspective on International Trade Credit Risk Management in China: A Cultural Values Evolution Approach. Asia Pac. Bus. Rev. 2022, 28, 333–353. [Google Scholar] [CrossRef]

- Lim, M.K.; Li, Y.; Wang, C.; Tseng, M.-L. A Literature Review of Blockchain Technology Applications in Supply Chains: A Comprehensive Analysis of Themes, Methodologies and Industries. Comput. Ind. Eng. 2021, 154, 107133. [Google Scholar] [CrossRef]

- Li, J.; Maiti, A.; Springer, M.; Gray, T. Blockchain for Supply Chain Quality Management: Challenges and Opportunities in Context of Open Manufacturing and Industrial Internet of Things. Int. J. Comput. Integr. Manuf. 2020, 33, 1321–1355. [Google Scholar] [CrossRef]

- Hirsch, B.; Nitzl, C.; Schoen, M. Interorganizational Trust and Agency Costs in Credit Relationships between Savings Banks and SMEs. J. Bank. Financ. 2018, 97, 37–50. [Google Scholar] [CrossRef]

- Jomthanachai, S.; Wong, W.-P.; Soh, K.-L.; Lim, C.-P. A Global Trade Supply Chain Vulnerability in COVID-19 Pandemic: An Assessment Metric of Risk and Resilience-Based Efficiency of CoDEA Method. Res. Transp. Econ. 2022, 93, 101166. [Google Scholar] [CrossRef]

- Gu, J.; Xia, X.; He, Y.; Xu, Z. An Approach to Evaluating the Spontaneous and Contagious Credit Risk for Supply Chain Enterprises Based on Fuzzy Preference Relations. Comput. Ind. Eng. 2017, 106, 361–372. [Google Scholar] [CrossRef]

- Zhou, Z.; Liu, Y.; Yu, H.; Chen, Q. Logistics Supply Chain Information Collaboration Based on FPGA and Internet of Things System. Microprocess. Microsyst. 2021, 80, 103589. [Google Scholar] [CrossRef]

- Zhang, W.; Yan, S.; Li, J.; Tian, X.; Yoshida, T. Credit Risk Prediction of SMEs in Supply Chain Finance by Fusing Demographic and Behavioral Data. Transp. Res. Part E Logist. Transp. Rev. 2022, 158, 102611. [Google Scholar] [CrossRef]

- Construction of the Credit Risk Indicator Evaluation System of Small and Medium-Sized Enterprises under Supply Chain Finance. Available online: http://journal26.magtechjournal.com/Jwk3_kygl/EN/Y2020/V41/I4/209 (accessed on 14 July 2022).

- Zhang, H.; Shi, Y.; Yang, X.; Zhou, R. A Firefly Algorithm Modified Support Vector Machine for the Credit Risk Assessment of Supply Chain Finance. Res. Int. Bus. Financ. 2021, 58, 101482. [Google Scholar] [CrossRef]

- Ozili, P.K. Central Bank Digital Currency Research around the World: A Review of Literature. J. Money Laund. Control, 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Central Bank Digital Currencies: Motives, Economic Implications, and the Research Frontier | Annual Review of Economics. Available online: https://www.annualreviews.org/doi/full/10.1146/annurev-economics-051420-020324 (accessed on 20 December 2022).

- Esposito, C.; Ficco, M.; Gupta, B.B. Blockchain-Based Authentication and Authorization for Smart City Applications. Inf. Process. Manag. 2021, 58, 102468. [Google Scholar] [CrossRef]

- Danezis, G.; Meiklejohn, S. Centrally Banked Cryptocurrencies. arXiv 2015, arXiv:1505.06895. [Google Scholar]

- Project Ubin: Central Bank Digital Money Using Distributed Ledger Technology. Available online: https://www.mas.gov.sg/schemes-and-initiatives/Project-Ubin (accessed on 20 December 2022).

- Peters, M.A.; Green, B.; Yang, H. (Melissa) Cryptocurrencies, China’s Sovereign Digital Currency (DCEP) and the US Dollar System. Educ. Philos. Theory 2022, 54, 1713–1719. [Google Scholar] [CrossRef]

- Sinelnikova-Muryleva, E. Central Banks Retail Digital Currencies: Risks and Prospects of Emission. Monit. Russ. Econ. Outlook. Trends Chall. Socio-Econ. Development. Mosc. 2020, 13, 7–11. [Google Scholar]

- Fegatelli, P. A Central Bank Digital Currency in a Heterogeneous Monetary Union: Managing the Effects on the Bank Lending Channel. J. Macroecon. 2022, 71, 103392. [Google Scholar] [CrossRef]

- Chang, S.E.; Chen, Y.-C.; Lu, M.-F. Supply Chain Re-Engineering Using Blockchain Technology: A Case of Smart Contract Based Tracking Process. Technol. Forecast. Soc. Change 2019, 144, 1–11. [Google Scholar] [CrossRef]

- Guo, L.; Chen, J.; Li, S.; Li, Y.; Lu, J. A Blockchain and IoT Based Lightweight Framework for Enabling Information Transparency in Supply Chain Finance. Digit. Commun. Netw. 2022, 8, 576–587. [Google Scholar] [CrossRef]

- Saberi, S.; Kouhizadeh, M.; Sarkis, J.; Shen, L. Blockchain Technology and Its Relationships to Sustainable Supply Chain Management. Int. J. Prod. Res. 2019, 57, 2117–2135. [Google Scholar] [CrossRef] [Green Version]

- Jiang, R.; Kang, Y.; Liu, Y.; Liang, Z.; Duan, Y.; Sun, Y.; Liu, J. A Trust Transitivity Model of Small and Medium-Sized Manufacturing Enterprises under Blockchain-Based Supply Chain Finance. Int. J. Prod. Econ. 2022, 247, 108469. [Google Scholar] [CrossRef]

- Chen, S.; Du, J.; He, W.; Siponen, M. Supply Chain Finance Platform Evaluation Based on Acceptability Analysis. Int. J. Prod. Econ. 2022, 243, 108350. [Google Scholar] [CrossRef]

- Du, M.; Chen, Q.; Xiao, J.; Yang, H.; Ma, X. Supply Chain Finance Innovation Using Blockchain. IEEE Trans. Eng. Manag. 2020, 67, 1045–1058. [Google Scholar] [CrossRef]

- Huijun, H.; Jing, Z. Recourse Accounts Receivable Factoring Financing Ratio Research Based on Multinational Supply Chain. In Proceedings of the 2016 13th International Conference on Service Systems and Service Management (ICSSSM), Kunming, China, 24–26 June 2016; pp. 1–4. [Google Scholar]

- Yao, Q. A Systematic Framework to Understand Central Bank Digital Currency. Sci. China Inf. Sci. 2018, 61, 033101. [Google Scholar] [CrossRef] [Green Version]

- Stiglitz, J.E. Macro-Economic Management in an Electronic Credit/Financial System. Natl. Bur. Econ. Res. 2017. [Google Scholar] [CrossRef]

- Fülöp, M.T.; Topor, D.I.; Ionescu, C.A.; Căpușneanu, S.; Breaz, T.O.; Stanescu, S.G. Fintech Accounting and Industry 4.0: Future-Proofing or Threats to the Accounting Profession? J. Bus. Econ. Manag. 2022, 23, 997–1015. [Google Scholar] [CrossRef]

- Allen, F.; Gu, X.; Jagtiani, J. Fintech, Cryptocurrencies, and CBDC: Financial Structural Transformation in China. J. Int. Money Financ. 2022, 124, 102625. [Google Scholar] [CrossRef]

- Zhao, Z.; Chen, D.; Wang, L.; Han, C. Credit Risk Diffusion in Supply Chain Finance: A Complex Networks Perspective. Sustainability 2018, 10, 4608. [Google Scholar] [CrossRef] [Green Version]

- Han, K.-M.; Park, S.W.; Lee, S. Anti-Fraud in International Supply Chain Finance: Focusing on Moneual Case. J. Korea Trade 2020, 24, 59–81. [Google Scholar] [CrossRef]

- Zou, W.; Lo, D.; Kochhar, P.S.; Le, X.-B.D.; Xia, X.; Feng, Y.; Chen, Z.; Xu, B. Smart Contract Development: Challenges and Opportunities. IEEE Trans. Softw. Eng. 2021, 47, 2084–2106. [Google Scholar] [CrossRef]

- Zhang, B.; Ye, Y.; Yue, X. Evolutionary Strategies of Supply Chain Finance From the Perspective of a Return Policy. IEEE Access 2019, 7, 110761–110769. [Google Scholar] [CrossRef]

- Cheng, Y.; Wu, D.D.; Olson, D.L.; Dolgui, A. Financing the Newsvendor with Preferential Credit: Bank vs. Manufacturer. Int. J. Prod. Res. 2021, 59, 4228–4247. [Google Scholar] [CrossRef]

- Figorilli, S.; Antonucci, F.; Costa, C.; Pallottino, F.; Raso, L.; Castiglione, M.; Pinci, E.; Del Vecchio, D.; Colle, G.; Proto, A.R.; et al. A Blockchain Implementation Prototype for the Electronic Open Source Traceability of Wood along the Whole Supply Chain. Sensors 2018, 18, 3133. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameters | Meaning of Parameters |

|---|---|

| Probabilities of financial institutions using or not using central bank digital currency technology | |

| Probabilities of SMEs repayment or non-repayment | |

| Loans provided to SMEs | |

| Accounts receivable loan interest rates | |

| Financial institutions investment rates | |

| Receivables income for SMEs | |

| Financial institutions’ credit costs | |

| Technology costs for central bank digital currency technology | |

| Costs for supervision capital flow | |

| SMEs share the expenses of loan fraud and counterfeiting. | |

| SMEs illegally acquired loans and exploited them to generate investment revenue. | |

| SMEs production costs | |

| Joint fraudulent loan allocation rate to SMEs | |

| Credit block incentives | |

| Financial institutions benefit from trust. | |

| Non-payment penalty for SMEs that use central bank digital currency technology | |

| Non-payment penalty for SMEs that no-use central bank digital currency technology |

| SMEs | |||

|---|---|---|---|

| Repay | Non-Repay | ||

| Financial institutions | use | ||

| not use | |||

| (0,0) | (0,1) | (1,0) | (1,1) | |||

|---|---|---|---|---|---|---|

| Condition1 | deJ | − | − | − | − | / |

| trJ | − | Unknown | + | Unknown | 0 | |

| Evolutionary Results | × | × | × | × | × | |

| Condition2 | deJ | + | + | + | + | / |

| trJ | − | + | Unknown | − | 0 | |

| Evolutionary Results | ESS | × | × | ESS | × | |

| Condition3 | deJ | + | − | + | + | / |

| trJ | + | − | Unknown | + | 0 | |

| Evolutionary Results | × | × | × | × | × | |

| Condition4 | deJ | − | − | − | − | / |

| trJ | + | Unknown | − | Unknown | 0 | |

| Evolutionary Results | × | × | × | × | × |

| Parameters | Partial Derivatives’ Positivity and Negativity | |

|---|---|---|

| + | positive | |

| − | negative | |

| − | negative | |

| + | positive | |

| + | positive | |

| + | positive | |

| − | negative |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Q.; Yang, D.; Qin, J. Multi-Party Evolutionary Game Analysis of Accounts Receivable Financing under the Application of Central Bank Digital Currency. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 394-415. https://doi.org/10.3390/jtaer18010021

Zhang Q, Yang D, Qin J. Multi-Party Evolutionary Game Analysis of Accounts Receivable Financing under the Application of Central Bank Digital Currency. Journal of Theoretical and Applied Electronic Commerce Research. 2023; 18(1):394-415. https://doi.org/10.3390/jtaer18010021

Chicago/Turabian StyleZhang, Qinglei, Dihong Yang, and Jiyun Qin. 2023. "Multi-Party Evolutionary Game Analysis of Accounts Receivable Financing under the Application of Central Bank Digital Currency" Journal of Theoretical and Applied Electronic Commerce Research 18, no. 1: 394-415. https://doi.org/10.3390/jtaer18010021